Strategic Information System for Business and Enterprise

VerifiedAdded on 2022/12/23

|18

|3963

|99

AI Summary

This report examines the Bell Studio business which is one of the Adelaide based distributors of the workmanship suppliers. It discusses the utilization cycle processes including payroll system and purchases system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Name of the student

Name of the university

Author notes

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Name of the student

Name of the university

Author notes

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Executive Summary:

This report examines the Bell Studio business which is one of the Adelaide based

distributers of the workmanship suppliers. Considering the manner in which that the

association has a united accounting structure with various frameworks organization

terminals in different territory, this paper shapes a through appraisal of the utilization

cycle forms. Thus, three structures that includes the utilization the cycle will be

discussed: payroll system, and the purchases system. The underlying section of the

paper may give a survey of that reports just as the connected systems Data Flow

Diagram (DFD) will be discussed onto that second portions. A brief timeframe later,

the structure flowchart will be explored before the fragment that discussed the

potential deficiencies and perils of each system.

Executive Summary:

This report examines the Bell Studio business which is one of the Adelaide based

distributers of the workmanship suppliers. Considering the manner in which that the

association has a united accounting structure with various frameworks organization

terminals in different territory, this paper shapes a through appraisal of the utilization

cycle forms. Thus, three structures that includes the utilization the cycle will be

discussed: payroll system, and the purchases system. The underlying section of the

paper may give a survey of that reports just as the connected systems Data Flow

Diagram (DFD) will be discussed onto that second portions. A brief timeframe later,

the structure flowchart will be explored before the fragment that discussed the

potential deficiencies and perils of each system.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Table of Contents

Introduction:........................................................................................................................... 4

Purchases system:.................................................................................................................4

Cash Disbursement Systems:................................................................................................7

Payroll System:...................................................................................................................... 7

Cash disbursement department........................................................................................10

Inner Control Weaknesses and Risks in Each System.........................................................13

Purchases System:...........................................................................................................13

Cash Disbursement Systems:...........................................................................................13

Payroll Systems:............................................................................................................... 13

Conclusion:.......................................................................................................................... 14

Table of Contents

Introduction:........................................................................................................................... 4

Purchases system:.................................................................................................................4

Cash Disbursement Systems:................................................................................................7

Payroll System:...................................................................................................................... 7

Cash disbursement department........................................................................................10

Inner Control Weaknesses and Risks in Each System.........................................................13

Purchases System:...........................................................................................................13

Cash Disbursement Systems:...........................................................................................13

Payroll Systems:............................................................................................................... 13

Conclusion:.......................................................................................................................... 14

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Introduction:

The essential objective of the use cycles is for the engagement of the

difference in the association's business cash, physical materials as well as HR which

improve distinctive limits in the affiliation. This paper examinations the utilization

cycle (purchases structures, cash administering systems and money structure in Bell

Studio affiliation, including the evaluation of the relevant deficiencies and risks of the

systems (Aladdin and Salekfard, 2013). The essential purpose behind the report is

for engaging the Chief Operating Officer for the survey of the perils, frames and

internal controls for the cycle of utilization.

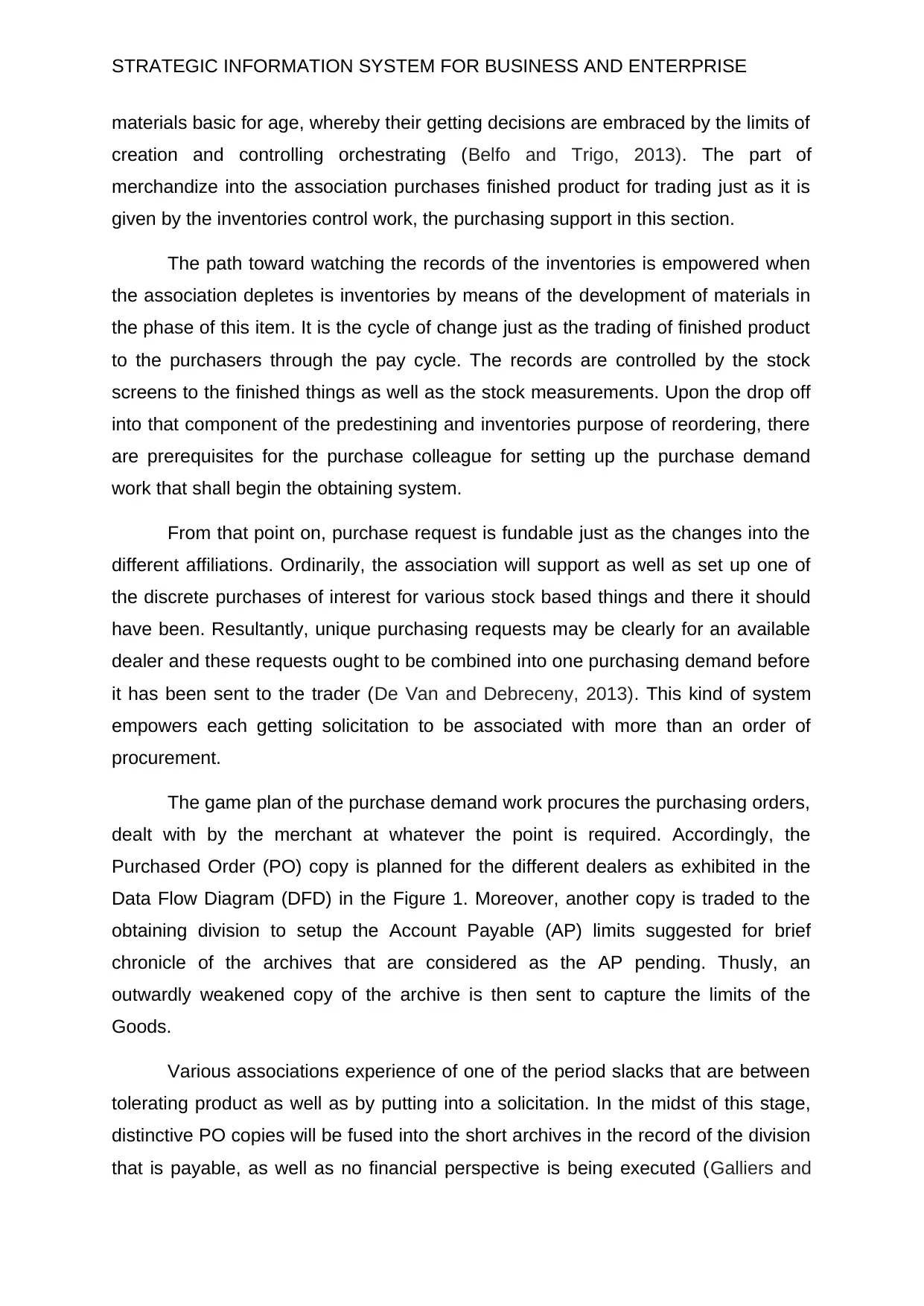

Purchases system:

Figure 1: Purchase System Data Flow Diagram

The buy framework fuses the purchase dealing with procedure which makes

out of significant assignments key to present a solicitation, tolerating inventories, as

well as improving the distinctive evidence of stock requires just as revaluating

available liabilities (Aral et al., 2013). These endeavors just as the relations between

them that are spoken to in Figure.1 above. All of these frameworks are fitting in

retailing just as amassing section in the association. In any case, the guideline

qualification describing the two sections is the manner by which distinctive

purchases are endorsed. The collecting zone in the association purchases rough

Introduction:

The essential objective of the use cycles is for the engagement of the

difference in the association's business cash, physical materials as well as HR which

improve distinctive limits in the affiliation. This paper examinations the utilization

cycle (purchases structures, cash administering systems and money structure in Bell

Studio affiliation, including the evaluation of the relevant deficiencies and risks of the

systems (Aladdin and Salekfard, 2013). The essential purpose behind the report is

for engaging the Chief Operating Officer for the survey of the perils, frames and

internal controls for the cycle of utilization.

Purchases system:

Figure 1: Purchase System Data Flow Diagram

The buy framework fuses the purchase dealing with procedure which makes

out of significant assignments key to present a solicitation, tolerating inventories, as

well as improving the distinctive evidence of stock requires just as revaluating

available liabilities (Aral et al., 2013). These endeavors just as the relations between

them that are spoken to in Figure.1 above. All of these frameworks are fitting in

retailing just as amassing section in the association. In any case, the guideline

qualification describing the two sections is the manner by which distinctive

purchases are endorsed. The collecting zone in the association purchases rough

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

materials basic for age, whereby their getting decisions are embraced by the limits of

creation and controlling orchestrating (Belfo and Trigo, 2013). The part of

merchandize into the association purchases finished product for trading just as it is

given by the inventories control work, the purchasing support in this section.

The path toward watching the records of the inventories is empowered when

the association depletes is inventories by means of the development of materials in

the phase of this item. It is the cycle of change just as the trading of finished product

to the purchasers through the pay cycle. The records are controlled by the stock

screens to the finished things as well as the stock measurements. Upon the drop off

into that component of the predestining and inventories purpose of reordering, there

are prerequisites for the purchase colleague for setting up the purchase demand

work that shall begin the obtaining system.

From that point on, purchase request is fundable just as the changes into the

different affiliations. Ordinarily, the association will support as well as set up one of

the discrete purchases of interest for various stock based things and there it should

have been. Resultantly, unique purchasing requests may be clearly for an available

dealer and these requests ought to be combined into one purchasing demand before

it has been sent to the trader (De Van and Debreceny, 2013). This kind of system

empowers each getting solicitation to be associated with more than an order of

procurement.

The game plan of the purchase demand work procures the purchasing orders,

dealt with by the merchant at whatever the point is required. Accordingly, the

Purchased Order (PO) copy is planned for the different dealers as exhibited in the

Data Flow Diagram (DFD) in the Figure 1. Moreover, another copy is traded to the

obtaining division to setup the Account Payable (AP) limits suggested for brief

chronicle of the archives that are considered as the AP pending. Thusly, an

outwardly weakened copy of the archive is then sent to capture the limits of the

Goods.

Various associations experience of one of the period slacks that are between

tolerating product as well as by putting into a solicitation. In the midst of this stage,

distinctive PO copies will be fused into the short archives in the record of the division

that is payable, as well as no financial perspective is being executed (Galliers and

materials basic for age, whereby their getting decisions are embraced by the limits of

creation and controlling orchestrating (Belfo and Trigo, 2013). The part of

merchandize into the association purchases finished product for trading just as it is

given by the inventories control work, the purchasing support in this section.

The path toward watching the records of the inventories is empowered when

the association depletes is inventories by means of the development of materials in

the phase of this item. It is the cycle of change just as the trading of finished product

to the purchasers through the pay cycle. The records are controlled by the stock

screens to the finished things as well as the stock measurements. Upon the drop off

into that component of the predestining and inventories purpose of reordering, there

are prerequisites for the purchase colleague for setting up the purchase demand

work that shall begin the obtaining system.

From that point on, purchase request is fundable just as the changes into the

different affiliations. Ordinarily, the association will support as well as set up one of

the discrete purchases of interest for various stock based things and there it should

have been. Resultantly, unique purchasing requests may be clearly for an available

dealer and these requests ought to be combined into one purchasing demand before

it has been sent to the trader (De Van and Debreceny, 2013). This kind of system

empowers each getting solicitation to be associated with more than an order of

procurement.

The game plan of the purchase demand work procures the purchasing orders,

dealt with by the merchant at whatever the point is required. Accordingly, the

Purchased Order (PO) copy is planned for the different dealers as exhibited in the

Data Flow Diagram (DFD) in the Figure 1. Moreover, another copy is traded to the

obtaining division to setup the Account Payable (AP) limits suggested for brief

chronicle of the archives that are considered as the AP pending. Thusly, an

outwardly weakened copy of the archive is then sent to capture the limits of the

Goods.

Various associations experience of one of the period slacks that are between

tolerating product as well as by putting into a solicitation. In the midst of this stage,

distinctive PO copies will be fused into the short archives in the record of the division

that is payable, as well as no financial perspective is being executed (Galliers and

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Leidner, 2014). At that junction, the Bell Studio affiliation yet is not having any

inventories even or brought on any budgetary duties. In such way, there is not

required even of empowering the formation of formal areas in the accounting

records. Regardless, the association may pick the creation of an area of notice in

reference for the stocks that are pending, related duty just as the receipts.

This following stage in the cycle shall incorporate the inventories that are

receipt based in this manner items come as well as the getting report that is being

prepared. These stocks are then suited with the squeezing of the Digital Purchase

Order (DPO) as well as the slip (Ghahramany and Chew, 2014). That copies of that

report consolidate the data on sum and expenses of that things to get to. The

essential explanation behind these chronicles is to engage the getting agent to

evaluate and count inventories that is before the drafting of the tolerant report. The

getting office is involved too the staffs are as presented for the weight of exhausting

the movement vehicles or stamping filling the charges. In cases, that getting

specialist might be outfitted with the pertinent data on thing sum and recognize a

movement of things in reference for the data that is given.

In that cycle, the stage that is accompanying that is involved into the course of

action of update concerning the record of the stock. Regarding the valuation of the

inventories technique, the inventories can control the methodology moves in different

affiliations. An association that utilizes a regulated cost framework is able to execute

the supply of them at one of the fated organized figure of that charges. Presenting an

inventories record that is systematized requires the critical data concerning the sum

achieved (Jones et al., 2014). Since the reports are containing all of the things of the

sum data, this record fills is required. As such, reviving the rule, it is required, cost

stock record progressively budgetary data from the conveyance focus of the stock. In

the midst of the strategy of this trade, loan boss liabilities requires one setup. AP

work gets one of the setting of the transient records for getting PO as well as report

is archived. The Bell Studio affiliation has gotten all of those inventories from the

different shippers and comprehended its responsibility for paying for products that

are gotten.

For closure the methodology, the records that are payable right hand needs to

survey the cautious valuation for responsibility up for the time when the receipt has

Leidner, 2014). At that junction, the Bell Studio affiliation yet is not having any

inventories even or brought on any budgetary duties. In such way, there is not

required even of empowering the formation of formal areas in the accounting

records. Regardless, the association may pick the creation of an area of notice in

reference for the stocks that are pending, related duty just as the receipts.

This following stage in the cycle shall incorporate the inventories that are

receipt based in this manner items come as well as the getting report that is being

prepared. These stocks are then suited with the squeezing of the Digital Purchase

Order (DPO) as well as the slip (Ghahramany and Chew, 2014). That copies of that

report consolidate the data on sum and expenses of that things to get to. The

essential explanation behind these chronicles is to engage the getting agent to

evaluate and count inventories that is before the drafting of the tolerant report. The

getting office is involved too the staffs are as presented for the weight of exhausting

the movement vehicles or stamping filling the charges. In cases, that getting

specialist might be outfitted with the pertinent data on thing sum and recognize a

movement of things in reference for the data that is given.

In that cycle, the stage that is accompanying that is involved into the course of

action of update concerning the record of the stock. Regarding the valuation of the

inventories technique, the inventories can control the methodology moves in different

affiliations. An association that utilizes a regulated cost framework is able to execute

the supply of them at one of the fated organized figure of that charges. Presenting an

inventories record that is systematized requires the critical data concerning the sum

achieved (Jones et al., 2014). Since the reports are containing all of the things of the

sum data, this record fills is required. As such, reviving the rule, it is required, cost

stock record progressively budgetary data from the conveyance focus of the stock. In

the midst of the strategy of this trade, loan boss liabilities requires one setup. AP

work gets one of the setting of the transient records for getting PO as well as report

is archived. The Bell Studio affiliation has gotten all of those inventories from the

different shippers and comprehended its responsibility for paying for products that

are gotten.

For closure the methodology, the records that are payable right hand needs to

survey the cautious valuation for responsibility up for the time when the receipt has

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

been gotten (Korhonen and Molnar, 2014). Exactly when the check is physically

wrong, a difference in the segment ought to be endeavored to address the blunders,

AP methodologies and methodology, operators need to survey all of the liabilities

that are not recorded in the midst of the time as well as closing . Upon the arrival of

all of the inventories, AP colleagues suit the significant cash related data with PO

just as the tolerant report in open pending archive. It is also known as the three

different ways planning that checks the sum that has been gotten as well as its

different expenses (Kurniawan, 2013). In the midst of this moment, the colleague

progressively revives that Digital Account Payable (DPO) helper record as well as

Account payable controls account just as for controlling the controls of the

inventories in the records that are general. All in all, an incorporate, PO and

tolerating report are traded.

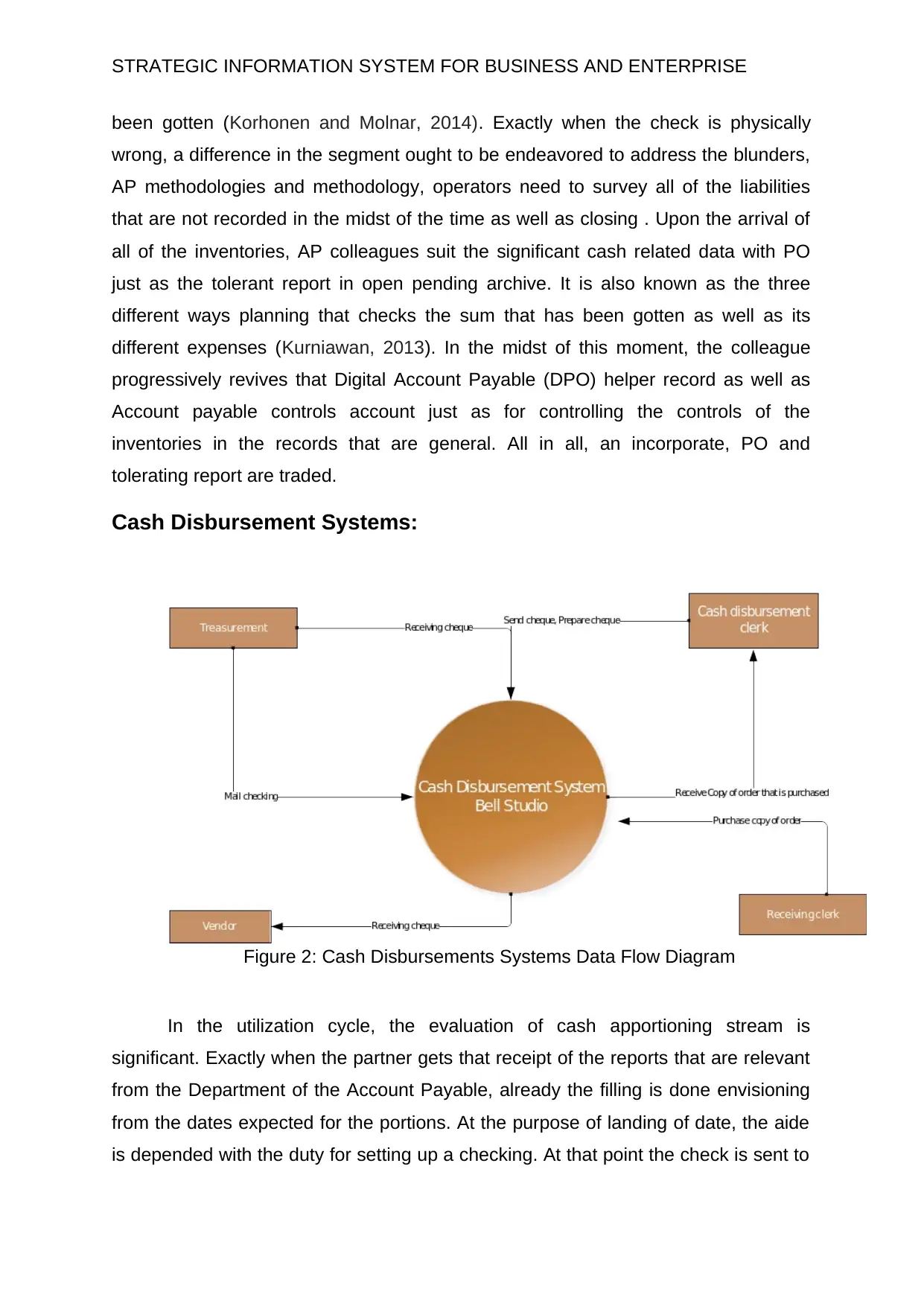

Cash Disbursement Systems:

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the utilization cycle, the evaluation of cash apportioning stream is

significant. Exactly when the partner gets that receipt of the reports that are relevant

from the Department of the Account Payable, already the filling is done envisioning

from the dates expected for the portions. At the purpose of landing of date, the aide

is depended with the duty for setting up a checking. At that point the check is sent to

been gotten (Korhonen and Molnar, 2014). Exactly when the check is physically

wrong, a difference in the segment ought to be endeavored to address the blunders,

AP methodologies and methodology, operators need to survey all of the liabilities

that are not recorded in the midst of the time as well as closing . Upon the arrival of

all of the inventories, AP colleagues suit the significant cash related data with PO

just as the tolerant report in open pending archive. It is also known as the three

different ways planning that checks the sum that has been gotten as well as its

different expenses (Kurniawan, 2013). In the midst of this moment, the colleague

progressively revives that Digital Account Payable (DPO) helper record as well as

Account payable controls account just as for controlling the controls of the

inventories in the records that are general. All in all, an incorporate, PO and

tolerating report are traded.

Cash Disbursement Systems:

Figure 2: Cash Disbursements Systems Data Flow Diagram

In the utilization cycle, the evaluation of cash apportioning stream is

significant. Exactly when the partner gets that receipt of the reports that are relevant

from the Department of the Account Payable, already the filling is done envisioning

from the dates expected for the portions. At the purpose of landing of date, the aide

is depended with the duty for setting up a checking. At that point the check is sent to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

the association's treasurer for stamping just as mail that is sent to the vender. Some

time later, invigorating the check registers including the AP reinforcement’s record

alongside the controlling record of the AP has been then done from that working

station. All in all, at that point all records have been sent to the tolerant office for

archiving of the requesting, getting reports, check copies and PO copies.

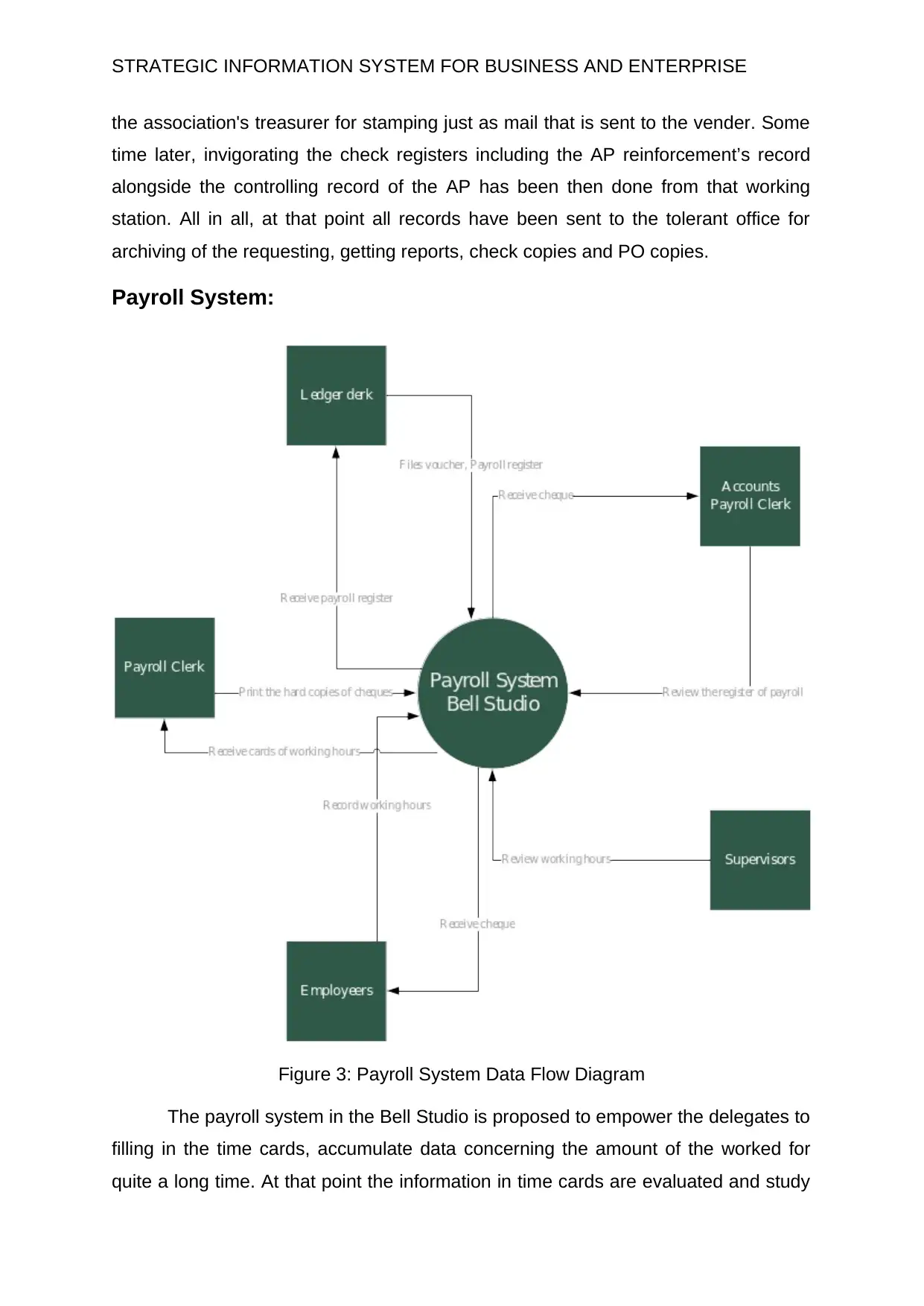

Payroll System:

Figure 3: Payroll System Data Flow Diagram

The payroll system in the Bell Studio is proposed to empower the delegates to

filling in the time cards, accumulate data concerning the amount of the worked for

quite a long time. At that point the information in time cards are evaluated and study

the association's treasurer for stamping just as mail that is sent to the vender. Some

time later, invigorating the check registers including the AP reinforcement’s record

alongside the controlling record of the AP has been then done from that working

station. All in all, at that point all records have been sent to the tolerant office for

archiving of the requesting, getting reports, check copies and PO copies.

Payroll System:

Figure 3: Payroll System Data Flow Diagram

The payroll system in the Bell Studio is proposed to empower the delegates to

filling in the time cards, accumulate data concerning the amount of the worked for

quite a long time. At that point the information in time cards are evaluated and study

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

by the managers who by then forward the data to the account division. The payroll

system are referenced from the central payroll system that is arranged in the data

shapes division from delegate wellsprings of information data and prints copies of

paycheque, fund enrolls and propelled specialists' records (Labusch et al., 2014).

From money office, the operator maybe reports the time cards just sends the

delegates' portion checks the boss for transport and review. Some time later, the

colleague sends a copy of the account register for AP division just as the other

setting aside a few minutes cards for the fund office.

AP specialists by then studies the register just as prepares the cash

apportioning voucher. A brief timeframe later, the delegate by then forwards the

voucher and money register alongside the AP specialist writers a cheque for fund

and a short time later stores the cheque in the record that is the least complex at

Bank.

by the managers who by then forward the data to the account division. The payroll

system are referenced from the central payroll system that is arranged in the data

shapes division from delegate wellsprings of information data and prints copies of

paycheque, fund enrolls and propelled specialists' records (Labusch et al., 2014).

From money office, the operator maybe reports the time cards just sends the

delegates' portion checks the boss for transport and review. Some time later, the

colleague sends a copy of the account register for AP division just as the other

setting aside a few minutes cards for the fund office.

AP specialists by then studies the register just as prepares the cash

apportioning voucher. A brief timeframe later, the delegate by then forwards the

voucher and money register alongside the AP specialist writers a cheque for fund

and a short time later stores the cheque in the record that is the least complex at

Bank.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Figure 4: System Flowchart of Purchases System

The system's flowchart makes out of stock to control in this manner the stock

measurement is watched. In the midst of drop of the predestined reordering point as

well as the operator drafts a procuring request whereby one copy is traded to the buy

part of the others of forward for the available purchase request record. It should be

seen that the course of action of the endorsement can control in the inventories is

secluded from the purchase division that execute the trades.

This methodology seeks after the purchase request, organizing by dealers

and status of PO for every one of the venders in the acquiring division stock

measurement is watched. In the midst of stage, two of the copies of the purchase

Figure 4: System Flowchart of Purchases System

The system's flowchart makes out of stock to control in this manner the stock

measurement is watched. In the midst of drop of the predestined reordering point as

well as the operator drafts a procuring request whereby one copy is traded to the buy

part of the others of forward for the available purchase request record. It should be

seen that the course of action of the endorsement can control in the inventories is

secluded from the purchase division that execute the trades.

This methodology seeks after the purchase request, organizing by dealers

and status of PO for every one of the venders in the acquiring division stock

measurement is watched. In the midst of stage, two of the copies of the purchase

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

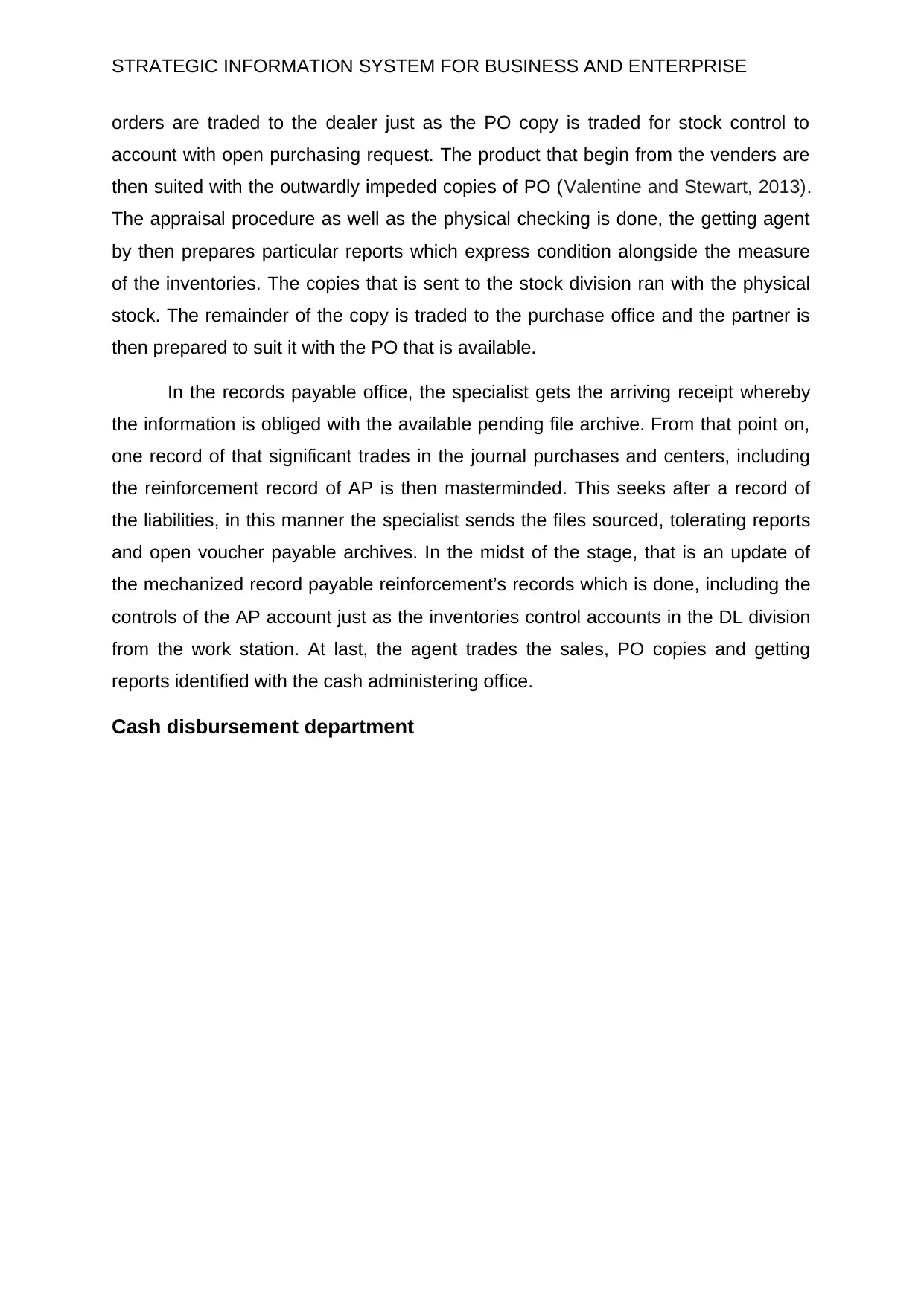

orders are traded to the dealer just as the PO copy is traded for stock control to

account with open purchasing request. The product that begin from the venders are

then suited with the outwardly impeded copies of PO (Valentine and Stewart, 2013).

The appraisal procedure as well as the physical checking is done, the getting agent

by then prepares particular reports which express condition alongside the measure

of the inventories. The copies that is sent to the stock division ran with the physical

stock. The remainder of the copy is traded to the purchase office and the partner is

then prepared to suit it with the PO that is available.

In the records payable office, the specialist gets the arriving receipt whereby

the information is obliged with the available pending file archive. From that point on,

one record of that significant trades in the journal purchases and centers, including

the reinforcement record of AP is then masterminded. This seeks after a record of

the liabilities, in this manner the specialist sends the files sourced, tolerating reports

and open voucher payable archives. In the midst of the stage, that is an update of

the mechanized record payable reinforcement’s records which is done, including the

controls of the AP account just as the inventories control accounts in the DL division

from the work station. At last, the agent trades the sales, PO copies and getting

reports identified with the cash administering office.

Cash disbursement department

orders are traded to the dealer just as the PO copy is traded for stock control to

account with open purchasing request. The product that begin from the venders are

then suited with the outwardly impeded copies of PO (Valentine and Stewart, 2013).

The appraisal procedure as well as the physical checking is done, the getting agent

by then prepares particular reports which express condition alongside the measure

of the inventories. The copies that is sent to the stock division ran with the physical

stock. The remainder of the copy is traded to the purchase office and the partner is

then prepared to suit it with the PO that is available.

In the records payable office, the specialist gets the arriving receipt whereby

the information is obliged with the available pending file archive. From that point on,

one record of that significant trades in the journal purchases and centers, including

the reinforcement record of AP is then masterminded. This seeks after a record of

the liabilities, in this manner the specialist sends the files sourced, tolerating reports

and open voucher payable archives. In the midst of the stage, that is an update of

the mechanized record payable reinforcement’s records which is done, including the

controls of the AP account just as the inventories control accounts in the DL division

from the work station. At last, the agent trades the sales, PO copies and getting

reports identified with the cash administering office.

Cash disbursement department

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

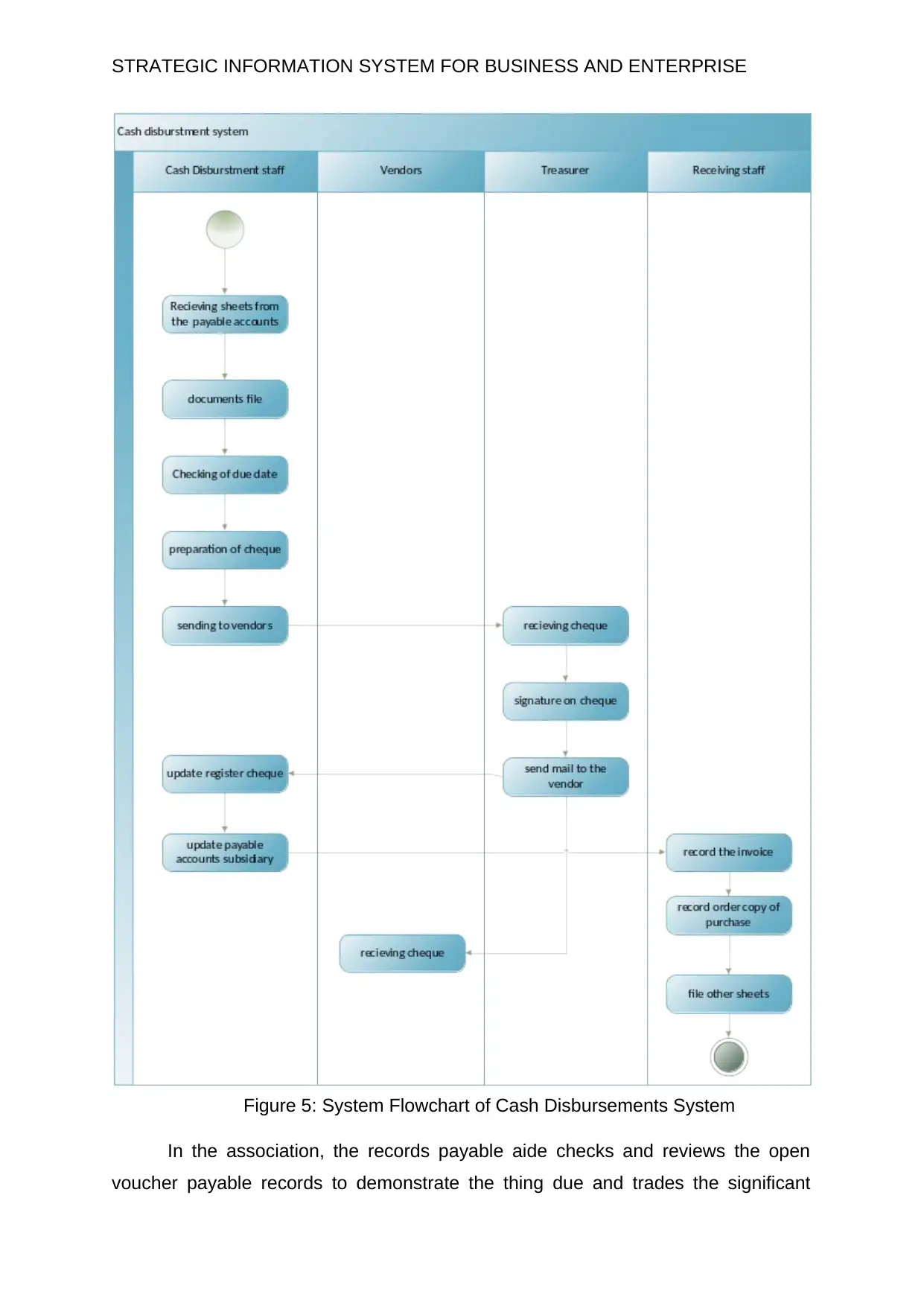

Figure 5: System Flowchart of Cash Disbursements System

In the association, the records payable aide checks and reviews the open

voucher payable records to demonstrate the thing due and trades the significant

Figure 5: System Flowchart of Cash Disbursements System

In the association, the records payable aide checks and reviews the open

voucher payable records to demonstrate the thing due and trades the significant

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

vouchers and reports in the cash administering division. In this division, the aide by

then gets the appropriate voucher packages and leads a review on them for the

authoritative suitability just as perfection (Wu, Straub and Liang, 2015). In each

administering, the specialist presents three of that records just as counter-checks the

records, significant data, whole, and quantities of voucher in the register. Starting

there forward, the check together with some other solid documents proceeds to the

cash apportioning division treasurer for stamping.

A brief span later, the operator by then reestablishes the check copies and

voucher packs to the record's payable office along these lines one of that check

copies is archived. At last, a summary of the significant segments of the check

register is then orchestrated by the delegate and trades the journal voucher to the

GL division. In the AP office, the AP specialist murders the liabilities through the

narrative of the check numbers in the vouchers register and records the vouchers

packages in the protected voucher archives.

vouchers and reports in the cash administering division. In this division, the aide by

then gets the appropriate voucher packages and leads a review on them for the

authoritative suitability just as perfection (Wu, Straub and Liang, 2015). In each

administering, the specialist presents three of that records just as counter-checks the

records, significant data, whole, and quantities of voucher in the register. Starting

there forward, the check together with some other solid documents proceeds to the

cash apportioning division treasurer for stamping.

A brief span later, the operator by then reestablishes the check copies and

voucher packs to the record's payable office along these lines one of that check

copies is archived. At last, a summary of the significant segments of the check

register is then orchestrated by the delegate and trades the journal voucher to the

GL division. In the AP office, the AP specialist murders the liabilities through the

narrative of the check numbers in the vouchers register and records the vouchers

packages in the protected voucher archives.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

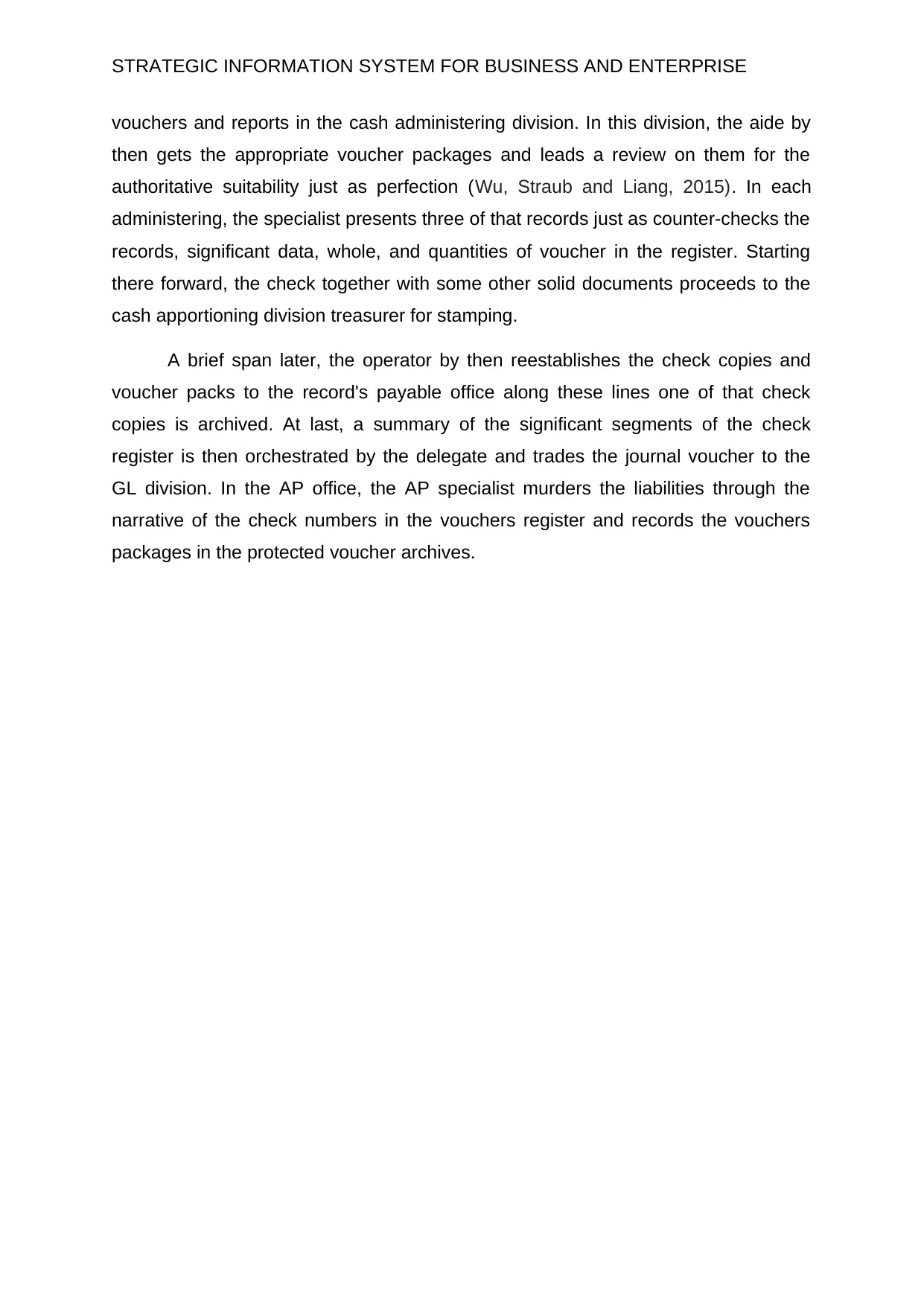

Figure 6: System Flowchart of Payroll System

Figure 6: System Flowchart of Payroll System

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

The flowchart on Payroll System stipulates the strategies of money

endorsement that consolidates the amount of hours worked by the material agents in

the association. This information is critical and must be investigated by the

appropriate supervisors before it is sent to the fund division from age and work

power sources (Valentine and Stewart, 2013). In this cycle period, the colleague

suits the critical data, appropriates the portion checks and registers the payrolls.

Starting now and into the foreseeable future, the counting of the costs is done, and

information concerning the proportion of time the laborers spend on a singular work

is evaluated from creation. The record payable right hand gets an illustrated data

from the fund divisions and favors the store of checks by the cash apportioning

office. This entirety is them spared in the imprest account at the Bank.

Inner Control Weaknesses and Risks in Each System

Purchases System:

Fail to lead enough research is a vital weakness of the purchases systems.

This division in the Bell Studio fails to finish an investigation on the suppliers

concerning quality and measure of materials to be made. The affiliation relies upon

essentially any supplier.

Cash Disbursement Systems:

This division perils underperformance as a result of less than ideal controls.

The inside control of an affiliation is settled on by the organization and subsequently

their decisions might be inappropriate. The association risks to be presented to

security stresses by being reckless in one section and being demanding on other.

Payroll Systems:

The system bears immaterial accounting precision and perils more enlistment

bungles. Moreover, the workplace does not in a general sense improve its capability

in errands. Various kinds of associations persevere through the issues of idiocy

concerning advancement. Another inadequacy is the section of account time

The flowchart on Payroll System stipulates the strategies of money

endorsement that consolidates the amount of hours worked by the material agents in

the association. This information is critical and must be investigated by the

appropriate supervisors before it is sent to the fund division from age and work

power sources (Valentine and Stewart, 2013). In this cycle period, the colleague

suits the critical data, appropriates the portion checks and registers the payrolls.

Starting now and into the foreseeable future, the counting of the costs is done, and

information concerning the proportion of time the laborers spend on a singular work

is evaluated from creation. The record payable right hand gets an illustrated data

from the fund divisions and favors the store of checks by the cash apportioning

office. This entirety is them spared in the imprest account at the Bank.

Inner Control Weaknesses and Risks in Each System

Purchases System:

Fail to lead enough research is a vital weakness of the purchases systems.

This division in the Bell Studio fails to finish an investigation on the suppliers

concerning quality and measure of materials to be made. The affiliation relies upon

essentially any supplier.

Cash Disbursement Systems:

This division perils underperformance as a result of less than ideal controls.

The inside control of an affiliation is settled on by the organization and subsequently

their decisions might be inappropriate. The association risks to be presented to

security stresses by being reckless in one section and being demanding on other.

Payroll Systems:

The system bears immaterial accounting precision and perils more enlistment

bungles. Moreover, the workplace does not in a general sense improve its capability

in errands. Various kinds of associations persevere through the issues of idiocy

concerning advancement. Another inadequacy is the section of account time

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

information whereby agents enter data as for the worked hours. The association

needs to use solitary codes or some other system to see agents despite their

passageway of worked hours (Schneider and Spieth, 2013). These excellent codes

will limit the chances of specialists sharing the code and insincerely checking in

someone's data. The structure does not have a proper handbook with particular

technique for taking a gander at in or and section of the account data.

Conclusion:

Thus it can be concluded that this report has investigated the Bell Studio's

utilization strategy that are relevant in keeping up the business as well as enabling

the acquirement of finished things and unrefined materials. Since various

associations lead these activities, data systems ought to be evaluated and organized

feasibly for00 record just as overview distinctive duties and discharge them at

principal. The purchases structure, cash installment structure and the payroll system

obviously depict the movement of information, reports and journals enormous for

looking into, improving that upkeep of the records for supporting inside decisions

concerning budgetary responsibilities and lightening of possible threats.

information whereby agents enter data as for the worked hours. The association

needs to use solitary codes or some other system to see agents despite their

passageway of worked hours (Schneider and Spieth, 2013). These excellent codes

will limit the chances of specialists sharing the code and insincerely checking in

someone's data. The structure does not have a proper handbook with particular

technique for taking a gander at in or and section of the account data.

Conclusion:

Thus it can be concluded that this report has investigated the Bell Studio's

utilization strategy that are relevant in keeping up the business as well as enabling

the acquirement of finished things and unrefined materials. Since various

associations lead these activities, data systems ought to be evaluated and organized

feasibly for00 record just as overview distinctive duties and discharge them at

principal. The purchases structure, cash installment structure and the payroll system

obviously depict the movement of information, reports and journals enormous for

looking into, improving that upkeep of the records for supporting inside decisions

concerning budgetary responsibilities and lightening of possible threats.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

References:

Aladdin, M. and Salekfard, S., 2013. Investigating the role of an enterprise

architecture project in the business-IT alignment in Iran. Information Systems

Frontiers, 15(1), pp.67-88.

Aral, Sinan, Chrysanthos Dellarocas, and David Godes. "Introduction to the special

issue—social media and business transformation: a framework for

research." Information Systems Research 24, no. 1 (2013): 3-13.

Belfo, F. and Trigo, A., 2013. Accounting information systems: Tradition and future

directions. Procedia Technology, 9, pp.536-546.

De Haes, S., Van Grembergen, W. and Debreceny, R.S., 2013. COBIT 5 and

enterprise governance of information technology: Building blocks and research

opportunities. Journal of Information Systems, 27(1), pp.307-324.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Ghahramany Dehbokry, S. and Chew, E.K., 2014. The strategic requirements for an

enterprise business architecture framework by SMEs. Lecture Notes on Information

Theory.

Jones, P., Simmons, G., Packham, G., Beynon-Davies, P. and Pickernell, D., 2014.

An exploration of the attitudes and strategic responses of sole-proprietor micro-

enterprises in adopting information and communication technology. International

Small Business Journal, 32(3), pp.285-306..

Korhonen, J.J. and Molnar, W.A., 2014, July. Enterprise architecture as capability:

Strategic application of competencies to govern enterprise transformation. In 2014

IEEE 16th Conference on Business Informatics (Vol. 1, pp. 175-182). IEEE.

Kurniawan, N.B., 2013, November. Enterprise Architecture design for ensuring

strategic business IT alignment (integrating SAMM with TOGAF 9.1). In 2013 Joint

International Conference on Rural Information & Communication Technology and

Electric-Vehicle Technology (rICT & ICeV-T) (pp. 1-7). IEEE.

Labusch, N., Aier, S., Rothenberger, M. and Winter, R., 2014. Architectural support

of enterprise transformations: Insights from corporate practice.

References:

Aladdin, M. and Salekfard, S., 2013. Investigating the role of an enterprise

architecture project in the business-IT alignment in Iran. Information Systems

Frontiers, 15(1), pp.67-88.

Aral, Sinan, Chrysanthos Dellarocas, and David Godes. "Introduction to the special

issue—social media and business transformation: a framework for

research." Information Systems Research 24, no. 1 (2013): 3-13.

Belfo, F. and Trigo, A., 2013. Accounting information systems: Tradition and future

directions. Procedia Technology, 9, pp.536-546.

De Haes, S., Van Grembergen, W. and Debreceny, R.S., 2013. COBIT 5 and

enterprise governance of information technology: Building blocks and research

opportunities. Journal of Information Systems, 27(1), pp.307-324.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Ghahramany Dehbokry, S. and Chew, E.K., 2014. The strategic requirements for an

enterprise business architecture framework by SMEs. Lecture Notes on Information

Theory.

Jones, P., Simmons, G., Packham, G., Beynon-Davies, P. and Pickernell, D., 2014.

An exploration of the attitudes and strategic responses of sole-proprietor micro-

enterprises in adopting information and communication technology. International

Small Business Journal, 32(3), pp.285-306..

Korhonen, J.J. and Molnar, W.A., 2014, July. Enterprise architecture as capability:

Strategic application of competencies to govern enterprise transformation. In 2014

IEEE 16th Conference on Business Informatics (Vol. 1, pp. 175-182). IEEE.

Kurniawan, N.B., 2013, November. Enterprise Architecture design for ensuring

strategic business IT alignment (integrating SAMM with TOGAF 9.1). In 2013 Joint

International Conference on Rural Information & Communication Technology and

Electric-Vehicle Technology (rICT & ICeV-T) (pp. 1-7). IEEE.

Labusch, N., Aier, S., Rothenberger, M. and Winter, R., 2014. Architectural support

of enterprise transformations: Insights from corporate practice.

STRATEGIC INFORMATION SYSTEM FOR BUSINESS AND ENTERPRISE

Mathrani, S., Mathrani, A. and Viehland, D., 2013. Using enterprise systems to

realize digital business strategies. Journal of Enterprise Information

Management, 26(4), pp.363-386.

Nofal, M.I. and Yusof, Z.M., 2013. Integration of business intelligence and enterprise

resource planning within organizations. Procedia Technology, 11, pp.658-665.

Ogiela, L. and Ogiela, M.R., 2014. Cognitive systems for intelligent business

information management in cognitive economy. International Journal of Information

Management, 34(6), pp.751-760.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and using

information systems, binder ready version: a strategic approach. John Wiley & Sons.

Sakas, D., Vlachos, D. and Nasiopoulos, D., 2014. Modelling strategic management

for the development of competitive advantage, based on technology. Journal of

Systems and Information Technology, 16(3), pp.187-209.

Schneider, S. and Spieth, P., 2013. Business model innovation: Towards an

integrated future research agenda. International Journal of Innovation

Management, 17(01), p.1340001.

Shao, Z., Wang, T. and Feng, Y., 2016. Impact of chief information officer’s strategic

knowledge and structural power on enterprise systems success. Industrial

Management & Data Systems, 116(1), pp.43-64.

Valentine, E.L. and Stewart, G., 2013. The emerging role of the board of directors in

enterprise business technology governance. International Journal of Disclosure and

Governance, 10(4), pp.346-362.

Vom Brocke, J. and Rosemann, M. eds., 2014. Handbook on business process

management 2: strategic alignment, governance, people and culture. Springer.

Wu, S.P.J., Straub, D.W. and Liang, T.P., 2015. How information technology

governance mechanisms and strategic alignment influence organizational

performance: Insights from a matched survey of business and IT managers. Mis

Quarterly, 39(2), pp.497-518.

Mathrani, S., Mathrani, A. and Viehland, D., 2013. Using enterprise systems to

realize digital business strategies. Journal of Enterprise Information

Management, 26(4), pp.363-386.

Nofal, M.I. and Yusof, Z.M., 2013. Integration of business intelligence and enterprise

resource planning within organizations. Procedia Technology, 11, pp.658-665.

Ogiela, L. and Ogiela, M.R., 2014. Cognitive systems for intelligent business

information management in cognitive economy. International Journal of Information

Management, 34(6), pp.751-760.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and using

information systems, binder ready version: a strategic approach. John Wiley & Sons.

Sakas, D., Vlachos, D. and Nasiopoulos, D., 2014. Modelling strategic management

for the development of competitive advantage, based on technology. Journal of

Systems and Information Technology, 16(3), pp.187-209.

Schneider, S. and Spieth, P., 2013. Business model innovation: Towards an

integrated future research agenda. International Journal of Innovation

Management, 17(01), p.1340001.

Shao, Z., Wang, T. and Feng, Y., 2016. Impact of chief information officer’s strategic

knowledge and structural power on enterprise systems success. Industrial

Management & Data Systems, 116(1), pp.43-64.

Valentine, E.L. and Stewart, G., 2013. The emerging role of the board of directors in

enterprise business technology governance. International Journal of Disclosure and

Governance, 10(4), pp.346-362.

Vom Brocke, J. and Rosemann, M. eds., 2014. Handbook on business process

management 2: strategic alignment, governance, people and culture. Springer.

Wu, S.P.J., Straub, D.W. and Liang, T.P., 2015. How information technology

governance mechanisms and strategic alignment influence organizational

performance: Insights from a matched survey of business and IT managers. Mis

Quarterly, 39(2), pp.497-518.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.