Strategic Financial Analysis: Traditional vs. Contemporary Methods

VerifiedAdded on 2020/04/21

|25

|7898

|88

Report

AI Summary

This report provides a critical analysis of financial statements for external users, focusing on two selected companies, Booker and Tate & Lyle. It begins by reviewing traditional financial analysis methods, including horizontal, vertical, and ratio analysis, highlighting their strengths and weaknesses. The report then introduces contemporary methods such as the Capital Asset Pricing Model (CAPM), Dividend Growth Model (DGM), and the Efficient Market Hypothesis, illustrating their effectiveness in overcoming the limitations of traditional approaches. The analysis includes a comparison of the two companies' financial performance using these methods, with detailed findings presented in the appendices. The report concludes by emphasizing the importance of utilizing contemporary methods for a more comprehensive and accurate financial analysis.

Strategic Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. Introduction..................................................................................................................................4

2. Critical Review of Traditional Methods of Financial Analysis...................................................4

2.1 Horizontal Analysis................................................................................................................4

Description of Analysis Method...............................................................................................4

Supporting the Analysis Method with using empirical academic literature............................4

Shortcomings............................................................................................................................5

Horizontal Analysis of two Selected Companies (See Appendix 1)........................................5

2.2 Vertical Analysis....................................................................................................................5

Description of Analysis Method...............................................................................................5

Supporting the Analysis Method with using empirical academic literature............................5

Shortcomings............................................................................................................................6

Vertical analysis of two Selected Companies (See Appendix 2).............................................6

2.3Traditional Ratio Analysis......................................................................................................6

Description of Analysis Method...............................................................................................6

Supporting the Analysis Method with using empirical academic literature............................6

Shortcomings............................................................................................................................7

Ratio Analysis of the two selected companies (See Appendix 3)............................................7

3. Contemporary Method of Financial Analysis..............................................................................8

3.1 Capital Asset Pricing Model (CAPM)...................................................................................8

Description of Analysis Method...............................................................................................8

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method.............8

Criticism of the Model.............................................................................................................9

3.2 Divided Growth Model (DGM).............................................................................................9

Description of Analysis Method...............................................................................................9

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method.............9

Criticism of the Model...........................................................................................................10

3.3 Effective Market Hypothesis...............................................................................................10

1. Introduction..................................................................................................................................4

2. Critical Review of Traditional Methods of Financial Analysis...................................................4

2.1 Horizontal Analysis................................................................................................................4

Description of Analysis Method...............................................................................................4

Supporting the Analysis Method with using empirical academic literature............................4

Shortcomings............................................................................................................................5

Horizontal Analysis of two Selected Companies (See Appendix 1)........................................5

2.2 Vertical Analysis....................................................................................................................5

Description of Analysis Method...............................................................................................5

Supporting the Analysis Method with using empirical academic literature............................5

Shortcomings............................................................................................................................6

Vertical analysis of two Selected Companies (See Appendix 2).............................................6

2.3Traditional Ratio Analysis......................................................................................................6

Description of Analysis Method...............................................................................................6

Supporting the Analysis Method with using empirical academic literature............................6

Shortcomings............................................................................................................................7

Ratio Analysis of the two selected companies (See Appendix 3)............................................7

3. Contemporary Method of Financial Analysis..............................................................................8

3.1 Capital Asset Pricing Model (CAPM)...................................................................................8

Description of Analysis Method...............................................................................................8

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method.............8

Criticism of the Model.............................................................................................................9

3.2 Divided Growth Model (DGM).............................................................................................9

Description of Analysis Method...............................................................................................9

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method.............9

Criticism of the Model...........................................................................................................10

3.3 Effective Market Hypothesis...............................................................................................10

Description of Analysis Method.............................................................................................10

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method...........10

Criticism of the Model...........................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Appendixes....................................................................................................................................13

Appendix 1.....................................................................................................................................13

Horizontal analysis Booker............................................................................................................13

Horizontal analysis Tate & Lyle....................................................................................................15

Appendix 2.....................................................................................................................................18

Vertical analysis Booker................................................................................................................18

Vertical analysis Tate & Lyle........................................................................................................20

Appendix 3:...................................................................................................................................23

Ratio Analysis of Booker...............................................................................................................23

Ratio Analysis of Tate & Lyle.......................................................................................................24

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method...........10

Criticism of the Model...........................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Appendixes....................................................................................................................................13

Appendix 1.....................................................................................................................................13

Horizontal analysis Booker............................................................................................................13

Horizontal analysis Tate & Lyle....................................................................................................15

Appendix 2.....................................................................................................................................18

Vertical analysis Booker................................................................................................................18

Vertical analysis Tate & Lyle........................................................................................................20

Appendix 3:...................................................................................................................................23

Ratio Analysis of Booker...............................................................................................................23

Ratio Analysis of Tate & Lyle.......................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Introduction

The present report is developed for providing a critical analysis of the accounts of

selected business organizations on the perspective of an external user. The report emphasizes on

the deficiencies present in the traditional method of financial analysis through carrying out the

financial analysis of two selected companies. The report proposes the use of contemporary

analysis methods for financial analysis in order to overcome the shortcomings of the traditional

analysis. The financial analysis can be described as method of developing an understanding of

the financial position of an entity through evaluating its general purpose financial statements

such as balance sheet, income statement, cash flow statement and others (Brigham and Ehrhardt,

2007). In this context, the report demonstrates a critical review of traditional method of financial

analysis such as horizontal, vertical and ratio analysis. The contemporary methods of financial

analysis examined under the report are capital asset pricing model (CAPM), dividend growth

model (DGM) and effective market hypothesis.

2. Critical Review of Traditional Methods of Financial Analysis

2.1 Horizontal Analysis

Description of Analysis Method

The horizontal analysis also known as trend analysis is a technique used for fundamental

analysis of business companies by financial analysts in which they compare the ratios and line

items over accounting periods. It is also known as time series analysis that emphasizes on change

in accounting numbers over certain period of time. It helps the potential investors and creditors

to analyse the growth incurred by a company over the number of years. It also analyses the

growth rate of a company through comparing it with its competitors and industry. It analyses the

performance of companies through evaluating the percentage change occurred in any item of its

financials such as revenues, earnings per share (EPS) and others. The major assumption used in

the analysis method is that it is based on evaluation of the financial data of past and therefore

cannot be regarded as accurate technique of analyzing the financial position of a company (Griff,

2014).

Supporting the Analysis Method with using empirical academic literature

The horizontal analysis method involves evaluating a consistent pattern within the

financial accounts and thus the results provided by it are based on percentage increase or

decrease and thus are reliable. Also, the horizontal analysis method enables the analysts to

compare the financial position of different companies irrespective of their size. This is because

the method provides the financial results on the basis of percentage increase or decrease and

therefore appropriate to evaluate the financial position of companies of different size. The

method is also useful for analyzing the large changes in each line item of the financial account of

The present report is developed for providing a critical analysis of the accounts of

selected business organizations on the perspective of an external user. The report emphasizes on

the deficiencies present in the traditional method of financial analysis through carrying out the

financial analysis of two selected companies. The report proposes the use of contemporary

analysis methods for financial analysis in order to overcome the shortcomings of the traditional

analysis. The financial analysis can be described as method of developing an understanding of

the financial position of an entity through evaluating its general purpose financial statements

such as balance sheet, income statement, cash flow statement and others (Brigham and Ehrhardt,

2007). In this context, the report demonstrates a critical review of traditional method of financial

analysis such as horizontal, vertical and ratio analysis. The contemporary methods of financial

analysis examined under the report are capital asset pricing model (CAPM), dividend growth

model (DGM) and effective market hypothesis.

2. Critical Review of Traditional Methods of Financial Analysis

2.1 Horizontal Analysis

Description of Analysis Method

The horizontal analysis also known as trend analysis is a technique used for fundamental

analysis of business companies by financial analysts in which they compare the ratios and line

items over accounting periods. It is also known as time series analysis that emphasizes on change

in accounting numbers over certain period of time. It helps the potential investors and creditors

to analyse the growth incurred by a company over the number of years. It also analyses the

growth rate of a company through comparing it with its competitors and industry. It analyses the

performance of companies through evaluating the percentage change occurred in any item of its

financials such as revenues, earnings per share (EPS) and others. The major assumption used in

the analysis method is that it is based on evaluation of the financial data of past and therefore

cannot be regarded as accurate technique of analyzing the financial position of a company (Griff,

2014).

Supporting the Analysis Method with using empirical academic literature

The horizontal analysis method involves evaluating a consistent pattern within the

financial accounts and thus the results provided by it are based on percentage increase or

decrease and thus are reliable. Also, the horizontal analysis method enables the analysts to

compare the financial position of different companies irrespective of their size. This is because

the method provides the financial results on the basis of percentage increase or decrease and

therefore appropriate to evaluate the financial position of companies of different size. The

method is also useful for analyzing the large changes in each line item of the financial account of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a company. It is the most useful method for analyzing the growth in the financial performance of

a company over large number of accounting periods (Megginson, Lucey and Smart, 2008).

Shortcomings

The horizontal analysis provides the results about the financial performance of a

company through the use of past financial data. Thus, the method is not useful for predicting the

present financial performance of a company. The method involves aggregating the financial

information of the past that may have changed over the period of time. The method prove to be

useful only when the analysis of financial statements of all the companies are carried out at the

same time in order to completely assess the complete impact of operational results on the

financial performance of a company. The results obtained from the use of horizontal analysis can

be modified by the analysts for intentionally mis-reporting the financial results (Bierman and

Smidt, 2003).

Horizontal Analysis of two Selected Companies (See Appendix 1)

As per the horizontal analysis carried out of Booker and Tate & Lyle given in the

appendix, it can be said that Booker depicts an increasing trend while Tate and Lyle have shown

a decreasing trend from the period 2012-2015. The Booker has shown an increasing trend in the

revenue generation while Tate & Lyle shows a decreasing trend of revenue generation. Similarly,

the trend analysis of the balance sheet of the two companies depicts that Booker records an

increase in the assets and liabilities while Tate & Lyle depicts a decreasing trend from the period

2012-2016. Thus, the trend analysis of the two companies has depicted the percentage changes in

the components of the income statement and the balance sheets in comparison to the originating

year for depicting the financial growth in the consecutive years.

2.2 Vertical Analysis

Description of Analysis Method

The vertical analysis can be described as a method of analyzing the financial position of a

company through assessing the proportion of the total account of assets, liabilities and equities in

the financial statements. The vertical analysis uses the base figures of total assets, total liabilities

and stakeholder’s equity in order to develop an individual statement depicting the financial

performance of a firm. The key assumption that is used in the method is that all asset groups are

condensed to depict the percentage of total assets that is used as a base figure for comparison.

For example, the vertical analysis of income statement uses sales figure as a base figure and all

other components such as cost of sales, gross profit, operating expenses, income tax are depicted

as sales percentage (Henderson et al., 2015).

Supporting the Analysis Method with using empirical academic literature

The vertical analysis also known as common-size analysis method helps in analyzing the

financial position of a company through evaluating the percentage of a base figure of each item

within the statement. This helps in predicting the percentage growth realized by a company in

a company over large number of accounting periods (Megginson, Lucey and Smart, 2008).

Shortcomings

The horizontal analysis provides the results about the financial performance of a

company through the use of past financial data. Thus, the method is not useful for predicting the

present financial performance of a company. The method involves aggregating the financial

information of the past that may have changed over the period of time. The method prove to be

useful only when the analysis of financial statements of all the companies are carried out at the

same time in order to completely assess the complete impact of operational results on the

financial performance of a company. The results obtained from the use of horizontal analysis can

be modified by the analysts for intentionally mis-reporting the financial results (Bierman and

Smidt, 2003).

Horizontal Analysis of two Selected Companies (See Appendix 1)

As per the horizontal analysis carried out of Booker and Tate & Lyle given in the

appendix, it can be said that Booker depicts an increasing trend while Tate and Lyle have shown

a decreasing trend from the period 2012-2015. The Booker has shown an increasing trend in the

revenue generation while Tate & Lyle shows a decreasing trend of revenue generation. Similarly,

the trend analysis of the balance sheet of the two companies depicts that Booker records an

increase in the assets and liabilities while Tate & Lyle depicts a decreasing trend from the period

2012-2016. Thus, the trend analysis of the two companies has depicted the percentage changes in

the components of the income statement and the balance sheets in comparison to the originating

year for depicting the financial growth in the consecutive years.

2.2 Vertical Analysis

Description of Analysis Method

The vertical analysis can be described as a method of analyzing the financial position of a

company through assessing the proportion of the total account of assets, liabilities and equities in

the financial statements. The vertical analysis uses the base figures of total assets, total liabilities

and stakeholder’s equity in order to develop an individual statement depicting the financial

performance of a firm. The key assumption that is used in the method is that all asset groups are

condensed to depict the percentage of total assets that is used as a base figure for comparison.

For example, the vertical analysis of income statement uses sales figure as a base figure and all

other components such as cost of sales, gross profit, operating expenses, income tax are depicted

as sales percentage (Henderson et al., 2015).

Supporting the Analysis Method with using empirical academic literature

The vertical analysis also known as common-size analysis method helps in analyzing the

financial position of a company through evaluating the percentage of a base figure of each item

within the statement. This helps in predicting the percentage growth realized by a company in

each item of its balance sheet by illustrating the relative sizes of different accounts. The

percentage in the method of vertical analysis is calculated through the use of following formula:

The use of vertical analysis helps in restating the financial statements of a company in the

percentage format that helps in comparing the results obtained in the present year with that of the

previous year. The use of vertical analysis helps in carrying out inter-company transactions of

enterprises having varied sizes as all the financial items are expressed as percentage of common

number. For example, there are two companies A and B operating in the same industry out of

which company A is small and company B is large. As such, the vertical analysis through the use

of sales figure as base can help in comparing the gross profit percentage for both the companies

(Besley and Brigham, 2014).

Shortcomings

The common size statement lacks standardizations as there is not standard method of

calculating the percentage change in different items of the financial statements. It is based on

historical costs and therefore provides misleading financial information. It is not helpful in

providing useful financial information during seasonal fluctuations such as closing stocks. It

does not help in assessing the liquidity and solvency position of a company (Bender, 2013).

Vertical analysis of two Selected Companies (See Appendix 2)

As per the vertical analysis of two companies depicted in the appendix section, the

Booker and Tate & Lyle income statement and balance sheet depicts different growth patterns.

The operating profit is showing an increasing trend as a percentage of the total sales for Booker

while it is depicting a decreasing trend for the Tate and Lyle. The balance sheet vertical analysis

represents the percentage changes in each line item in comparison to the total assets. The current

assets for the Booker represent an increasing trend while that for Tate and Lyle depicts a

decreasing trend. Therefore, it can be said from the vertical analysis of the two companies that

Booker financial performance is much better than Tate & Lyle over the financial period of 2012-

2016.

2.3Traditional Ratio Analysis

Description of Analysis Method

The ratio analysis method is used for analyzing the financial performance of a company

though examining its efficiency, liquidity, profitability and solvency condition. The ratios are

compared over the period of time to predict the financial growth or devaluation in a company

value (Horngren et al., 2012).

percentage in the method of vertical analysis is calculated through the use of following formula:

The use of vertical analysis helps in restating the financial statements of a company in the

percentage format that helps in comparing the results obtained in the present year with that of the

previous year. The use of vertical analysis helps in carrying out inter-company transactions of

enterprises having varied sizes as all the financial items are expressed as percentage of common

number. For example, there are two companies A and B operating in the same industry out of

which company A is small and company B is large. As such, the vertical analysis through the use

of sales figure as base can help in comparing the gross profit percentage for both the companies

(Besley and Brigham, 2014).

Shortcomings

The common size statement lacks standardizations as there is not standard method of

calculating the percentage change in different items of the financial statements. It is based on

historical costs and therefore provides misleading financial information. It is not helpful in

providing useful financial information during seasonal fluctuations such as closing stocks. It

does not help in assessing the liquidity and solvency position of a company (Bender, 2013).

Vertical analysis of two Selected Companies (See Appendix 2)

As per the vertical analysis of two companies depicted in the appendix section, the

Booker and Tate & Lyle income statement and balance sheet depicts different growth patterns.

The operating profit is showing an increasing trend as a percentage of the total sales for Booker

while it is depicting a decreasing trend for the Tate and Lyle. The balance sheet vertical analysis

represents the percentage changes in each line item in comparison to the total assets. The current

assets for the Booker represent an increasing trend while that for Tate and Lyle depicts a

decreasing trend. Therefore, it can be said from the vertical analysis of the two companies that

Booker financial performance is much better than Tate & Lyle over the financial period of 2012-

2016.

2.3Traditional Ratio Analysis

Description of Analysis Method

The ratio analysis method is used for analyzing the financial performance of a company

though examining its efficiency, liquidity, profitability and solvency condition. The ratios are

compared over the period of time to predict the financial growth or devaluation in a company

value (Horngren et al., 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Supporting the Analysis Method with using empirical academic literature

The method is easy to be implemented and helps in comparing the financial performance

of companies operating in the same or different industry. It established the quantitative

relationship between the financial performance of a company over the years for ascertaining its

strengths and weaknesses. It helps in forecasting the financial performance of a company based

on the past trends such as profitability, liquidity and efficiency. It is also helpful in developing

the budgets of the companies on the basis of its performance in the past (Megginson, Lucey and

Smart, 2008).

Shortcomings

The method of ratio analysis also has certain limitations. The major limitation is that the

method is based on the historical data and thus do not reflect the actual financial performance. It

can also be not utilized for predicting the future financial performance of a company. Also, the

financial performance of the companies using different accounting policies for developing the

financial statements cannot be compared through the use of ratio analysis. It is entirely based on

quantitative factors and does not take into account the qualitative factors that many impact the

financial performance of a firm (Weil, Schipper and Francis, 2013).

Ratio Analysis of the two selected companies (See Appendix 3)

The ratio analysis of Booker and Tate&Lyle has assessed their liquidity, efficiency,

profitability, cash flows and leverage condition. As per the ratio analysis of Booker, it can be

stated that company’s liquidity position has improved over the period 2012-2016. The current

and quick ratio of the company has increased significantly depicting that its ability to meet its

financial obligations has improved over the financial period. On the contrary, the liquidity

position of the company is on a declining trend over the financial period of 2012-2016 as

depicted from a decreasing pattern f its current and quick ratio. The efficiency analysis of the

two companies has depicted their abilities to effectively use their assets and liabilities internally.

The Booker efficacy position has improved from 2012-2016 with an increasing trend of its ratios

of days of sales outstanding, day of inventory on hand, days of payables and cash conversion

cycle while that of Tate & Lyle have significantly declined with declining trend in its efficiency

ratios. The profitability analysis of the two companies have also depicted that Booker

profitability position is much better than Tate and Lyle. The cash flow position of the two

companies analyzed from their operating cash flow ratios have depicted an increasing pattern for

both thus inferring that they maintain an adequate cash for meeting the need of their operational

activities. In addition to this, the leverage ratios of the two companies such as debt to equity and

debt to assets ratio have stated that Booker is incorporating larger use of debt in its capital

structure as compared to Tate and Lyle. Thus, it can be said from the ratio analysis of both the

companies that Booker financial performance is superior over Tate & Lyle for the period of

2014-2016.

The method is easy to be implemented and helps in comparing the financial performance

of companies operating in the same or different industry. It established the quantitative

relationship between the financial performance of a company over the years for ascertaining its

strengths and weaknesses. It helps in forecasting the financial performance of a company based

on the past trends such as profitability, liquidity and efficiency. It is also helpful in developing

the budgets of the companies on the basis of its performance in the past (Megginson, Lucey and

Smart, 2008).

Shortcomings

The method of ratio analysis also has certain limitations. The major limitation is that the

method is based on the historical data and thus do not reflect the actual financial performance. It

can also be not utilized for predicting the future financial performance of a company. Also, the

financial performance of the companies using different accounting policies for developing the

financial statements cannot be compared through the use of ratio analysis. It is entirely based on

quantitative factors and does not take into account the qualitative factors that many impact the

financial performance of a firm (Weil, Schipper and Francis, 2013).

Ratio Analysis of the two selected companies (See Appendix 3)

The ratio analysis of Booker and Tate&Lyle has assessed their liquidity, efficiency,

profitability, cash flows and leverage condition. As per the ratio analysis of Booker, it can be

stated that company’s liquidity position has improved over the period 2012-2016. The current

and quick ratio of the company has increased significantly depicting that its ability to meet its

financial obligations has improved over the financial period. On the contrary, the liquidity

position of the company is on a declining trend over the financial period of 2012-2016 as

depicted from a decreasing pattern f its current and quick ratio. The efficiency analysis of the

two companies has depicted their abilities to effectively use their assets and liabilities internally.

The Booker efficacy position has improved from 2012-2016 with an increasing trend of its ratios

of days of sales outstanding, day of inventory on hand, days of payables and cash conversion

cycle while that of Tate & Lyle have significantly declined with declining trend in its efficiency

ratios. The profitability analysis of the two companies have also depicted that Booker

profitability position is much better than Tate and Lyle. The cash flow position of the two

companies analyzed from their operating cash flow ratios have depicted an increasing pattern for

both thus inferring that they maintain an adequate cash for meeting the need of their operational

activities. In addition to this, the leverage ratios of the two companies such as debt to equity and

debt to assets ratio have stated that Booker is incorporating larger use of debt in its capital

structure as compared to Tate and Lyle. Thus, it can be said from the ratio analysis of both the

companies that Booker financial performance is superior over Tate & Lyle for the period of

2014-2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Contemporary Method of Financial Analysis

3.1 Capital Asset Pricing Model (CAPM)

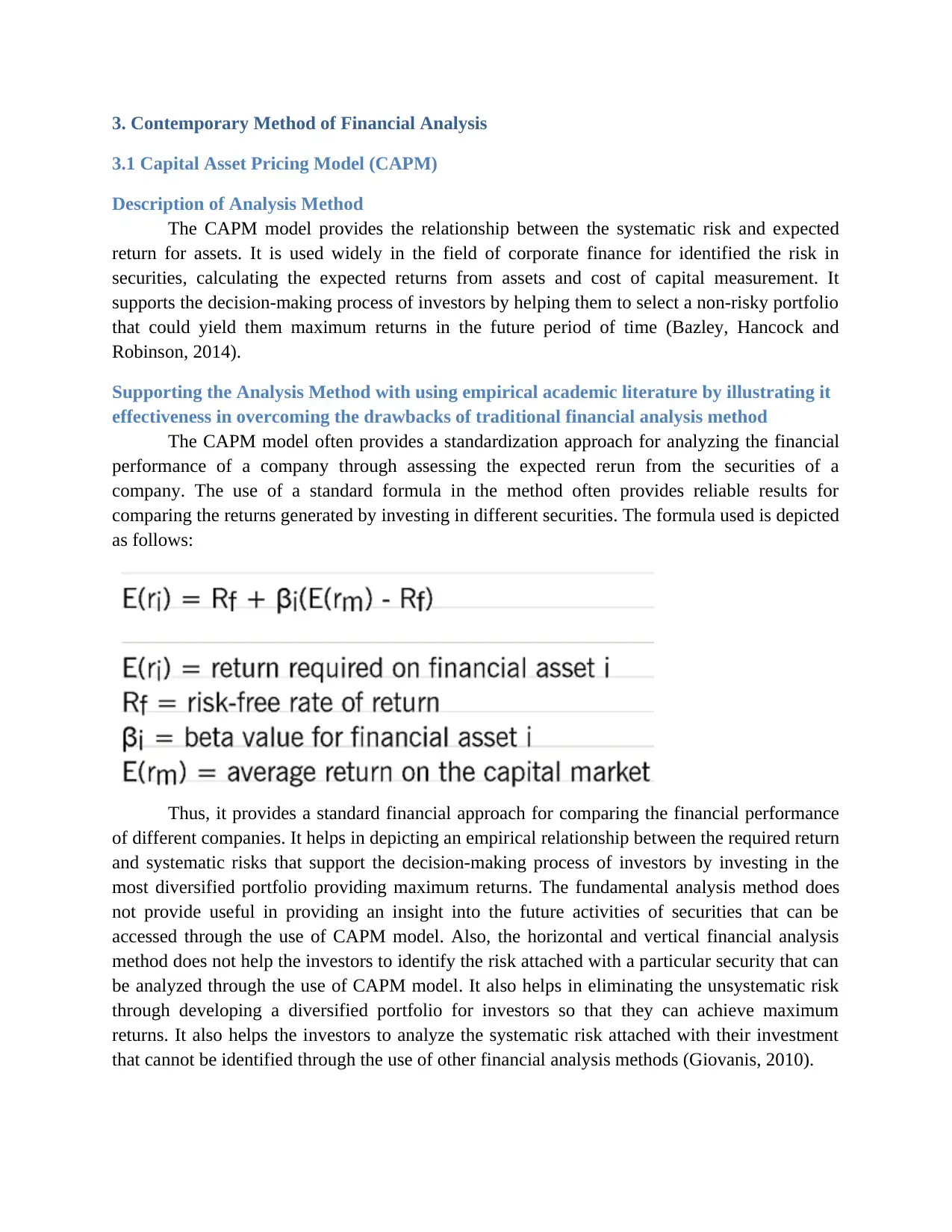

Description of Analysis Method

The CAPM model provides the relationship between the systematic risk and expected

return for assets. It is used widely in the field of corporate finance for identified the risk in

securities, calculating the expected returns from assets and cost of capital measurement. It

supports the decision-making process of investors by helping them to select a non-risky portfolio

that could yield them maximum returns in the future period of time (Bazley, Hancock and

Robinson, 2014).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The CAPM model often provides a standardization approach for analyzing the financial

performance of a company through assessing the expected rerun from the securities of a

company. The use of a standard formula in the method often provides reliable results for

comparing the returns generated by investing in different securities. The formula used is depicted

as follows:

Thus, it provides a standard financial approach for comparing the financial performance

of different companies. It helps in depicting an empirical relationship between the required return

and systematic risks that support the decision-making process of investors by investing in the

most diversified portfolio providing maximum returns. The fundamental analysis method does

not provide useful in providing an insight into the future activities of securities that can be

accessed through the use of CAPM model. Also, the horizontal and vertical financial analysis

method does not help the investors to identify the risk attached with a particular security that can

be analyzed through the use of CAPM model. It also helps in eliminating the unsystematic risk

through developing a diversified portfolio for investors so that they can achieve maximum

returns. It also helps the investors to analyze the systematic risk attached with their investment

that cannot be identified through the use of other financial analysis methods (Giovanis, 2010).

3.1 Capital Asset Pricing Model (CAPM)

Description of Analysis Method

The CAPM model provides the relationship between the systematic risk and expected

return for assets. It is used widely in the field of corporate finance for identified the risk in

securities, calculating the expected returns from assets and cost of capital measurement. It

supports the decision-making process of investors by helping them to select a non-risky portfolio

that could yield them maximum returns in the future period of time (Bazley, Hancock and

Robinson, 2014).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The CAPM model often provides a standardization approach for analyzing the financial

performance of a company through assessing the expected rerun from the securities of a

company. The use of a standard formula in the method often provides reliable results for

comparing the returns generated by investing in different securities. The formula used is depicted

as follows:

Thus, it provides a standard financial approach for comparing the financial performance

of different companies. It helps in depicting an empirical relationship between the required return

and systematic risks that support the decision-making process of investors by investing in the

most diversified portfolio providing maximum returns. The fundamental analysis method does

not provide useful in providing an insight into the future activities of securities that can be

accessed through the use of CAPM model. Also, the horizontal and vertical financial analysis

method does not help the investors to identify the risk attached with a particular security that can

be analyzed through the use of CAPM model. It also helps in eliminating the unsystematic risk

through developing a diversified portfolio for investors so that they can achieve maximum

returns. It also helps the investors to analyze the systematic risk attached with their investment

that cannot be identified through the use of other financial analysis methods (Giovanis, 2010).

Criticism of the Model

The CAPM model is associated with the drawback of based on too many assumptions.

The major assumption that is used in the model is that the investors can borrow and lend at risk-

free rate that is not achievable in reality. The model is based on the use of historic data for

analyzing the future returns and thus the results provided by the use of the method are less

reliable. The expected returns obtained from a security are based on the various subjective

judgments of the financial analysts and therefore less reliable (Huang, 2010). This is because the

subjective assumptions of the financial analysts are very difficult to be quantified and therefore

the model does not provide an accurate estimation of the future returns to be obtained from a

security. The model is based on the assumption that securities are operating in a perfect capital

market where their prices reflect all the necessary information and therefore it is not possible to

beat the market. The model based on large number of assumptions is not used widely by the

investors for analyzing the expected returns of a security. The investors have to carry out a risk-

return trade-off for their investment decisions to be based on the results of the CAPM model.

The investors have to incorporate the use of other financial analysis models other than CAPM for

examining the financial performance of a security (Bazley, Hancock and Robinson, 2014).

3.2 Divided Growth Model (DGM)

Description of Analysis Method

The dividend growth model (DGM) is referred to as a financial valuation method used for

calculating the fair value of stock. It helps in assessing the accurate value of a stock that is,

identifying whether the stock is undervalued or overvalued by assuming that the dividend of an

entity grows at a stable rate or in perpetuity. The investors incorporate the use of DGM model for

determining the value of an investment on the basis of the dividend growth rate. It analyses the

value of equity of a company through the use of future dividends likely to be received by the

shareholders (Bender, 2013).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The DGM model is relatively easy to use and understand as compared to the traditional

method of analysis such as horizontal and vertical analysis. The method can easily calculate the

value of a stock irrespective of the market conditions through only analyzing the future dividend

payments. The simplicity of the model makes it relatively easy to be implemented and as such it

is widely used by the analysts over other methods of financial analysis models. It can also be

used to compare the stock value of different companies irrespective of their sizes and industries.

The model can be used in large number of companies and therefore it is used by the investors for

analyzing the financial growth of a company. The growth model can also be used to analyse

whether the market indices are correctly valued or whether there exist an uncertainty in the

market. The method is also helpful for the investors to predict the future value of their

investments by analyzing the share prices. Also, it restricts the shareholders to gain large

The CAPM model is associated with the drawback of based on too many assumptions.

The major assumption that is used in the model is that the investors can borrow and lend at risk-

free rate that is not achievable in reality. The model is based on the use of historic data for

analyzing the future returns and thus the results provided by the use of the method are less

reliable. The expected returns obtained from a security are based on the various subjective

judgments of the financial analysts and therefore less reliable (Huang, 2010). This is because the

subjective assumptions of the financial analysts are very difficult to be quantified and therefore

the model does not provide an accurate estimation of the future returns to be obtained from a

security. The model is based on the assumption that securities are operating in a perfect capital

market where their prices reflect all the necessary information and therefore it is not possible to

beat the market. The model based on large number of assumptions is not used widely by the

investors for analyzing the expected returns of a security. The investors have to carry out a risk-

return trade-off for their investment decisions to be based on the results of the CAPM model.

The investors have to incorporate the use of other financial analysis models other than CAPM for

examining the financial performance of a security (Bazley, Hancock and Robinson, 2014).

3.2 Divided Growth Model (DGM)

Description of Analysis Method

The dividend growth model (DGM) is referred to as a financial valuation method used for

calculating the fair value of stock. It helps in assessing the accurate value of a stock that is,

identifying whether the stock is undervalued or overvalued by assuming that the dividend of an

entity grows at a stable rate or in perpetuity. The investors incorporate the use of DGM model for

determining the value of an investment on the basis of the dividend growth rate. It analyses the

value of equity of a company through the use of future dividends likely to be received by the

shareholders (Bender, 2013).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The DGM model is relatively easy to use and understand as compared to the traditional

method of analysis such as horizontal and vertical analysis. The method can easily calculate the

value of a stock irrespective of the market conditions through only analyzing the future dividend

payments. The simplicity of the model makes it relatively easy to be implemented and as such it

is widely used by the analysts over other methods of financial analysis models. It can also be

used to compare the stock value of different companies irrespective of their sizes and industries.

The model can be used in large number of companies and therefore it is used by the investors for

analyzing the financial growth of a company. The growth model can also be used to analyse

whether the market indices are correctly valued or whether there exist an uncertainty in the

market. The method is also helpful for the investors to predict the future value of their

investments by analyzing the share prices. Also, it restricts the shareholders to gain large

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

dividend from a company as the excess profit realized than expected is re-invested by the

management (Levy, 2011).

Criticism of the Model

The model has also certain limitations as the results obtained from the model are only

based on dividend growth rate. The model does not incorporate the non-dividend factors such as

brand loyalty, customer retention and other factors that have a major effect on the value of a

company. Also, it is based on the assumption that dividend growth rate is stable that is not

possible always in reality. Therefore, the model does not provide reliable results if the dividend

growth rate is uneven and not stable. In addition to this, the model has stated that share price of a

company is largely influenced by the dividend growth rate which cannot exceed the cost of

equity which is not always the case (Besley and Brigham, 2014).

3.3 Effective Market Hypothesis

Description of Analysis Method

The effective market hypothesis is regarded as the fundamental theory for depicting the

movements in price of assets. As per the theory, the markets operate efficiently as such the price

of stocks reflects all the available information. Therefore, it is not possible for the investors to

beat the market and therefore realize larger returns than the average without undertaking the

extra financial risk (Ang, Goetzmann and Schaefer, 2011).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The major benefit of using the method of efficient market hypothesis is that managers can

realize benefits from the market condition through carefully analyzing the market prices. Also,

the managers cannot manipulate the financial information through the use of creative accounting

practices. It also makes relatively easy for the managers to carry out market speculation. The

investors can randomly select the stocks if the market is fully efficient fro realizing average

returns (Ang, Goetzmann and Schaefer, 2011).

Criticism of the Model

The theory does not provide an adequate understanding of the inefficiencies that exist in

market and the arsons for investors realizing larger returns than the average value. Thus, it is not

widely used for financial analysis of a security. It lacks practical perspectives and therefore

investors do not use it widely for financial analysis. The theory is based on the fact that investors

can access the financial information at same pace which is not true. This is because the

increasing number of communication channels such as online medium has enabled the investors

to access the financial information more rapidly and easily (Bhimani, 2006).

management (Levy, 2011).

Criticism of the Model

The model has also certain limitations as the results obtained from the model are only

based on dividend growth rate. The model does not incorporate the non-dividend factors such as

brand loyalty, customer retention and other factors that have a major effect on the value of a

company. Also, it is based on the assumption that dividend growth rate is stable that is not

possible always in reality. Therefore, the model does not provide reliable results if the dividend

growth rate is uneven and not stable. In addition to this, the model has stated that share price of a

company is largely influenced by the dividend growth rate which cannot exceed the cost of

equity which is not always the case (Besley and Brigham, 2014).

3.3 Effective Market Hypothesis

Description of Analysis Method

The effective market hypothesis is regarded as the fundamental theory for depicting the

movements in price of assets. As per the theory, the markets operate efficiently as such the price

of stocks reflects all the available information. Therefore, it is not possible for the investors to

beat the market and therefore realize larger returns than the average without undertaking the

extra financial risk (Ang, Goetzmann and Schaefer, 2011).

Supporting the Analysis Method with using empirical academic literature by illustrating it

effectiveness in overcoming the drawbacks of traditional financial analysis method

The major benefit of using the method of efficient market hypothesis is that managers can

realize benefits from the market condition through carefully analyzing the market prices. Also,

the managers cannot manipulate the financial information through the use of creative accounting

practices. It also makes relatively easy for the managers to carry out market speculation. The

investors can randomly select the stocks if the market is fully efficient fro realizing average

returns (Ang, Goetzmann and Schaefer, 2011).

Criticism of the Model

The theory does not provide an adequate understanding of the inefficiencies that exist in

market and the arsons for investors realizing larger returns than the average value. Thus, it is not

widely used for financial analysis of a security. It lacks practical perspectives and therefore

investors do not use it widely for financial analysis. The theory is based on the fact that investors

can access the financial information at same pace which is not true. This is because the

increasing number of communication channels such as online medium has enabled the investors

to access the financial information more rapidly and easily (Bhimani, 2006).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

Thus, it can be summarized from the overall discussion held in the report that traditional

method of financial analysis such as fundamental and ratio analysis are still sued widely by the

investors for analyzing the financial performance of a company. This is because the methods are

relatively easy to use and understand. However, there are several drawbacks of the method as

discussed in the report that is causing the investors to incorporate the use of contemporary

method of analysis. The most widely used contemporary methods are capital asset pricing model,

dividend growth model and effective market hypothesis. The method is advantageous over the

traditional method of analysis as these helps in predicting the future financial performance of a

company. However, there are several shortcomings in these methods and thus it is recommended

to the company to incorporate the contemporary method of financial analysis in addition to the

traditional analysis method.

Thus, it can be summarized from the overall discussion held in the report that traditional

method of financial analysis such as fundamental and ratio analysis are still sued widely by the

investors for analyzing the financial performance of a company. This is because the methods are

relatively easy to use and understand. However, there are several drawbacks of the method as

discussed in the report that is causing the investors to incorporate the use of contemporary

method of analysis. The most widely used contemporary methods are capital asset pricing model,

dividend growth model and effective market hypothesis. The method is advantageous over the

traditional method of analysis as these helps in predicting the future financial performance of a

company. However, there are several shortcomings in these methods and thus it is recommended

to the company to incorporate the contemporary method of financial analysis in addition to the

traditional analysis method.

References

Ang, A., Goetzmann, W.N. and Schaefer, S.M. 2011. The Efficient Market Theory and Evidence:

Implications for Active Investment Management. Now Publishers Inc.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Bender, R. 2013. Corporate Financial Strategy. Routledge.

Besley, S. and Brigham, E. 2014. Principles of Finance. Cengage Learning.

Bhimani, A. 2006. Contemporary Issues in Management Accounting. Oxford University Press.

Bierman, H. and Smidt, S. 2003. Financial Management for Decision Making. Beard Books.

Brigham, E. and Ehrhardt, M. 2007. Financial Management: Theory & Practice. Cengage

Learning.

Giovanis, A. 2010. Application of Capital Asset Pricing (CAPM) and Arbitrage Pricing Theory

(APT) Models in Athens Exchange Stock Market. GRIN Verlag.

Griff, M. 2014. Professional Accounting Essays and Assignments. Lulu Press, Inc.

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Huang, X. 2010. Portfolio Analysis: From Probabilistic to Credibilistic and Uncertain

Approaches. Springer Science & Business Media.

Levy, H. 2011. The Capital Asset Pricing Model in the 21st Century: Analytical, Empirical, and

Behavioral Perspectives. Cambridge University Press.

Megginson, W., Lucey, B and Smart, S. 2008. Introduction to Corporate Finance. Cengage

Learning EMEA.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

Ang, A., Goetzmann, W.N. and Schaefer, S.M. 2011. The Efficient Market Theory and Evidence:

Implications for Active Investment Management. Now Publishers Inc.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Bender, R. 2013. Corporate Financial Strategy. Routledge.

Besley, S. and Brigham, E. 2014. Principles of Finance. Cengage Learning.

Bhimani, A. 2006. Contemporary Issues in Management Accounting. Oxford University Press.

Bierman, H. and Smidt, S. 2003. Financial Management for Decision Making. Beard Books.

Brigham, E. and Ehrhardt, M. 2007. Financial Management: Theory & Practice. Cengage

Learning.

Giovanis, A. 2010. Application of Capital Asset Pricing (CAPM) and Arbitrage Pricing Theory

(APT) Models in Athens Exchange Stock Market. GRIN Verlag.

Griff, M. 2014. Professional Accounting Essays and Assignments. Lulu Press, Inc.

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Huang, X. 2010. Portfolio Analysis: From Probabilistic to Credibilistic and Uncertain

Approaches. Springer Science & Business Media.

Levy, H. 2011. The Capital Asset Pricing Model in the 21st Century: Analytical, Empirical, and

Behavioral Perspectives. Cambridge University Press.

Megginson, W., Lucey, B and Smart, S. 2008. Introduction to Corporate Finance. Cengage

Learning EMEA.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.