Impairment Loss Allocation to Assets

VerifiedAdded on 2020/04/01

|10

|1620

|119

AI Summary

This assignment focuses on calculating the impairment loss allocation for a company's assets, specifically machinery and a patent. It provides a scenario where the fair value of the patent is lower than its carrying amount, triggering an impairment assessment. The student must determine the appropriate allocation of the impairment loss between the assets based on their carrying amounts and assigned ratios. The assignment also explores different scenarios with varying fair values to demonstrate the impact on allocation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

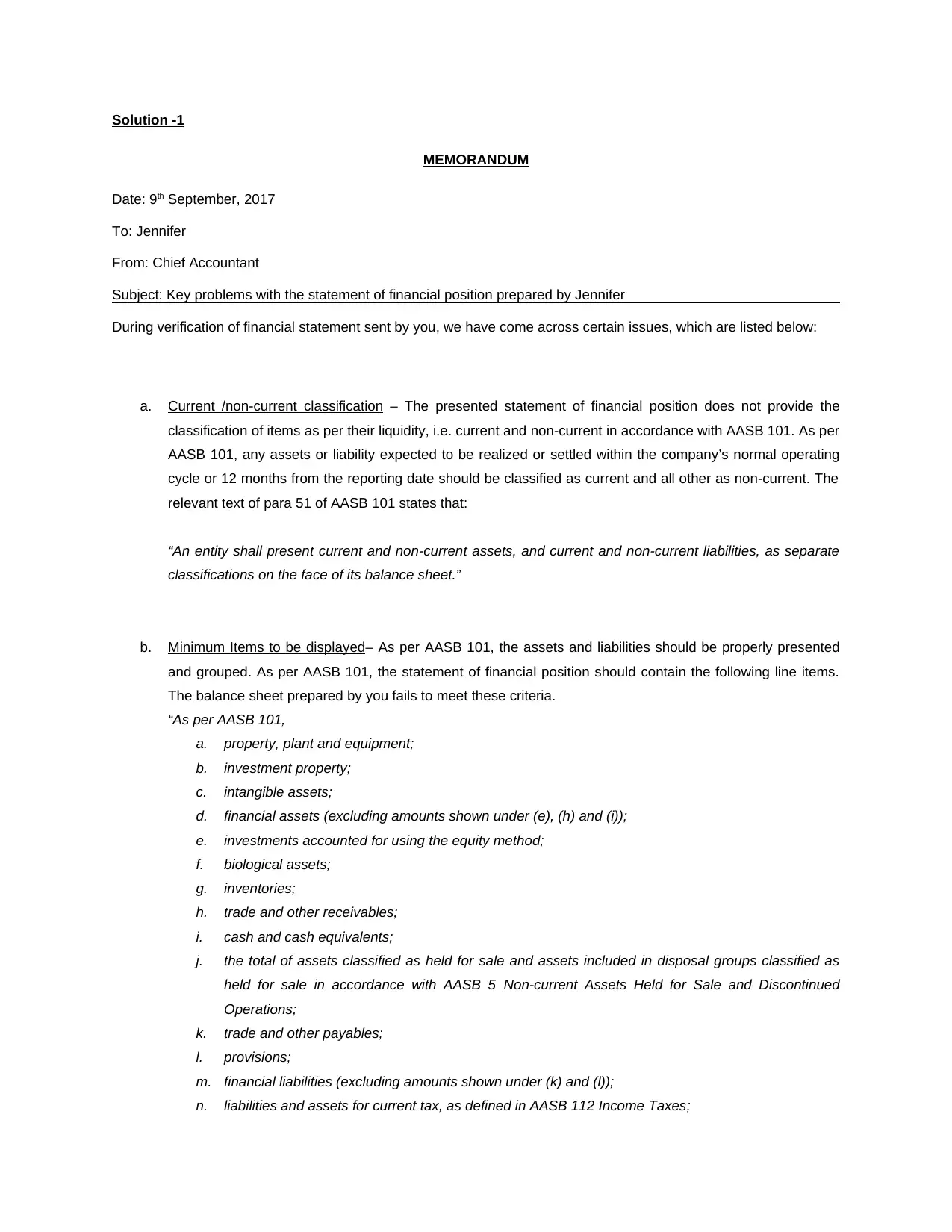

Solution -1

MEMORANDUM

Date: 9th September, 2017

To: Jennifer

From: Chief Accountant

Subject: Key problems with the statement of financial position prepared by Jennifer

During verification of financial statement sent by you, we have come across certain issues, which are listed below:

a. Current /non-current classification – The presented statement of financial position does not provide the

classification of items as per their liquidity, i.e. current and non-current in accordance with AASB 101. As per

AASB 101, any assets or liability expected to be realized or settled within the company’s normal operating

cycle or 12 months from the reporting date should be classified as current and all other as non-current. The

relevant text of para 51 of AASB 101 states that:

“An entity shall present current and non-current assets, and current and non-current liabilities, as separate

classifications on the face of its balance sheet.”

b. Minimum Items to be displayed– As per AASB 101, the assets and liabilities should be properly presented

and grouped. As per AASB 101, the statement of financial position should contain the following line items.

The balance sheet prepared by you fails to meet these criteria.

“As per AASB 101,

a. property, plant and equipment;

b. investment property;

c. intangible assets;

d. financial assets (excluding amounts shown under (e), (h) and (i));

e. investments accounted for using the equity method;

f. biological assets;

g. inventories;

h. trade and other receivables;

i. cash and cash equivalents;

j. the total of assets classified as held for sale and assets included in disposal groups classified as

held for sale in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued

Operations;

k. trade and other payables;

l. provisions;

m. financial liabilities (excluding amounts shown under (k) and (l));

n. liabilities and assets for current tax, as defined in AASB 112 Income Taxes;

MEMORANDUM

Date: 9th September, 2017

To: Jennifer

From: Chief Accountant

Subject: Key problems with the statement of financial position prepared by Jennifer

During verification of financial statement sent by you, we have come across certain issues, which are listed below:

a. Current /non-current classification – The presented statement of financial position does not provide the

classification of items as per their liquidity, i.e. current and non-current in accordance with AASB 101. As per

AASB 101, any assets or liability expected to be realized or settled within the company’s normal operating

cycle or 12 months from the reporting date should be classified as current and all other as non-current. The

relevant text of para 51 of AASB 101 states that:

“An entity shall present current and non-current assets, and current and non-current liabilities, as separate

classifications on the face of its balance sheet.”

b. Minimum Items to be displayed– As per AASB 101, the assets and liabilities should be properly presented

and grouped. As per AASB 101, the statement of financial position should contain the following line items.

The balance sheet prepared by you fails to meet these criteria.

“As per AASB 101,

a. property, plant and equipment;

b. investment property;

c. intangible assets;

d. financial assets (excluding amounts shown under (e), (h) and (i));

e. investments accounted for using the equity method;

f. biological assets;

g. inventories;

h. trade and other receivables;

i. cash and cash equivalents;

j. the total of assets classified as held for sale and assets included in disposal groups classified as

held for sale in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued

Operations;

k. trade and other payables;

l. provisions;

m. financial liabilities (excluding amounts shown under (k) and (l));

n. liabilities and assets for current tax, as defined in AASB 112 Income Taxes;

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

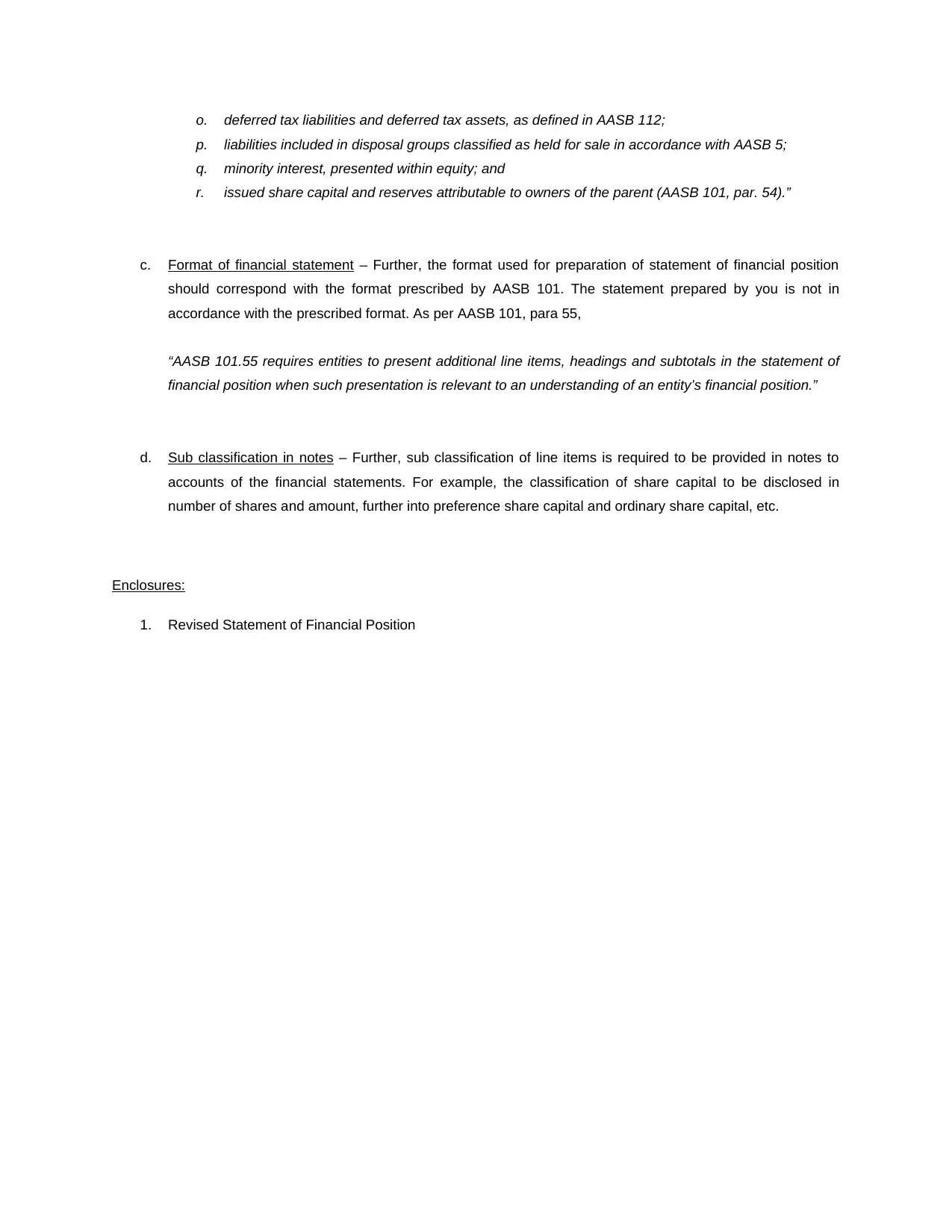

o. deferred tax liabilities and deferred tax assets, as defined in AASB 112;

p. liabilities included in disposal groups classified as held for sale in accordance with AASB 5;

q. minority interest, presented within equity; and

r. issued share capital and reserves attributable to owners of the parent (AASB 101, par. 54).”

c. Format of financial statement – Further, the format used for preparation of statement of financial position

should correspond with the format prescribed by AASB 101. The statement prepared by you is not in

accordance with the prescribed format. As per AASB 101, para 55,

“AASB 101.55 requires entities to present additional line items, headings and subtotals in the statement of

financial position when such presentation is relevant to an understanding of an entity’s financial position.”

d. Sub classification in notes – Further, sub classification of line items is required to be provided in notes to

accounts of the financial statements. For example, the classification of share capital to be disclosed in

number of shares and amount, further into preference share capital and ordinary share capital, etc.

Enclosures:

1. Revised Statement of Financial Position

p. liabilities included in disposal groups classified as held for sale in accordance with AASB 5;

q. minority interest, presented within equity; and

r. issued share capital and reserves attributable to owners of the parent (AASB 101, par. 54).”

c. Format of financial statement – Further, the format used for preparation of statement of financial position

should correspond with the format prescribed by AASB 101. The statement prepared by you is not in

accordance with the prescribed format. As per AASB 101, para 55,

“AASB 101.55 requires entities to present additional line items, headings and subtotals in the statement of

financial position when such presentation is relevant to an understanding of an entity’s financial position.”

d. Sub classification in notes – Further, sub classification of line items is required to be provided in notes to

accounts of the financial statements. For example, the classification of share capital to be disclosed in

number of shares and amount, further into preference share capital and ordinary share capital, etc.

Enclosures:

1. Revised Statement of Financial Position

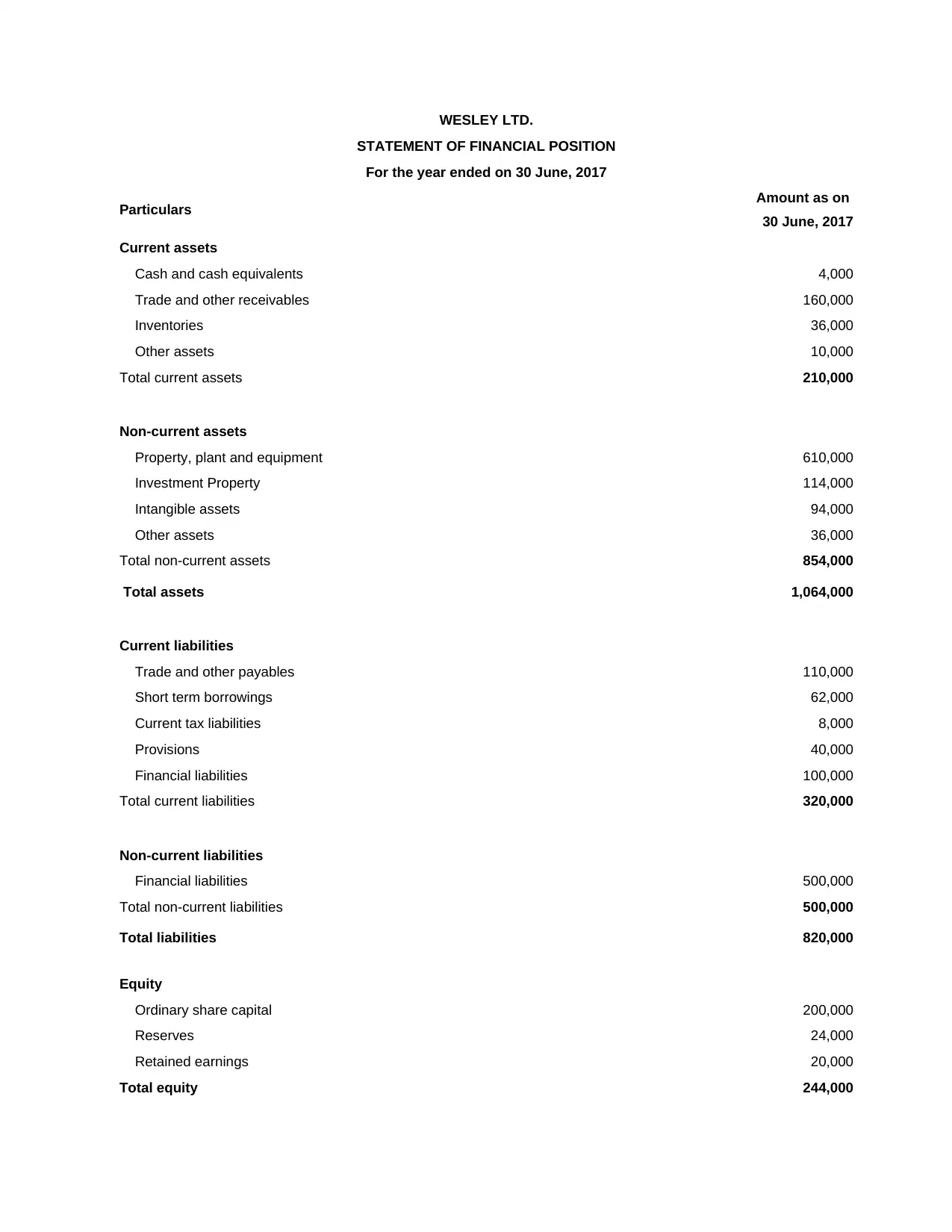

WESLEY LTD.

STATEMENT OF FINANCIAL POSITION

For the year ended on 30 June, 2017

Particulars Amount as on

30 June, 2017

Current assets

Cash and cash equivalents 4,000

Trade and other receivables 160,000

Inventories 36,000

Other assets 10,000

Total current assets 210,000

Non-current assets

Property, plant and equipment 610,000

Investment Property 114,000

Intangible assets 94,000

Other assets 36,000

Total non-current assets 854,000

Total assets 1,064,000

Current liabilities

Trade and other payables 110,000

Short term borrowings 62,000

Current tax liabilities 8,000

Provisions 40,000

Financial liabilities 100,000

Total current liabilities 320,000

Non-current liabilities

Financial liabilities 500,000

Total non-current liabilities 500,000

Total liabilities 820,000

Equity

Ordinary share capital 200,000

Reserves 24,000

Retained earnings 20,000

Total equity 244,000

STATEMENT OF FINANCIAL POSITION

For the year ended on 30 June, 2017

Particulars Amount as on

30 June, 2017

Current assets

Cash and cash equivalents 4,000

Trade and other receivables 160,000

Inventories 36,000

Other assets 10,000

Total current assets 210,000

Non-current assets

Property, plant and equipment 610,000

Investment Property 114,000

Intangible assets 94,000

Other assets 36,000

Total non-current assets 854,000

Total assets 1,064,000

Current liabilities

Trade and other payables 110,000

Short term borrowings 62,000

Current tax liabilities 8,000

Provisions 40,000

Financial liabilities 100,000

Total current liabilities 320,000

Non-current liabilities

Financial liabilities 500,000

Total non-current liabilities 500,000

Total liabilities 820,000

Equity

Ordinary share capital 200,000

Reserves 24,000

Retained earnings 20,000

Total equity 244,000

Total liabilities and equity 1,064,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Solution-2

Journal Entries in the books of Ansett Ltd

Date Description

Dr./

Cr. Debit Credit

31-Jul-16 Bank Account Dr. 8,250,000

To Share Application Money Account 8,250,000

(Share application money received on 5,500,000 shares)

12-Aug-16 Share Application Money Account Dr. 8,250,000

To Share Capital Account 7,500,000

To Bank Account 750,000

(5,000,000 shares allotted and application money on 500,000 shares

returned)

12-Aug-16 Share Allotment Account Dr. 1,500,000

To Share Capital Account 1,500,000

(Amount due on share allotment)

12-Sep-16 Bank Account Dr. 1,500,000

To Share Allotment Account 1,500,000

(Allotment money received)

20-Mar-17 Share First Call Account Dr. 1,000,000

To Share Capital Account 1,000,000

(Amount due on share first call)

30-Apr-17 Bank Account Dr. 990,000

To Share First Call Account 990,000

(First call received on 4,950,000)

31-May-17 Share Capital Account Dr. 100,000

To Share First Call Account 10,000

To Forfeited Shares Account 90,000

(50,000 shares forfeited for non-payment of share first call amount)

Journal Entries in the books of Ansett Ltd

Date Description

Dr./

Cr. Debit Credit

31-Jul-16 Bank Account Dr. 8,250,000

To Share Application Money Account 8,250,000

(Share application money received on 5,500,000 shares)

12-Aug-16 Share Application Money Account Dr. 8,250,000

To Share Capital Account 7,500,000

To Bank Account 750,000

(5,000,000 shares allotted and application money on 500,000 shares

returned)

12-Aug-16 Share Allotment Account Dr. 1,500,000

To Share Capital Account 1,500,000

(Amount due on share allotment)

12-Sep-16 Bank Account Dr. 1,500,000

To Share Allotment Account 1,500,000

(Allotment money received)

20-Mar-17 Share First Call Account Dr. 1,000,000

To Share Capital Account 1,000,000

(Amount due on share first call)

30-Apr-17 Bank Account Dr. 990,000

To Share First Call Account 990,000

(First call received on 4,950,000)

31-May-17 Share Capital Account Dr. 100,000

To Share First Call Account 10,000

To Forfeited Shares Account 90,000

(50,000 shares forfeited for non-payment of share first call amount)

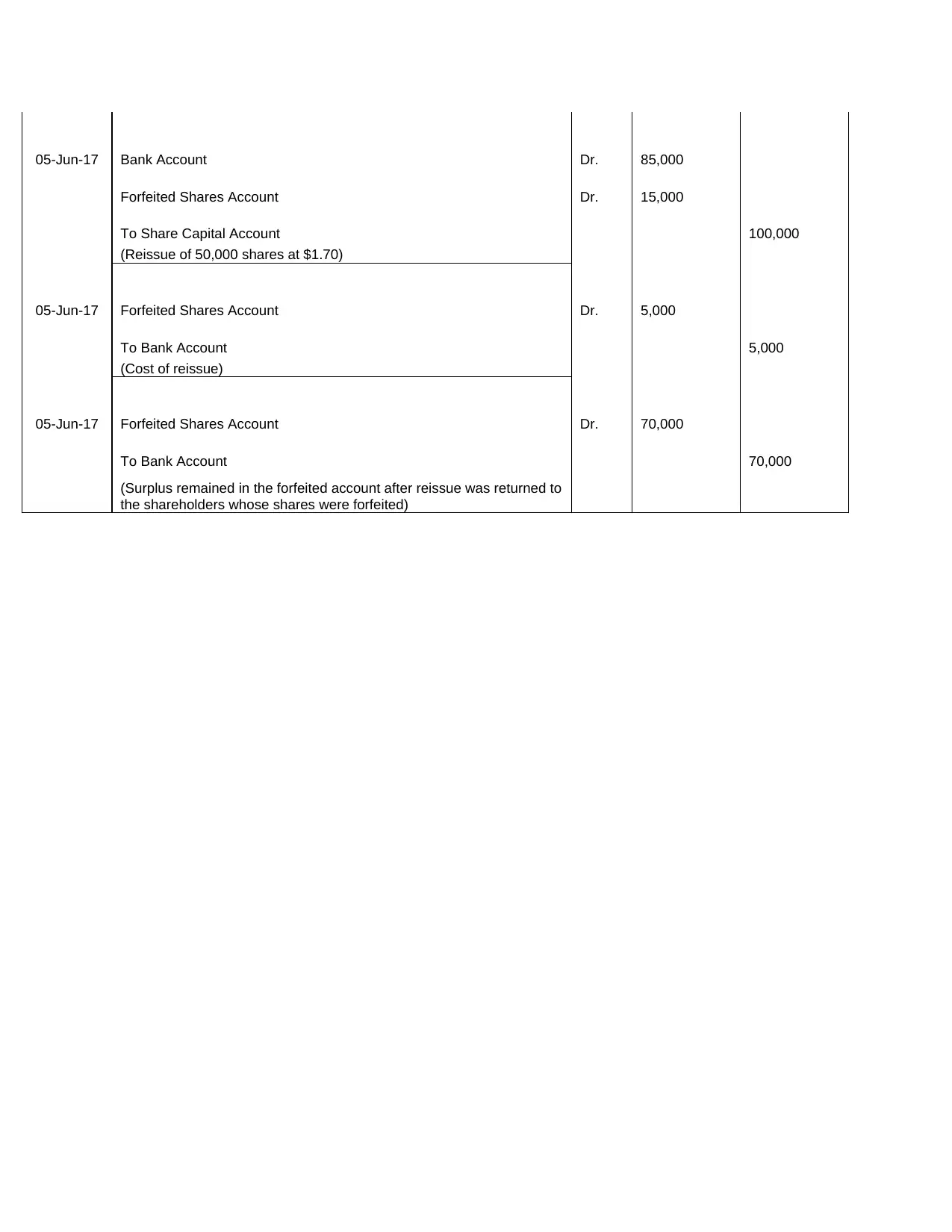

05-Jun-17 Bank Account Dr. 85,000

Forfeited Shares Account Dr. 15,000

To Share Capital Account 100,000

(Reissue of 50,000 shares at $1.70)

05-Jun-17 Forfeited Shares Account Dr. 5,000

To Bank Account 5,000

(Cost of reissue)

05-Jun-17 Forfeited Shares Account Dr. 70,000

To Bank Account 70,000

(Surplus remained in the forfeited account after reissue was returned to

the shareholders whose shares were forfeited)

Forfeited Shares Account Dr. 15,000

To Share Capital Account 100,000

(Reissue of 50,000 shares at $1.70)

05-Jun-17 Forfeited Shares Account Dr. 5,000

To Bank Account 5,000

(Cost of reissue)

05-Jun-17 Forfeited Shares Account Dr. 70,000

To Bank Account 70,000

(Surplus remained in the forfeited account after reissue was returned to

the shareholders whose shares were forfeited)

Solution-3

Journal Entries in the books of Genesis Ltd

Date Description

Dr. /

Cr. Debit Credit

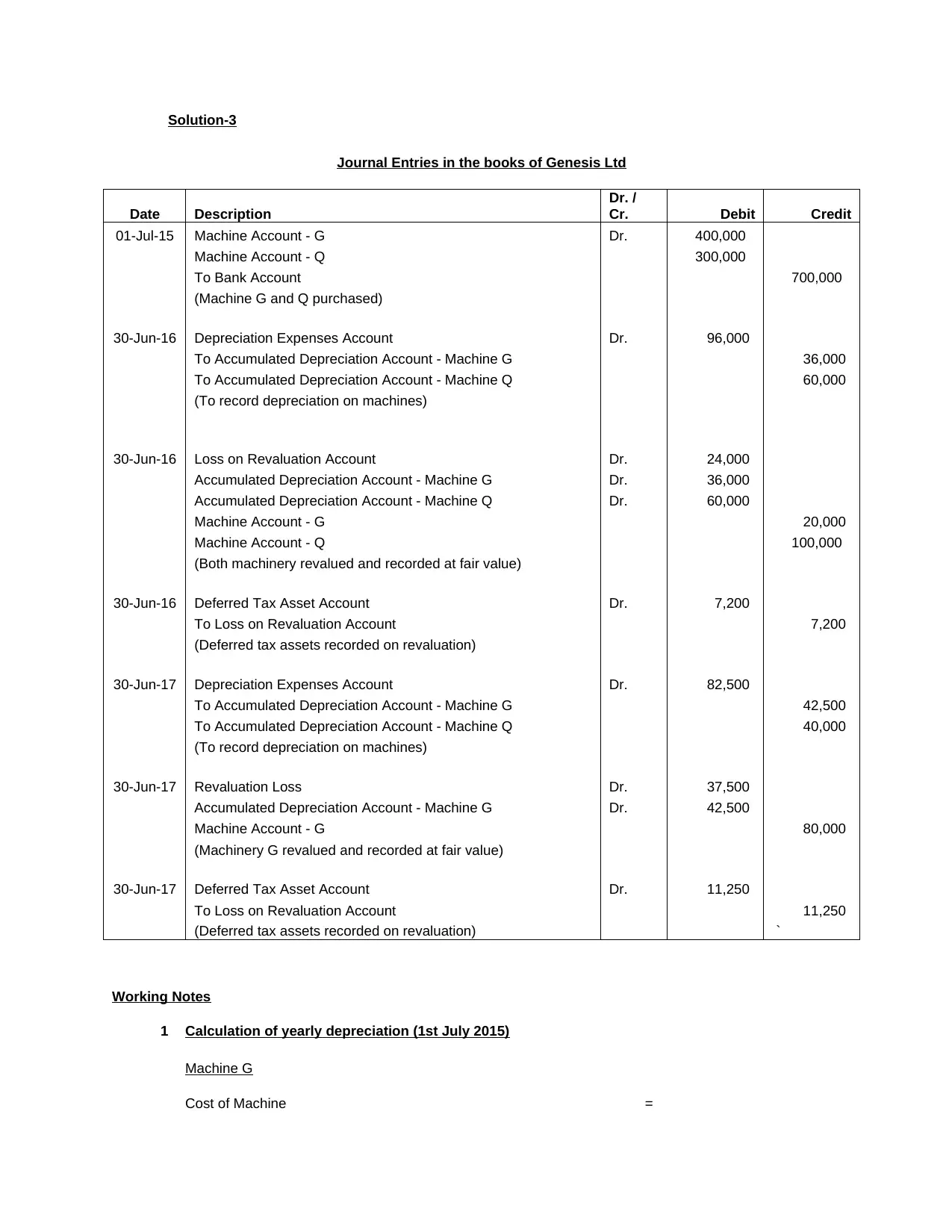

01-Jul-15 Machine Account - G Dr. 400,000

Machine Account - Q 300,000

To Bank Account 700,000

(Machine G and Q purchased)

30-Jun-16 Depreciation Expenses Account Dr. 96,000

To Accumulated Depreciation Account - Machine G 36,000

To Accumulated Depreciation Account - Machine Q 60,000

(To record depreciation on machines)

30-Jun-16 Loss on Revaluation Account Dr. 24,000

Accumulated Depreciation Account - Machine G Dr. 36,000

Accumulated Depreciation Account - Machine Q Dr. 60,000

Machine Account - G 20,000

Machine Account - Q 100,000

(Both machinery revalued and recorded at fair value)

30-Jun-16 Deferred Tax Asset Account Dr. 7,200

To Loss on Revaluation Account 7,200

(Deferred tax assets recorded on revaluation)

30-Jun-17 Depreciation Expenses Account Dr. 82,500

To Accumulated Depreciation Account - Machine G 42,500

To Accumulated Depreciation Account - Machine Q 40,000

(To record depreciation on machines)

30-Jun-17 Revaluation Loss Dr. 37,500

Accumulated Depreciation Account - Machine G Dr. 42,500

Machine Account - G 80,000

(Machinery G revalued and recorded at fair value)

30-Jun-17 Deferred Tax Asset Account Dr. 11,250

To Loss on Revaluation Account 11,250

(Deferred tax assets recorded on revaluation) `

Working Notes

1 Calculation of yearly depreciation (1st July 2015)

Machine G

Cost of Machine =

Journal Entries in the books of Genesis Ltd

Date Description

Dr. /

Cr. Debit Credit

01-Jul-15 Machine Account - G Dr. 400,000

Machine Account - Q 300,000

To Bank Account 700,000

(Machine G and Q purchased)

30-Jun-16 Depreciation Expenses Account Dr. 96,000

To Accumulated Depreciation Account - Machine G 36,000

To Accumulated Depreciation Account - Machine Q 60,000

(To record depreciation on machines)

30-Jun-16 Loss on Revaluation Account Dr. 24,000

Accumulated Depreciation Account - Machine G Dr. 36,000

Accumulated Depreciation Account - Machine Q Dr. 60,000

Machine Account - G 20,000

Machine Account - Q 100,000

(Both machinery revalued and recorded at fair value)

30-Jun-16 Deferred Tax Asset Account Dr. 7,200

To Loss on Revaluation Account 7,200

(Deferred tax assets recorded on revaluation)

30-Jun-17 Depreciation Expenses Account Dr. 82,500

To Accumulated Depreciation Account - Machine G 42,500

To Accumulated Depreciation Account - Machine Q 40,000

(To record depreciation on machines)

30-Jun-17 Revaluation Loss Dr. 37,500

Accumulated Depreciation Account - Machine G Dr. 42,500

Machine Account - G 80,000

(Machinery G revalued and recorded at fair value)

30-Jun-17 Deferred Tax Asset Account Dr. 11,250

To Loss on Revaluation Account 11,250

(Deferred tax assets recorded on revaluation) `

Working Notes

1 Calculation of yearly depreciation (1st July 2015)

Machine G

Cost of Machine =

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

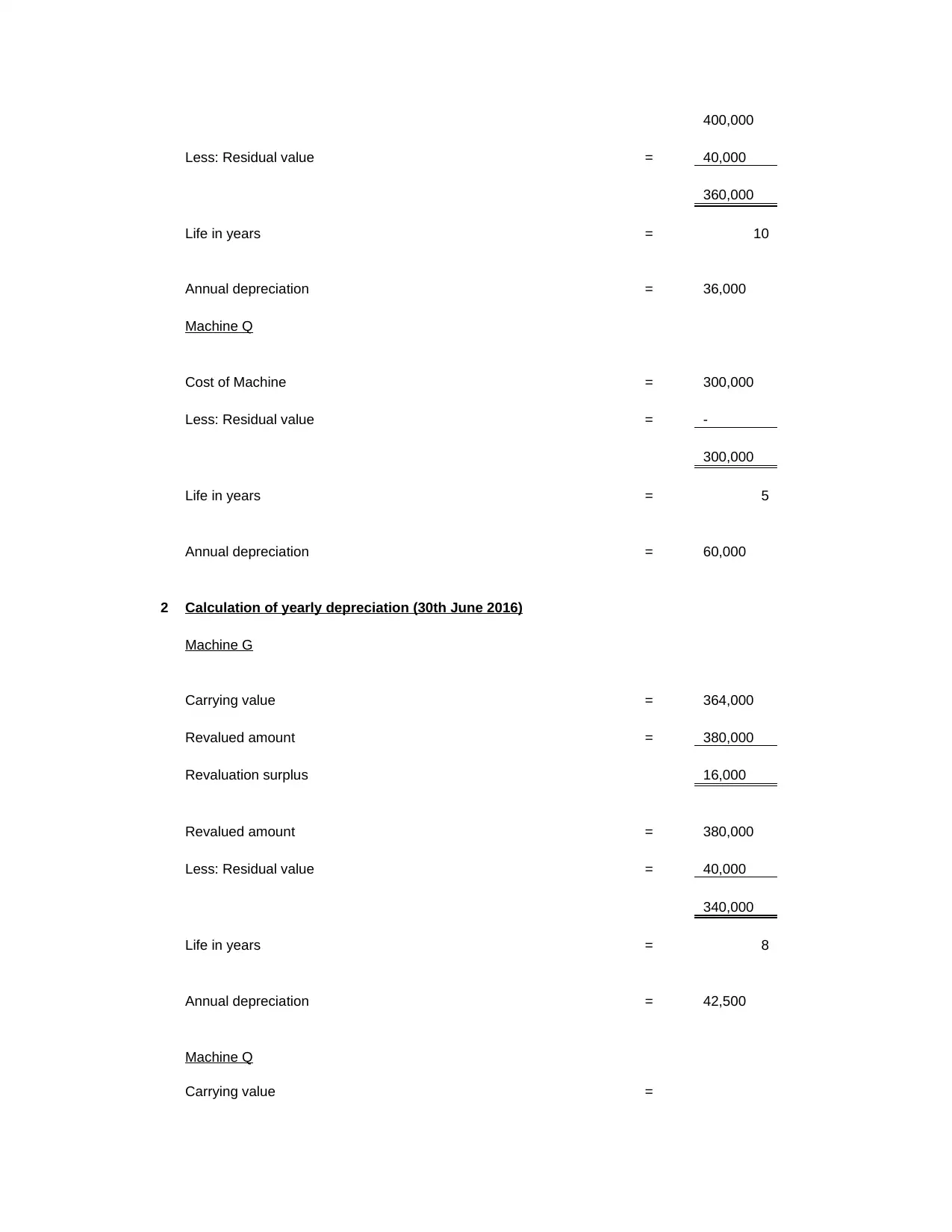

400,000

Less: Residual value = 40,000

360,000

Life in years = 10

Annual depreciation = 36,000

Machine Q

Cost of Machine = 300,000

Less: Residual value = -

300,000

Life in years = 5

Annual depreciation = 60,000

2 Calculation of yearly depreciation (30th June 2016)

Machine G

Carrying value = 364,000

Revalued amount = 380,000

Revaluation surplus 16,000

Revalued amount = 380,000

Less: Residual value = 40,000

340,000

Life in years = 8

Annual depreciation = 42,500

Machine Q

Carrying value =

Less: Residual value = 40,000

360,000

Life in years = 10

Annual depreciation = 36,000

Machine Q

Cost of Machine = 300,000

Less: Residual value = -

300,000

Life in years = 5

Annual depreciation = 60,000

2 Calculation of yearly depreciation (30th June 2016)

Machine G

Carrying value = 364,000

Revalued amount = 380,000

Revaluation surplus 16,000

Revalued amount = 380,000

Less: Residual value = 40,000

340,000

Life in years = 8

Annual depreciation = 42,500

Machine Q

Carrying value =

240,000

Revalued amount = 200,000

Revaluation loss 40,000

Revalued amount = 200,000

Less: Residual value = -

200,000

Life in years = 5

Annual depreciation = 40,000

3 Calculation of yearly depreciation (30th June 2017)

Machine G

Carrying value = 337,500

Revalued amount = 300,000

Revaluation loss 37,500

Machine Q

Carrying value = 160,000

Revalued amount = 160,000

-

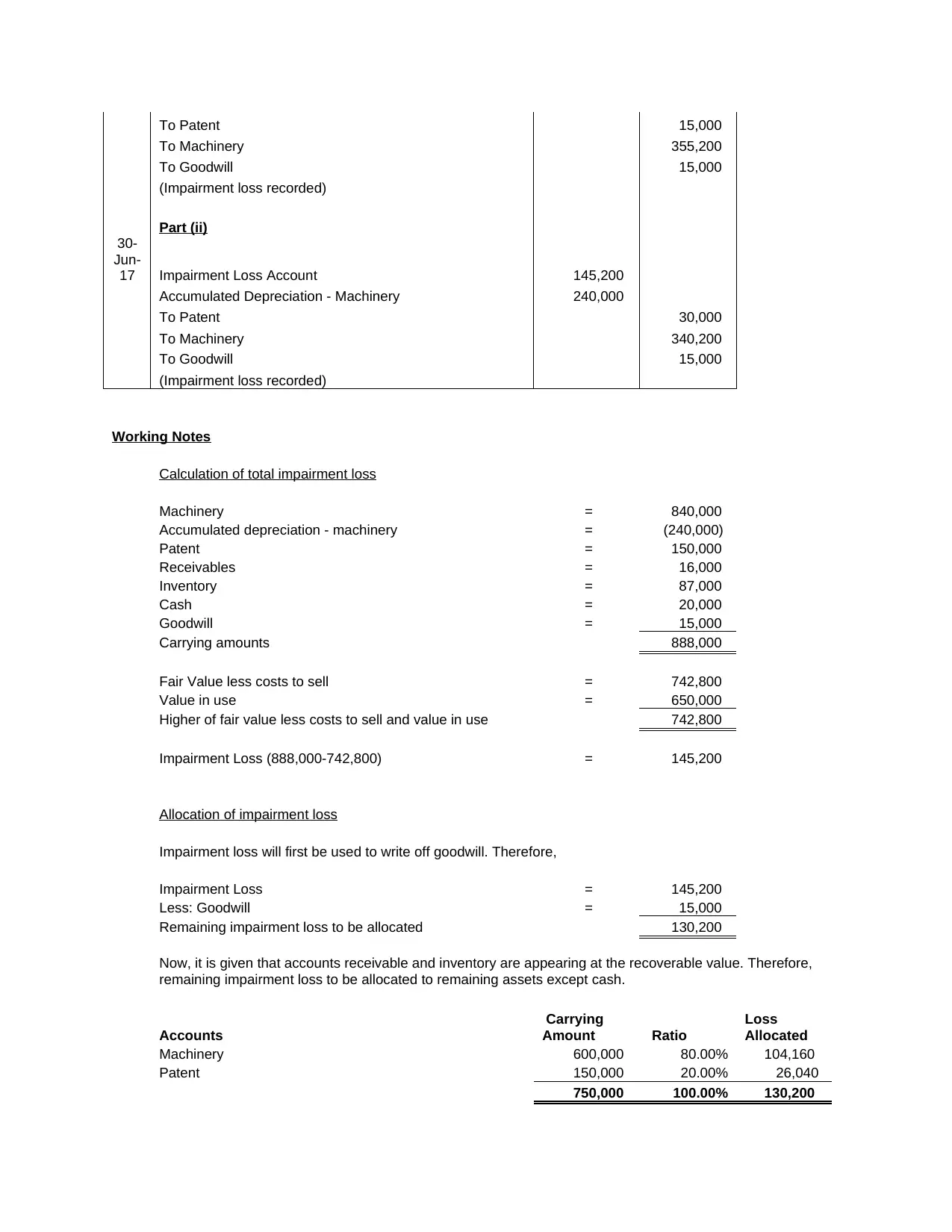

Solution-4

Journal Entries in the books of Big Friday Ltd

Dat

e Description Debit Credit

Part (i)

30-

Jun-

17 Impairment Loss Account 145,200

Accumulated Depreciation - Machinery 240,000

Revalued amount = 200,000

Revaluation loss 40,000

Revalued amount = 200,000

Less: Residual value = -

200,000

Life in years = 5

Annual depreciation = 40,000

3 Calculation of yearly depreciation (30th June 2017)

Machine G

Carrying value = 337,500

Revalued amount = 300,000

Revaluation loss 37,500

Machine Q

Carrying value = 160,000

Revalued amount = 160,000

-

Solution-4

Journal Entries in the books of Big Friday Ltd

Dat

e Description Debit Credit

Part (i)

30-

Jun-

17 Impairment Loss Account 145,200

Accumulated Depreciation - Machinery 240,000

To Patent 15,000

To Machinery 355,200

To Goodwill 15,000

(Impairment loss recorded)

Part (ii)

30-

Jun-

17 Impairment Loss Account 145,200

Accumulated Depreciation - Machinery 240,000

To Patent 30,000

To Machinery 340,200

To Goodwill 15,000

(Impairment loss recorded)

Working Notes

Calculation of total impairment loss

Machinery = 840,000

Accumulated depreciation - machinery = (240,000)

Patent = 150,000

Receivables = 16,000

Inventory = 87,000

Cash = 20,000

Goodwill = 15,000

Carrying amounts 888,000

Fair Value less costs to sell = 742,800

Value in use = 650,000

Higher of fair value less costs to sell and value in use 742,800

Impairment Loss (888,000-742,800) = 145,200

Allocation of impairment loss

Impairment loss will first be used to write off goodwill. Therefore,

Impairment Loss = 145,200

Less: Goodwill = 15,000

Remaining impairment loss to be allocated 130,200

Now, it is given that accounts receivable and inventory are appearing at the recoverable value. Therefore,

remaining impairment loss to be allocated to remaining assets except cash.

Accounts

Carrying

Amount Ratio

Loss

Allocated

Machinery 600,000 80.00% 104,160

Patent 150,000 20.00% 26,040

750,000 100.00% 130,200

To Machinery 355,200

To Goodwill 15,000

(Impairment loss recorded)

Part (ii)

30-

Jun-

17 Impairment Loss Account 145,200

Accumulated Depreciation - Machinery 240,000

To Patent 30,000

To Machinery 340,200

To Goodwill 15,000

(Impairment loss recorded)

Working Notes

Calculation of total impairment loss

Machinery = 840,000

Accumulated depreciation - machinery = (240,000)

Patent = 150,000

Receivables = 16,000

Inventory = 87,000

Cash = 20,000

Goodwill = 15,000

Carrying amounts 888,000

Fair Value less costs to sell = 742,800

Value in use = 650,000

Higher of fair value less costs to sell and value in use 742,800

Impairment Loss (888,000-742,800) = 145,200

Allocation of impairment loss

Impairment loss will first be used to write off goodwill. Therefore,

Impairment Loss = 145,200

Less: Goodwill = 15,000

Remaining impairment loss to be allocated 130,200

Now, it is given that accounts receivable and inventory are appearing at the recoverable value. Therefore,

remaining impairment loss to be allocated to remaining assets except cash.

Accounts

Carrying

Amount Ratio

Loss

Allocated

Machinery 600,000 80.00% 104,160

Patent 150,000 20.00% 26,040

750,000 100.00% 130,200

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.