Strategic Financial Management: AYR Co Project Analysis Report

VerifiedAdded on 2021/12/22

|15

|4138

|97

Report

AI Summary

This report analyzes two investment proposals, Project Aspire and Project Wolf, for AYR Co to enhance market share and maximize shareholder wealth. It applies capital budgeting techniques like Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to evaluate the projects, considering initial outlays, incremental cash flows, and salvage values. The analysis includes detailed calculations and a comparison of the two projects based on quantitative and qualitative factors, such as project scope, risk management, and competitor activity. The report also considers the role of financing, costs, and stakeholder impact associated with debt and equity, and concludes with a recommendation for the superior project based on the evaluation criteria. The report emphasizes that the decision-making should not solely rely on quantitative analysis but also considers selected qualitative parameters.

STRATEGIC FINANCIAL MANAGEMENT

STUDENT ID

[Pick the date]

STUDENT ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction................................................................................................................................2

Application of Capital Budgeting Techniques...........................................................................2

Project Aspire.........................................................................................................................2

Project Wolf............................................................................................................................4

Analysis and Evaluation.............................................................................................................5

Sources of Finance.....................................................................................................................8

Conclusion................................................................................................................................10

REFERENCES.........................................................................................................................11

APPENDIX 1...........................................................................................................................13

1

Introduction................................................................................................................................2

Application of Capital Budgeting Techniques...........................................................................2

Project Aspire.........................................................................................................................2

Project Wolf............................................................................................................................4

Analysis and Evaluation.............................................................................................................5

Sources of Finance.....................................................................................................................8

Conclusion................................................................................................................................10

REFERENCES.........................................................................................................................11

APPENDIX 1...........................................................................................................................13

1

Introduction

In the given situation, a company named AYR Co is evaluating two investment proposals so

as to enhance the overall market share for the business and maximise the shareholders’

wealth. For the two proposals (projects) under consideration, market research has been

carried out and capital budgeting analysis is to be carried out based on the information

obtained from the market research. However, the decision making would not solely rely on

quantitative analysis and would also consider selected qualitative parameters. In this

background, the objective of this report is to analyse the two projects and also consider the

key qualitative parameters which should be included in decision making process. Besides,

considering the role of financing, the report also aims to enlist the associated costs and key

stakeholder impact associated with issue of debt and equity.

Application of Capital Budgeting Techniques

The two projects that need to be analysed using capital budgeting techniques are ”Project

Aspire” and “Project Wolf”. In order to apply any of the capital budgeting techniques, the

first step ought to be estimation of the incremental cash flows associated with the given

projects based on the information extended by AYR Co on the basis of the market research.

Project Aspire

A key noteworthy information related to the cost of $ 120,000 incurred in market research

which is considered as a sunk cost owing to the fact that recovery of the same is not possible

even if the company decides not to go ahead with either of the projects. Hence, this cost

would be categorised as a sunk cost which is not of significance to capital budgeting analysis

for either of the given projects (Damodaran, 2015).

On the basis of the information provided, it is apparent that project useful life is for five

years. The initial outlay for this project would lead to $2,250,000 cash outlay incurred with

regards to the acquisition of plant and machinery. Also, incremental working capital

requirement of $ 140,000 is required which is 100% recoverable at the project useful life end.

Besides, it is known that salvage value of the plant machinery at the project end would be $

375,000

Therefore, annual depreciation expense = [(Cost – Salvage Value)/Useful Life] = (2,250,000

– 375000)/5 = $375,000

2

In the given situation, a company named AYR Co is evaluating two investment proposals so

as to enhance the overall market share for the business and maximise the shareholders’

wealth. For the two proposals (projects) under consideration, market research has been

carried out and capital budgeting analysis is to be carried out based on the information

obtained from the market research. However, the decision making would not solely rely on

quantitative analysis and would also consider selected qualitative parameters. In this

background, the objective of this report is to analyse the two projects and also consider the

key qualitative parameters which should be included in decision making process. Besides,

considering the role of financing, the report also aims to enlist the associated costs and key

stakeholder impact associated with issue of debt and equity.

Application of Capital Budgeting Techniques

The two projects that need to be analysed using capital budgeting techniques are ”Project

Aspire” and “Project Wolf”. In order to apply any of the capital budgeting techniques, the

first step ought to be estimation of the incremental cash flows associated with the given

projects based on the information extended by AYR Co on the basis of the market research.

Project Aspire

A key noteworthy information related to the cost of $ 120,000 incurred in market research

which is considered as a sunk cost owing to the fact that recovery of the same is not possible

even if the company decides not to go ahead with either of the projects. Hence, this cost

would be categorised as a sunk cost which is not of significance to capital budgeting analysis

for either of the given projects (Damodaran, 2015).

On the basis of the information provided, it is apparent that project useful life is for five

years. The initial outlay for this project would lead to $2,250,000 cash outlay incurred with

regards to the acquisition of plant and machinery. Also, incremental working capital

requirement of $ 140,000 is required which is 100% recoverable at the project useful life end.

Besides, it is known that salvage value of the plant machinery at the project end would be $

375,000

Therefore, annual depreciation expense = [(Cost – Salvage Value)/Useful Life] = (2,250,000

– 375000)/5 = $375,000

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is estimated that the implementation of the project would result in generation of

incremental sales for which incremental variable cost would be incurred and information for

the same has been provided. Besides, for the capital expenditure incurred by the company,

there would be extension of capital allowances which would lead to reduction in outflow of

tax on the incremental profits made. A key aspect of the project is payment of tax in arrears

thereby implying that tax on the profits derived in a particular year would be paid at the end

of the following year only.

Appendix 1 highlights the post-tax incremental cash flows for the project under consideration

considering the information provided. Taking into consideration the projection of incremental

post tax cash flows, the evaluation of the project has been carried out using requisite capital

budgeting tools as highlighted below.

Net Present Value (NPV)

This may be defined as the net sum of present value of all the post-tax incremental cash flows

arising on account of the project during the useful life (Parrino and Kidwell, 2014). As it

considers the time value of money, hence a pivotal input in the form of discount rate is

required which is 10% for the given project. The computation of NPV is indicated as follows.

YEAR

Particulars 0 1 2 3 4 5 6

Incrementa

l cash flows

($)

-2,390,000 1,223,000 1,010,328 1,006,403 1,005,570 1,508,06

3 -166,599

Present

Value factor

(@10%)

1.00 0.91 0.83 0.75 0.68 0.62 0.56

Present

Value of

Cash flows

($)

-2,390,000 1,111,81

8 834,981 756,125 686,818 936,389 -94,041

NPV 1,842,091

From the above table, it is evident that project NPV is $ 1,842,091.

Internal Rate of Return (IRR)

IRR refers to the discount rate which produces a zero NPV (Arnold, 2015). The computation

of IRR has been facilitated through Excel with the underlying computations indicated below.

3

incremental sales for which incremental variable cost would be incurred and information for

the same has been provided. Besides, for the capital expenditure incurred by the company,

there would be extension of capital allowances which would lead to reduction in outflow of

tax on the incremental profits made. A key aspect of the project is payment of tax in arrears

thereby implying that tax on the profits derived in a particular year would be paid at the end

of the following year only.

Appendix 1 highlights the post-tax incremental cash flows for the project under consideration

considering the information provided. Taking into consideration the projection of incremental

post tax cash flows, the evaluation of the project has been carried out using requisite capital

budgeting tools as highlighted below.

Net Present Value (NPV)

This may be defined as the net sum of present value of all the post-tax incremental cash flows

arising on account of the project during the useful life (Parrino and Kidwell, 2014). As it

considers the time value of money, hence a pivotal input in the form of discount rate is

required which is 10% for the given project. The computation of NPV is indicated as follows.

YEAR

Particulars 0 1 2 3 4 5 6

Incrementa

l cash flows

($)

-2,390,000 1,223,000 1,010,328 1,006,403 1,005,570 1,508,06

3 -166,599

Present

Value factor

(@10%)

1.00 0.91 0.83 0.75 0.68 0.62 0.56

Present

Value of

Cash flows

($)

-2,390,000 1,111,81

8 834,981 756,125 686,818 936,389 -94,041

NPV 1,842,091

From the above table, it is evident that project NPV is $ 1,842,091.

Internal Rate of Return (IRR)

IRR refers to the discount rate which produces a zero NPV (Arnold, 2015). The computation

of IRR has been facilitated through Excel with the underlying computations indicated below.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

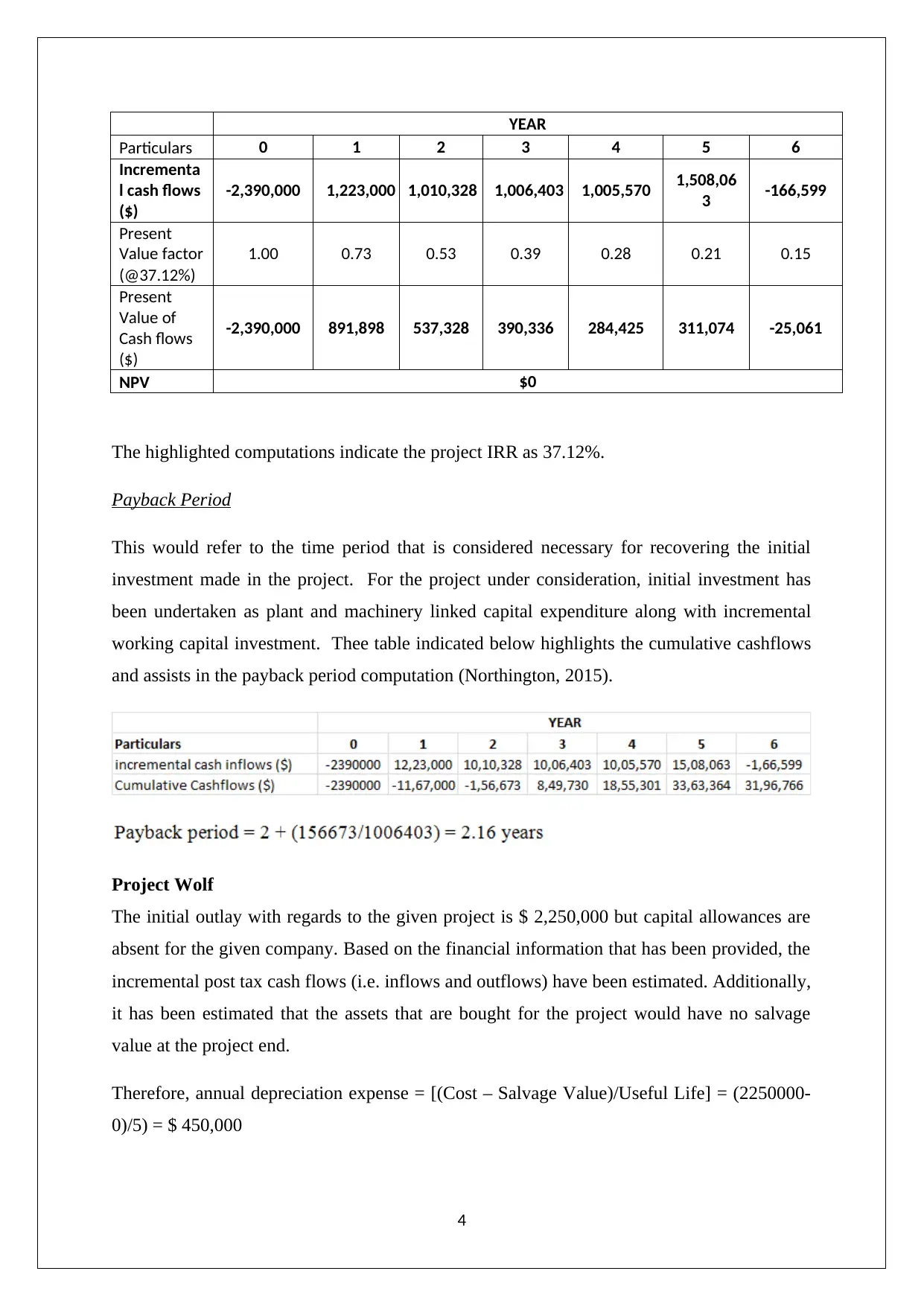

YEAR

Particulars 0 1 2 3 4 5 6

Incrementa

l cash flows

($)

-2,390,000 1,223,000 1,010,328 1,006,403 1,005,570 1,508,06

3 -166,599

Present

Value factor

(@37.12%)

1.00 0.73 0.53 0.39 0.28 0.21 0.15

Present

Value of

Cash flows

($)

-2,390,000 891,898 537,328 390,336 284,425 311,074 -25,061

NPV $0

The highlighted computations indicate the project IRR as 37.12%.

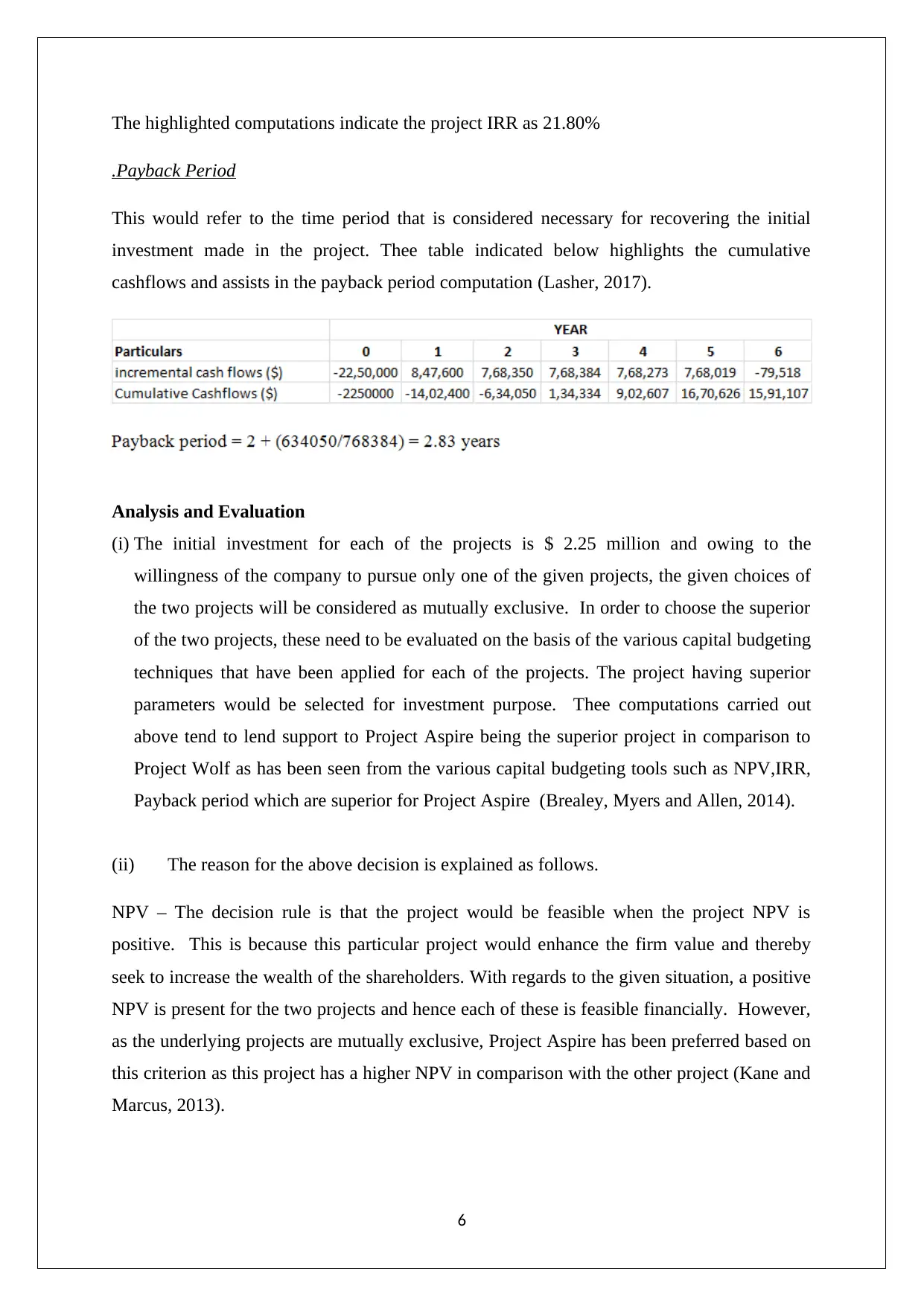

Payback Period

This would refer to the time period that is considered necessary for recovering the initial

investment made in the project. For the project under consideration, initial investment has

been undertaken as plant and machinery linked capital expenditure along with incremental

working capital investment. Thee table indicated below highlights the cumulative cashflows

and assists in the payback period computation (Northington, 2015).

Project Wolf

The initial outlay with regards to the given project is $ 2,250,000 but capital allowances are

absent for the given company. Based on the financial information that has been provided, the

incremental post tax cash flows (i.e. inflows and outflows) have been estimated. Additionally,

it has been estimated that the assets that are bought for the project would have no salvage

value at the project end.

Therefore, annual depreciation expense = [(Cost – Salvage Value)/Useful Life] = (2250000-

0)/5) = $ 450,000

4

Particulars 0 1 2 3 4 5 6

Incrementa

l cash flows

($)

-2,390,000 1,223,000 1,010,328 1,006,403 1,005,570 1,508,06

3 -166,599

Present

Value factor

(@37.12%)

1.00 0.73 0.53 0.39 0.28 0.21 0.15

Present

Value of

Cash flows

($)

-2,390,000 891,898 537,328 390,336 284,425 311,074 -25,061

NPV $0

The highlighted computations indicate the project IRR as 37.12%.

Payback Period

This would refer to the time period that is considered necessary for recovering the initial

investment made in the project. For the project under consideration, initial investment has

been undertaken as plant and machinery linked capital expenditure along with incremental

working capital investment. Thee table indicated below highlights the cumulative cashflows

and assists in the payback period computation (Northington, 2015).

Project Wolf

The initial outlay with regards to the given project is $ 2,250,000 but capital allowances are

absent for the given company. Based on the financial information that has been provided, the

incremental post tax cash flows (i.e. inflows and outflows) have been estimated. Additionally,

it has been estimated that the assets that are bought for the project would have no salvage

value at the project end.

Therefore, annual depreciation expense = [(Cost – Salvage Value)/Useful Life] = (2250000-

0)/5) = $ 450,000

4

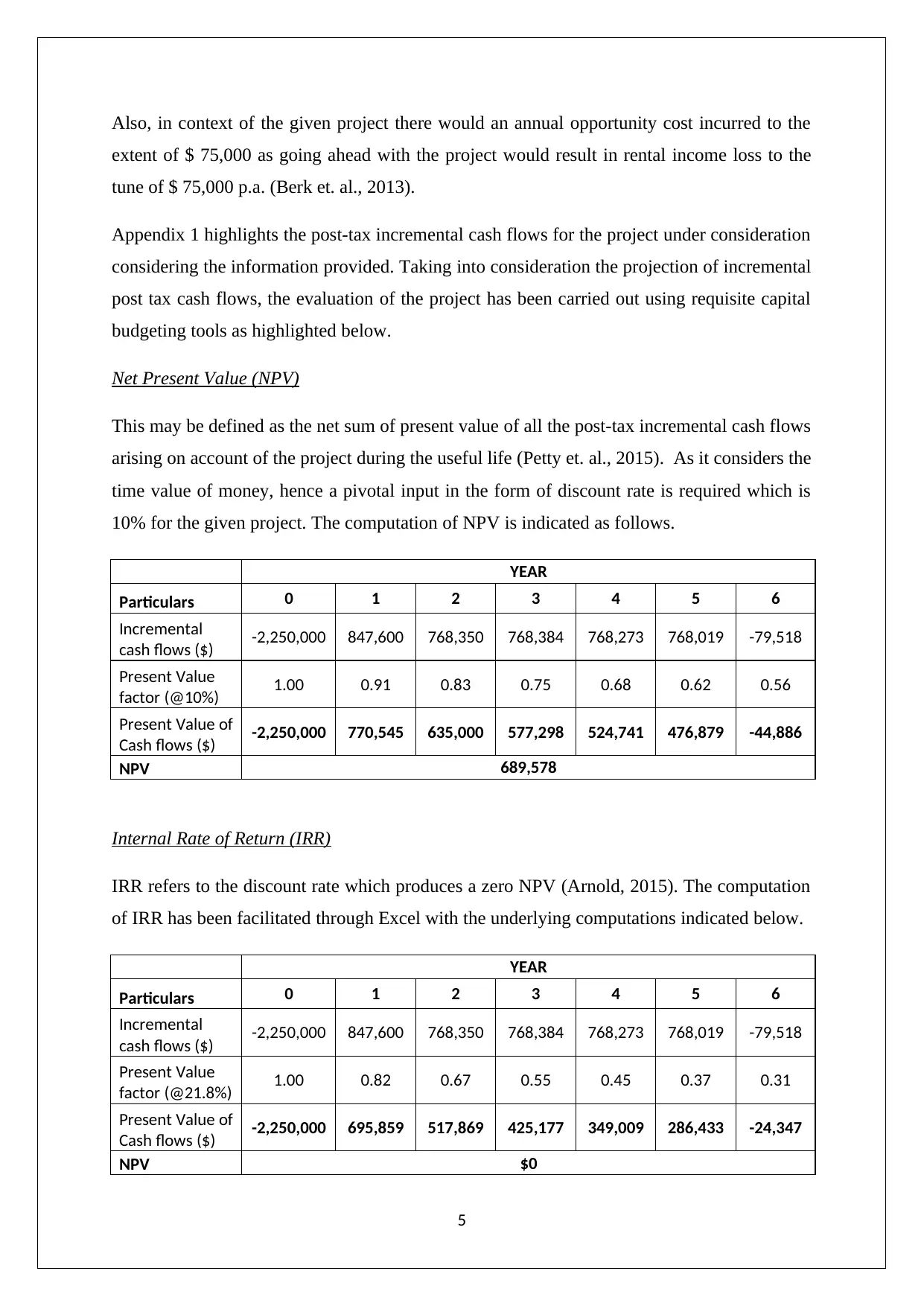

Also, in context of the given project there would an annual opportunity cost incurred to the

extent of $ 75,000 as going ahead with the project would result in rental income loss to the

tune of $ 75,000 p.a. (Berk et. al., 2013).

Appendix 1 highlights the post-tax incremental cash flows for the project under consideration

considering the information provided. Taking into consideration the projection of incremental

post tax cash flows, the evaluation of the project has been carried out using requisite capital

budgeting tools as highlighted below.

Net Present Value (NPV)

This may be defined as the net sum of present value of all the post-tax incremental cash flows

arising on account of the project during the useful life (Petty et. al., 2015). As it considers the

time value of money, hence a pivotal input in the form of discount rate is required which is

10% for the given project. The computation of NPV is indicated as follows.

YEAR

Particulars 0 1 2 3 4 5 6

Incremental

cash flows ($) -2,250,000 847,600 768,350 768,384 768,273 768,019 -79,518

Present Value

factor (@10%) 1.00 0.91 0.83 0.75 0.68 0.62 0.56

Present Value of

Cash flows ($) -2,250,000 770,545 635,000 577,298 524,741 476,879 -44,886

NPV 689,578

Internal Rate of Return (IRR)

IRR refers to the discount rate which produces a zero NPV (Arnold, 2015). The computation

of IRR has been facilitated through Excel with the underlying computations indicated below.

YEAR

Particulars 0 1 2 3 4 5 6

Incremental

cash flows ($) -2,250,000 847,600 768,350 768,384 768,273 768,019 -79,518

Present Value

factor (@21.8%) 1.00 0.82 0.67 0.55 0.45 0.37 0.31

Present Value of

Cash flows ($) -2,250,000 695,859 517,869 425,177 349,009 286,433 -24,347

NPV $0

5

extent of $ 75,000 as going ahead with the project would result in rental income loss to the

tune of $ 75,000 p.a. (Berk et. al., 2013).

Appendix 1 highlights the post-tax incremental cash flows for the project under consideration

considering the information provided. Taking into consideration the projection of incremental

post tax cash flows, the evaluation of the project has been carried out using requisite capital

budgeting tools as highlighted below.

Net Present Value (NPV)

This may be defined as the net sum of present value of all the post-tax incremental cash flows

arising on account of the project during the useful life (Petty et. al., 2015). As it considers the

time value of money, hence a pivotal input in the form of discount rate is required which is

10% for the given project. The computation of NPV is indicated as follows.

YEAR

Particulars 0 1 2 3 4 5 6

Incremental

cash flows ($) -2,250,000 847,600 768,350 768,384 768,273 768,019 -79,518

Present Value

factor (@10%) 1.00 0.91 0.83 0.75 0.68 0.62 0.56

Present Value of

Cash flows ($) -2,250,000 770,545 635,000 577,298 524,741 476,879 -44,886

NPV 689,578

Internal Rate of Return (IRR)

IRR refers to the discount rate which produces a zero NPV (Arnold, 2015). The computation

of IRR has been facilitated through Excel with the underlying computations indicated below.

YEAR

Particulars 0 1 2 3 4 5 6

Incremental

cash flows ($) -2,250,000 847,600 768,350 768,384 768,273 768,019 -79,518

Present Value

factor (@21.8%) 1.00 0.82 0.67 0.55 0.45 0.37 0.31

Present Value of

Cash flows ($) -2,250,000 695,859 517,869 425,177 349,009 286,433 -24,347

NPV $0

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The highlighted computations indicate the project IRR as 21.80%

.Payback Period

This would refer to the time period that is considered necessary for recovering the initial

investment made in the project. Thee table indicated below highlights the cumulative

cashflows and assists in the payback period computation (Lasher, 2017).

Analysis and Evaluation

(i) The initial investment for each of the projects is $ 2.25 million and owing to the

willingness of the company to pursue only one of the given projects, the given choices of

the two projects will be considered as mutually exclusive. In order to choose the superior

of the two projects, these need to be evaluated on the basis of the various capital budgeting

techniques that have been applied for each of the projects. The project having superior

parameters would be selected for investment purpose. Thee computations carried out

above tend to lend support to Project Aspire being the superior project in comparison to

Project Wolf as has been seen from the various capital budgeting tools such as NPV,IRR,

Payback period which are superior for Project Aspire (Brealey, Myers and Allen, 2014).

(ii) The reason for the above decision is explained as follows.

NPV – The decision rule is that the project would be feasible when the project NPV is

positive. This is because this particular project would enhance the firm value and thereby

seek to increase the wealth of the shareholders. With regards to the given situation, a positive

NPV is present for the two projects and hence each of these is feasible financially. However,

as the underlying projects are mutually exclusive, Project Aspire has been preferred based on

this criterion as this project has a higher NPV in comparison with the other project (Kane and

Marcus, 2013).

6

.Payback Period

This would refer to the time period that is considered necessary for recovering the initial

investment made in the project. Thee table indicated below highlights the cumulative

cashflows and assists in the payback period computation (Lasher, 2017).

Analysis and Evaluation

(i) The initial investment for each of the projects is $ 2.25 million and owing to the

willingness of the company to pursue only one of the given projects, the given choices of

the two projects will be considered as mutually exclusive. In order to choose the superior

of the two projects, these need to be evaluated on the basis of the various capital budgeting

techniques that have been applied for each of the projects. The project having superior

parameters would be selected for investment purpose. Thee computations carried out

above tend to lend support to Project Aspire being the superior project in comparison to

Project Wolf as has been seen from the various capital budgeting tools such as NPV,IRR,

Payback period which are superior for Project Aspire (Brealey, Myers and Allen, 2014).

(ii) The reason for the above decision is explained as follows.

NPV – The decision rule is that the project would be feasible when the project NPV is

positive. This is because this particular project would enhance the firm value and thereby

seek to increase the wealth of the shareholders. With regards to the given situation, a positive

NPV is present for the two projects and hence each of these is feasible financially. However,

as the underlying projects are mutually exclusive, Project Aspire has been preferred based on

this criterion as this project has a higher NPV in comparison with the other project (Kane and

Marcus, 2013).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IRR – For a project to be financially viable, the project IRR should exceed the cost of capital.

For this project, the NPV would be positive and hence the shareholders’ wealth would be

increased. For the given two projects, the cost of capital is given as 10%, As the respective

IRR of these two projects tend to exceed 10%, hence each of these two projects is feasible.

But the situation demands that the superior project ought to be chosen and in this regards

Project Aspire is preferred owing to it having a greater value of IRR than the corresponding

value of Project Wolf (Northington, 2015).

Payback Period – For a project to be financially viable, the project payback period must be

smaller than the project useful life which is five years for each of the projects being

considered. With regards to the given criterion, each of the two projects are feasible as the

payback period tends to lesser than five years. But the situation demands that the superior

project ought to be chosen and in this regards Project Aspire is preferred owing to it having a

lower value of payback period in comparison to Project Wolf (Gitman, Juchaou, and

Flanagan, 2017).

(iii) It is essential that the decision should not be solely driven by quantitative aspects and

the following qualitative aspects also ought to be taken into consideration (Graham and

Smart,2012).

1) A key aspect to be considered is the project scope. With regards to Project Aspire, the

company would target the existing customers and would aim to introduce new products in

the existing product range. Hence, the objective of the project is to garner a higher share

of the existing customer base and derive higher revenue per customer by offering more

products. In sharp contrast, Project Wolf is aimed at venturing into a new sphere of

business and targeting those customers which are not currently being targeted by the

company. Thus, from the strategy angle, Project Wolf would be considered superior as it

tends to widen the customer base of the company and would bring about cross selling

opportunities in the future. Besides, from the perspective of risk management, it would

make sense for the company to diversify. Business diversification is carried out by Project

Wolf and hence the risk would be lowered especially when the existing business of the

company underperforms. As a result, the Project Wolf is preferable to Project Aspire on

this count.

2) Another critical parameter to be considered is competitor activity along with underlying

trends in market. In the context of only five year, it may be prudent to go ahead with

project Aspire but considering the strategic planning and long term vision for the

7

For this project, the NPV would be positive and hence the shareholders’ wealth would be

increased. For the given two projects, the cost of capital is given as 10%, As the respective

IRR of these two projects tend to exceed 10%, hence each of these two projects is feasible.

But the situation demands that the superior project ought to be chosen and in this regards

Project Aspire is preferred owing to it having a greater value of IRR than the corresponding

value of Project Wolf (Northington, 2015).

Payback Period – For a project to be financially viable, the project payback period must be

smaller than the project useful life which is five years for each of the projects being

considered. With regards to the given criterion, each of the two projects are feasible as the

payback period tends to lesser than five years. But the situation demands that the superior

project ought to be chosen and in this regards Project Aspire is preferred owing to it having a

lower value of payback period in comparison to Project Wolf (Gitman, Juchaou, and

Flanagan, 2017).

(iii) It is essential that the decision should not be solely driven by quantitative aspects and

the following qualitative aspects also ought to be taken into consideration (Graham and

Smart,2012).

1) A key aspect to be considered is the project scope. With regards to Project Aspire, the

company would target the existing customers and would aim to introduce new products in

the existing product range. Hence, the objective of the project is to garner a higher share

of the existing customer base and derive higher revenue per customer by offering more

products. In sharp contrast, Project Wolf is aimed at venturing into a new sphere of

business and targeting those customers which are not currently being targeted by the

company. Thus, from the strategy angle, Project Wolf would be considered superior as it

tends to widen the customer base of the company and would bring about cross selling

opportunities in the future. Besides, from the perspective of risk management, it would

make sense for the company to diversify. Business diversification is carried out by Project

Wolf and hence the risk would be lowered especially when the existing business of the

company underperforms. As a result, the Project Wolf is preferable to Project Aspire on

this count.

2) Another critical parameter to be considered is competitor activity along with underlying

trends in market. In the context of only five year, it may be prudent to go ahead with

project Aspire but considering the strategic planning and long term vision for the

7

company, it might be possible that the company may need to shift into new businesses

owing to altering business dynamics whereby it does not make sense to remain in the

current business for long due to concerns regarding growth, competition, declining

profitability. This is quite true in the context of business which are impacted by change in

technology and therefore need to constantly reinvent the business model (Brealey, Myers

and Allen, 2014).

The above discussion leads to the conclusion that in terms of the qualitative parameters and

consideration, Project Wolf seems to be the superior choice as it would lead the company into

a new business and hence lead to diversification of business risks. It is essential that a

strategic decision ought to be taken by the company considering not only the present value

added but also the future aspects particularly the industry and competitive dynamics. This

would provide an estimate of the project’s strategic fit which is as imperative as the

quantitative performance and hence based on both these aspects, final decision ought to be

taken based on the subjective importance that the decision maker provides to these factors

(Ehrhardt and Brigham, 2016).

Sources of Finance

(i) With regards to financing, two common sources exist in the form of debt and equity. Debt

financing would refer to financing where money is raised in the form of debt and paid

back at the time of maturity with regular interest payments (Damodaran, 2015). Equity

based financing highlights the financing which is raised through the issue of shares. In this

funding, there is no need to repay the amount of money that is raised and also interest

payment is absent (Arnold, 2015). However, there is dilution of equity which can lead to

loss of control of the promoters. On the other hand, there is higher credit risk with regards

to debt financing and hence a trade-off is involved with regards to usage of either

financing source (Christensen et. al., 2013).

(ii) The returns for a lender would be earned in the form of interest payments which

would be over and above debt repayment. These interest payments periodically received

constitute the returns for extending debt funding to a borrower and usually this is assured.

In sharp contrast, the returns for equity investors are earned through capital appreciation as

the firm value enhances coupled with dividend payments. However, these are not assured

as there is no compulsion on the company to pay dividends (Northington, 2015).

8

owing to altering business dynamics whereby it does not make sense to remain in the

current business for long due to concerns regarding growth, competition, declining

profitability. This is quite true in the context of business which are impacted by change in

technology and therefore need to constantly reinvent the business model (Brealey, Myers

and Allen, 2014).

The above discussion leads to the conclusion that in terms of the qualitative parameters and

consideration, Project Wolf seems to be the superior choice as it would lead the company into

a new business and hence lead to diversification of business risks. It is essential that a

strategic decision ought to be taken by the company considering not only the present value

added but also the future aspects particularly the industry and competitive dynamics. This

would provide an estimate of the project’s strategic fit which is as imperative as the

quantitative performance and hence based on both these aspects, final decision ought to be

taken based on the subjective importance that the decision maker provides to these factors

(Ehrhardt and Brigham, 2016).

Sources of Finance

(i) With regards to financing, two common sources exist in the form of debt and equity. Debt

financing would refer to financing where money is raised in the form of debt and paid

back at the time of maturity with regular interest payments (Damodaran, 2015). Equity

based financing highlights the financing which is raised through the issue of shares. In this

funding, there is no need to repay the amount of money that is raised and also interest

payment is absent (Arnold, 2015). However, there is dilution of equity which can lead to

loss of control of the promoters. On the other hand, there is higher credit risk with regards

to debt financing and hence a trade-off is involved with regards to usage of either

financing source (Christensen et. al., 2013).

(ii) The returns for a lender would be earned in the form of interest payments which

would be over and above debt repayment. These interest payments periodically received

constitute the returns for extending debt funding to a borrower and usually this is assured.

In sharp contrast, the returns for equity investors are earned through capital appreciation as

the firm value enhances coupled with dividend payments. However, these are not assured

as there is no compulsion on the company to pay dividends (Northington, 2015).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The underlying financing means cost is dependent on the associated risk with the underlying

source. As per the portfolio theory, the source which has a higher associated risk would

provide higher returns which essentially act as an incentive for the investor. The higher

amount of risk is associated with equity as repayment is not done and the results are not

assured and it is quite possible that negative returns are also earned. Also, the priority of

equity investors with regards to business liquidation is the lowest and usually has no proceeds

from equity (Brealey, Myers and Allen, 2014). This implies that the returns for the

equityholders would arise only on account of appreciation of the value of company and

dividend payment. Owing to this higher risk, the equity investors would expect a higher

returns than debt investors (Brigham and Houston, 2014).

For debt funding, the underlying risk is comparatively lower considering that debt repayment

is assured and is typically backed by a collateral in the form of a fixed assets coupled with

financial securities. Thus, in the event of liquidation, the underlying collateral and other

business assets would be used to discharge the outstanding debts. Besides, the interest

payments typically are monthly and hence in case of outstanding pending interest, the loan

amount can be recalled (Ehrhardt and Brigham, 2016).

The summary of the discussion above is that owing to higher risk associated with equity

based financing, the returns desired by equity investors is significantly higher when

compared with the debtors that are at considerably lesser risk.

(iii) The data provided in the question indicates the firm WACC as 10%. Besides, it is also

evident that the current capital structure comprises of majority equity based funding with

minority funding from debt. For the extra $ 2.25 million funding the company may

explore the following options.

100% equity financing – For this option, the cost of financing would be comparatively higher

as no debt based funding is used. This would alter the WACC that is being current used and

hence would adversely impact the project viability as the WACC would be greater than the

current value of 10%. As a result, it does not seem to be a suitable funding mechanism (Berk

et. al., 2013).

100% debt financing – The costs associated with debt based financing is considering lower in

comparison to equity based financing. Thus, if the complete project is funded using debt, then

9

source. As per the portfolio theory, the source which has a higher associated risk would

provide higher returns which essentially act as an incentive for the investor. The higher

amount of risk is associated with equity as repayment is not done and the results are not

assured and it is quite possible that negative returns are also earned. Also, the priority of

equity investors with regards to business liquidation is the lowest and usually has no proceeds

from equity (Brealey, Myers and Allen, 2014). This implies that the returns for the

equityholders would arise only on account of appreciation of the value of company and

dividend payment. Owing to this higher risk, the equity investors would expect a higher

returns than debt investors (Brigham and Houston, 2014).

For debt funding, the underlying risk is comparatively lower considering that debt repayment

is assured and is typically backed by a collateral in the form of a fixed assets coupled with

financial securities. Thus, in the event of liquidation, the underlying collateral and other

business assets would be used to discharge the outstanding debts. Besides, the interest

payments typically are monthly and hence in case of outstanding pending interest, the loan

amount can be recalled (Ehrhardt and Brigham, 2016).

The summary of the discussion above is that owing to higher risk associated with equity

based financing, the returns desired by equity investors is significantly higher when

compared with the debtors that are at considerably lesser risk.

(iii) The data provided in the question indicates the firm WACC as 10%. Besides, it is also

evident that the current capital structure comprises of majority equity based funding with

minority funding from debt. For the extra $ 2.25 million funding the company may

explore the following options.

100% equity financing – For this option, the cost of financing would be comparatively higher

as no debt based funding is used. This would alter the WACC that is being current used and

hence would adversely impact the project viability as the WACC would be greater than the

current value of 10%. As a result, it does not seem to be a suitable funding mechanism (Berk

et. al., 2013).

100% debt financing – The costs associated with debt based financing is considering lower in

comparison to equity based financing. Thus, if the complete project is funded using debt, then

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the WACC would be lower but there would be higher repayment burden along with interest

outflow associated with the project (Murray and Goyal, 2008).

However, if the debt and equity mix is used by the company for financing the project with

individual contributions in the same ratio as the existing capital structure, then in such case

the WACC would be 10%.

(iv) The finance source selection will have significant impact on various stakeholders such

as lenders and shareholders. This has been highlighted as indicated below.

Equity Financing – Using equity based financing to raise money for the project would lead to

equity dilution for the existing investors. Further, owing to rise in the number of shares

outstanding, the EPS will reduce till the time incremental earnings are received from the

project. If the earnings estimated do not materialise, then the price would drop which would

lower the wealth of shareholders. Owing to more outstanding shares, there would be higher

market float which may lead to restricted capital appreciation (Lasher, 2017)

.

Besides, with regards to the promoters, excessive equity dilution could result in control being

lost which may adversely impact the long term vision and strategic intent for the company.

Also, this would increase the WACC owing to higher cost being associated with the same.

However, lenders consider equity financing as positive as it improves the balance sheet

strength and also improves the capability of the business to service the existing debt on the

books (Brealey, Myers and Allen, 2014).

Debt Financing – If the debt levels remain within limits and do not result in over-leveraging

of the balance sheet, then adverse impacts are quite minimal. Owing to payment of interest,

there would be reduction in EPS till the time incremental earnings grow and failure in this

regards would lower the share price (Christensen et. al., 2013). Considering the lower cost of

debt, debt financing is preferred by the shareholders to the extent that the debt can be

serviced by the company. Lenders do not prefer assumption of incremental debt as the

balance sheet may become overleveraged and also the ability of the firm to service the

existing lenders may be impaired leading to higher credit risk (Kane and Marcus, 2013).

On account of the above discussion, it would be prudent to conclude that adhering to any one

of the above discussed funding means would not be appropriate and a mix of debt and equity

based funding in the same proportion as optimum capital structure would be best suited.

10

outflow associated with the project (Murray and Goyal, 2008).

However, if the debt and equity mix is used by the company for financing the project with

individual contributions in the same ratio as the existing capital structure, then in such case

the WACC would be 10%.

(iv) The finance source selection will have significant impact on various stakeholders such

as lenders and shareholders. This has been highlighted as indicated below.

Equity Financing – Using equity based financing to raise money for the project would lead to

equity dilution for the existing investors. Further, owing to rise in the number of shares

outstanding, the EPS will reduce till the time incremental earnings are received from the

project. If the earnings estimated do not materialise, then the price would drop which would

lower the wealth of shareholders. Owing to more outstanding shares, there would be higher

market float which may lead to restricted capital appreciation (Lasher, 2017)

.

Besides, with regards to the promoters, excessive equity dilution could result in control being

lost which may adversely impact the long term vision and strategic intent for the company.

Also, this would increase the WACC owing to higher cost being associated with the same.

However, lenders consider equity financing as positive as it improves the balance sheet

strength and also improves the capability of the business to service the existing debt on the

books (Brealey, Myers and Allen, 2014).

Debt Financing – If the debt levels remain within limits and do not result in over-leveraging

of the balance sheet, then adverse impacts are quite minimal. Owing to payment of interest,

there would be reduction in EPS till the time incremental earnings grow and failure in this

regards would lower the share price (Christensen et. al., 2013). Considering the lower cost of

debt, debt financing is preferred by the shareholders to the extent that the debt can be

serviced by the company. Lenders do not prefer assumption of incremental debt as the

balance sheet may become overleveraged and also the ability of the firm to service the

existing lenders may be impaired leading to higher credit risk (Kane and Marcus, 2013).

On account of the above discussion, it would be prudent to conclude that adhering to any one

of the above discussed funding means would not be appropriate and a mix of debt and equity

based funding in the same proportion as optimum capital structure would be best suited.

10

Conclusion

The discussion above highlights that on the basis of only the quantitative aspects, the project

Aspire would be preferred. But taking into consideration the qualitative aspects and long

term strategic planning, Project Wolf is a preferred option. Further, in order to decide on the

best project, the decision maker would need to consider both the quantitative and qualitative

aspects. Also, with regards to raising funding through debt or equity, it is apparent that there

are associated pros and cons with both means of financing and neither of the method is

without demerits. As a result, it is prudent that a mix of both these financing means must be

considered in the ratio of optimum capital structure so as to maximise the benefits derived.

11

The discussion above highlights that on the basis of only the quantitative aspects, the project

Aspire would be preferred. But taking into consideration the qualitative aspects and long

term strategic planning, Project Wolf is a preferred option. Further, in order to decide on the

best project, the decision maker would need to consider both the quantitative and qualitative

aspects. Also, with regards to raising funding through debt or equity, it is apparent that there

are associated pros and cons with both means of financing and neither of the method is

without demerits. As a result, it is prudent that a mix of both these financing means must be

considered in the ratio of optimum capital structure so as to maximise the benefits derived.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.