Risk Adjusted Cost of Capital: How organizations can lower the WACC

VerifiedAdded on 2021/02/18

|13

|3820

|391

AI Summary

The market value of equity and debt has been calculated as : WACC = (E/V * Re) + ((D/V * Rd)) In the above formula, E represents market value of the organisation's equity which can be also known as market cap, D represents market value of organisation's debt, V represents total value of capital i.e. equity plus debt, E/V % of capital that is equity, D/V % of capital that

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Strategic and Financial

decision making

decision making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1 Weighted average cost of capital in different scenario...................................................1

Task 2 Cost of capital..................................................................................................................2

Task 3 Estimation of risk-adjusted Weighted Average Cost of Capital.....................................3

3.1 Calculation of risk adjusted specific discount rate......................................................3

3.2 WACC for Noggin plc.................................................................................................3

Task 4 How organizations can lower the WACC.......................................................................4

Task 5 Benefits of two types of growth: Organic and Acquisitive growth.................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Appendix..........................................................................................................................................9

INTRODUCTION...........................................................................................................................1

Task 1 Weighted average cost of capital in different scenario...................................................1

Task 2 Cost of capital..................................................................................................................2

Task 3 Estimation of risk-adjusted Weighted Average Cost of Capital.....................................3

3.1 Calculation of risk adjusted specific discount rate......................................................3

3.2 WACC for Noggin plc.................................................................................................3

Task 4 How organizations can lower the WACC.......................................................................4

Task 5 Benefits of two types of growth: Organic and Acquisitive growth.................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Appendix..........................................................................................................................................9

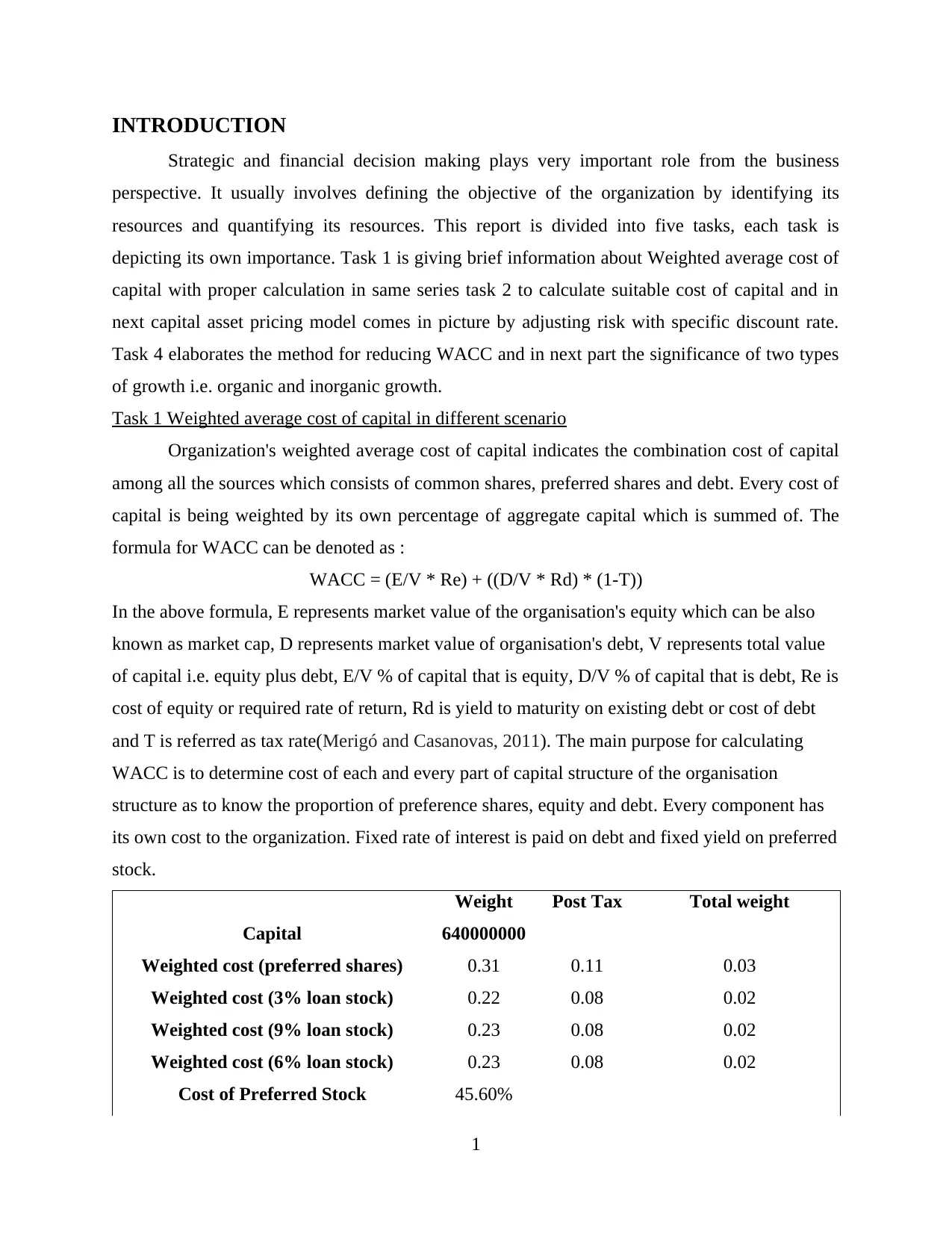

INTRODUCTION

Strategic and financial decision making plays very important role from the business

perspective. It usually involves defining the objective of the organization by identifying its

resources and quantifying its resources. This report is divided into five tasks, each task is

depicting its own importance. Task 1 is giving brief information about Weighted average cost of

capital with proper calculation in same series task 2 to calculate suitable cost of capital and in

next capital asset pricing model comes in picture by adjusting risk with specific discount rate.

Task 4 elaborates the method for reducing WACC and in next part the significance of two types

of growth i.e. organic and inorganic growth.

Task 1 Weighted average cost of capital in different scenario

Organization's weighted average cost of capital indicates the combination cost of capital

among all the sources which consists of common shares, preferred shares and debt. Every cost of

capital is being weighted by its own percentage of aggregate capital which is summed of. The

formula for WACC can be denoted as :

WACC = (E/V * Re) + ((D/V * Rd) * (1-T))

In the above formula, E represents market value of the organisation's equity which can be also

known as market cap, D represents market value of organisation's debt, V represents total value

of capital i.e. equity plus debt, E/V % of capital that is equity, D/V % of capital that is debt, Re is

cost of equity or required rate of return, Rd is yield to maturity on existing debt or cost of debt

and T is referred as tax rate(Merigó and Casanovas, 2011). The main purpose for calculating

WACC is to determine cost of each and every part of capital structure of the organisation

structure as to know the proportion of preference shares, equity and debt. Every component has

its own cost to the organization. Fixed rate of interest is paid on debt and fixed yield on preferred

stock.

Weight Post Tax Total weight

Capital 640000000

Weighted cost (preferred shares) 0.31 0.11 0.03

Weighted cost (3% loan stock) 0.22 0.08 0.02

Weighted cost (9% loan stock) 0.23 0.08 0.02

Weighted cost (6% loan stock) 0.23 0.08 0.02

Cost of Preferred Stock 45.60%

1

Strategic and financial decision making plays very important role from the business

perspective. It usually involves defining the objective of the organization by identifying its

resources and quantifying its resources. This report is divided into five tasks, each task is

depicting its own importance. Task 1 is giving brief information about Weighted average cost of

capital with proper calculation in same series task 2 to calculate suitable cost of capital and in

next capital asset pricing model comes in picture by adjusting risk with specific discount rate.

Task 4 elaborates the method for reducing WACC and in next part the significance of two types

of growth i.e. organic and inorganic growth.

Task 1 Weighted average cost of capital in different scenario

Organization's weighted average cost of capital indicates the combination cost of capital

among all the sources which consists of common shares, preferred shares and debt. Every cost of

capital is being weighted by its own percentage of aggregate capital which is summed of. The

formula for WACC can be denoted as :

WACC = (E/V * Re) + ((D/V * Rd) * (1-T))

In the above formula, E represents market value of the organisation's equity which can be also

known as market cap, D represents market value of organisation's debt, V represents total value

of capital i.e. equity plus debt, E/V % of capital that is equity, D/V % of capital that is debt, Re is

cost of equity or required rate of return, Rd is yield to maturity on existing debt or cost of debt

and T is referred as tax rate(Merigó and Casanovas, 2011). The main purpose for calculating

WACC is to determine cost of each and every part of capital structure of the organisation

structure as to know the proportion of preference shares, equity and debt. Every component has

its own cost to the organization. Fixed rate of interest is paid on debt and fixed yield on preferred

stock.

Weight Post Tax Total weight

Capital 640000000

Weighted cost (preferred shares) 0.31 0.11 0.03

Weighted cost (3% loan stock) 0.22 0.08 0.02

Weighted cost (9% loan stock) 0.23 0.08 0.02

Weighted cost (6% loan stock) 0.23 0.08 0.02

Cost of Preferred Stock 45.60%

1

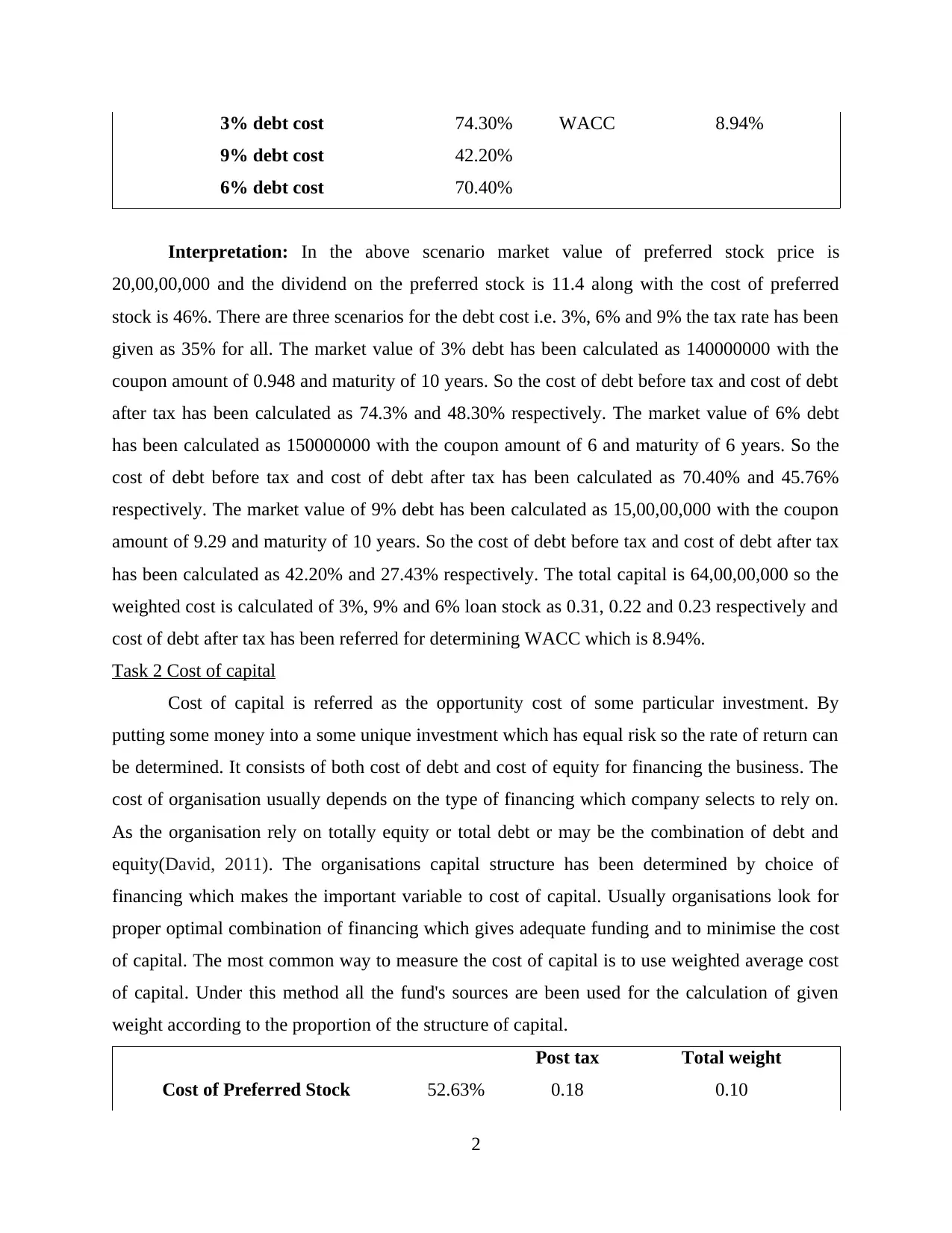

3% debt cost 74.30% WACC 8.94%

9% debt cost 42.20%

6% debt cost 70.40%

Interpretation: In the above scenario market value of preferred stock price is

20,00,00,000 and the dividend on the preferred stock is 11.4 along with the cost of preferred

stock is 46%. There are three scenarios for the debt cost i.e. 3%, 6% and 9% the tax rate has been

given as 35% for all. The market value of 3% debt has been calculated as 140000000 with the

coupon amount of 0.948 and maturity of 10 years. So the cost of debt before tax and cost of debt

after tax has been calculated as 74.3% and 48.30% respectively. The market value of 6% debt

has been calculated as 150000000 with the coupon amount of 6 and maturity of 6 years. So the

cost of debt before tax and cost of debt after tax has been calculated as 70.40% and 45.76%

respectively. The market value of 9% debt has been calculated as 15,00,00,000 with the coupon

amount of 9.29 and maturity of 10 years. So the cost of debt before tax and cost of debt after tax

has been calculated as 42.20% and 27.43% respectively. The total capital is 64,00,00,000 so the

weighted cost is calculated of 3%, 9% and 6% loan stock as 0.31, 0.22 and 0.23 respectively and

cost of debt after tax has been referred for determining WACC which is 8.94%.

Task 2 Cost of capital

Cost of capital is referred as the opportunity cost of some particular investment. By

putting some money into a some unique investment which has equal risk so the rate of return can

be determined. It consists of both cost of debt and cost of equity for financing the business. The

cost of organisation usually depends on the type of financing which company selects to rely on.

As the organisation rely on totally equity or total debt or may be the combination of debt and

equity(David, 2011). The organisations capital structure has been determined by choice of

financing which makes the important variable to cost of capital. Usually organisations look for

proper optimal combination of financing which gives adequate funding and to minimise the cost

of capital. The most common way to measure the cost of capital is to use weighted average cost

of capital. Under this method all the fund's sources are been used for the calculation of given

weight according to the proportion of the structure of capital.

Post tax Total weight

Cost of Preferred Stock 52.63% 0.18 0.10

2

9% debt cost 42.20%

6% debt cost 70.40%

Interpretation: In the above scenario market value of preferred stock price is

20,00,00,000 and the dividend on the preferred stock is 11.4 along with the cost of preferred

stock is 46%. There are three scenarios for the debt cost i.e. 3%, 6% and 9% the tax rate has been

given as 35% for all. The market value of 3% debt has been calculated as 140000000 with the

coupon amount of 0.948 and maturity of 10 years. So the cost of debt before tax and cost of debt

after tax has been calculated as 74.3% and 48.30% respectively. The market value of 6% debt

has been calculated as 150000000 with the coupon amount of 6 and maturity of 6 years. So the

cost of debt before tax and cost of debt after tax has been calculated as 70.40% and 45.76%

respectively. The market value of 9% debt has been calculated as 15,00,00,000 with the coupon

amount of 9.29 and maturity of 10 years. So the cost of debt before tax and cost of debt after tax

has been calculated as 42.20% and 27.43% respectively. The total capital is 64,00,00,000 so the

weighted cost is calculated of 3%, 9% and 6% loan stock as 0.31, 0.22 and 0.23 respectively and

cost of debt after tax has been referred for determining WACC which is 8.94%.

Task 2 Cost of capital

Cost of capital is referred as the opportunity cost of some particular investment. By

putting some money into a some unique investment which has equal risk so the rate of return can

be determined. It consists of both cost of debt and cost of equity for financing the business. The

cost of organisation usually depends on the type of financing which company selects to rely on.

As the organisation rely on totally equity or total debt or may be the combination of debt and

equity(David, 2011). The organisations capital structure has been determined by choice of

financing which makes the important variable to cost of capital. Usually organisations look for

proper optimal combination of financing which gives adequate funding and to minimise the cost

of capital. The most common way to measure the cost of capital is to use weighted average cost

of capital. Under this method all the fund's sources are been used for the calculation of given

weight according to the proportion of the structure of capital.

Post tax Total weight

Cost of Preferred Stock 52.63% 0.18 0.10

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

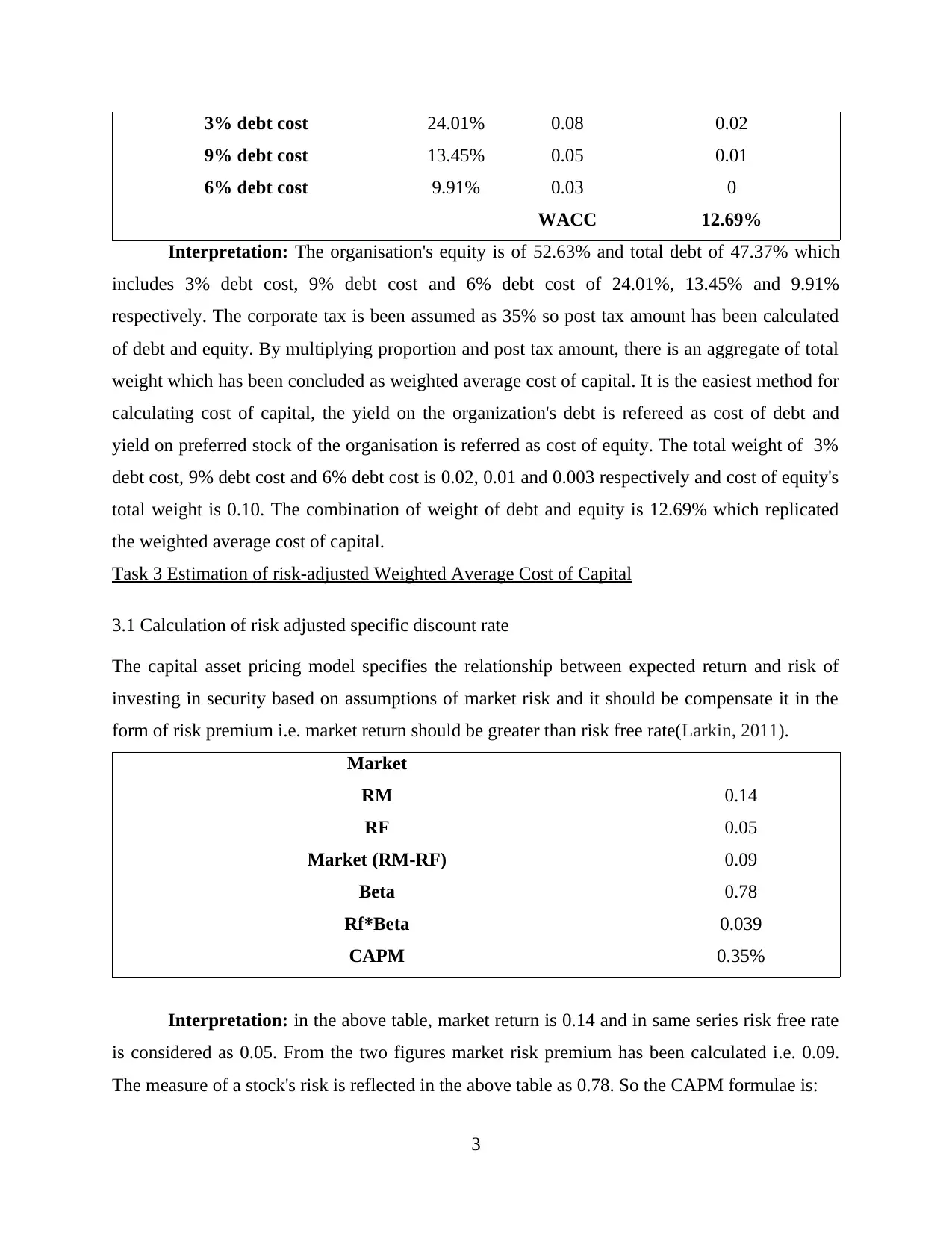

3% debt cost 24.01% 0.08 0.02

9% debt cost 13.45% 0.05 0.01

6% debt cost 9.91% 0.03 0

WACC 12.69%

Interpretation: The organisation's equity is of 52.63% and total debt of 47.37% which

includes 3% debt cost, 9% debt cost and 6% debt cost of 24.01%, 13.45% and 9.91%

respectively. The corporate tax is been assumed as 35% so post tax amount has been calculated

of debt and equity. By multiplying proportion and post tax amount, there is an aggregate of total

weight which has been concluded as weighted average cost of capital. It is the easiest method for

calculating cost of capital, the yield on the organization's debt is refereed as cost of debt and

yield on preferred stock of the organisation is referred as cost of equity. The total weight of 3%

debt cost, 9% debt cost and 6% debt cost is 0.02, 0.01 and 0.003 respectively and cost of equity's

total weight is 0.10. The combination of weight of debt and equity is 12.69% which replicated

the weighted average cost of capital.

Task 3 Estimation of risk-adjusted Weighted Average Cost of Capital

3.1 Calculation of risk adjusted specific discount rate

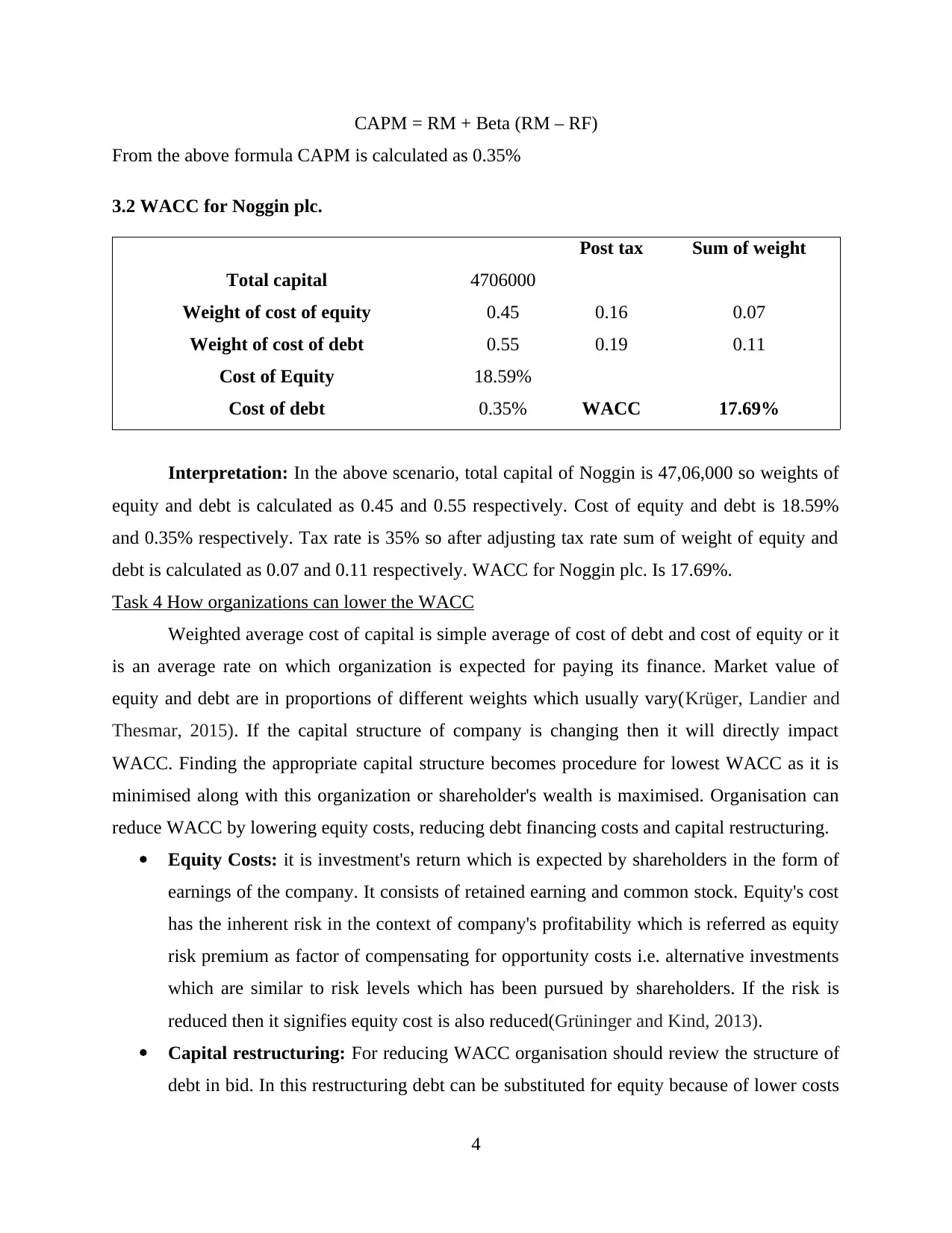

The capital asset pricing model specifies the relationship between expected return and risk of

investing in security based on assumptions of market risk and it should be compensate it in the

form of risk premium i.e. market return should be greater than risk free rate(Larkin, 2011).

Market

RM 0.14

RF 0.05

Market (RM-RF) 0.09

Beta 0.78

Rf*Beta 0.039

CAPM 0.35%

Interpretation: in the above table, market return is 0.14 and in same series risk free rate

is considered as 0.05. From the two figures market risk premium has been calculated i.e. 0.09.

The measure of a stock's risk is reflected in the above table as 0.78. So the CAPM formulae is:

3

9% debt cost 13.45% 0.05 0.01

6% debt cost 9.91% 0.03 0

WACC 12.69%

Interpretation: The organisation's equity is of 52.63% and total debt of 47.37% which

includes 3% debt cost, 9% debt cost and 6% debt cost of 24.01%, 13.45% and 9.91%

respectively. The corporate tax is been assumed as 35% so post tax amount has been calculated

of debt and equity. By multiplying proportion and post tax amount, there is an aggregate of total

weight which has been concluded as weighted average cost of capital. It is the easiest method for

calculating cost of capital, the yield on the organization's debt is refereed as cost of debt and

yield on preferred stock of the organisation is referred as cost of equity. The total weight of 3%

debt cost, 9% debt cost and 6% debt cost is 0.02, 0.01 and 0.003 respectively and cost of equity's

total weight is 0.10. The combination of weight of debt and equity is 12.69% which replicated

the weighted average cost of capital.

Task 3 Estimation of risk-adjusted Weighted Average Cost of Capital

3.1 Calculation of risk adjusted specific discount rate

The capital asset pricing model specifies the relationship between expected return and risk of

investing in security based on assumptions of market risk and it should be compensate it in the

form of risk premium i.e. market return should be greater than risk free rate(Larkin, 2011).

Market

RM 0.14

RF 0.05

Market (RM-RF) 0.09

Beta 0.78

Rf*Beta 0.039

CAPM 0.35%

Interpretation: in the above table, market return is 0.14 and in same series risk free rate

is considered as 0.05. From the two figures market risk premium has been calculated i.e. 0.09.

The measure of a stock's risk is reflected in the above table as 0.78. So the CAPM formulae is:

3

CAPM = RM + Beta (RM – RF)

From the above formula CAPM is calculated as 0.35%

3.2 WACC for Noggin plc.

Post tax Sum of weight

Total capital 4706000

Weight of cost of equity 0.45 0.16 0.07

Weight of cost of debt 0.55 0.19 0.11

Cost of Equity 18.59%

Cost of debt 0.35% WACC 17.69%

Interpretation: In the above scenario, total capital of Noggin is 47,06,000 so weights of

equity and debt is calculated as 0.45 and 0.55 respectively. Cost of equity and debt is 18.59%

and 0.35% respectively. Tax rate is 35% so after adjusting tax rate sum of weight of equity and

debt is calculated as 0.07 and 0.11 respectively. WACC for Noggin plc. Is 17.69%.

Task 4 How organizations can lower the WACC

Weighted average cost of capital is simple average of cost of debt and cost of equity or it

is an average rate on which organization is expected for paying its finance. Market value of

equity and debt are in proportions of different weights which usually vary(Krüger, Landier and

Thesmar, 2015). If the capital structure of company is changing then it will directly impact

WACC. Finding the appropriate capital structure becomes procedure for lowest WACC as it is

minimised along with this organization or shareholder's wealth is maximised. Organisation can

reduce WACC by lowering equity costs, reducing debt financing costs and capital restructuring.

Equity Costs: it is investment's return which is expected by shareholders in the form of

earnings of the company. It consists of retained earning and common stock. Equity's cost

has the inherent risk in the context of company's profitability which is referred as equity

risk premium as factor of compensating for opportunity costs i.e. alternative investments

which are similar to risk levels which has been pursued by shareholders. If the risk is

reduced then it signifies equity cost is also reduced(Grüninger and Kind, 2013).

Capital restructuring: For reducing WACC organisation should review the structure of

debt in bid. In this restructuring debt can be substituted for equity because of lower costs

4

From the above formula CAPM is calculated as 0.35%

3.2 WACC for Noggin plc.

Post tax Sum of weight

Total capital 4706000

Weight of cost of equity 0.45 0.16 0.07

Weight of cost of debt 0.55 0.19 0.11

Cost of Equity 18.59%

Cost of debt 0.35% WACC 17.69%

Interpretation: In the above scenario, total capital of Noggin is 47,06,000 so weights of

equity and debt is calculated as 0.45 and 0.55 respectively. Cost of equity and debt is 18.59%

and 0.35% respectively. Tax rate is 35% so after adjusting tax rate sum of weight of equity and

debt is calculated as 0.07 and 0.11 respectively. WACC for Noggin plc. Is 17.69%.

Task 4 How organizations can lower the WACC

Weighted average cost of capital is simple average of cost of debt and cost of equity or it

is an average rate on which organization is expected for paying its finance. Market value of

equity and debt are in proportions of different weights which usually vary(Krüger, Landier and

Thesmar, 2015). If the capital structure of company is changing then it will directly impact

WACC. Finding the appropriate capital structure becomes procedure for lowest WACC as it is

minimised along with this organization or shareholder's wealth is maximised. Organisation can

reduce WACC by lowering equity costs, reducing debt financing costs and capital restructuring.

Equity Costs: it is investment's return which is expected by shareholders in the form of

earnings of the company. It consists of retained earning and common stock. Equity's cost

has the inherent risk in the context of company's profitability which is referred as equity

risk premium as factor of compensating for opportunity costs i.e. alternative investments

which are similar to risk levels which has been pursued by shareholders. If the risk is

reduced then it signifies equity cost is also reduced(Grüninger and Kind, 2013).

Capital restructuring: For reducing WACC organisation should review the structure of

debt in bid. In this restructuring debt can be substituted for equity because of lower costs

4

after taxation. If equity is raised then it will directly attracts the marginal cost of capital

which signifies raising new capital's cost along with equity risk premium. Organisations

can substitute common stock by preferred stock for decreasing WACC which is less

expensive as compared to common stock due to less equity premium rates.

Cost of debt is less expensive from cost of equity because of factor risk, equity is more

risky as compared to debt, return which is required for compensating debt is less than equity

because of interest payment is of fixed amount which is paid initially in the form of dividend

payments. Debt is less risky than equity because of liquidation factor, capital repayment will be

first received by debt holders before shareholders because of top position in creditor hierarchy

and last payment is paid to shareholders. In debt financing costs, debt's cost is interest rate which

is applied on loans borrowed from financial institutions and non bank financial institutions. The

interest rate which is applicable reflects risk for non payment relative collateral which is required

for attaching loans. Non payment leads to cutting debt, if the alternative capital's interest rate is

higher, then organisation should pay off the debt and alternative capital should be sourced so

obligation for repayment of alternative capital at less interest rates(Zabarankin, Pavlikov and

Uryasev, 2014). From the organization's perspective also debt is cheaper than compared to equity

because of taxation that corporate tax of interests and dividend's treatment. Interest is excluded

before the calculation of tax in profit and loss account and companies get tax free on interest.

When tax is calculated dividends are excluded and there is no tax relief on dividends by the

organisation. More expensive equity replaces by less expensive debt for reducing the average

WACC. If more debt is issued which is also referred as gearing then more interest payment on

profits before the payment of dividends by shareholders and interest payment increases then

volatility of payment of dividends to shareholders because if company is facing poor year then

still payments of interests should be still paid giving effect on the ability of organisation to pay

dividends. If the volatility is increased for dividend payment to shareholders which will lead to

increment in financial risk for shareholders. And if the financial risk of shareholders increases

then there is huge requirement of return for compensating them for risk increment and if the

equity's cost will increase then it will lead to increment in WACC.

After knowing all the elements of WACC the first step is working on the ways how to

lower it. In the context of debt, organisations can decrease cost of issuing bonds by less interest

rate which is offered to investors. Even this can be done by being most credit worthy. The

5

which signifies raising new capital's cost along with equity risk premium. Organisations

can substitute common stock by preferred stock for decreasing WACC which is less

expensive as compared to common stock due to less equity premium rates.

Cost of debt is less expensive from cost of equity because of factor risk, equity is more

risky as compared to debt, return which is required for compensating debt is less than equity

because of interest payment is of fixed amount which is paid initially in the form of dividend

payments. Debt is less risky than equity because of liquidation factor, capital repayment will be

first received by debt holders before shareholders because of top position in creditor hierarchy

and last payment is paid to shareholders. In debt financing costs, debt's cost is interest rate which

is applied on loans borrowed from financial institutions and non bank financial institutions. The

interest rate which is applicable reflects risk for non payment relative collateral which is required

for attaching loans. Non payment leads to cutting debt, if the alternative capital's interest rate is

higher, then organisation should pay off the debt and alternative capital should be sourced so

obligation for repayment of alternative capital at less interest rates(Zabarankin, Pavlikov and

Uryasev, 2014). From the organization's perspective also debt is cheaper than compared to equity

because of taxation that corporate tax of interests and dividend's treatment. Interest is excluded

before the calculation of tax in profit and loss account and companies get tax free on interest.

When tax is calculated dividends are excluded and there is no tax relief on dividends by the

organisation. More expensive equity replaces by less expensive debt for reducing the average

WACC. If more debt is issued which is also referred as gearing then more interest payment on

profits before the payment of dividends by shareholders and interest payment increases then

volatility of payment of dividends to shareholders because if company is facing poor year then

still payments of interests should be still paid giving effect on the ability of organisation to pay

dividends. If the volatility is increased for dividend payment to shareholders which will lead to

increment in financial risk for shareholders. And if the financial risk of shareholders increases

then there is huge requirement of return for compensating them for risk increment and if the

equity's cost will increase then it will lead to increment in WACC.

After knowing all the elements of WACC the first step is working on the ways how to

lower it. In the context of debt, organisations can decrease cost of issuing bonds by less interest

rate which is offered to investors. Even this can be done by being most credit worthy. The

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisations whose credit rating is worse should offer bonds with higher rates. If the company is

moving for high tax rate but this leads to counter productive. In terms of equity, shares of less

beta can be offered by the company to low risky investors who offers less risk premium. In the

same series general market risk and risk free premium are not in company's control i.e. outside

the company's control. Caution should be always taken regardless of company's method for

reducing WACC because of each method depends on the suitability on existing capital structure

of the company(Kukko, 2013). As huge amount of debts which are long-term can be extremely

burden and difficult to the organization.

Last but not least, WACC can be the lowest by: issuing more debt but contrary to that

more debt increases the WACC as Financial risk, gearing, beta equity and Keg WACC. Keg is

beta equity's function which consists of both financial risk and business risk. If there is increment

in financial risk then beta equity will increase, Keg will increase and majorly WACC will

increase. The WACC reduction is majorly caused by great amount of less expensive debt or the

increment in WACC is due to Increase in the financial risk.

Task 5 Benefits of two types of growth: Organic and Acquisitive growth

Two types of growth are: Organic growth and Acquisition growth

Organic growth: It is the growth rate of company which can be achieved by enhancing

sales and increasing output internally or the expansion of the organization by the operations from

its own resources which are generated internally without borrowing or acquiring other

companies. As it is from perspective of long term, so many investors and executives value it and

gives perfect commitment for building a business. This can be also taken as in negative manner

because it signifies contracting of business. Organic growth observed by investors for the

purpose of keeping track on increasing revenues and sales and to check the sustainability is

increasing or not in long term(Geus, 2011). Organic growth shows that how the management of

the organisation is optimising and utilising the internal resources for generating a rise in sales

and output. There is presence of artificial boost on organization's sales and revenue figures by

mergers, takeovers and acquisitions. The special focus on organic growth shows that how

organization is able to achieve it goals and objectives along with internal means.

Organic growth is usually more preferred by investors because of management's efficient

use of resources and commitment for the business and also because it gives proper analysis of the

organization and in easy manner. By observing the financials of the company, the main

6

moving for high tax rate but this leads to counter productive. In terms of equity, shares of less

beta can be offered by the company to low risky investors who offers less risk premium. In the

same series general market risk and risk free premium are not in company's control i.e. outside

the company's control. Caution should be always taken regardless of company's method for

reducing WACC because of each method depends on the suitability on existing capital structure

of the company(Kukko, 2013). As huge amount of debts which are long-term can be extremely

burden and difficult to the organization.

Last but not least, WACC can be the lowest by: issuing more debt but contrary to that

more debt increases the WACC as Financial risk, gearing, beta equity and Keg WACC. Keg is

beta equity's function which consists of both financial risk and business risk. If there is increment

in financial risk then beta equity will increase, Keg will increase and majorly WACC will

increase. The WACC reduction is majorly caused by great amount of less expensive debt or the

increment in WACC is due to Increase in the financial risk.

Task 5 Benefits of two types of growth: Organic and Acquisitive growth

Two types of growth are: Organic growth and Acquisition growth

Organic growth: It is the growth rate of company which can be achieved by enhancing

sales and increasing output internally or the expansion of the organization by the operations from

its own resources which are generated internally without borrowing or acquiring other

companies. As it is from perspective of long term, so many investors and executives value it and

gives perfect commitment for building a business. This can be also taken as in negative manner

because it signifies contracting of business. Organic growth observed by investors for the

purpose of keeping track on increasing revenues and sales and to check the sustainability is

increasing or not in long term(Geus, 2011). Organic growth shows that how the management of

the organisation is optimising and utilising the internal resources for generating a rise in sales

and output. There is presence of artificial boost on organization's sales and revenue figures by

mergers, takeovers and acquisitions. The special focus on organic growth shows that how

organization is able to achieve it goals and objectives along with internal means.

Organic growth is usually more preferred by investors because of management's efficient

use of resources and commitment for the business and also because it gives proper analysis of the

organization and in easy manner. By observing the financials of the company, the main

6

indication is about to note that sales and revenue numbers must be inflated because of recent

acquisitions. And because of this, investors will rid off the non organic growth from the financial

of the organization which signifies potential of true growth to the company's core. There are very

less organisation who relies on mergers and acquisitions because there analysis is about to get

only the core figure. It can maintain current management culture, style and ethics as it is less

risky which can expand where it is expertise. It makes easier for the organization to manage

internal growth. There is less disruption changes i.e. worker's productivity and efficiency and

their morale should be at highest.

Acquisition growth: It can be also refereed as inorganic growth, in which the operation's

growth of business comes from acquisition and merger, instead of increment in organisation's

own business activity. Goodway Plc can also expand into the unfamiliar industry by acquisition

i.e. Noggin plc. If there is need of expansion, then company can select to facilitate by acquiring

some small business. This acquisition leads to fast and rapid growth but along with this difficult

issues are also in the picture. The main advantage of acquisition is that organisation can gain

experience, assets and goodwill of other organization. Efficiency can be improved from the

merger if the acquired business compliment others about its operations. There is positive

relationship between staff, assets and output, profits. Strength and weakness of both the

companies should be merged.

Acquisition leads to excitement in shareholders like if public company's shareholders

hear the news of acquisition or merger then positive framework has been established as well as

valuation of the organisation (Pal, and.et.al, 2018). It may leads to rise in stock price and

investment's equity. It will lead to focus on the priorities and business aspects which are more

important for development. It will give encouragement to build and grow a better and bigger

business. The experience of company will help in curing calculated risks for growth which is

optimal. Wit the help of acquisitions, new people brings fresh ideas and perspectives to run

business for creating brand image and good margins. Knowledge base is required while working

with the expert team who are more passionate about guiding to achieve and accomplish goals

and objectives.

CONCLUSION

From the above report it has been concluded that strategic and financial decision-making

is very important from the perspective of business for every organization. To evaluate cost of

7

acquisitions. And because of this, investors will rid off the non organic growth from the financial

of the organization which signifies potential of true growth to the company's core. There are very

less organisation who relies on mergers and acquisitions because there analysis is about to get

only the core figure. It can maintain current management culture, style and ethics as it is less

risky which can expand where it is expertise. It makes easier for the organization to manage

internal growth. There is less disruption changes i.e. worker's productivity and efficiency and

their morale should be at highest.

Acquisition growth: It can be also refereed as inorganic growth, in which the operation's

growth of business comes from acquisition and merger, instead of increment in organisation's

own business activity. Goodway Plc can also expand into the unfamiliar industry by acquisition

i.e. Noggin plc. If there is need of expansion, then company can select to facilitate by acquiring

some small business. This acquisition leads to fast and rapid growth but along with this difficult

issues are also in the picture. The main advantage of acquisition is that organisation can gain

experience, assets and goodwill of other organization. Efficiency can be improved from the

merger if the acquired business compliment others about its operations. There is positive

relationship between staff, assets and output, profits. Strength and weakness of both the

companies should be merged.

Acquisition leads to excitement in shareholders like if public company's shareholders

hear the news of acquisition or merger then positive framework has been established as well as

valuation of the organisation (Pal, and.et.al, 2018). It may leads to rise in stock price and

investment's equity. It will lead to focus on the priorities and business aspects which are more

important for development. It will give encouragement to build and grow a better and bigger

business. The experience of company will help in curing calculated risks for growth which is

optimal. Wit the help of acquisitions, new people brings fresh ideas and perspectives to run

business for creating brand image and good margins. Knowledge base is required while working

with the expert team who are more passionate about guiding to achieve and accomplish goals

and objectives.

CONCLUSION

From the above report it has been concluded that strategic and financial decision-making

is very important from the perspective of business for every organization. To evaluate cost of

7

capital, many methods are used like Weighted average cost of capital, Capital Asset pricing

model by adjusting risk. It has been cleared from the report that Weighted average cost of capital

considers full capital structure i.e. weight of cost of debt and weight of cost of equity. It is the

easiest method for calculating cost of capital. If risk free rate, required rate of return and beta has

to be considered for measuring cost of capital then Capital asset pricing model should come into

the picture. As in the series of growth there are basically two types of growth which are organic

growth and acquisition growth. For some small companies organic growth is important but in the

present case for company to increase cost of capital inorganic growth has been considered. From

this we can conclude that type of growth is based on type of industry.

8

model by adjusting risk. It has been cleared from the report that Weighted average cost of capital

considers full capital structure i.e. weight of cost of debt and weight of cost of equity. It is the

easiest method for calculating cost of capital. If risk free rate, required rate of return and beta has

to be considered for measuring cost of capital then Capital asset pricing model should come into

the picture. As in the series of growth there are basically two types of growth which are organic

growth and acquisition growth. For some small companies organic growth is important but in the

present case for company to increase cost of capital inorganic growth has been considered. From

this we can conclude that type of growth is based on type of industry.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Brusov, P.and.et.al., 2011. Weighted average cost of capital in the theory of Modigliani–Miller,

modified for a finite lifetime company. Applied Financial Economics. 21(11). pp.815-824.

Da, Z., Guo, R. J. and Jagannathan, R., 2012. CAPM for estimating the cost of equity capital:

Interpreting the empirical evidence. Journal of Financial Economics. 103(1). pp.204-220.

David, F. R., 2011. Strategic management: Concepts and cases. Peaeson/Prentice Hall.

Fernandez, P., Aguirreamalloa, J. and Linares, P., 2013. Market Risk Premium and Risk Free

Rate used for 51 countries in 2013: a survey with 6,237 answers.

Geus, A., 2011. The living company: Growth, learning and longevity in business. Nicholas

Brealey Publishing.

Grüninger, M. C. and Kind, A. H., 2013. WACC calculations in practice: Incorrect results due to

inconsistent assumptions-status quo and improvements. Accounting and finance

research. 2(2). p.36.

Krüger, P., Landier, A. and Thesmar, D., 2015. The WACC fallacy: The real effects of using a

unique discount rate. The Journal of Finance. 70(3). pp.1253-1285.

Kukko, M., 2013. Knowledge sharing barriers in organic growth: A case study from a software

company. The Journal of High Technology Management Research. 24(1). pp.18-29.

Larkin, P. J., 2011. To iterate or not to iterate? Using the WACC in equity valuation. Journal of

Business & Economics Research (Online). 9(11). p.29.

Merigó, J. M. and Casanovas, M., 2011. Induced aggregation operators in the Euclidean distance

and its application in financial decision making. Expert Systems with Applications. 38(6).

pp.7603-7608.

Pal, R. P., and.et.al., 2018. Influence of feeding inorganic vanadium on growth performance,

endocrine variables and biomarkers of bone health in crossbred calves. Biological trace

element research. 182(2). pp.248-256.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM) with

drawdown measure. European Journal of Operational Research. 234(2). pp.508-517.

Online

Cost of Capital, 2018. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/finance/cost-of-capital/>

9

Books and Journals

Brusov, P.and.et.al., 2011. Weighted average cost of capital in the theory of Modigliani–Miller,

modified for a finite lifetime company. Applied Financial Economics. 21(11). pp.815-824.

Da, Z., Guo, R. J. and Jagannathan, R., 2012. CAPM for estimating the cost of equity capital:

Interpreting the empirical evidence. Journal of Financial Economics. 103(1). pp.204-220.

David, F. R., 2011. Strategic management: Concepts and cases. Peaeson/Prentice Hall.

Fernandez, P., Aguirreamalloa, J. and Linares, P., 2013. Market Risk Premium and Risk Free

Rate used for 51 countries in 2013: a survey with 6,237 answers.

Geus, A., 2011. The living company: Growth, learning and longevity in business. Nicholas

Brealey Publishing.

Grüninger, M. C. and Kind, A. H., 2013. WACC calculations in practice: Incorrect results due to

inconsistent assumptions-status quo and improvements. Accounting and finance

research. 2(2). p.36.

Krüger, P., Landier, A. and Thesmar, D., 2015. The WACC fallacy: The real effects of using a

unique discount rate. The Journal of Finance. 70(3). pp.1253-1285.

Kukko, M., 2013. Knowledge sharing barriers in organic growth: A case study from a software

company. The Journal of High Technology Management Research. 24(1). pp.18-29.

Larkin, P. J., 2011. To iterate or not to iterate? Using the WACC in equity valuation. Journal of

Business & Economics Research (Online). 9(11). p.29.

Merigó, J. M. and Casanovas, M., 2011. Induced aggregation operators in the Euclidean distance

and its application in financial decision making. Expert Systems with Applications. 38(6).

pp.7603-7608.

Pal, R. P., and.et.al., 2018. Influence of feeding inorganic vanadium on growth performance,

endocrine variables and biomarkers of bone health in crossbred calves. Biological trace

element research. 182(2). pp.248-256.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM) with

drawdown measure. European Journal of Operational Research. 234(2). pp.508-517.

Online

Cost of Capital, 2018. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/finance/cost-of-capital/>

9

10

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.