Strategy, Competition, and Financial Analysis: Nebraska Container Co.

VerifiedAdded on 2023/06/15

|15

|4145

|63

Report

AI Summary

This report evaluates the performance and position of The Nebraska Container Company based on financial and marketing factors. It presents strategic plans and recommendations for the next 5 years, focusing on asset reduction, new investments, return on equity improvements, operating expense management, and balance sheet adjustments. The report includes quantitative analysis of these areas, detailing the potential financial impacts of each recommendation. It also touches upon cash flow analysis and net present value techniques across the company's financial services, energy, packaging, and forecast products divisions, aiming to enhance the company's financial performance and market position.

Running Head: Strategy and Competition

1

Project Report: Strategy and Competition

1

Project Report: Strategy and Competition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategy and Competition

2

Contents

Introduction.......................................................................................................................3

List of recommendation....................................................................................................3

Quantitative analysis.........................................................................................................4

Financial impact of the recommendation.........................................................................6

Cash flow analysis and Net present value techniques......................................................8

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

Appendix.........................................................................................................................12

2

Contents

Introduction.......................................................................................................................3

List of recommendation....................................................................................................3

Quantitative analysis.........................................................................................................4

Financial impact of the recommendation.........................................................................6

Cash flow analysis and Net present value techniques......................................................8

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

Appendix.........................................................................................................................12

Strategy and Competition

3

Introduction:

This report has been prepared to evaluate the performance and the position of the

company, The Nebraska Container Company, on the basis of financial and marketing factor

of the company. The given case explains that the company has an uneven history and various

changes are required to be done by the company to manage the financial performance and the

stock performance in the market. In this report, strategic plans of the company have been

presented and the recommendation has been given to the company for next 5 years for

betterment of the company. Further, it also explains that the how the changes would impact

on the financial performance and the position of the company.

For preparing this report, the entire case and the last 5 years performance of the

company has been evaluated and the recommendation has been provided to the management

of the company accordingly. The company has faced few changes in last 5 years and explains

that the performance and the position of the company would also change in near future.

Further, it explains that the recommendation would assist the company to manage the

performance.

List of recommendation:

Following is the list of recommendation which must be done by the company to

manage and evaluate the performance of the company. These recommendations make it

easier for the company to achieve the goal and enhance the performance and the profitability

position of the company. It explains that the performance and the operations of the company

should be changed to manage the financial position of the company. Recommendations are as

follows:

1. Reduce the level of the assets so that the profitability position of the company on the

basis of assets has been enhanced and the maximum utilization of minimum resources

could be done (Schaltegger & Burritt, 2017).

2. Investment must be done in new projects to enhance the return level of the company.

3. Return on equity level of the company should be improved through making the

changes into the capital structure of the company and the operations of the company.

3

Introduction:

This report has been prepared to evaluate the performance and the position of the

company, The Nebraska Container Company, on the basis of financial and marketing factor

of the company. The given case explains that the company has an uneven history and various

changes are required to be done by the company to manage the financial performance and the

stock performance in the market. In this report, strategic plans of the company have been

presented and the recommendation has been given to the company for next 5 years for

betterment of the company. Further, it also explains that the how the changes would impact

on the financial performance and the position of the company.

For preparing this report, the entire case and the last 5 years performance of the

company has been evaluated and the recommendation has been provided to the management

of the company accordingly. The company has faced few changes in last 5 years and explains

that the performance and the position of the company would also change in near future.

Further, it explains that the recommendation would assist the company to manage the

performance.

List of recommendation:

Following is the list of recommendation which must be done by the company to

manage and evaluate the performance of the company. These recommendations make it

easier for the company to achieve the goal and enhance the performance and the profitability

position of the company. It explains that the performance and the operations of the company

should be changed to manage the financial position of the company. Recommendations are as

follows:

1. Reduce the level of the assets so that the profitability position of the company on the

basis of assets has been enhanced and the maximum utilization of minimum resources

could be done (Schaltegger & Burritt, 2017).

2. Investment must be done in new projects to enhance the return level of the company.

3. Return on equity level of the company should be improved through making the

changes into the capital structure of the company and the operations of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategy and Competition

4

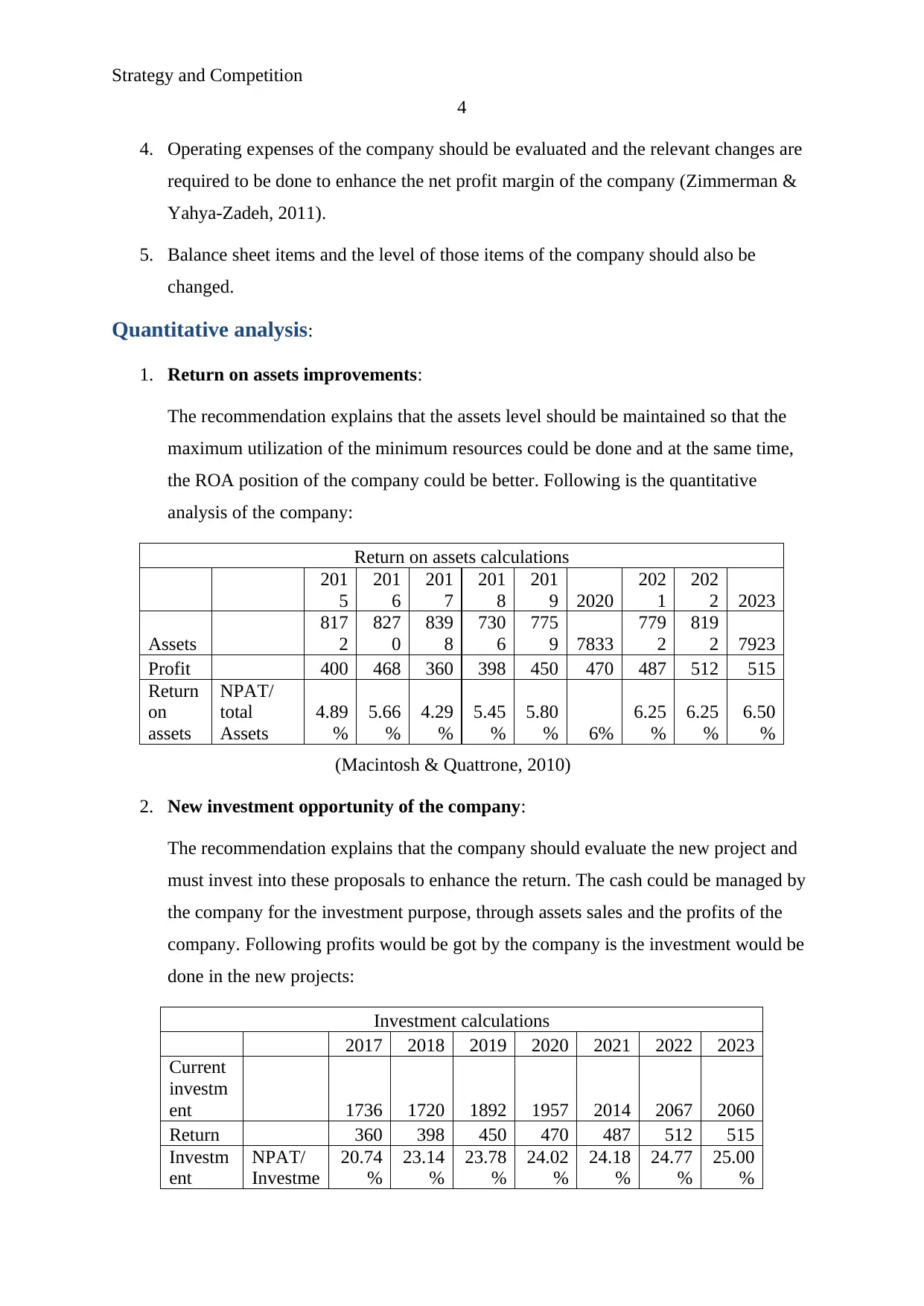

4. Operating expenses of the company should be evaluated and the relevant changes are

required to be done to enhance the net profit margin of the company (Zimmerman &

Yahya-Zadeh, 2011).

5. Balance sheet items and the level of those items of the company should also be

changed.

Quantitative analysis:

1. Return on assets improvements:

The recommendation explains that the assets level should be maintained so that the

maximum utilization of the minimum resources could be done and at the same time,

the ROA position of the company could be better. Following is the quantitative

analysis of the company:

Return on assets calculations

201

5

201

6

201

7

201

8

201

9 2020

202

1

202

2 2023

Assets

817

2

827

0

839

8

730

6

775

9 7833

779

2

819

2 7923

Profit 400 468 360 398 450 470 487 512 515

Return

on

assets

NPAT/

total

Assets

4.89

%

5.66

%

4.29

%

5.45

%

5.80

% 6%

6.25

%

6.25

%

6.50

%

(Macintosh & Quattrone, 2010)

2. New investment opportunity of the company:

The recommendation explains that the company should evaluate the new project and

must invest into these proposals to enhance the return. The cash could be managed by

the company for the investment purpose, through assets sales and the profits of the

company. Following profits would be got by the company is the investment would be

done in the new projects:

Investment calculations

2017 2018 2019 2020 2021 2022 2023

Current

investm

ent 1736 1720 1892 1957 2014 2067 2060

Return 360 398 450 470 487 512 515

Investm

ent

NPAT/

Investme

20.74

%

23.14

%

23.78

%

24.02

%

24.18

%

24.77

%

25.00

%

4

4. Operating expenses of the company should be evaluated and the relevant changes are

required to be done to enhance the net profit margin of the company (Zimmerman &

Yahya-Zadeh, 2011).

5. Balance sheet items and the level of those items of the company should also be

changed.

Quantitative analysis:

1. Return on assets improvements:

The recommendation explains that the assets level should be maintained so that the

maximum utilization of the minimum resources could be done and at the same time,

the ROA position of the company could be better. Following is the quantitative

analysis of the company:

Return on assets calculations

201

5

201

6

201

7

201

8

201

9 2020

202

1

202

2 2023

Assets

817

2

827

0

839

8

730

6

775

9 7833

779

2

819

2 7923

Profit 400 468 360 398 450 470 487 512 515

Return

on

assets

NPAT/

total

Assets

4.89

%

5.66

%

4.29

%

5.45

%

5.80

% 6%

6.25

%

6.25

%

6.50

%

(Macintosh & Quattrone, 2010)

2. New investment opportunity of the company:

The recommendation explains that the company should evaluate the new project and

must invest into these proposals to enhance the return. The cash could be managed by

the company for the investment purpose, through assets sales and the profits of the

company. Following profits would be got by the company is the investment would be

done in the new projects:

Investment calculations

2017 2018 2019 2020 2021 2022 2023

Current

investm

ent 1736 1720 1892 1957 2014 2067 2060

Return 360 398 450 470 487 512 515

Investm

ent

NPAT/

Investme

20.74

%

23.14

%

23.78

%

24.02

%

24.18

%

24.77

%

25.00

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategy and Competition

5

return nt

(Higgins, 2012)

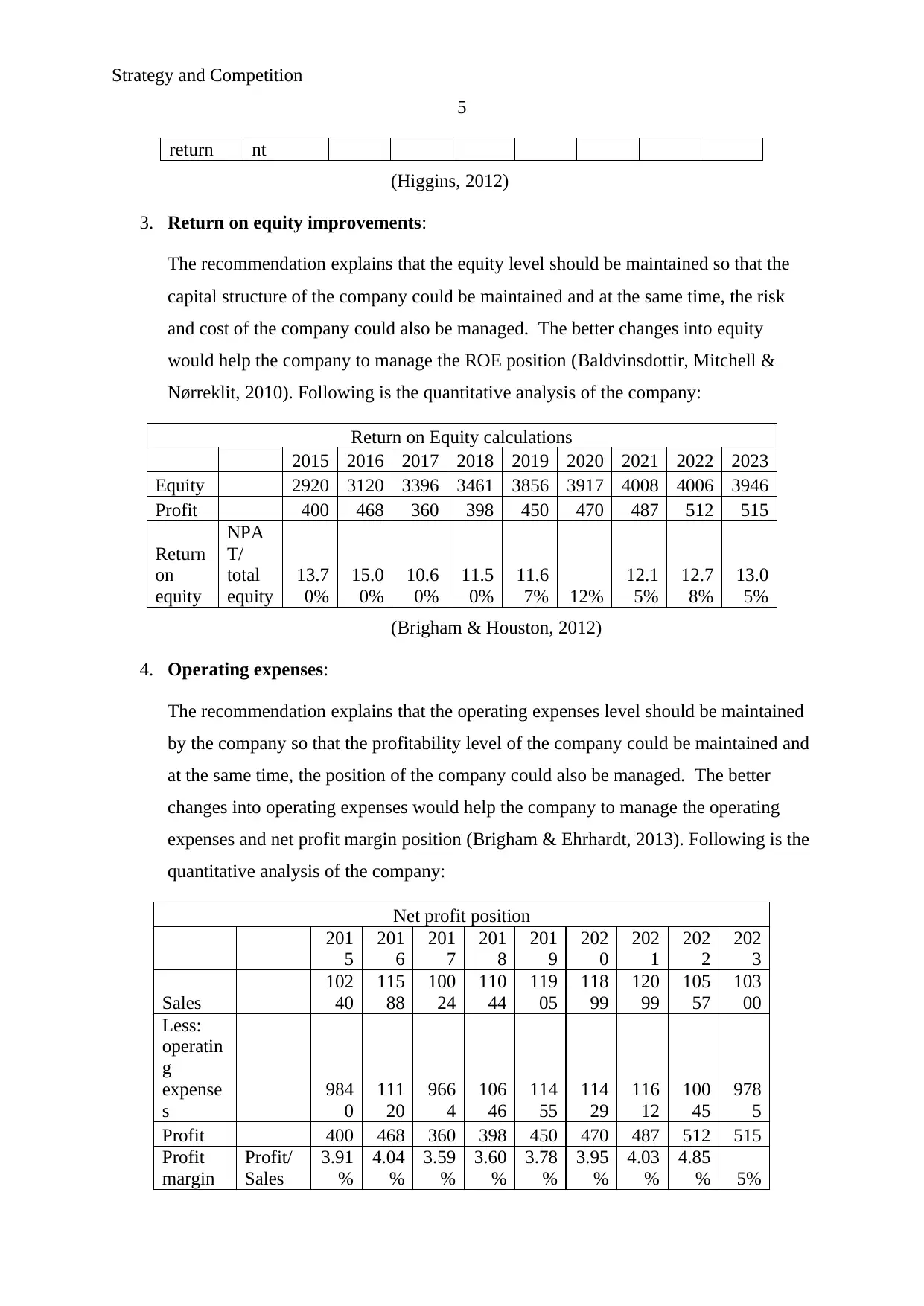

3. Return on equity improvements:

The recommendation explains that the equity level should be maintained so that the

capital structure of the company could be maintained and at the same time, the risk

and cost of the company could also be managed. The better changes into equity

would help the company to manage the ROE position (Baldvinsdottir, Mitchell &

Nørreklit, 2010). Following is the quantitative analysis of the company:

Return on Equity calculations

2015 2016 2017 2018 2019 2020 2021 2022 2023

Equity 2920 3120 3396 3461 3856 3917 4008 4006 3946

Profit 400 468 360 398 450 470 487 512 515

Return

on

equity

NPA

T/

total

equity

13.7

0%

15.0

0%

10.6

0%

11.5

0%

11.6

7% 12%

12.1

5%

12.7

8%

13.0

5%

(Brigham & Houston, 2012)

4. Operating expenses:

The recommendation explains that the operating expenses level should be maintained

by the company so that the profitability level of the company could be maintained and

at the same time, the position of the company could also be managed. The better

changes into operating expenses would help the company to manage the operating

expenses and net profit margin position (Brigham & Ehrhardt, 2013). Following is the

quantitative analysis of the company:

Net profit position

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

Sales

102

40

115

88

100

24

110

44

119

05

118

99

120

99

105

57

103

00

Less:

operatin

g

expense

s

984

0

111

20

966

4

106

46

114

55

114

29

116

12

100

45

978

5

Profit 400 468 360 398 450 470 487 512 515

Profit

margin

Profit/

Sales

3.91

%

4.04

%

3.59

%

3.60

%

3.78

%

3.95

%

4.03

%

4.85

% 5%

5

return nt

(Higgins, 2012)

3. Return on equity improvements:

The recommendation explains that the equity level should be maintained so that the

capital structure of the company could be maintained and at the same time, the risk

and cost of the company could also be managed. The better changes into equity

would help the company to manage the ROE position (Baldvinsdottir, Mitchell &

Nørreklit, 2010). Following is the quantitative analysis of the company:

Return on Equity calculations

2015 2016 2017 2018 2019 2020 2021 2022 2023

Equity 2920 3120 3396 3461 3856 3917 4008 4006 3946

Profit 400 468 360 398 450 470 487 512 515

Return

on

equity

NPA

T/

total

equity

13.7

0%

15.0

0%

10.6

0%

11.5

0%

11.6

7% 12%

12.1

5%

12.7

8%

13.0

5%

(Brigham & Houston, 2012)

4. Operating expenses:

The recommendation explains that the operating expenses level should be maintained

by the company so that the profitability level of the company could be maintained and

at the same time, the position of the company could also be managed. The better

changes into operating expenses would help the company to manage the operating

expenses and net profit margin position (Brigham & Ehrhardt, 2013). Following is the

quantitative analysis of the company:

Net profit position

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

Sales

102

40

115

88

100

24

110

44

119

05

118

99

120

99

105

57

103

00

Less:

operatin

g

expense

s

984

0

111

20

966

4

106

46

114

55

114

29

116

12

100

45

978

5

Profit 400 468 360 398 450 470 487 512 515

Profit

margin

Profit/

Sales

3.91

%

4.04

%

3.59

%

3.60

%

3.78

%

3.95

%

4.03

%

4.85

% 5%

Strategy and Competition

6

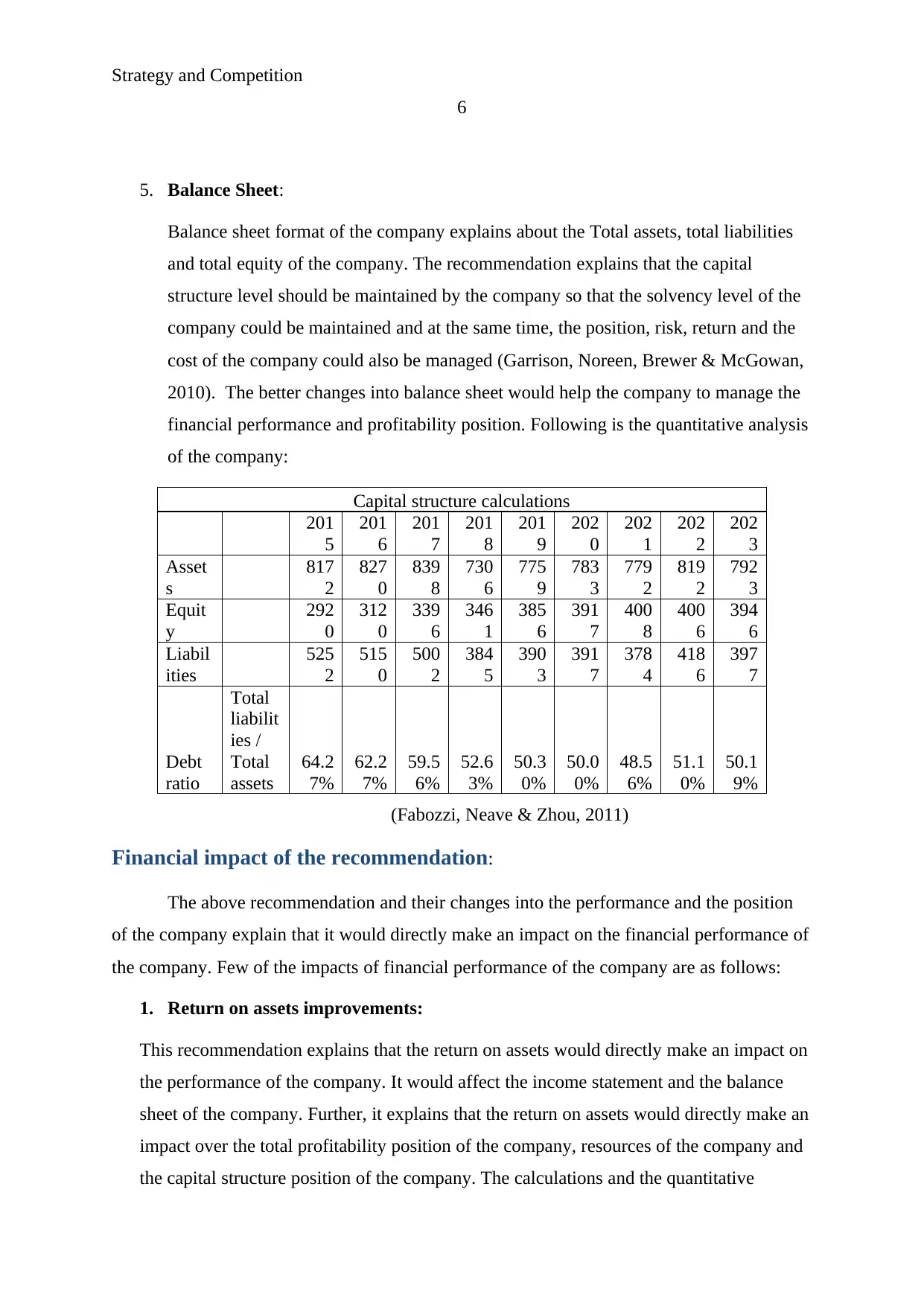

5. Balance Sheet:

Balance sheet format of the company explains about the Total assets, total liabilities

and total equity of the company. The recommendation explains that the capital

structure level should be maintained by the company so that the solvency level of the

company could be maintained and at the same time, the position, risk, return and the

cost of the company could also be managed (Garrison, Noreen, Brewer & McGowan,

2010). The better changes into balance sheet would help the company to manage the

financial performance and profitability position. Following is the quantitative analysis

of the company:

Capital structure calculations

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

Asset

s

817

2

827

0

839

8

730

6

775

9

783

3

779

2

819

2

792

3

Equit

y

292

0

312

0

339

6

346

1

385

6

391

7

400

8

400

6

394

6

Liabil

ities

525

2

515

0

500

2

384

5

390

3

391

7

378

4

418

6

397

7

Debt

ratio

Total

liabilit

ies /

Total

assets

64.2

7%

62.2

7%

59.5

6%

52.6

3%

50.3

0%

50.0

0%

48.5

6%

51.1

0%

50.1

9%

(Fabozzi, Neave & Zhou, 2011)

Financial impact of the recommendation:

The above recommendation and their changes into the performance and the position

of the company explain that it would directly make an impact on the financial performance of

the company. Few of the impacts of financial performance of the company are as follows:

1. Return on assets improvements:

This recommendation explains that the return on assets would directly make an impact on

the performance of the company. It would affect the income statement and the balance

sheet of the company. Further, it explains that the return on assets would directly make an

impact over the total profitability position of the company, resources of the company and

the capital structure position of the company. The calculations and the quantitative

6

5. Balance Sheet:

Balance sheet format of the company explains about the Total assets, total liabilities

and total equity of the company. The recommendation explains that the capital

structure level should be maintained by the company so that the solvency level of the

company could be maintained and at the same time, the position, risk, return and the

cost of the company could also be managed (Garrison, Noreen, Brewer & McGowan,

2010). The better changes into balance sheet would help the company to manage the

financial performance and profitability position. Following is the quantitative analysis

of the company:

Capital structure calculations

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

Asset

s

817

2

827

0

839

8

730

6

775

9

783

3

779

2

819

2

792

3

Equit

y

292

0

312

0

339

6

346

1

385

6

391

7

400

8

400

6

394

6

Liabil

ities

525

2

515

0

500

2

384

5

390

3

391

7

378

4

418

6

397

7

Debt

ratio

Total

liabilit

ies /

Total

assets

64.2

7%

62.2

7%

59.5

6%

52.6

3%

50.3

0%

50.0

0%

48.5

6%

51.1

0%

50.1

9%

(Fabozzi, Neave & Zhou, 2011)

Financial impact of the recommendation:

The above recommendation and their changes into the performance and the position

of the company explain that it would directly make an impact on the financial performance of

the company. Few of the impacts of financial performance of the company are as follows:

1. Return on assets improvements:

This recommendation explains that the return on assets would directly make an impact on

the performance of the company. It would affect the income statement and the balance

sheet of the company. Further, it explains that the return on assets would directly make an

impact over the total profitability position of the company, resources of the company and

the capital structure position of the company. The calculations and the quantitative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategy and Competition

7

calculations explain about the better performance of the company is next 5 years. It

further explains that if the company would follow the given recommendation than the

position and the performance of the company would be better (Hilton & Platt, 2013).

2. New investment opportunity of the company:

This recommendation explains that the new investment opportunity of the company

would directly make an impact on the return, performance of the company. It would

affect the income statement and the balance sheet and the cash flow statement of the

company (Khamees, Al-Fayoumi & Al-Thuneibat, 2010). Further, it explains that the

new investment would directly make an impact over the total profitability position

and total cash flow of the company, resources of the company and the capital

structure position of the company. The calculations and the quantitative calculations

explain about the better performance of the company is next 5 years (Ward, 2012). It

further explains that if the company would follow the given recommendation than the

position and the performance of the company would be better.

3. Return on equity improvements:

This recommendation explains that the return on equity would directly make an

impact on the performance of the company. It would affect the income statement and

the balance sheet of the company (Baker, Dutta & Saadi, 2010). Further, it explains

that the return on equity would directly make an impact over the total profitability

position of the company, resources of the company and the capital structure position

of the company. The calculations and the quantitative calculations explain about the

better performance of the company is next 5 years. It further explains that if the

company would follow the given recommendation than the position and the

performance of the company would be better (Singh, Jain & Yadav, 2012).

4. Operating expenses:

Further, this recommendation explains that the operating expenses would directly

make an impact on the profitability position and the performance of the company. It

would affect the income statement firstly and after it, the balance sheet of the

company and the cash flow statement would also be affected (Jagannathan, Matsa,

Meier & Tarhan, 2017). Further, it explains that the operating expenses would directly

make an impact over the total profitability position of the company, resources of the

7

calculations explain about the better performance of the company is next 5 years. It

further explains that if the company would follow the given recommendation than the

position and the performance of the company would be better (Hilton & Platt, 2013).

2. New investment opportunity of the company:

This recommendation explains that the new investment opportunity of the company

would directly make an impact on the return, performance of the company. It would

affect the income statement and the balance sheet and the cash flow statement of the

company (Khamees, Al-Fayoumi & Al-Thuneibat, 2010). Further, it explains that the

new investment would directly make an impact over the total profitability position

and total cash flow of the company, resources of the company and the capital

structure position of the company. The calculations and the quantitative calculations

explain about the better performance of the company is next 5 years (Ward, 2012). It

further explains that if the company would follow the given recommendation than the

position and the performance of the company would be better.

3. Return on equity improvements:

This recommendation explains that the return on equity would directly make an

impact on the performance of the company. It would affect the income statement and

the balance sheet of the company (Baker, Dutta & Saadi, 2010). Further, it explains

that the return on equity would directly make an impact over the total profitability

position of the company, resources of the company and the capital structure position

of the company. The calculations and the quantitative calculations explain about the

better performance of the company is next 5 years. It further explains that if the

company would follow the given recommendation than the position and the

performance of the company would be better (Singh, Jain & Yadav, 2012).

4. Operating expenses:

Further, this recommendation explains that the operating expenses would directly

make an impact on the profitability position and the performance of the company. It

would affect the income statement firstly and after it, the balance sheet of the

company and the cash flow statement would also be affected (Jagannathan, Matsa,

Meier & Tarhan, 2017). Further, it explains that the operating expenses would directly

make an impact over the total profitability position of the company, resources of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategy and Competition

8

company and the profitability position of the company (Lukka & Modell, 2010). The

calculations and the quantitative calculations explain about the better performance of

the company is next 5 years. It further explains that if the company would follow the

given recommendation than the position and the performance of the company would

be better.

5. Balance Sheet

Lastly, the recommendation about the balance sheet of the company explains that the

total assets, total liabilities and total equity would directly make an impact on the

performance and the financial position of the company (Hornstein & Zhao, 2011). It

would affect the balance sheet of the company and due to it; the income statement and

cash flow statement of the company would also be affected. Further, it explains that

the balance sheet would directly make an impact over the total debt position, capital

structure position of the company, resources of the company etc of the company. The

calculations and the quantitative calculations explain about the better performance of

the company is next 5 years (Parker, 2012). It further explains that if the company

would follow the given recommendation than the position and the performance of the

company would be better.

Cash flow analysis and Net present value techniques:

Further, the study has been done on the four divisions of the company which are

financial services outlook, energy and packaging and forecast products. The study has been

conducted on all the four segments to evaluate the cash flow analysis of all the projects and it

has been evaluated that the cash flow of all the four projects is different to each other. The

evaluation on the financial service outlook has been done firstly and it has been found that the

cash outflow and the cash inflow of the project would be different in each year and it would

explains the company about the total profit of the company which could be earn by the

company in current financial year (Renz & Herman, 2016). Further, it explains about the total

performance and the total position of the company. The net profit valuation of the company

explains about the total profit of $ 62,40,87,014.85 in 8 years.

Further, the calculations of energy sector has been evaluated and it has been found

that the cash outflow and the cash inflow of the project would be different in each year and

the returns of the project also varies in each year. Further, it would explain the company

8

company and the profitability position of the company (Lukka & Modell, 2010). The

calculations and the quantitative calculations explain about the better performance of

the company is next 5 years. It further explains that if the company would follow the

given recommendation than the position and the performance of the company would

be better.

5. Balance Sheet

Lastly, the recommendation about the balance sheet of the company explains that the

total assets, total liabilities and total equity would directly make an impact on the

performance and the financial position of the company (Hornstein & Zhao, 2011). It

would affect the balance sheet of the company and due to it; the income statement and

cash flow statement of the company would also be affected. Further, it explains that

the balance sheet would directly make an impact over the total debt position, capital

structure position of the company, resources of the company etc of the company. The

calculations and the quantitative calculations explain about the better performance of

the company is next 5 years (Parker, 2012). It further explains that if the company

would follow the given recommendation than the position and the performance of the

company would be better.

Cash flow analysis and Net present value techniques:

Further, the study has been done on the four divisions of the company which are

financial services outlook, energy and packaging and forecast products. The study has been

conducted on all the four segments to evaluate the cash flow analysis of all the projects and it

has been evaluated that the cash flow of all the four projects is different to each other. The

evaluation on the financial service outlook has been done firstly and it has been found that the

cash outflow and the cash inflow of the project would be different in each year and it would

explains the company about the total profit of the company which could be earn by the

company in current financial year (Renz & Herman, 2016). Further, it explains about the total

performance and the total position of the company. The net profit valuation of the company

explains about the total profit of $ 62,40,87,014.85 in 8 years.

Further, the calculations of energy sector has been evaluated and it has been found

that the cash outflow and the cash inflow of the project would be different in each year and

the returns of the project also varies in each year. Further, it would explain the company

Strategy and Competition

9

about the total profit of the company which could be earn by the company after 12 years.

Further, it explains that this project is not more profitable for the company. The net profit

valuation of the company explains about the loss would be faced by the company in this case

(Bierman & Smidt, 2012).

In addition, the calculations of packaging sector has been evaluated and it has been

found that the cash outflow and the cash inflow of the project would totally be dependable on

the total sales and the operations of the company. Further, it would explain the company

about the total profit of the company which could be earn by the company after 10 years.

Further, it explains that this project average profitable for the company. The net profit

valuation of the company explains about the moderate position of the investment and

explains about the average performance of the company (Bennouna, Meredith & Marchant,

2010).

In addition, the calculations of forest product outlook sector has been evaluated and it

has been found that the cash outflow and the cash inflow of the project would totally be

dependable on the total products and their position in the market. Further, it would explain

the company about the total profit of the company which could be earn by the company after

10 years (Gervais, Heaton & Odean, 2011). Further, it explains that this project is quite

profitable for the company. The net profit valuation of the company explains about the good

position of the investment and explains about the better performance of the company in the

market. More, it depicts that the company would offer huge return to the company.

Recommendation and conclusion:

The above study explains about the financial position and the performance of the

company. This report has explained about the performance and the position of the company,

The Nebraska Container Company, on the basis of financial and marketing factor of the

company. The study explains that the company has an uneven history and thus few

recommendations have been given to the company to manage the financial performance and

the stock performance in the market. According to this report, strategic plans of the company

for next 5 years explain that the company would enjoy the betterment. Further, it also

explains that the recommendation would impact on the financial performance and the

position of the company.

9

about the total profit of the company which could be earn by the company after 12 years.

Further, it explains that this project is not more profitable for the company. The net profit

valuation of the company explains about the loss would be faced by the company in this case

(Bierman & Smidt, 2012).

In addition, the calculations of packaging sector has been evaluated and it has been

found that the cash outflow and the cash inflow of the project would totally be dependable on

the total sales and the operations of the company. Further, it would explain the company

about the total profit of the company which could be earn by the company after 10 years.

Further, it explains that this project average profitable for the company. The net profit

valuation of the company explains about the moderate position of the investment and

explains about the average performance of the company (Bennouna, Meredith & Marchant,

2010).

In addition, the calculations of forest product outlook sector has been evaluated and it

has been found that the cash outflow and the cash inflow of the project would totally be

dependable on the total products and their position in the market. Further, it would explain

the company about the total profit of the company which could be earn by the company after

10 years (Gervais, Heaton & Odean, 2011). Further, it explains that this project is quite

profitable for the company. The net profit valuation of the company explains about the good

position of the investment and explains about the better performance of the company in the

market. More, it depicts that the company would offer huge return to the company.

Recommendation and conclusion:

The above study explains about the financial position and the performance of the

company. This report has explained about the performance and the position of the company,

The Nebraska Container Company, on the basis of financial and marketing factor of the

company. The study explains that the company has an uneven history and thus few

recommendations have been given to the company to manage the financial performance and

the stock performance in the market. According to this report, strategic plans of the company

for next 5 years explain that the company would enjoy the betterment. Further, it also

explains that the recommendation would impact on the financial performance and the

position of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategy and Competition

10

The case explains that the financial performance and the position of the company

would be better if all the given recommendations would be followed by the company. Further

it explains that if the company would follow the given recommendation than the position and

the performance of the company would be better.

10

The case explains that the financial performance and the position of the company

would be better if all the given recommendations would be followed by the company. Further

it explains that if the company would follow the given recommendation than the position and

the performance of the company would be better.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategy and Competition

11

References:

Baker, H. K., Dutta, S., & Saadi, S. (2010). Management views on real options in capital

budgeting.

Baldvinsdottir, G., Mitchell, F., & Nørreklit, H. (2010). Issues in the relationship between

theory and practice in management accounting. Management Accounting

Research, 21(2), 79-82.

Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision

making: evidence from Canada. Management decision, 48(2), 225-247.

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice.

Cengage Learning.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. Cengage

Learning.

Fabozzi, F. J., Neave, E. H., & Zhou, G. (2011). Financial economics. Wiley Global

Education.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Gervais, S., Heaton, J. B., & Odean, T. (2011). Overconfidence, compensation contracts, and

capital budgeting. The Journal of Finance, 66(5), 1735-1777.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Hornstein, A. S., & Zhao, M. (2011). Corporate capital budgeting decisions and information

sharing. Journal of Economics & Management Strategy, 20(4), 1135-1170.

Jagannathan, R., Matsa, D. A., Meier, I., & Tarhan, V. (2017). Search in. CFA Digest, 47(4).

11

References:

Baker, H. K., Dutta, S., & Saadi, S. (2010). Management views on real options in capital

budgeting.

Baldvinsdottir, G., Mitchell, F., & Nørreklit, H. (2010). Issues in the relationship between

theory and practice in management accounting. Management Accounting

Research, 21(2), 79-82.

Bennouna, K., Meredith, G. G., & Marchant, T. (2010). Improved capital budgeting decision

making: evidence from Canada. Management decision, 48(2), 225-247.

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice.

Cengage Learning.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. Cengage

Learning.

Fabozzi, F. J., Neave, E. H., & Zhou, G. (2011). Financial economics. Wiley Global

Education.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Gervais, S., Heaton, J. B., & Odean, T. (2011). Overconfidence, compensation contracts, and

capital budgeting. The Journal of Finance, 66(5), 1735-1777.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Hornstein, A. S., & Zhao, M. (2011). Corporate capital budgeting decisions and information

sharing. Journal of Economics & Management Strategy, 20(4), 1135-1170.

Jagannathan, R., Matsa, D. A., Meier, I., & Tarhan, V. (2017). Search in. CFA Digest, 47(4).

Strategy and Competition

12

Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices

in the Jordanian industrial corporations. International journal of commerce and

management, 20(1), 49-63.

Lukka, K., & Modell, S. (2010). Validation in interpretive management accounting

research. Accounting, organizations and society, 35(4), 462-477.

Macintosh, N. B., & Quattrone, P. (2010). Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Parker, L. D. (2012). Qualitative management accounting research: Assessing deliverables

and relevance. Critical perspectives on accounting, 23(1), 54-70.

Renz, D. O., & Herman, R. D. (Eds.). (2016). The Jossey-Bass handbook of nonprofit

leadership and management. John Wiley & Sons.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Singh, S., Jain, P. K., & Yadav, S. S. (2012). Capital budgeting decisions: evidence from

India. Journal of Advances in Management Research, 9(1), 96-112.

Ward, K. (2012). Strategic management accounting. Routledge.

Zimmerman, J. L., & Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

12

Khamees, B. A., Al-Fayoumi, N., & Al-Thuneibat, A. A. (2010). Capital budgeting practices

in the Jordanian industrial corporations. International journal of commerce and

management, 20(1), 49-63.

Lukka, K., & Modell, S. (2010). Validation in interpretive management accounting

research. Accounting, organizations and society, 35(4), 462-477.

Macintosh, N. B., & Quattrone, P. (2010). Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Parker, L. D. (2012). Qualitative management accounting research: Assessing deliverables

and relevance. Critical perspectives on accounting, 23(1), 54-70.

Renz, D. O., & Herman, R. D. (Eds.). (2016). The Jossey-Bass handbook of nonprofit

leadership and management. John Wiley & Sons.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Singh, S., Jain, P. K., & Yadav, S. S. (2012). Capital budgeting decisions: evidence from

India. Journal of Advances in Management Research, 9(1), 96-112.

Ward, K. (2012). Strategic management accounting. Routledge.

Zimmerman, J. L., & Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.