Strategic Financial Management Project Report and Analysis

VerifiedAdded on 2023/04/11

1

Project Report: Strategic Financial Management

Paraphrase This Document

Contents

Task 1: Memo...................................................................................................................3

Task 2................................................................................................................................7

Introduction...................................................................................................................7

Source of funding.........................................................................................................7

Recommendation and conclusion...............................................................................11

Task 3..............................................................................................................................14

References.......................................................................................................................26

Appendix.........................................................................................................................28

Task 1: Memo

To,

Investhical CEO

48, New South Wales,

Australia.

Dear Sir,

Hope you are doing well!

It is always important for a business to measure and evaluate the stock performance and

position of financial activities of an organization before making an investment into the

company. As Investhical is looking for 3 stocks from different sector to make an investment,

5 different stocks from 5 different sectors have been collected and compared to reach over

best 3 best stocks. Sonic healthcare, Woolworths, BHP Billiton, Boral limited and National

Takaful’s stock have been considered to evaluate the investment and return positions of the

stock. In order to make an investment decision, ratio analysis study has been conducted over

all the 5 stocks and different key financial position such as profitability, asset efficiency,

liquidity, market position and capital structure has been calculated to reach over conclusion

about investment.

The profitability ratio analysis study explains that performance of Sonic health care, BHP

Billiton and National Takaful is better than Woolworths and Boral limited.

Ratio Calculations Sonic

Healthcar

e

Woolwort

hs

BHP Billiton Boral

Limited

National

Takaful

Profitability Ratios: 2018 2018 2018 2018 2018

Return on Capital

employed

Operating profit / 660,251 -9,291,000 14,751,000 210 92,706

Capital employed

(total assets - current

liabilities)

4,776,41

2

14,362,00

0

98,004,000 8,515 262,112

Answer: % 13.82% -64.69% 15.05% 2.47% 35.37%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on assets

Net profit / 475,606 1,724,000 3,705,000 441 12,343

Total assets 8,200,93

4

23,558,00

0

111,993,000 9,510 399,815

Answer: 5.8% 7.3% 3.3% 4.6% 3.1%

Net profit margin %

Net profit / 475,606 1,724,000 3,705,000 441 12,343

Sales Revenue % 5,476,175 56,726,000 43,638,000 5,731 201,564

Answer: 8.7% 3.0% 8.5% 7.7% 6.1%

(Annual report, 2018)

Further, the asset efficiency ratio study explains that performance of Sonic health

care, Boral Limited and National Takaful is better than Woolworths and BHP Billiton.

Ratio Calculations Sonic

Healthcare

Woolworths BHP

Billiton

Boral

Limited

National

Takaful

Asset Efficiency Ratios 2018 2018 2018 2018 2018

Creditors turnover

days

Accounts payable/ 207,024 5,316,000 5,977,000 752 137,703

Cost of sales 918,211 40,256,000 10,916,000 3,829 108,858

Answer: (note the

above needs to be x

365)

#

days

0.23 0.13 0.55 0.20 1.26

Debtors Turnover

(days)

Average trade debtors / 716,101 420,000 3,096,000 876 240,320

Sales revenue (note

used operating revenue)

#

days

5,476,175 56,726,000 43,638,00

0

5,73

1

201,56

4

Answer: (note the

above needs to be x 365)

0.13 0.01 0.07 0.15 1.19

(Annual report, 2018)

More to it, study has been done on liquidity position of the stocks and found that performance

of Sonic health care, Boral Limited and National Takaful is better than Woolworths and BHP

Billiton.

Ratio Calculations Sonic

Healthcare

Woolworths BHP

Billiton

Boral

Limited

National

Takaful

Liquidity Ratios 2018 2018 2018 2018 2018

Paraphrase This Document

Current Ratio

Current Assets / 1,231,709 7,181,000 35,130,000 1,738 159,495

Current liabilities 867,863 9,196,000 13,989,00

0

99

5

138,22

7

Answer: 1.42 0.78 2.51 1.75 1.15

Quick ratio

Current Assets -

Inventory /

1,124,929 2,948,000 31,366,000 1,124 159,495

Current Liabilities 867,863 9,196,000 13,989,00

0

99

5

138,22

7

Answer: 1.30 0.32 2.24 1.13 1.15

(Annual report, 2018)

Capital structure study has been conducted further in order to measure the management of

solvency level. Study defines that Sonic health care, Boral Limited and BHP Billiton is better

than Woolworths and National Takaful.

Ratio Calculations Sonic

Healthcare

Woolworths BHP

Billiton

Boral

Limited

National

Takaful

Capital Structure Ratios 2018 2018 2018 2018 2018

Debt equity ratio

Total liabilities / 4,023,527 13,077,000 56,401,000 3,780 303,950

Total equity 4,177,407 10,481,000 55,592,000 5,731 95,865

Answer: % 0.96 1.25 1.01 0.66 3.17

Debt ratio

Total debt / 4,023,527 13,077,000 56,401,000 3,780 303,950

Total assets 8,200,934 23,558,000 111,993,000 9,510 399,815

Answer: % 0.49 0.56 0.50 0.40 0.76

Interest Coverage Ratio

EBIT / 660,251 -9,291,000 14,751,000 210 92,706

Net Finance Costs (used

net interest expense)

78,444 154,000 1,029,000 106 12,481

Answer: times

p.a

8.42 -60.33 14.34 1.98 7.43

(Annual report, 2018)

Lastly, market value ratios define that earnings per share of Sonic health care, Woolworths

and BHP Billiton is better in the market.

Ratio Calculations Sonic

Healthcare

Woolworths BHP

Billiton

Boral

Limited

National

Takaful

Market value

Ratios

2018 2018 2018 2018 2018

Earnings per share

Net income 475,606 1,724,000 3,705,000 441 12,343

Weighted average

shares outstanding

422,212 1,300,500 2,661,500 1,172 150,000

Answer: 1.13 1.33 1.39 0.38 0.08

(Annual report, 2018)

Hence, the study recommends Investhical to invest in Sonic Healthcare, BHP Billiton and

National Takaful to reduce the financial risk and maintain the return level for a long time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2:

Introduction:

Funds management is one of the crucial works of financial manager of an

organization. It is important for the manager to set the solvency position and reduce the risk

through raising the fund in such a way that all the short term and long term funds could be

paid off easily with the help of available resources in the market. In order to raise the funds

for short term and long term, bank loan, creditors, overdrafts, equity, debentures etc are the

main source (Zimmerman and Yahya-Zadeh, 2011). The report focuses on 3 companies Sonic

Healthcare, BHP Billiton and National Takaful to make an investment. In order to make

investment in these companies, Investhical would require £ 3,000,000 which would be raised

through taking the help of short term and long term capital sources. The main focus of the

report is on various funds which could be raised for short term and long term to meet the

demand of the company and maintain the solvency, liquidity and profitability position of the

company.

Source of funding:

Funding is a process in which financial resources are provided to the company in form

of money or other financial resources in order to finance the need, proposal, project or any

program in an organization. Mainly the source of funding is divided into 2 categories i.e.

short term funds and long term funds. Those funds which are generated by the company for

short term projects such as working capital, operation etc is called short term funds. Further,

those funds which are generated by the company for long term projects such as new

investment, property, plant and equipment, new project etc is called long term funds (Weil,

Schipper and Francis, 2013). Short term funds are generated by the company for the projects

or operations which would take place in less than 1 year whereas all those funds which are

generated for more than 1 year is called long term funds.

Short term funds:

Basically, a firm is required to raise the funds through short term sources to manage

the daily activities of the company and maintain the working capital level. Short term

obligations are met by the company through generating the short term funds. Overall short

term activities such as management of liquidity level, production cycle, enough funds etc are

managed through short term funds only (Horngren, 2009). In the report, few methods of short

Paraphrase This Document

term have been studied which could be used by Investhical to manage the performance and

production cycle of the company:

Bank overdraft:

It is one of the common sources of short term funds. Company could raise the funds

till an overdraft limit from the bank for short term to manage the operations and needs of the

company. Bank overdraft is quite easier way to generate the funds. However, overdraft

interest rate is higher and user is obligated to pay the funds in shorter time (Deegan, 2013). In

terms of Invethical case, this is not a good idea as company wants to generate the fund for

longer period.

Advance from customers:

It is mostly used source of short term funds. Company could raise the funds through

taking the online payment from the customers of the company (Edwards, 2013). Advanced

from customers is quite easier way to generate the funds as well as company is not required

to do any documentation. However, there is a risk of goodwill as well as liquidity position of

the company. In terms of Investhical case, this is not a good idea as company wants to

generate the fund for longer period.

Overdraft agreement:

Overdraft agreement is a source of short term funds. Company could raise the funds

through selling some overdraft agreement in the market. It is not required for the company to

be checked and evaluated for overdraft agreement. However, there is a risk of cash flow

fluctuations and outflow limit (DRURY, 2013). In terms of Investhical case, this is not a

good idea as company wants to generate the fund for longer period.

Treasury bills:

T-Bills are a source of short term funds. Company could raise the funds through

selling some T bills in the market. It is quite simple to sell and generate the funds. However,

there is a risk of cash flow fluctuations and liquidity position of the company. In terms of

Investhical case, this is not a good idea as company wants to generate the fund for longer

period.

Commercial paper:

Commercial paper is a source of short term funds. Company could raise the funds

through selling some commercial paper in the market. It is quite simple to sell and generate

the funds. However, there is a risk of cash flow fluctuations and liquidity position of the

company. In terms of Investhical case, this is not a good idea as company wants to generate

the fund for longer period.

Long term funds:

Basically, a firm is required to raise the funds through long term sources to manage

the long term activities of the company and maintain the funds for long term projects. Long

term obligations are met by the company through generating the long term funds. Overall

long term activities such as investment into fixed assets, new projects etc are managed

through long term funds only (Deegna, 2012). In the report, few methods of long term have

been studied which could be used by Investhical to manage the funds for long term:

Long term loan:

It is one of the common sources of long term funds. Company could raise the funds

through raking long term loans from bank for long time to manage the various new long term

projects and long term sustainability of the business. Loan from bank is quite easier way to

generate the funds as only credit history and financial statement of the company are checked.

However, it is important for the company to repay the loans in the given time along with the

higher interest. In terms of Invethical case, this is a good idea as currently the cost of capital

of the bank loan of the company is 0.07%. It explains that the funds would be managed by

the company in lower cost.

Cost of bank loan:

Net finance cost 55.00

Less: Tax @35% 19.25

After tax cost of debt 35.75

Bank loan amount 1,585.00

After tax cost of bank loan

(%) 2.26%

(Deegan, 2012)

Borrowings:

It is one of the common sources of long term funds. Company could raise the funds

through taking borrowings from the market or any financial institution on the basis of credit

rating and fund payment system of the company. Borrowings are quite easier way to generate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the funds as only credit history and financial statement of the company are checked.

However, it is important for the company to repay the loans in the given time along with the

higher interest. In terms of Invethical case, this is a good idea as currently the cost of capital

of the borrowings of the company is 0.07% (Ward, 2012). It explains that the funds would be

managed by the company in lower cost.

Cost of borrowings:

Net finance cost 85.00

Less: Tax @35% 29.75

After tax cost of debt 55.25

Borrowings amount 2,125.00

After tax cost of borrowings

(%) 2.60%

Debts:

Debt is the most used and common source of long term funds. Company could raise

the funds through issuing the debentures in the market. Debentures are quite easier way to

generate the funds as only available resources and overall financial and credit position of the

company is checked by the agencies and capital market. However, it is important for the

company to repay the debt payment in the given time along with the higher interest. In terms

of Invethical case, this is a good idea as currently the cost of capital of the borrowings of the

company is 0.07% (Lord, 2007). It explains that the funds would be managed by the

company in lower cost.

Cost of debt:

Net finance cost 167.00

Less: Tax @35% 58.45

After tax cost of debt 108.55

Borrowings amount 165,723.00

After tax cost of debt (%) 0.07%

Equity and Retained earnings:

Paraphrase This Document

Lastly, owner’s equity, retained earnings and equity funds are the long term funds

which are managed by every organization. Company could raise the funds through issuing the

shares in the market, retain some amount from net profit generated and owners could invest

the fund for long term betterment of the company. Equity is quite easier way to generate the

funds as no tough documentation is required (Schwartz, 2017). However, it impacts over the

solvency and capital structure level of the company. In terms of Invethical case, this is a good

idea as currently the cost of equity of the company is 3.33%. It explains that the funds would

be managed by the company in lower cost.

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of return 8%

C. Beta 0.11

D. CAPM 3.33%

Recommendation and conclusion:

The overall study over Investhical explains that Investhical requires £ 3,000,000 to

make an investment in Sonic Healthcare, BHP Billiton and National Takaful. Currently,

company owns £ 2,000,000 and additional funds of £ 1,000,000 is required to make the

investment. Various available resources in the market for the company has been studied and

on the basis of study, it has been concluded that short tern funds are not feasible for this case

as it would raise the funds for short tern only and company requires fund for long term

project. Further, it has been identified that cost of debt, cost of borrowings, cost of bank loan

and cost of equity of the company is 0.07%, 2.60%, 2.26% and 3.33%.

Through the investigation, it has been concluded that it is best for the company to

raise £ 6,00,000 through equity and £ 4,00,000 through debt to manage the solvency level,

capital risk and other financial risk of the company. Through study, it has been recognized

that below are the market share, cost of debt, cost of equity and total cost of capital of the

company:

Book Value Weights

Debt Equity Total

Equity shares

£

600,000

Value of debt (short term £

borrowings+ long term

borrowings) 400,000

Total

£

400,000

£

600,000

£

1,000,000

D. Weights 40.00% 60.00%

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of return 8%

C. Beta 0.11

D. CAPM 3.33%

Cost of debt:

Net finance cost 167.00

Less: Tax @35% 58.45

After tax cost of debt 108.55

Borrowings amount 165,723.00

After tax cost of debt (%) 0.07%

Debt

Ordinary

Shares Total

Cost of

Finance 0.07% 3.33%

Market

Weights 0.40 0.60

WACC 0.03% 2.00% 2.02%

WACC of company is 2.02%. It explains that if the company invest into equity and

debt in the ratio of 60:40 then the total cost of the company would be 2.02% and more than

2.02% could be earn by the company easily through investing in the Sonic Healthcare, BHP

Billiton and National Takaful. The return from all the three companies is as follows:

Sonic Healthcare

Cost of Equity: CAPM model

A. Risk free rate 2.75%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B. Market rate of return 8%

C. Beta 0.78

D. CAPM 6.85%

BHP Billiton

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of return 8%

C. Beta 0.56

D. CAPM 5.69%

National Takaful

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of return 8%

C. Beta -0.09

D. CAPM 2.28%

Hence, it concludes that current investment of 60:40 in equity and debt is better

option for the company. It must be done by the company to manage and improve the overall

performance in the market.

Paraphrase This Document

Task 3:

Nyota minerals limited are a British company which is a gold exploration and

development company. Company is listed in Australian stock exchange as well as London

stock exchange. Company is mainly based in Australian market and owns around 70% stock

in Ivrea project. The report focuses on the various expenses of the company as well as

budgetary evaluation in order to manage the current performance and forecast the future

position of the company. Restated financial reports of the company has been studied to

manipulation in the accounting policies and found that error in the company. Various cost

tools and budgetary reports have been studied ad prepared for Nyota minerals to improve the

overall performance of the company.

The process of cost accounting assist an organization to identify the cost associated

with the production level and operating activities of the organization in order to determine

that what the additional and irrelevant cost in the business is. This identification helps the

business to eliminate the same so that the profitability level of the business could be

improved and the common goal of the business could be met (Higgins, 2012). It helps the

company to maintain all the operating cost, factory cost and total production cost in an

efficient manner. Cost accounting’s main process includes recording, analyzing, evaluation

and allocation of various costs on the basis of a common base or the type of cost.

In case of Nyota minerals limited, cost accounting process has been applied to reach

over conclusion about performance of the company. Annual report (2014) of Nyota Minerals

explains that various expenses of the company have been restated in 2014 of 2013. These

amounts have been restated because of wrong allocation of cost and no proper use of

accounting policies. Below is the report of restated statement of the company:

(Annual report, 2014)

Annual report (2014) explains about huge changes into the expenses of the company

after restatement. It explains that after such changes, the overall performance of the company

has lead towards improvement. Along with that, company has been successful to maintain a

significant amount as profit. Overall total restated profit of the company is $ -25,344,879

which explains about decrement in the loss level of the company.

The financial statement of year 2014 explains that significant changes have been done

by the company in its annual report to improve the overall performance and position level.

Currently, the production cost and other operating expenses of the company have been

reduced at great level which directly has impacted over the profitability level. Hence, it has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

been found that it is important for the business to follow proper accounting policies so that

better outcome could be received (Kaplan and Atkinson, 2015).

The main aim of cost accounting process is to gather, evaluate, analyze and offer

proper information about various cost involved into the production process and elsewhere in

the organization to the managers of the organizations. This will help the managers to measure

the cost level and profitability position of the business so that a better conclusion could be

reached and better policies could be prepared for the betterment of the business in near future

(Garrison, Noreen, Brewer and McGowan, 2010). There is huge number of statistical

methods which could be applied by the managers in an organization to evaluate that how

much unnecessary cost is associated with the business and how could it be overcome to

improve the performance of the company.

The main aim of this overall performance is to meet the common goal of the

organization and offer better statistical data to the stakeholders of the company in a

presentable manner. Cost accounting makes it easier for the business to manage all the

operations in efficient manner (Gitman and Zutter, 2012). However, it is not mandatory for

the business to showcase the cost accounting data to the stakeholders of the business as these

are the internal reports which are prepared to make better decision for overall performance of

organization. The different cost involved in the business is studied to reduce it in order to

improve the profitability level and market performance of organization.

In case of Nyota Minerals limited, it has been studied that the overall performance of

the company has been improved at great extent in the year of 2014 against the previous year

financial performance. Study explains that these changes have occurred because of better

policies and scrutiny of unnecessary cost involved in the business. It concludes that these

changes and cost accounting tools have helped the business at great extent to improve the

overall level of the company.

More to it, it has been studied that costing design is called to a set of methods which

has been prepared and applied over the organization in order to manage the various cost level

and factors of the company which are used to make a decision about the cost system of the

company (Deegan, 2012). These cost design tools assist the business to evaluate all the

irrelevant cost in the business and offer a format to manage all the cost in a presentable

manner in order to make better decision about the performance level of the company. The

Paraphrase This Document

cost design and cost system approach assist the administration of business to gather, identify

and record all the cost expenses in better way in order to take decision in lesser time.

These reports are basically prepared for the internal stakeholders of the business so

that a blue print could be prepared about the future work in order to meet the common goal

and strategically position in the business. Cost design system is mainly divined into 2 parts;

one is internal cost design system and other one of external cost design system.

Internal data of Nyota minerals limited has been considered while preparing the

internal cost design system. The main aim behind applying this process into the organization

is to evaluate the profitability level, financial performance level and position of the company

at internal level. This process always makes t easier for the organization and its management

to evaluate the required changes so that better strategies could be prepared accordingly (Lord,

2007). On the basis of internal cost design tools, performance of the company has been

measured at internal level so that proper policies implementation could be done accordingly

in Nyota minerals limited. This system only takes consideration over the internal

performance and measure whether the company is able to meet all the internal performance

level. The internal cost design system makes it easier for Nyota minerals limited and its

management to make better decision, decision, strategy, plan, policy etc in order to improve

the overall performance level of the company. Along with that, this tool also assists the

business to make decision about the government and other stakeholders of the business.

Further, external factors and data of Nyota minerals limited has been considered while

preparing the external cost design system. The main aim behind applying this process into the

organization is to evaluate the profitability level, market position and overall market shares of

the company at external level. This process always makes it easier for the organization and its

management to evaluate the required changes so that better strategies could be prepared

accordingly (Deegan, 2012). On the basis of external cost design tools, performance of the

company has been measured at external level so that proper policies implementation could be

done accordingly in Nyota minerals limited. This system only takes consideration over the

external aspects and performance and measure whether the company is able to meet all the

external performance level. The internal cost design system makes it easier for Nyota

minerals limited and its management to make better decision, decision, strategy, plan, policy

etc in order to improve the overall performance level of the company. Along with that, this

tool also assists the business to make decision about the government and other stakeholders

of the business.

Through conducting the system over cost design and cost system over Nyota minerals

limited, it has been found that few changes must be done by the company in its internal

policies so that the level of irrelevant and additional cost could be reduced and ultimately, it

help the business to improve overall profitability position of the business. Annual report

(2014) explains that there is huge gap in the company to maintain the cost level. If proper

evaluation done over each of the associated cost of the business then it would directly

overcome the cost level of the business and along with that, the production process of the

business would be improved. Nyota is also recommended to forecast the future performance

through considering the current market position and historical data of the company in order to

measure how much units must be produced and in order to do so, how many labour hours and

raw material is used or so on. So that, the additional cost of the business could be controlled.

These changes must be done by the company in internal level and it will automatically

improve the external level of the business. It is the most important part of an organization to

measure the relevant and irrelevant cost and make better decision accordingly.

Nyota minerals limited must forecast the future performance through considering the

current market position and historical data of the company in order to make proper budgetary

reports. These budgetary reports assist the business to measure how much units must be

produced and in order to do so, how many labour hours and raw materials are used or so on.

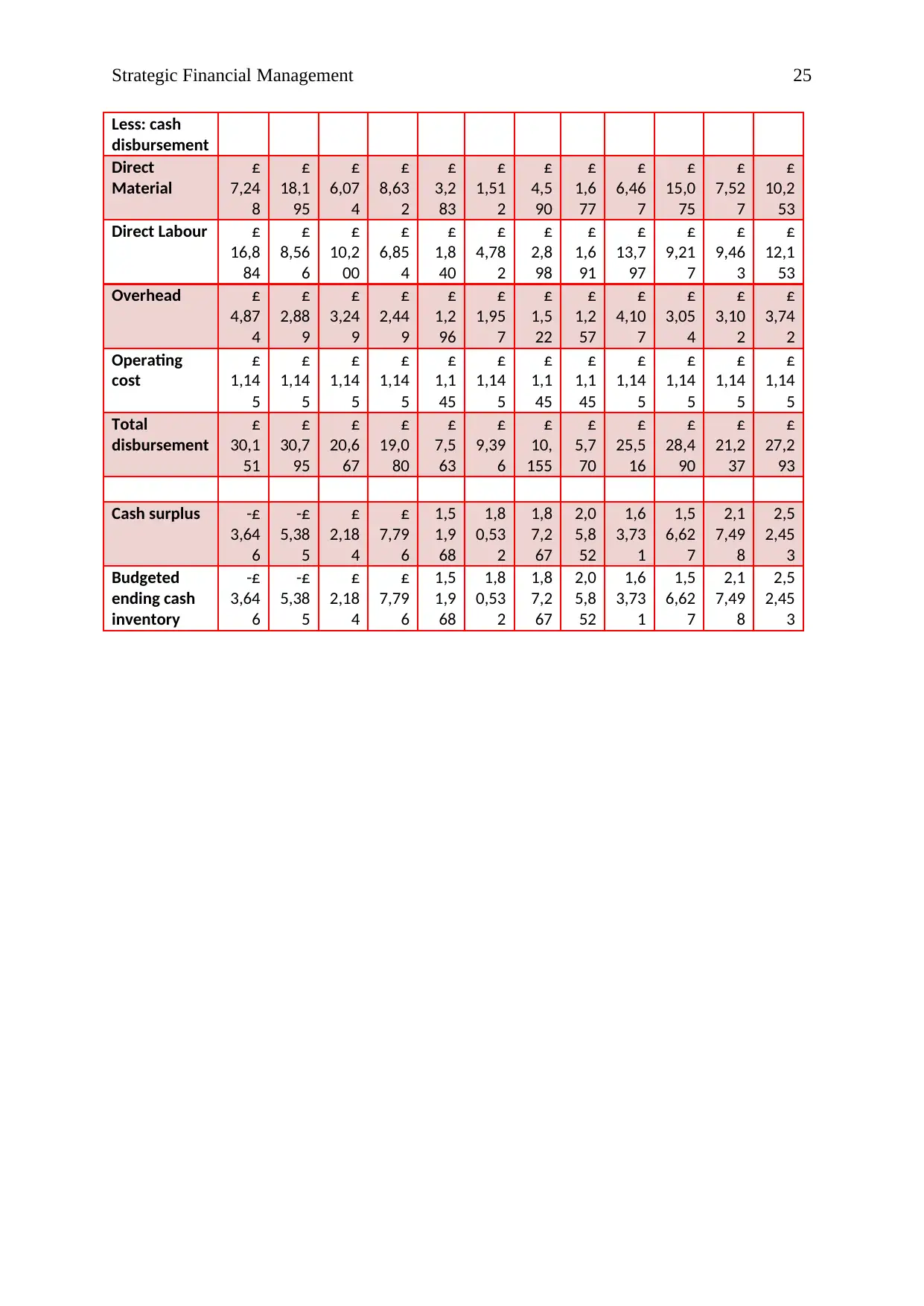

In current situation, below are the master budget reports of the company:

Monthly sales revenue budget

Sales Units Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Copper 1,50

0

1,20

0

1,30

0

1,00

0

400 500 400 200 1,30

0

1,20

0

1,20

0

1,50

0

Selling price

Copper $10

0.00

$10

0.00

$10

0.00

$10

0.00

$10

0.0

0

$10

0.00

$10

0.0

0

$10

0.0

0

$10

0.00

$10

0.00

$10

0.00

$10

0.00

Sales

Revenue

Copper $

1,50

,000

$

1,20

,000

$

1,30

,000

$

1,00

,000

$40

,00

0

$50,

000

$40

,00

0

$20

,00

0

$

1,30

,000

$

1,20

,000

$

1,20

,000

$

1,50

,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Sales

Revenue

$

1,50

,000

$

1,20

,000

$

1,30

,000

$

1,00

,000

400

00

500

00

400

00

200

00

$

1,30

,000

$

1,20

,000

$

1,20

,000

$

1,50

,000

Cash collection budget

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Total Sales

Revenue

$

1,50

,000

$

1,20

,000

$

1,30

,000

$

1,00

,000

400

00

500

00

400

00

200

00

$

1,30

,000

$

1,20

,000

$

1,20

,000

$

1,50

,000

Total cash

sales

500

00

455

4

478

2

378

2

185

0

213

8

163

8

108

8

478

2

455

4

455

4

542

0

Credit sales

(1st month

amount)

100

000

136

62

143

46

113

46

555

0

641

4

491

4

326

4

143

46

136

62

136

62

162

60

Credit sales

(2nd month

amount)

108

40

910

8

956

4

756

4

370

0

427

6

327

6

217

6

956

4

910

8

910

8

Total Cash

collection

150

000

290

56

282

36

246

92

149

64

122

52

108

28

762

8

213

04

277

80

273

24

307

88

Production budget in units

Budgeted

sales

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Copper 1,50

0

1,20

0

1,30

0

1,00

0

400 500 400 200 1,30

0

1,20

0

1,20

0

1,50

0

Add: desired

ending

inventory

Copper 750 600 650 500 200 250 200 100 650 600 600 750

Total needs

Copper 2,25

0

1,80

0

1,95

0

1,50

0

600 750 600 300 1,95

0

1,80

0

1,80

0

2,25

0

Less:

Beginning

Inventory

Copper 750 600 650 500 200 250 200 100 650 600 600

Paraphrase This Document

Required

production

Copper 3,00

0

1,65

0

2,00

0

1,35

0

300 800 550 200 2,50

0

1,75

0

1,80

0

2,40

0

Total

Required

production

3,00

0

1,65

0

2,00

0

1,35

0

300 800 550 200 2,50

0

1,75

0

1,80

0

2,40

0

Direct Material and cash purchase budget

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Budgeted

production

units

Copper 225 105 135 85 10 55 35 10 185 115 120 165

Material

units needed

for

production

Copper 225 105 135 85 10 55 35 10 185 115 120 165

Add: desired

inventory

level

Copper 113 53 68 43 5 28 18 5 93 58 60 83

Total

material

units

required

Copper 338 158 203 128 15 83 53 15 278 173 180 248

Less:

Beginning

inventory

Copper 0 113 53 68 43 5 28 18 5 93 58 60

Material

units to be

purchased

Copper 338 45 150 60 -28 78 25 -3 273 80 123 188

Raw material

1

Copper 632

8

844 281

3

112

5

-

516

145

3

469 -47 510

9

150

0

229

7

351

6

Raw material

2

Copper 455

6

608 202

5

810 -

371

104

6

338 -34 367

9

108

0

165

4

253

1

Total cost of

direct

material

241

5

427

8

102

64

482

2

-

310

576

3

185

4

126

5

180

7

524

0

214

7

283

5

Cash

Purchase

724

8

128

3

307

9

144

7

-93 172

9

556 379 558

2

205

0

274

4

385

1

0 169

12

299

4

718

5

337

6

-217 403

4

129

8

885 130

25

478

3

640

3

724

8

181

95

607

4

863

2

328

3

151

2

459

0

167

7

646

7

150

75

752

7

102

53

Direct Labour budget

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Budgeted

production

units

Copper 337

5

157

5

202

5

127

5

150 825 525 150 277

5

172

5

180

0

247

5

Total Direct

Labour hour

needed

Copper (1

hour)

337

5

157

5

202

5

127

5

150 825 525 150 277

5

172

5

180

0

247

5

Direct labour

cost per hour

Copper 945

00

441

00

567

00

357

00

420

0

231

00

147

00

420

0

777

00

483

00

504

00

693

00

Total Labour

cost

945

00

441

00

567

00

357

00

420

0

231

00

147

00

420

0

777

00

483

00

504

00

693

00

Manufacturing Overhead Budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Units to be

produced

Copper 337

5

157

5

202

5

127

5

150 825 525 150 277

5

172

5

180

0

247

5

Variable

Overhead

cost

Indirect

Material

120

60

611

8.5

728

5.5

489

6

131

4

341

5.5

207

0

120

7.5

985

5

658

3.5

675

9

868

0.5

Indirect

Labour

603

0

305

9.25

364

2.75

244

8

657 170

7.75

103

5

603

.75

492

7.5

329

1.75

337

9.5

434

0.25

Total

Variable

Overhead

cost

180

90

917

7.75

109

28.2

5

734

4

197

1

512

3.25

310

5

181

1.2

5

147

82.5

987

5.25

101

38.5

130

20.7

5

Fixed

Overhead

cost

Indirect

Material

148

50

756

0

879

0

585

0

174

0

405

0

249

0

159

0

119

40

819

0

834

0

106

80

Indirect

Labour

742

5

378

0

439

5

292

5

870 202

5

124

5

795 597

0

409

5

417

0

534

0

Utilities 550 550 550 550 550 550 550 550 550 550 550 550

Insurance 200 200 200 200 200 200 200 200 200 200 200 200

Repair

and

maintenance

s

625 625 625 625 625 625 625 625 625 625 625 625

Rent 700

0

700

0

700

0

700

0

700

0

700

0

700

0

700

0

700

0

700

0

700

0

700

0

Depreciation

750 750 750 750 750 750 750 750 750 750 750 750

Total fixed

Overhead

cost

314

00

204

65

223

10

179

00

117

35

152

00

128

60

115

10

270

35

214

10

216

35

251

45

Total

overhead

cost

494

90

296

42.7

5

332

38.2

5

252

44

137

06

203

23.2

5

159

65

133

21.

25

418

17.5

312

85.2

5

317

73.5

381

65.7

5

Less:

depreciation

750 750 750 750 750 750 750 750 750 750 750 750

Paraphrase This Document

Cash

payment for

overheads

487

40

288

92.7

5

324

88.2

5

244

94

129

56

195

73.2

5

152

15

125

71.

25

410

67.5

305

35.2

5

310

23.5

374

15.7

5

Monthly operating cost budget

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Expenses:

Utilities 50 50 50 50 50 50 50 50 50 50 50 50

Insurance 600

0

600

0

600

0

600

0

600

0

600

0

600

0

600

0

600

0

600

0

600

0

600

0

Administratio

n Staff Wages

250

0

250

0

250

0

250

0

250

0

250

0

250

0

250

0

250

0

250

0

250

0

250

0

General

Office

Expenses

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Rent 140

0

140

0

140

0

140

0

140

0

140

0

140

0

140

0

140

0

140

0

140

0

140

0

Total

monthly cost

budget

114

50

114

50

114

50

114

50

114

50

114

50

114

50

114

50

114

50

114

50

114

50

114

50

Inventory Budget for the finished goods

Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Copper 225

0

105

0

135

0

850 100 550 350 100 185

0

115

0

120

0

165

0

Desired

inventory

level for

finished

goods

Copper 112

5

525 675 425 50 275 175 50 925 575 600 825

Platinum 150 85 75 50 15 15 20 20 110 95 90 105

Total

inventory

247

5

126

0

146

5

975 290 675 415 265 199

0

136

5

139

0

178

0

Cost of sales budget

Sales Units Jan-

18

Feb-

18

Mar

-18

Apr-

18

Ma

y-

18

Jun-

18

Jul-

18

Aug

-18

Sep-

18

Oct-

18

Nov-

18

Dec-

18

Copper 150

0

120

0

130

0

100

0

400 500 400 200 130

0

120

0

120

0

150

0

Diamond 120

0

110

0

116

0

100

0

600 700 500 400 116

0

110

0

110

0

120

0

Iron ore 400 300 260 140 80 40 40 40 260 300 300 400

Platinum 200 180 160 120 60 40 40 40 160 180 180 200

Selling unit

Copper 100 100 100 100 100 100 100 100 100 100 100 100

Diamond 75 75 75 75 75 75 75 75 75 75 75 75

Iron ore 45 45 45 45 45 45 45 45 45 45 45 45

Platinum 65 65 65 65 65 65 65 65 65 65 65 65

Sales

Revenue

Copper $

1,50

,000

$

1,20

,000

$

1,30

,000

$

1,00

,000

$40

,00

0

$50,

000

$40

,00

0

$20

,00

0

$

1,30

,000

$

1,20

,000

$

1,20

,000

$

1,50

,000

Diamond $90,

000

$82,

500

$87,

000

$75,

000

$45

,00

0

$52,

500

$37

,50

0

$30

,00

0

$87,

000

$82,

500

$82,

500

$90,

000

Iron ore $18,

000

$13,

500

$11,

700

$6,3

00

$3,

600

$1,8

00

$1,

800

$1,

800

$11,

700

$13,

500

$13,

500

$18,

000

Platinum $13,

000

$11,

700

$10,

400

$7,8

00

$3,

900

$2,6

00

$2,

600

$2,

600

$10,

400

$11,

700

$11,

700

$13,

000

cost of sales $

4,70

,624

$

1,68

,778

$

2,48

,578

$

1,52

,712

$39

,69

8

$

1,36

,468

$74

,18

1

$53

,57

1

$

3,76

,560

$

2,02

,483

$

2,28

,567

$

2,98

,743

Monthly cash budget

Beginning

cash balance

£

4,82

5

-£

3,64

6

-£

5,38

5

£

2,18

4

£

7,7

96

1,5

1,96

8

1,8

0,5

32

1,8

7,2

67

2,0

5,85

2

1,6

3,73

1

1,5

6,62

7

2,1

7,49

8

ADD:

Budgeted

cash receipts

£

21,6

80

£

29,0

56

£

28,2

36

£

24,6

92

£

14,

964

£

12,2

52

£

10,

828

£

7,6

28

£

21,3

04

£

27,7

80

£

27,3

24

£

30,7

88

Total cash

available

2,6

5,05

0

2,5

4,10

2

2,2

8,51

2

2,6

8,76

0

2,2

7,5

95

2,7

4,48

8

2,8

8,8

12

2,6

3,5

47

4,1

8,89

2

4,4

1,53

1

4,2

9,86

7

5,2

5,37

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: cash

disbursement

Direct

Material

£

7,24

8

£

18,1

95

£

6,07

4

£

8,63

2

£

3,2

83

£

1,51

2

£

4,5

90

£

1,6

77

£

6,46

7

£

15,0

75

£

7,52

7

£

10,2

53

Direct Labour £

16,8

84

£

8,56

6

£

10,2

00

£

6,85

4

£

1,8

40

£

4,78

2

£

2,8

98

£

1,6

91

£

13,7

97

£

9,21

7

£

9,46

3

£

12,1

53

Overhead £

4,87

4

£

2,88

9

£

3,24

9

£

2,44

9

£

1,2

96

£

1,95

7

£

1,5

22

£

1,2

57

£

4,10

7

£

3,05

4

£

3,10

2

£

3,74

2

Operating

cost

£

1,14

5

£

1,14

5

£

1,14

5

£

1,14

5

£

1,1

45

£

1,14

5

£

1,1

45

£

1,1

45

£

1,14

5

£

1,14

5

£

1,14

5

£

1,14

5

Total

disbursement

£

30,1

51

£

30,7

95

£

20,6

67

£

19,0

80

£

7,5

63

£

9,39

6

£

10,

155

£

5,7

70

£

25,5

16

£

28,4

90

£

21,2

37

£

27,2

93

Cash surplus -£

3,64

6

-£

5,38

5

£

2,18

4

£

7,79

6

1,5

1,9

68

1,8

0,53

2

1,8

7,2

67

2,0

5,8

52

1,6

3,73

1

1,5

6,62

7

2,1

7,49

8

2,5

2,45

3

Budgeted

ending cash

inventory

-£

3,64

6

-£

5,38

5

£

2,18

4

£

7,79

6

1,5

1,9

68

1,8

0,53

2

1,8

7,2

67

2,0

5,8

52

1,6

3,73

1

1,5

6,62

7

2,1

7,49

8

2,5

2,45

3

Paraphrase This Document

References:

Annual report. 2014. Nyota Mierals limited. (online). Accessed on:

http://www.nyotaminerals.com/financials/ [available at 16/5/19].

Annual report. 2018. BHP Billiton limited. (online). Accessed on:

https://www.bhp.com/investor-centre/annual-reporting-2018 [available at 16/5/19].

Annual report. 2018. Boral limited. (online). Accessed on:

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf [available at 16/5/19].

Annual report. 2018. National takaful co. (online). Accessed on: https://takaful.ae/en/about-

us/financials-investors-relations/ [available at 16/5/19].

Annual report. 2018. Sonic Healthcare lmited. (online). Accessed on:

https://investors.sonichealthcare.com/Investors/?page=annual-reports [available at 16/5/19].

Annual report. 2018. Woolworths limited. (online). Accessed on:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [available

at 16/5/19].

Deegan, C. 2012. Australian financial accounting. McGraw-Hill Education Australia.

Deegan, C. 2013. Financial accounting theory. McGraw-Hill Education Australia.

DRURY, C. M. 2013. Management and cost accounting. Springer.

Edwards, J. R. 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, 25(4), pp.792-793.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Horngren, C. T. 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Schwartz, M.S., 2017. Corporate social responsibility. Routledge.

Ward, K., 2012. Strategic management accounting. Routledge.

Weil, R. L., Schipper, K., and Francis, J. 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Zimmerman, J. L., and Yahya-Zadeh, M. 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix:

Refer to attached spreadsheet

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.