Financial Ratio Analysis of Two Companies

VerifiedAdded on 2020/01/28

|36

|5153

|120

Report

AI Summary

This assignment examines the financial health and performance of two companies, Wolseley and Booker, through a comprehensive analysis of financial ratios. The analysis encompasses both traditional ratios (liquidity, solvency, profitability, activity) and comparative techniques like vertical and horizontal analysis across income statement, balance sheet, and cash flow statement data.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

STRATEGIC FINANCIAL

ANALYSIS

ANALYSIS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Strategic financial analysis and its importance......................................................................1

Objectives...............................................................................................................................1

Overview of companies..........................................................................................................1

Methods of analysis................................................................................................................1

RATIO ANALYSIS.........................................................................................................................1

Profitability Ratios..................................................................................................................2

Liquidity Ratios......................................................................................................................6

Efficiency ratios......................................................................................................................8

Solvency ratio.......................................................................................................................12

Investor ratio.........................................................................................................................13

COMMON –SIZE..........................................................................................................................15

Horizontal.............................................................................................................................15

Vertical analysis...................................................................................................................16

Du-Pont.................................................................................................................................16

Segmental revenues..............................................................................................................17

ADVANTAGE AND DISADVANTAGE....................................................................................17

Ratio analysis........................................................................................................................17

Du-Pont.................................................................................................................................18

Segmental.............................................................................................................................18

CONCLUSION & RECOMMENDATIONS................................................................................18

Conclusion............................................................................................................................18

Recommendation..................................................................................................................19

CONTEMPROARY METHODS..................................................................................................19

CAPM model........................................................................................................................19

Efficient market hypothesis..................................................................................................19

Economic value added (EVA)..............................................................................................20

REFERENCES..............................................................................................................................21

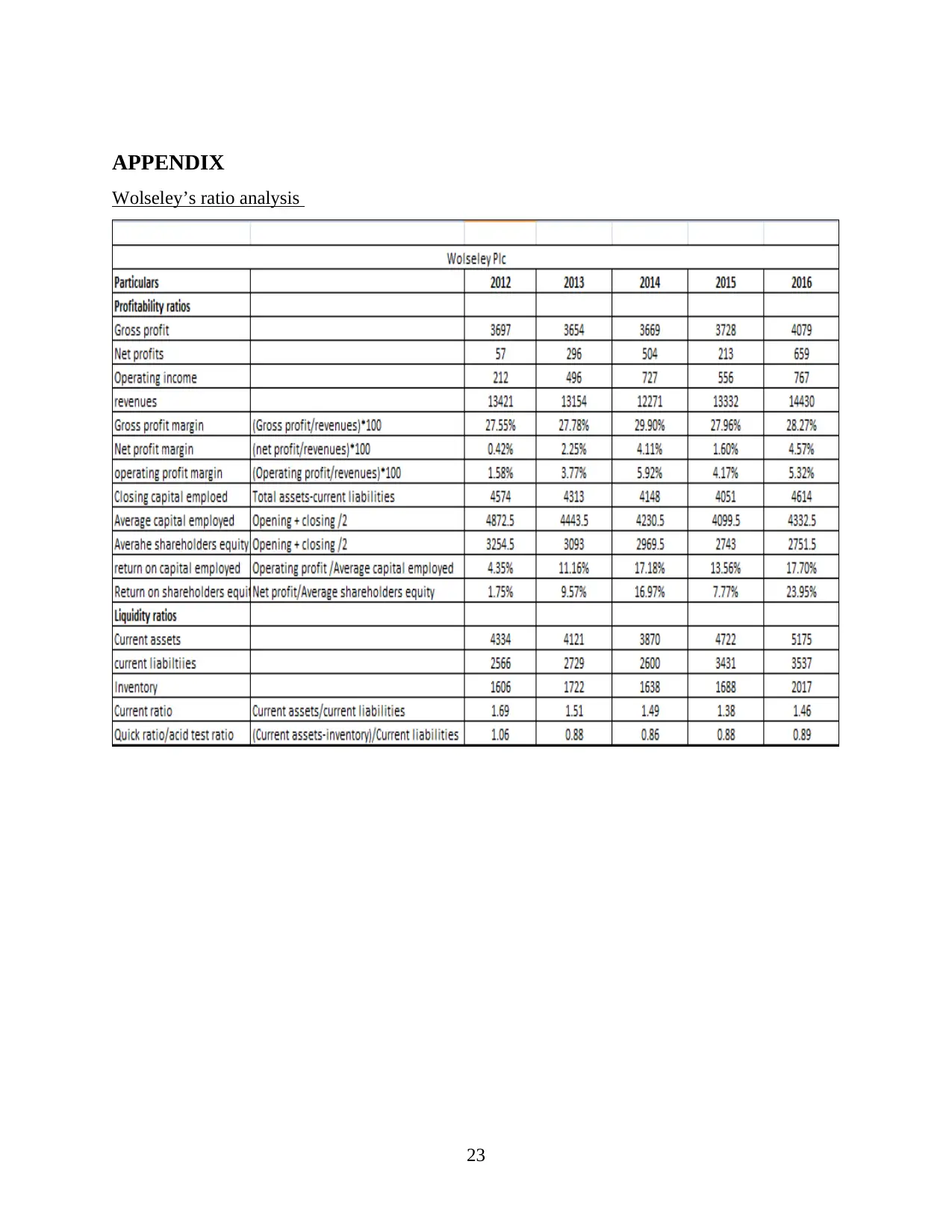

APPENDIX....................................................................................................................................23

Wolseley’s ratio analysis......................................................................................................23

INTRODUCTION...........................................................................................................................1

Strategic financial analysis and its importance......................................................................1

Objectives...............................................................................................................................1

Overview of companies..........................................................................................................1

Methods of analysis................................................................................................................1

RATIO ANALYSIS.........................................................................................................................1

Profitability Ratios..................................................................................................................2

Liquidity Ratios......................................................................................................................6

Efficiency ratios......................................................................................................................8

Solvency ratio.......................................................................................................................12

Investor ratio.........................................................................................................................13

COMMON –SIZE..........................................................................................................................15

Horizontal.............................................................................................................................15

Vertical analysis...................................................................................................................16

Du-Pont.................................................................................................................................16

Segmental revenues..............................................................................................................17

ADVANTAGE AND DISADVANTAGE....................................................................................17

Ratio analysis........................................................................................................................17

Du-Pont.................................................................................................................................18

Segmental.............................................................................................................................18

CONCLUSION & RECOMMENDATIONS................................................................................18

Conclusion............................................................................................................................18

Recommendation..................................................................................................................19

CONTEMPROARY METHODS..................................................................................................19

CAPM model........................................................................................................................19

Efficient market hypothesis..................................................................................................19

Economic value added (EVA)..............................................................................................20

REFERENCES..............................................................................................................................21

APPENDIX....................................................................................................................................23

Wolseley’s ratio analysis......................................................................................................23

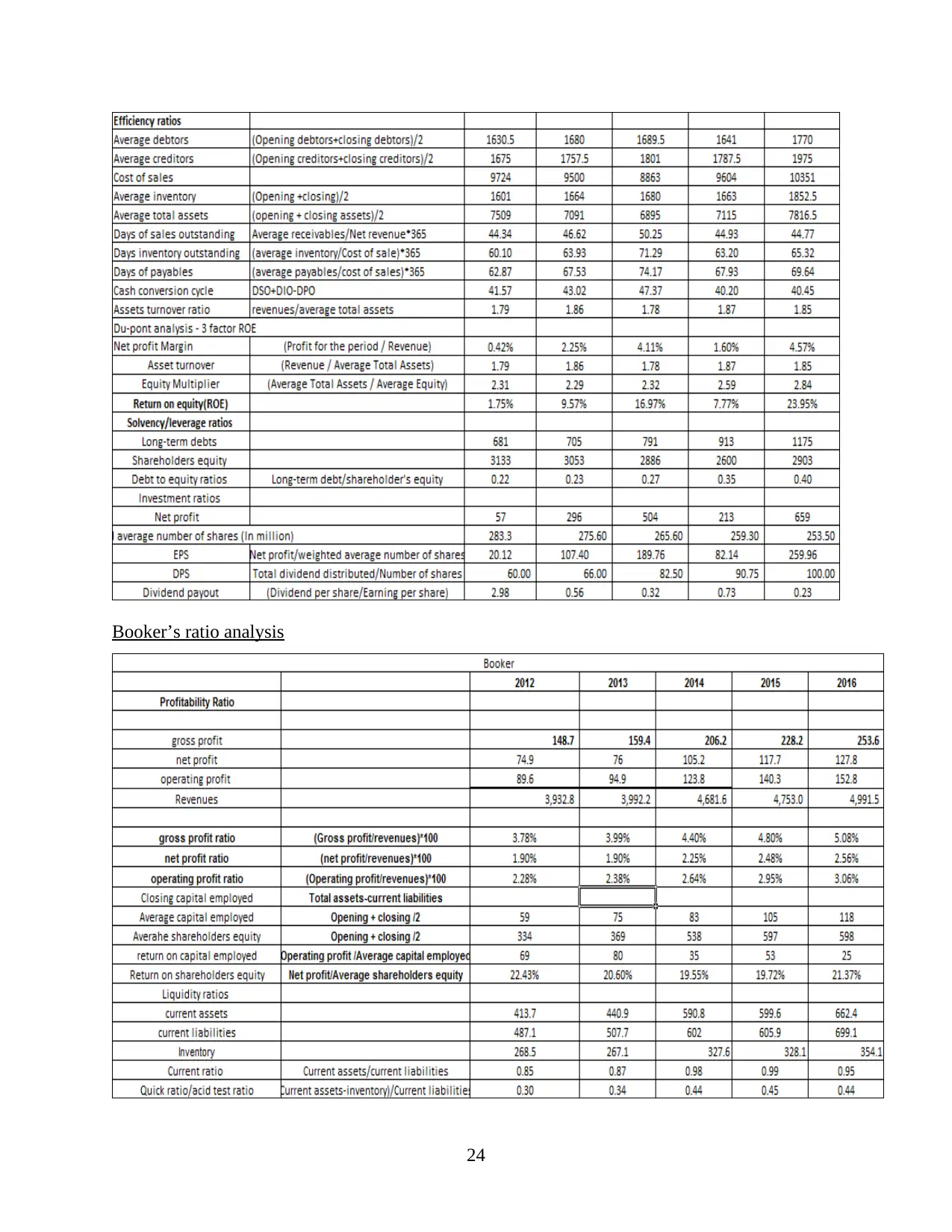

Booker’s ratio analysis.........................................................................................................24

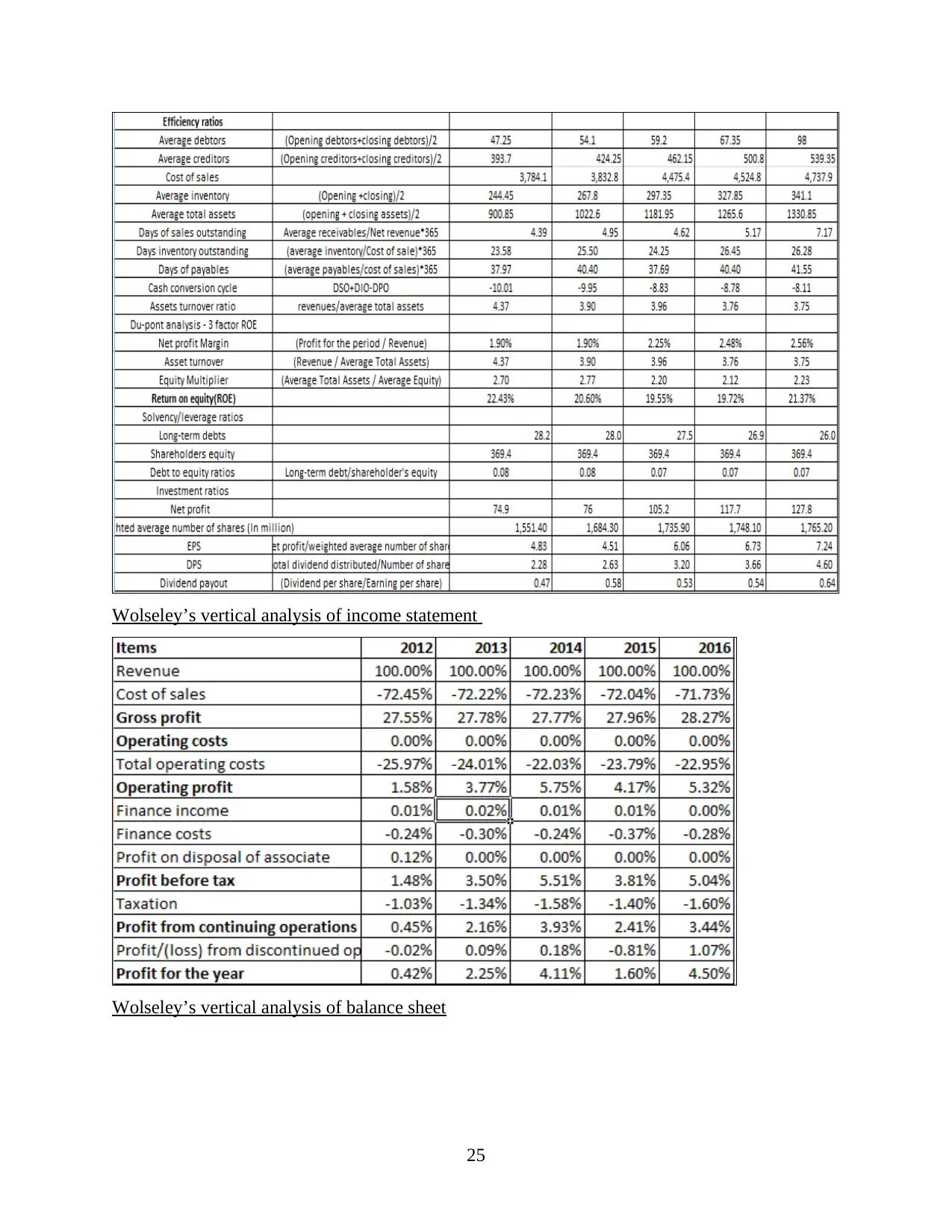

Wolseley’s vertical analysis of income statement................................................................25

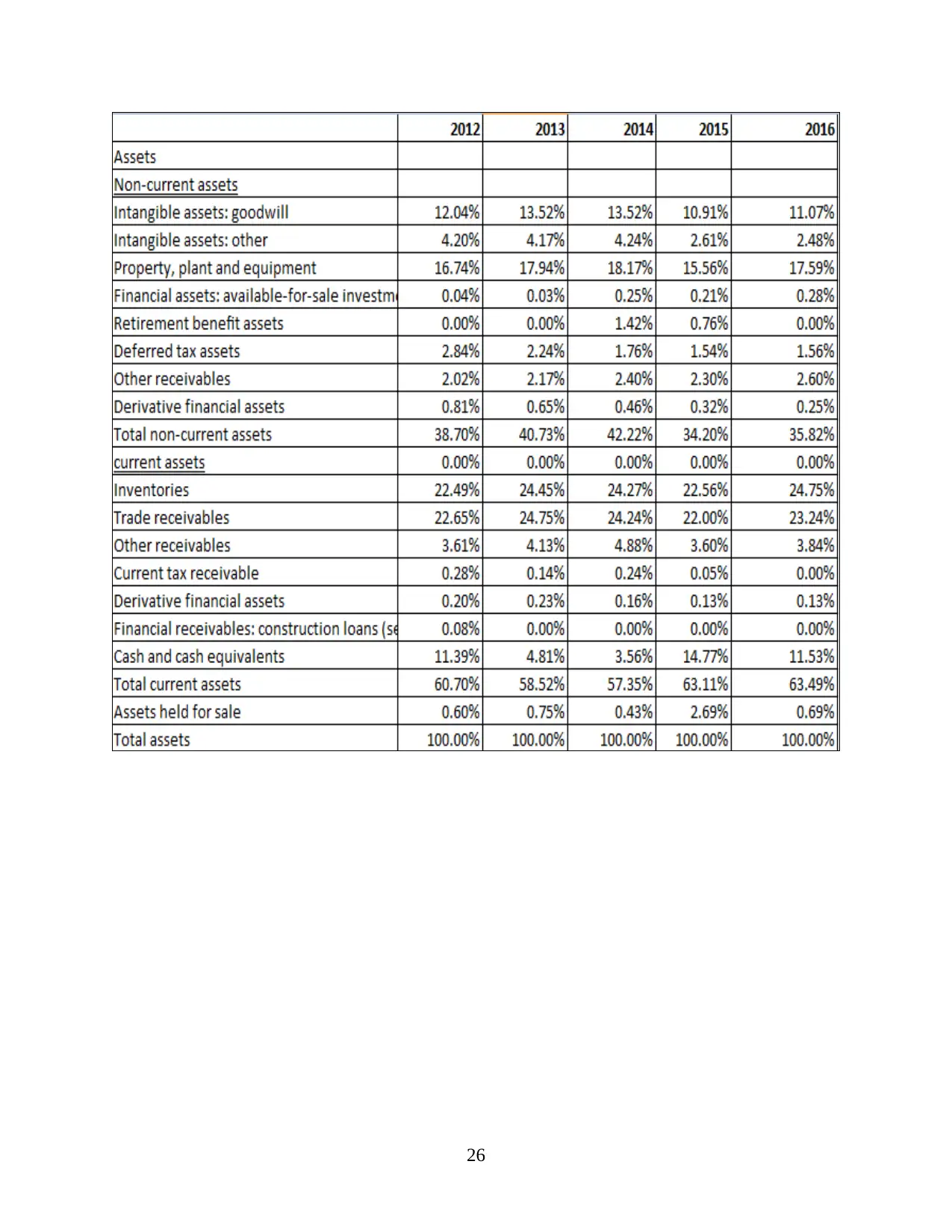

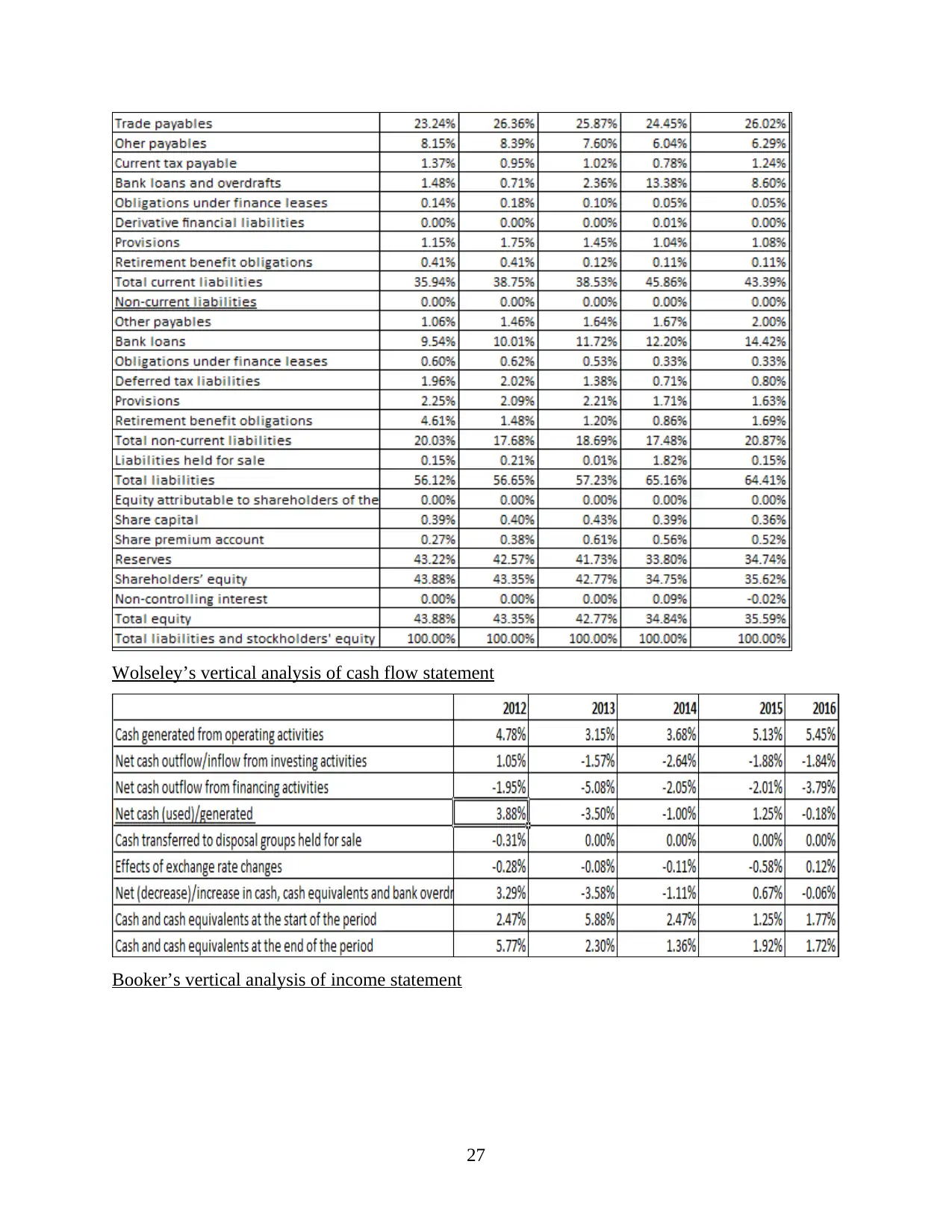

Wolseley’s vertical analysis of balance sheet......................................................................25

Wolseley’s vertical analysis of cash flow statement............................................................27

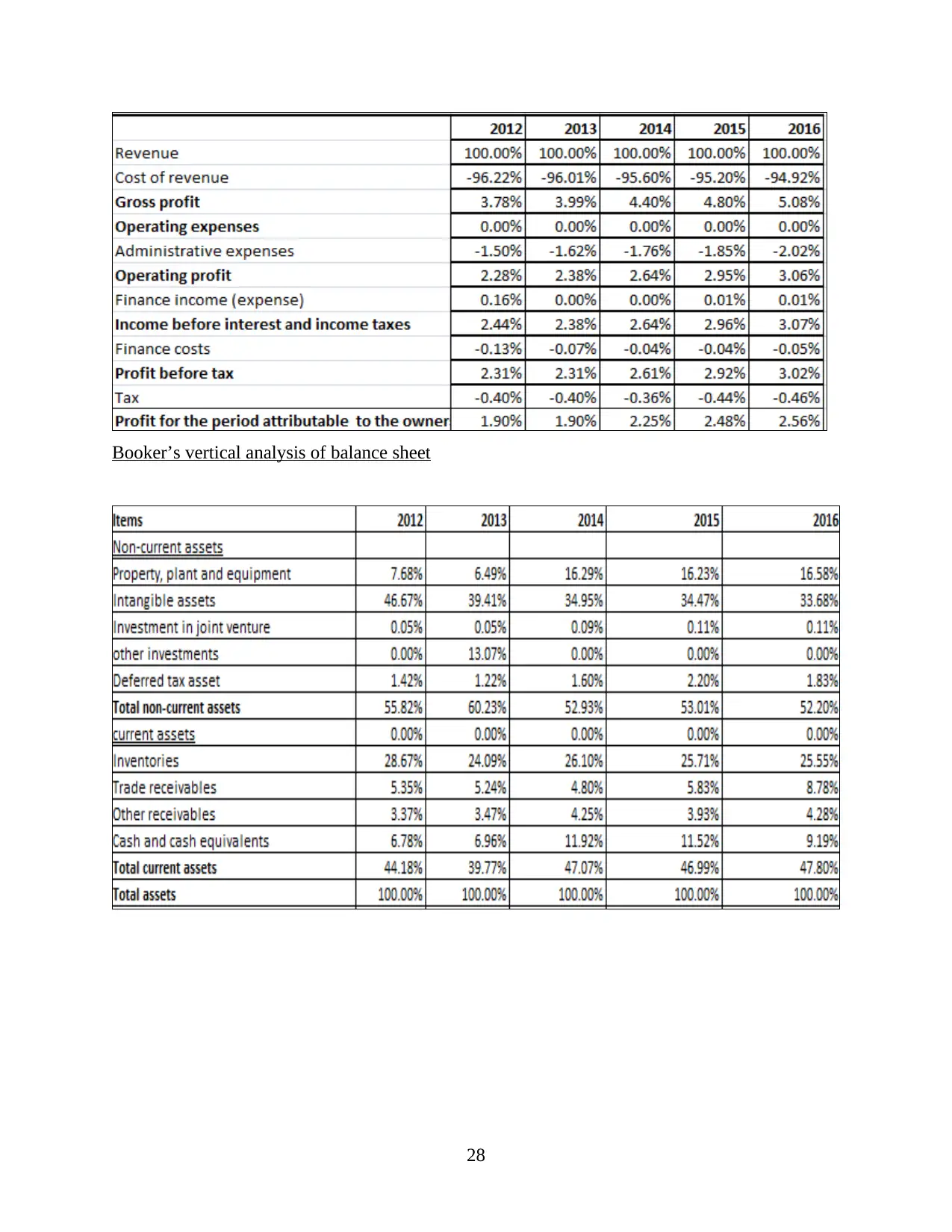

Booker’s vertical analysis of income statement...................................................................27

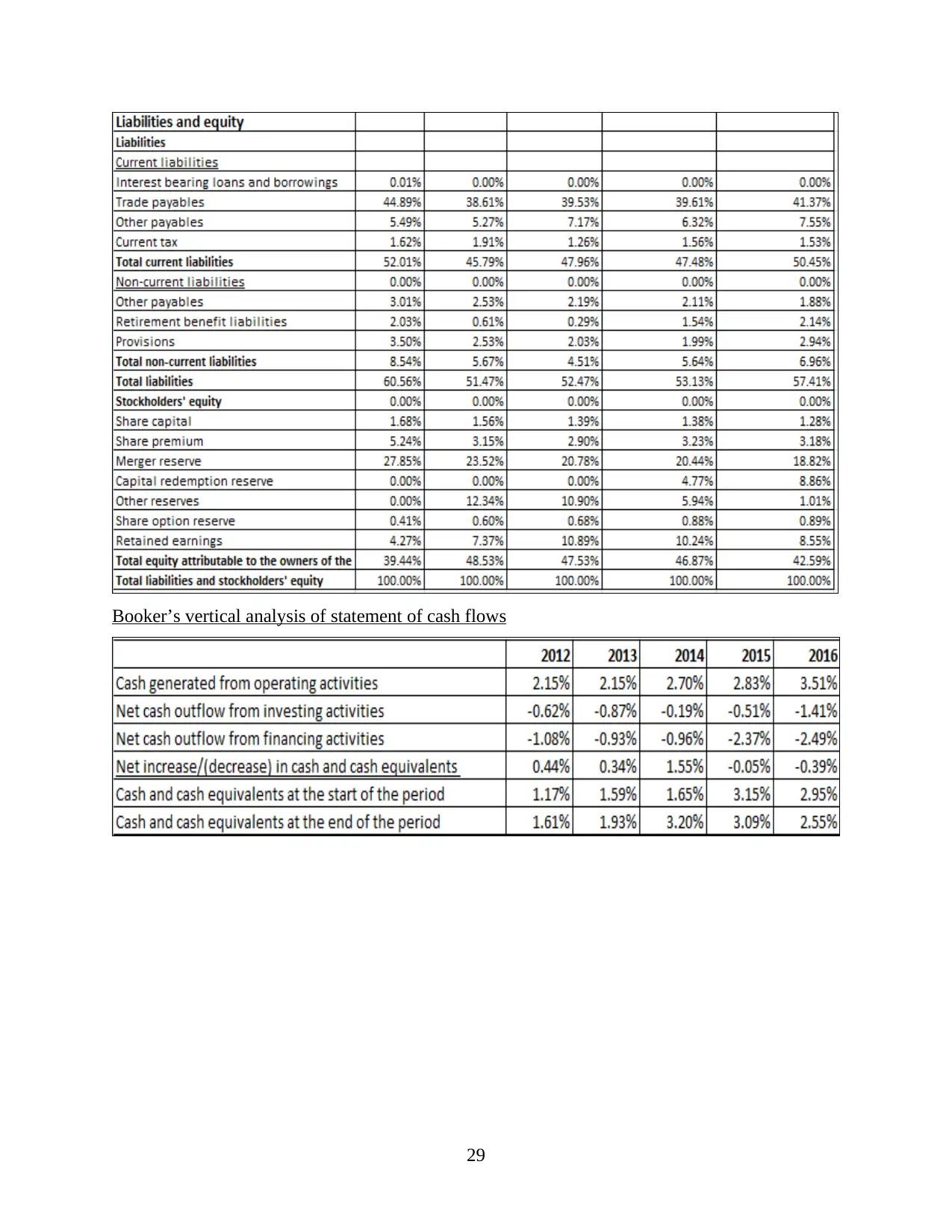

Booker’s vertical analysis of balance sheet..........................................................................28

Booker’s vertical analysis of statement of cash flows..........................................................29

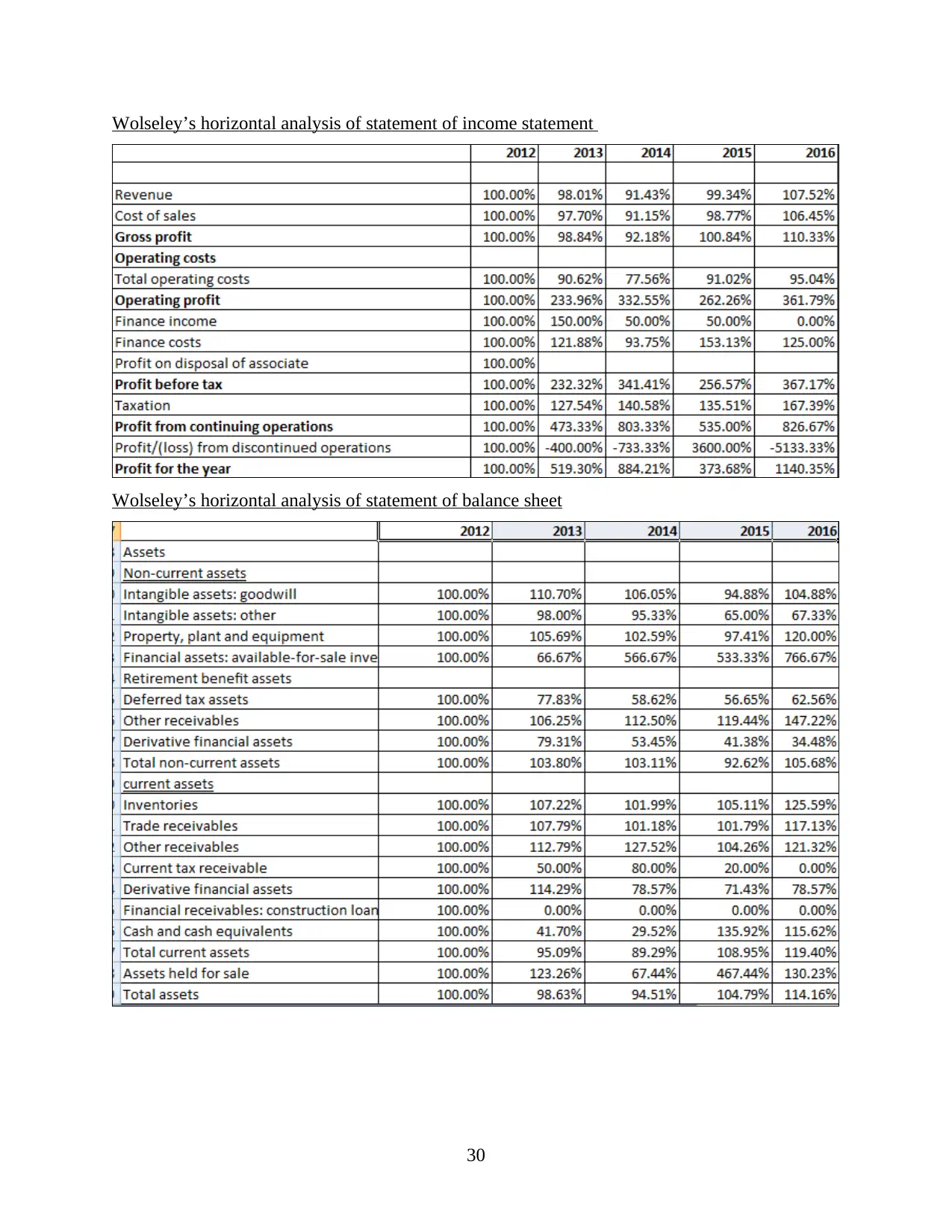

Wolseley’s horizontal analysis of statement of income statement.......................................30

Wolseley’s horizontal analysis of statement of balance sheet..............................................30

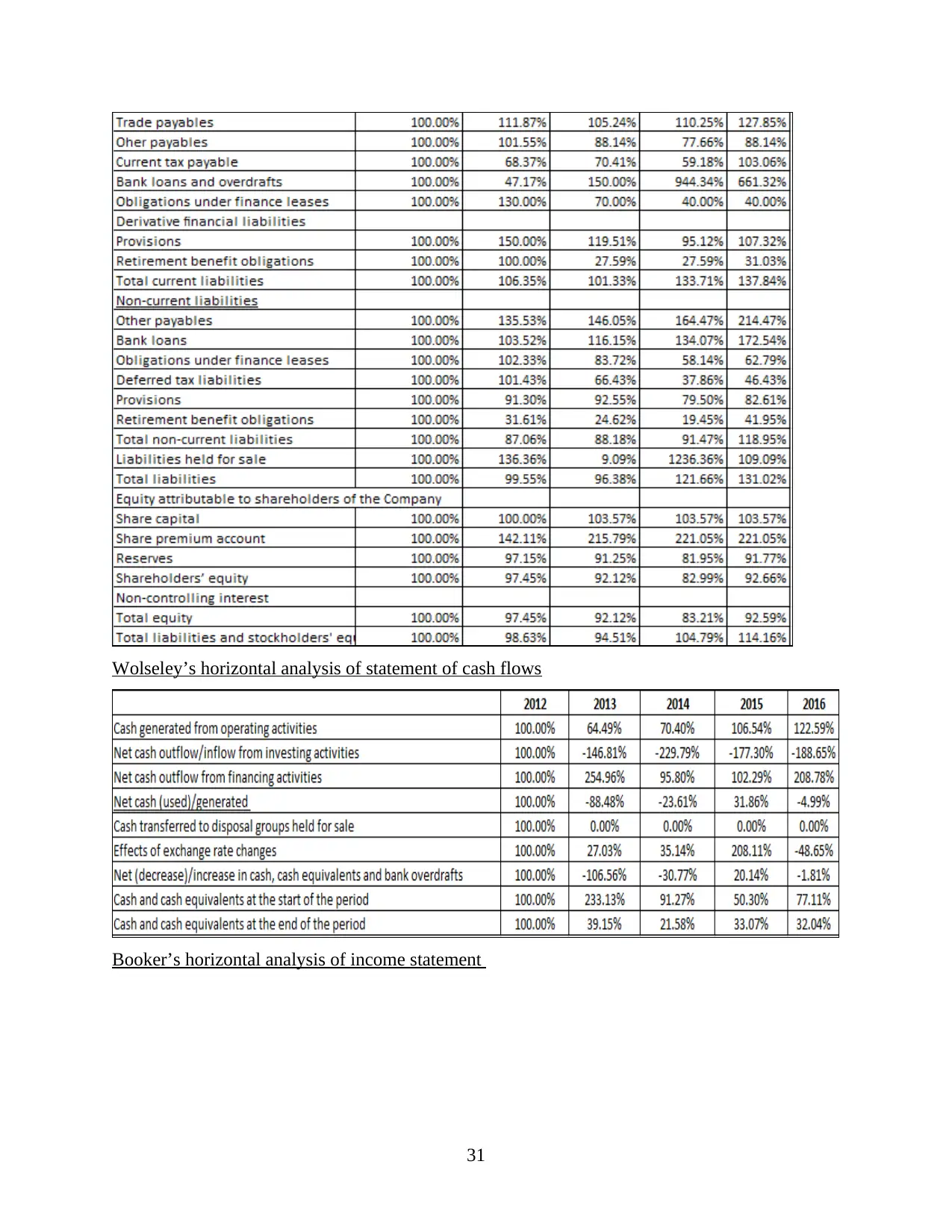

Wolseley’s horizontal analysis of statement of cash flows..................................................31

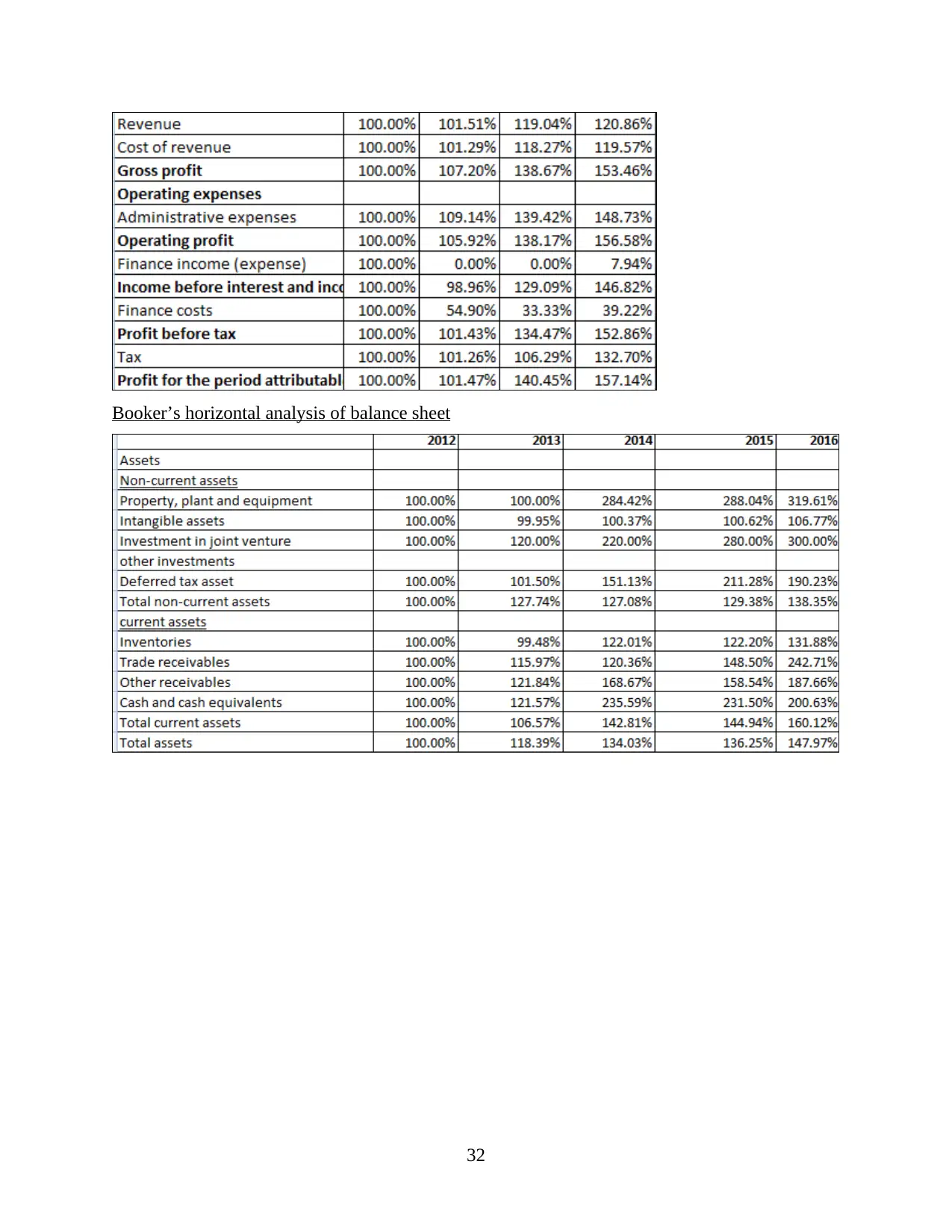

Booker’s horizontal analysis of income statement...............................................................31

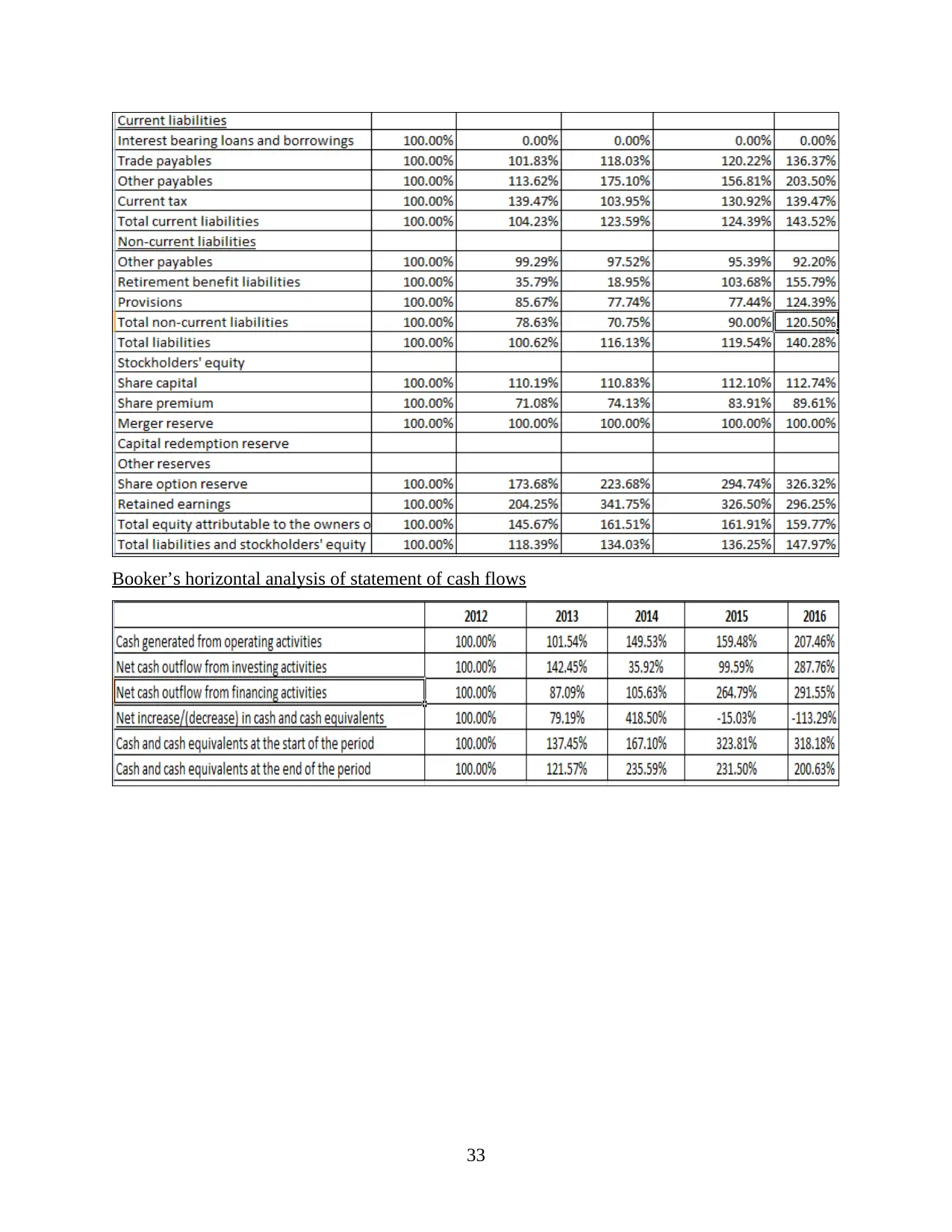

Booker’s horizontal analysis of balance sheet......................................................................32

Booker’s horizontal analysis of statement of cash flows.....................................................33

Wolseley’s vertical analysis of income statement................................................................25

Wolseley’s vertical analysis of balance sheet......................................................................25

Wolseley’s vertical analysis of cash flow statement............................................................27

Booker’s vertical analysis of income statement...................................................................27

Booker’s vertical analysis of balance sheet..........................................................................28

Booker’s vertical analysis of statement of cash flows..........................................................29

Wolseley’s horizontal analysis of statement of income statement.......................................30

Wolseley’s horizontal analysis of statement of balance sheet..............................................30

Wolseley’s horizontal analysis of statement of cash flows..................................................31

Booker’s horizontal analysis of income statement...............................................................31

Booker’s horizontal analysis of balance sheet......................................................................32

Booker’s horizontal analysis of statement of cash flows.....................................................33

INTRODUCTION

Strategic financial analysis and its importance

Strategic financial analysis (SFA) regards to the process of analyzing business financial

performance and thereby makes right decisions at the right time to drive success. There are

number of tools and techniques available to the entrepreneur such as ratio analysis, horizontal

and vertical analysis and many others. SFA is of utmost importance for the manager to determine

and assess their financial difficulties, so that, managers, directors and executives can make

qualitative decisions for accomplishing the defined targets and objectives.

Objectives

The report targeted at analysing the financial position and operational performance of two

existing companies, Wolseley and Booker. The report will make financial analysis of both the

companies by applying ratio analysis and horizontal as well as vertical analysis of all the

necessary financial accounts profitability statement, cash flow statement and balance sheet.

Moreover, it will also analyse the limitations of all the methods. Besides this, contemporary

techniques like Capital Assets pricing Model, Efficient Market Hypothesis and Economic Value

Added will be analysed that how these techniques can assist business to examine and evaluate

their success and operational excellence.

Overview of companies

Booker group is operating in food sector that offers variety of products and services to

buyers including grocers, restaurants and pub etc. Another organization is Wolseley deals in the

construction of buildings.

Methods of analysis

Ratio analysis will be used to determine relationship between various elements of

financial statement. However, horizontal analysis will be used to examine volatility trend over

the years whereas vertical analysis technique will be incorporated to determine the relationship

of each and every element from the revenues and total assets. Besides this, Du-pont model and

segmental reports will be prepared for in-depth analysis of business performance.

RATIO ANALYSIS

Ratio analysis may be defined as a tool which helps in analyzing the financial statements

of the business organization in an effectual way. By this, financial health, performance and

position of the firm can be measured in against to the competitor. Besides this, by evaluating the

1

Strategic financial analysis and its importance

Strategic financial analysis (SFA) regards to the process of analyzing business financial

performance and thereby makes right decisions at the right time to drive success. There are

number of tools and techniques available to the entrepreneur such as ratio analysis, horizontal

and vertical analysis and many others. SFA is of utmost importance for the manager to determine

and assess their financial difficulties, so that, managers, directors and executives can make

qualitative decisions for accomplishing the defined targets and objectives.

Objectives

The report targeted at analysing the financial position and operational performance of two

existing companies, Wolseley and Booker. The report will make financial analysis of both the

companies by applying ratio analysis and horizontal as well as vertical analysis of all the

necessary financial accounts profitability statement, cash flow statement and balance sheet.

Moreover, it will also analyse the limitations of all the methods. Besides this, contemporary

techniques like Capital Assets pricing Model, Efficient Market Hypothesis and Economic Value

Added will be analysed that how these techniques can assist business to examine and evaluate

their success and operational excellence.

Overview of companies

Booker group is operating in food sector that offers variety of products and services to

buyers including grocers, restaurants and pub etc. Another organization is Wolseley deals in the

construction of buildings.

Methods of analysis

Ratio analysis will be used to determine relationship between various elements of

financial statement. However, horizontal analysis will be used to examine volatility trend over

the years whereas vertical analysis technique will be incorporated to determine the relationship

of each and every element from the revenues and total assets. Besides this, Du-pont model and

segmental reports will be prepared for in-depth analysis of business performance.

RATIO ANALYSIS

Ratio analysis may be defined as a tool which helps in analyzing the financial statements

of the business organization in an effectual way. By this, financial health, performance and

position of the firm can be measured in against to the competitor. Besides this, by evaluating the

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

own performance in against to the competitors business unit can take suitable decision for the

improvement purposs (Xu and et.al., 2014). The ratio analysis includes different types of ratios

by which analyser can interpret about the financial position of company. The different ratios are

such as Profitability, liquidity, efficiency, solvency, gearing etc.

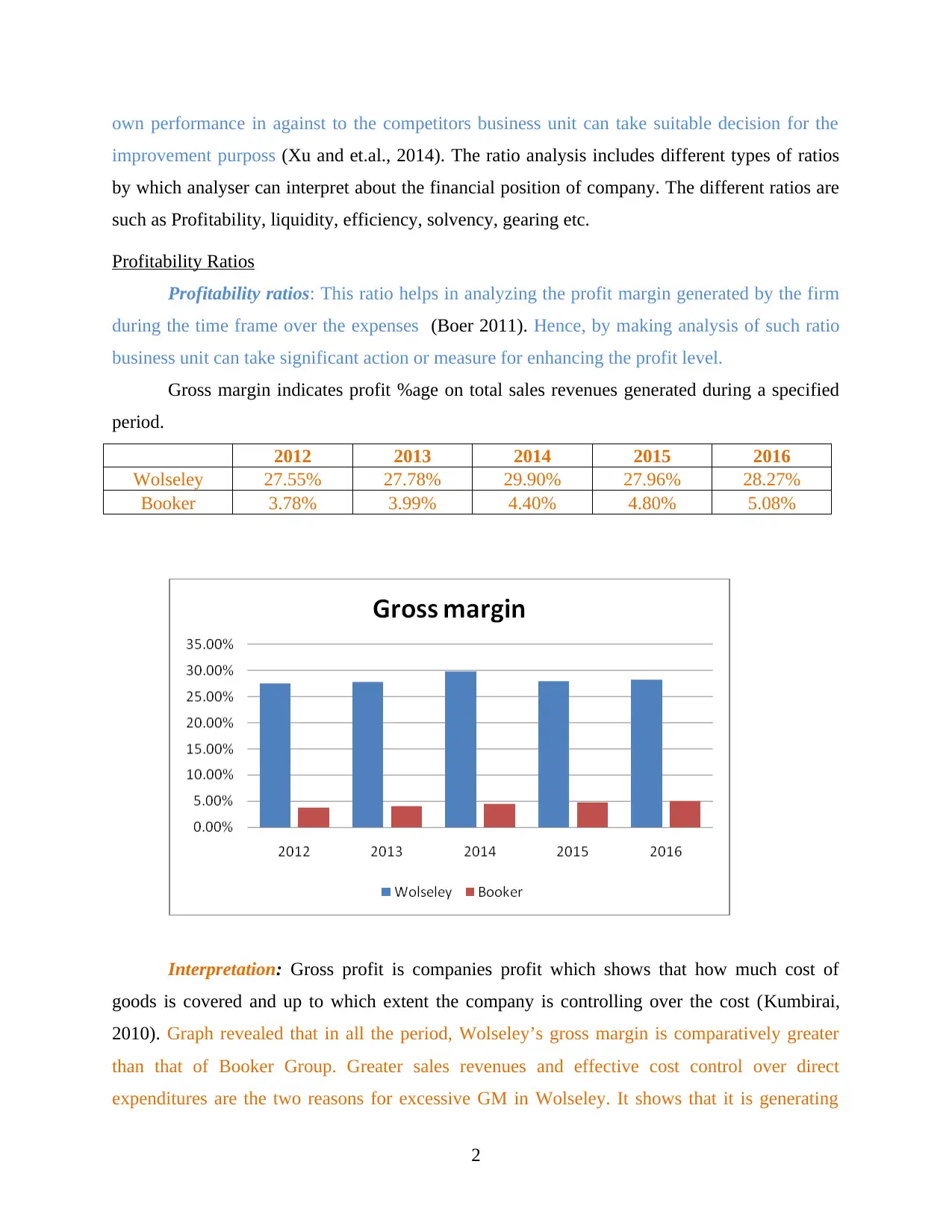

Profitability Ratios

Profitability ratios: This ratio helps in analyzing the profit margin generated by the firm

during the time frame over the expenses (Boer 2011). Hence, by making analysis of such ratio

business unit can take significant action or measure for enhancing the profit level.

Gross margin indicates profit %age on total sales revenues generated during a specified

period.

2012 2013 2014 2015 2016

Wolseley 27.55% 27.78% 29.90% 27.96% 28.27%

Booker 3.78% 3.99% 4.40% 4.80% 5.08%

Interpretation: Gross profit is companies profit which shows that how much cost of

goods is covered and up to which extent the company is controlling over the cost (Kumbirai,

2010). Graph revealed that in all the period, Wolseley’s gross margin is comparatively greater

than that of Booker Group. Greater sales revenues and effective cost control over direct

expenditures are the two reasons for excessive GM in Wolseley. It shows that it is generating

2

improvement purposs (Xu and et.al., 2014). The ratio analysis includes different types of ratios

by which analyser can interpret about the financial position of company. The different ratios are

such as Profitability, liquidity, efficiency, solvency, gearing etc.

Profitability Ratios

Profitability ratios: This ratio helps in analyzing the profit margin generated by the firm

during the time frame over the expenses (Boer 2011). Hence, by making analysis of such ratio

business unit can take significant action or measure for enhancing the profit level.

Gross margin indicates profit %age on total sales revenues generated during a specified

period.

2012 2013 2014 2015 2016

Wolseley 27.55% 27.78% 29.90% 27.96% 28.27%

Booker 3.78% 3.99% 4.40% 4.80% 5.08%

Interpretation: Gross profit is companies profit which shows that how much cost of

goods is covered and up to which extent the company is controlling over the cost (Kumbirai,

2010). Graph revealed that in all the period, Wolseley’s gross margin is comparatively greater

than that of Booker Group. Greater sales revenues and effective cost control over direct

expenditures are the two reasons for excessive GM in Wolseley. It shows that it is generating

2

enough return on their turnover and performing excellent than Booker. In the year 2016,

Wolseley’s GM is 28.27% whilst in case of Booker, it is only 5.08% represent that first company

is performing better as it is generating higher return through adding a mark-up on cost of sale.

Thus, business unit needs to make effort in relation to enhancing the sales level through the

means of advertisement.

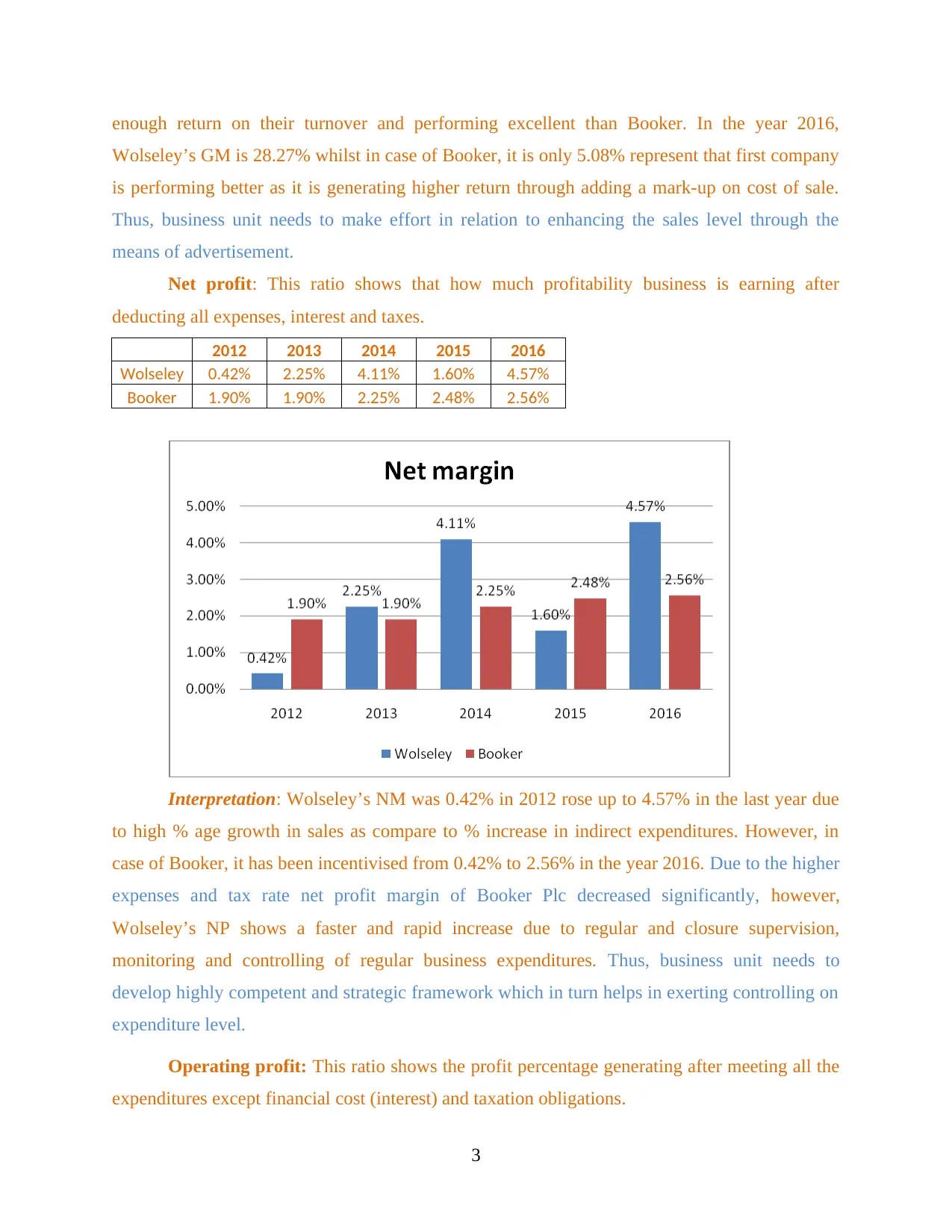

Net profit: This ratio shows that how much profitability business is earning after

deducting all expenses, interest and taxes.

2012 2013 2014 2015 2016

Wolseley 0.42% 2.25% 4.11% 1.60% 4.57%

Booker 1.90% 1.90% 2.25% 2.48% 2.56%

Interpretation: Wolseley’s NM was 0.42% in 2012 rose up to 4.57% in the last year due

to high % age growth in sales as compare to % increase in indirect expenditures. However, in

case of Booker, it has been incentivised from 0.42% to 2.56% in the year 2016. Due to the higher

expenses and tax rate net profit margin of Booker Plc decreased significantly, however,

Wolseley’s NP shows a faster and rapid increase due to regular and closure supervision,

monitoring and controlling of regular business expenditures. Thus, business unit needs to

develop highly competent and strategic framework which in turn helps in exerting controlling on

expenditure level.

Operating profit: This ratio shows the profit percentage generating after meeting all the

expenditures except financial cost (interest) and taxation obligations.

3

Wolseley’s GM is 28.27% whilst in case of Booker, it is only 5.08% represent that first company

is performing better as it is generating higher return through adding a mark-up on cost of sale.

Thus, business unit needs to make effort in relation to enhancing the sales level through the

means of advertisement.

Net profit: This ratio shows that how much profitability business is earning after

deducting all expenses, interest and taxes.

2012 2013 2014 2015 2016

Wolseley 0.42% 2.25% 4.11% 1.60% 4.57%

Booker 1.90% 1.90% 2.25% 2.48% 2.56%

Interpretation: Wolseley’s NM was 0.42% in 2012 rose up to 4.57% in the last year due

to high % age growth in sales as compare to % increase in indirect expenditures. However, in

case of Booker, it has been incentivised from 0.42% to 2.56% in the year 2016. Due to the higher

expenses and tax rate net profit margin of Booker Plc decreased significantly, however,

Wolseley’s NP shows a faster and rapid increase due to regular and closure supervision,

monitoring and controlling of regular business expenditures. Thus, business unit needs to

develop highly competent and strategic framework which in turn helps in exerting controlling on

expenditure level.

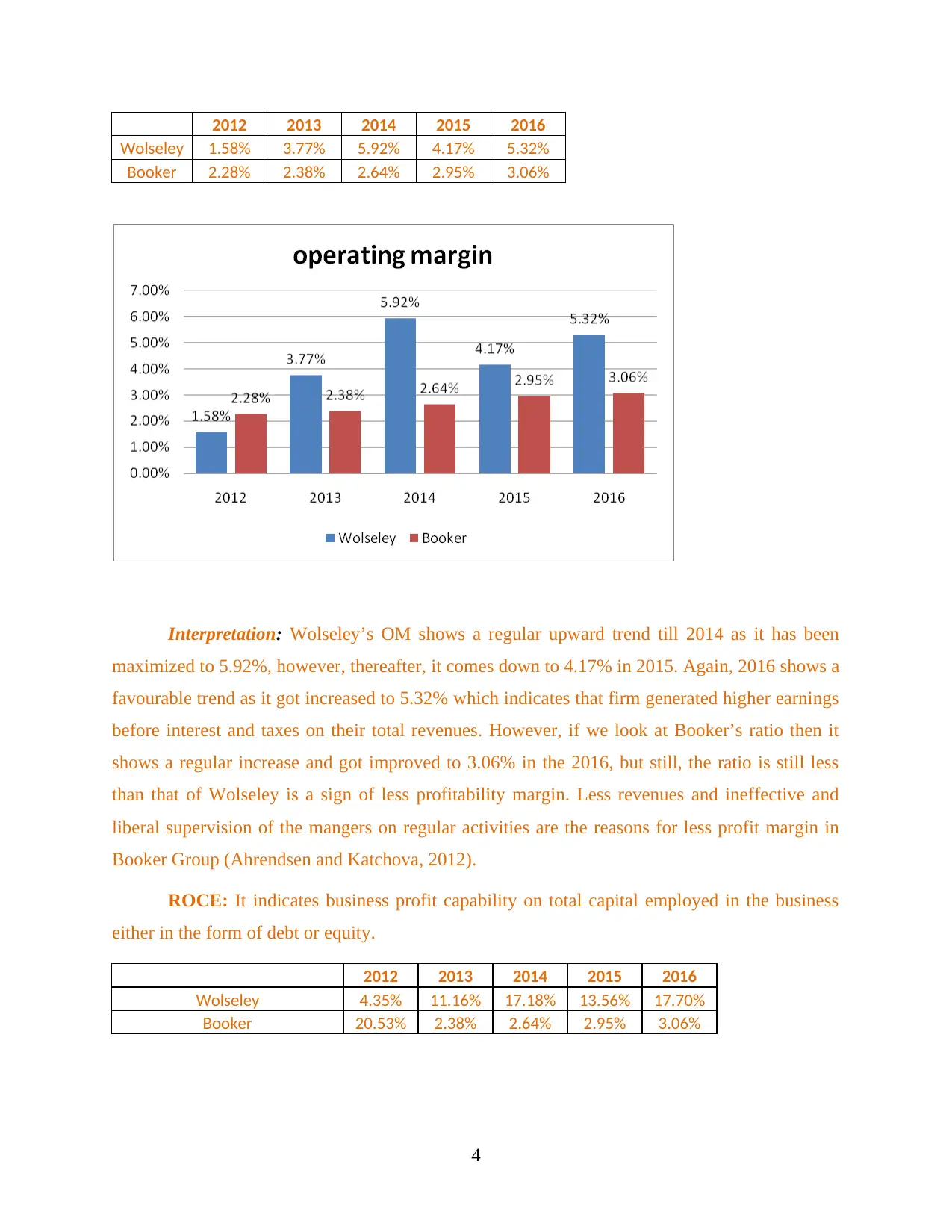

Operating profit: This ratio shows the profit percentage generating after meeting all the

expenditures except financial cost (interest) and taxation obligations.

3

2012 2013 2014 2015 2016

Wolseley 1.58% 3.77% 5.92% 4.17% 5.32%

Booker 2.28% 2.38% 2.64% 2.95% 3.06%

Interpretation: Wolseley’s OM shows a regular upward trend till 2014 as it has been

maximized to 5.92%, however, thereafter, it comes down to 4.17% in 2015. Again, 2016 shows a

favourable trend as it got increased to 5.32% which indicates that firm generated higher earnings

before interest and taxes on their total revenues. However, if we look at Booker’s ratio then it

shows a regular increase and got improved to 3.06% in the 2016, but still, the ratio is still less

than that of Wolseley is a sign of less profitability margin. Less revenues and ineffective and

liberal supervision of the mangers on regular activities are the reasons for less profit margin in

Booker Group (Ahrendsen and Katchova, 2012).

ROCE: It indicates business profit capability on total capital employed in the business

either in the form of debt or equity.

2012 2013 2014 2015 2016

Wolseley 4.35% 11.16% 17.18% 13.56% 17.70%

Booker 20.53% 2.38% 2.64% 2.95% 3.06%

4

Wolseley 1.58% 3.77% 5.92% 4.17% 5.32%

Booker 2.28% 2.38% 2.64% 2.95% 3.06%

Interpretation: Wolseley’s OM shows a regular upward trend till 2014 as it has been

maximized to 5.92%, however, thereafter, it comes down to 4.17% in 2015. Again, 2016 shows a

favourable trend as it got increased to 5.32% which indicates that firm generated higher earnings

before interest and taxes on their total revenues. However, if we look at Booker’s ratio then it

shows a regular increase and got improved to 3.06% in the 2016, but still, the ratio is still less

than that of Wolseley is a sign of less profitability margin. Less revenues and ineffective and

liberal supervision of the mangers on regular activities are the reasons for less profit margin in

Booker Group (Ahrendsen and Katchova, 2012).

ROCE: It indicates business profit capability on total capital employed in the business

either in the form of debt or equity.

2012 2013 2014 2015 2016

Wolseley 4.35% 11.16% 17.18% 13.56% 17.70%

Booker 20.53% 2.38% 2.64% 2.95% 3.06%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

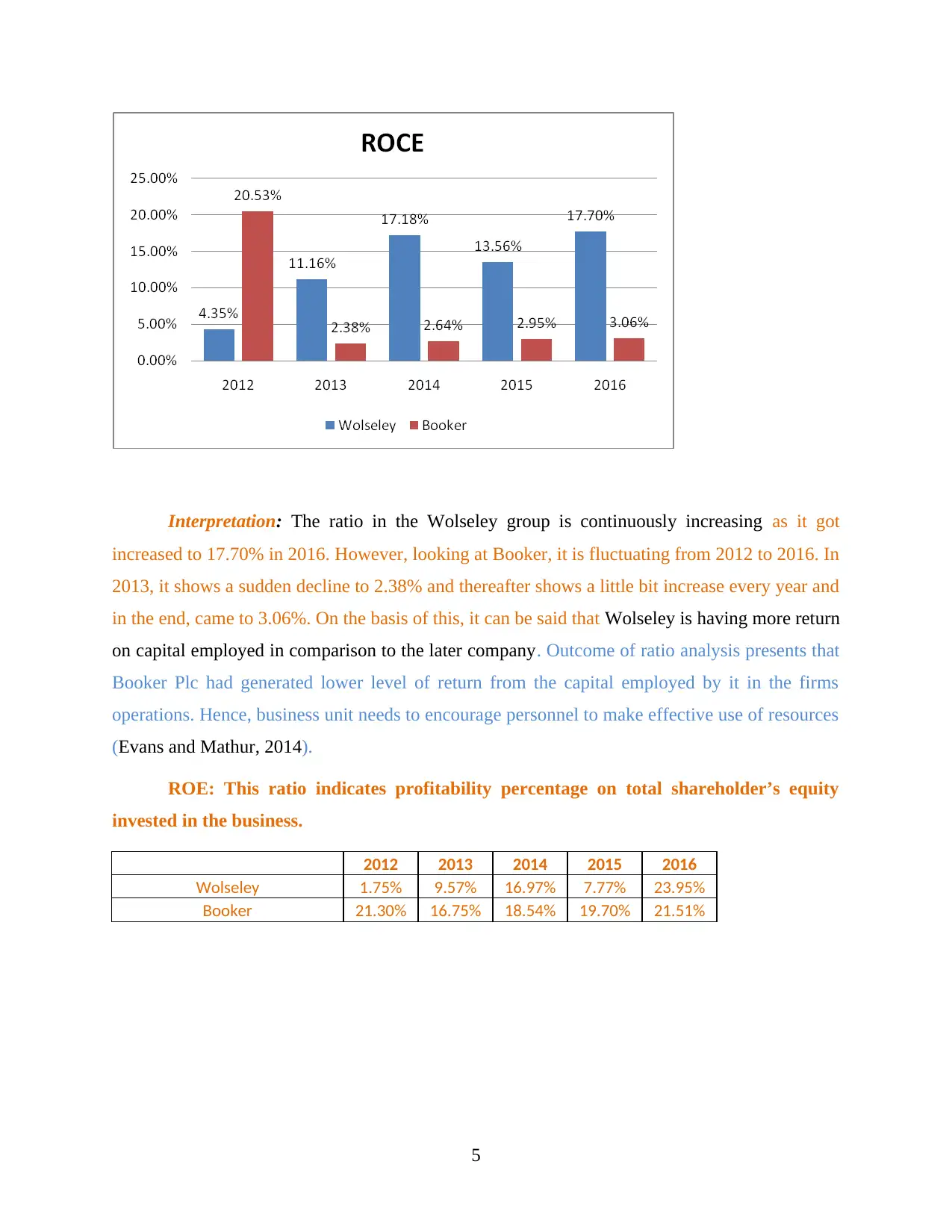

Interpretation: The ratio in the Wolseley group is continuously increasing as it got

increased to 17.70% in 2016. However, looking at Booker, it is fluctuating from 2012 to 2016. In

2013, it shows a sudden decline to 2.38% and thereafter shows a little bit increase every year and

in the end, came to 3.06%. On the basis of this, it can be said that Wolseley is having more return

on capital employed in comparison to the later company. Outcome of ratio analysis presents that

Booker Plc had generated lower level of return from the capital employed by it in the firms

operations. Hence, business unit needs to encourage personnel to make effective use of resources

(Evans and Mathur, 2014).

ROE: This ratio indicates profitability percentage on total shareholder’s equity

invested in the business.

2012 2013 2014 2015 2016

Wolseley 1.75% 9.57% 16.97% 7.77% 23.95%

Booker 21.30% 16.75% 18.54% 19.70% 21.51%

5

increased to 17.70% in 2016. However, looking at Booker, it is fluctuating from 2012 to 2016. In

2013, it shows a sudden decline to 2.38% and thereafter shows a little bit increase every year and

in the end, came to 3.06%. On the basis of this, it can be said that Wolseley is having more return

on capital employed in comparison to the later company. Outcome of ratio analysis presents that

Booker Plc had generated lower level of return from the capital employed by it in the firms

operations. Hence, business unit needs to encourage personnel to make effective use of resources

(Evans and Mathur, 2014).

ROE: This ratio indicates profitability percentage on total shareholder’s equity

invested in the business.

2012 2013 2014 2015 2016

Wolseley 1.75% 9.57% 16.97% 7.77% 23.95%

Booker 21.30% 16.75% 18.54% 19.70% 21.51%

5

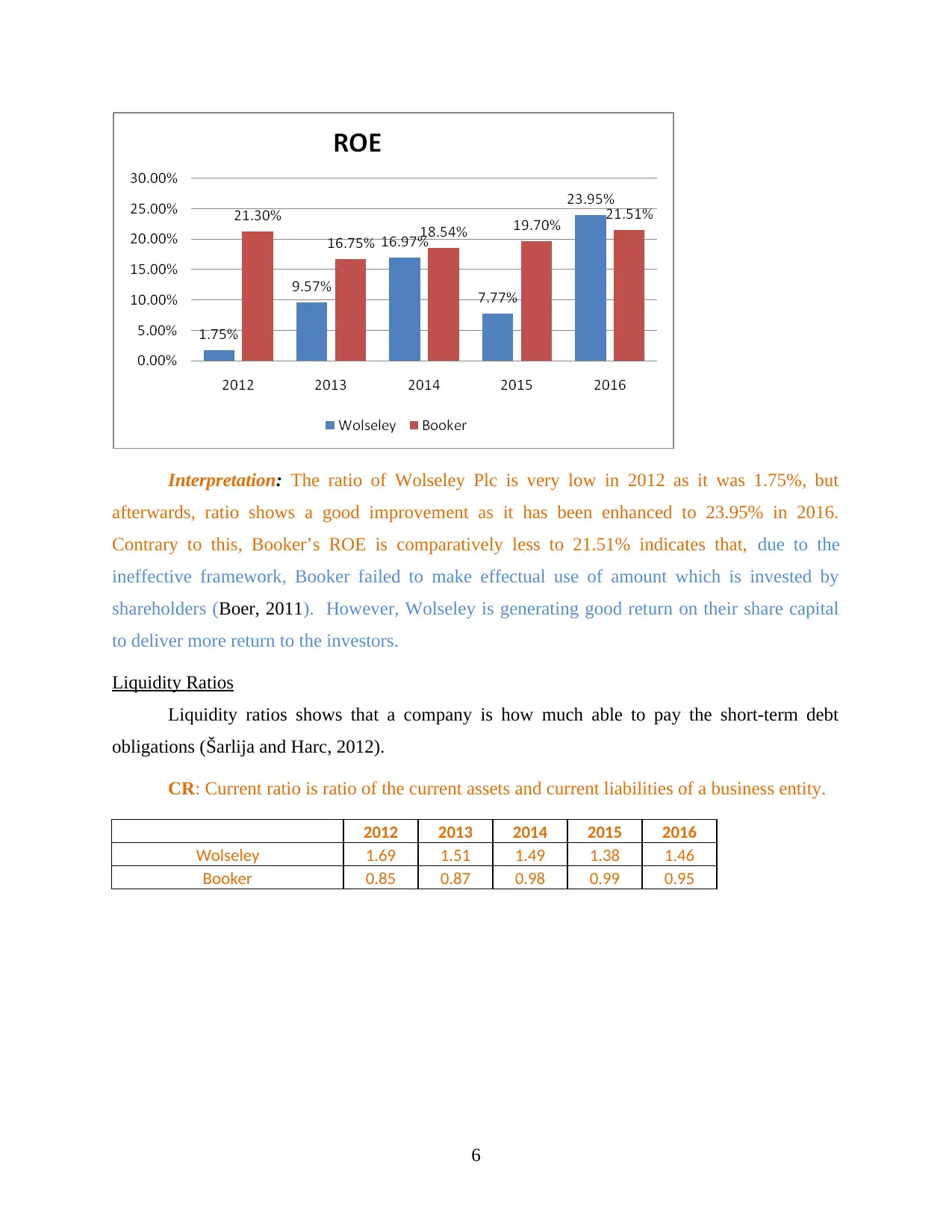

Interpretation: The ratio of Wolseley Plc is very low in 2012 as it was 1.75%, but

afterwards, ratio shows a good improvement as it has been enhanced to 23.95% in 2016.

Contrary to this, Booker’s ROE is comparatively less to 21.51% indicates that, due to the

ineffective framework, Booker failed to make effectual use of amount which is invested by

shareholders (Boer, 2011). However, Wolseley is generating good return on their share capital

to deliver more return to the investors.

Liquidity Ratios

Liquidity ratios shows that a company is how much able to pay the short-term debt

obligations (Šarlija and Harc, 2012).

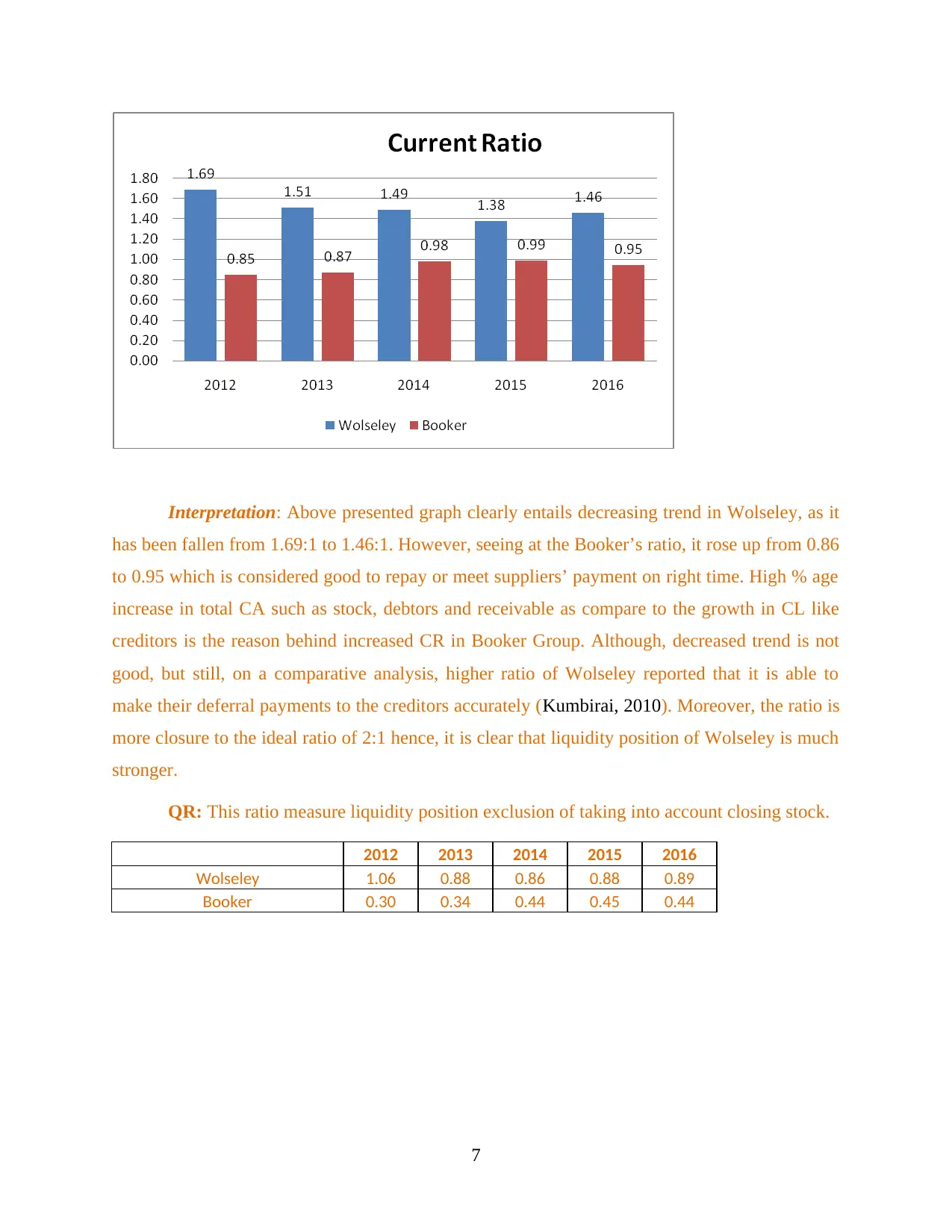

CR: Current ratio is ratio of the current assets and current liabilities of a business entity.

2012 2013 2014 2015 2016

Wolseley 1.69 1.51 1.49 1.38 1.46

Booker 0.85 0.87 0.98 0.99 0.95

6

afterwards, ratio shows a good improvement as it has been enhanced to 23.95% in 2016.

Contrary to this, Booker’s ROE is comparatively less to 21.51% indicates that, due to the

ineffective framework, Booker failed to make effectual use of amount which is invested by

shareholders (Boer, 2011). However, Wolseley is generating good return on their share capital

to deliver more return to the investors.

Liquidity Ratios

Liquidity ratios shows that a company is how much able to pay the short-term debt

obligations (Šarlija and Harc, 2012).

CR: Current ratio is ratio of the current assets and current liabilities of a business entity.

2012 2013 2014 2015 2016

Wolseley 1.69 1.51 1.49 1.38 1.46

Booker 0.85 0.87 0.98 0.99 0.95

6

Interpretation: Above presented graph clearly entails decreasing trend in Wolseley, as it

has been fallen from 1.69:1 to 1.46:1. However, seeing at the Booker’s ratio, it rose up from 0.86

to 0.95 which is considered good to repay or meet suppliers’ payment on right time. High % age

increase in total CA such as stock, debtors and receivable as compare to the growth in CL like

creditors is the reason behind increased CR in Booker Group. Although, decreased trend is not

good, but still, on a comparative analysis, higher ratio of Wolseley reported that it is able to

make their deferral payments to the creditors accurately (Kumbirai, 2010). Moreover, the ratio is

more closure to the ideal ratio of 2:1 hence, it is clear that liquidity position of Wolseley is much

stronger.

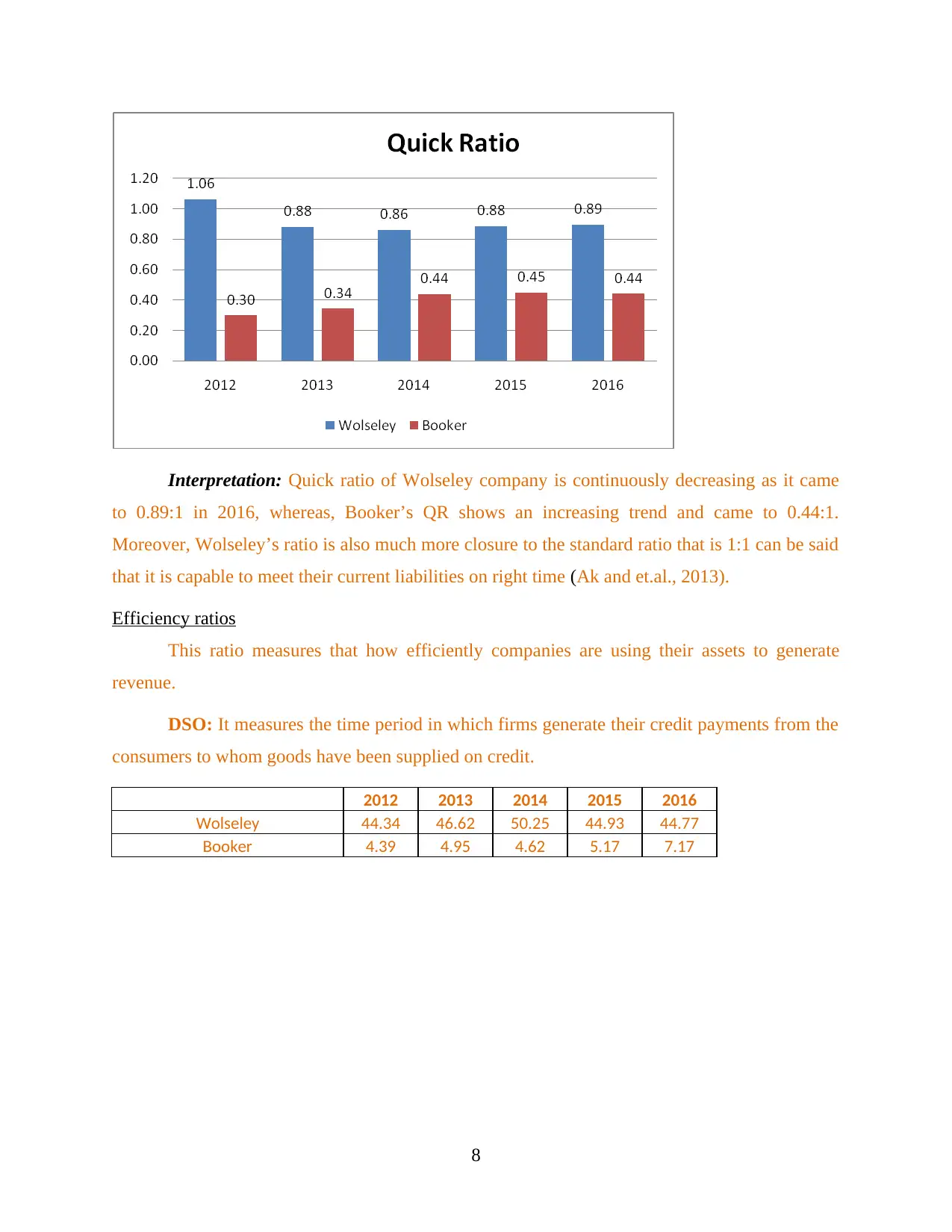

QR: This ratio measure liquidity position exclusion of taking into account closing stock.

2012 2013 2014 2015 2016

Wolseley 1.06 0.88 0.86 0.88 0.89

Booker 0.30 0.34 0.44 0.45 0.44

7

has been fallen from 1.69:1 to 1.46:1. However, seeing at the Booker’s ratio, it rose up from 0.86

to 0.95 which is considered good to repay or meet suppliers’ payment on right time. High % age

increase in total CA such as stock, debtors and receivable as compare to the growth in CL like

creditors is the reason behind increased CR in Booker Group. Although, decreased trend is not

good, but still, on a comparative analysis, higher ratio of Wolseley reported that it is able to

make their deferral payments to the creditors accurately (Kumbirai, 2010). Moreover, the ratio is

more closure to the ideal ratio of 2:1 hence, it is clear that liquidity position of Wolseley is much

stronger.

QR: This ratio measure liquidity position exclusion of taking into account closing stock.

2012 2013 2014 2015 2016

Wolseley 1.06 0.88 0.86 0.88 0.89

Booker 0.30 0.34 0.44 0.45 0.44

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Interpretation: Quick ratio of Wolseley company is continuously decreasing as it came

to 0.89:1 in 2016, whereas, Booker’s QR shows an increasing trend and came to 0.44:1.

Moreover, Wolseley’s ratio is also much more closure to the standard ratio that is 1:1 can be said

that it is capable to meet their current liabilities on right time (Ak and et.al., 2013).

Efficiency ratios

This ratio measures that how efficiently companies are using their assets to generate

revenue.

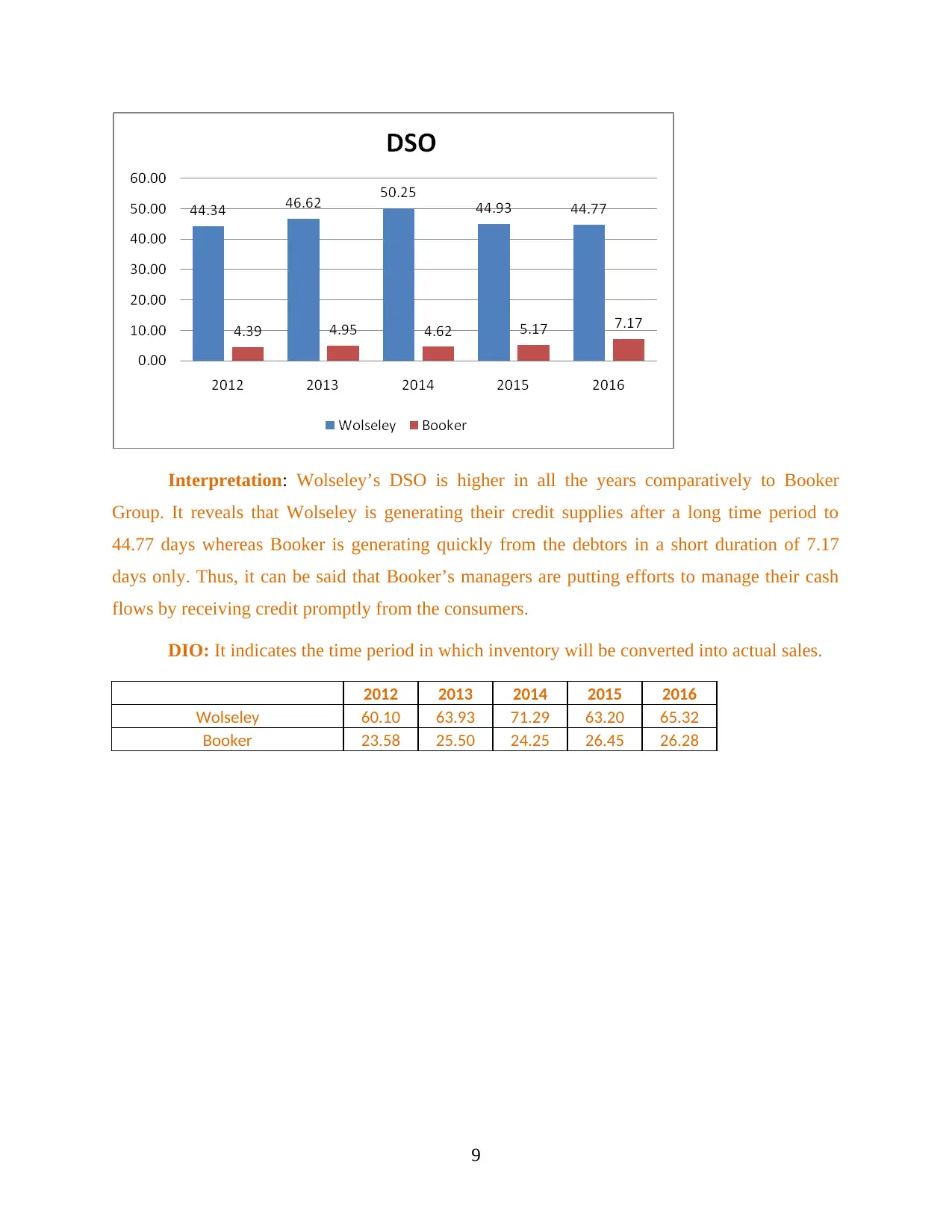

DSO: It measures the time period in which firms generate their credit payments from the

consumers to whom goods have been supplied on credit.

2012 2013 2014 2015 2016

Wolseley 44.34 46.62 50.25 44.93 44.77

Booker 4.39 4.95 4.62 5.17 7.17

8

to 0.89:1 in 2016, whereas, Booker’s QR shows an increasing trend and came to 0.44:1.

Moreover, Wolseley’s ratio is also much more closure to the standard ratio that is 1:1 can be said

that it is capable to meet their current liabilities on right time (Ak and et.al., 2013).

Efficiency ratios

This ratio measures that how efficiently companies are using their assets to generate

revenue.

DSO: It measures the time period in which firms generate their credit payments from the

consumers to whom goods have been supplied on credit.

2012 2013 2014 2015 2016

Wolseley 44.34 46.62 50.25 44.93 44.77

Booker 4.39 4.95 4.62 5.17 7.17

8

Interpretation: Wolseley’s DSO is higher in all the years comparatively to Booker

Group. It reveals that Wolseley is generating their credit supplies after a long time period to

44.77 days whereas Booker is generating quickly from the debtors in a short duration of 7.17

days only. Thus, it can be said that Booker’s managers are putting efforts to manage their cash

flows by receiving credit promptly from the consumers.

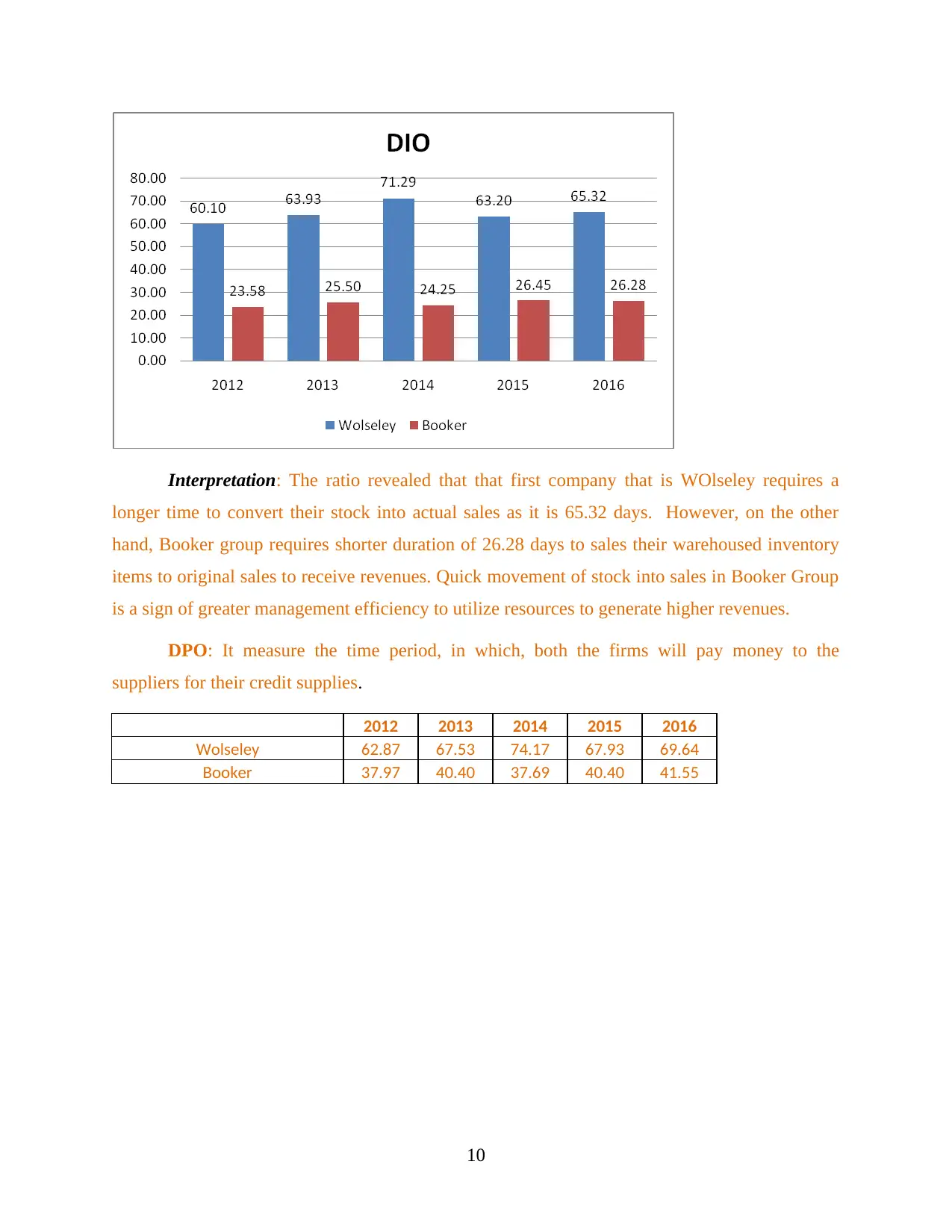

DIO: It indicates the time period in which inventory will be converted into actual sales.

2012 2013 2014 2015 2016

Wolseley 60.10 63.93 71.29 63.20 65.32

Booker 23.58 25.50 24.25 26.45 26.28

9

Group. It reveals that Wolseley is generating their credit supplies after a long time period to

44.77 days whereas Booker is generating quickly from the debtors in a short duration of 7.17

days only. Thus, it can be said that Booker’s managers are putting efforts to manage their cash

flows by receiving credit promptly from the consumers.

DIO: It indicates the time period in which inventory will be converted into actual sales.

2012 2013 2014 2015 2016

Wolseley 60.10 63.93 71.29 63.20 65.32

Booker 23.58 25.50 24.25 26.45 26.28

9

Interpretation: The ratio revealed that that first company that is WOlseley requires a

longer time to convert their stock into actual sales as it is 65.32 days. However, on the other

hand, Booker group requires shorter duration of 26.28 days to sales their warehoused inventory

items to original sales to receive revenues. Quick movement of stock into sales in Booker Group

is a sign of greater management efficiency to utilize resources to generate higher revenues.

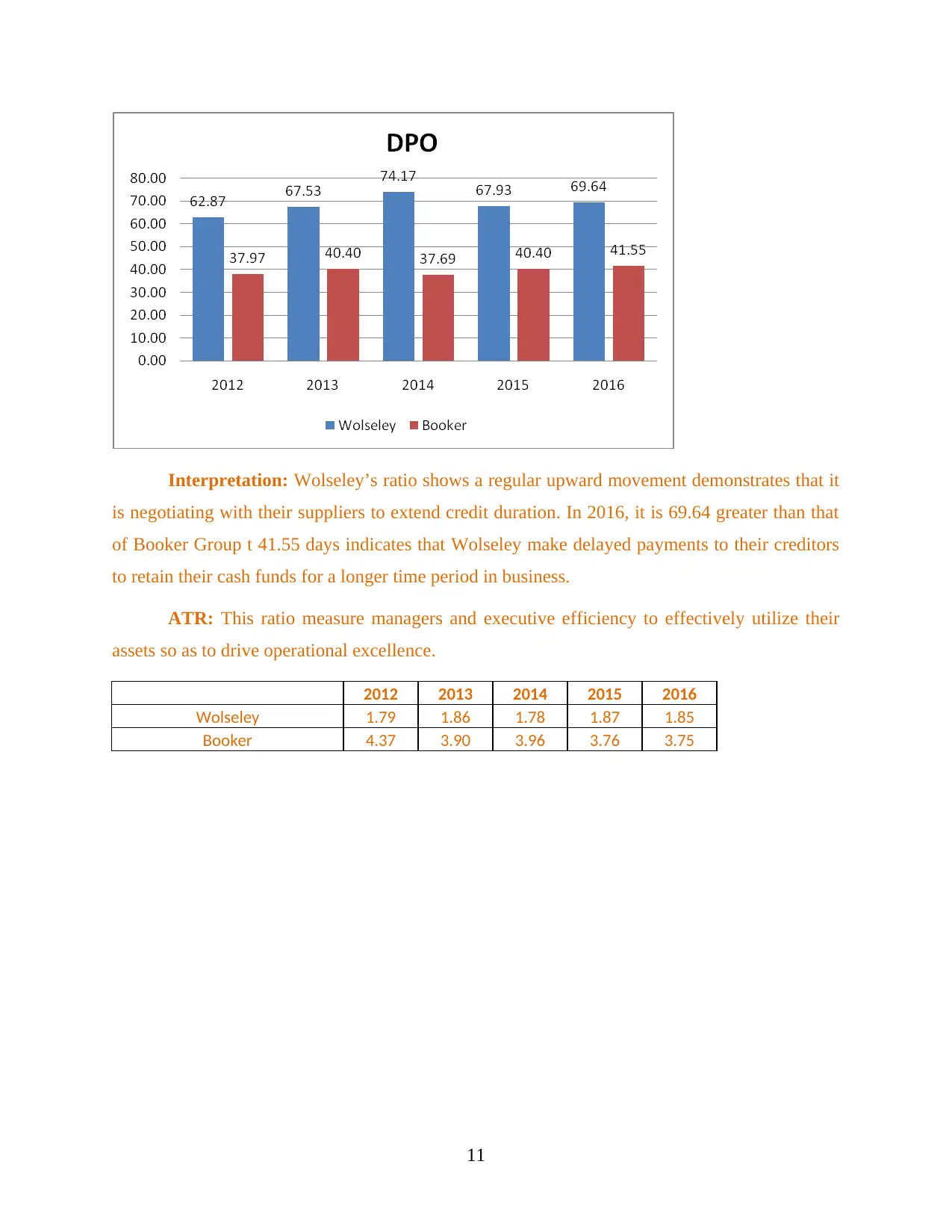

DPO: It measure the time period, in which, both the firms will pay money to the

suppliers for their credit supplies.

2012 2013 2014 2015 2016

Wolseley 62.87 67.53 74.17 67.93 69.64

Booker 37.97 40.40 37.69 40.40 41.55

10

longer time to convert their stock into actual sales as it is 65.32 days. However, on the other

hand, Booker group requires shorter duration of 26.28 days to sales their warehoused inventory

items to original sales to receive revenues. Quick movement of stock into sales in Booker Group

is a sign of greater management efficiency to utilize resources to generate higher revenues.

DPO: It measure the time period, in which, both the firms will pay money to the

suppliers for their credit supplies.

2012 2013 2014 2015 2016

Wolseley 62.87 67.53 74.17 67.93 69.64

Booker 37.97 40.40 37.69 40.40 41.55

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: Wolseley’s ratio shows a regular upward movement demonstrates that it

is negotiating with their suppliers to extend credit duration. In 2016, it is 69.64 greater than that

of Booker Group t 41.55 days indicates that Wolseley make delayed payments to their creditors

to retain their cash funds for a longer time period in business.

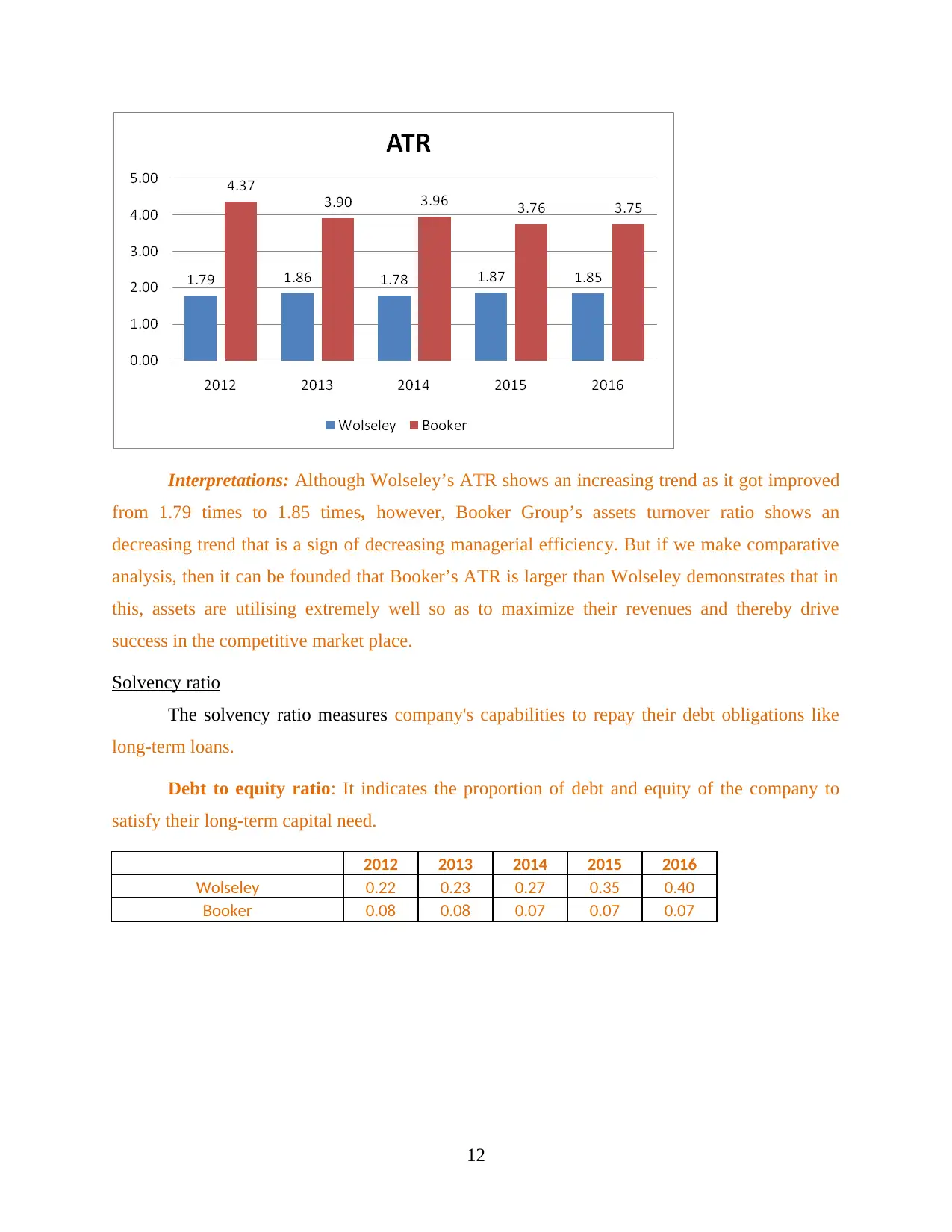

ATR: This ratio measure managers and executive efficiency to effectively utilize their

assets so as to drive operational excellence.

2012 2013 2014 2015 2016

Wolseley 1.79 1.86 1.78 1.87 1.85

Booker 4.37 3.90 3.96 3.76 3.75

11

is negotiating with their suppliers to extend credit duration. In 2016, it is 69.64 greater than that

of Booker Group t 41.55 days indicates that Wolseley make delayed payments to their creditors

to retain their cash funds for a longer time period in business.

ATR: This ratio measure managers and executive efficiency to effectively utilize their

assets so as to drive operational excellence.

2012 2013 2014 2015 2016

Wolseley 1.79 1.86 1.78 1.87 1.85

Booker 4.37 3.90 3.96 3.76 3.75

11

Interpretations: Although Wolseley’s ATR shows an increasing trend as it got improved

from 1.79 times to 1.85 times, however, Booker Group’s assets turnover ratio shows an

decreasing trend that is a sign of decreasing managerial efficiency. But if we make comparative

analysis, then it can be founded that Booker’s ATR is larger than Wolseley demonstrates that in

this, assets are utilising extremely well so as to maximize their revenues and thereby drive

success in the competitive market place.

Solvency ratio

The solvency ratio measures company's capabilities to repay their debt obligations like

long-term loans.

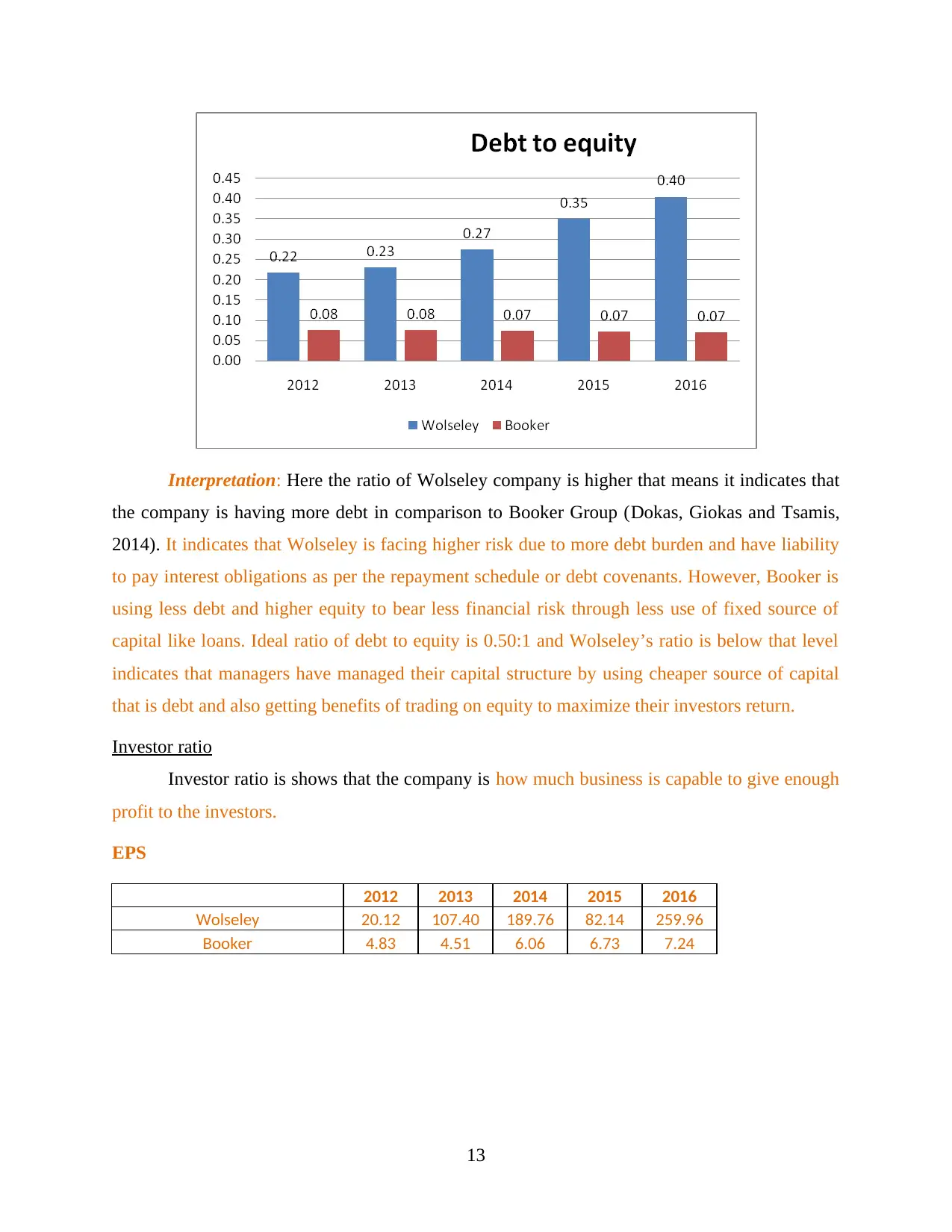

Debt to equity ratio: It indicates the proportion of debt and equity of the company to

satisfy their long-term capital need.

2012 2013 2014 2015 2016

Wolseley 0.22 0.23 0.27 0.35 0.40

Booker 0.08 0.08 0.07 0.07 0.07

12

from 1.79 times to 1.85 times, however, Booker Group’s assets turnover ratio shows an

decreasing trend that is a sign of decreasing managerial efficiency. But if we make comparative

analysis, then it can be founded that Booker’s ATR is larger than Wolseley demonstrates that in

this, assets are utilising extremely well so as to maximize their revenues and thereby drive

success in the competitive market place.

Solvency ratio

The solvency ratio measures company's capabilities to repay their debt obligations like

long-term loans.

Debt to equity ratio: It indicates the proportion of debt and equity of the company to

satisfy their long-term capital need.

2012 2013 2014 2015 2016

Wolseley 0.22 0.23 0.27 0.35 0.40

Booker 0.08 0.08 0.07 0.07 0.07

12

Interpretation: Here the ratio of Wolseley company is higher that means it indicates that

the company is having more debt in comparison to Booker Group (Dokas, Giokas and Tsamis,

2014). It indicates that Wolseley is facing higher risk due to more debt burden and have liability

to pay interest obligations as per the repayment schedule or debt covenants. However, Booker is

using less debt and higher equity to bear less financial risk through less use of fixed source of

capital like loans. Ideal ratio of debt to equity is 0.50:1 and Wolseley’s ratio is below that level

indicates that managers have managed their capital structure by using cheaper source of capital

that is debt and also getting benefits of trading on equity to maximize their investors return.

Investor ratio

Investor ratio is shows that the company is how much business is capable to give enough

profit to the investors.

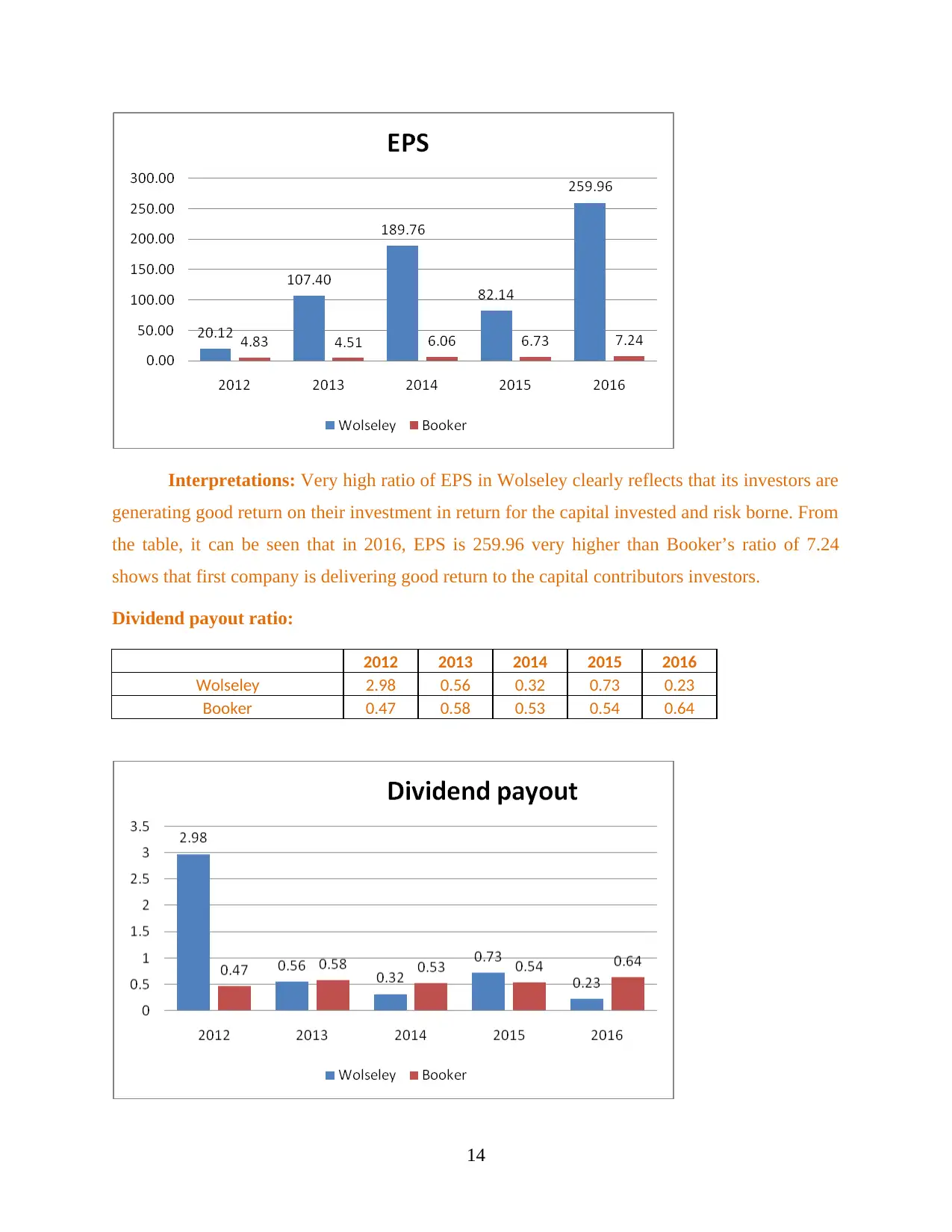

EPS

2012 2013 2014 2015 2016

Wolseley 20.12 107.40 189.76 82.14 259.96

Booker 4.83 4.51 6.06 6.73 7.24

13

the company is having more debt in comparison to Booker Group (Dokas, Giokas and Tsamis,

2014). It indicates that Wolseley is facing higher risk due to more debt burden and have liability

to pay interest obligations as per the repayment schedule or debt covenants. However, Booker is

using less debt and higher equity to bear less financial risk through less use of fixed source of

capital like loans. Ideal ratio of debt to equity is 0.50:1 and Wolseley’s ratio is below that level

indicates that managers have managed their capital structure by using cheaper source of capital

that is debt and also getting benefits of trading on equity to maximize their investors return.

Investor ratio

Investor ratio is shows that the company is how much business is capable to give enough

profit to the investors.

EPS

2012 2013 2014 2015 2016

Wolseley 20.12 107.40 189.76 82.14 259.96

Booker 4.83 4.51 6.06 6.73 7.24

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Interpretations: Very high ratio of EPS in Wolseley clearly reflects that its investors are

generating good return on their investment in return for the capital invested and risk borne. From

the table, it can be seen that in 2016, EPS is 259.96 very higher than Booker’s ratio of 7.24

shows that first company is delivering good return to the capital contributors investors.

Dividend payout ratio:

2012 2013 2014 2015 2016

Wolseley 2.98 0.56 0.32 0.73 0.23

Booker 0.47 0.58 0.53 0.54 0.64

14

generating good return on their investment in return for the capital invested and risk borne. From

the table, it can be seen that in 2016, EPS is 259.96 very higher than Booker’s ratio of 7.24

shows that first company is delivering good return to the capital contributors investors.

Dividend payout ratio:

2012 2013 2014 2015 2016

Wolseley 2.98 0.56 0.32 0.73 0.23

Booker 0.47 0.58 0.53 0.54 0.64

14

Interpretations: It shows a volatile and fluctuationg trend due to changing EPS and

DPS. In the year 2016, Wolseley’s ratio is 0.23 however, Booker’s ratio is 0.64 comparatively

greater shows that it is making higher payments as dividend out of net earning generated through

operations.

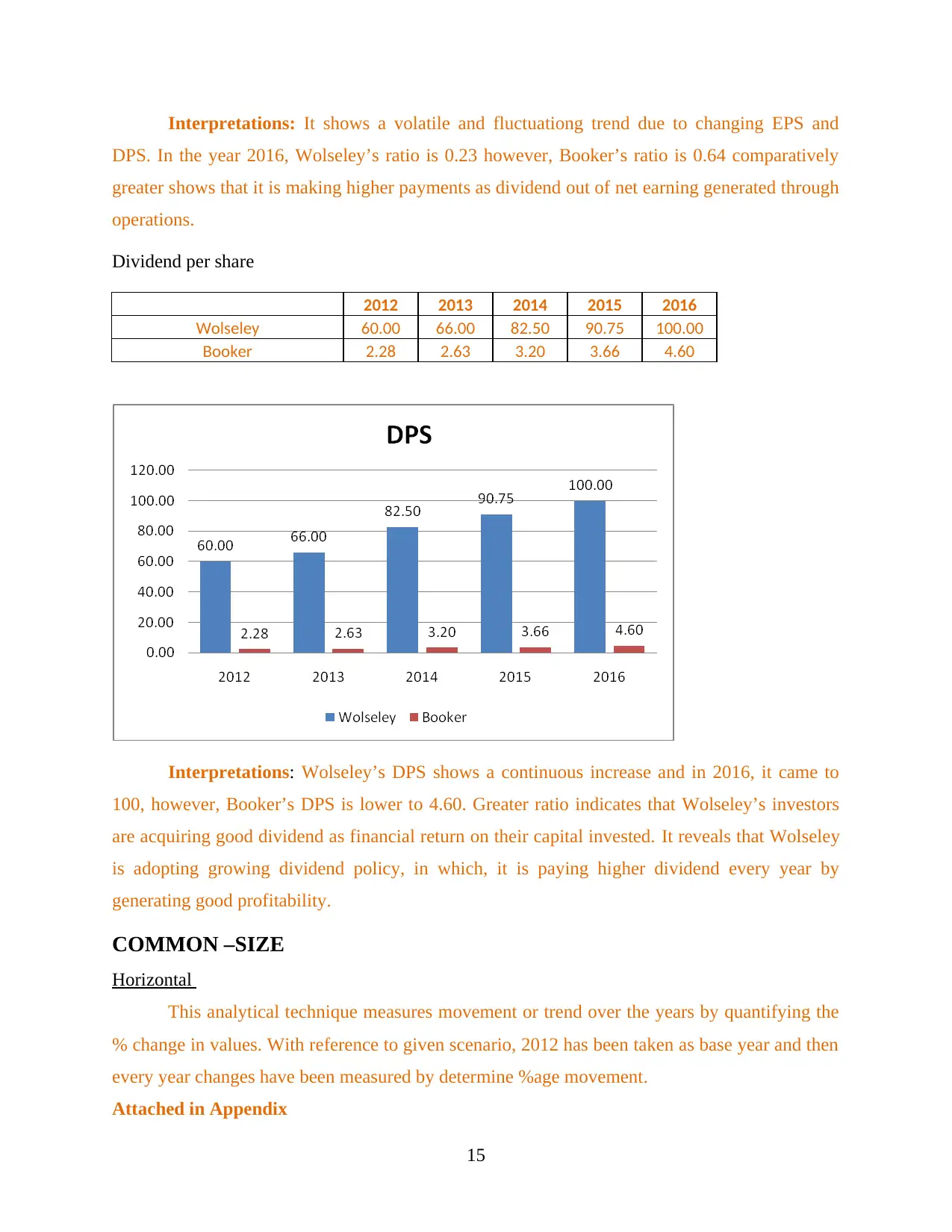

Dividend per share

2012 2013 2014 2015 2016

Wolseley 60.00 66.00 82.50 90.75 100.00

Booker 2.28 2.63 3.20 3.66 4.60

Interpretations: Wolseley’s DPS shows a continuous increase and in 2016, it came to

100, however, Booker’s DPS is lower to 4.60. Greater ratio indicates that Wolseley’s investors

are acquiring good dividend as financial return on their capital invested. It reveals that Wolseley

is adopting growing dividend policy, in which, it is paying higher dividend every year by

generating good profitability.

COMMON –SIZE

Horizontal

This analytical technique measures movement or trend over the years by quantifying the

% change in values. With reference to given scenario, 2012 has been taken as base year and then

every year changes have been measured by determine %age movement.

Attached in Appendix

15

DPS. In the year 2016, Wolseley’s ratio is 0.23 however, Booker’s ratio is 0.64 comparatively

greater shows that it is making higher payments as dividend out of net earning generated through

operations.

Dividend per share

2012 2013 2014 2015 2016

Wolseley 60.00 66.00 82.50 90.75 100.00

Booker 2.28 2.63 3.20 3.66 4.60

Interpretations: Wolseley’s DPS shows a continuous increase and in 2016, it came to

100, however, Booker’s DPS is lower to 4.60. Greater ratio indicates that Wolseley’s investors

are acquiring good dividend as financial return on their capital invested. It reveals that Wolseley

is adopting growing dividend policy, in which, it is paying higher dividend every year by

generating good profitability.

COMMON –SIZE

Horizontal

This analytical technique measures movement or trend over the years by quantifying the

% change in values. With reference to given scenario, 2012 has been taken as base year and then

every year changes have been measured by determine %age movement.

Attached in Appendix

15

Wolseley’s analysis revealed positive trend in sales after 2014 as its % rose up by

91.43%, 99.34% and 107.52% respectively. Similarly, Booker’s turnover also got improved

continuously and in end, it came to 120.86%. However, on the other side, %age increase in net

profit got improved to 157.14% whereas in Wolseley, it is 1140.35% in comparison to the profit

of 2012 worth 57.

Vertical analysis

In profitability statement, sales revenues has been considered as base, however, in

balance sheet, total assets and liabilities has been taken base element and all the other element’s

% age has been compared on this base element.

Attached in Appendix

In 2016, Wolseley’s COGS % on sales got decreased from 72.45% to 71.73% whereas

Booker’s COGS %age has been fallen from 96.22% to 94.92%. Furthermore, its total operating

cost dropped down to 22.95% whilst Booker’s administrative cost gone improved from 1.50% to

2.02%.

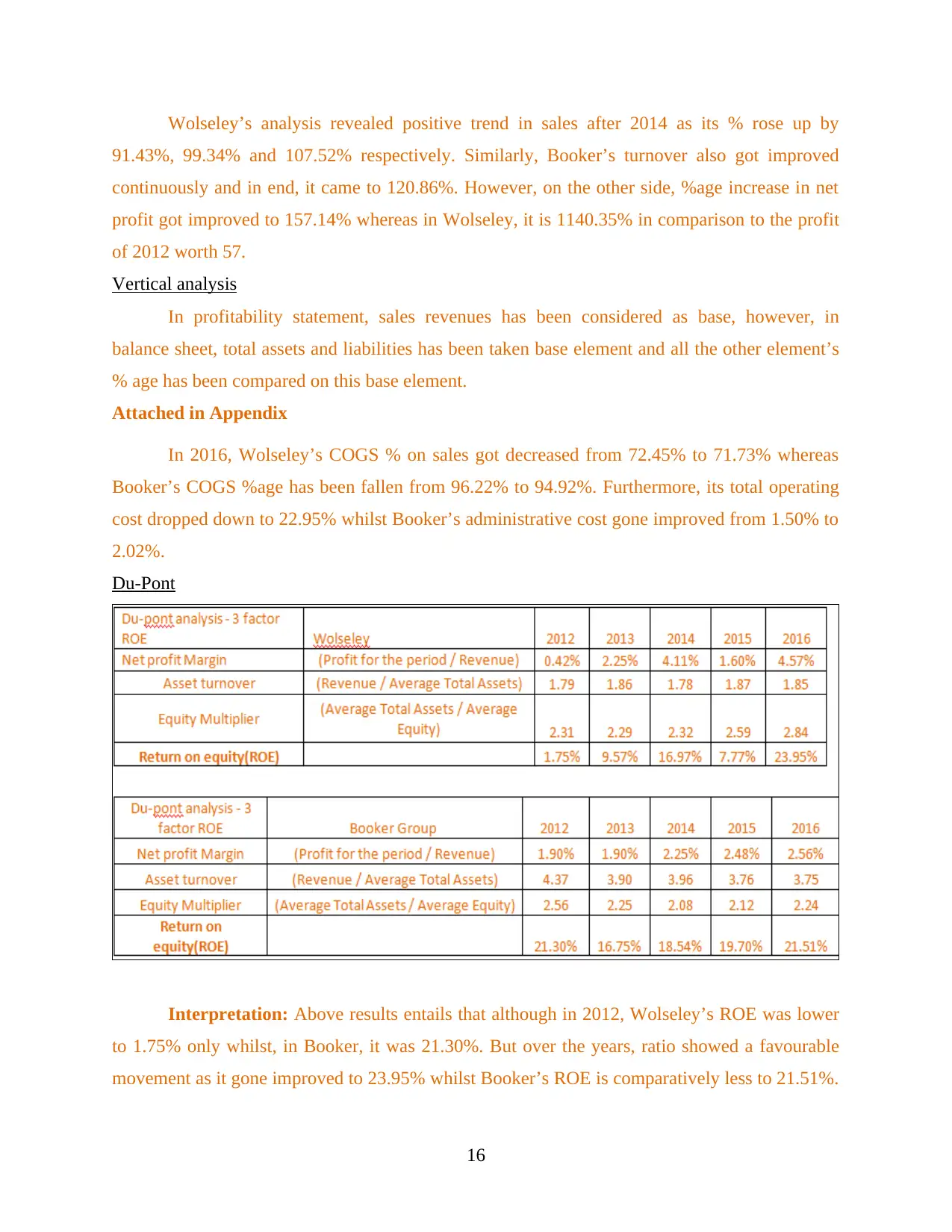

Du-Pont

Interpretation: Above results entails that although in 2012, Wolseley’s ROE was lower

to 1.75% only whilst, in Booker, it was 21.30%. But over the years, ratio showed a favourable

movement as it gone improved to 23.95% whilst Booker’s ROE is comparatively less to 21.51%.

16

91.43%, 99.34% and 107.52% respectively. Similarly, Booker’s turnover also got improved

continuously and in end, it came to 120.86%. However, on the other side, %age increase in net

profit got improved to 157.14% whereas in Wolseley, it is 1140.35% in comparison to the profit

of 2012 worth 57.

Vertical analysis

In profitability statement, sales revenues has been considered as base, however, in

balance sheet, total assets and liabilities has been taken base element and all the other element’s

% age has been compared on this base element.

Attached in Appendix

In 2016, Wolseley’s COGS % on sales got decreased from 72.45% to 71.73% whereas

Booker’s COGS %age has been fallen from 96.22% to 94.92%. Furthermore, its total operating

cost dropped down to 22.95% whilst Booker’s administrative cost gone improved from 1.50% to

2.02%.

Du-Pont

Interpretation: Above results entails that although in 2012, Wolseley’s ROE was lower

to 1.75% only whilst, in Booker, it was 21.30%. But over the years, ratio showed a favourable

movement as it gone improved to 23.95% whilst Booker’s ROE is comparatively less to 21.51%.

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thus, data clearly reveals that Wolseley’s satisfied its investors by generating greater yield or net

earnings on their equity capital invested in the business.

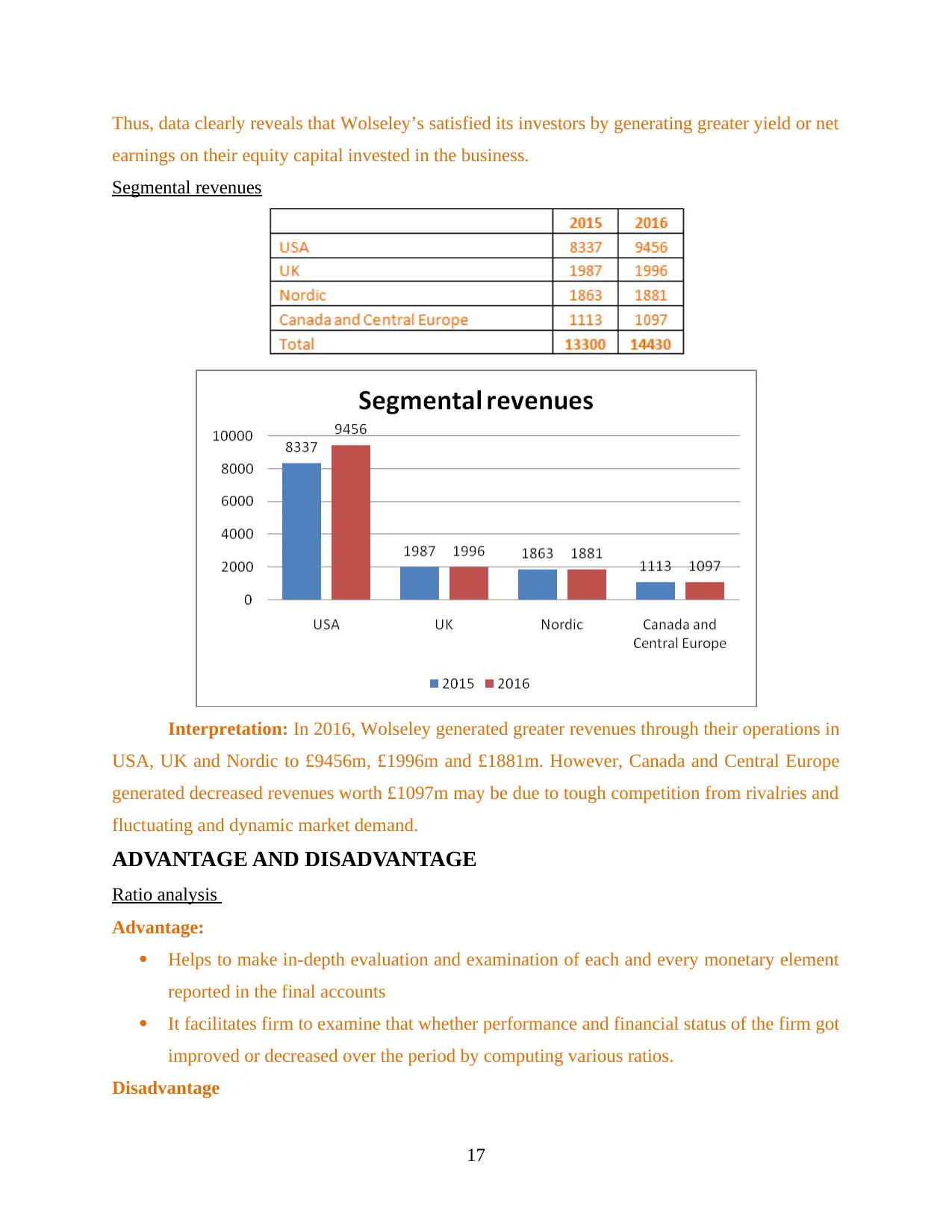

Segmental revenues

Interpretation: In 2016, Wolseley generated greater revenues through their operations in

USA, UK and Nordic to £9456m, £1996m and £1881m. However, Canada and Central Europe

generated decreased revenues worth £1097m may be due to tough competition from rivalries and

fluctuating and dynamic market demand.

ADVANTAGE AND DISADVANTAGE

Ratio analysis

Advantage:

Helps to make in-depth evaluation and examination of each and every monetary element

reported in the final accounts

It facilitates firm to examine that whether performance and financial status of the firm got

improved or decreased over the period by computing various ratios.

Disadvantage

17

earnings on their equity capital invested in the business.

Segmental revenues

Interpretation: In 2016, Wolseley generated greater revenues through their operations in

USA, UK and Nordic to £9456m, £1996m and £1881m. However, Canada and Central Europe

generated decreased revenues worth £1097m may be due to tough competition from rivalries and

fluctuating and dynamic market demand.

ADVANTAGE AND DISADVANTAGE

Ratio analysis

Advantage:

Helps to make in-depth evaluation and examination of each and every monetary element

reported in the final accounts

It facilitates firm to examine that whether performance and financial status of the firm got

improved or decreased over the period by computing various ratios.

Disadvantage

17

Ignore qualitative elements like consumer satisfaction, market reputation, product

portfolio and so on.

Results are based on reported figures in the final accounts which may be incorrect and

leads to make wrong decisions.

Avoid accounting policies, conventions, rules and regulations which might me vary from

year to year.

Does not consider market movement like inflation, technological upgradation, change in

legislations and regulatory framework.

Du-Pont

Advantage:

Take into consideration three important factors that are net profit margin, assets utilizing

efficiency and leverage that helps to make better decisions (Hanushek and Rivkin, 2010).

Disadvantage:

Misleading data in the financial statement may distort or adversely affect the usefulness

of results.

Change in accounting rules and policies are also not considered which may bring changes

in the ratios for ROE computation (Patton and Timmermann, 2010).

Segmental

Advantage:

Separation of total sales revenues into different sub-components according to business

operations gives assistance to make suitable business decisions to maximize overall

performance.

Disadvantage:

Data manipulation in the reporting structure and non-adhering with the accounting rules

may results in taking harmful decisions (Kamoto, 2014).

CONCLUSION & RECOMMENDATIONS

Conclusion

The analysis conducted above bring the fact into consideration that Wolseley is

performing excellent as compare to Booker Group as it is generating more return. Moreover, it is

not suffering cash problems and liquidity crunch as its liquidity position is good. Due to greater

return, this company is also delivering better yield to the investors in return for their risk

18

portfolio and so on.

Results are based on reported figures in the final accounts which may be incorrect and

leads to make wrong decisions.

Avoid accounting policies, conventions, rules and regulations which might me vary from

year to year.

Does not consider market movement like inflation, technological upgradation, change in

legislations and regulatory framework.

Du-Pont

Advantage:

Take into consideration three important factors that are net profit margin, assets utilizing

efficiency and leverage that helps to make better decisions (Hanushek and Rivkin, 2010).

Disadvantage:

Misleading data in the financial statement may distort or adversely affect the usefulness

of results.

Change in accounting rules and policies are also not considered which may bring changes

in the ratios for ROE computation (Patton and Timmermann, 2010).

Segmental

Advantage:

Separation of total sales revenues into different sub-components according to business

operations gives assistance to make suitable business decisions to maximize overall

performance.

Disadvantage:

Data manipulation in the reporting structure and non-adhering with the accounting rules

may results in taking harmful decisions (Kamoto, 2014).

CONCLUSION & RECOMMENDATIONS

Conclusion

The analysis conducted above bring the fact into consideration that Wolseley is

performing excellent as compare to Booker Group as it is generating more return. Moreover, it is

not suffering cash problems and liquidity crunch as its liquidity position is good. Due to greater

return, this company is also delivering better yield to the investors in return for their risk

18

undertaken by investing their own money. Besides this, solvency position is also sound as it

maintained the effective mix of debt and equity. However, efficiency analysis identified

managerial inefficiency as assets are not using optimally.

Recommendation

Booker Group must make several policies and decisions in order to stronger their revenue

stream and also must apply cost control mechanism so as to maximize profitability.

Closure and regular managerial monitoring and supervisions is also a better way to

curtain unnecessary spending and encourage saving.

Market expansion, new product, innovative technologies etc. can be used to enhance

performance.

Increase in CA and decrease in CL will also enable firm to strengthen their

creditworthiness to make their deferral payments on right time.

CONTEMPROARY METHODS

CAPM model

This model is generally used to assess the relationship between and risk and return by

creating portfolio of assets. However, this model reflects information related to risk free rate of

return and beta which is considered as market risk. This shows that if beta of assets is 1 then total

risk associated with portfolio will be equivalent to market risk (Barberis, Greenwood, Jin and

Shleifer, 2015).

Efficient market hypothesis

This is another important concept related to investment which detail regarding the return

generated by security in particular situation (LeRoy, 2010). EMH reflects that investor cannot

get abnormal return out a portfolio or particular assets as prices already contain all information

19

maintained the effective mix of debt and equity. However, efficiency analysis identified

managerial inefficiency as assets are not using optimally.

Recommendation

Booker Group must make several policies and decisions in order to stronger their revenue

stream and also must apply cost control mechanism so as to maximize profitability.

Closure and regular managerial monitoring and supervisions is also a better way to

curtain unnecessary spending and encourage saving.

Market expansion, new product, innovative technologies etc. can be used to enhance

performance.

Increase in CA and decrease in CL will also enable firm to strengthen their

creditworthiness to make their deferral payments on right time.

CONTEMPROARY METHODS

CAPM model

This model is generally used to assess the relationship between and risk and return by

creating portfolio of assets. However, this model reflects information related to risk free rate of

return and beta which is considered as market risk. This shows that if beta of assets is 1 then total

risk associated with portfolio will be equivalent to market risk (Barberis, Greenwood, Jin and

Shleifer, 2015).

Efficient market hypothesis

This is another important concept related to investment which detail regarding the return

generated by security in particular situation (LeRoy, 2010). EMH reflects that investor cannot

get abnormal return out a portfolio or particular assets as prices already contain all information

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

available in the marketplace. Efficient market hypothesis depicts that no past prices and other

indicator affect the current prices of stock. Apart from this, other assumption related to semi,

strong and weak form do not allow investors to generate return on the basis of available

information (Lee, Lee and Lee, 2010).

Economic value added (EVA)

Economic value added is referred as internal management performance measures

whereby comparison is made between net operating profit and total cost of capital (Priester and

Wang, 2010). It is also known as economic profit which enable firm to opt appropriate strategies

by taking into account extracted results. It is considered as the best way to compare

establishment’s economic profit with the expected return percentage (Hanushek and Rivkin,

2010).

20

indicator affect the current prices of stock. Apart from this, other assumption related to semi,

strong and weak form do not allow investors to generate return on the basis of available

information (Lee, Lee and Lee, 2010).

Economic value added (EVA)

Economic value added is referred as internal management performance measures

whereby comparison is made between net operating profit and total cost of capital (Priester and

Wang, 2010). It is also known as economic profit which enable firm to opt appropriate strategies

by taking into account extracted results. It is considered as the best way to compare

establishment’s economic profit with the expected return percentage (Hanushek and Rivkin,

2010).

20

REFERENCES

Books and Journals

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS data.

Agricultural Finance Review. 72(2). pp. 262-272.

Ak, B.K. and et.al., 2013. The use of financial ratio models to help investors predict and interpret

significant corporate events. Australian journal of management. 38(3). pp. 553-598.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative capital

asset pricing model. Journal of Financial Economics. 115(1). pp.1-24.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA). 1(1). pp. 40-59.

Evans, J.R. and Mathur, A., 2014. Retailing and the period leading up to the Great Recession: a

model and a 25-year financial ratio analysis of US retailing. The International Review of

Retail, Distribution and Consumer Research. 24(1). pp. 30-58.

Hanushek, E.A. and Rivkin, S.G., 2010. Generalizations about using value-added measures of

teacher quality. The American Economic Review, 100(2). pp.267-271.

Kamoto, S., 2014. Impacts of internal financing on investment decisions by optimistic and

overconfident managers. European Financial Management. 20(1). pp. 107-125.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social

Science. 4(3).

Lee, C.C., Lee, J.D. and Lee, C.C., 2010. Stock prices and the efficient market hypothesis:

Evidence from a panel stationary test with structural breaks. Japan and the world

economy. 22(1). pp.49-58.

LeRoy, S.F., 2010. Efficient market hypothesis. Encyclopedia of Quantitative Finance.

Mishra, L., 2013. HERD MENTALITY IN INDIAN FUND MANAGERS: A REALITY OR A

MYTH? A BEHAVIOURAL FINANCE PERSPECTIVE. International Journal of

Applied Financial Management Perspectives. 2(1). p. 216.

21

Books and Journals

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS data.

Agricultural Finance Review. 72(2). pp. 262-272.

Ak, B.K. and et.al., 2013. The use of financial ratio models to help investors predict and interpret

significant corporate events. Australian journal of management. 38(3). pp. 553-598.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative capital

asset pricing model. Journal of Financial Economics. 115(1). pp.1-24.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA). 1(1). pp. 40-59.

Evans, J.R. and Mathur, A., 2014. Retailing and the period leading up to the Great Recession: a

model and a 25-year financial ratio analysis of US retailing. The International Review of

Retail, Distribution and Consumer Research. 24(1). pp. 30-58.

Hanushek, E.A. and Rivkin, S.G., 2010. Generalizations about using value-added measures of

teacher quality. The American Economic Review, 100(2). pp.267-271.

Kamoto, S., 2014. Impacts of internal financing on investment decisions by optimistic and

overconfident managers. European Financial Management. 20(1). pp. 107-125.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social

Science. 4(3).

Lee, C.C., Lee, J.D. and Lee, C.C., 2010. Stock prices and the efficient market hypothesis:

Evidence from a panel stationary test with structural breaks. Japan and the world

economy. 22(1). pp.49-58.

LeRoy, S.F., 2010. Efficient market hypothesis. Encyclopedia of Quantitative Finance.

Mishra, L., 2013. HERD MENTALITY IN INDIAN FUND MANAGERS: A REALITY OR A

MYTH? A BEHAVIOURAL FINANCE PERSPECTIVE. International Journal of

Applied Financial Management Perspectives. 2(1). p. 216.

21

Nguyen, T. and Schüßler, A., 2013. How to make better decisions? Lessons learned from

behavioral corporate finance. International Business Research. 6(1). p. 187.

Patton, A.J. and Timmermann, A., 2010. Monotonicity in asset returns: New tests with

applications to the term structure, the CAPM, and portfolio sorts. Journal of Financial

Economics. 98(3). pp.605-625.

Priester, C. and Wang, J., 2010. Economic Value Added. In Financial Strategies for the

Manager (pp. 118-135). Springer Berlin Heidelberg.

QIN, X.J. and Xing-jun, L.L., 2014. A Study of the Impact of Corporate Governance on

Managers' Self-Interest Motivation and Cost Stickiness.".Contemporary Finance &

Economics. 2. pp. 38-45.ZHU, G.Y., XI, A.Q. and DING, J.X., 2014. Empirical Research

on Effects of the Irrational Performance of Managers in Corporate Finance Decisions.

Journal of Guizhou University of Finance and Economics. 4. p. 008.

Šarlija, N. and Harc, M., 2012. The impact of liquidity on the capital structure: a case study of

Croatian firms. Business Systems Research. 3(1). pp. 30-36.

Xu, W. and et.al., 2014. Financial ratio selection for business failure prediction using soft set

theory. Knowledge-Based Systems. 63. pp. 59-67.

Online

Boer, P., 2011. Basics of Financial Management. [Online]. Accessed

Through:<http://www.noordhoffuitgevers.nl/nuweb/assets/Inhoudsopgave_97890018029

12.pdf>: [Accessed on 23rd November 2016].

Kumbirai, M., 2010. A financial Ratio Analysis of Commercial Bank Performance in South

Africa. [Online]. Accessed

Through:<http://african-review.com/Vol.%202%20(1)/Financial%20Ratio%20Analysis

%20of%20Bank%20Performance.pdf>: [Accessed on 23rd November 2016].

22

behavioral corporate finance. International Business Research. 6(1). p. 187.

Patton, A.J. and Timmermann, A., 2010. Monotonicity in asset returns: New tests with

applications to the term structure, the CAPM, and portfolio sorts. Journal of Financial

Economics. 98(3). pp.605-625.

Priester, C. and Wang, J., 2010. Economic Value Added. In Financial Strategies for the

Manager (pp. 118-135). Springer Berlin Heidelberg.

QIN, X.J. and Xing-jun, L.L., 2014. A Study of the Impact of Corporate Governance on

Managers' Self-Interest Motivation and Cost Stickiness.".Contemporary Finance &

Economics. 2. pp. 38-45.ZHU, G.Y., XI, A.Q. and DING, J.X., 2014. Empirical Research

on Effects of the Irrational Performance of Managers in Corporate Finance Decisions.

Journal of Guizhou University of Finance and Economics. 4. p. 008.

Šarlija, N. and Harc, M., 2012. The impact of liquidity on the capital structure: a case study of

Croatian firms. Business Systems Research. 3(1). pp. 30-36.

Xu, W. and et.al., 2014. Financial ratio selection for business failure prediction using soft set

theory. Knowledge-Based Systems. 63. pp. 59-67.

Online

Boer, P., 2011. Basics of Financial Management. [Online]. Accessed

Through:<http://www.noordhoffuitgevers.nl/nuweb/assets/Inhoudsopgave_97890018029

12.pdf>: [Accessed on 23rd November 2016].

Kumbirai, M., 2010. A financial Ratio Analysis of Commercial Bank Performance in South

Africa. [Online]. Accessed

Through:<http://african-review.com/Vol.%202%20(1)/Financial%20Ratio%20Analysis

%20of%20Bank%20Performance.pdf>: [Accessed on 23rd November 2016].

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Wolseley’s ratio analysis

23

Wolseley’s ratio analysis

23

Booker’s ratio analysis

24

24

Wolseley’s vertical analysis of income statement

Wolseley’s vertical analysis of balance sheet

25

Wolseley’s vertical analysis of balance sheet

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

26

Wolseley’s vertical analysis of cash flow statement

Booker’s vertical analysis of income statement

27

Booker’s vertical analysis of income statement

27

Booker’s vertical analysis of balance sheet

28

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Booker’s vertical analysis of statement of cash flows

29

29

Wolseley’s horizontal analysis of statement of income statement

Wolseley’s horizontal analysis of statement of balance sheet

30

Wolseley’s horizontal analysis of statement of balance sheet

30

Wolseley’s horizontal analysis of statement of cash flows

Booker’s horizontal analysis of income statement

31

Booker’s horizontal analysis of income statement

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Booker’s horizontal analysis of balance sheet

32

32

Booker’s horizontal analysis of statement of cash flows

33

33

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.