Holmes Institute HC1010 Accounting for Business: Analysis

VerifiedAdded on 2023/03/23

|8

|1585

|20

Homework Assignment

AI Summary

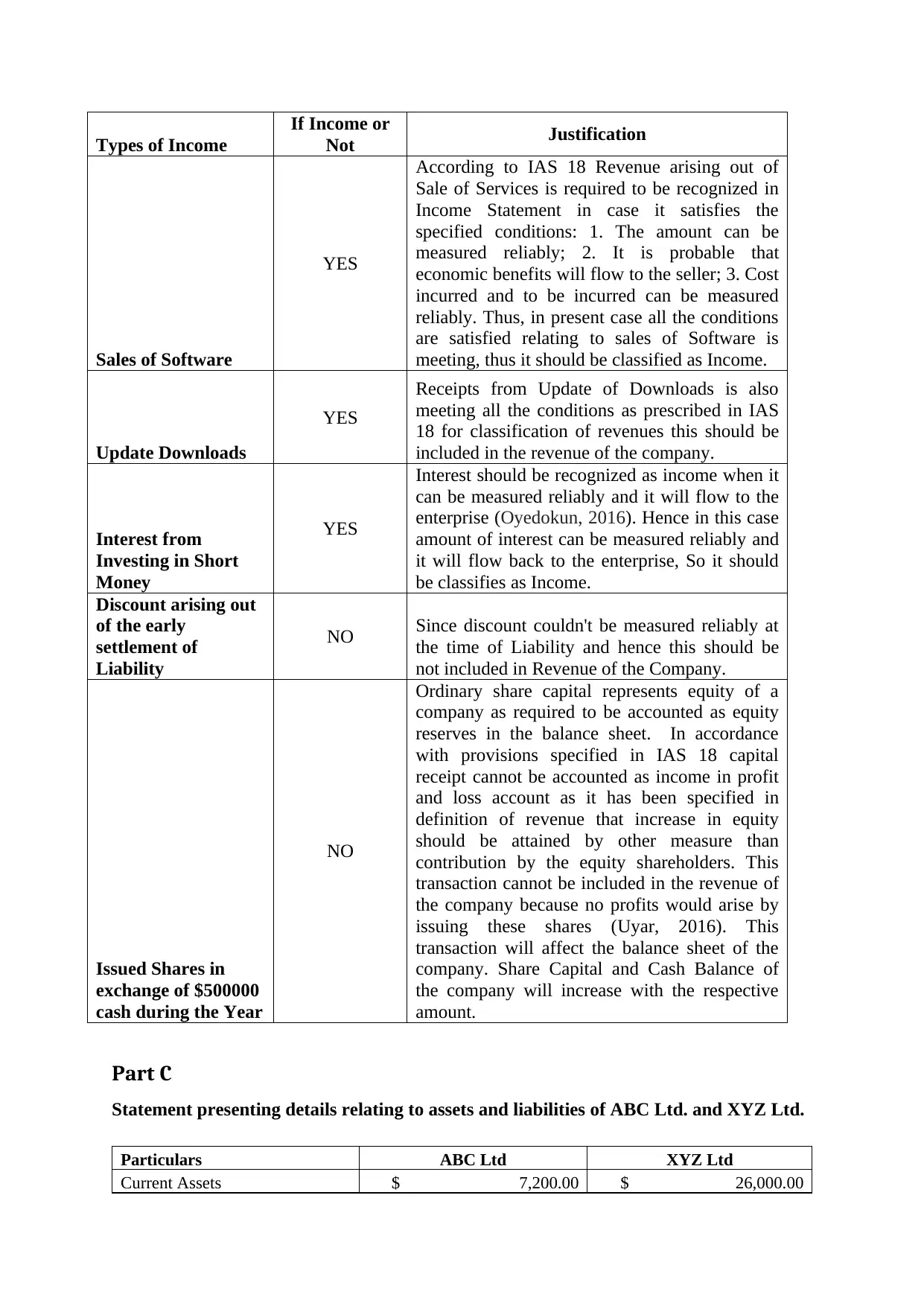

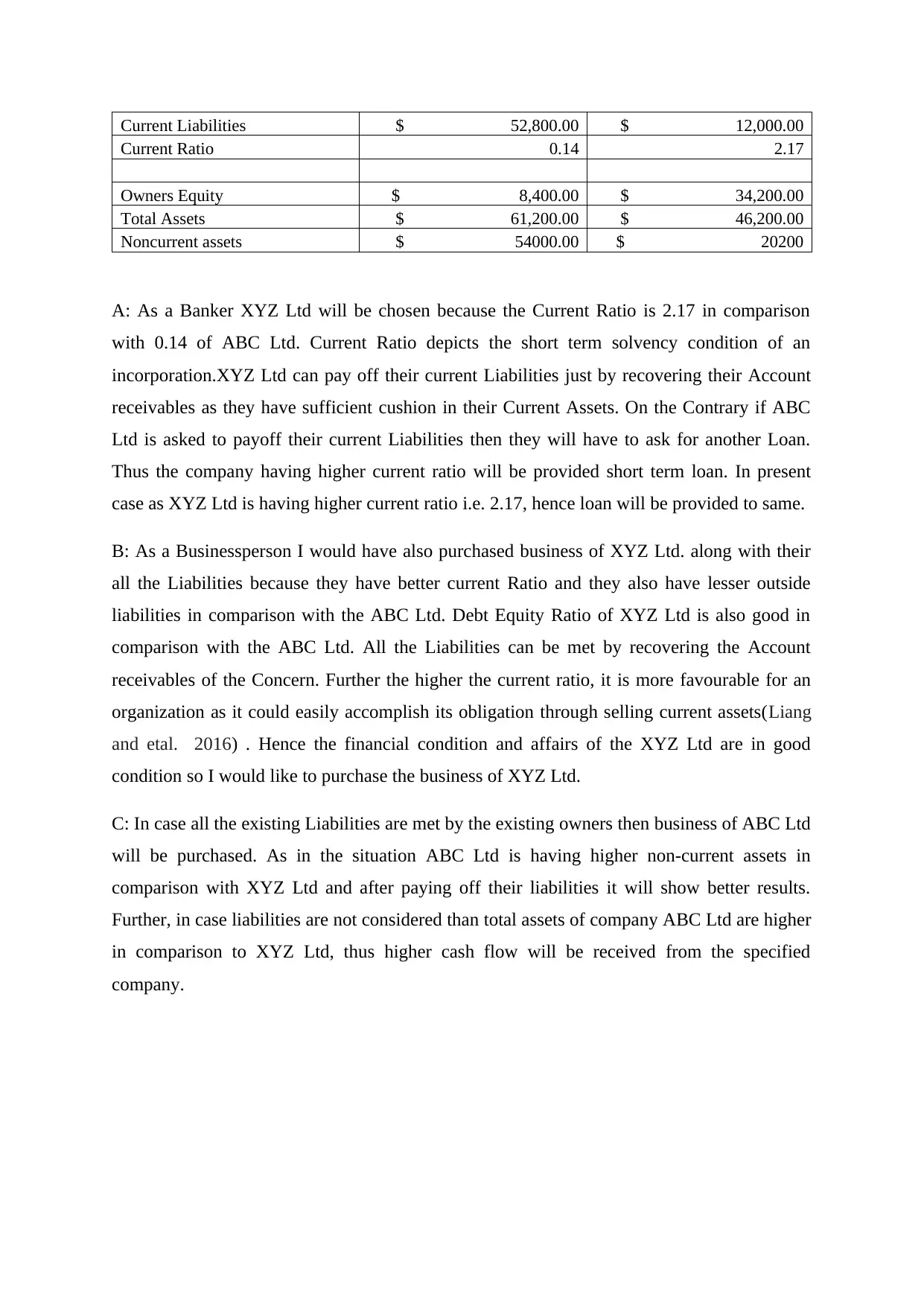

This assignment provides a comprehensive analysis of financial statements, focusing on key elements and ratio analysis. It includes calculations of current and quick ratios, accounts receivable turnover, and inventory turnover. The analysis interprets short-term solvency, revenue recognition according to IAS 18, and assesses the financial positions of two companies, ABC Ltd. and XYZ Ltd., for loan and business purchase decisions. The assignment concludes with recommendations based on the calculated ratios and asset evaluations, providing insights into financial health and investment potential. Desklib offers a wide range of past papers and solved assignments to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.