Strategic Management Accounting Report: Gemini plc Profit Maximization

VerifiedAdded on 2023/01/10

|11

|3655

|82

Report

AI Summary

This report provides a detailed analysis of strategic management accounting for Gemini plc. The report begins by determining the optimal production plan to maximize weekly profit, including a profit statement. It then addresses considerations for overcoming the inability to meet customer demand, evaluating the impact of overtime labor costs on profitability. A critical evaluation of the chosen strategy is provided, discussing expected increases in contribution and issues requiring resolution. The report concludes with an examination of transfer pricing methods, specifically market-based and full-cost transfer pricing, along with their respective advantages. The analysis uses financial data to assess profitability and make strategic recommendations.

STRATEGIC MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................3

a) Determine production plan that will maximise weekly profit of the Gemini plc and profit

statement showing profits that plan will be yielding...................................................................3

b) Considerations for overcoming the inability to meet quantity demanded by the customers.. 3

Critical evaluation of the strategy as to expected increase in the contribution and issues arising

that needs to be resolved..............................................................................................................5

QUESTION 3..................................................................................................................................6

a) Market Based Transfer Pricing................................................................................................6

b) Full cost transfer pricing..........................................................................................................8

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................3

a) Determine production plan that will maximise weekly profit of the Gemini plc and profit

statement showing profits that plan will be yielding...................................................................3

b) Considerations for overcoming the inability to meet quantity demanded by the customers.. 3

Critical evaluation of the strategy as to expected increase in the contribution and issues arising

that needs to be resolved..............................................................................................................5

QUESTION 3..................................................................................................................................6

a) Market Based Transfer Pricing................................................................................................6

b) Full cost transfer pricing..........................................................................................................8

REFERENCES..............................................................................................................................10

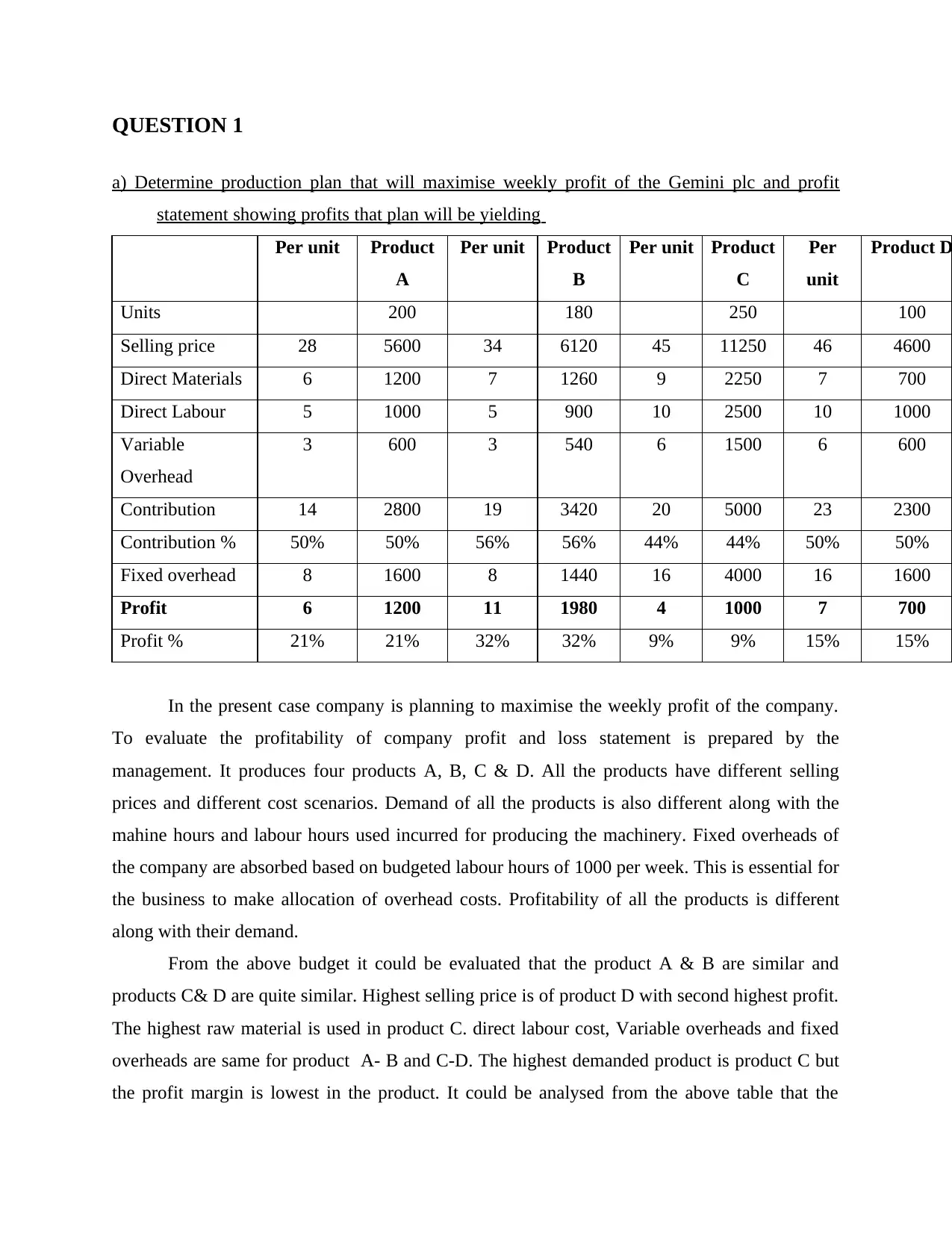

QUESTION 1

a) Determine production plan that will maximise weekly profit of the Gemini plc and profit

statement showing profits that plan will be yielding

Per unit Product

A

Per unit Product

B

Per unit Product

C

Per

unit

Product D

Units 200 180 250 100

Selling price 28 5600 34 6120 45 11250 46 4600

Direct Materials 6 1200 7 1260 9 2250 7 700

Direct Labour 5 1000 5 900 10 2500 10 1000

Variable

Overhead

3 600 3 540 6 1500 6 600

Contribution 14 2800 19 3420 20 5000 23 2300

Contribution % 50% 50% 56% 56% 44% 44% 50% 50%

Fixed overhead 8 1600 8 1440 16 4000 16 1600

Profit 6 1200 11 1980 4 1000 7 700

Profit % 21% 21% 32% 32% 9% 9% 15% 15%

In the present case company is planning to maximise the weekly profit of the company.

To evaluate the profitability of company profit and loss statement is prepared by the

management. It produces four products A, B, C & D. All the products have different selling

prices and different cost scenarios. Demand of all the products is also different along with the

mahine hours and labour hours used incurred for producing the machinery. Fixed overheads of

the company are absorbed based on budgeted labour hours of 1000 per week. This is essential for

the business to make allocation of overhead costs. Profitability of all the products is different

along with their demand.

From the above budget it could be evaluated that the product A & B are similar and

products C& D are quite similar. Highest selling price is of product D with second highest profit.

The highest raw material is used in product C. direct labour cost, Variable overheads and fixed

overheads are same for product A- B and C-D. The highest demanded product is product C but

the profit margin is lowest in the product. It could be analysed from the above table that the

a) Determine production plan that will maximise weekly profit of the Gemini plc and profit

statement showing profits that plan will be yielding

Per unit Product

A

Per unit Product

B

Per unit Product

C

Per

unit

Product D

Units 200 180 250 100

Selling price 28 5600 34 6120 45 11250 46 4600

Direct Materials 6 1200 7 1260 9 2250 7 700

Direct Labour 5 1000 5 900 10 2500 10 1000

Variable

Overhead

3 600 3 540 6 1500 6 600

Contribution 14 2800 19 3420 20 5000 23 2300

Contribution % 50% 50% 56% 56% 44% 44% 50% 50%

Fixed overhead 8 1600 8 1440 16 4000 16 1600

Profit 6 1200 11 1980 4 1000 7 700

Profit % 21% 21% 32% 32% 9% 9% 15% 15%

In the present case company is planning to maximise the weekly profit of the company.

To evaluate the profitability of company profit and loss statement is prepared by the

management. It produces four products A, B, C & D. All the products have different selling

prices and different cost scenarios. Demand of all the products is also different along with the

mahine hours and labour hours used incurred for producing the machinery. Fixed overheads of

the company are absorbed based on budgeted labour hours of 1000 per week. This is essential for

the business to make allocation of overhead costs. Profitability of all the products is different

along with their demand.

From the above budget it could be evaluated that the product A & B are similar and

products C& D are quite similar. Highest selling price is of product D with second highest profit.

The highest raw material is used in product C. direct labour cost, Variable overheads and fixed

overheads are same for product A- B and C-D. The highest demanded product is product C but

the profit margin is lowest in the product. It could be analysed from the above table that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit per unit is highest of product B with selling price of 34.

It could be evaluated from the above table that among the different plans that company is

proposing to adopt that all the above four plans are profitable. The profit statement shows that

the plan B will maximise weekly profit of the company. The profitability margin of plan B is

32% and contribution margin is 56% of the plan. Other most profitable plan is A with profit

margin is 21% and contribution margin is 50%. Least profitable plan is 9% which is plan C and

also contribution margin is 44%. Fixed overheads of all the plans are absorbed on the weekly

labour hours of 1000.

To maximise the weekly profit of Gemini plc it should adopt for product B with highest

profit margins. But the selling price of product is highest as compared with other plans.

b) Considerations for overcoming the inability to meet quantity demanded by the customers.

Profit and loss statement of the company showing all the products with increase in normal

hours

Per unit Product

A

Per unit Product

B

Per unit Product

C

Per

unit

Product

D

Units 200 180 250 100

Selling price 28 5600 34 6120 45 11250 46 4600

Direct Materials 6 1200 7 1260 9 2250 7 700

Direct Labour 5 1000 5 900 10 2500 10 1000

Variable

Overhead

4.5 900 4.5 810 9 2250 9 900

Contribution 12.5 2500 17.5 3150 17 4250 20 2000

Contribution % 45% 45% 51% 51% 38% 38% 43% 43%

Fixed overhead 12 2400 12 2160 24 6000 24 2400

Profit 0.5 100 5.5 990 -7 -1750 -4 -400

Profit % 2% 2% 16% 16% -16% -16% -9% -9%

Working Notes

Calculation of increased labour rates

Labour hour per unit 1 1 2 2

Units 200 180 250 100

Labour rate per unit 8 8 16 16

It could be evaluated from the above table that among the different plans that company is

proposing to adopt that all the above four plans are profitable. The profit statement shows that

the plan B will maximise weekly profit of the company. The profitability margin of plan B is

32% and contribution margin is 56% of the plan. Other most profitable plan is A with profit

margin is 21% and contribution margin is 50%. Least profitable plan is 9% which is plan C and

also contribution margin is 44%. Fixed overheads of all the plans are absorbed on the weekly

labour hours of 1000.

To maximise the weekly profit of Gemini plc it should adopt for product B with highest

profit margins. But the selling price of product is highest as compared with other plans.

b) Considerations for overcoming the inability to meet quantity demanded by the customers.

Profit and loss statement of the company showing all the products with increase in normal

hours

Per unit Product

A

Per unit Product

B

Per unit Product

C

Per

unit

Product

D

Units 200 180 250 100

Selling price 28 5600 34 6120 45 11250 46 4600

Direct Materials 6 1200 7 1260 9 2250 7 700

Direct Labour 5 1000 5 900 10 2500 10 1000

Variable

Overhead

4.5 900 4.5 810 9 2250 9 900

Contribution 12.5 2500 17.5 3150 17 4250 20 2000

Contribution % 45% 45% 51% 51% 38% 38% 43% 43%

Fixed overhead 12 2400 12 2160 24 6000 24 2400

Profit 0.5 100 5.5 990 -7 -1750 -4 -400

Profit % 2% 2% 16% 16% -16% -16% -9% -9%

Working Notes

Calculation of increased labour rates

Labour hour per unit 1 1 2 2

Units 200 180 250 100

Labour rate per unit 8 8 16 16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increase in labour rates

50%

12 12 24 24

Calculation of variable overheads 50%

Variable overheads 3 3 6 6

Increase 50% 4.5 4.5 9 9

As the company is unable to meet quantity demanded by the customers and for overcoming

the increase in number of hours worked using existing machinery by the working overtime.

Company is proposing to pay the overtime at premium of 50% above the normal labour rates.

According it proposes that variable overheads of the company would be also increasing in

proportion to the labour costs. To resolve the issues company has taken the step for raising the

time worked on machines. It could be analysed that on increasing the labour cost for overtime

cost the rate will increase to 12 for products A and B and 24 per unit for product C & D with

highest selling prices. The labour hours used are also highest in the product c &d. Increasing the

labour rate has declined the profit margins significantly as the available cost have raised along

with the labour of the company.

It could be evaluated that increase in labour rate due to the overtime will reduce the profit

margins of plans considerably. Due to the overtime company has to pay labour rate at 50%

which increases the labour rate and also the variable cost will be increased in proportion of

labour costs. Only plan that remains profitable after the increase in labour cost is Product B.

However the profit margins are reduced from 32% to 16%. While other products plan have gone

negative due to increase in labour cost and variable overheads. Hence if the company increases

the labour rate for overtime the profit magins will be declined significantly and also the products

C & D will become loss making as company would not be able to cover the cost at existing price

of the products.

Critical evaluation of the strategy as to expected increase in the contribution and issues arising

that needs to be resolved.

In current case Gemini plc is manufacturing four products using same machinery. Fixed

overheads are absorbed on budgeted labour hours of company and the maximum capacity of

50%

12 12 24 24

Calculation of variable overheads 50%

Variable overheads 3 3 6 6

Increase 50% 4.5 4.5 9 9

As the company is unable to meet quantity demanded by the customers and for overcoming

the increase in number of hours worked using existing machinery by the working overtime.

Company is proposing to pay the overtime at premium of 50% above the normal labour rates.

According it proposes that variable overheads of the company would be also increasing in

proportion to the labour costs. To resolve the issues company has taken the step for raising the

time worked on machines. It could be analysed that on increasing the labour cost for overtime

cost the rate will increase to 12 for products A and B and 24 per unit for product C & D with

highest selling prices. The labour hours used are also highest in the product c &d. Increasing the

labour rate has declined the profit margins significantly as the available cost have raised along

with the labour of the company.

It could be evaluated that increase in labour rate due to the overtime will reduce the profit

margins of plans considerably. Due to the overtime company has to pay labour rate at 50%

which increases the labour rate and also the variable cost will be increased in proportion of

labour costs. Only plan that remains profitable after the increase in labour cost is Product B.

However the profit margins are reduced from 32% to 16%. While other products plan have gone

negative due to increase in labour cost and variable overheads. Hence if the company increases

the labour rate for overtime the profit magins will be declined significantly and also the products

C & D will become loss making as company would not be able to cover the cost at existing price

of the products.

Critical evaluation of the strategy as to expected increase in the contribution and issues arising

that needs to be resolved.

In current case Gemini plc is manufacturing four products using same machinery. Fixed

overheads are absorbed on budgeted labour hours of company and the maximum capacity of

machine hours is 2000 per week. As per the above evaluation from profit statement it could be

stated that that production plan of product B will prove to be most beneficial for the company as

the contribution margin as well as profit margins are highest in this production plan. Also the

selling price of the products is adequate and company will be able to sell the 180 units at lower

marketing cost. In other company will be required to incur additional marketing as number of

units to be sold for covering the costs is high in Products C & D. The strategy to produce will

prove to be beneficial as the labour hours are less in product B. Machine hours for producing

single unit of Product B is only 3 hours which is lowest as compared with the other product

plans.

If the company plans to do overtime for meeting the demands of the consumer it is

proposing to pay the labour rate at 50% premium than the normal rate which is quite higher and

is making the cost high. The premium will reduce the profit levels of company to significant

level and this is a matter of concern for the management. Increase in labour cost will also raise

the variable overheads increasing the cost further. From the quantitative perspective the strategy

of company will decrease the profits of company to significant level. The company can

outsource some of the processes that make the parts of the product partially, when the employees

are made to do overtime the productivity and efficiency is not as good as in normal hours. The

output in overtime is less as compared to that in the normal working hours of the company.

Along with this managerial cost and other expenses will also rise for monitoring the activities

and operation of the business in overtime.

Company will maximise the profits by producing product B. It could produce the product at

lower cost due to which contribution margins are higher. Higher profit margins could be earned

selling less products at reasonable rate. Increasing the production of B will enable the company

to earn higher profits at lower cost. Even company has to increase the labour cost due to

overtime production it will not be suffering losses as like in other products. It will still be earning

sufficient profits of 16% with the increase in variable overheads.

In the calculation it is essential to determine the existing labour rate of producing the

products. It has to pay overtime rate at 50% more than the normal rate. In the present case issues

were found in determining the existing labour rate. However as the labour rates are based over

the hours worked it could be found that labour hours are lowest in product A and B. Issues will

also be faced in allocating the fixed costs over the labour hours as they will include the overtime

stated that that production plan of product B will prove to be most beneficial for the company as

the contribution margin as well as profit margins are highest in this production plan. Also the

selling price of the products is adequate and company will be able to sell the 180 units at lower

marketing cost. In other company will be required to incur additional marketing as number of

units to be sold for covering the costs is high in Products C & D. The strategy to produce will

prove to be beneficial as the labour hours are less in product B. Machine hours for producing

single unit of Product B is only 3 hours which is lowest as compared with the other product

plans.

If the company plans to do overtime for meeting the demands of the consumer it is

proposing to pay the labour rate at 50% premium than the normal rate which is quite higher and

is making the cost high. The premium will reduce the profit levels of company to significant

level and this is a matter of concern for the management. Increase in labour cost will also raise

the variable overheads increasing the cost further. From the quantitative perspective the strategy

of company will decrease the profits of company to significant level. The company can

outsource some of the processes that make the parts of the product partially, when the employees

are made to do overtime the productivity and efficiency is not as good as in normal hours. The

output in overtime is less as compared to that in the normal working hours of the company.

Along with this managerial cost and other expenses will also rise for monitoring the activities

and operation of the business in overtime.

Company will maximise the profits by producing product B. It could produce the product at

lower cost due to which contribution margins are higher. Higher profit margins could be earned

selling less products at reasonable rate. Increasing the production of B will enable the company

to earn higher profits at lower cost. Even company has to increase the labour cost due to

overtime production it will not be suffering losses as like in other products. It will still be earning

sufficient profits of 16% with the increase in variable overheads.

In the calculation it is essential to determine the existing labour rate of producing the

products. It has to pay overtime rate at 50% more than the normal rate. In the present case issues

were found in determining the existing labour rate. However as the labour rates are based over

the hours worked it could be found that labour hours are lowest in product A and B. Issues will

also be faced in allocating the fixed costs over the labour hours as they will include the overtime

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

worked. It has to resolve the issue related to determining proportion of variable overheads

increase due to increase in labour cost.

QUESTION 3

Transfers pricing tends to occur between the two companies that are part of same

international group and are trading with each other. Determining the exact costs of the

transactions between the related parties in company is referred as transfer pricing. It is essential

for accurate accounting and also mandatory to report by the multinationals. OECD has developed

guidelines for reporting and avoiding the transfer pricing. It is used by the business for earning

profits by reducing tax by providing goods to the customers across borders. They reduce the

overall exposure to manage the exchange controls. Over operational front, companies use

transfer pricing across the divisions or departments for meeting the working capital

requirements.

a) Market Based Transfer Pricing

The market based transfer pricing is considered as transfer pricing method available to

the companies. Supply chain in which goods are passing from 1 division to other are working

well for the company without many subsidiaries. In cases where there are many number of small

subsidiaries where each one is required to have separate accounting transfer pricing is used. It is

the process to determine how different divisions could be charged for different goods by the

companies. It is believed that MBTP where goods are priced on the basis of open market prices

is most adequate method of pricing.

General rule specifies transfer prices as sum of the two components of costs. First

component outlay cost which is incurred by division producing goods or service to transfer.

Outlay cost includes direct variable cost of product or service and other cost that incur only

because of transfer (Perčević and Hladika, 2017). Second component in transfer pricing is

opportunity costs of organisation due to transfer pricing.

Market price is the price in intermediate market of independent sellers and buyers.

Where the product has competitive market for transferred products, prices of market work well

as the transfer prices. Recording goods transferred at the market prices performance of divisions

represent economic contribution of divisions as against total profits of company. If products are

increase due to increase in labour cost.

QUESTION 3

Transfers pricing tends to occur between the two companies that are part of same

international group and are trading with each other. Determining the exact costs of the

transactions between the related parties in company is referred as transfer pricing. It is essential

for accurate accounting and also mandatory to report by the multinationals. OECD has developed

guidelines for reporting and avoiding the transfer pricing. It is used by the business for earning

profits by reducing tax by providing goods to the customers across borders. They reduce the

overall exposure to manage the exchange controls. Over operational front, companies use

transfer pricing across the divisions or departments for meeting the working capital

requirements.

a) Market Based Transfer Pricing

The market based transfer pricing is considered as transfer pricing method available to

the companies. Supply chain in which goods are passing from 1 division to other are working

well for the company without many subsidiaries. In cases where there are many number of small

subsidiaries where each one is required to have separate accounting transfer pricing is used. It is

the process to determine how different divisions could be charged for different goods by the

companies. It is believed that MBTP where goods are priced on the basis of open market prices

is most adequate method of pricing.

General rule specifies transfer prices as sum of the two components of costs. First

component outlay cost which is incurred by division producing goods or service to transfer.

Outlay cost includes direct variable cost of product or service and other cost that incur only

because of transfer (Perčević and Hladika, 2017). Second component in transfer pricing is

opportunity costs of organisation due to transfer pricing.

Market price is the price in intermediate market of independent sellers and buyers.

Where the product has competitive market for transferred products, prices of market work well

as the transfer prices. Recording goods transferred at the market prices performance of divisions

represent economic contribution of divisions as against total profits of company. If products are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not purchased from division in the company intermediate products would be purchased at current

market prices from outside market.

Advantages

Divisional profitability could be compared directly with profitability of the similar firms

operating in same business. Managers of selling and buying decisions are indifferent on trading

with outsiders or each other. Divisions could not be benefited at expenses of the other division.

Opportunity cost in the method ensures that the correct price of transfer is market price. In this

method buying division could acquire goods at market prices, so that it will not be able to pay

more for the internally transferred products. As minimum transfer prices for selling divisions are

market prices and maximum prices are also market price for buying decision. Only transfer price

is market price.

In market based transfer pricing market prices could be used for resolving conflicts

among selling and buying divisions. Market prices do not allow profits or losses in the full

efficiency of selling division. This saves the administrative cost as use of the market prices of

products are free from the arguments, dispute and biases. It is easiest form of the transfer pricing

methods when comes over determining prices to be paid between the divisions of same company

(Li and Paisey, 2019). This uses market rate which will be paid if goods are bought from open

market. It enables the subsidiaries to transfer goods and services between each other as if they

are bought from third parties. Overt other methods used in transfer pricing one of the subsidiary

have gains and other has to suffer reduction in profits.

Disadvantages

There are advantages but companies do face issues in using the transfer prcing method. It

is difficult to determine adequate market price for the product if market does not exists. There

are cases where the catalogue prices are vaguely related to the actual sale prices. On taking

marker prices there may be issues as prices changes very fast. Internal selling costs are less as

compared with products sold to the outsiders. Centres may be part of different economies and

prices prevailing in economies may be different. One may gain advantage where other may

suffer due to change in prices.

It is not easy to identify the opportunity costs associated with the transactions. Transfer

pricing rule promotes decisions that are goal congruent if rules could be implemented. It could

not be implemented effectively as measuring opportunity cost is difficult. Cost measurement

market prices from outside market.

Advantages

Divisional profitability could be compared directly with profitability of the similar firms

operating in same business. Managers of selling and buying decisions are indifferent on trading

with outsiders or each other. Divisions could not be benefited at expenses of the other division.

Opportunity cost in the method ensures that the correct price of transfer is market price. In this

method buying division could acquire goods at market prices, so that it will not be able to pay

more for the internally transferred products. As minimum transfer prices for selling divisions are

market prices and maximum prices are also market price for buying decision. Only transfer price

is market price.

In market based transfer pricing market prices could be used for resolving conflicts

among selling and buying divisions. Market prices do not allow profits or losses in the full

efficiency of selling division. This saves the administrative cost as use of the market prices of

products are free from the arguments, dispute and biases. It is easiest form of the transfer pricing

methods when comes over determining prices to be paid between the divisions of same company

(Li and Paisey, 2019). This uses market rate which will be paid if goods are bought from open

market. It enables the subsidiaries to transfer goods and services between each other as if they

are bought from third parties. Overt other methods used in transfer pricing one of the subsidiary

have gains and other has to suffer reduction in profits.

Disadvantages

There are advantages but companies do face issues in using the transfer prcing method. It

is difficult to determine adequate market price for the product if market does not exists. There

are cases where the catalogue prices are vaguely related to the actual sale prices. On taking

marker prices there may be issues as prices changes very fast. Internal selling costs are less as

compared with products sold to the outsiders. Centres may be part of different economies and

prices prevailing in economies may be different. One may gain advantage where other may

suffer due to change in prices.

It is not easy to identify the opportunity costs associated with the transactions. Transfer

pricing rule promotes decisions that are goal congruent if rules could be implemented. It could

not be implemented effectively as measuring opportunity cost is difficult. Cost measurement

issues may arise due to various reasons. Other issue associated with the market based method is

determining the uniqueness of transferred goods (Gorgieva-Trajkovska and et.al., 2019). There

are cases where the organisations face significant capacity with extremely low prices.

b) Full cost transfer pricing

Company could set transfer prices at the full cost that is sum of the variable & fixed cost

per unit. For ensuring that selling division is earning profit they could add mark up. In this

approach transfer prices are based over total cost of the product per unit that includes cost of

direct materials, cost of direct labour and the factory overheads. When the company uses full

cost transfer pricing method selling divisions could not realise the profits over goods transferred.

It could be disincentive for the selling divisions. Full cost transfer prices could provide the

perverse incentives & distort performance measure. Full cost transfer pricing method may shut

down chances for negotiation between the division about the selling over transfer pricing.

Transfer of the intermediate goods & services over the division of firm are values at free

costs. Apart from the market based approach, full cost transfer pricing is commonly used method

by the companies for internal management as well as taxation reporting purposes. One common

concern is double marginalisation. Buying division will charge high for the product as the fixed

costs are also included in the full costs of the products. In full cost pricing approach export prices

of the goods should recover all the costs that are fixed as well as variable. In addition, full cost

method considers factor of the desirable profit. The pricing method requires companies to

consider all the cost associated with the product which are variable as well as fixed costs.

Objective of the full cost method is used for covering the costs and for deriving the pre

determined percent of the profits (Li and Ji, 2017). Periodic payments for the transfer from

upstream to downstream division depends on initial capacities and current level of production.

Full cost transfer pricing refers to pricing method where transfer payments are equal to present

value of the cash outflows related with capacity assigned to downstream divisions and

subsequent ustput products to the division.

Advantage

An advantage of the advantage of the pricing method is that the method is consistent with

profit centred organisation which holds individual division accountable for own profits. Full cost

transfer pricing method could also be modified for obtaining goal congruent solutions. Full cost

transfer pricing method is considered easy and simple in calculating the prices of products to be

determining the uniqueness of transferred goods (Gorgieva-Trajkovska and et.al., 2019). There

are cases where the organisations face significant capacity with extremely low prices.

b) Full cost transfer pricing

Company could set transfer prices at the full cost that is sum of the variable & fixed cost

per unit. For ensuring that selling division is earning profit they could add mark up. In this

approach transfer prices are based over total cost of the product per unit that includes cost of

direct materials, cost of direct labour and the factory overheads. When the company uses full

cost transfer pricing method selling divisions could not realise the profits over goods transferred.

It could be disincentive for the selling divisions. Full cost transfer prices could provide the

perverse incentives & distort performance measure. Full cost transfer pricing method may shut

down chances for negotiation between the division about the selling over transfer pricing.

Transfer of the intermediate goods & services over the division of firm are values at free

costs. Apart from the market based approach, full cost transfer pricing is commonly used method

by the companies for internal management as well as taxation reporting purposes. One common

concern is double marginalisation. Buying division will charge high for the product as the fixed

costs are also included in the full costs of the products. In full cost pricing approach export prices

of the goods should recover all the costs that are fixed as well as variable. In addition, full cost

method considers factor of the desirable profit. The pricing method requires companies to

consider all the cost associated with the product which are variable as well as fixed costs.

Objective of the full cost method is used for covering the costs and for deriving the pre

determined percent of the profits (Li and Ji, 2017). Periodic payments for the transfer from

upstream to downstream division depends on initial capacities and current level of production.

Full cost transfer pricing refers to pricing method where transfer payments are equal to present

value of the cash outflows related with capacity assigned to downstream divisions and

subsequent ustput products to the division.

Advantage

An advantage of the advantage of the pricing method is that the method is consistent with

profit centred organisation which holds individual division accountable for own profits. Full cost

transfer pricing method could also be modified for obtaining goal congruent solutions. Full cost

transfer pricing method is considered easy and simple in calculating the prices of products to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transferred to other divisions. It ensures that reasonable return is earned by the exporter. Using

this method firms could avoid price competition between the companies and subsidiaries as same

pricing pattern is used by the companies. There are very less possibility of suffering losses as all

the costs associated with the products that are both variable and fixed are covered in the prices

charged. In full cost method collection of cost data could be avoided as the costs to be charged

are available on the cost sheet and other cost reports. Managers makes use of pricing method to

make effective decisions for quoting prices to other divisions. The method could be used by all

types of companies whether they are producing single or multiple products. This helps managers

to make economical decisions. Adoption of full cost pricing method helps in protecting firms

against the price wars and price competition and also provides increased flexibility at adjusting

the prices over cost changes. This is useful when companies are facing uncertainties from

market.

Disadvantages

Full cost transfer pricing method could lead to the sub optimal allocation of the resources.

Major issues with the transfer pricing is high reserves maintained by the buying divisions of their

production capacity as it faces the uncertain demands for the products but full cost charge is

applied only to the utilised capacity of the product. The advantages of the method are deceptive,

it ignores completely all aspects of the competition & the strategies adopted by the competitors.

Method do not considers demand factor and calculating the average fixed cost of the product is a

complex process for multiple product companies (Talab, Flayhh and Yassir, 2017). Method

only considers historical costs and not future cost information for allocating the costs to

products. Method is based over circular reasoning of price, quantity demanded and cost per unit.

It ignores incremental or marginal cost and uses the average cost method. Influence of the

demand is also ignored by the method. It fails to represent forces of the competition

appropriately.

this method firms could avoid price competition between the companies and subsidiaries as same

pricing pattern is used by the companies. There are very less possibility of suffering losses as all

the costs associated with the products that are both variable and fixed are covered in the prices

charged. In full cost method collection of cost data could be avoided as the costs to be charged

are available on the cost sheet and other cost reports. Managers makes use of pricing method to

make effective decisions for quoting prices to other divisions. The method could be used by all

types of companies whether they are producing single or multiple products. This helps managers

to make economical decisions. Adoption of full cost pricing method helps in protecting firms

against the price wars and price competition and also provides increased flexibility at adjusting

the prices over cost changes. This is useful when companies are facing uncertainties from

market.

Disadvantages

Full cost transfer pricing method could lead to the sub optimal allocation of the resources.

Major issues with the transfer pricing is high reserves maintained by the buying divisions of their

production capacity as it faces the uncertain demands for the products but full cost charge is

applied only to the utilised capacity of the product. The advantages of the method are deceptive,

it ignores completely all aspects of the competition & the strategies adopted by the competitors.

Method do not considers demand factor and calculating the average fixed cost of the product is a

complex process for multiple product companies (Talab, Flayhh and Yassir, 2017). Method

only considers historical costs and not future cost information for allocating the costs to

products. Method is based over circular reasoning of price, quantity demanded and cost per unit.

It ignores incremental or marginal cost and uses the average cost method. Influence of the

demand is also ignored by the method. It fails to represent forces of the competition

appropriately.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Perčević, H. and Hladika, M., 2017. Application of transfer pricing methods in related

companies in Croatia. Economic research-Ekonomska istraživanja. 30(1). pp.611-628.

Li, J. and Paisey, A., 2019. Transfer Pricing Methods. In Transfer Pricing in China (pp. 39-46).

Palgrave Macmillan, Singapore.

Gorgieva-Trajkovska, and et.al., 2019. Transfer pricing–definition and methods. Knowledge-

International Journal, Scientific Papers.

Li, J. and Ji, S., 2017. Location Specific Advantages: A Rising Disruptive Factor in Transfer

Pricing. Bulletin for International Taxation, May.

Talab, H.R., Flayhh, H.H. and Yassir, N.M., 2017. Transfer pricing and its effect on financial

reporting: A theoretical analysis of global tax in multinational companies. International

Business Management. 11(4). pp.921-928.

Manohar, H. M. and Appaiah, S., 2017. Stabilization of FIFO system and Inventory

Management. International Research Journal of Engineering and Technology. 4(6).

p.5637.

Mittal, M. and Shah, N. H. eds., 2016. Optimal inventory control and management techniques.

IGI Global.

Trihatmoko, R. A. and Purnamasari, D. I., 2019. New product pricing strategy and product

performance assessment in fast moving consumer goods.

Online

Alternatives to Discounting Your Product. 2016. [Online]. Available Through:<

http://www.theshopfiles.com/alternatives-to-discounting-your-product/>.

Walts, A., 2020. Your Essential Guide to Effective Inventory Management + 18 Techniques You

Need to Know. [Online]. Available Through:<

https://www.bigcommerce.com/blog/inventory-management/#common-inventory-

management-questions>.

Books and Journals

Perčević, H. and Hladika, M., 2017. Application of transfer pricing methods in related

companies in Croatia. Economic research-Ekonomska istraživanja. 30(1). pp.611-628.

Li, J. and Paisey, A., 2019. Transfer Pricing Methods. In Transfer Pricing in China (pp. 39-46).

Palgrave Macmillan, Singapore.

Gorgieva-Trajkovska, and et.al., 2019. Transfer pricing–definition and methods. Knowledge-

International Journal, Scientific Papers.

Li, J. and Ji, S., 2017. Location Specific Advantages: A Rising Disruptive Factor in Transfer

Pricing. Bulletin for International Taxation, May.

Talab, H.R., Flayhh, H.H. and Yassir, N.M., 2017. Transfer pricing and its effect on financial

reporting: A theoretical analysis of global tax in multinational companies. International

Business Management. 11(4). pp.921-928.

Manohar, H. M. and Appaiah, S., 2017. Stabilization of FIFO system and Inventory

Management. International Research Journal of Engineering and Technology. 4(6).

p.5637.

Mittal, M. and Shah, N. H. eds., 2016. Optimal inventory control and management techniques.

IGI Global.

Trihatmoko, R. A. and Purnamasari, D. I., 2019. New product pricing strategy and product

performance assessment in fast moving consumer goods.

Online

Alternatives to Discounting Your Product. 2016. [Online]. Available Through:<

http://www.theshopfiles.com/alternatives-to-discounting-your-product/>.

Walts, A., 2020. Your Essential Guide to Effective Inventory Management + 18 Techniques You

Need to Know. [Online]. Available Through:<

https://www.bigcommerce.com/blog/inventory-management/#common-inventory-

management-questions>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.