Strategic Information for Business and Enterprise

VerifiedAdded on 2022/12/23

|13

|2769

|37

AI Summary

This report discusses the strategic information for business and enterprise, focusing on the centralized accounting system of Bell Studio. It includes data flow diagrams and system flowcharts, as well as internal control weaknesses and associated risks. The report also addresses the purchasing system, cash disbursements system, and payroll system of the organization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Strategic Information for Business and Enterprise

Name of Student-

Name of University-

Author’s Note

Strategic Information for Business and Enterprise

Name of Student-

Name of University-

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Executive Summary

Bell Studio is the wholesaler of the art supplies and follows the centralized accounting

information system to execute all the business operations in the organization. The

enterprise of Bell Studio includes different transaction cycles, different financial

reporting for the business operations, the management reporting of the system and the

e-commerce that is involved in the system. This particular report includes the operating

system of the Bell studio stating its working of the computer based systems. This report

also contains the opportunities that can be involved to overcome the computer fraud as

well as the security measures in the form of electronic commerce. The evaluation in this

report is done in the form of data flow diagram and system flowcharts of the related

system of Bell Studio.

Executive Summary

Bell Studio is the wholesaler of the art supplies and follows the centralized accounting

information system to execute all the business operations in the organization. The

enterprise of Bell Studio includes different transaction cycles, different financial

reporting for the business operations, the management reporting of the system and the

e-commerce that is involved in the system. This particular report includes the operating

system of the Bell studio stating its working of the computer based systems. This report

also contains the opportunities that can be involved to overcome the computer fraud as

well as the security measures in the form of electronic commerce. The evaluation in this

report is done in the form of data flow diagram and system flowcharts of the related

system of Bell Studio.

2STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Table of Contents

1. Introduction....................................................................................................................3

2. Data Flow Diagram for the Purchasing system and system of Cash Disbursements...4

3. Data Flow Diagram of Payroll System...........................................................................5

4. System Flowchart of Purchases System.......................................................................6

5. System Flowchart of Cash Disbursements System......................................................6

6. System Flowchart of Payroll System.............................................................................8

7. Internal Control Weakness and Risk Associated..........................................................8

8. Conclusion.....................................................................................................................9

Reference........................................................................................................................11

Table of Contents

1. Introduction....................................................................................................................3

2. Data Flow Diagram for the Purchasing system and system of Cash Disbursements...4

3. Data Flow Diagram of Payroll System...........................................................................5

4. System Flowchart of Purchases System.......................................................................6

5. System Flowchart of Cash Disbursements System......................................................6

6. System Flowchart of Payroll System.............................................................................8

7. Internal Control Weakness and Risk Associated..........................................................8

8. Conclusion.....................................................................................................................9

Reference........................................................................................................................11

3STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

1. Introduction

Centralization is referred as a process that includes the activities involving the

planning as well as decision making of the system of Bell Studio (Kanodia and Sapra

2016). Centralization involves decision making and planning is done by the particular

leaders of the organization. The executives of an organization and the specialists of an

organization takes most critical decisions that are actually based on the head office.

The case study of Bell Studio includes centralized accounting system for

business operations (Haislip et al. 2015). Using the centralized system, the organization

has many advantages. The benefits that Bell Studio gets from their centralized payroll

system are having a clear chain of all the commands in the organization, fulfils the

vision of the company very easily, have low cost maintaining costs, and as the decisions

are mainly taken by the supervisors and the clerks, the enterprise is able to take quick

decisions relation to the process of the organisation.

But the centralized system in the Bell Studio also has many disadvantages that

are needed to be taken care off (Sun 2016). This report explains the business operation

of the system from the perspective of the business analyst and those business

operations area shown in the form of data flow diagram and system flowchart in this

report. This report also states the internal weakens of controlling the transaction cycles,

the management cycles and the financial cycle of the business operations and

addresses the risks that are associated with the internal weakness in controlling the

system. Some security measures are also explained in this report related to the risks

addressed (Zimmermann, Rentrop and Felden 2016).

1. Introduction

Centralization is referred as a process that includes the activities involving the

planning as well as decision making of the system of Bell Studio (Kanodia and Sapra

2016). Centralization involves decision making and planning is done by the particular

leaders of the organization. The executives of an organization and the specialists of an

organization takes most critical decisions that are actually based on the head office.

The case study of Bell Studio includes centralized accounting system for

business operations (Haislip et al. 2015). Using the centralized system, the organization

has many advantages. The benefits that Bell Studio gets from their centralized payroll

system are having a clear chain of all the commands in the organization, fulfils the

vision of the company very easily, have low cost maintaining costs, and as the decisions

are mainly taken by the supervisors and the clerks, the enterprise is able to take quick

decisions relation to the process of the organisation.

But the centralized system in the Bell Studio also has many disadvantages that

are needed to be taken care off (Sun 2016). This report explains the business operation

of the system from the perspective of the business analyst and those business

operations area shown in the form of data flow diagram and system flowchart in this

report. This report also states the internal weakens of controlling the transaction cycles,

the management cycles and the financial cycle of the business operations and

addresses the risks that are associated with the internal weakness in controlling the

system. Some security measures are also explained in this report related to the risks

addressed (Zimmermann, Rentrop and Felden 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

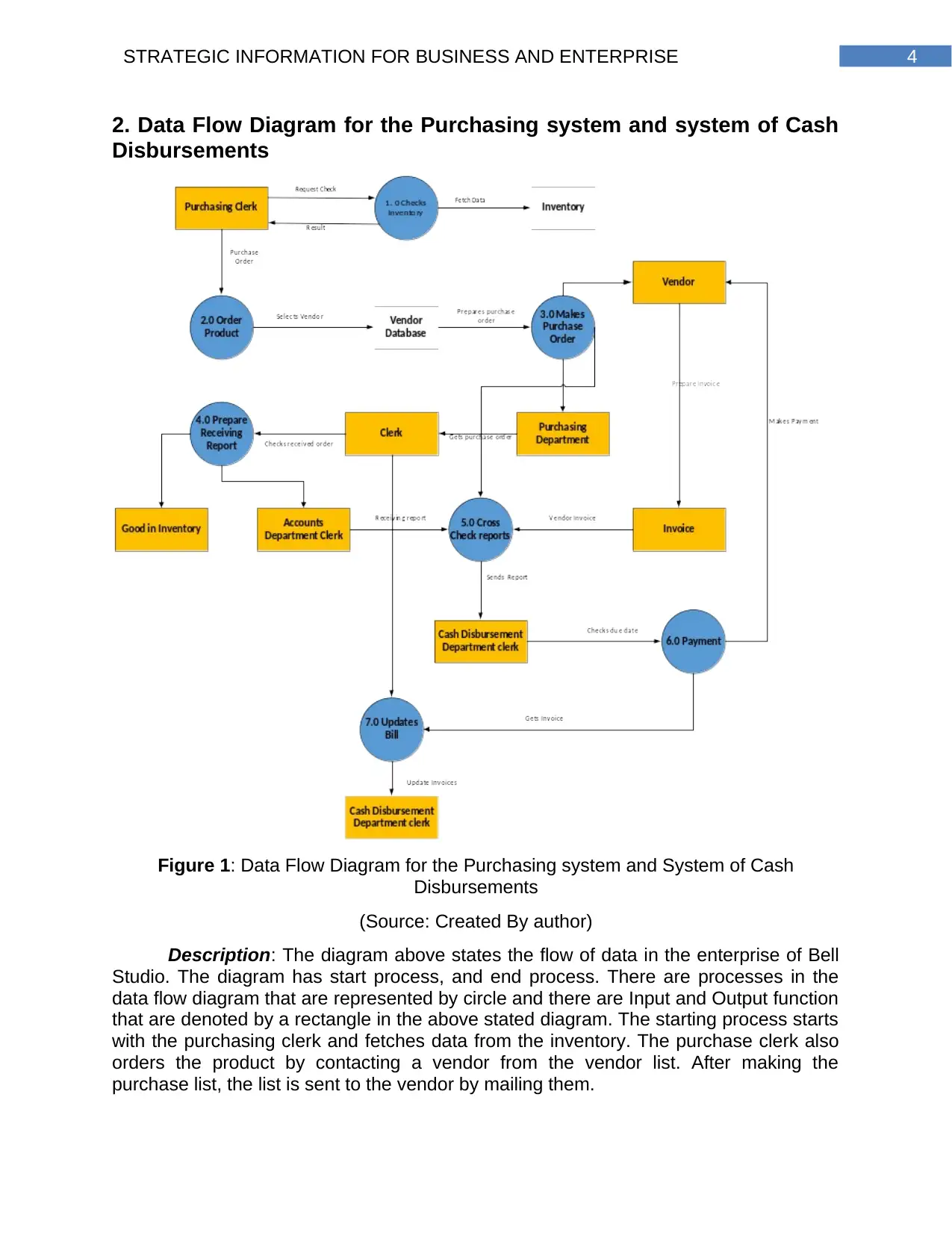

2. Data Flow Diagram for the Purchasing system and system of Cash

Disbursements

Figure 1: Data Flow Diagram for the Purchasing system and System of Cash

Disbursements

(Source: Created By author)

Description: The diagram above states the flow of data in the enterprise of Bell

Studio. The diagram has start process, and end process. There are processes in the

data flow diagram that are represented by circle and there are Input and Output function

that are denoted by a rectangle in the above stated diagram. The starting process starts

with the purchasing clerk and fetches data from the inventory. The purchase clerk also

orders the product by contacting a vendor from the vendor list. After making the

purchase list, the list is sent to the vendor by mailing them.

2. Data Flow Diagram for the Purchasing system and system of Cash

Disbursements

Figure 1: Data Flow Diagram for the Purchasing system and System of Cash

Disbursements

(Source: Created By author)

Description: The diagram above states the flow of data in the enterprise of Bell

Studio. The diagram has start process, and end process. There are processes in the

data flow diagram that are represented by circle and there are Input and Output function

that are denoted by a rectangle in the above stated diagram. The starting process starts

with the purchasing clerk and fetches data from the inventory. The purchase clerk also

orders the product by contacting a vendor from the vendor list. After making the

purchase list, the list is sent to the vendor by mailing them.

5STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

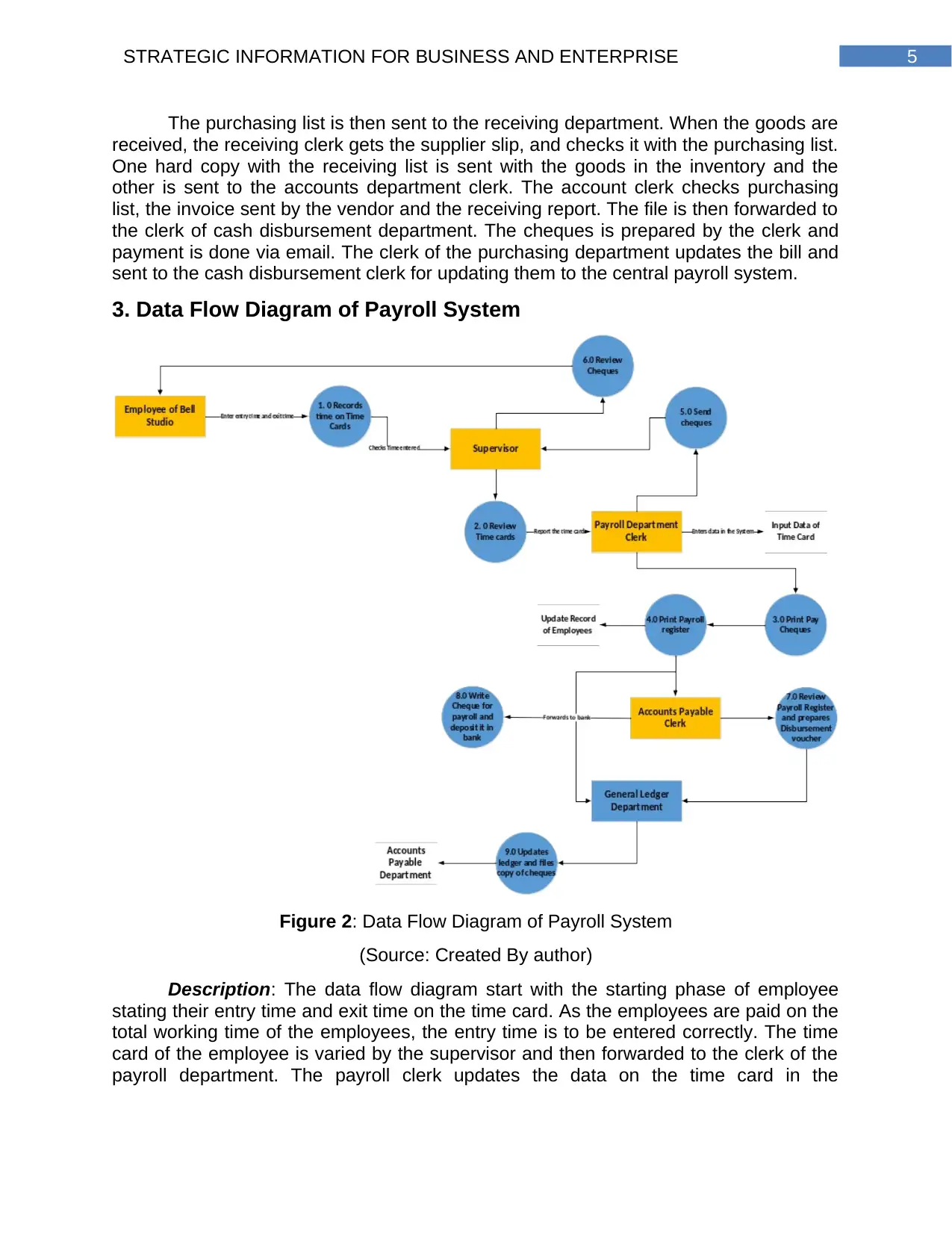

The purchasing list is then sent to the receiving department. When the goods are

received, the receiving clerk gets the supplier slip, and checks it with the purchasing list.

One hard copy with the receiving list is sent with the goods in the inventory and the

other is sent to the accounts department clerk. The account clerk checks purchasing

list, the invoice sent by the vendor and the receiving report. The file is then forwarded to

the clerk of cash disbursement department. The cheques is prepared by the clerk and

payment is done via email. The clerk of the purchasing department updates the bill and

sent to the cash disbursement clerk for updating them to the central payroll system.

3. Data Flow Diagram of Payroll System

Figure 2: Data Flow Diagram of Payroll System

(Source: Created By author)

Description: The data flow diagram start with the starting phase of employee

stating their entry time and exit time on the time card. As the employees are paid on the

total working time of the employees, the entry time is to be entered correctly. The time

card of the employee is varied by the supervisor and then forwarded to the clerk of the

payroll department. The payroll clerk updates the data on the time card in the

The purchasing list is then sent to the receiving department. When the goods are

received, the receiving clerk gets the supplier slip, and checks it with the purchasing list.

One hard copy with the receiving list is sent with the goods in the inventory and the

other is sent to the accounts department clerk. The account clerk checks purchasing

list, the invoice sent by the vendor and the receiving report. The file is then forwarded to

the clerk of cash disbursement department. The cheques is prepared by the clerk and

payment is done via email. The clerk of the purchasing department updates the bill and

sent to the cash disbursement clerk for updating them to the central payroll system.

3. Data Flow Diagram of Payroll System

Figure 2: Data Flow Diagram of Payroll System

(Source: Created By author)

Description: The data flow diagram start with the starting phase of employee

stating their entry time and exit time on the time card. As the employees are paid on the

total working time of the employees, the entry time is to be entered correctly. The time

card of the employee is varied by the supervisor and then forwarded to the clerk of the

payroll department. The payroll clerk updates the data on the time card in the

6STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

employee’s record in the database. The clerk prints the cheques that are to be paid and

update the payroll registers.

The file is then given to the account payable clerk. The clerk then first reviews

the register and prepares the disbursement voucher. The clerk there writes the cheque

for the entire payroll amount and deposit it to the bank. The payroll register is updated

by the ledger department and finally the files are stored in the account payable

department.

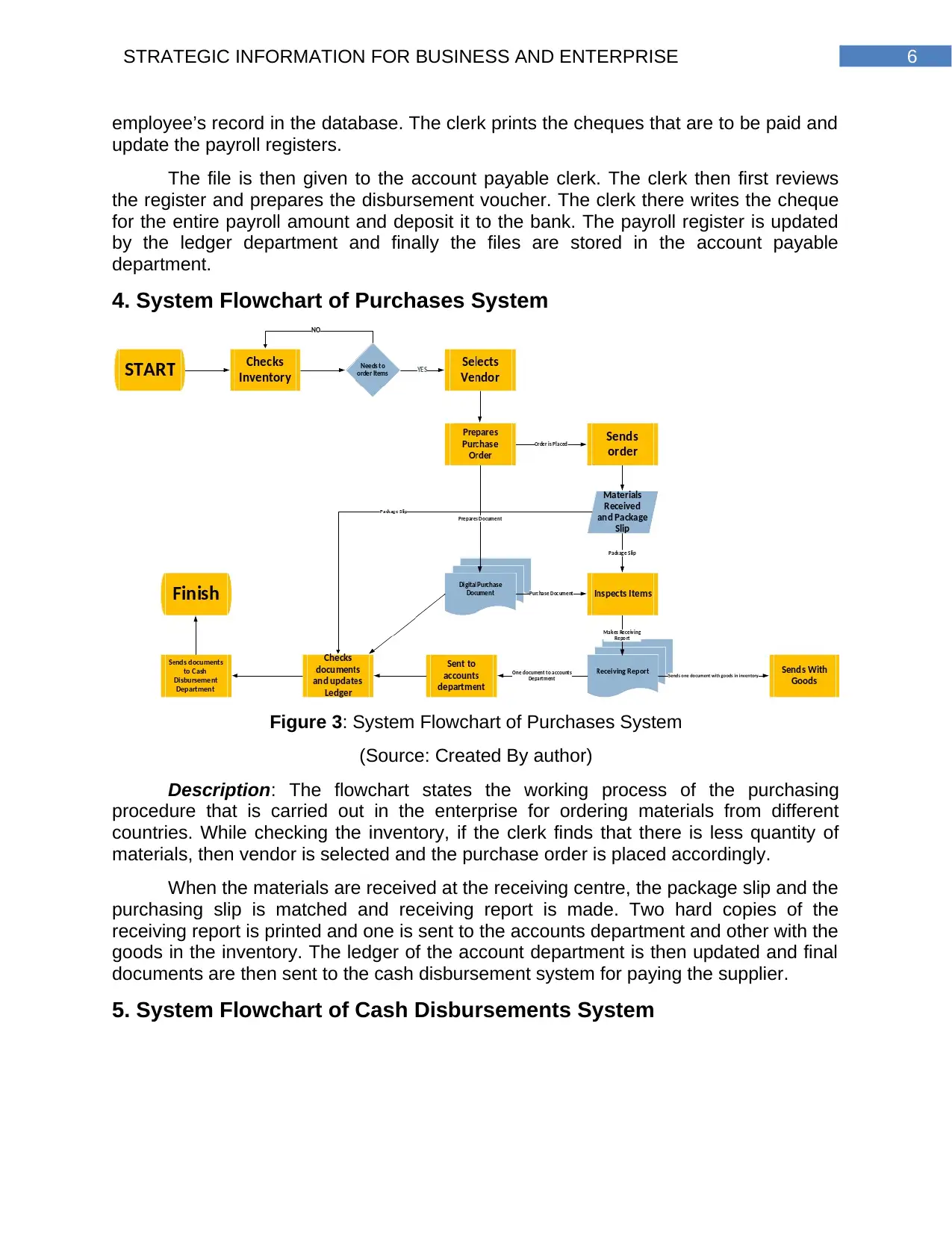

4. System Flowchart of Purchases System

Figure 3: System Flowchart of Purchases System

(Source: Created By author)

Description: The flowchart states the working process of the purchasing

procedure that is carried out in the enterprise for ordering materials from different

countries. While checking the inventory, if the clerk finds that there is less quantity of

materials, then vendor is selected and the purchase order is placed accordingly.

When the materials are received at the receiving centre, the package slip and the

purchasing slip is matched and receiving report is made. Two hard copies of the

receiving report is printed and one is sent to the accounts department and other with the

goods in the inventory. The ledger of the account department is then updated and final

documents are then sent to the cash disbursement system for paying the supplier.

5. System Flowchart of Cash Disbursements System

employee’s record in the database. The clerk prints the cheques that are to be paid and

update the payroll registers.

The file is then given to the account payable clerk. The clerk then first reviews

the register and prepares the disbursement voucher. The clerk there writes the cheque

for the entire payroll amount and deposit it to the bank. The payroll register is updated

by the ledger department and finally the files are stored in the account payable

department.

4. System Flowchart of Purchases System

Figure 3: System Flowchart of Purchases System

(Source: Created By author)

Description: The flowchart states the working process of the purchasing

procedure that is carried out in the enterprise for ordering materials from different

countries. While checking the inventory, if the clerk finds that there is less quantity of

materials, then vendor is selected and the purchase order is placed accordingly.

When the materials are received at the receiving centre, the package slip and the

purchasing slip is matched and receiving report is made. Two hard copies of the

receiving report is printed and one is sent to the accounts department and other with the

goods in the inventory. The ledger of the account department is then updated and final

documents are then sent to the cash disbursement system for paying the supplier.

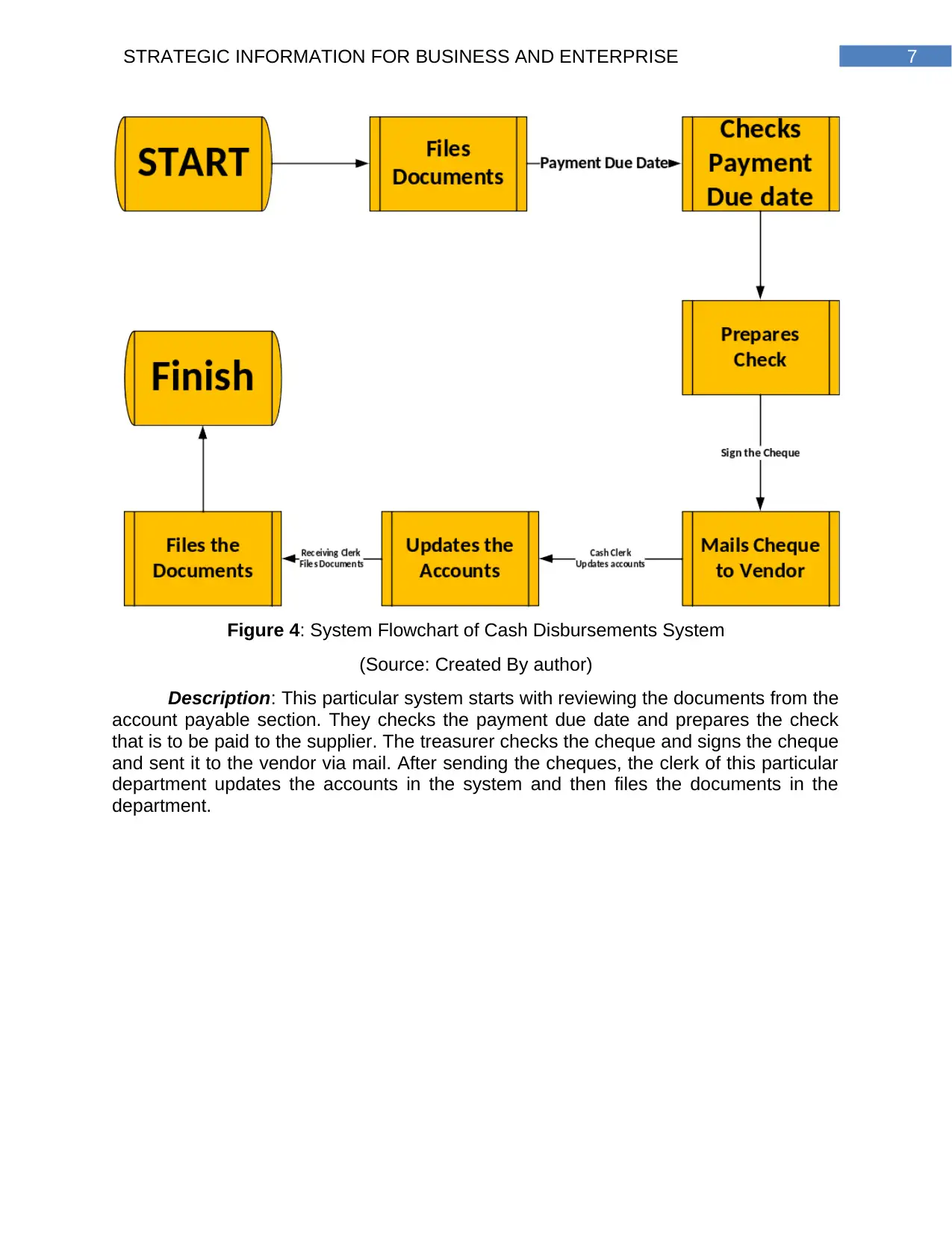

5. System Flowchart of Cash Disbursements System

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Figure 4: System Flowchart of Cash Disbursements System

(Source: Created By author)

Description: This particular system starts with reviewing the documents from the

account payable section. They checks the payment due date and prepares the check

that is to be paid to the supplier. The treasurer checks the cheque and signs the cheque

and sent it to the vendor via mail. After sending the cheques, the clerk of this particular

department updates the accounts in the system and then files the documents in the

department.

Figure 4: System Flowchart of Cash Disbursements System

(Source: Created By author)

Description: This particular system starts with reviewing the documents from the

account payable section. They checks the payment due date and prepares the check

that is to be paid to the supplier. The treasurer checks the cheque and signs the cheque

and sent it to the vendor via mail. After sending the cheques, the clerk of this particular

department updates the accounts in the system and then files the documents in the

department.

8STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

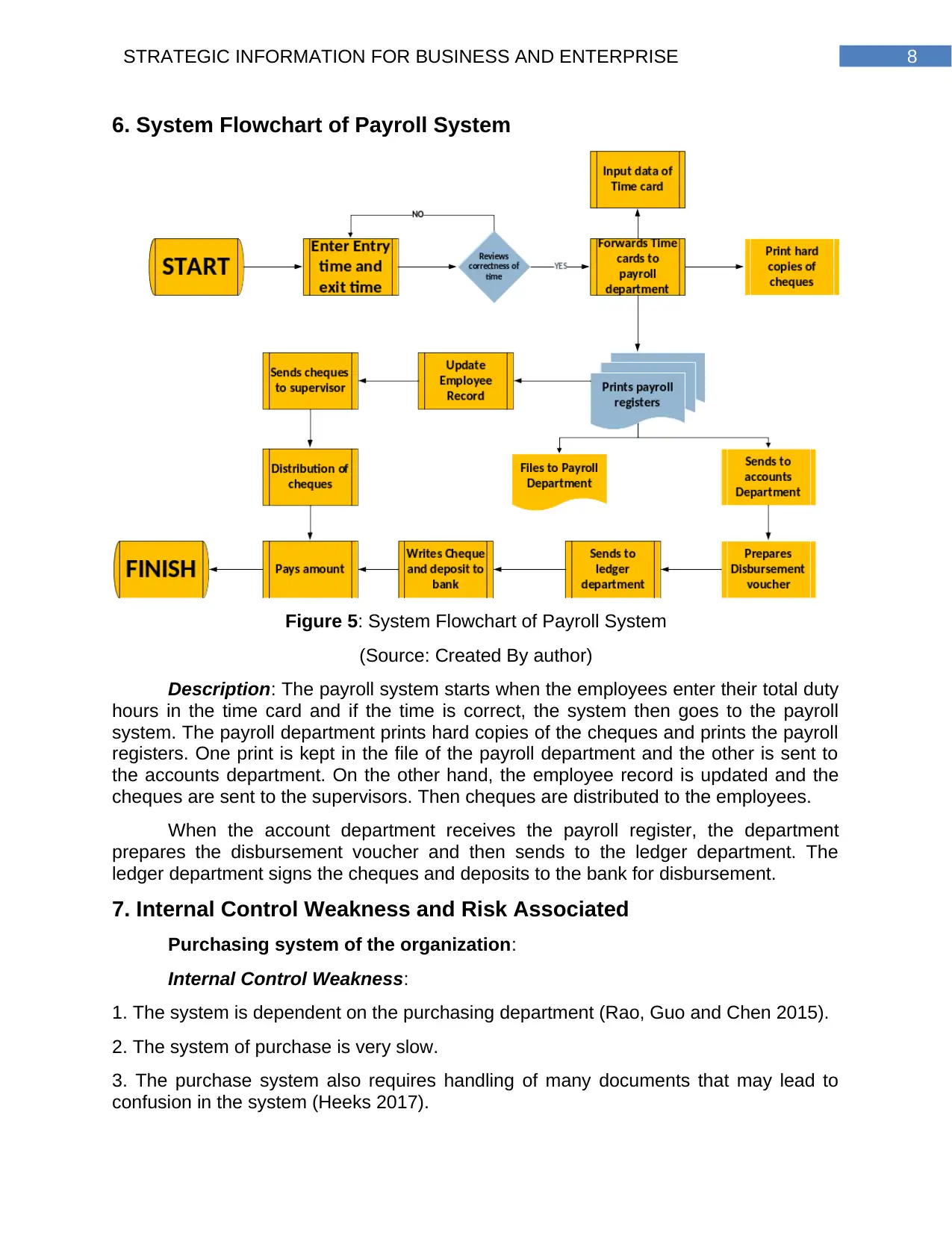

6. System Flowchart of Payroll System

Figure 5: System Flowchart of Payroll System

(Source: Created By author)

Description: The payroll system starts when the employees enter their total duty

hours in the time card and if the time is correct, the system then goes to the payroll

system. The payroll department prints hard copies of the cheques and prints the payroll

registers. One print is kept in the file of the payroll department and the other is sent to

the accounts department. On the other hand, the employee record is updated and the

cheques are sent to the supervisors. Then cheques are distributed to the employees.

When the account department receives the payroll register, the department

prepares the disbursement voucher and then sends to the ledger department. The

ledger department signs the cheques and deposits to the bank for disbursement.

7. Internal Control Weakness and Risk Associated

Purchasing system of the organization:

Internal Control Weakness:

1. The system is dependent on the purchasing department (Rao, Guo and Chen 2015).

2. The system of purchase is very slow.

3. The purchase system also requires handling of many documents that may lead to

confusion in the system (Heeks 2017).

6. System Flowchart of Payroll System

Figure 5: System Flowchart of Payroll System

(Source: Created By author)

Description: The payroll system starts when the employees enter their total duty

hours in the time card and if the time is correct, the system then goes to the payroll

system. The payroll department prints hard copies of the cheques and prints the payroll

registers. One print is kept in the file of the payroll department and the other is sent to

the accounts department. On the other hand, the employee record is updated and the

cheques are sent to the supervisors. Then cheques are distributed to the employees.

When the account department receives the payroll register, the department

prepares the disbursement voucher and then sends to the ledger department. The

ledger department signs the cheques and deposits to the bank for disbursement.

7. Internal Control Weakness and Risk Associated

Purchasing system of the organization:

Internal Control Weakness:

1. The system is dependent on the purchasing department (Rao, Guo and Chen 2015).

2. The system of purchase is very slow.

3. The purchase system also requires handling of many documents that may lead to

confusion in the system (Heeks 2017).

9STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Risks Associated with the system:

1.1 Risk of making the system slow down as the process involved in the system needs

more manual labour (Thompson 2017).

2.1 Risk of conducting human error as the system mainly depends on the process done

by the clerk (Duncan and Whittington 2016).

3.1 The information or the data are uploaded on the central payroll section that might

crash anytime making the system stop for some time.

Cash Disbursement system of the organization:

Internal Control Weakness:

1. While writing the cheques, mistake may occur and mistake can also occur while

cheques are transferred from department to another (Safari et al. 2016).

2. Security breach might take place with the centralized system as the system is not

secured (Ji, Lu and Qu 2017). There might be internal password theft or hardware or

software failure.

3. There is also a risk of denial of service in the enterprise business operations.

Risks Associated with the system:

1.1 Spam, scams as well as phishing might take place as the system (Gallemore and

Labro 2015).

2.1 Security breach might take place with the centralized system as the system is not

secured. There might be internal password theft or hardware or software failure (Chen

et al. 2016).

3.1 There is also a risk of denial of service in the enterprise business operations

(Avgerou and Walsham 2017).

Payroll system of the organization:

Internal Control Weakness:

1. The employee may not be fair to enter their working hours in the system as the

system is carried out manually (Aladwan 2018).

2. Human mistakes are very common with the system as because the system deals with

human errors of dealing with the business operations.

Risks Associated with the system:

1.1 Making the system slow and have infected virus and malware in the system (Khan

and Gray 2016).

2.1 Fraud caused by the humans and the password theft is caused by the system is risk

to Bell Studio.

3.1 Risk of staff dishonesty is involved in the system (Salterio 2015).

Risks Associated with the system:

1.1 Risk of making the system slow down as the process involved in the system needs

more manual labour (Thompson 2017).

2.1 Risk of conducting human error as the system mainly depends on the process done

by the clerk (Duncan and Whittington 2016).

3.1 The information or the data are uploaded on the central payroll section that might

crash anytime making the system stop for some time.

Cash Disbursement system of the organization:

Internal Control Weakness:

1. While writing the cheques, mistake may occur and mistake can also occur while

cheques are transferred from department to another (Safari et al. 2016).

2. Security breach might take place with the centralized system as the system is not

secured (Ji, Lu and Qu 2017). There might be internal password theft or hardware or

software failure.

3. There is also a risk of denial of service in the enterprise business operations.

Risks Associated with the system:

1.1 Spam, scams as well as phishing might take place as the system (Gallemore and

Labro 2015).

2.1 Security breach might take place with the centralized system as the system is not

secured. There might be internal password theft or hardware or software failure (Chen

et al. 2016).

3.1 There is also a risk of denial of service in the enterprise business operations

(Avgerou and Walsham 2017).

Payroll system of the organization:

Internal Control Weakness:

1. The employee may not be fair to enter their working hours in the system as the

system is carried out manually (Aladwan 2018).

2. Human mistakes are very common with the system as because the system deals with

human errors of dealing with the business operations.

Risks Associated with the system:

1.1 Making the system slow and have infected virus and malware in the system (Khan

and Gray 2016).

2.1 Fraud caused by the humans and the password theft is caused by the system is risk

to Bell Studio.

3.1 Risk of staff dishonesty is involved in the system (Salterio 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

8. Conclusion

The information system of the Bell Studio includes manual working procedure

and documenting working procedure. All the procedures are done mainly by the clerks

of each department. Bell Studio has transaction process, management process and the

report g process and three sub systems were chosen from the operation of the business

that included in the Bell Studio.

The system that this report mentions is the purchasing system that contains

about material ordering of Bell Studio. The other systems that are included are payroll

process of paying their employee and the cash disbursement system of paying their

supplier with the required amount for their supplies. This project details the business

operations of the system that includes the DFD (Data Flow Diagrams) of the systems

and the flowchart of the systems. As stated from the perspective of business analyst, it

is the duty to make all the procedure advanced and up to date. So, this report also

states the internal flaws that business operations of the system incurs and the risks that

are included in the system. The report above shows the internal control weakness of the

three system and their risks associated with the system.

8. Conclusion

The information system of the Bell Studio includes manual working procedure

and documenting working procedure. All the procedures are done mainly by the clerks

of each department. Bell Studio has transaction process, management process and the

report g process and three sub systems were chosen from the operation of the business

that included in the Bell Studio.

The system that this report mentions is the purchasing system that contains

about material ordering of Bell Studio. The other systems that are included are payroll

process of paying their employee and the cash disbursement system of paying their

supplier with the required amount for their supplies. This project details the business

operations of the system that includes the DFD (Data Flow Diagrams) of the systems

and the flowchart of the systems. As stated from the perspective of business analyst, it

is the duty to make all the procedure advanced and up to date. So, this report also

states the internal flaws that business operations of the system incurs and the risks that

are included in the system. The report above shows the internal control weakness of the

three system and their risks associated with the system.

11STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Reference

Aladwan, M., 2018. Undertaking of environmental accounting responsibility to achieve

sustainable development: evidence from Jordanian chemical and mining

companies. International Journal of Managerial and Financial Accounting, 10(1), pp.48-

64.

Avgerou, C. and Walsham, G. eds., 2017. Information technology in context: Studies

from the perspective of developing countries: Studies from the perspective of

developing countries. Routledge.

Chen, Y., Knechel, W.R., Marisetty, V.B., Truong, C. and Veeraraghavan, M., 2016.

Board independence and internal control weakness: Evidence from SOX 404

disclosures. Auditing: A Journal of Practice & Theory, 36(2), pp.45-62.

Duncan, R.A.K. and Whittington, M., 2016. Enhancing cloud security and privacy: the

power and the weakness of the audit trail. CLOUD COMPUTING 2016.

Gallemore, J. and Labro, E., 2015. The importance of the internal information

environment for tax avoidance. Journal of Accounting and Economics, 60(1), pp.149-

167.

Haislip, J.Z., Masli, A., Richardson, V.J. and Sanchez, J.M., 2015. Repairing

organizational legitimacy following information technology (IT) material weaknesses:

Executive turnover, IT expertise, and IT system upgrades. Journal of Information

Systems, 30(1), pp.41-70.

Heeks, R., 2017. Information technology, information systems and public sector

accountability. In Information Technology in Context: Studies from the Perspective of

Developing Countries (pp. 201-219). Routledge.

Ji, X.D., Lu, W. and Qu, W., 2017. Voluntary disclosure of internal control weakness and

earnings quality: Evidence from China. The International Journal of Accounting, 52(1),

pp.27-44.

Kanodia, C. and Sapra, H., 2016. A real effects perspective to accounting measurement

and disclosure: Implications and insights for future research. Journal of Accounting

Research, 54(2), pp.623-676.

Khan, T. and Gray, R., 2016. Accounting, identity, autopoiesis+ sustainability: A

comment, development and expansion on Lawrence, Botes, Collins and Roper

(2013). Meditari Accountancy Research, 24(1), pp.36-55.

Rao, Y., Guo, K.H. and Chen, Y., 2015. Information systems maturity, knowledge

sharing, and firm performance. International Journal of Accounting & Information

Management, 23(2), pp.106-127.

Safari, H., Faraji, Z. and Majidian, S., 2016. Identifying and evaluating enterprise

architecture risks using FMEA and fuzzy VIKOR. Journal of Intelligent

Manufacturing, 27(2), pp.475-486.7

Reference

Aladwan, M., 2018. Undertaking of environmental accounting responsibility to achieve

sustainable development: evidence from Jordanian chemical and mining

companies. International Journal of Managerial and Financial Accounting, 10(1), pp.48-

64.

Avgerou, C. and Walsham, G. eds., 2017. Information technology in context: Studies

from the perspective of developing countries: Studies from the perspective of

developing countries. Routledge.

Chen, Y., Knechel, W.R., Marisetty, V.B., Truong, C. and Veeraraghavan, M., 2016.

Board independence and internal control weakness: Evidence from SOX 404

disclosures. Auditing: A Journal of Practice & Theory, 36(2), pp.45-62.

Duncan, R.A.K. and Whittington, M., 2016. Enhancing cloud security and privacy: the

power and the weakness of the audit trail. CLOUD COMPUTING 2016.

Gallemore, J. and Labro, E., 2015. The importance of the internal information

environment for tax avoidance. Journal of Accounting and Economics, 60(1), pp.149-

167.

Haislip, J.Z., Masli, A., Richardson, V.J. and Sanchez, J.M., 2015. Repairing

organizational legitimacy following information technology (IT) material weaknesses:

Executive turnover, IT expertise, and IT system upgrades. Journal of Information

Systems, 30(1), pp.41-70.

Heeks, R., 2017. Information technology, information systems and public sector

accountability. In Information Technology in Context: Studies from the Perspective of

Developing Countries (pp. 201-219). Routledge.

Ji, X.D., Lu, W. and Qu, W., 2017. Voluntary disclosure of internal control weakness and

earnings quality: Evidence from China. The International Journal of Accounting, 52(1),

pp.27-44.

Kanodia, C. and Sapra, H., 2016. A real effects perspective to accounting measurement

and disclosure: Implications and insights for future research. Journal of Accounting

Research, 54(2), pp.623-676.

Khan, T. and Gray, R., 2016. Accounting, identity, autopoiesis+ sustainability: A

comment, development and expansion on Lawrence, Botes, Collins and Roper

(2013). Meditari Accountancy Research, 24(1), pp.36-55.

Rao, Y., Guo, K.H. and Chen, Y., 2015. Information systems maturity, knowledge

sharing, and firm performance. International Journal of Accounting & Information

Management, 23(2), pp.106-127.

Safari, H., Faraji, Z. and Majidian, S., 2016. Identifying and evaluating enterprise

architecture risks using FMEA and fuzzy VIKOR. Journal of Intelligent

Manufacturing, 27(2), pp.475-486.7

12STRATEGIC INFORMATION FOR BUSINESS AND ENTERPRISE

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting

research. Journal of Management Accounting Research, 27(1), pp.151-170.

Sun, Y., 2016. Internal control weakness disclosure and firm investment. Journal of

Accounting, Auditing & Finance, 31(2), pp.277-307.

Thompson, J.D., 2017. Organizations in action: Social science bases of administrative

theory. Routledge.

Zimmermann, S., Rentrop, C. and Felden, C., 2016. A multiple case study on the nature

and management of shadow information technology. Journal of Information

Systems, 31(1), pp.79-101.

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting

research. Journal of Management Accounting Research, 27(1), pp.151-170.

Sun, Y., 2016. Internal control weakness disclosure and firm investment. Journal of

Accounting, Auditing & Finance, 31(2), pp.277-307.

Thompson, J.D., 2017. Organizations in action: Social science bases of administrative

theory. Routledge.

Zimmermann, S., Rentrop, C. and Felden, C., 2016. A multiple case study on the nature

and management of shadow information technology. Journal of Information

Systems, 31(1), pp.79-101.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.