Strategic Information Systems for Business and Enterprise

VerifiedAdded on 2022/12/13

|9

|2597

|87

AI Summary

This report discusses the importance of strategic information systems in business and enterprise. It explores the benefits of separating departments in the revenue cycle of RCE Limited and identifies potential weaknesses, risks, and frauds in sales order processing procedures and cash receipts procedures. The report concludes with recommendations for mitigating these risks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Strategic Information Systems

for Business and Enterprise

for Business and Enterprise

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Discussing the statement..............................................................................................................3

Potential internal control weakness in Sales Order Processing Procedures and Cash Receipts

Procedures....................................................................................................................................5

Potential risks identified..............................................................................................................7

Possible Types of frauds..............................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

Discussing the statement..............................................................................................................3

Potential internal control weakness in Sales Order Processing Procedures and Cash Receipts

Procedures....................................................................................................................................5

Potential risks identified..............................................................................................................7

Possible Types of frauds..............................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Strategic Information System is basically a business information system which has

appropriate features in it. This deals with the platform embedded with technology for integrating

and coordinating the business processes on the foundation which is robust. This involves vision,

setting goals along with appropriate steps to reach those goals. RCE limited is a whole seller

which deals in the camping and rafting of the equipments and it is based in Queensland. The

report will shed light on discussing the investment which company makes in separating the

departments instead of making them as one and this will consider the revenue cycle of RCE. This

will be followed by mentioning the weaknesses, risks and frauds of Sales Order Processing

procedure and Cash receipt procedure and the ways to mitigate them.

Discussing the statement

The companies like RCE invest more in establishing the separate departments for

shipping, warehousing and inventory control. The company considers this as the additional costs

but necessary for the enhanced benefits of control over inventory. This statement will be

analysed by considering the revenue cycle of RCE. The company RCE limited has separate

department for the purpose of warehousing as the main function of this department is offering

appropriate and sufficient space for stocking the merchandise with full safety from the elements.

This function needs to be performed separately as compared to other functions. The shipping

department must be separate as it focuses on the movement of inventory which can be outgoing

as well as incoming (Ritchi and et.al., 2020). The small companies might have combined

department for all these functions as they as one warehouse for more than one function. The

larger firms like RCE have separate departments and warehouses for handling these tasks. The

major reason behind separating larger firms is keeping space which is free of obstruction at the

place of loading dock.

The warehouse in RCE Company is responsible for maintaining the inventory control’s

inventory section. The major two approaches which are applicable for the control of inventory

under the situations of emergency are reorder cycle policy and reorder level policy. When the

supply is matched with the demand which is created by customers along with building a supply

chain management which has both adaptableness and elasticity is considered as inventory

management task. In the world of today’s business, it is must to separate all the functions of the

3

Strategic Information System is basically a business information system which has

appropriate features in it. This deals with the platform embedded with technology for integrating

and coordinating the business processes on the foundation which is robust. This involves vision,

setting goals along with appropriate steps to reach those goals. RCE limited is a whole seller

which deals in the camping and rafting of the equipments and it is based in Queensland. The

report will shed light on discussing the investment which company makes in separating the

departments instead of making them as one and this will consider the revenue cycle of RCE. This

will be followed by mentioning the weaknesses, risks and frauds of Sales Order Processing

procedure and Cash receipt procedure and the ways to mitigate them.

Discussing the statement

The companies like RCE invest more in establishing the separate departments for

shipping, warehousing and inventory control. The company considers this as the additional costs

but necessary for the enhanced benefits of control over inventory. This statement will be

analysed by considering the revenue cycle of RCE. The company RCE limited has separate

department for the purpose of warehousing as the main function of this department is offering

appropriate and sufficient space for stocking the merchandise with full safety from the elements.

This function needs to be performed separately as compared to other functions. The shipping

department must be separate as it focuses on the movement of inventory which can be outgoing

as well as incoming (Ritchi and et.al., 2020). The small companies might have combined

department for all these functions as they as one warehouse for more than one function. The

larger firms like RCE have separate departments and warehouses for handling these tasks. The

major reason behind separating larger firms is keeping space which is free of obstruction at the

place of loading dock.

The warehouse in RCE Company is responsible for maintaining the inventory control’s

inventory section. The major two approaches which are applicable for the control of inventory

under the situations of emergency are reorder cycle policy and reorder level policy. When the

supply is matched with the demand which is created by customers along with building a supply

chain management which has both adaptableness and elasticity is considered as inventory

management task. In the world of today’s business, it is must to separate all the functions of the

3

business. This is why, RCE also prefers investing more money in separating the different

departments. The inventory management in today’s emerging world is becoming computerized.

In the system of vendor management, there is generation of daily reports and then the same are

sent to the distributor who is responsible for stocking up as per the requirements (Nababan and

et.al., 2020). The distributor is able to see what is being sold and also various appropriate

provisions are created for restocking the customers. In this system, when the departments are

separated and perform their functions separately, there is also no paperwork required for keeping

the supply chain continuous and all the functions can be performed computerized. This

additional cost is not considered by RCE as it provide various types of benefits of control over

inventory.

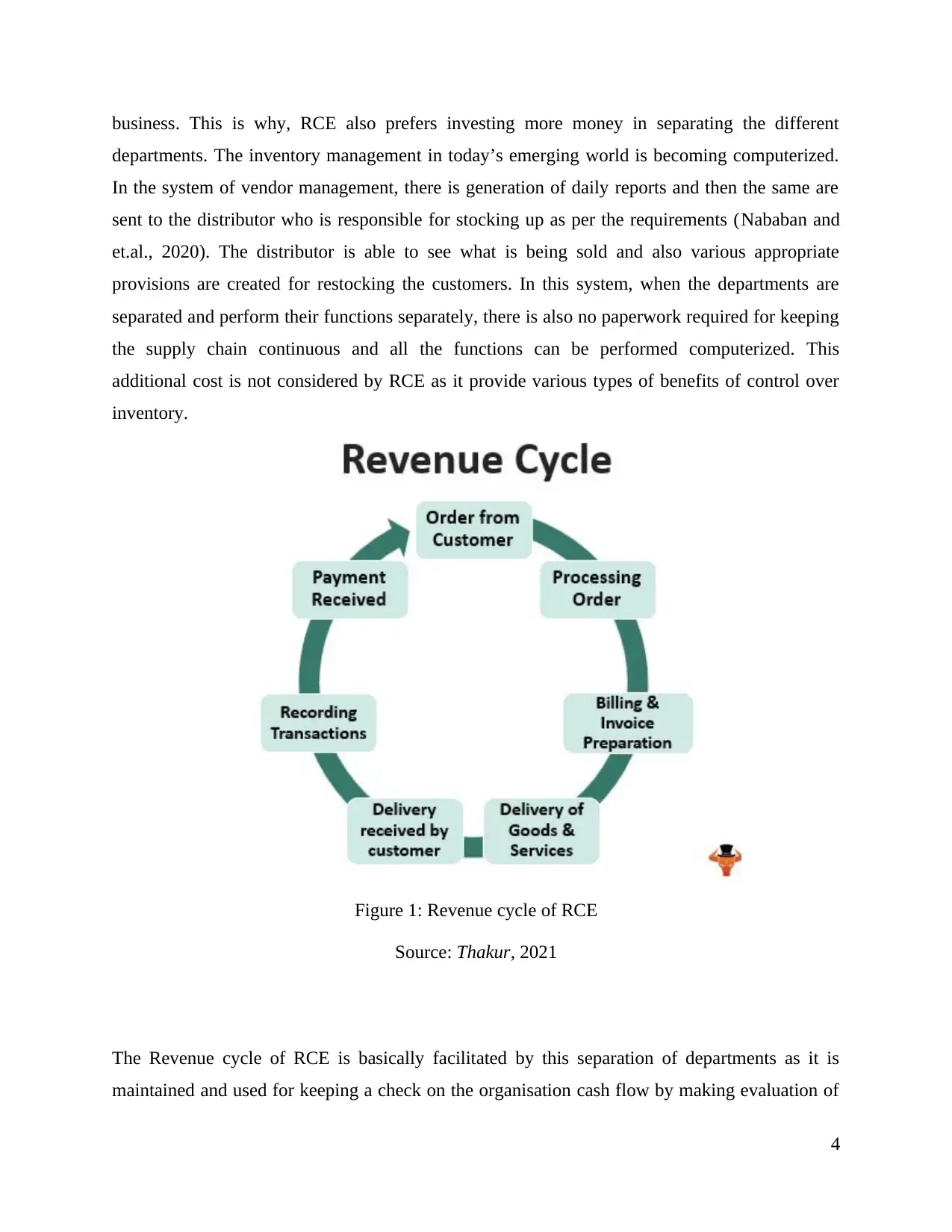

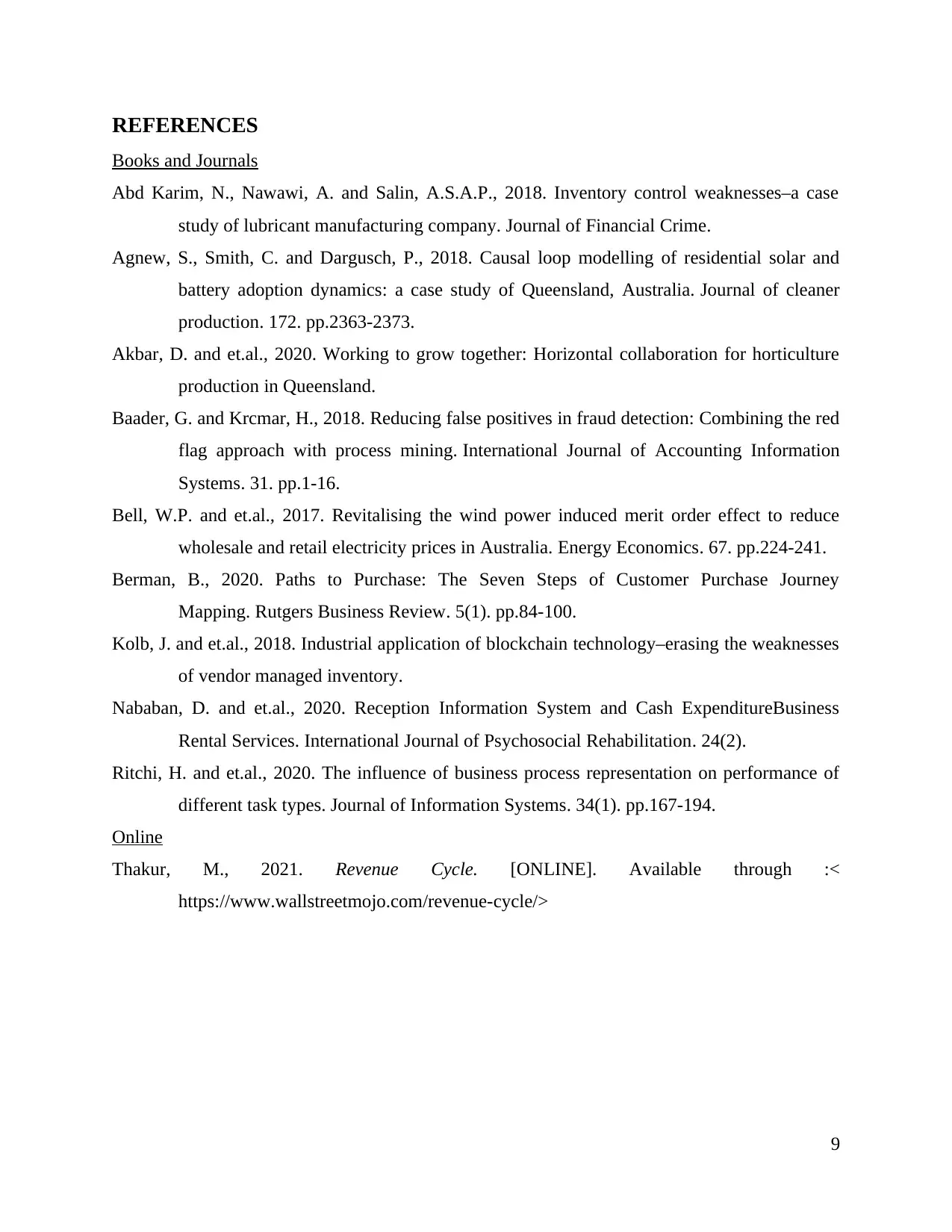

Figure 1: Revenue cycle of RCE

Source: Thakur, 2021

The Revenue cycle of RCE is basically facilitated by this separation of departments as it is

maintained and used for keeping a check on the organisation cash flow by making evaluation of

4

departments. The inventory management in today’s emerging world is becoming computerized.

In the system of vendor management, there is generation of daily reports and then the same are

sent to the distributor who is responsible for stocking up as per the requirements (Nababan and

et.al., 2020). The distributor is able to see what is being sold and also various appropriate

provisions are created for restocking the customers. In this system, when the departments are

separated and perform their functions separately, there is also no paperwork required for keeping

the supply chain continuous and all the functions can be performed computerized. This

additional cost is not considered by RCE as it provide various types of benefits of control over

inventory.

Figure 1: Revenue cycle of RCE

Source: Thakur, 2021

The Revenue cycle of RCE is basically facilitated by this separation of departments as it is

maintained and used for keeping a check on the organisation cash flow by making evaluation of

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the profit making activities. When the departments are separated, then this can help in gaining

the management of cycle by reducing the time of receipt of the services or product of the

organisation to the customers who are interested along with reducing the time of payment which

is basically received from the customers. This is how; RCE is being facilitated from the

separation of departments and warehouses (Baader and Krcmar, 2018). The revenue cycle of

RCE is divided into various systematic phases such as receiving order from customer, processing

the order, billing and preparing of invoices, delivery of invoice and goods to the customer,

receiving of delivery by customer, records of accounts to be received and payments by the

customers. If all these processes are to be done under one department then the functioning cannot

be smooth and effective. This is why, the RCE limited do not hesitate in investing more amount

in separating the departments of warehouse, shipping and inventory. This is how, the revenue

cycle of the RCE limited provide many benefits to the company.

Potential internal control weakness in Sales Order Processing Procedures and Cash Receipts

Procedures

The sales department of RCE limited is responsible for receiving the unstandardised sales

order because the customers’ orders are faxed, emailed etc. to the department of sales. The clerk

of the sales converts the unstandardised into standardised sales by requesting any missing kind of

information if any. Then the creditworthiness of the customers is checked by the sales clerk by

making use of accounting department also if they have any relevant information regarding the

same. If the credit is not verified then the order is rejected. Therefore, the process of SOPP starts

after the verification of the credit. It is the responsibility of the sales clerk to record the sales

order in the system through the terminal. The weakness here is there are lot many problems in

case of absence of sales clerk. This is why, the digital copy is also distributed to the shipping as

well as warehouse department. This weakness is solved in RCE by making use of computers

which automatically records the sale in the journal of sales (Agnew, Smith and Dargusch, 2018).

The clerk is responsible for reviewing the entry and files the customer’s hard copy in the

department of sales. On the computer of the warehouse manager, the digital sales receipt is

prompted and then shipping notice and stock release also becomes accessible at the terminal of

warehouse. The same is then printed. The weakness here is that every department is depended on

the other. When there is inefficient functioning of one department then the functioning of the

5

the management of cycle by reducing the time of receipt of the services or product of the

organisation to the customers who are interested along with reducing the time of payment which

is basically received from the customers. This is how; RCE is being facilitated from the

separation of departments and warehouses (Baader and Krcmar, 2018). The revenue cycle of

RCE is divided into various systematic phases such as receiving order from customer, processing

the order, billing and preparing of invoices, delivery of invoice and goods to the customer,

receiving of delivery by customer, records of accounts to be received and payments by the

customers. If all these processes are to be done under one department then the functioning cannot

be smooth and effective. This is why, the RCE limited do not hesitate in investing more amount

in separating the departments of warehouse, shipping and inventory. This is how, the revenue

cycle of the RCE limited provide many benefits to the company.

Potential internal control weakness in Sales Order Processing Procedures and Cash Receipts

Procedures

The sales department of RCE limited is responsible for receiving the unstandardised sales

order because the customers’ orders are faxed, emailed etc. to the department of sales. The clerk

of the sales converts the unstandardised into standardised sales by requesting any missing kind of

information if any. Then the creditworthiness of the customers is checked by the sales clerk by

making use of accounting department also if they have any relevant information regarding the

same. If the credit is not verified then the order is rejected. Therefore, the process of SOPP starts

after the verification of the credit. It is the responsibility of the sales clerk to record the sales

order in the system through the terminal. The weakness here is there are lot many problems in

case of absence of sales clerk. This is why, the digital copy is also distributed to the shipping as

well as warehouse department. This weakness is solved in RCE by making use of computers

which automatically records the sale in the journal of sales (Agnew, Smith and Dargusch, 2018).

The clerk is responsible for reviewing the entry and files the customer’s hard copy in the

department of sales. On the computer of the warehouse manager, the digital sales receipt is

prompted and then shipping notice and stock release also becomes accessible at the terminal of

warehouse. The same is then printed. The weakness here is that every department is depended on

the other. When there is inefficient functioning of one department then the functioning of the

5

other is automatically disturbed. The warehouse department can only access the information

when it becomes accessible by the sales department otherwise no ways to do so. By making use

of stock release copy, the items are selected and picked by the warehouse clerk then these are

sent to the shipping department along with the shipping notice and stock release. The physical

stock, shipping notice and stock release ate received by the shipping clerk from the warehouse

manager. Then these are then checked with the digital sales. If there is a match of everything

then three hard copies are printed. Two copies are of bill of lading and the other is of packing

slip. The shipping clerk then submits the shipping notice and stock release to the account

receivable clerk (Berman, 2020). The hard copy is then printed and sent to the customer through

mails. Then the records are adjusted and updated.

The weakness in the SOPP of RCE are noticed that all the processes are linked or depended on

the previous one which is why if there comes an issue in any one of the department then this

disturbs the whole process from company to consumer. Therefore, the RCE must develop a

system such that the data from one department is send to all other departments together so that if

any problem arises, there is no loss of data and the process can be continued from the same point.

The Cash Receipt Procedure (CRP) of RCE limited also has some of the weaknesses. The

general mailroom collects the payments from the customers along with the other mails, then sorts

the mail, open the payment envelops, remove the check of the customers and then reconcile the

documents. Two hard copies are made manually by the clerk and sent to the accounts receivable

department and cash receipt department. The treasurer mainly performs some functions such as

reconciling the documents, endorsing the checks, preparing the deposit slip hard copies, updates

the journal and ledger from the computer and then the copies to the bank. The remittance advice

and list are then received by accounts receivable clerk (Kolb and et.al., 2018). The weakness

here is that the actual payment is not updated by every department which can lead to

misunderstanding as well as chaos situation. This can be solved by establishing such a system in

which when the customer makes a payment then the message must be received by every

department so that in case of any fault, every department must be aware of the same. When the

hard copies are made manually there can be chances of mistakes intentionally or unintentionally

which can lead to many problems financially.

6

when it becomes accessible by the sales department otherwise no ways to do so. By making use

of stock release copy, the items are selected and picked by the warehouse clerk then these are

sent to the shipping department along with the shipping notice and stock release. The physical

stock, shipping notice and stock release ate received by the shipping clerk from the warehouse

manager. Then these are then checked with the digital sales. If there is a match of everything

then three hard copies are printed. Two copies are of bill of lading and the other is of packing

slip. The shipping clerk then submits the shipping notice and stock release to the account

receivable clerk (Berman, 2020). The hard copy is then printed and sent to the customer through

mails. Then the records are adjusted and updated.

The weakness in the SOPP of RCE are noticed that all the processes are linked or depended on

the previous one which is why if there comes an issue in any one of the department then this

disturbs the whole process from company to consumer. Therefore, the RCE must develop a

system such that the data from one department is send to all other departments together so that if

any problem arises, there is no loss of data and the process can be continued from the same point.

The Cash Receipt Procedure (CRP) of RCE limited also has some of the weaknesses. The

general mailroom collects the payments from the customers along with the other mails, then sorts

the mail, open the payment envelops, remove the check of the customers and then reconcile the

documents. Two hard copies are made manually by the clerk and sent to the accounts receivable

department and cash receipt department. The treasurer mainly performs some functions such as

reconciling the documents, endorsing the checks, preparing the deposit slip hard copies, updates

the journal and ledger from the computer and then the copies to the bank. The remittance advice

and list are then received by accounts receivable clerk (Kolb and et.al., 2018). The weakness

here is that the actual payment is not updated by every department which can lead to

misunderstanding as well as chaos situation. This can be solved by establishing such a system in

which when the customer makes a payment then the message must be received by every

department so that in case of any fault, every department must be aware of the same. When the

hard copies are made manually there can be chances of mistakes intentionally or unintentionally

which can lead to many problems financially.

6

Potential risks identified

There are many risks associated with the SOPP and CRP of RCE limited. When there is

no proper procedure to check the inventory, then RCE limited is likely to face the risks of

carrying costs, stock-outs as well as markdowns. The warehouse manger may face the risks in

picking the items when the shipping documents are printed without the information from the

report of inventory checking. This is especially faced when the products become out of stock.

The business of RCE sometimes will need to incur the carrying costs for sourcing the products.

This stock out challenges can be reduced by installing such a system which will notify the

warehouse department when the economic order of the item reaches the quantity. The checking

of the creditworthiness of the customers by the sales clerk also poses risk to the customers who

have poor credit (Abd Karim, Nawawi and Salin, 2018). The RCE limited does not keep the

accounts of the new customers so no list of them is obtained from the accounting department.

This may lead to bad debts rise. RCE limited can make use of the IT solutions for checking the

creditworthiness of the customers. This risk can be mitigated by mailing to the credit manager

regarding the accounts which need specific authorization.

The weaknesses in the CRP at RCE can also cause risk of orders which are not legitimate. RCE

company can face the risk to fulfil the orders which are not placed by the customers as any error

made in the remittance list can lead to illegitimate orders. Also, due to the weakness of CRP,

there can be risks of customer credit, cash theft and many more. There can be taking place of

fraudulent activity due to the manual records (Bell and et.al., 2017). Any error in the manual

record can result in the customer credit theft. This risk can be mitigated when the customer remit

to the bank directly and then the notification can be sent by the bank to the accounts receivable

department.

Possible Types of frauds

Many frauds can occur due to the weakness and the risks faced by CRP and SOPP of

RCE limited. The employee fraud is the major fraud which affects the operations as well as the

output of the business. When the treasurer intentionally omits any deposits and then channels

them into personal account then this will lead to major loss to the company financially. Then the

RCE company will need extra funding to meet the expenses of the operations. When the internal

7

There are many risks associated with the SOPP and CRP of RCE limited. When there is

no proper procedure to check the inventory, then RCE limited is likely to face the risks of

carrying costs, stock-outs as well as markdowns. The warehouse manger may face the risks in

picking the items when the shipping documents are printed without the information from the

report of inventory checking. This is especially faced when the products become out of stock.

The business of RCE sometimes will need to incur the carrying costs for sourcing the products.

This stock out challenges can be reduced by installing such a system which will notify the

warehouse department when the economic order of the item reaches the quantity. The checking

of the creditworthiness of the customers by the sales clerk also poses risk to the customers who

have poor credit (Abd Karim, Nawawi and Salin, 2018). The RCE limited does not keep the

accounts of the new customers so no list of them is obtained from the accounting department.

This may lead to bad debts rise. RCE limited can make use of the IT solutions for checking the

creditworthiness of the customers. This risk can be mitigated by mailing to the credit manager

regarding the accounts which need specific authorization.

The weaknesses in the CRP at RCE can also cause risk of orders which are not legitimate. RCE

company can face the risk to fulfil the orders which are not placed by the customers as any error

made in the remittance list can lead to illegitimate orders. Also, due to the weakness of CRP,

there can be risks of customer credit, cash theft and many more. There can be taking place of

fraudulent activity due to the manual records (Bell and et.al., 2017). Any error in the manual

record can result in the customer credit theft. This risk can be mitigated when the customer remit

to the bank directly and then the notification can be sent by the bank to the accounts receivable

department.

Possible Types of frauds

Many frauds can occur due to the weakness and the risks faced by CRP and SOPP of

RCE limited. The employee fraud is the major fraud which affects the operations as well as the

output of the business. When the treasurer intentionally omits any deposits and then channels

them into personal account then this will lead to major loss to the company financially. Then the

RCE company will need extra funding to meet the expenses of the operations. When the internal

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

control systems are not proper then this will maximize the chances of the employee fraud in

which the employees will manipulate the system to gain personally thereby affecting the

organisation negatively (Akbar and et.al., 2020). Most of the departments in RCE are ran by the

individuals, so clashes among them can lead to financial management fraud despite the rules and

regulations. These frauds can be managed by segregation of the duties which will help in

addressing the fraud threats, collusion, management control changes and the modifications in IT

team. The overdependence on every department must be minimized so that the management can

ensure the contribution of transaction of every department.

CONCLUSION

The report focussed on the RCE Company which is based in Queensland. The revenue cycle

of the company was highlighted to discuss the statement that the more investment which the

company makes for the functioning of the departments of shipping, warehousing and inventory

control separately is necessary. The report also discussed about the weaknesses of SOPP and

CRP along with highlighting the risks and frauds associated with the same.

8

which the employees will manipulate the system to gain personally thereby affecting the

organisation negatively (Akbar and et.al., 2020). Most of the departments in RCE are ran by the

individuals, so clashes among them can lead to financial management fraud despite the rules and

regulations. These frauds can be managed by segregation of the duties which will help in

addressing the fraud threats, collusion, management control changes and the modifications in IT

team. The overdependence on every department must be minimized so that the management can

ensure the contribution of transaction of every department.

CONCLUSION

The report focussed on the RCE Company which is based in Queensland. The revenue cycle

of the company was highlighted to discuss the statement that the more investment which the

company makes for the functioning of the departments of shipping, warehousing and inventory

control separately is necessary. The report also discussed about the weaknesses of SOPP and

CRP along with highlighting the risks and frauds associated with the same.

8

REFERENCES

Books and Journals

Abd Karim, N., Nawawi, A. and Salin, A.S.A.P., 2018. Inventory control weaknesses–a case

study of lubricant manufacturing company. Journal of Financial Crime.

Agnew, S., Smith, C. and Dargusch, P., 2018. Causal loop modelling of residential solar and

battery adoption dynamics: a case study of Queensland, Australia. Journal of cleaner

production. 172. pp.2363-2373.

Akbar, D. and et.al., 2020. Working to grow together: Horizontal collaboration for horticulture

production in Queensland.

Baader, G. and Krcmar, H., 2018. Reducing false positives in fraud detection: Combining the red

flag approach with process mining. International Journal of Accounting Information

Systems. 31. pp.1-16.

Bell, W.P. and et.al., 2017. Revitalising the wind power induced merit order effect to reduce

wholesale and retail electricity prices in Australia. Energy Economics. 67. pp.224-241.

Berman, B., 2020. Paths to Purchase: The Seven Steps of Customer Purchase Journey

Mapping. Rutgers Business Review. 5(1). pp.84-100.

Kolb, J. and et.al., 2018. Industrial application of blockchain technology–erasing the weaknesses

of vendor managed inventory.

Nababan, D. and et.al., 2020. Reception Information System and Cash ExpenditureBusiness

Rental Services. International Journal of Psychosocial Rehabilitation. 24(2).

Ritchi, H. and et.al., 2020. The influence of business process representation on performance of

different task types. Journal of Information Systems. 34(1). pp.167-194.

Online

Thakur, M., 2021. Revenue Cycle. [ONLINE]. Available through :<

https://www.wallstreetmojo.com/revenue-cycle/>

9

Books and Journals

Abd Karim, N., Nawawi, A. and Salin, A.S.A.P., 2018. Inventory control weaknesses–a case

study of lubricant manufacturing company. Journal of Financial Crime.

Agnew, S., Smith, C. and Dargusch, P., 2018. Causal loop modelling of residential solar and

battery adoption dynamics: a case study of Queensland, Australia. Journal of cleaner

production. 172. pp.2363-2373.

Akbar, D. and et.al., 2020. Working to grow together: Horizontal collaboration for horticulture

production in Queensland.

Baader, G. and Krcmar, H., 2018. Reducing false positives in fraud detection: Combining the red

flag approach with process mining. International Journal of Accounting Information

Systems. 31. pp.1-16.

Bell, W.P. and et.al., 2017. Revitalising the wind power induced merit order effect to reduce

wholesale and retail electricity prices in Australia. Energy Economics. 67. pp.224-241.

Berman, B., 2020. Paths to Purchase: The Seven Steps of Customer Purchase Journey

Mapping. Rutgers Business Review. 5(1). pp.84-100.

Kolb, J. and et.al., 2018. Industrial application of blockchain technology–erasing the weaknesses

of vendor managed inventory.

Nababan, D. and et.al., 2020. Reception Information System and Cash ExpenditureBusiness

Rental Services. International Journal of Psychosocial Rehabilitation. 24(2).

Ritchi, H. and et.al., 2020. The influence of business process representation on performance of

different task types. Journal of Information Systems. 34(1). pp.167-194.

Online

Thakur, M., 2021. Revenue Cycle. [ONLINE]. Available through :<

https://www.wallstreetmojo.com/revenue-cycle/>

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.