BAP11 Principles of Accounting: Cash Flow Statement Analysis 2018

VerifiedAdded on 2023/06/09

provided for every question.

.

Due date for this assignment is Week 11 (week starting 23 July 2018): oYour hand-written attempt

must be handed to the lecturer by latest end of lecture 11 class. oLate submissions will be subject to

a 25% reduction in marks obtained.

Results for this assessment will be released at the end of week 12.

ASSIGNMENT MARKING SHEET

For use by Examiners only.

Question Student Mark

1. /10

2. /20

3. /20

4. /10

5. /40

Total /100= /25

Lecturer’s comments

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

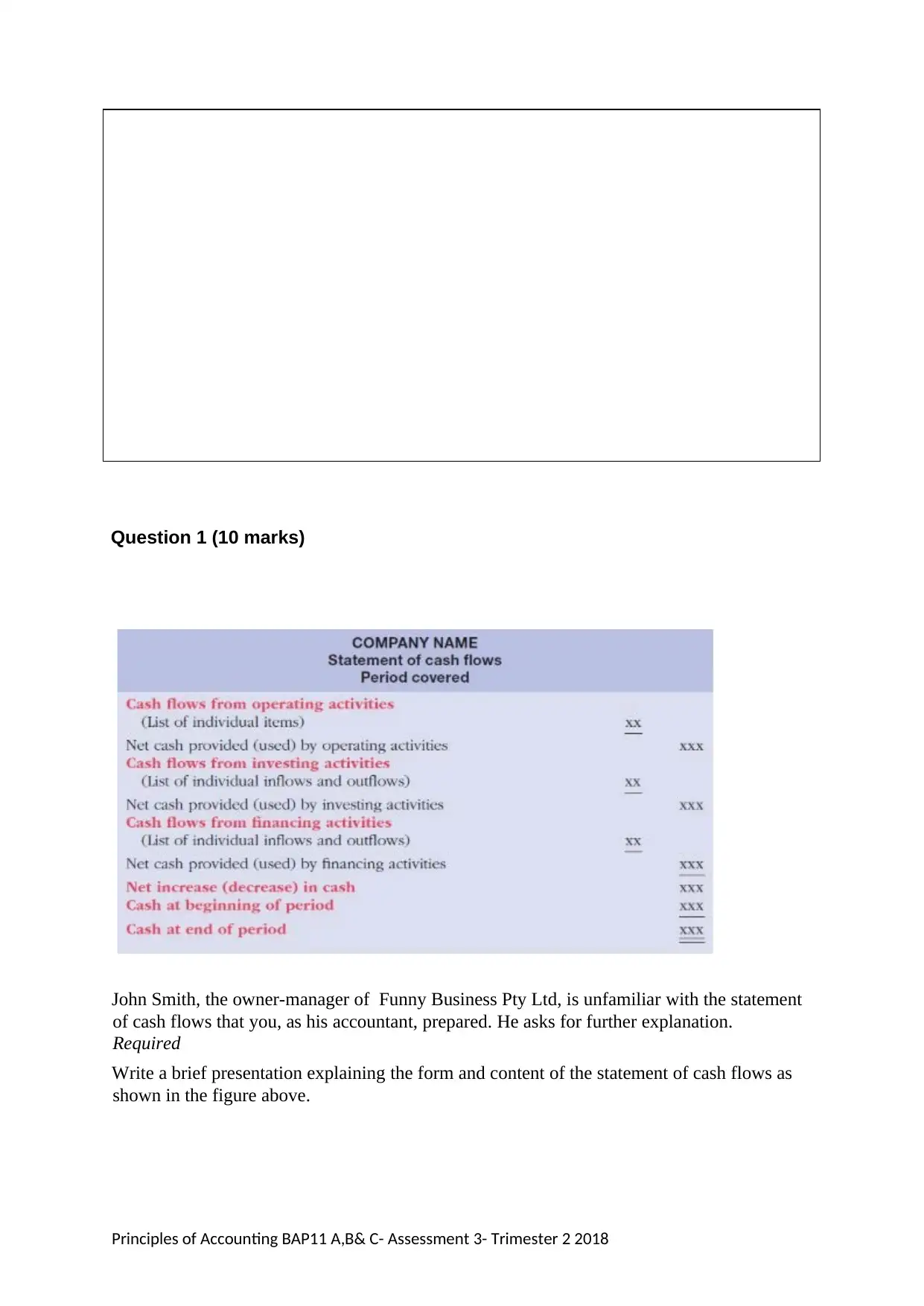

John Smith, the owner-manager of Funny Business Pty Ltd, is unfamiliar with the statement

of cash flows that you, as his accountant, prepared. He asks for further explanation.

Required

Write a brief presentation explaining the form and content of the statement of cash flows as

shown in the figure above.

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

cash to and from the business of the reporting entity. While preparing the cash flow statements entities do

not have to take into account the non-cash activities or transactions undertaken during the reported period

of time in the course of business. Cash flows statement generally covers three major activities of the

business which results in inflow and outflow of cash from the business. These activities are: operating

activities, investing activities and financing activities. The statement of cash flows bridges the gap between

the statement of income (profit and loss account) and statement of final position (balance sheet). The above

figure depicts that cash flow statement prepared using the direct approach as the cash flows from operating

activities are directly to be shown under the heading of operating activities and not supposed to be adjusted

from the current year’s balance of net income or loss. The possible cash flows from operating activities can

range from cash collection from trade receivables (increase in cash flows), cash payments to the trade

payables (decrease in cash flows), payment of income taxes and other operating expenses (decrease in cash

flows) of the business such as interests, wages and salaries. The said activities are undertaken as a result of

basic business operations and hence often referred as principle activities that produce revenues for the

entity. These activities primarily affect the short term assets and liabilities of the business. Investing activities

are those activities that involve purchase and sale of non-current assets of the business such as plant and

machinery, equipment, furniture and fixtures, motor vehicles, investments that are not covered by cash

equivalents (Higgins, 2012). The disposal of the above mentioned assets increases the flow of cash for the

business and the acquisition of such assets decreases the cash flows. The third item in the above figure

depicts the cash flows from financing activities. Financing activities are those activities that lead to change in

size or composition of firm’s equity capital or its borrowings. Cash flows from financing activities typically

cover repayment of loans taken from banks and financial institutions, issuance of debentures and shares to

raise the capital, buy-back of the entities of the shares. It also includes payment of interest and dividend to

the shareholders and other investors of the company. The borrowings from banks and the raising of funds

through the issuance of shares and debentures increase the cash flows of the business. Further, the

repayments of the same results in cash outflow of the business. The net cash flows from all the three

activities is adjusted to the opening balance of cash or cash equivalents of that year and from the total of

these two items must be equal to the closing cash balance of the business. If the total cash flows along with

the opening balance do not match with the closing cash balance, then it signifies that there is some clerical

or logical error in the preparation of cash flow statement (Brahmasrene, Strupeck & Whitten, 2004).

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

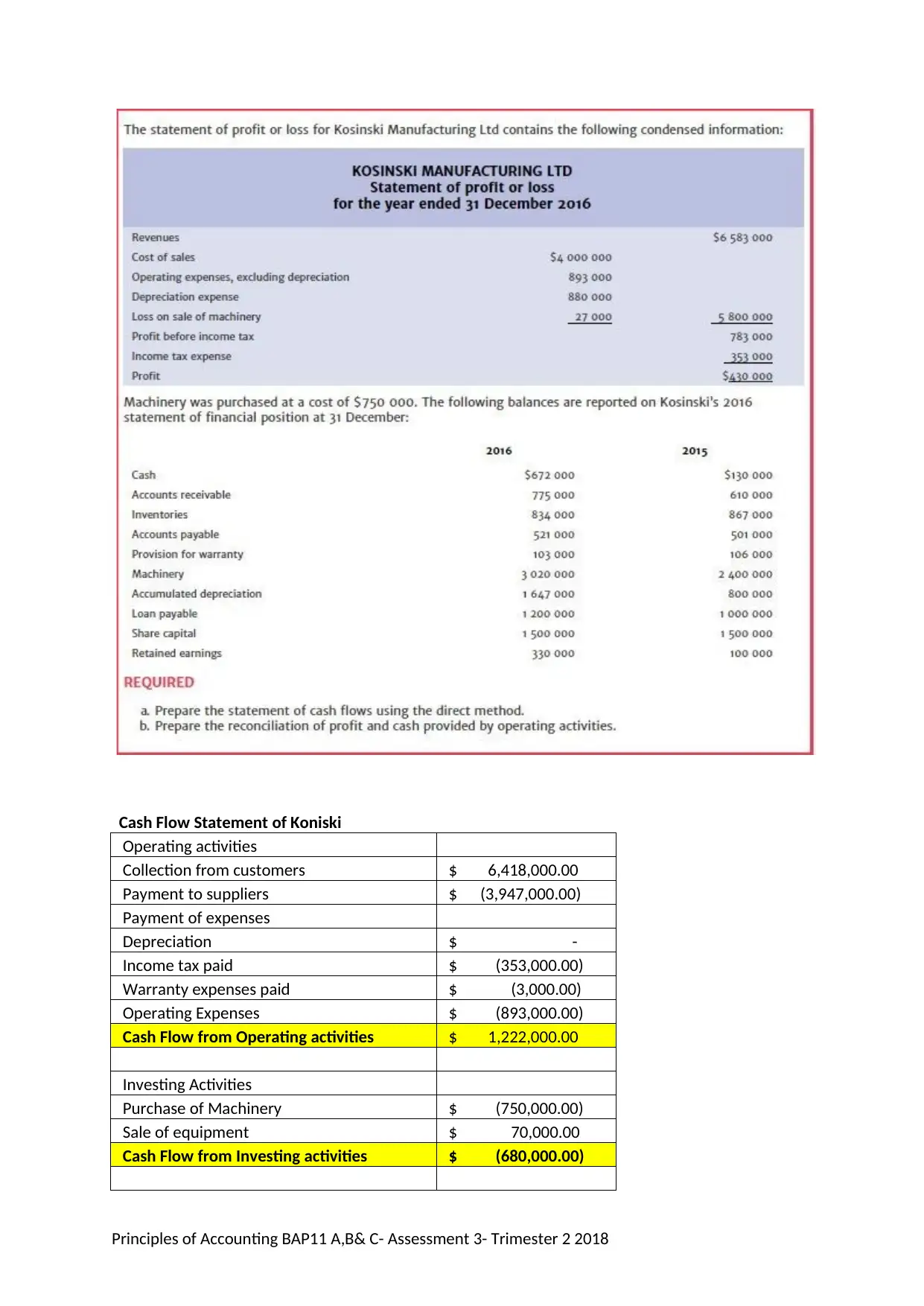

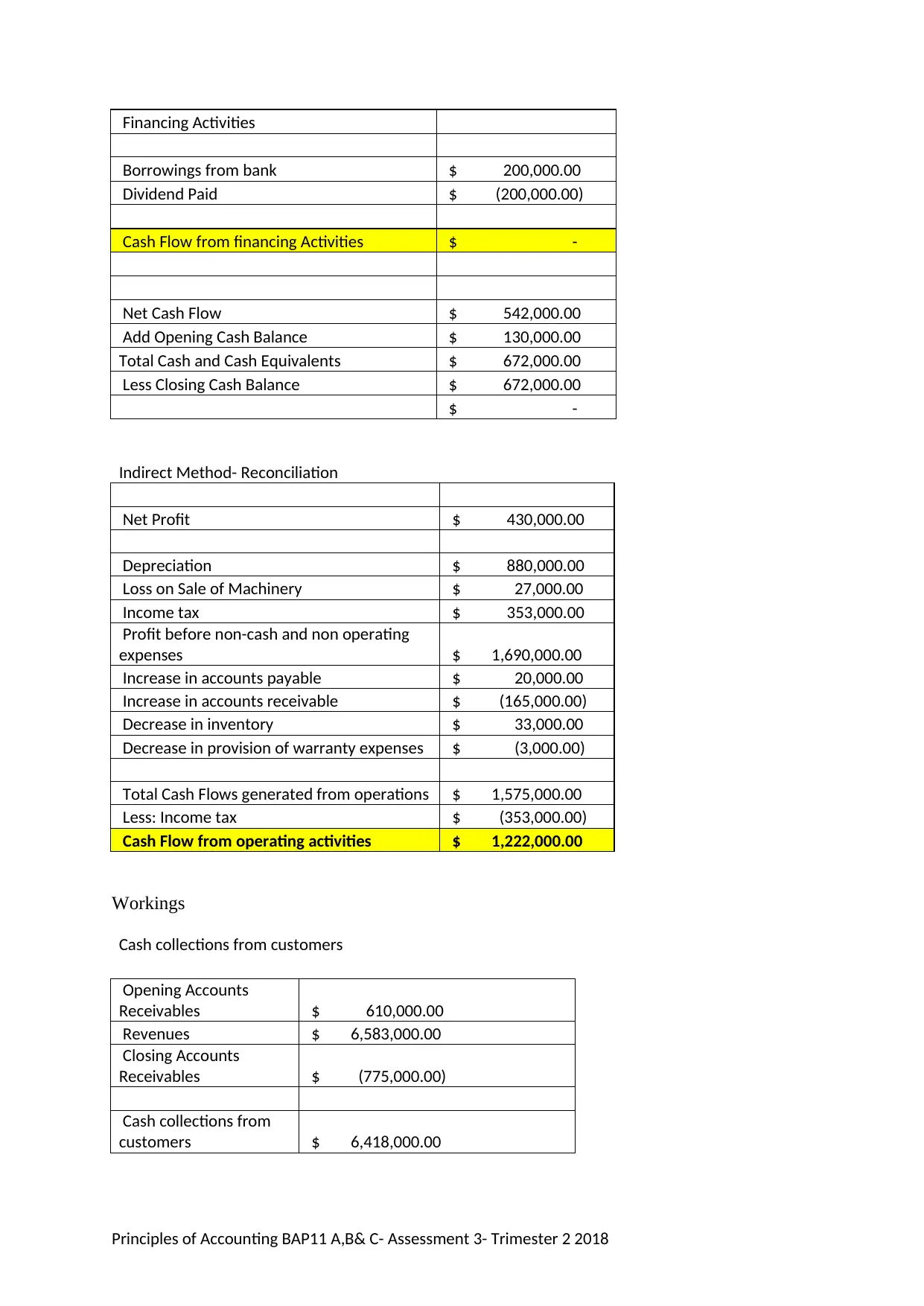

Operating activities

Collection from customers $ 6,418,000.00

Payment to suppliers $ (3,947,000.00)

Payment of expenses

Depreciation $ -

Income tax paid $ (353,000.00)

Warranty expenses paid $ (3,000.00)

Operating Expenses $ (893,000.00)

Cash Flow from Operating activities $ 1,222,000.00

Investing Activities

Purchase of Machinery $ (750,000.00)

Sale of equipment $ 70,000.00

Cash Flow from Investing activities $ (680,000.00)

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Borrowings from bank $ 200,000.00

Dividend Paid $ (200,000.00)

Cash Flow from financing Activities $ -

Net Cash Flow $ 542,000.00

Add Opening Cash Balance $ 130,000.00

Total Cash and Cash Equivalents $ 672,000.00

Less Closing Cash Balance $ 672,000.00

$ -

Indirect Method- Reconciliation

Net Profit $ 430,000.00

Depreciation $ 880,000.00

Loss on Sale of Machinery $ 27,000.00

Income tax $ 353,000.00

Profit before non-cash and non operating

expenses $ 1,690,000.00

Increase in accounts payable $ 20,000.00

Increase in accounts receivable $ (165,000.00)

Decrease in inventory $ 33,000.00

Decrease in provision of warranty expenses $ (3,000.00)

Total Cash Flows generated from operations $ 1,575,000.00

Less: Income tax $ (353,000.00)

Cash Flow from operating activities $ 1,222,000.00

Workings

Cash collections from customers

Opening Accounts

Receivables $ 610,000.00

Revenues $ 6,583,000.00

Closing Accounts

Receivables $ (775,000.00)

Cash collections from

customers $ 6,418,000.00

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

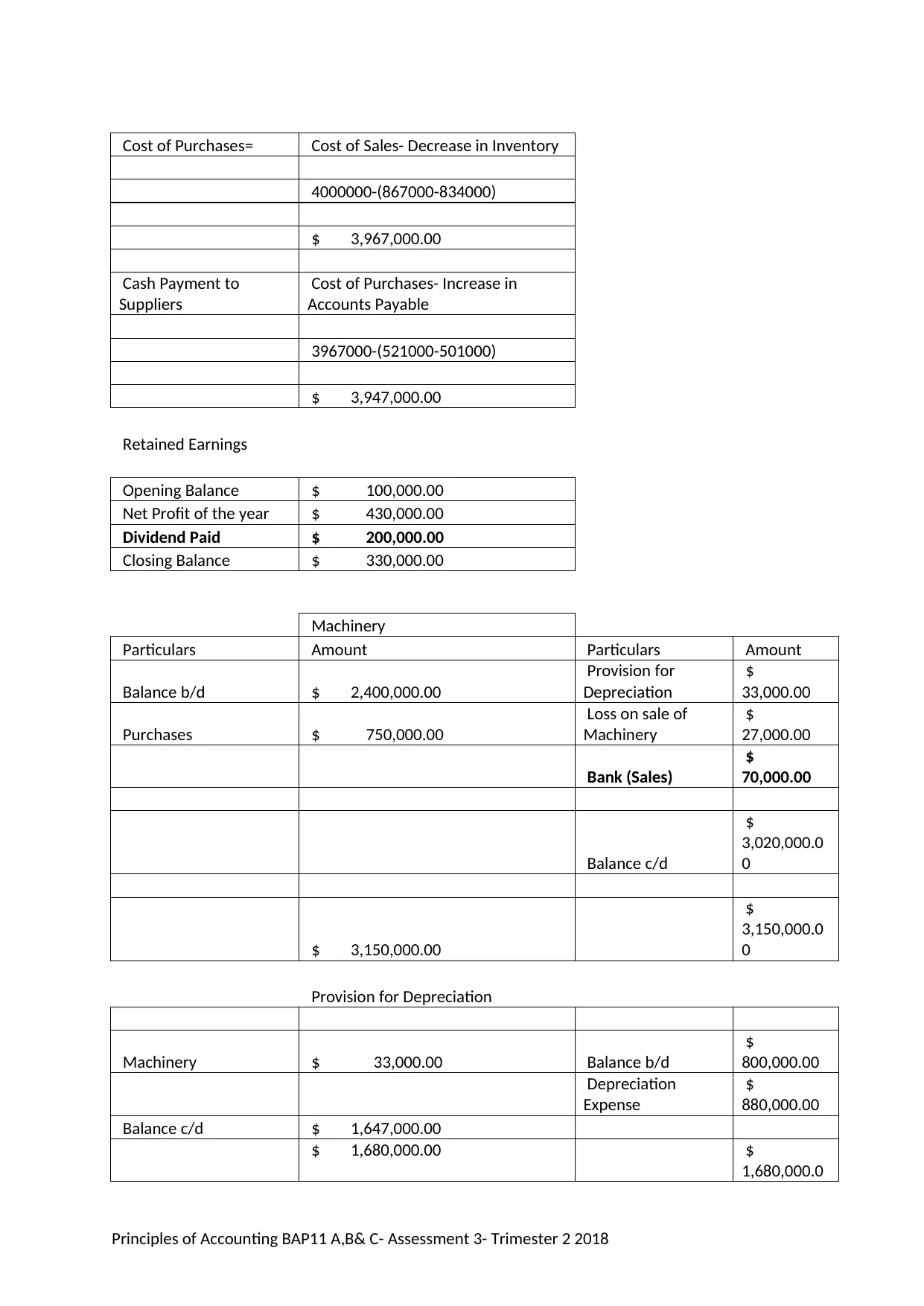

4000000-(867000-834000)

$ 3,967,000.00

Cash Payment to

Suppliers

Cost of Purchases- Increase in

Accounts Payable

3967000-(521000-501000)

$ 3,947,000.00

Retained Earnings

Opening Balance $ 100,000.00

Net Profit of the year $ 430,000.00

Dividend Paid $ 200,000.00

Closing Balance $ 330,000.00

Machinery

Particulars Amount Particulars Amount

Balance b/d $ 2,400,000.00

Provision for

Depreciation

$

33,000.00

Purchases $ 750,000.00

Loss on sale of

Machinery

$

27,000.00

Bank (Sales)

$

70,000.00

Balance c/d

$

3,020,000.0

0

$ 3,150,000.00

$

3,150,000.0

0

Provision for Depreciation

Machinery $ 33,000.00 Balance b/d

$

800,000.00

Depreciation

Expense

$

880,000.00

Balance c/d $ 1,647,000.00

$ 1,680,000.00 $

1,680,000.0

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

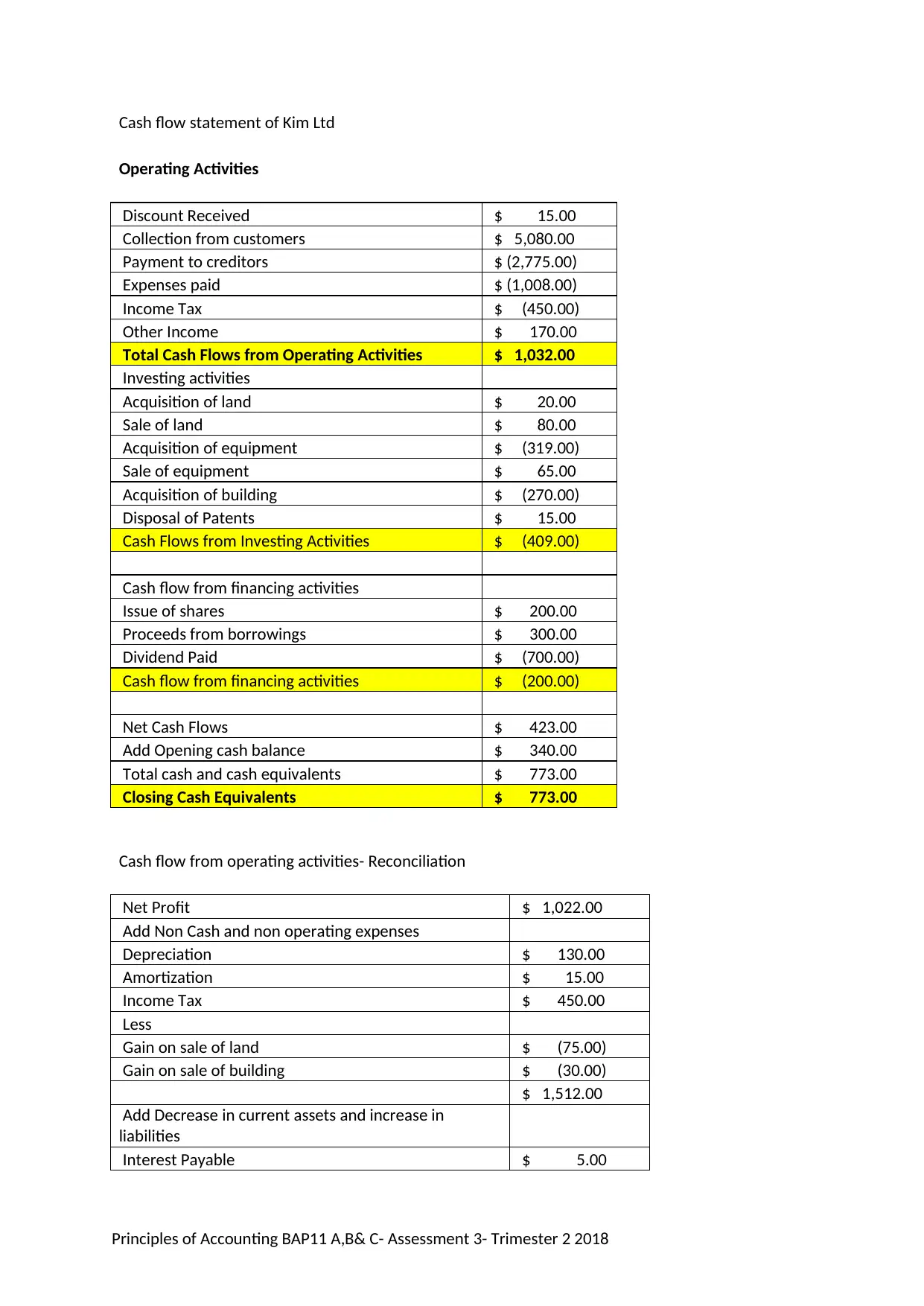

Operating Activities

Discount Received $ 15.00

Collection from customers $ 5,080.00

Payment to creditors $ (2,775.00)

Expenses paid $ (1,008.00)

Income Tax $ (450.00)

Other Income $ 170.00

Total Cash Flows from Operating Activities $ 1,032.00

Investing activities

Acquisition of land $ 20.00

Sale of land $ 80.00

Acquisition of equipment $ (319.00)

Sale of equipment $ 65.00

Acquisition of building $ (270.00)

Disposal of Patents $ 15.00

Cash Flows from Investing Activities $ (409.00)

Cash flow from financing activities

Issue of shares $ 200.00

Proceeds from borrowings $ 300.00

Dividend Paid $ (700.00)

Cash flow from financing activities $ (200.00)

Net Cash Flows $ 423.00

Add Opening cash balance $ 340.00

Total cash and cash equivalents $ 773.00

Closing Cash Equivalents $ 773.00

Cash flow from operating activities- Reconciliation

Net Profit $ 1,022.00

Add Non Cash and non operating expenses

Depreciation $ 130.00

Amortization $ 15.00

Income Tax $ 450.00

Less

Gain on sale of land $ (75.00)

Gain on sale of building $ (30.00)

$ 1,512.00

Add Decrease in current assets and increase in

liabilities

Interest Payable $ 5.00

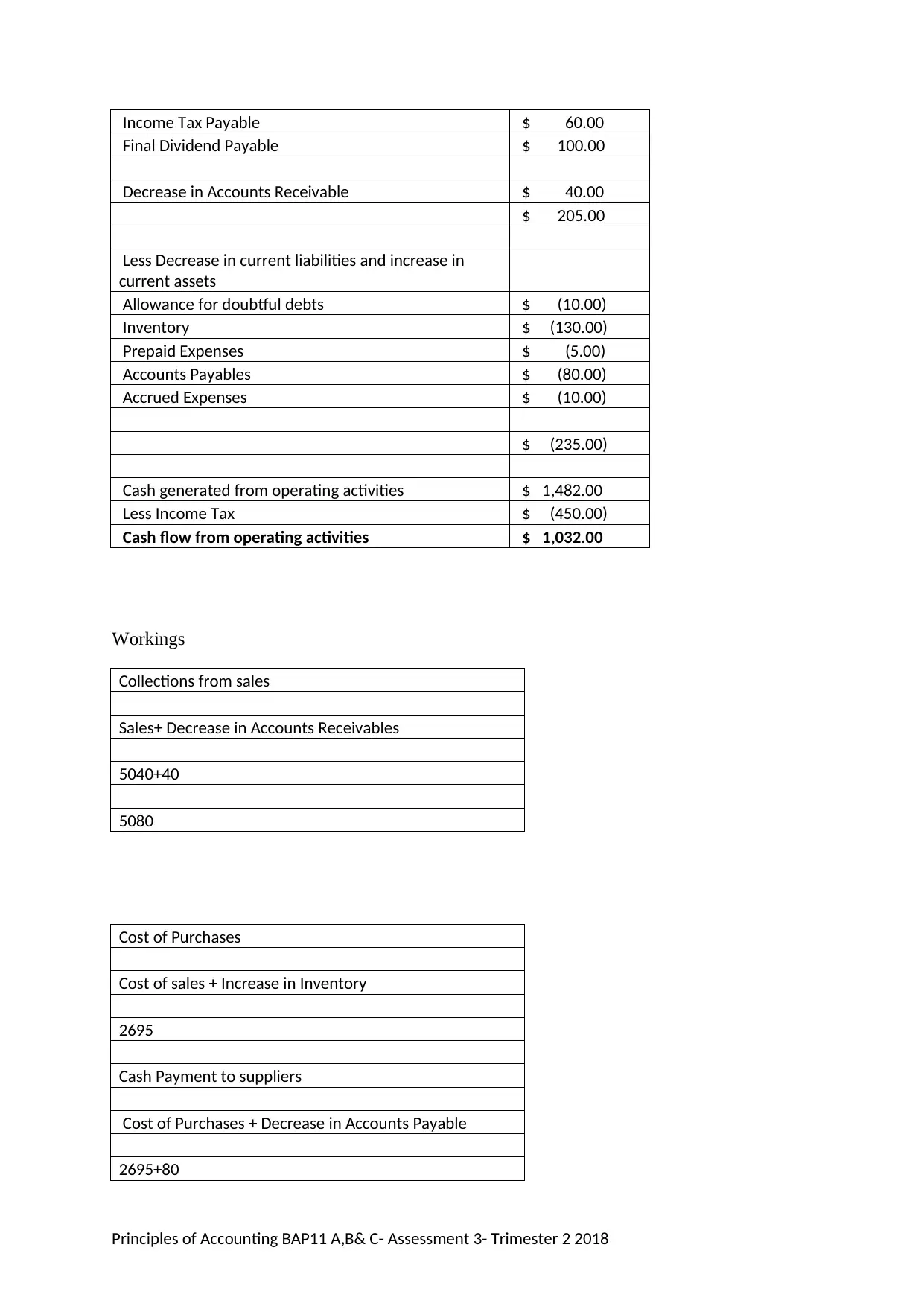

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

Final Dividend Payable $ 100.00

Decrease in Accounts Receivable $ 40.00

$ 205.00

Less Decrease in current liabilities and increase in

current assets

Allowance for doubtful debts $ (10.00)

Inventory $ (130.00)

Prepaid Expenses $ (5.00)

Accounts Payables $ (80.00)

Accrued Expenses $ (10.00)

$ (235.00)

Cash generated from operating activities $ 1,482.00

Less Income Tax $ (450.00)

Cash flow from operating activities $ 1,032.00

Workings

Collections from sales

Sales+ Decrease in Accounts Receivables

5040+40

5080

Cost of Purchases

Cost of sales + Increase in Inventory

2695

Cash Payment to suppliers

Cost of Purchases + Decrease in Accounts Payable

2695+80

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

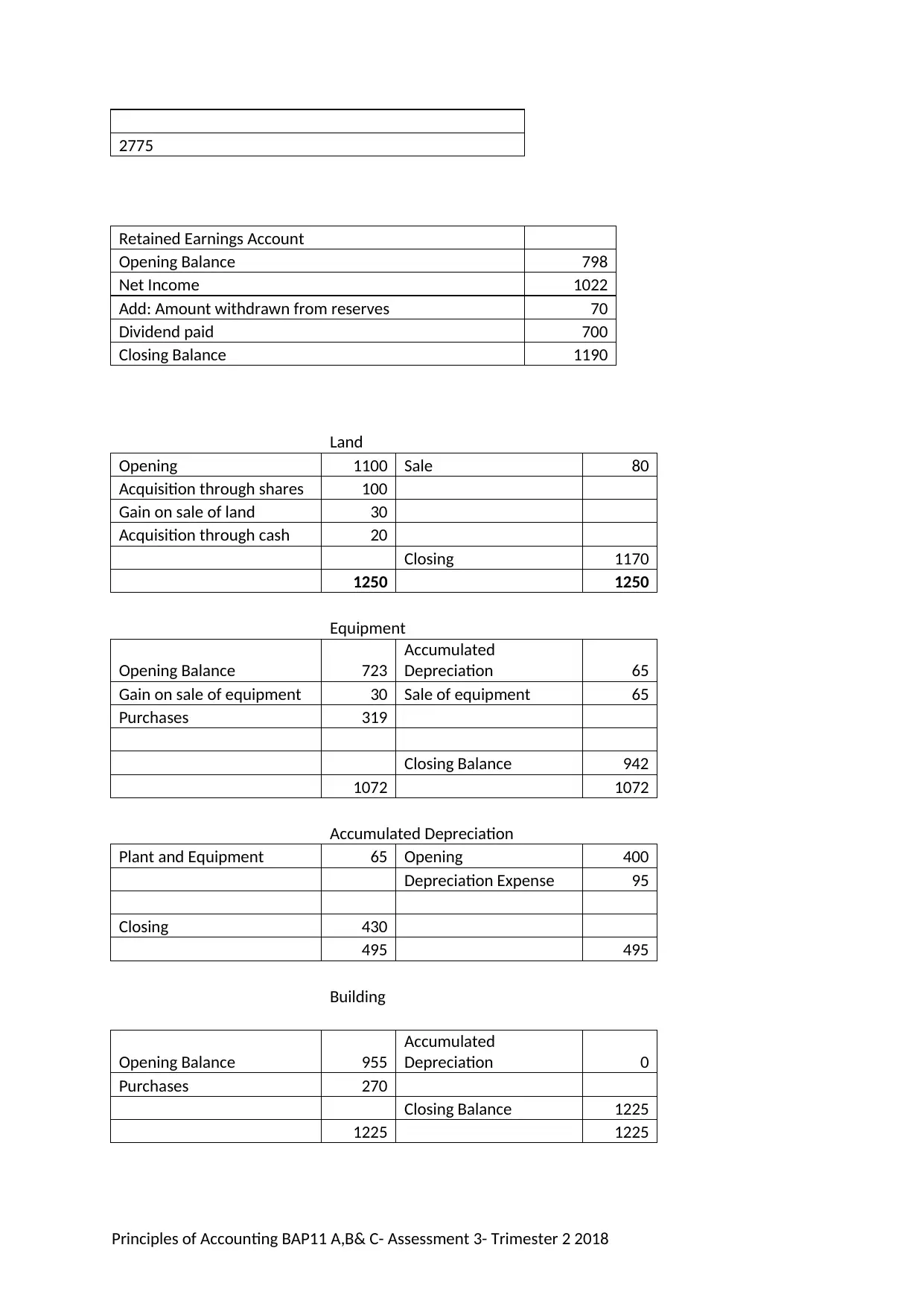

Retained Earnings Account

Opening Balance 798

Net Income 1022

Add: Amount withdrawn from reserves 70

Dividend paid 700

Closing Balance 1190

Land

Opening 1100 Sale 80

Acquisition through shares 100

Gain on sale of land 30

Acquisition through cash 20

Closing 1170

1250 1250

Equipment

Opening Balance 723

Accumulated

Depreciation 65

Gain on sale of equipment 30 Sale of equipment 65

Purchases 319

Closing Balance 942

1072 1072

Accumulated Depreciation

Plant and Equipment 65 Opening 400

Depreciation Expense 95

Closing 430

495 495

Building

Opening Balance 955

Accumulated

Depreciation 0

Purchases 270

Closing Balance 1225

1225 1225

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

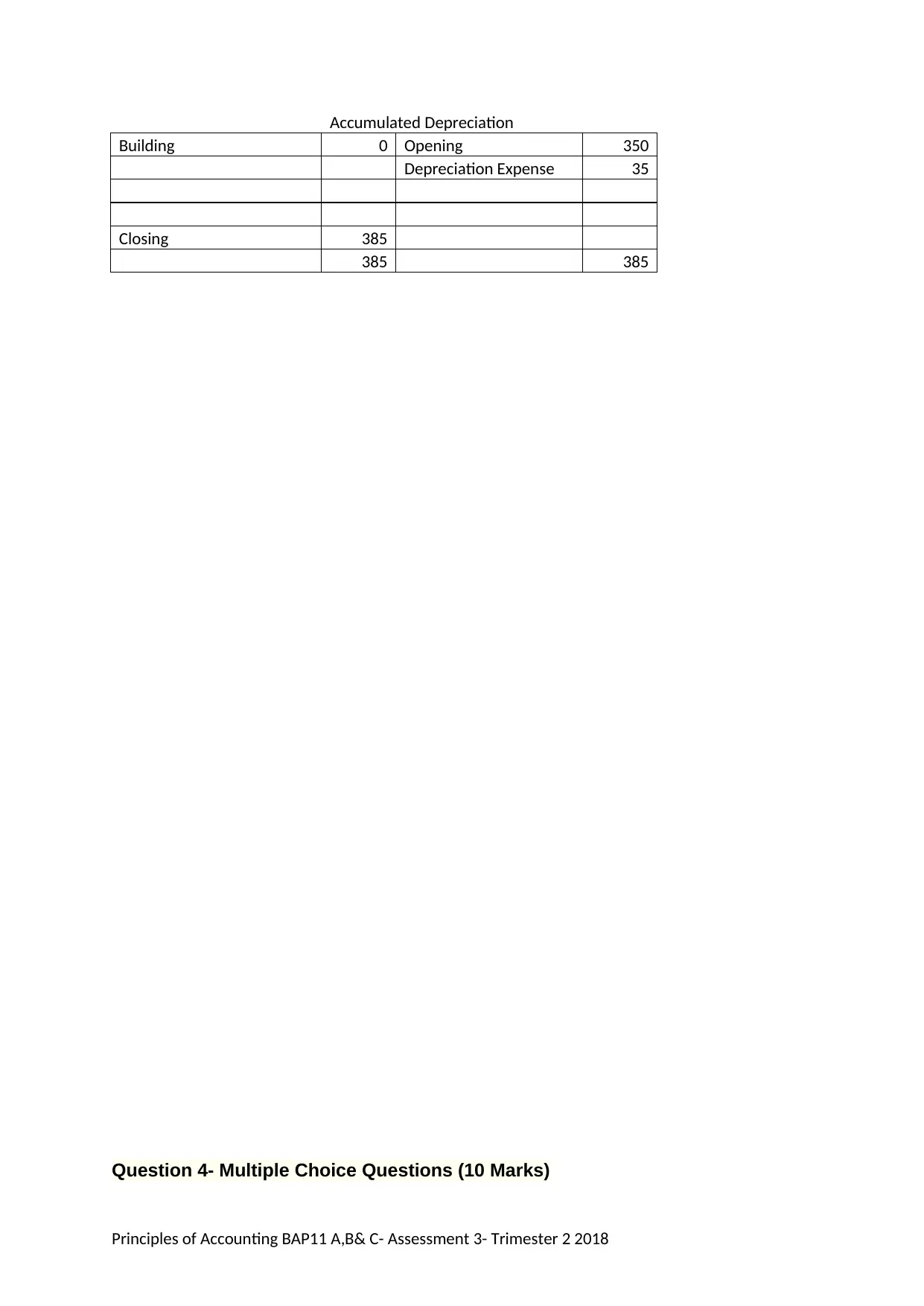

Building 0 Opening 350

Depreciation Expense 35

Closing 385

385 385

Question 4- Multiple Choice Questions (10 Marks)

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

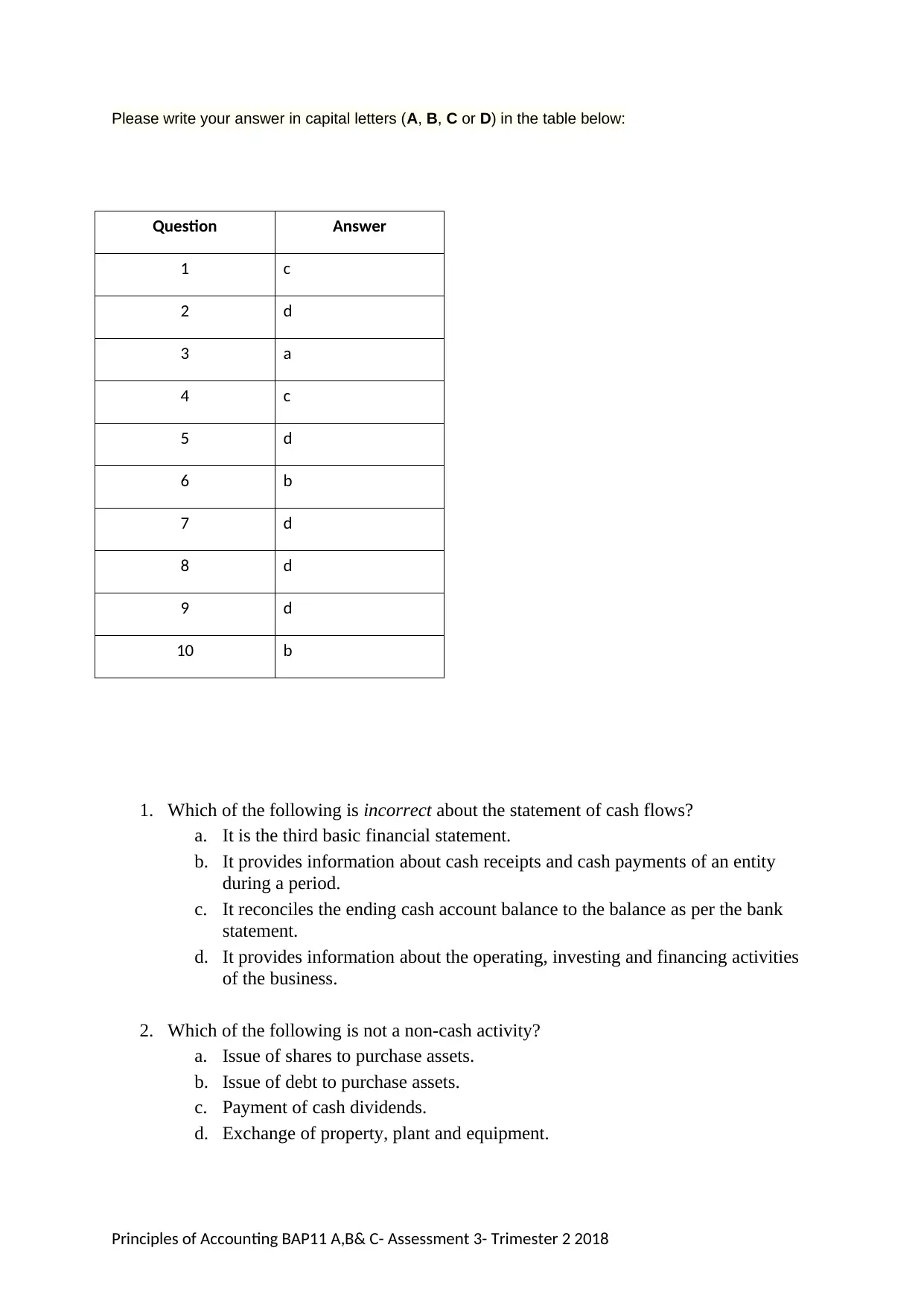

Question Answer

1 c

2 d

3 a

4 c

5 d

6 b

7 d

8 d

9 d

10 b

1. Which of the following is incorrect about the statement of cash flows?

a. It is the third basic financial statement.

b. It provides information about cash receipts and cash payments of an entity

during a period.

c. It reconciles the ending cash account balance to the balance as per the bank

statement.

d. It provides information about the operating, investing and financing activities

of the business.

2. Which of the following is not a non-cash activity?

a. Issue of shares to purchase assets.

b. Issue of debt to purchase assets.

c. Payment of cash dividends.

d. Exchange of property, plant and equipment.

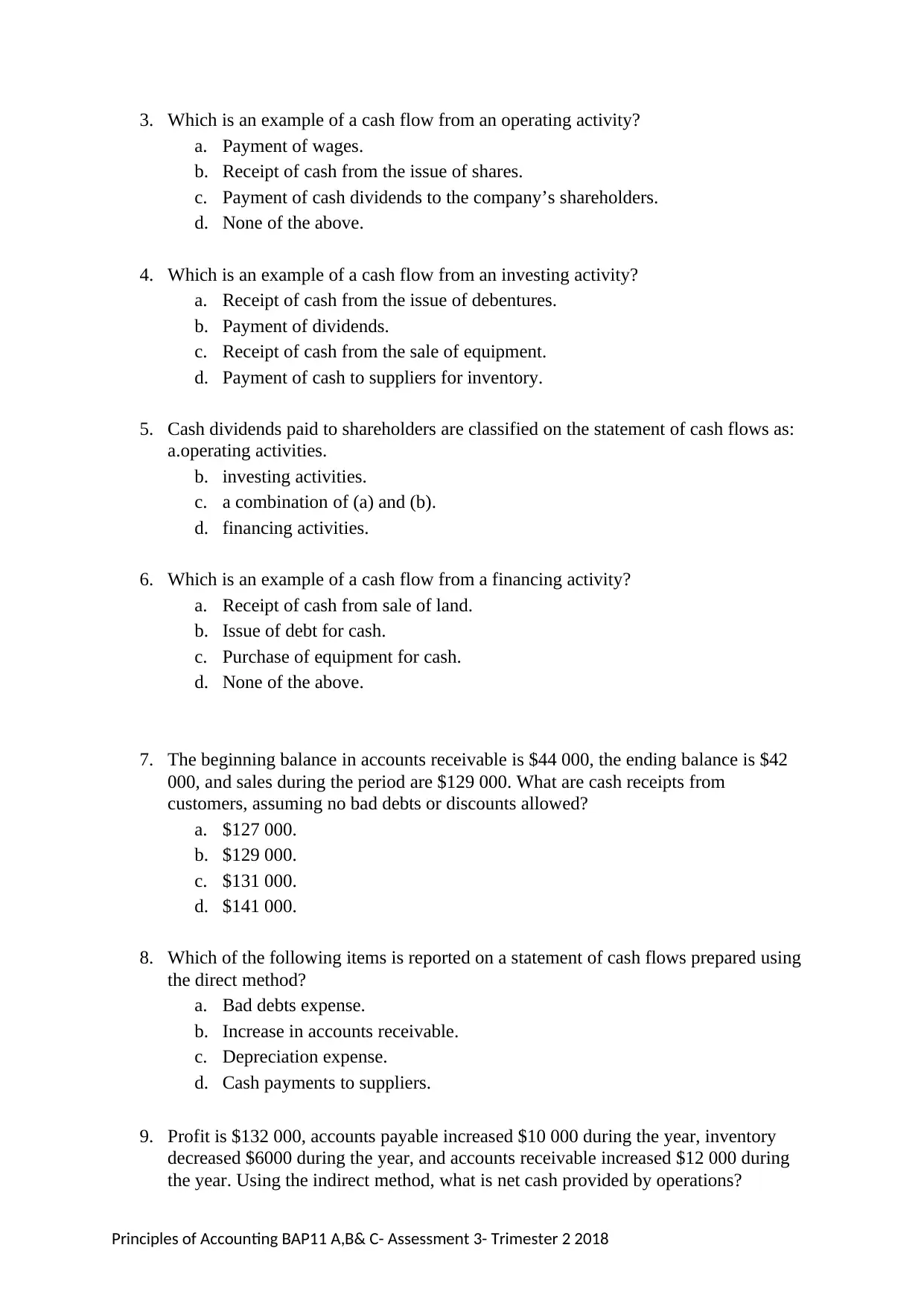

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

a. Payment of wages.

b. Receipt of cash from the issue of shares.

c. Payment of cash dividends to the company’s shareholders.

d. None of the above.

4. Which is an example of a cash flow from an investing activity?

a. Receipt of cash from the issue of debentures.

b. Payment of dividends.

c. Receipt of cash from the sale of equipment.

d. Payment of cash to suppliers for inventory.

5. Cash dividends paid to shareholders are classified on the statement of cash flows as:

a.operating activities.

b. investing activities.

c. a combination of (a) and (b).

d. financing activities.

6. Which is an example of a cash flow from a financing activity?

a. Receipt of cash from sale of land.

b. Issue of debt for cash.

c. Purchase of equipment for cash.

d. None of the above.

7. The beginning balance in accounts receivable is $44 000, the ending balance is $42

000, and sales during the period are $129 000. What are cash receipts from

customers, assuming no bad debts or discounts allowed?

a. $127 000.

b. $129 000.

c. $131 000.

d. $141 000.

8. Which of the following items is reported on a statement of cash flows prepared using

the direct method?

a. Bad debts expense.

b. Increase in accounts receivable.

c. Depreciation expense.

d. Cash payments to suppliers.

9. Profit is $132 000, accounts payable increased $10 000 during the year, inventory

decreased $6000 during the year, and accounts receivable increased $12 000 during

the year. Using the indirect method, what is net cash provided by operations?

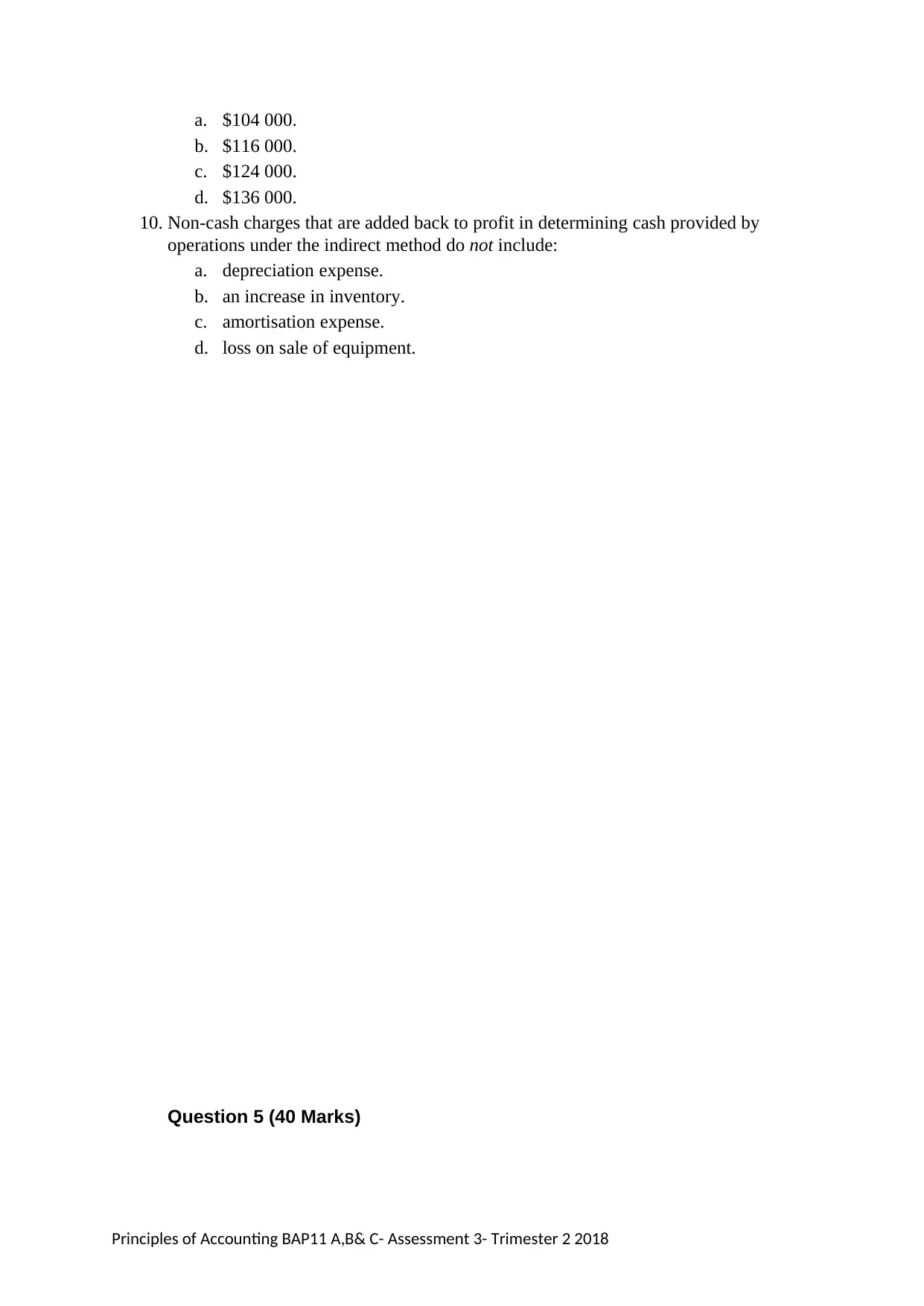

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b. $116 000.

c. $124 000.

d. $136 000.

10. Non-cash charges that are added back to profit in determining cash provided by

operations under the indirect method do not include:

a. depreciation expense.

b. an increase in inventory.

c. amortisation expense.

d. loss on sale of equipment.

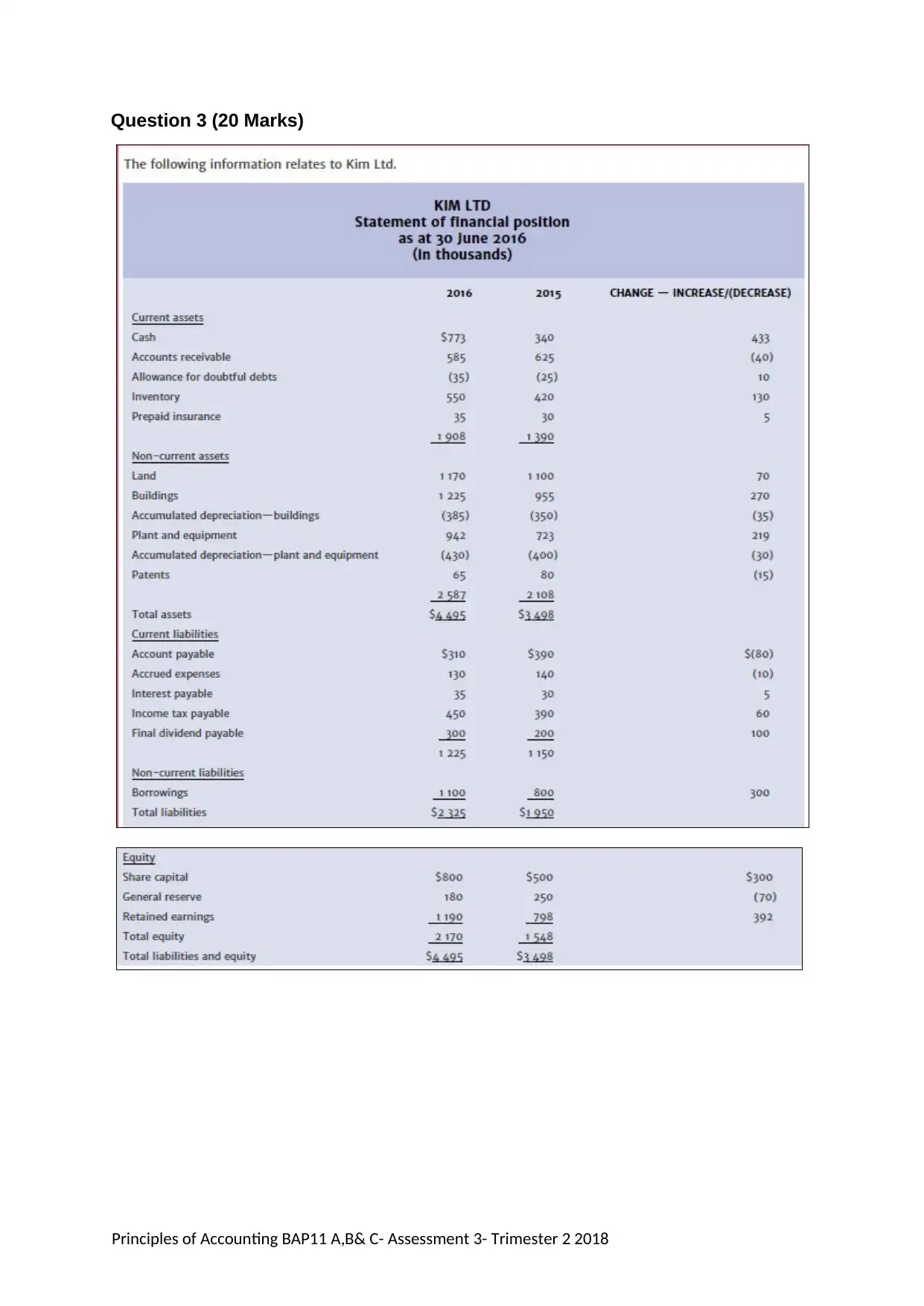

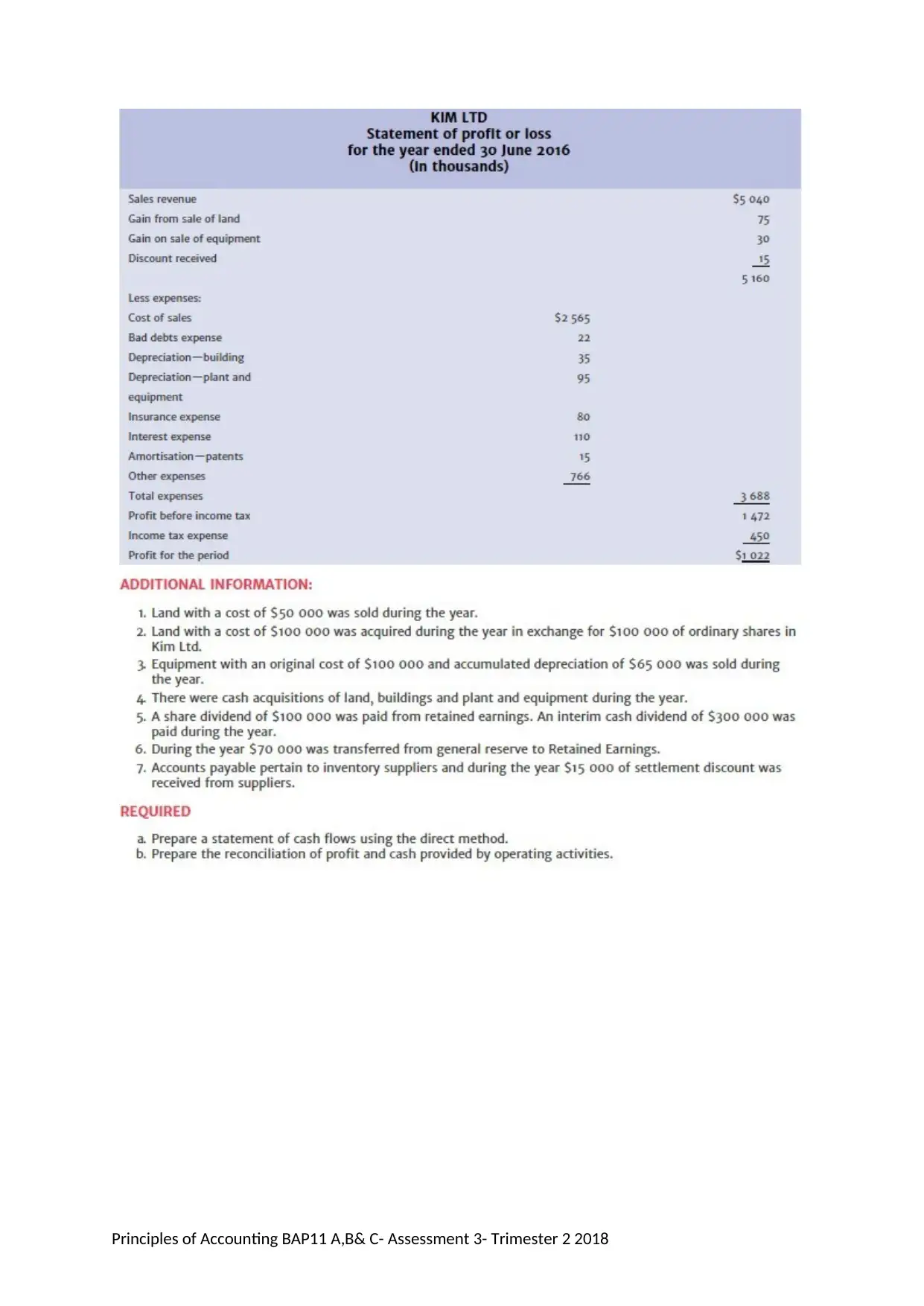

Question 5 (40 Marks)

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

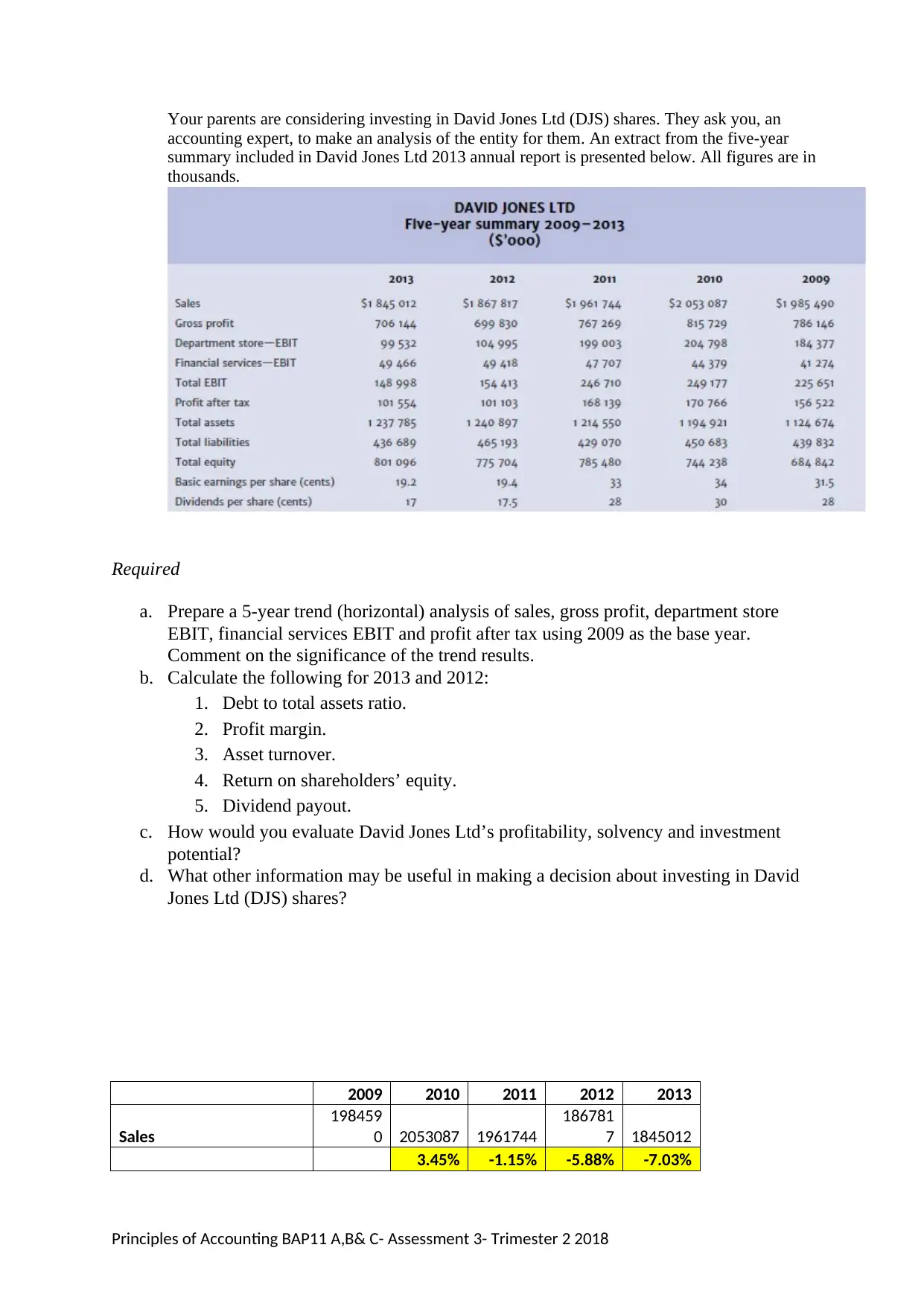

Paraphrase This Document

accounting expert, to make an analysis of the entity for them. An extract from the five-year

summary included in David Jones Ltd 2013 annual report is presented below. All figures are in

thousands.

Required

a. Prepare a 5-year trend (horizontal) analysis of sales, gross profit, department store

EBIT, financial services EBIT and profit after tax using 2009 as the base year.

Comment on the significance of the trend results.

b. Calculate the following for 2013 and 2012:

1. Debt to total assets ratio.

2. Profit margin.

3. Asset turnover.

4. Return on shareholders’ equity.

5. Dividend payout.

c. How would you evaluate David Jones Ltd’s profitability, solvency and investment

potential?

d. What other information may be useful in making a decision about investing in David

Jones Ltd (DJS) shares?

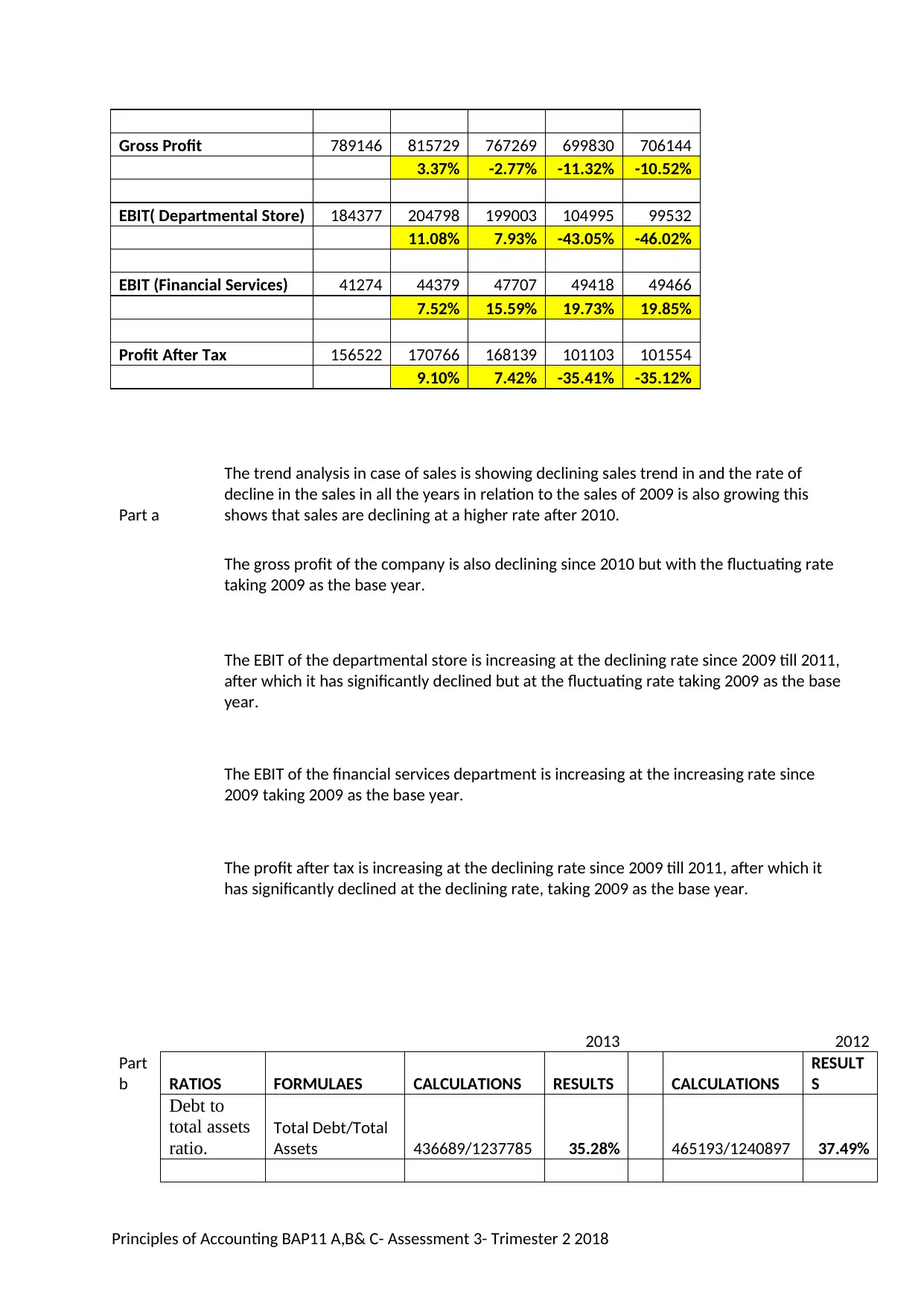

2009 2010 2011 2012 2013

Sales

198459

0 2053087 1961744

186781

7 1845012

3.45% -1.15% -5.88% -7.03%

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

3.37% -2.77% -11.32% -10.52%

EBIT( Departmental Store) 184377 204798 199003 104995 99532

11.08% 7.93% -43.05% -46.02%

EBIT (Financial Services) 41274 44379 47707 49418 49466

7.52% 15.59% 19.73% 19.85%

Profit After Tax 156522 170766 168139 101103 101554

9.10% 7.42% -35.41% -35.12%

Part a

The trend analysis in case of sales is showing declining sales trend in and the rate of

decline in the sales in all the years in relation to the sales of 2009 is also growing this

shows that sales are declining at a higher rate after 2010.

The gross profit of the company is also declining since 2010 but with the fluctuating rate

taking 2009 as the base year.

The EBIT of the departmental store is increasing at the declining rate since 2009 till 2011,

after which it has significantly declined but at the fluctuating rate taking 2009 as the base

year.

The EBIT of the financial services department is increasing at the increasing rate since

2009 taking 2009 as the base year.

The profit after tax is increasing at the declining rate since 2009 till 2011, after which it

has significantly declined at the declining rate, taking 2009 as the base year.

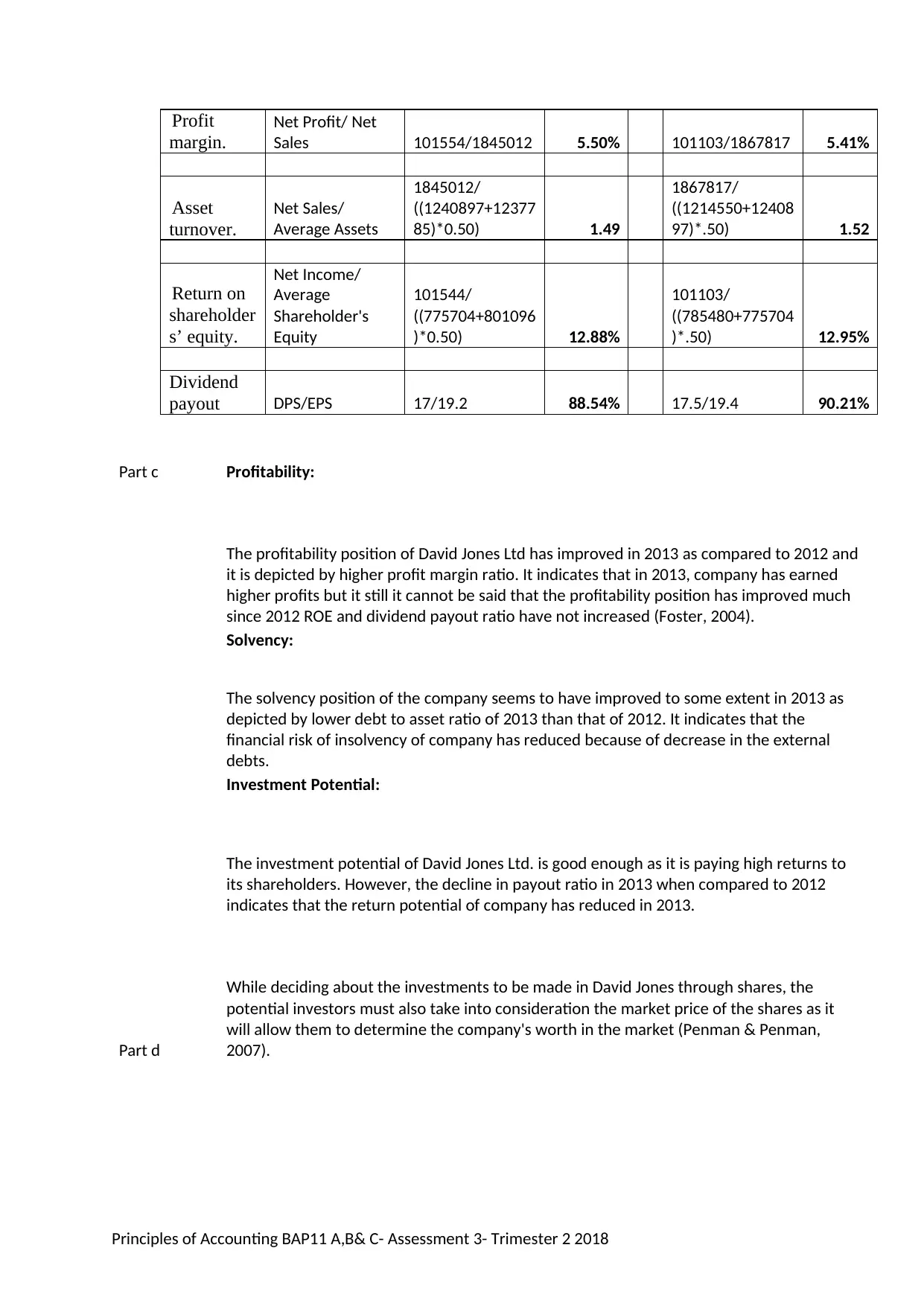

2013 2012

Part

b RATIOS FORMULAES CALCULATIONS RESULTS CALCULATIONS

RESULT

S

Debt to

total assets

ratio.

Total Debt/Total

Assets 436689/1237785 35.28% 465193/1240897 37.49%

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

margin.

Net Profit/ Net

Sales 101554/1845012 5.50% 101103/1867817 5.41%

Asset

turnover.

Net Sales/

Average Assets

1845012/

((1240897+12377

85)*0.50) 1.49

1867817/

((1214550+12408

97)*.50) 1.52

Return on

shareholder

s’ equity.

Net Income/

Average

Shareholder's

Equity

101544/

((775704+801096

)*0.50) 12.88%

101103/

((785480+775704

)*.50) 12.95%

Dividend

payout DPS/EPS 17/19.2 88.54% 17.5/19.4 90.21%

Part c Profitability:

The profitability position of David Jones Ltd has improved in 2013 as compared to 2012 and

it is depicted by higher profit margin ratio. It indicates that in 2013, company has earned

higher profits but it still it cannot be said that the profitability position has improved much

since 2012 ROE and dividend payout ratio have not increased (Foster, 2004).

Solvency:

The solvency position of the company seems to have improved to some extent in 2013 as

depicted by lower debt to asset ratio of 2013 than that of 2012. It indicates that the

financial risk of insolvency of company has reduced because of decrease in the external

debts.

Investment Potential:

The investment potential of David Jones Ltd. is good enough as it is paying high returns to

its shareholders. However, the decline in payout ratio in 2013 when compared to 2012

indicates that the return potential of company has reduced in 2013.

Part d

While deciding about the investments to be made in David Jones through shares, the

potential investors must also take into consideration the market price of the shares as it

will allow them to determine the company's worth in the market (Penman & Penman,

2007).

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Paraphrase This Document

Brahmasrene, T., Strupeck, C.D. and Whitten, D., 2004. Examining preferences in cash flow

statement format. CPA Journal, 74(10), pp.58-60.

Foster, G., 2004. Financial Statement Analysis, 2/e. Pearson Education India. Foster, G.,

2004. Financial Statement Analysis, 2/e. Pearson Education India.

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

valuation (p. 476). New York: McGraw-Hill.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Principles of Accounting BAP11 A,B& C- Assessment 3- Trimester 2 2018

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.