Managerial Accounting Report: Standard Costing in Business

VerifiedAdded on 2023/06/07

|17

|3739

|352

Report

AI Summary

This managerial accounting report delves into the concept of standard costing, a crucial technique for cost control and performance evaluation within organizations. The report begins with an executive summary and introduction, followed by an explanation of standard costing, detailing its purpose and application. It then analyzes two journal articles, one focusing on the impact of standard costing on the profitability of MTN Nigeria and the other examining its implications in a manufacturing context. The report explores the similarities and differences between the findings of these studies, highlighting advantages and disadvantages of standard costing, and providing specific outcomes useful for management accountants in Australian organizations. It emphasizes improved cost control, managerial planning, inventory measurement, and potential cost reductions. The report concludes by summarizing the key takeaways and providing references to the sources used.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The present report has concentrated on the usage of standard costing system concerning the

overall business affiliations. It has been surveyed that standard costing considers the fixation

of pre-chosen assessments of cost for outfitting a start to differentiate and the genuine costs.

Likewise, standard costing system is used as the benchmark where the genuine costs are

showed up distinctively in connection to the standard costs. This construes the structure

starting at now sets the volume to be made and the surveyed development levels, which

would then be differentiated and the genuine execution. The endorsement is made by picking

two journal articles, which reveal that standard costing has a vital activity in raising the

advantage level of an affiliation, at whatever point realized reasonably.

Executive Summary:

The present report has concentrated on the usage of standard costing system concerning the

overall business affiliations. It has been surveyed that standard costing considers the fixation

of pre-chosen assessments of cost for outfitting a start to differentiate and the genuine costs.

Likewise, standard costing system is used as the benchmark where the genuine costs are

showed up distinctively in connection to the standard costs. This construes the structure

starting at now sets the volume to be made and the surveyed development levels, which

would then be differentiated and the genuine execution. The endorsement is made by picking

two journal articles, which reveal that standard costing has a vital activity in raising the

advantage level of an affiliation, at whatever point realized reasonably.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

An Explanation of Standard Costing:........................................................................................3

An explanation of the purpose of two studies and the research question set out to explore

about standard costing:...............................................................................................................5

A discussion about similarities and differences in the findings of two studies:........................8

Description of standard costing system:.............................................................................8

Advantages And Disadvantages:.........................................................................................8

The comparative disadvantages that could be recognized from both the exploration

papers comprise of the accompanying:..............................................................................9

Four specific outcomes of the research findings of two studies useful for the management

accountants in Australian organizations:.................................................................................11

Improved cost control:.......................................................................................................11

Managerial planning and decision making:.....................................................................11

Reasonable inventory measurement.................................................................................12

Possible minimisations in cost of production:..................................................................12

Conclusion:..............................................................................................................................13

Reference..................................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................3

An Explanation of Standard Costing:........................................................................................3

An explanation of the purpose of two studies and the research question set out to explore

about standard costing:...............................................................................................................5

A discussion about similarities and differences in the findings of two studies:........................8

Description of standard costing system:.............................................................................8

Advantages And Disadvantages:.........................................................................................8

The comparative disadvantages that could be recognized from both the exploration

papers comprise of the accompanying:..............................................................................9

Four specific outcomes of the research findings of two studies useful for the management

accountants in Australian organizations:.................................................................................11

Improved cost control:.......................................................................................................11

Managerial planning and decision making:.....................................................................11

Reasonable inventory measurement.................................................................................12

Possible minimisations in cost of production:..................................................................12

Conclusion:..............................................................................................................................13

Reference..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

Managerial accounting is the technique for recognizing, checking, evaluating,

translating and passing on information to the business directors for meeting the goals of the

organisation. In this way several viewpoints like activity-based costing, planning and

standard costing, out of which standard costing has been chosen for fulfilling the purpose

behind the report. The initial part would give a short survey of the standard costing

concerning the business affiliations (Langfield-Smith et al. 2017). The second part would be

established on two research articles ontandard costing and the inspiration driving these two

articles would be explored regarding standard costing. Finally, the report would find out the

effects and outcome of these two articles that will prove to be advantageous for management

accountants.

An Explanation of Standard Costing:

The standard costing is a system that utilises standards for expenses and wages for the

purpose of controlling with the assistance of different analytical process. To be more precise

standard costing helps in choosing the proportion of expense to be caused under particular

working conditions. Standard expense could be portrayed as an arrangement to determine the

expense for units. This approach is recognized all around as a reasonable instrument in

association with cost control in mechanical sections (Posteucă et al. 2018). Notwithstanding

the way that standard expenses and planned expenses are used a portion of the time on the

other hand, planned expenses construe the general arranged expenses for various things.

Therefore, the standard costing system gives a basis of budgetary control stock valuation,

work in progress and setting a selling value

Introduction:

Managerial accounting is the technique for recognizing, checking, evaluating,

translating and passing on information to the business directors for meeting the goals of the

organisation. In this way several viewpoints like activity-based costing, planning and

standard costing, out of which standard costing has been chosen for fulfilling the purpose

behind the report. The initial part would give a short survey of the standard costing

concerning the business affiliations (Langfield-Smith et al. 2017). The second part would be

established on two research articles ontandard costing and the inspiration driving these two

articles would be explored regarding standard costing. Finally, the report would find out the

effects and outcome of these two articles that will prove to be advantageous for management

accountants.

An Explanation of Standard Costing:

The standard costing is a system that utilises standards for expenses and wages for the

purpose of controlling with the assistance of different analytical process. To be more precise

standard costing helps in choosing the proportion of expense to be caused under particular

working conditions. Standard expense could be portrayed as an arrangement to determine the

expense for units. This approach is recognized all around as a reasonable instrument in

association with cost control in mechanical sections (Posteucă et al. 2018). Notwithstanding

the way that standard expenses and planned expenses are used a portion of the time on the

other hand, planned expenses construe the general arranged expenses for various things.

Therefore, the standard costing system gives a basis of budgetary control stock valuation,

work in progress and setting a selling value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

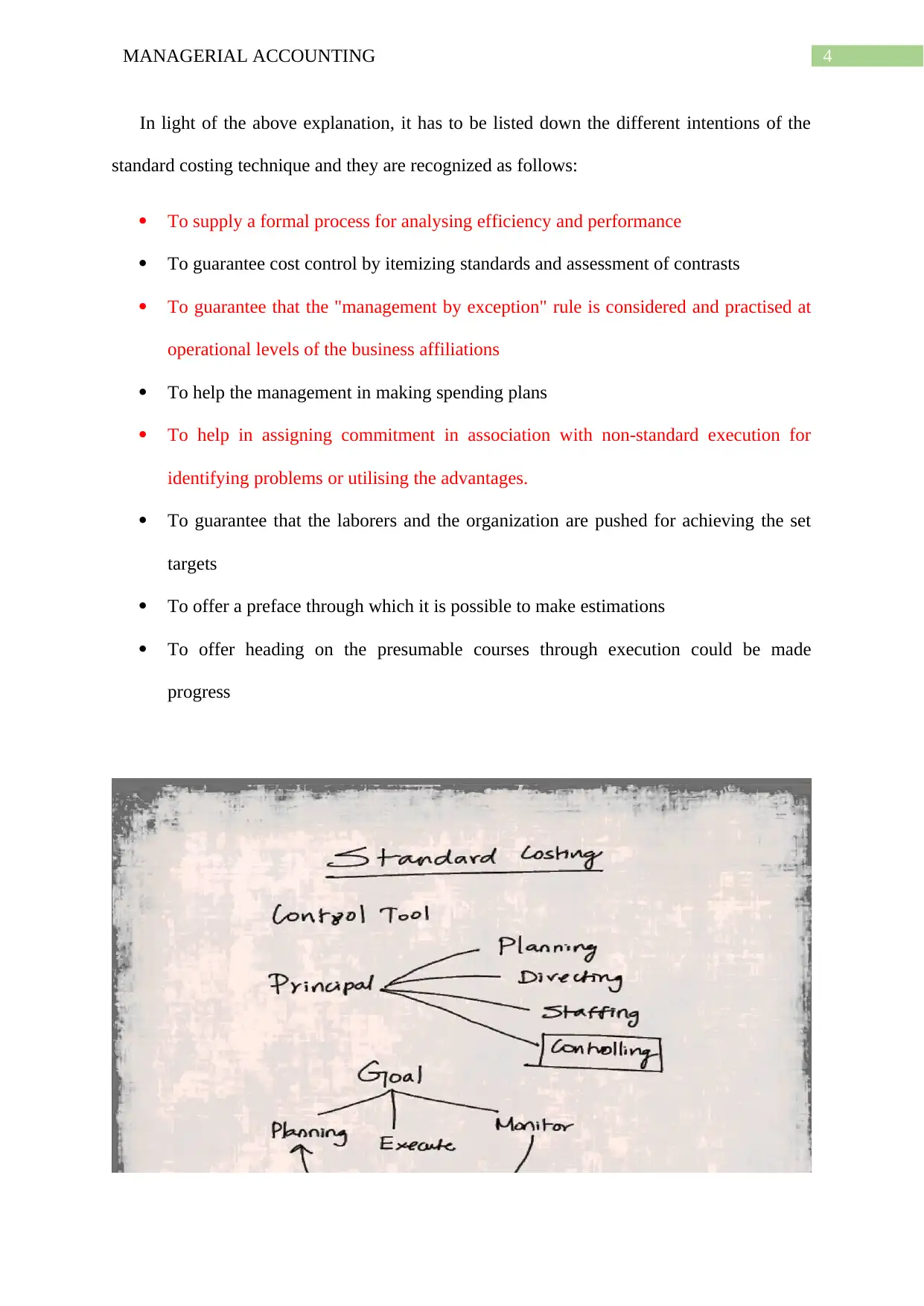

In light of the above explanation, it has to be listed down the different intentions of the

standard costing technique and they are recognized as follows:

To supply a formal process for analysing efficiency and performance

To guarantee cost control by itemizing standards and assessment of contrasts

To guarantee that the "management by exception" rule is considered and practised at

operational levels of the business affiliations

To help the management in making spending plans

To help in assigning commitment in association with non-standard execution for

identifying problems or utilising the advantages.

To guarantee that the laborers and the organization are pushed for achieving the set

targets

To offer a preface through which it is possible to make estimations

To offer heading on the presumable courses through execution could be made

progress

In light of the above explanation, it has to be listed down the different intentions of the

standard costing technique and they are recognized as follows:

To supply a formal process for analysing efficiency and performance

To guarantee cost control by itemizing standards and assessment of contrasts

To guarantee that the "management by exception" rule is considered and practised at

operational levels of the business affiliations

To help the management in making spending plans

To help in assigning commitment in association with non-standard execution for

identifying problems or utilising the advantages.

To guarantee that the laborers and the organization are pushed for achieving the set

targets

To offer a preface through which it is possible to make estimations

To offer heading on the presumable courses through execution could be made

progress

5MANAGERIAL ACCOUNTING

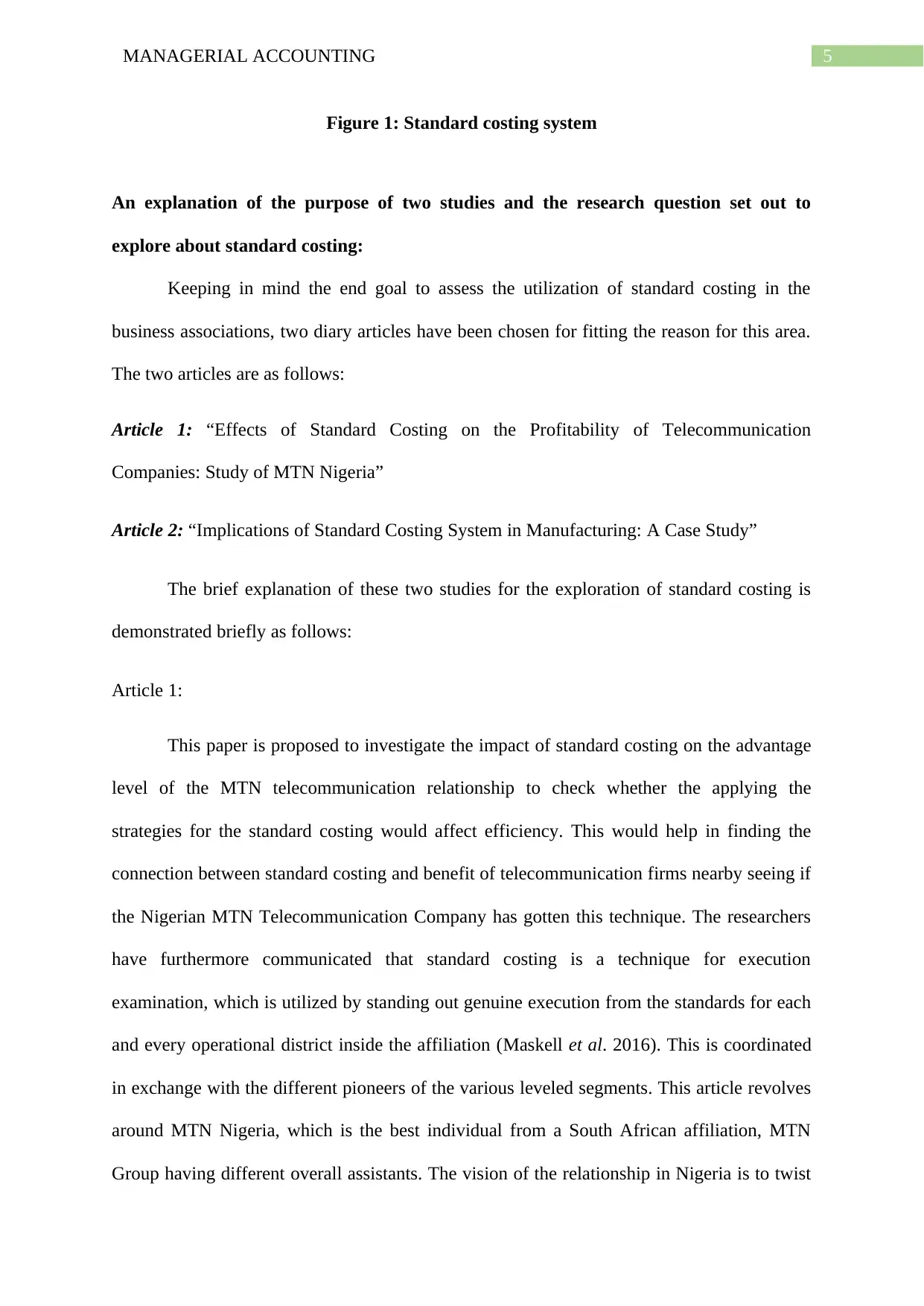

Figure 1: Standard costing system

An explanation of the purpose of two studies and the research question set out to

explore about standard costing:

Keeping in mind the end goal to assess the utilization of standard costing in the

business associations, two diary articles have been chosen for fitting the reason for this area.

The two articles are as follows:

Article 1: “Effects of Standard Costing on the Profitability of Telecommunication

Companies: Study of MTN Nigeria”

Article 2: “Implications of Standard Costing System in Manufacturing: A Case Study”

The brief explanation of these two studies for the exploration of standard costing is

demonstrated briefly as follows:

Article 1:

This paper is proposed to investigate the impact of standard costing on the advantage

level of the MTN telecommunication relationship to check whether the applying the

strategies for the standard costing would affect efficiency. This would help in finding the

connection between standard costing and benefit of telecommunication firms nearby seeing if

the Nigerian MTN Telecommunication Company has gotten this technique. The researchers

have furthermore communicated that standard costing is a technique for execution

examination, which is utilized by standing out genuine execution from the standards for each

and every operational district inside the affiliation (Maskell et al. 2016). This is coordinated

in exchange with the different pioneers of the various leveled segments. This article revolves

around MTN Nigeria, which is the best individual from a South African affiliation, MTN

Group having different overall assistants. The vision of the relationship in Nigeria is to twist

Figure 1: Standard costing system

An explanation of the purpose of two studies and the research question set out to

explore about standard costing:

Keeping in mind the end goal to assess the utilization of standard costing in the

business associations, two diary articles have been chosen for fitting the reason for this area.

The two articles are as follows:

Article 1: “Effects of Standard Costing on the Profitability of Telecommunication

Companies: Study of MTN Nigeria”

Article 2: “Implications of Standard Costing System in Manufacturing: A Case Study”

The brief explanation of these two studies for the exploration of standard costing is

demonstrated briefly as follows:

Article 1:

This paper is proposed to investigate the impact of standard costing on the advantage

level of the MTN telecommunication relationship to check whether the applying the

strategies for the standard costing would affect efficiency. This would help in finding the

connection between standard costing and benefit of telecommunication firms nearby seeing if

the Nigerian MTN Telecommunication Company has gotten this technique. The researchers

have furthermore communicated that standard costing is a technique for execution

examination, which is utilized by standing out genuine execution from the standards for each

and every operational district inside the affiliation (Maskell et al. 2016). This is coordinated

in exchange with the different pioneers of the various leveled segments. This article revolves

around MTN Nigeria, which is the best individual from a South African affiliation, MTN

Group having different overall assistants. The vision of the relationship in Nigeria is to twist

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

up the fundamental master center in telecommunication division and its vision is to pass on

the best framework quality, customer regard and organization. It has been perceived that

advantage is fundamental to guarantee the achievement of any business affiliation and the

telecommunication business is one of the snappiest creating portions on the planet.

It is important for the affiliations working in the telecommunication division to place assets

into structure, apparatus, programming and collaborations for giving quality organizations to

the customers in order to guarantee such improvement plan,. The purchaser quality, rising

mechanical advancement and globalization has left these relationship with a bundle of

alternatives than to make interests in the above explained things (Eldenburg et al. 2016).

Along these lines, the administrators working in these affiliations are confronted with issues

concerning cost minimisation so the general salaries and advantages could be expanded. A

part of the basic issues considers acquisition of the best in class item adapt like raising

exchanging of advantages, wandering, transmission and others, center around programs

yielding more imperative salaries like promoting organizations, advancements, considering

creative arrangements, commitment organization and cost decreasing procedure.

By thinking about, the telecommunications region of Nigeria, the paper is relied upon to

find the courses through which these issues are directed and the manner in which advantage

level is affected by the equality of the levels of different sorts of advantages and liabilities. In

like manner, the examination went for finding the examples in advantage in the part over the

customers for lighting up essential administration by approach makers and theorists

(Fullerton et al. 2014). In light of such assessment, the accompanying examination questions

have been set out for investigating the theme:

up the fundamental master center in telecommunication division and its vision is to pass on

the best framework quality, customer regard and organization. It has been perceived that

advantage is fundamental to guarantee the achievement of any business affiliation and the

telecommunication business is one of the snappiest creating portions on the planet.

It is important for the affiliations working in the telecommunication division to place assets

into structure, apparatus, programming and collaborations for giving quality organizations to

the customers in order to guarantee such improvement plan,. The purchaser quality, rising

mechanical advancement and globalization has left these relationship with a bundle of

alternatives than to make interests in the above explained things (Eldenburg et al. 2016).

Along these lines, the administrators working in these affiliations are confronted with issues

concerning cost minimisation so the general salaries and advantages could be expanded. A

part of the basic issues considers acquisition of the best in class item adapt like raising

exchanging of advantages, wandering, transmission and others, center around programs

yielding more imperative salaries like promoting organizations, advancements, considering

creative arrangements, commitment organization and cost decreasing procedure.

By thinking about, the telecommunications region of Nigeria, the paper is relied upon to

find the courses through which these issues are directed and the manner in which advantage

level is affected by the equality of the levels of different sorts of advantages and liabilities. In

like manner, the examination went for finding the examples in advantage in the part over the

customers for lighting up essential administration by approach makers and theorists

(Fullerton et al. 2014). In light of such assessment, the accompanying examination questions

have been set out for investigating the theme:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

What are the present patterns in profitability in the Nigerian telecommunication

industry?

What is the impact of standard costing of standard costing on the profitability of MTN

Nigeria?

What are the conceivable courses through which the profitability pattern of the

organization could be enhanced?

Article 2:

This article is revolved around discussing the consequences of standard costing

structure in light of a relevant examples. The study of those examples is incorporated with

watching out for a particular circumstance. As demonstrated by the study, there has been

basic decline in income from sale of ASL between first March 2014 and 28th February 2015

due to the failure of standard costing system in keeping an eye on the business needs, as

communicated by the Operations Manager of the affiliation. Notwithstanding the way that the

structure assisted with saving the expense of production process, it has been a dissatisfied

change and likewise solving the issues of the individual customers (Armitage et al. 2016). In

this manner, it has suffered loss in revenue for ASL. With a particular ultimate objective to

address the point of view of the administrator, the Chief Financial Officer (CFO) of the

affiliation has requested to give an essential examination from the drawbacks and advantages

of the standard costing system. Along these lines, with a particular ultimate objective to give

the feedback to the CFO, a low down depiction of the standard costing structure has been

fused into this article.

According to the professional, the standard costs for staffs, materials and distinctive

expenses are planned depending upon organization appraisals of costs, work use and

materials close by planned produced volume and overhead costs. Finally, fitting

What are the present patterns in profitability in the Nigerian telecommunication

industry?

What is the impact of standard costing of standard costing on the profitability of MTN

Nigeria?

What are the conceivable courses through which the profitability pattern of the

organization could be enhanced?

Article 2:

This article is revolved around discussing the consequences of standard costing

structure in light of a relevant examples. The study of those examples is incorporated with

watching out for a particular circumstance. As demonstrated by the study, there has been

basic decline in income from sale of ASL between first March 2014 and 28th February 2015

due to the failure of standard costing system in keeping an eye on the business needs, as

communicated by the Operations Manager of the affiliation. Notwithstanding the way that the

structure assisted with saving the expense of production process, it has been a dissatisfied

change and likewise solving the issues of the individual customers (Armitage et al. 2016). In

this manner, it has suffered loss in revenue for ASL. With a particular ultimate objective to

address the point of view of the administrator, the Chief Financial Officer (CFO) of the

affiliation has requested to give an essential examination from the drawbacks and advantages

of the standard costing system. Along these lines, with a particular ultimate objective to give

the feedback to the CFO, a low down depiction of the standard costing structure has been

fused into this article.

According to the professional, the standard costs for staffs, materials and distinctive

expenses are planned depending upon organization appraisals of costs, work use and

materials close by planned produced volume and overhead costs. Finally, fitting

8MANAGERIAL ACCOUNTING

recommendations have been given so the perceived issues could be settled in ASL by

recalling the problems raised by the Operations Manager of the affiliation (Szychta and

Dobroszek 2016). In view of the above assessment, the accompanying exploration questions

have been produced for this paper:

Does standard costing framework neglect to deliver giving administrations to singular

client demand?

Does the act of standard costing framework result in loss of offers income for ASL?

What are the benefits and disadvantages related with the standard costing framework?

What are the conceivable proposals for expanding the business income of ASL?

A discussion about similarities and differences in the findings of two studies:

There are certain similarities that has been observed in the findings of two studies and they

are as follows:

Description of standard costing system:

In both the articles, a thorough description of the standard costing structure has been given.

The experts of both the articles have communicated that the distinctions gotten by using the

standard costing system could be overviewed execution appraisal, explanations behind cost

control and assessing. In this one of a kind circumstance, it ought to be said that standard

costing covers an immense bit of the methods of managerial accounting that mull over

obligation accounting declaration and additionally planning system (Parker and Fleischman

2017).

Advantages And Disadvantages:

In both the articles, the researchers have given a sensible portrayal of the great

circumstances and basic in standard costing structure. A bit of the typical advantages said in

both the articles join the accompanying:

recommendations have been given so the perceived issues could be settled in ASL by

recalling the problems raised by the Operations Manager of the affiliation (Szychta and

Dobroszek 2016). In view of the above assessment, the accompanying exploration questions

have been produced for this paper:

Does standard costing framework neglect to deliver giving administrations to singular

client demand?

Does the act of standard costing framework result in loss of offers income for ASL?

What are the benefits and disadvantages related with the standard costing framework?

What are the conceivable proposals for expanding the business income of ASL?

A discussion about similarities and differences in the findings of two studies:

There are certain similarities that has been observed in the findings of two studies and they

are as follows:

Description of standard costing system:

In both the articles, a thorough description of the standard costing structure has been given.

The experts of both the articles have communicated that the distinctions gotten by using the

standard costing system could be overviewed execution appraisal, explanations behind cost

control and assessing. In this one of a kind circumstance, it ought to be said that standard

costing covers an immense bit of the methods of managerial accounting that mull over

obligation accounting declaration and additionally planning system (Parker and Fleischman

2017).

Advantages And Disadvantages:

In both the articles, the researchers have given a sensible portrayal of the great

circumstances and basic in standard costing structure. A bit of the typical advantages said in

both the articles join the accompanying:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Standard costing structure is used as the benchmark where the original cost is

comapred with standard cost. This proposes the system starting at now sets the

volume to be made and the surveyed development levels, which would then be

differentiated and the authentic execution (McLean et al. 2016).

It is possible to change the suppliers and there could be introduction of redesigned

methodology and materials for accomplishing cost objectives.

The comparative disadvantages that could be recognized from both the exploration

papers comprise of the accompanying:

In this structure, it isn't possible to control a couple of costs or they could be to an

awesome degree high for achievement. Thus, the specialists most likely won't feel

propelled, if the organization views them as accountable for troublesome contrasts.

Standard costing system routinely results in definitive weight to the directors in view

of off base estimation of significant worth chronicle and run of the mill hardship

(Nuhu et al. 2016).

In any case, certain basic difference in the revelations of the two studies are indentified and

they are indicated rapidly as takes after:

Even anyway both the articles have focused on one particular affiliation each, the two

affiliations don't have a place with a comparable part. For the essential article, the

standard costing has been used with respect to MTN, which is an organization

affiliation giving telecommunication organizations to its customers in Nigeria.

Thusly, the qualification that is clear is the utilization of the standard costing system

in collecting and organization fragment (Klychova et al. 2014).

It has been found that the article has inspected various sorts of standard costing,

which fuse culminate standard, achievable standard, current standard, fundamental

Standard costing structure is used as the benchmark where the original cost is

comapred with standard cost. This proposes the system starting at now sets the

volume to be made and the surveyed development levels, which would then be

differentiated and the authentic execution (McLean et al. 2016).

It is possible to change the suppliers and there could be introduction of redesigned

methodology and materials for accomplishing cost objectives.

The comparative disadvantages that could be recognized from both the exploration

papers comprise of the accompanying:

In this structure, it isn't possible to control a couple of costs or they could be to an

awesome degree high for achievement. Thus, the specialists most likely won't feel

propelled, if the organization views them as accountable for troublesome contrasts.

Standard costing system routinely results in definitive weight to the directors in view

of off base estimation of significant worth chronicle and run of the mill hardship

(Nuhu et al. 2016).

In any case, certain basic difference in the revelations of the two studies are indentified and

they are indicated rapidly as takes after:

Even anyway both the articles have focused on one particular affiliation each, the two

affiliations don't have a place with a comparable part. For the essential article, the

standard costing has been used with respect to MTN, which is an organization

affiliation giving telecommunication organizations to its customers in Nigeria.

Thusly, the qualification that is clear is the utilization of the standard costing system

in collecting and organization fragment (Klychova et al. 2014).

It has been found that the article has inspected various sorts of standard costing,

which fuse culminate standard, achievable standard, current standard, fundamental

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

standard, work standard and material standard. The material standard relies upon

building and concentrated subtle elements and the work standard depicts the right

assessments of work to be utilized. In the second article, no affirmations could be

found as for the sorts of standard costing.

The consideration is on how the telecommunication organizations of Nigeria use

standard costing structure for cost control and the techniques through which such cost

control could be enhanced further to raise the advantage level of MTN. Regardless, it

has been recognized that the Operations Manager of ASL assumes that the affiliation

is encountering loss of offers salary as a result of standard costing structure.

standard, work standard and material standard. The material standard relies upon

building and concentrated subtle elements and the work standard depicts the right

assessments of work to be utilized. In the second article, no affirmations could be

found as for the sorts of standard costing.

The consideration is on how the telecommunication organizations of Nigeria use

standard costing structure for cost control and the techniques through which such cost

control could be enhanced further to raise the advantage level of MTN. Regardless, it

has been recognized that the Operations Manager of ASL assumes that the affiliation

is encountering loss of offers salary as a result of standard costing structure.

11MANAGERIAL ACCOUNTING

Four specific outcomes of the research findings of two studies useful for the

management accountants in Australian organizations:

Certain outcomes have been perceived that could be significant for the general

population filling in as administration accountants in the Australian firms and two of them

have been distinguished from the main article (Zoni 2017). They are explained rapidly as

takes after:

Improved cost control:

It has been perceived that MTN could get expanded cost control, if it sets standards

for each one of the costs caused and after this; the variances and exceptions could be included

if there ought to emerge an event of models where there are differentiates between the

arranged circumstance and the genuine circumstance. The distinctions give a beginning base

with a particular true objective to condemn the feasibility of administrators to control the

costs for which they are dependable (Ji 2017). For instance, in the production house of MTN,

it is acknowledged that the genuine material cost of $52,015 have gone past the standard

costs by $6,015. It is useful for the administration accountants to understand that the material

costs have outperform by $6,015, instead of realizing that the genuine material cost indicated

$52,015.

In perspective of this information, the management could determine the reasons for

the increase of genuine cost over standard cost and in like manner, exercises could be

endeavored for amending the same. Additional examinations would disclose whether the

distinction happened in light of insufficient material use or higher costs in perspective of

expansion or inadequate purchase. In either case, standard costing system gives early banner

by revealing insight into the potential risk for helping the administration of the affiliation.

Four specific outcomes of the research findings of two studies useful for the

management accountants in Australian organizations:

Certain outcomes have been perceived that could be significant for the general

population filling in as administration accountants in the Australian firms and two of them

have been distinguished from the main article (Zoni 2017). They are explained rapidly as

takes after:

Improved cost control:

It has been perceived that MTN could get expanded cost control, if it sets standards

for each one of the costs caused and after this; the variances and exceptions could be included

if there ought to emerge an event of models where there are differentiates between the

arranged circumstance and the genuine circumstance. The distinctions give a beginning base

with a particular true objective to condemn the feasibility of administrators to control the

costs for which they are dependable (Ji 2017). For instance, in the production house of MTN,

it is acknowledged that the genuine material cost of $52,015 have gone past the standard

costs by $6,015. It is useful for the administration accountants to understand that the material

costs have outperform by $6,015, instead of realizing that the genuine material cost indicated

$52,015.

In perspective of this information, the management could determine the reasons for

the increase of genuine cost over standard cost and in like manner, exercises could be

endeavored for amending the same. Additional examinations would disclose whether the

distinction happened in light of insufficient material use or higher costs in perspective of

expansion or inadequate purchase. In either case, standard costing system gives early banner

by revealing insight into the potential risk for helping the administration of the affiliation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.