Consolidation Accounting Solutions

VerifiedAdded on 2020/02/18

|9

|1422

|53

Practical Assignment

AI Summary

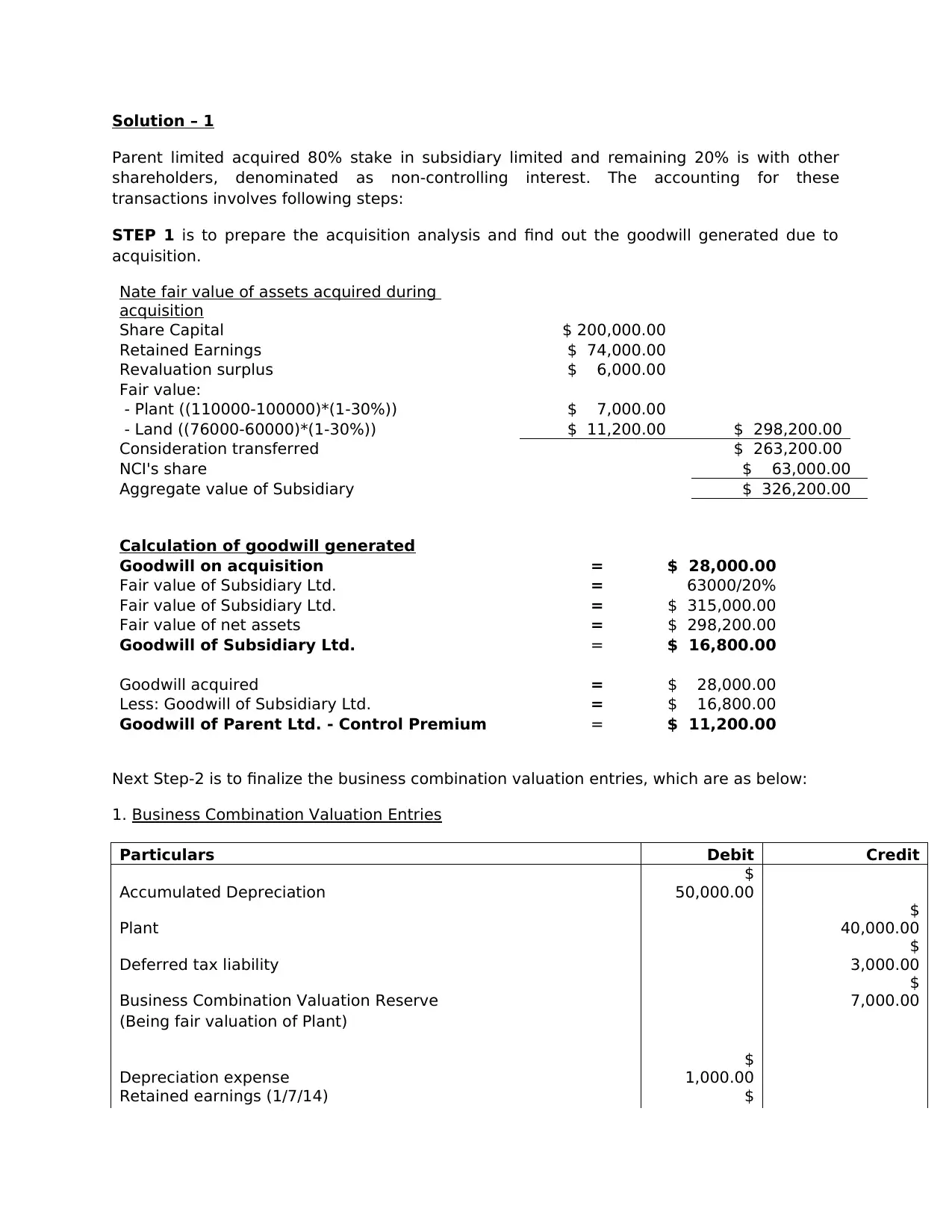

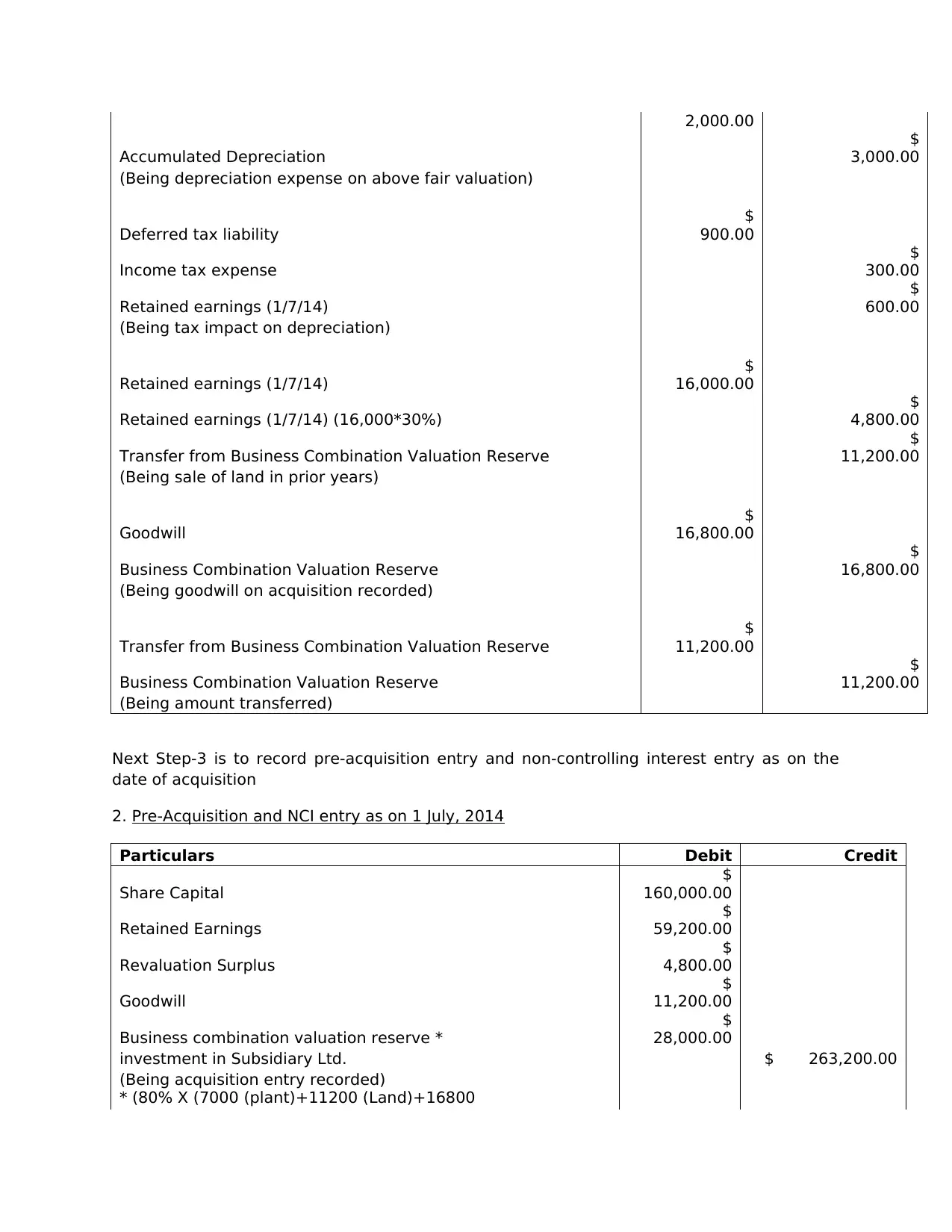

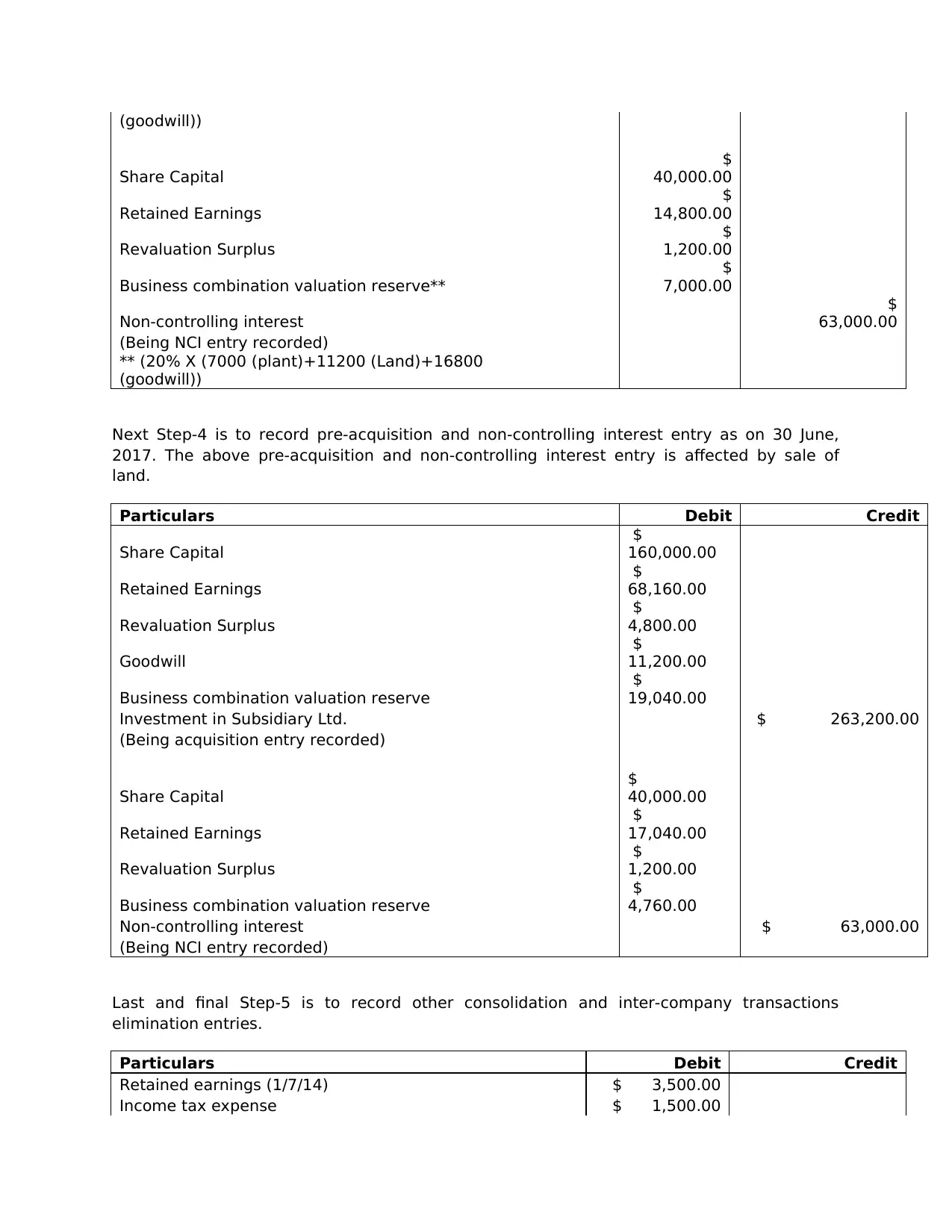

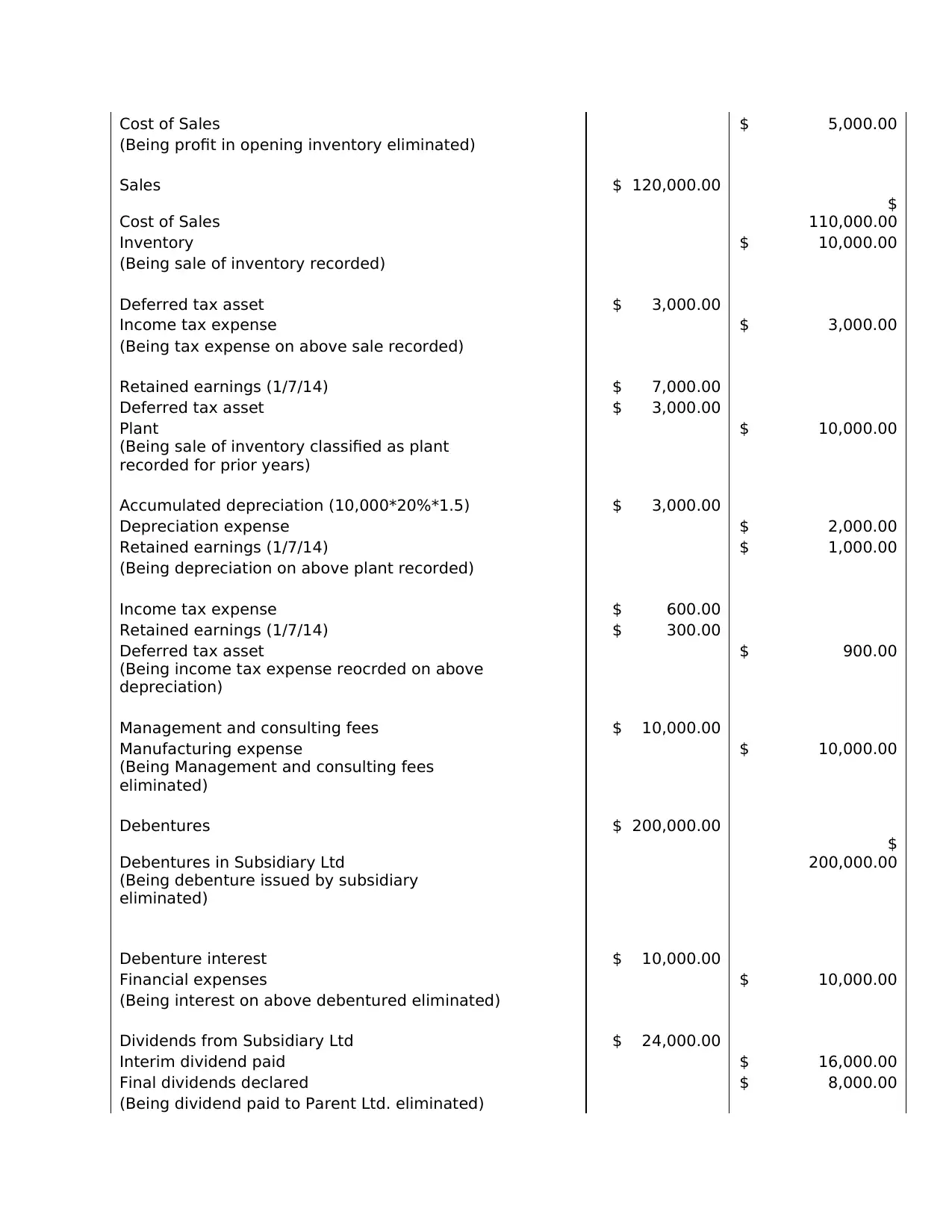

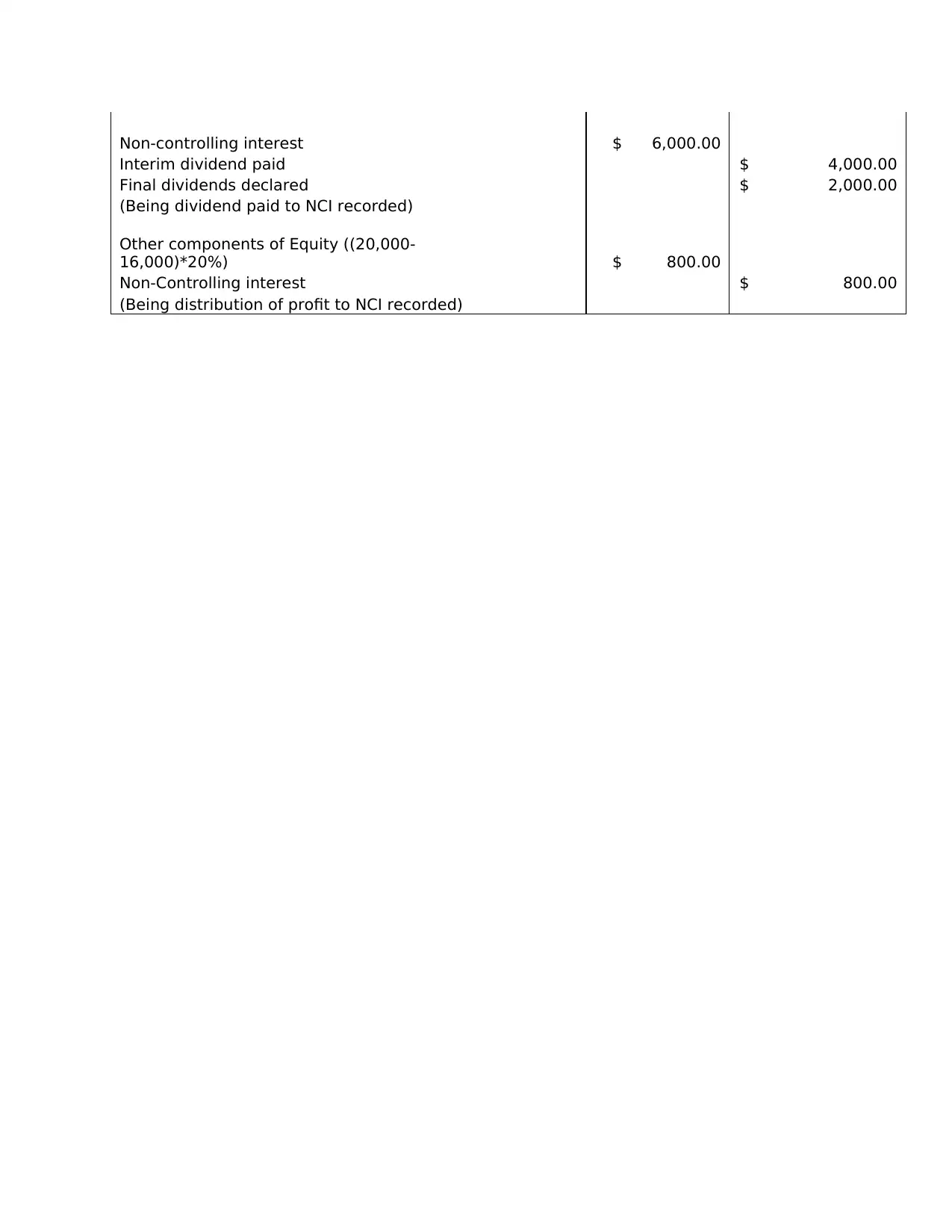

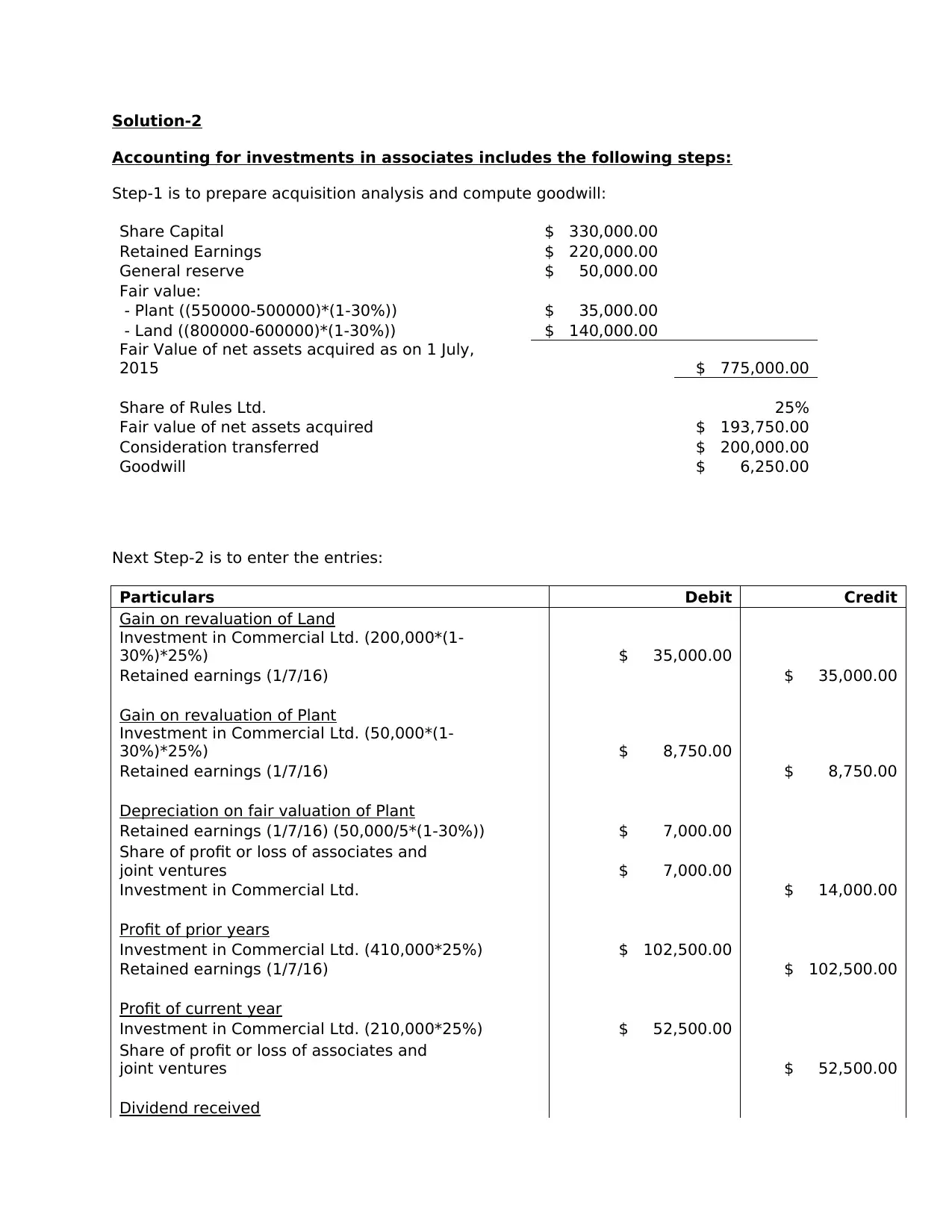

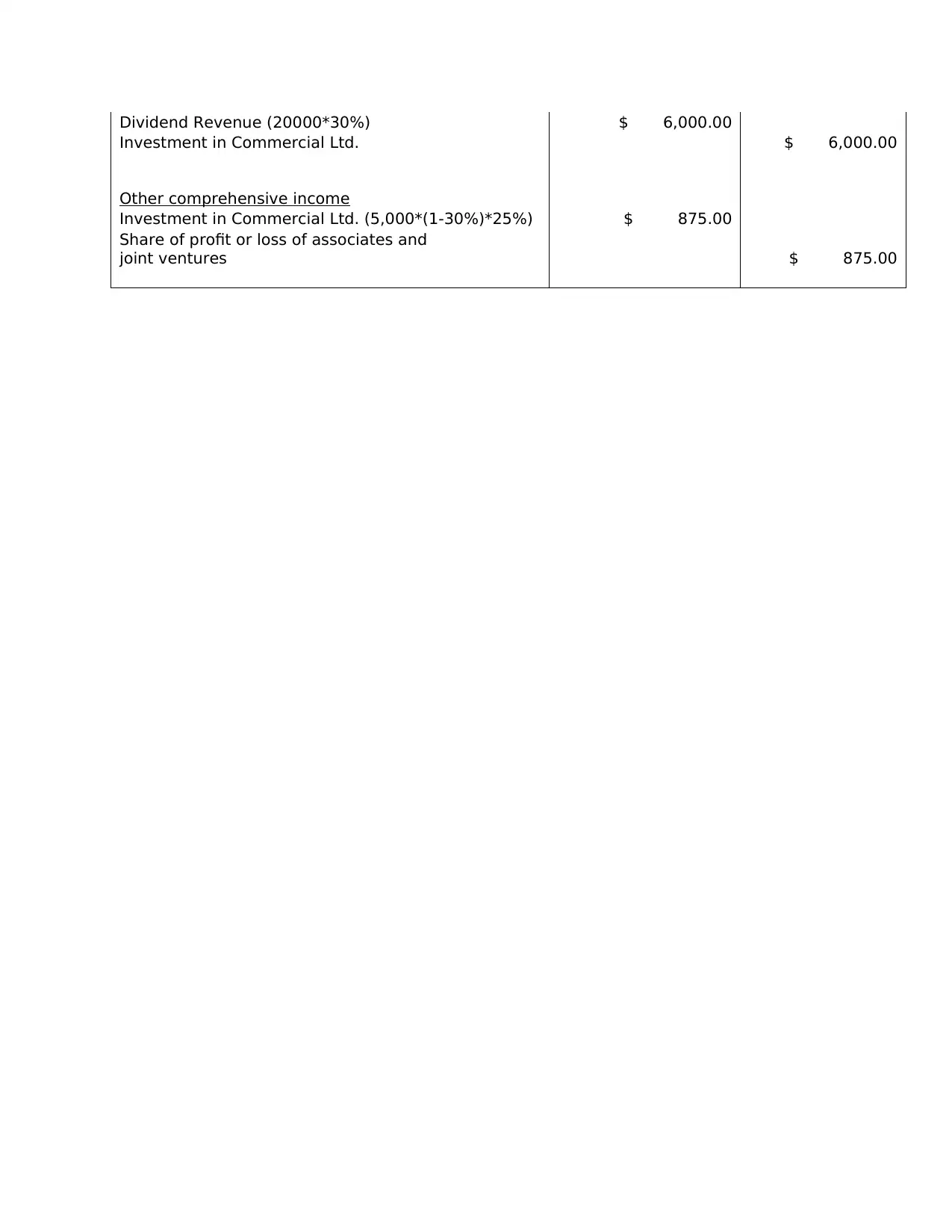

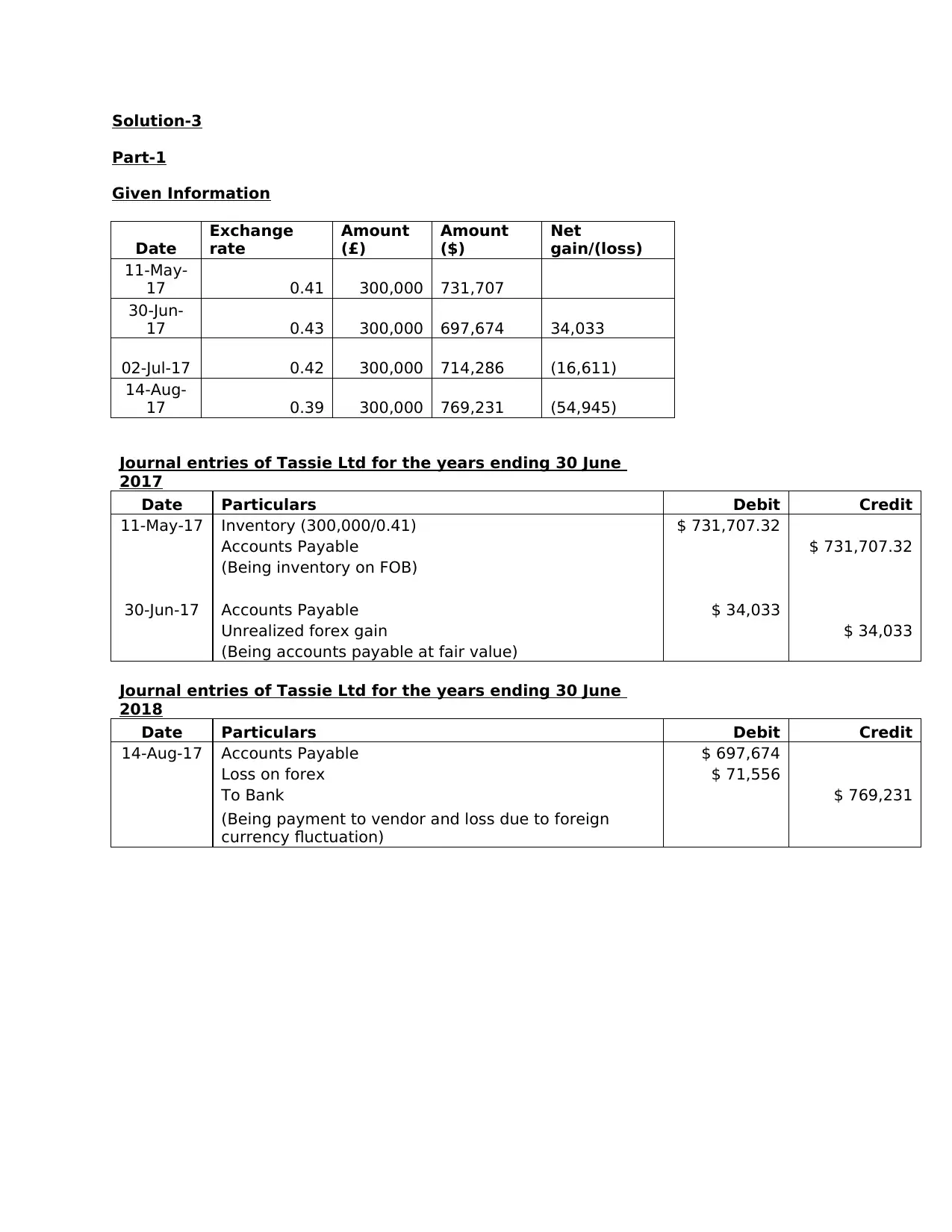

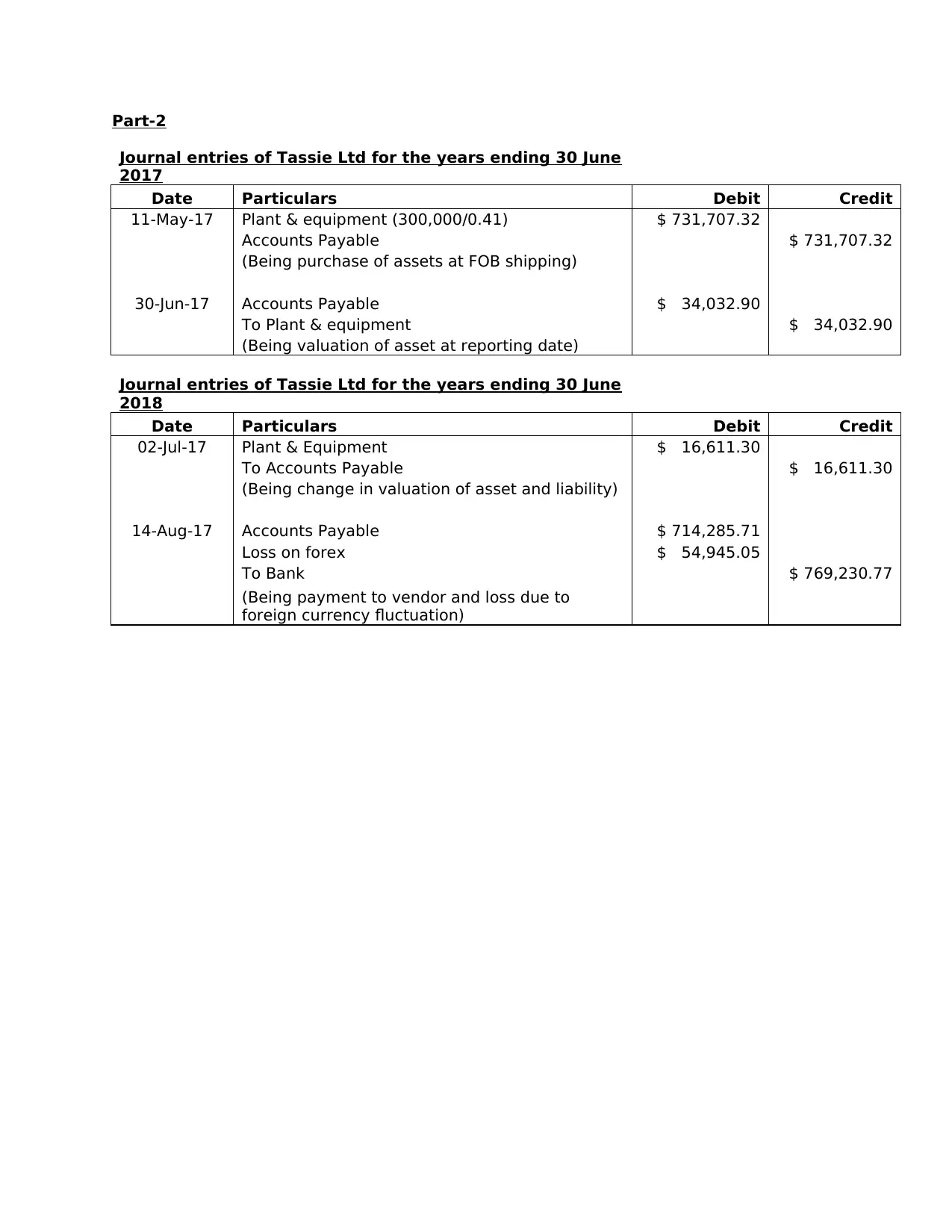

This document presents solutions to three different consolidation accounting problems. Solution 1 details the steps involved in accounting for an 80% stake acquisition in a subsidiary, including acquisition analysis, goodwill calculation, business combination valuation entries, pre-acquisition and non-controlling interest entries, and inter-company transaction eliminations. Solution 2 focuses on accounting for investments in associates, covering acquisition analysis, goodwill computation, and journal entries related to revaluation gains, depreciation, profit sharing, and dividend receipts. Solution 3 addresses foreign exchange transactions, demonstrating journal entries for inventory and plant & equipment purchases, and accounting for unrealized forex gains and losses. The solutions provide detailed journal entries and explanations for each step, making them a valuable resource for students learning about consolidation accounting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.