Finance and Statistics: Comparative Analysis of IBM and Boeing Stocks

VerifiedAdded on 2020/05/11

|13

|1706

|214

Homework Assignment

AI Summary

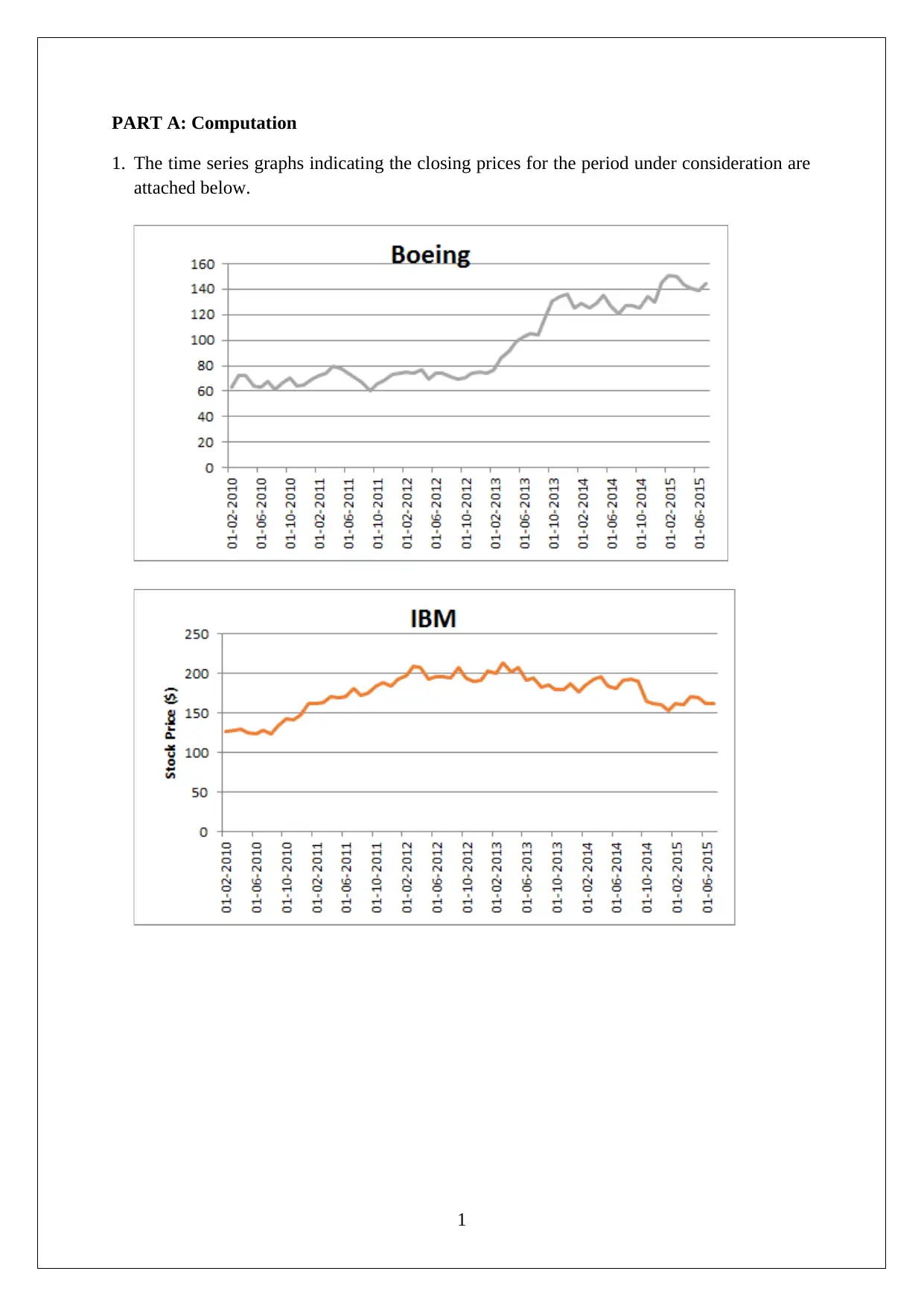

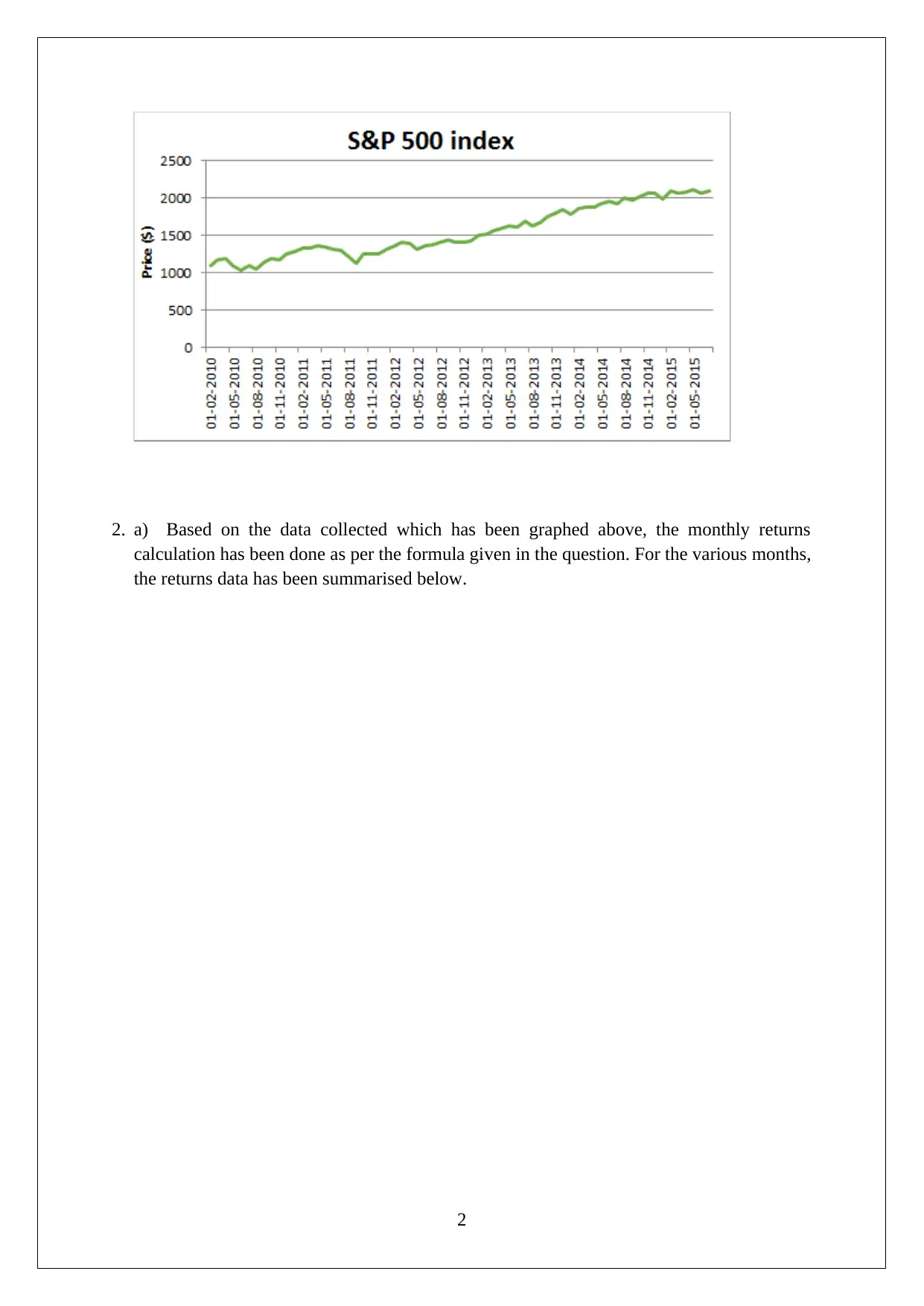

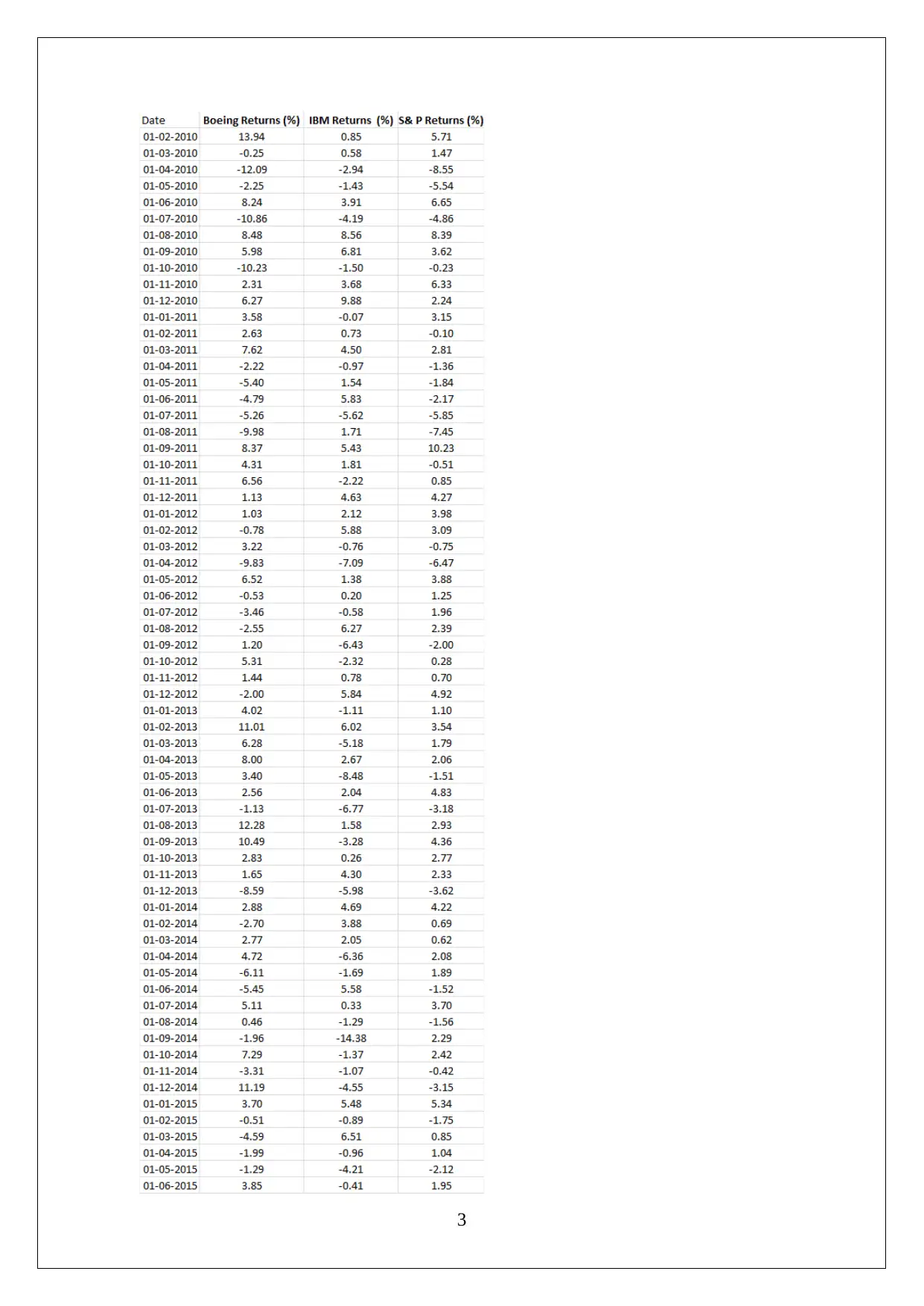

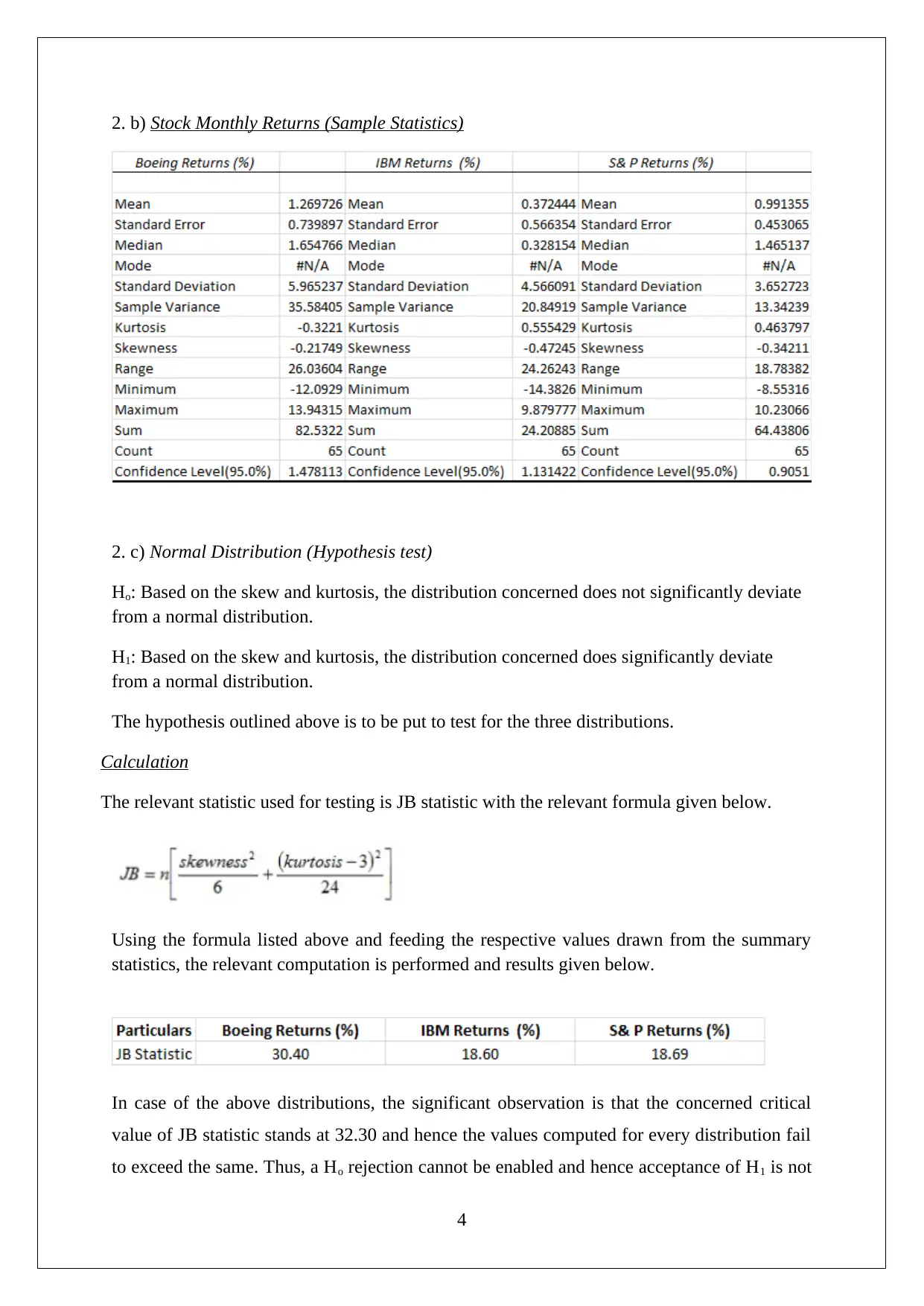

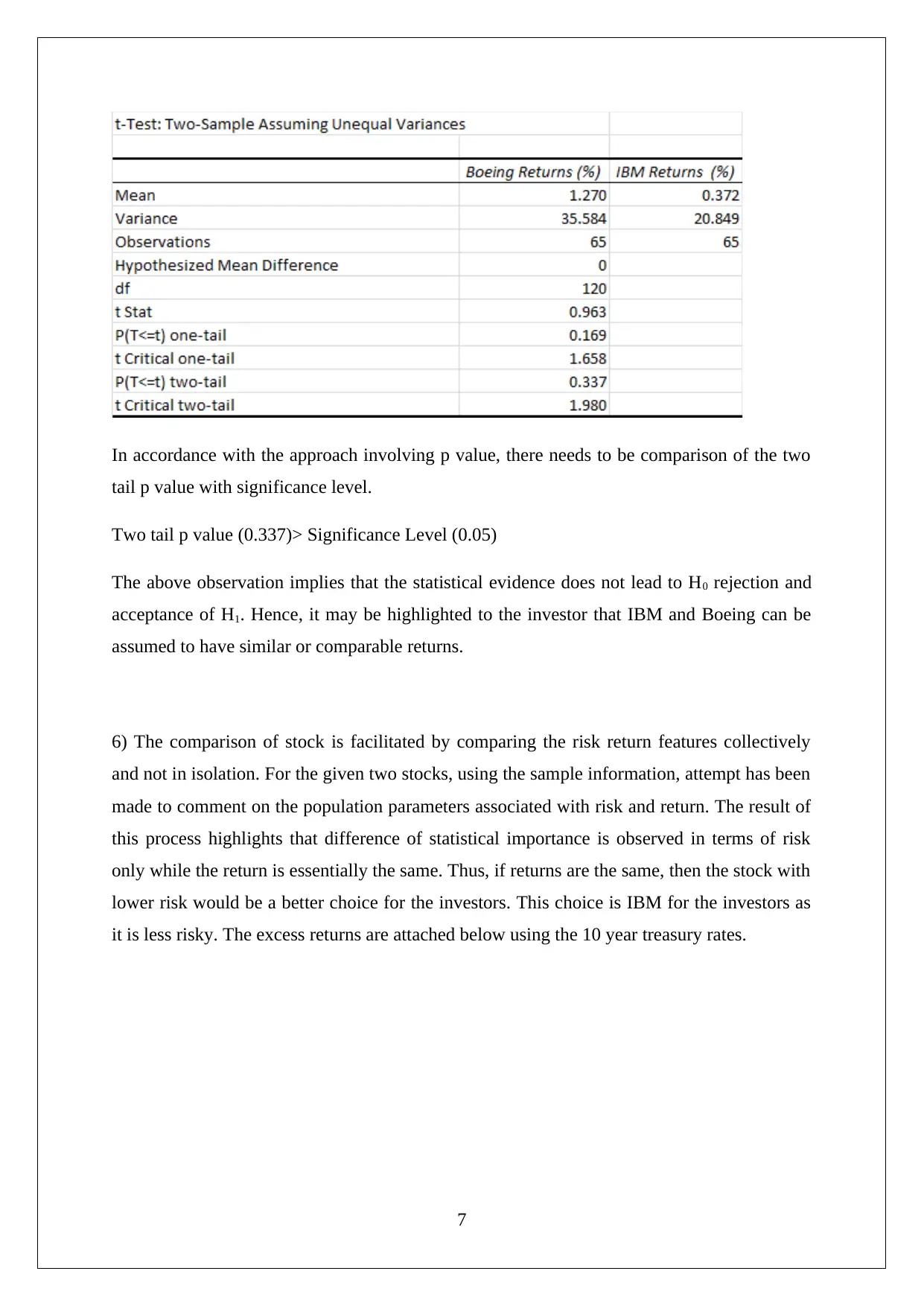

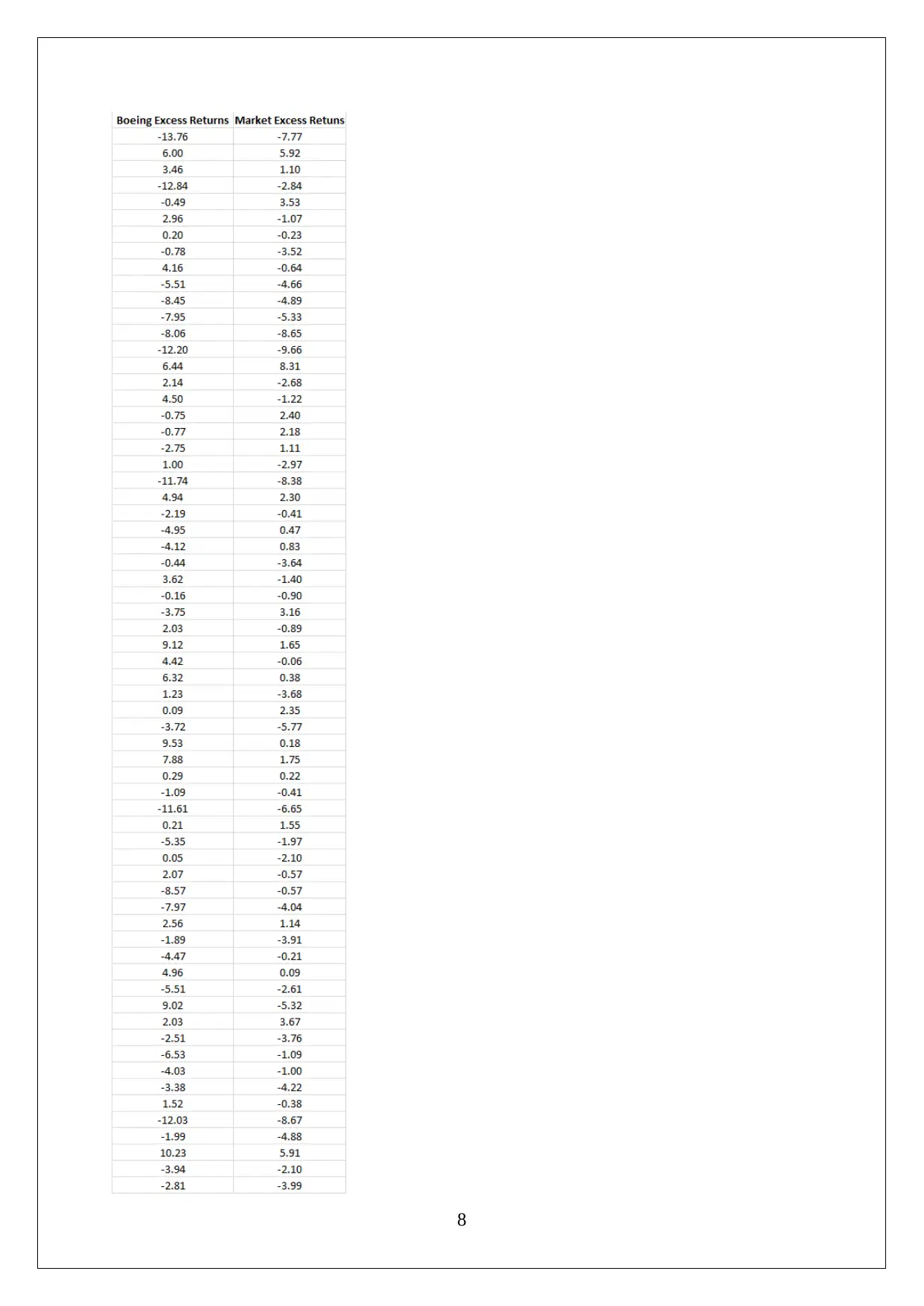

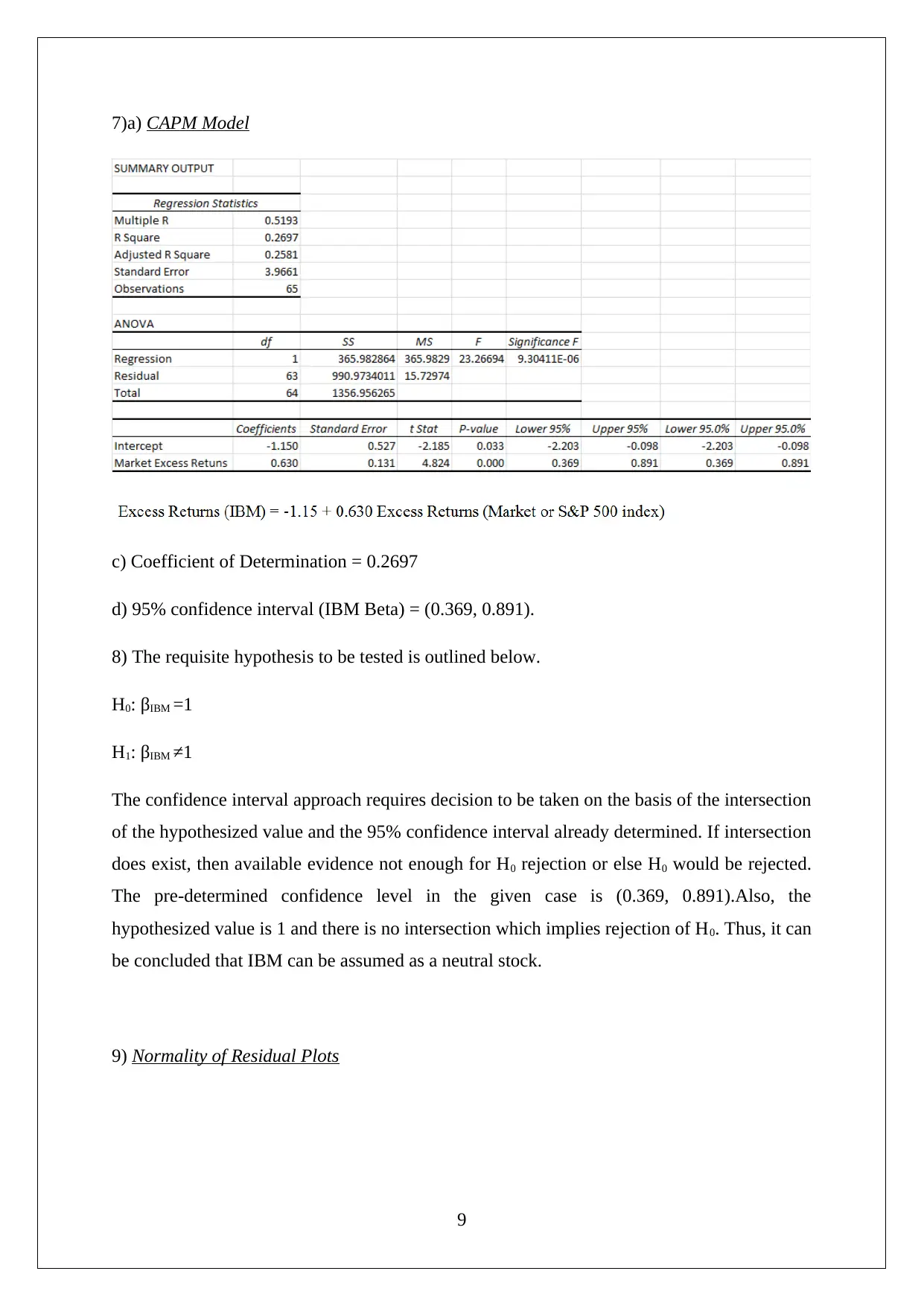

This homework assignment presents a comprehensive statistical analysis of IBM and Boeing stocks, encompassing various aspects of financial analysis. The student calculates monthly returns, performs hypothesis tests to assess the normality of return distributions, and compares the risks and returns of the two stocks using sample statistics. The assignment also includes the application of the CAPM model, calculation of the coefficient of determination, and construction of a 95% confidence interval for the beta of IBM stock. Furthermore, the student interprets stock price trends, evaluates the importance of normality testing, and provides insights into the relationship between IBM stock and the S&P 500 index. The analysis involves the use of T-tests, F-tests, and the interpretation of residual plots to validate the assumptions of the regression model. The conclusion highlights that while both stocks offer similar returns, IBM is the less risky option for investors.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.