Strategic Management for Commonwealth Bank: Innovation through FinTech

VerifiedAdded on 2023/06/11

|19

|4022

|207

AI Summary

This report sheds light on the business growth through strategic innovation. Commonwealth Bank can reinvent the value of the customers through strategic innovation. The report evaluates the current growth strategy of Commonwealth Bank using BCG and McKinsey GE frameworks and recommends innovation opportunities using MACS framework.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: STRATEGIC MANAGEMENT

Strategic Management

Assignment 2

Student’s name:

Name of the university:

Author’s note:

Strategic Management

Assignment 2

Student’s name:

Name of the university:

Author’s note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1STRATEGIC MANAGEMENT

Executive Summary

This report sheds light on the business growth through strategic innovation. Commonwealth

Bank is the largest bank of Australia and Commonwealth Bank can reinvent the value of the

customers through strategic innovation. In Australia, the banking sector of Australia is currently

focusing on the scrutinising the current earning through legal oversight. The customers must be

able to access the banking facility all across the globe. Bankers think that threat of banking lie in

the online platform from the tech giant Google, Apple and Facebook. Economic condition is

stable in Australia and people keep their money in bank and financial instructions. Technologies

play important role in banking as the people like to use Smartphone and desktop for money

transaction. BCG matrix is used to justify the position of the products of the bank;

Commonwealth Bank can keep the stars for online banking and cash cows for the various types

of loans. GE McKinsey Framework has been given in this report to show the position and

investment opportunity in innovation. Commonwealth Bank is taking the innovation of FinTech

which aims to compete with traditional financial methods that can deliver the financial services.

MACS framework has been used to as it shows the snapshot of the business as it considers

improving the service innovation. FinTech technology is the innovation in the financial banking

sector as it is the use of financial study that can apply in the technology to develop financial

activities. FinTech is the new processes, applications and products of the business models in the

financial businesses.

Executive Summary

This report sheds light on the business growth through strategic innovation. Commonwealth

Bank is the largest bank of Australia and Commonwealth Bank can reinvent the value of the

customers through strategic innovation. In Australia, the banking sector of Australia is currently

focusing on the scrutinising the current earning through legal oversight. The customers must be

able to access the banking facility all across the globe. Bankers think that threat of banking lie in

the online platform from the tech giant Google, Apple and Facebook. Economic condition is

stable in Australia and people keep their money in bank and financial instructions. Technologies

play important role in banking as the people like to use Smartphone and desktop for money

transaction. BCG matrix is used to justify the position of the products of the bank;

Commonwealth Bank can keep the stars for online banking and cash cows for the various types

of loans. GE McKinsey Framework has been given in this report to show the position and

investment opportunity in innovation. Commonwealth Bank is taking the innovation of FinTech

which aims to compete with traditional financial methods that can deliver the financial services.

MACS framework has been used to as it shows the snapshot of the business as it considers

improving the service innovation. FinTech technology is the innovation in the financial banking

sector as it is the use of financial study that can apply in the technology to develop financial

activities. FinTech is the new processes, applications and products of the business models in the

financial businesses.

2STRATEGIC MANAGEMENT

Table of Contents

Introduction......................................................................................................................................3

Overview of the organisation: Commonwealth Bank.....................................................................3

1. Identifying the need for innovation.............................................................................................4

Threats evident from industry analysis........................................................................................4

Threats from PESTLE analysis...................................................................................................5

2. Identifying and evaluating its current growth strategy................................................................6

BCG Matrix.................................................................................................................................6

McKinsey GE framework............................................................................................................7

3. Evaluating innovation opportunity it is currently pursuing.......................................................10

MACS framework and considering its growth vehicle choice..................................................10

Recommendations..........................................................................................................................12

Conclusion.....................................................................................................................................13

Reference List................................................................................................................................14

Appendix........................................................................................................................................17

Table of Contents

Introduction......................................................................................................................................3

Overview of the organisation: Commonwealth Bank.....................................................................3

1. Identifying the need for innovation.............................................................................................4

Threats evident from industry analysis........................................................................................4

Threats from PESTLE analysis...................................................................................................5

2. Identifying and evaluating its current growth strategy................................................................6

BCG Matrix.................................................................................................................................6

McKinsey GE framework............................................................................................................7

3. Evaluating innovation opportunity it is currently pursuing.......................................................10

MACS framework and considering its growth vehicle choice..................................................10

Recommendations..........................................................................................................................12

Conclusion.....................................................................................................................................13

Reference List................................................................................................................................14

Appendix........................................................................................................................................17

3STRATEGIC MANAGEMENT

Introduction

Strategic innovation is about establishing the growth strategies, net service categories or

the business model that help the organisation to change the process of generating new values for

the customers and the organisation itself. Innovative strategies help the organisation to drive the

success without changing the underlying technologies (Palacios-Marques et al. 2015). Strategic

innovation is about the making an innovation of the strategy and the organisations can make

dramatic redefinition of the base of the customers. The organisations can reinvent the concept of

the value of the customers and the management of the organisations can also choose dramatic

redesign of the end-to-end value chain of the architecture.

In this report, Commonwealth Bank is chosen to identify the need for the innovation of

the business. At the first part of the report, threats evident from the industry and the external

environment are explained. In the second part, identification and evaluation of the current

innovation strategy are discussed using BCG and McKinsey GE frameworks. In the final section

of the report, one innovation opportunity of Commonwealth Bank which the bank is currently

pursuing is stated using the MACS framework.

Overview of the organisation: Commonwealth Bank

Commonwealth Bank is public sector bank with businesses across Asia, New Zealand,

Australia and the United States and in the UK. Headquarter of the Commonwealth Bank is

situated in Darling Harbour in Sydney, Australia. Currently, Commonwealth Bank of Australia

has its branches in more than 1100 locations. Commonwealth Bank offers the products and

services like finances and insurances, corporate banking, investment banking, global wealth

Introduction

Strategic innovation is about establishing the growth strategies, net service categories or

the business model that help the organisation to change the process of generating new values for

the customers and the organisation itself. Innovative strategies help the organisation to drive the

success without changing the underlying technologies (Palacios-Marques et al. 2015). Strategic

innovation is about the making an innovation of the strategy and the organisations can make

dramatic redefinition of the base of the customers. The organisations can reinvent the concept of

the value of the customers and the management of the organisations can also choose dramatic

redesign of the end-to-end value chain of the architecture.

In this report, Commonwealth Bank is chosen to identify the need for the innovation of

the business. At the first part of the report, threats evident from the industry and the external

environment are explained. In the second part, identification and evaluation of the current

innovation strategy are discussed using BCG and McKinsey GE frameworks. In the final section

of the report, one innovation opportunity of Commonwealth Bank which the bank is currently

pursuing is stated using the MACS framework.

Overview of the organisation: Commonwealth Bank

Commonwealth Bank is public sector bank with businesses across Asia, New Zealand,

Australia and the United States and in the UK. Headquarter of the Commonwealth Bank is

situated in Darling Harbour in Sydney, Australia. Currently, Commonwealth Bank of Australia

has its branches in more than 1100 locations. Commonwealth Bank offers the products and

services like finances and insurances, corporate banking, investment banking, global wealth

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4STRATEGIC MANAGEMENT

management, private equity, credit cards and mortgages. Commonwealth Bank employs more

than 51,800 employees and revenue of the organisation was AUD 26,005 billion in the year 2017

(Commbank.com.au 2018). Commonwealth Bank made the innovation in the banking structures

as they introduced retail banking, premium businesses services, wealth management and

executive leadership.

1. Identifying the need for innovation

Threats evident from industry analysis

In Australia, big banks can no longer depend on the market power or consistent price

growth that helps to underpin returns. The banking industry in Australia put recent efforts of

regulators to ensure the financial stability so that they can address the community concerns. In

recent time, the market expects the margin can peak in the next six months when the housing

loans growth will be slowed down. As stated by Funk (2014), new technologies like the mobile-

banking payment and real-time payment is blissful for the customers; however, it makes the

banking process complex for the banks. This disruptive innovation can lift near-time investment

before the technologies can pursue a step change to cost savings. Australian banking sector is

scrutinising the current earnings estimate as it fully capturing the downside risks stemming from

the regulatory and legal oversight. Banking sector cited the risks of the capital management as it

highlights the recent assets sakes that will free up the money for share buybacks.

Therefore, Commonwealth needs innovation in satisfying the customers and the global

peers through technological improvement. The customers must be able to access the banking

facility all across the globe. Bankers think that threat of banking lies in the online platform from

the tech giant Google, Apple and Facebook. The banking industry is trying to invest more in

management, private equity, credit cards and mortgages. Commonwealth Bank employs more

than 51,800 employees and revenue of the organisation was AUD 26,005 billion in the year 2017

(Commbank.com.au 2018). Commonwealth Bank made the innovation in the banking structures

as they introduced retail banking, premium businesses services, wealth management and

executive leadership.

1. Identifying the need for innovation

Threats evident from industry analysis

In Australia, big banks can no longer depend on the market power or consistent price

growth that helps to underpin returns. The banking industry in Australia put recent efforts of

regulators to ensure the financial stability so that they can address the community concerns. In

recent time, the market expects the margin can peak in the next six months when the housing

loans growth will be slowed down. As stated by Funk (2014), new technologies like the mobile-

banking payment and real-time payment is blissful for the customers; however, it makes the

banking process complex for the banks. This disruptive innovation can lift near-time investment

before the technologies can pursue a step change to cost savings. Australian banking sector is

scrutinising the current earnings estimate as it fully capturing the downside risks stemming from

the regulatory and legal oversight. Banking sector cited the risks of the capital management as it

highlights the recent assets sakes that will free up the money for share buybacks.

Therefore, Commonwealth needs innovation in satisfying the customers and the global

peers through technological improvement. The customers must be able to access the banking

facility all across the globe. Bankers think that threat of banking lies in the online platform from

the tech giant Google, Apple and Facebook. The banking industry is trying to invest more in

5STRATEGIC MANAGEMENT

financing technology (FinTech). Commonwealth bank can be innovative in increased the

scrutiny related to the current earnings estimates of the bank.

Threats from PESTLE analysis

The political condition of Australia is stable and financial sector is under the scrutiny of

the government. In addition, warming relationship with China and other Asian countries will be

fruitful for the banking industry. The government has not increased the tax rate and it will be

beneficial for the banking industry. The economic condition of Australia is stable also as the

GDP growth is 3% at present and the PPP was $1.24 trillion in the year 2017. The inflation rate

in Australia is 1.8% and the labour force in Australia 12.7 million (Bell 2017). Gloomy

macroeconomic outlook is risky for the business and ageing population can help to evolve the

business. In the banking sector, the threat lies in the poor GDP growth and the lower FDI in

Australia. Social factors in financing are associated with the cosmopolitan culture and the

preferences of the people are associated with the user of the mobile and online transaction.

People do not like to visit the banks now; as they want to make the transaction using Smartphone

or computers. Technological factors are investments in generation financial technology to build

the banking strong financial network. Banking industry started investing the financial technology

so that they can provide support to the customers. As stated by Booth and Whelan (2017),

banking and financing sector is a major area of cybercrime as cybersecurity is the major area of

the concern in the financial industry. In addition, financial allegations of money laundering cases

can make differences. In Australia, laws are there to wipe out the corruptions in the banking

sector. The government laws and litigations can impact on the banking sector (Mortimer et al.

2015). Lastly, in the environment; banking institutions can regulate the land and water

resources. Legal actions can be taken on failure to disclose the CSR and climate change risks.

financing technology (FinTech). Commonwealth bank can be innovative in increased the

scrutiny related to the current earnings estimates of the bank.

Threats from PESTLE analysis

The political condition of Australia is stable and financial sector is under the scrutiny of

the government. In addition, warming relationship with China and other Asian countries will be

fruitful for the banking industry. The government has not increased the tax rate and it will be

beneficial for the banking industry. The economic condition of Australia is stable also as the

GDP growth is 3% at present and the PPP was $1.24 trillion in the year 2017. The inflation rate

in Australia is 1.8% and the labour force in Australia 12.7 million (Bell 2017). Gloomy

macroeconomic outlook is risky for the business and ageing population can help to evolve the

business. In the banking sector, the threat lies in the poor GDP growth and the lower FDI in

Australia. Social factors in financing are associated with the cosmopolitan culture and the

preferences of the people are associated with the user of the mobile and online transaction.

People do not like to visit the banks now; as they want to make the transaction using Smartphone

or computers. Technological factors are investments in generation financial technology to build

the banking strong financial network. Banking industry started investing the financial technology

so that they can provide support to the customers. As stated by Booth and Whelan (2017),

banking and financing sector is a major area of cybercrime as cybersecurity is the major area of

the concern in the financial industry. In addition, financial allegations of money laundering cases

can make differences. In Australia, laws are there to wipe out the corruptions in the banking

sector. The government laws and litigations can impact on the banking sector (Mortimer et al.

2015). Lastly, in the environment; banking institutions can regulate the land and water

resources. Legal actions can be taken on failure to disclose the CSR and climate change risks.

6STRATEGIC MANAGEMENT

Therefore, the innovation is needed in the technological improvement of making the next-

generation financial technology along with the cyber-security.

2. Identifying and evaluating its current growth strategy

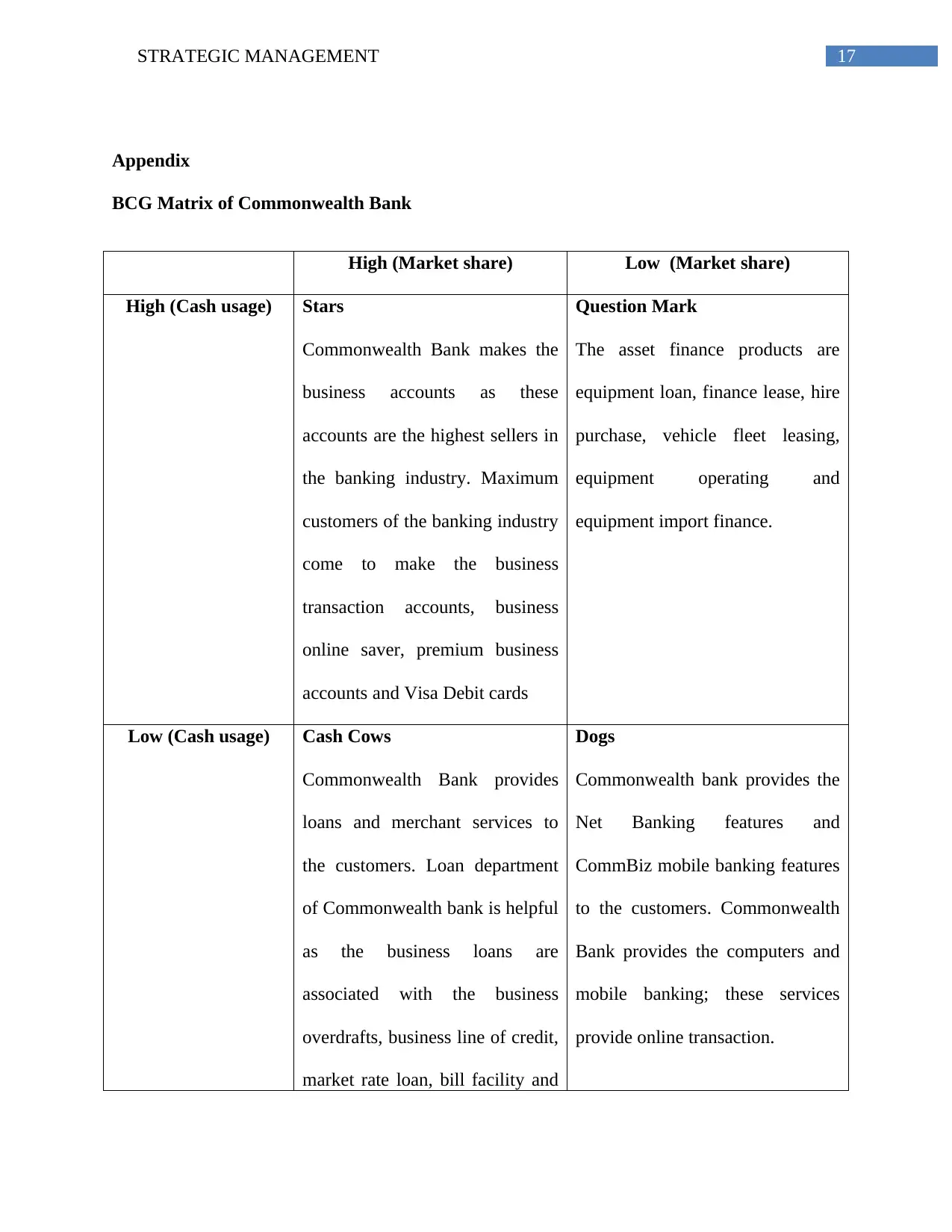

BCG Matrix

BCG framework assumes that market share improvement can help the organisation to

generate maximum cash (Torquati et al. 2018). This kind of assumption is real as the

organisation makes the experience curve.

Dogs: ‘Dogs’ is in the low market share and in low growth rate; therefore, this place does

not consume or generate a large amount of cash. As stated by Palia et al. (2014), dogs can be

treated as cash traps as the money can be tied up in the business that has just little potential.

Commonwealth bank offers various types of services and products to the customers; among this;

asset finance can be categorised as the Dogs as in this section; the bank is not the market leader.

The asset finance products are equipment loan, finance lease, hire purchase, vehicle fleet leasing,

equipment operating and equipment import finance.

Question marks: Question marks can be defined growing rapidly and this may consume

a large amount of cash. The question mark has the potential to achieve the market share and it

can become the star. The question mark may not be succeeded in becoming the leader of the

market; these products can be treated as dogs. Commonwealth bank provides the Net Banking

features and CommBiz mobile banking features to the customers. Commonwealth Bank provides

the computers and mobile banking; these services provide online transaction.

Therefore, the innovation is needed in the technological improvement of making the next-

generation financial technology along with the cyber-security.

2. Identifying and evaluating its current growth strategy

BCG Matrix

BCG framework assumes that market share improvement can help the organisation to

generate maximum cash (Torquati et al. 2018). This kind of assumption is real as the

organisation makes the experience curve.

Dogs: ‘Dogs’ is in the low market share and in low growth rate; therefore, this place does

not consume or generate a large amount of cash. As stated by Palia et al. (2014), dogs can be

treated as cash traps as the money can be tied up in the business that has just little potential.

Commonwealth bank offers various types of services and products to the customers; among this;

asset finance can be categorised as the Dogs as in this section; the bank is not the market leader.

The asset finance products are equipment loan, finance lease, hire purchase, vehicle fleet leasing,

equipment operating and equipment import finance.

Question marks: Question marks can be defined growing rapidly and this may consume

a large amount of cash. The question mark has the potential to achieve the market share and it

can become the star. The question mark may not be succeeded in becoming the leader of the

market; these products can be treated as dogs. Commonwealth bank provides the Net Banking

features and CommBiz mobile banking features to the customers. Commonwealth Bank provides

the computers and mobile banking; these services provide online transaction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STRATEGIC MANAGEMENT

Stars: Stars mark can generate a huge amount of cash as this product provides strong

relative and market share. This product helps to provide a large amount of cash as it has high

growth rate and helps to generate high market share. If star mark can maintain strong market

share for a long time; it may become the cash cow. Commonwealth Bank makes the business

accounts as these accounts are the highest sellers in the banking industry. Maximum customers

of the banking industry come to make the business transaction accounts, business online saver,

premium business accounts and Visa Debit cards (Lukkanen 2016). The customers opt to take

the business credit cards, such as low rate credit cards, corporate credit cards, interest-free days

credit cards and awards credit cards.

Cash cows: ‘Cash cows' is the leader in the market share as this product or service

provides the return on the assets as it is greater in the market growth rate. This product or service

of the company ‘return on asset' is more than the market growth rate; hence this product or

service can generate more cash. Commonwealth Bank provides loans and merchant services to

the customers. Loan department of Commonwealth bank is helpful as the business loans are

associated with the business overdrafts, business line of credit, market rate loan, bill facility and

Butter-business loans. In addition, merchant services are payment-in-store, simple merchant

plan, payments on the go and accept bill payments. These merchant services will be famous in

the future more as this has a technological link to provide financial technology services.

(Refer to Appendix 1)

McKinsey GE framework

GE framework of McKinsey is the nine-box matrix that offers a systematic approach for

the decentralised corporation to determine the place to invest the cash. There are two sides'

Stars: Stars mark can generate a huge amount of cash as this product provides strong

relative and market share. This product helps to provide a large amount of cash as it has high

growth rate and helps to generate high market share. If star mark can maintain strong market

share for a long time; it may become the cash cow. Commonwealth Bank makes the business

accounts as these accounts are the highest sellers in the banking industry. Maximum customers

of the banking industry come to make the business transaction accounts, business online saver,

premium business accounts and Visa Debit cards (Lukkanen 2016). The customers opt to take

the business credit cards, such as low rate credit cards, corporate credit cards, interest-free days

credit cards and awards credit cards.

Cash cows: ‘Cash cows' is the leader in the market share as this product or service

provides the return on the assets as it is greater in the market growth rate. This product or service

of the company ‘return on asset' is more than the market growth rate; hence this product or

service can generate more cash. Commonwealth Bank provides loans and merchant services to

the customers. Loan department of Commonwealth bank is helpful as the business loans are

associated with the business overdrafts, business line of credit, market rate loan, bill facility and

Butter-business loans. In addition, merchant services are payment-in-store, simple merchant

plan, payments on the go and accept bill payments. These merchant services will be famous in

the future more as this has a technological link to provide financial technology services.

(Refer to Appendix 1)

McKinsey GE framework

GE framework of McKinsey is the nine-box matrix that offers a systematic approach for

the decentralised corporation to determine the place to invest the cash. There are two sides'

8STRATEGIC MANAGEMENT

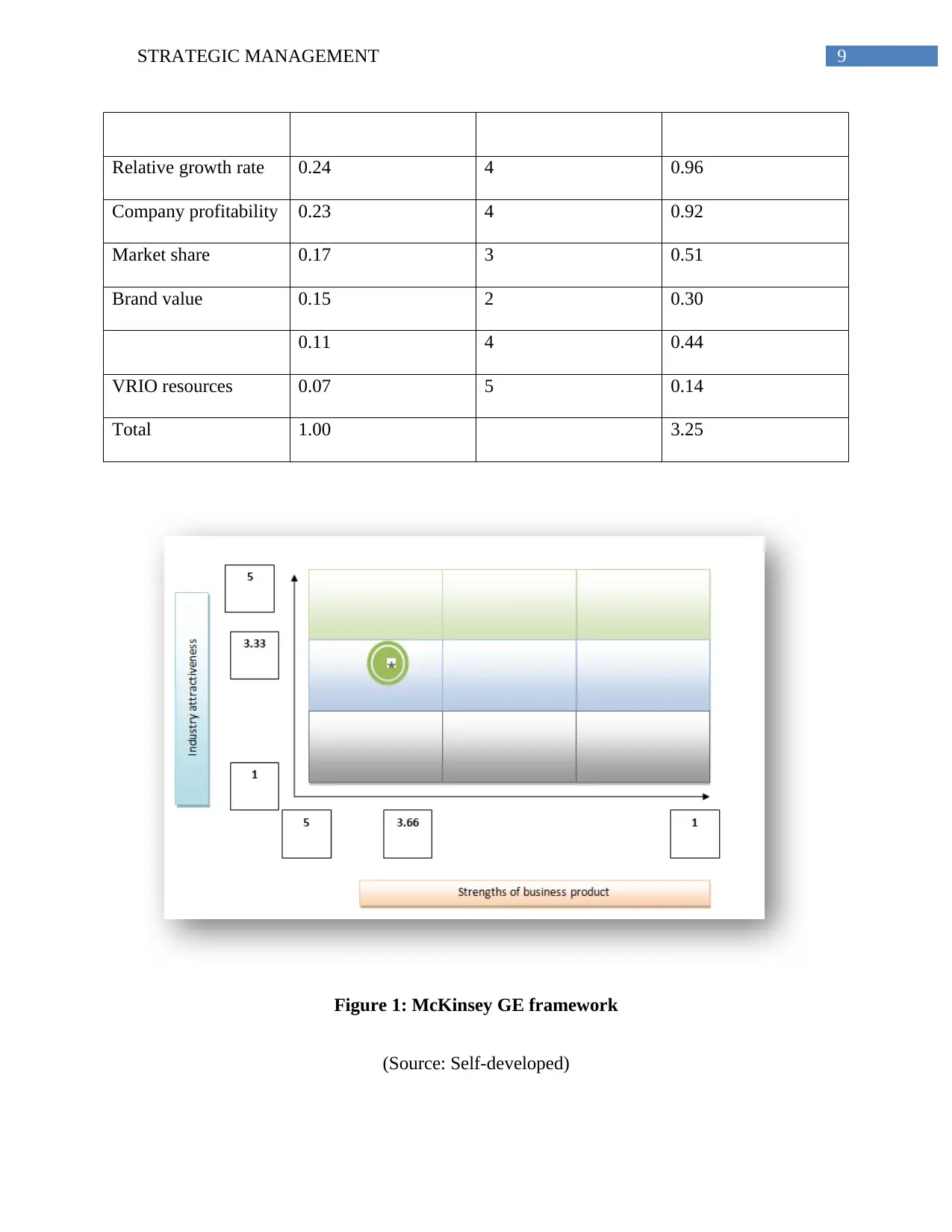

matrix; industry attractiveness and strengths of business unit or product. Industry attractiveness

shows how it is hard or easy to make a profit in business. As stated by Johnson (2016), the more

profitable the industry is more attractive it becomes. Industry attractiveness consists of the

factors to determine the competition level. Some of the factors of industry attractiveness are

long-run growth rate, industry profitability, industry size, industry structure, product lifecycle

changes, seasonality and trend of prices and availability of labour and market segmentation.

Competitive strengths of the business are the market rivalry as the businesses always try to

manage the competitive advantage. The factors of competitive strengths are total market share,

market share and growth, the profitability of the company, customer loyalty and VRIO resources

and level of product differentiation.

Industry attractiveness:

Factors Weight Rating Weighted score

Industry size 0.22 4 0.88

Industry profitability 0.25 3 0.75

Industry infrastructure 0.18 2 0.36

Trend of prices 0.16 3 0.48

Market segmentation 0.10 4 0.40

Industry growth rate 0.09 5 0.45

Total 1.00 3.32

Competitive strengths:

Factors Weight Rating Weighted score

matrix; industry attractiveness and strengths of business unit or product. Industry attractiveness

shows how it is hard or easy to make a profit in business. As stated by Johnson (2016), the more

profitable the industry is more attractive it becomes. Industry attractiveness consists of the

factors to determine the competition level. Some of the factors of industry attractiveness are

long-run growth rate, industry profitability, industry size, industry structure, product lifecycle

changes, seasonality and trend of prices and availability of labour and market segmentation.

Competitive strengths of the business are the market rivalry as the businesses always try to

manage the competitive advantage. The factors of competitive strengths are total market share,

market share and growth, the profitability of the company, customer loyalty and VRIO resources

and level of product differentiation.

Industry attractiveness:

Factors Weight Rating Weighted score

Industry size 0.22 4 0.88

Industry profitability 0.25 3 0.75

Industry infrastructure 0.18 2 0.36

Trend of prices 0.16 3 0.48

Market segmentation 0.10 4 0.40

Industry growth rate 0.09 5 0.45

Total 1.00 3.32

Competitive strengths:

Factors Weight Rating Weighted score

9STRATEGIC MANAGEMENT

Relative growth rate 0.24 4 0.96

Company profitability 0.23 4 0.92

Market share 0.17 3 0.51

Brand value 0.15 2 0.30

0.11 4 0.44

VRIO resources 0.07 5 0.14

Total 1.00 3.25

Figure 1: McKinsey GE framework

(Source: Self-developed)

Relative growth rate 0.24 4 0.96

Company profitability 0.23 4 0.92

Market share 0.17 3 0.51

Brand value 0.15 2 0.30

0.11 4 0.44

VRIO resources 0.07 5 0.14

Total 1.00 3.25

Figure 1: McKinsey GE framework

(Source: Self-developed)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10STRATEGIC MANAGEMENT

There are different investment implications that need to follow in depending on the

matrix. Commonwealth Bank has to choose selectivity/earnings more in business innovation as

this business promises to the high return. Banking sector requires a lot of money in order to

operate; however; financial technological innovation can bring the business desired market to

grow. Commonwealth bank can invest into the business on online banking product if the

business has leftover money for investment.

3. Evaluating innovation opportunity it is currently pursuing

MACS framework and considering its growth vehicle choice

MACS framework represents the recent thinking and strategy of the finance. MACS

helps to measure the business' stand-alone value within an organisation and it can measure the

existing business' fitness. The horizontal axis of MACS framework states about business's value

creation potential as the stand-alone enterprise and the vertical framework states company's

ability to extract value (Fostel and Geanakopols 2016). The horizontal dimension states the

potential to create value and Commonwealth Bank can create value through innovation. One of

the existing innovations of Commonwealth Bank is using financial technology (FinTech).

FinTech is the new technology and it is the innovation aiming to compete with traditional

financial methods that can deliver the financial services. The use of Smartphone and Computers

are the potential spheres to use the FinTech technology. The recent improvement in the investing

in crypto-currency and mobile app-based banking is some of the usages of the FinTech

technology. Commonwealth Bank is trying to take this sphere to replace another small

technology start-up to enhance the usage of financial services of the company.

There are different investment implications that need to follow in depending on the

matrix. Commonwealth Bank has to choose selectivity/earnings more in business innovation as

this business promises to the high return. Banking sector requires a lot of money in order to

operate; however; financial technological innovation can bring the business desired market to

grow. Commonwealth bank can invest into the business on online banking product if the

business has leftover money for investment.

3. Evaluating innovation opportunity it is currently pursuing

MACS framework and considering its growth vehicle choice

MACS framework represents the recent thinking and strategy of the finance. MACS

helps to measure the business' stand-alone value within an organisation and it can measure the

existing business' fitness. The horizontal axis of MACS framework states about business's value

creation potential as the stand-alone enterprise and the vertical framework states company's

ability to extract value (Fostel and Geanakopols 2016). The horizontal dimension states the

potential to create value and Commonwealth Bank can create value through innovation. One of

the existing innovations of Commonwealth Bank is using financial technology (FinTech).

FinTech is the new technology and it is the innovation aiming to compete with traditional

financial methods that can deliver the financial services. The use of Smartphone and Computers

are the potential spheres to use the FinTech technology. The recent improvement in the investing

in crypto-currency and mobile app-based banking is some of the usages of the FinTech

technology. Commonwealth Bank is trying to take this sphere to replace another small

technology start-up to enhance the usage of financial services of the company.

11STRATEGIC MANAGEMENT

Horizontal dimension shows the potential value of and the measure can be qualitative.

Commonwealth Bank can calculate the maximum potential value of FinTech and the optimal

value can depend on the industry attractiveness as it is the function of the structure-conduct-

performance model. In this horizontal dimension; the position of the business within the industry

can be shown along with sustain higher price. Commonwealth Bank can improve the chance of

attractiveness through improving the competitive positioning. On the other side, vertical axis

measures the organisation’s ability to extract the values. As stated by Sibirskaya et al. (2014), the

strength of the vertical dimension is the explicit true requirement of the corporate performance

and it can extract the value from the assets.

Figure 2: MACS framework

(Source: Self-developed)

Horizontal dimension shows the potential value of and the measure can be qualitative.

Commonwealth Bank can calculate the maximum potential value of FinTech and the optimal

value can depend on the industry attractiveness as it is the function of the structure-conduct-

performance model. In this horizontal dimension; the position of the business within the industry

can be shown along with sustain higher price. Commonwealth Bank can improve the chance of

attractiveness through improving the competitive positioning. On the other side, vertical axis

measures the organisation’s ability to extract the values. As stated by Sibirskaya et al. (2014), the

strength of the vertical dimension is the explicit true requirement of the corporate performance

and it can extract the value from the assets.

Figure 2: MACS framework

(Source: Self-developed)

12STRATEGIC MANAGEMENT

MACS matrix shows the snapshot of the business as it considers improving the service

innovation. Commonwealth Bank takes the service innovation of FinTech technology as the

bank is well equipped to enhance the value of the business through internal development.

Commonwealth Bank divests structurally to attract the business and the bank provides top

priority that lies toward the far left of the matrix. The organisation tries to develop the products

internally if the products are the natural owner. Commonwealth Bank has its business units

located in Australia and New Zealand. Subsidiaries of Commonwealth Bank are the Bankwest,

ASB Bank, Sovereign Limited and Colonial First State. The parent company may take the

strategy of envisioning the future to sell, buy or manipulate the assets that can create the new

equilibrium.

Recommendations

Commonwealth Bank Australia can start providing various types of loans to the

customers in Australia and they can advertise on the print media and in the online platforms.

Commonwealth bank can start advertising on the social media about loans; loans processes can

be done without visiting the bank physically. Therefore, the customers can apply for the loan and

the bank can develop the technology to approve the loan process via online. Most importantly,

Commonwealth Bank can start investing in the research about financial technology. The whole

process of banking in Commonwealth bank can be done through online or through mobile

banking. This innovation process can bring the issue of cybercrime. Therefore, the bank can start

the data security so that the process can be out of scamming, hacking and phishing. Data breach

is another issue of the banking sector when the bank provides the service of online transaction.

The process of the online transaction can increase the target of distributed denial of service

extortion by rivals.

MACS matrix shows the snapshot of the business as it considers improving the service

innovation. Commonwealth Bank takes the service innovation of FinTech technology as the

bank is well equipped to enhance the value of the business through internal development.

Commonwealth Bank divests structurally to attract the business and the bank provides top

priority that lies toward the far left of the matrix. The organisation tries to develop the products

internally if the products are the natural owner. Commonwealth Bank has its business units

located in Australia and New Zealand. Subsidiaries of Commonwealth Bank are the Bankwest,

ASB Bank, Sovereign Limited and Colonial First State. The parent company may take the

strategy of envisioning the future to sell, buy or manipulate the assets that can create the new

equilibrium.

Recommendations

Commonwealth Bank Australia can start providing various types of loans to the

customers in Australia and they can advertise on the print media and in the online platforms.

Commonwealth bank can start advertising on the social media about loans; loans processes can

be done without visiting the bank physically. Therefore, the customers can apply for the loan and

the bank can develop the technology to approve the loan process via online. Most importantly,

Commonwealth Bank can start investing in the research about financial technology. The whole

process of banking in Commonwealth bank can be done through online or through mobile

banking. This innovation process can bring the issue of cybercrime. Therefore, the bank can start

the data security so that the process can be out of scamming, hacking and phishing. Data breach

is another issue of the banking sector when the bank provides the service of online transaction.

The process of the online transaction can increase the target of distributed denial of service

extortion by rivals.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13STRATEGIC MANAGEMENT

Commonwealth Bank in Australia is the largest bank and it is the multinational bank with

a presence in Asian countries and in the UK. Commonwealth Bank needs innovation in the

business so that they can grow in the market to gain more customers. The bank can reach more

customers if the bank uses FinTech technology. FinTech technology is the innovation in the

financial banking sector as it is the use of a financial study that can apply the technology to

develop financial activities. FinTech is the new processes, applications and products of the

business models in the financial businesses.

Conclusion

The strategic innovation of Commonwealth Bank can be brought through collaborative

effort process across various departmental functions and teams can be aligned with the mission

of the organisation. The banking sector has the potentiality to bring strategic innovation to the

customer's groups are larger in the banking industry. Strategic innovation is the episodic reaction

to isolate the initiative and Commonwealth Bank is the senior-leader-led culture that can bring

together the multi-functional approach of the creative assets. Commonwealth Bank has the

technological threats from the larger technological giants as the large multinational IT companies

are coming up with the FinTech technologies to attract the customers. Commonwealth Bank is

taking the growth strategy to diversify the business in FinTech where the bank can provide

technical services regarding financial services.

Commonwealth Bank in Australia is the largest bank and it is the multinational bank with

a presence in Asian countries and in the UK. Commonwealth Bank needs innovation in the

business so that they can grow in the market to gain more customers. The bank can reach more

customers if the bank uses FinTech technology. FinTech technology is the innovation in the

financial banking sector as it is the use of a financial study that can apply the technology to

develop financial activities. FinTech is the new processes, applications and products of the

business models in the financial businesses.

Conclusion

The strategic innovation of Commonwealth Bank can be brought through collaborative

effort process across various departmental functions and teams can be aligned with the mission

of the organisation. The banking sector has the potentiality to bring strategic innovation to the

customer's groups are larger in the banking industry. Strategic innovation is the episodic reaction

to isolate the initiative and Commonwealth Bank is the senior-leader-led culture that can bring

together the multi-functional approach of the creative assets. Commonwealth Bank has the

technological threats from the larger technological giants as the large multinational IT companies

are coming up with the FinTech technologies to attract the customers. Commonwealth Bank is

taking the growth strategy to diversify the business in FinTech where the bank can provide

technical services regarding financial services.

14STRATEGIC MANAGEMENT

Reference List

Anderson, N., Potočnik, K. and Zhou, J., 2014. Innovation and creativity in organizations: A

state-of-the-science review, prospective commentary, and guiding framework. Journal of

Management, 40(5), pp.1297-1333.

Bell, S., 2017. Great Ideas of Central Banking: Values, Ideas and the Transformation of Central

Banking and Monetary Policy in Australia. In Government Reformed (pp. 35-54). Abingdon:

Routledge.

Booth, S. and Whelan, J., 2017. Hungry for change: the food banking industry in

Australia. British Food Journal, 116(9), pp.1392-1404.

Commonwealth Bank. 2018. Strategies of Commonwealth Bank. Available at:

https://www.commbank.com.au/content/dam/commbank/microsite/2013shareholderreview/

downloads/CBA-OurStrategy-2013. [Accessed on 29th May 2018]

Fostel, A. and Geanakoplos, J., 2016. Financial innovation, collateral, and investment. American

Economic Journal: Macroeconomics, 8(1), pp.242-84.

Funk, R.J., 2014. Making the most of where you are: Geography, networks, and innovation in

organizations. Academy of Management Journal, 57(1), pp.193-222.

Goetsch, D.L. and Davis, S.B., 2014. Quality management for organizational excellence. Upper

Saddle River, NJ: Pearson.

Reference List

Anderson, N., Potočnik, K. and Zhou, J., 2014. Innovation and creativity in organizations: A

state-of-the-science review, prospective commentary, and guiding framework. Journal of

Management, 40(5), pp.1297-1333.

Bell, S., 2017. Great Ideas of Central Banking: Values, Ideas and the Transformation of Central

Banking and Monetary Policy in Australia. In Government Reformed (pp. 35-54). Abingdon:

Routledge.

Booth, S. and Whelan, J., 2017. Hungry for change: the food banking industry in

Australia. British Food Journal, 116(9), pp.1392-1404.

Commonwealth Bank. 2018. Strategies of Commonwealth Bank. Available at:

https://www.commbank.com.au/content/dam/commbank/microsite/2013shareholderreview/

downloads/CBA-OurStrategy-2013. [Accessed on 29th May 2018]

Fostel, A. and Geanakoplos, J., 2016. Financial innovation, collateral, and investment. American

Economic Journal: Macroeconomics, 8(1), pp.242-84.

Funk, R.J., 2014. Making the most of where you are: Geography, networks, and innovation in

organizations. Academy of Management Journal, 57(1), pp.193-222.

Goetsch, D.L. and Davis, S.B., 2014. Quality management for organizational excellence. Upper

Saddle River, NJ: Pearson.

15STRATEGIC MANAGEMENT

Herrmann, N. and Herrmann-Nehdi, A., 2015. The Whole Brain Business Book: Unlocking the

Power of Whole Brain Thinking in Organizations, Teams, and Individuals. McGraw-Hill

Education.

Johnson, G., 2016. Exploring strategy: text and cases. Pearson Education.

Laeven, L., Levine, R. and Michalopoulos, S., 2015. Financial innovation and endogenous

growth. Journal of Financial Intermediation, 24(1), pp.1-24.

Laukkanen, T., 2016. Consumer adoption versus rejection decisions in seemingly similar service

innovations: The case of the Internet and mobile banking. Journal of Business Research, 69(7),

pp.2432-2439.

MACS framework and considering its growth vehicle choice (500)

Mortimer, G., Neale, L., Hasan, S.F.E. and Dunphy, B., 2015. Investigating the factors

influencing the adoption of m-banking: a cross-cultural study. International Journal of Bank

Marketing, 33(4), pp.545-570.

Palacios-Marqués, D., Merigó, J.M. and Soto-Acosta, P., 2015. Online social networks as an

enabler of innovation in organizations. Management Decision, 53(9), pp.1906-1920.

Palia, A.P., De Ryck, J. and Mak, W.K., 2014. Interactive Online Strategic Market Planning

With the Web-Based Boston Consulting Group (BCG) Matrix Graphics Package. Developments

in Business Simulation and Experiential Learning, 29, pp.23-34.

Sibirskaya, E.V., Stroeva, O.A., Khokhlova, O.A. and Oveshnikova, L.V., 2014. An analysis of

investment-innovation activity in Russia. Life Sci J, 11(7s), pp.155-158.

Herrmann, N. and Herrmann-Nehdi, A., 2015. The Whole Brain Business Book: Unlocking the

Power of Whole Brain Thinking in Organizations, Teams, and Individuals. McGraw-Hill

Education.

Johnson, G., 2016. Exploring strategy: text and cases. Pearson Education.

Laeven, L., Levine, R. and Michalopoulos, S., 2015. Financial innovation and endogenous

growth. Journal of Financial Intermediation, 24(1), pp.1-24.

Laukkanen, T., 2016. Consumer adoption versus rejection decisions in seemingly similar service

innovations: The case of the Internet and mobile banking. Journal of Business Research, 69(7),

pp.2432-2439.

MACS framework and considering its growth vehicle choice (500)

Mortimer, G., Neale, L., Hasan, S.F.E. and Dunphy, B., 2015. Investigating the factors

influencing the adoption of m-banking: a cross-cultural study. International Journal of Bank

Marketing, 33(4), pp.545-570.

Palacios-Marqués, D., Merigó, J.M. and Soto-Acosta, P., 2015. Online social networks as an

enabler of innovation in organizations. Management Decision, 53(9), pp.1906-1920.

Palia, A.P., De Ryck, J. and Mak, W.K., 2014. Interactive Online Strategic Market Planning

With the Web-Based Boston Consulting Group (BCG) Matrix Graphics Package. Developments

in Business Simulation and Experiential Learning, 29, pp.23-34.

Sibirskaya, E.V., Stroeva, O.A., Khokhlova, O.A. and Oveshnikova, L.V., 2014. An analysis of

investment-innovation activity in Russia. Life Sci J, 11(7s), pp.155-158.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16STRATEGIC MANAGEMENT

Torquati, B., Scarpa, R., Petrosillo, I., Ligonzo, M.G. and Paffarini, C., 2018. How Can

Consumer Science Help Firms Transform Their Dog (BCG Matrix) Products Into Profitable

Products?. In Case of Studies in the Traditional Food Sector (pp. 255-279).

Torquati, B., Scarpa, R., Petrosillo, I., Ligonzo, M.G. and Paffarini, C., 2018. How Can

Consumer Science Help Firms Transform Their Dog (BCG Matrix) Products Into Profitable

Products?. In Case of Studies in the Traditional Food Sector (pp. 255-279).

17STRATEGIC MANAGEMENT

Appendix

BCG Matrix of Commonwealth Bank

High (Market share) Low (Market share)

High (Cash usage) Stars

Commonwealth Bank makes the

business accounts as these

accounts are the highest sellers in

the banking industry. Maximum

customers of the banking industry

come to make the business

transaction accounts, business

online saver, premium business

accounts and Visa Debit cards

Question Mark

The asset finance products are

equipment loan, finance lease, hire

purchase, vehicle fleet leasing,

equipment operating and

equipment import finance.

Low (Cash usage) Cash Cows

Commonwealth Bank provides

loans and merchant services to

the customers. Loan department

of Commonwealth bank is helpful

as the business loans are

associated with the business

overdrafts, business line of credit,

market rate loan, bill facility and

Dogs

Commonwealth bank provides the

Net Banking features and

CommBiz mobile banking features

to the customers. Commonwealth

Bank provides the computers and

mobile banking; these services

provide online transaction.

Appendix

BCG Matrix of Commonwealth Bank

High (Market share) Low (Market share)

High (Cash usage) Stars

Commonwealth Bank makes the

business accounts as these

accounts are the highest sellers in

the banking industry. Maximum

customers of the banking industry

come to make the business

transaction accounts, business

online saver, premium business

accounts and Visa Debit cards

Question Mark

The asset finance products are

equipment loan, finance lease, hire

purchase, vehicle fleet leasing,

equipment operating and

equipment import finance.

Low (Cash usage) Cash Cows

Commonwealth Bank provides

loans and merchant services to

the customers. Loan department

of Commonwealth bank is helpful

as the business loans are

associated with the business

overdrafts, business line of credit,

market rate loan, bill facility and

Dogs

Commonwealth bank provides the

Net Banking features and

CommBiz mobile banking features

to the customers. Commonwealth

Bank provides the computers and

mobile banking; these services

provide online transaction.

18STRATEGIC MANAGEMENT

Butter-business loans.

Butter-business loans.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.