Accounting and Finance Report: Investment, Budgeting, and Rules

VerifiedAdded on 2020/04/13

|11

|3928

|49

Report

AI Summary

This report analyzes two scenarios related to accounting and finance. Scenario I focuses on Dangerous Dessert Company (DDC), evaluating an investment proposal for direct vanilla ice cream delivery using Net Present Value (NPV) and Payback Period methods. The report calculates cash inflows and outflows, determines the NPV, and assesses the project's viability, concluding that the project should be rejected. It also includes a budget analysis, calculating contribution per kilogram for different ice cream ranges (Single, Double, and Triple Whammy), determining the profit-maximizing sales mix, and performing a limiting factor analysis. Scenario II addresses the financial accounts of Bespoke Golf Club, discussing accounting rules and the proper format for financial reporting. The report provides detailed calculations, explanations of financial concepts, and recommendations based on the analysis. It emphasizes the importance of capital budgeting tools, cost-volume-profit analysis, and adherence to accounting standards in making informed financial decisions.

Running Head: ACCOUNTING AND FINANCE

Accounting and finance

Accounting and finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance 1

Contents

Introduction...........................................................................................................................................2

Scenario I..............................................................................................................................................2

Investment Appraisal.........................................................................................................................2

Calculation of Net Present Value...................................................................................................2

Calculation of Pay-Back Period.....................................................................................................4

Analysis of the methods used........................................................................................................5

Budget...............................................................................................................................................5

Calculation of contribution per Kilogram......................................................................................5

Profit maximising Sales Mix.........................................................................................................6

Limiting factor analysis.................................................................................................................7

Scenario II.............................................................................................................................................8

Accounting rules adopted by the treasurer.........................................................................................8

Accounting rules should be adopted by treasurer..............................................................................8

Financial accounts of the club...........................................................................................................9

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Contents

Introduction...........................................................................................................................................2

Scenario I..............................................................................................................................................2

Investment Appraisal.........................................................................................................................2

Calculation of Net Present Value...................................................................................................2

Calculation of Pay-Back Period.....................................................................................................4

Analysis of the methods used........................................................................................................5

Budget...............................................................................................................................................5

Calculation of contribution per Kilogram......................................................................................5

Profit maximising Sales Mix.........................................................................................................6

Limiting factor analysis.................................................................................................................7

Scenario II.............................................................................................................................................8

Accounting rules adopted by the treasurer.........................................................................................8

Accounting rules should be adopted by treasurer..............................................................................8

Financial accounts of the club...........................................................................................................9

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Accounting and Finance 2

Introduction

Capital budgeting tools and techniques are used to analyse an investment proposal. Various

methods like Net Present Value, Internal Rate of Return, Pay-Back Period are been applied to

check the effectiveness of the proposal. It is considered to be the most challenging task for

the management because it involves the process of decision making about the investment in a

particular plan. This includes allocation of funds to a specific project for a specific period of

time in order to achieve the goals and objectives of the organization. A company can choose

its investment proposal on the basis of capital budgeting methods. Cost- Volume Profit

analysis is a method of determining changes in cost and volume which directly affect

operating profit of an organization. The analysis also helps in calculating contribution per

unit, analysis of limiting factor and to identify the profit maximising sales mix.

Dangerous Dessert Company (DDC) is an enterprise that deals in the production of desserts

and offers a wide range of products like bakery items, fresh fruit products, dairy products and

ice creams. The company has set a division range for one of its product that is vanilla ice

cream. The division range of the ice cream is Single Whammy, Double Whammy and Triple

Whammy. Recently the company has opted for an investment proposal for delivering vanilla

ice cream directly to the general public. It has also prepared a budget for the same product.

Bespoke Golf Club is an organization which is financed by the employees of Bespoke Built

Ltd. Peter Kwok has recently joined the club and want to know about the final accounts of the

club. The report presented by the treasurer in the meeting did not show a clear picture of the

financial position of the club and was not according to the rules of accounting. Peter wanted

the accounts to be reported in a proper format and also according to standard rules and

guidelines.

This report consist of the analysis of the investment proposal chosen by DDC and the

calculation of contribution per unit, sales mix and analysis of limiting factor as per the budget

prepared by DDC. The report also contains the information about the accounting rules which

are required to be adopted by the treasurer of Bespoke along with their explanation.

Preparation of club’s accounts in proper format and as per rules is also done in this report.

Scenario I

Investment Appraisal

DDC is evaluating an investment proposal which is concerned with the direct delivery of ice-

creams to the public. NPV method and Pay-Back Period method is used to evaluate this

project.

Calculation of Net Present Value

Cash Outflows ($ million)

Years 0 1 2 3 4 5

Cost of Vans 60000

Pre-launch advertising 100000

Salary of van drivers 50000 50000 125000 125000 125000

Van running cost 10000 12000 14000 16000 18000

cost of running central services 60000 60000 80000 80000 80000

Advertising Budget cost 50000 50000 50000 50000 50000

Introduction

Capital budgeting tools and techniques are used to analyse an investment proposal. Various

methods like Net Present Value, Internal Rate of Return, Pay-Back Period are been applied to

check the effectiveness of the proposal. It is considered to be the most challenging task for

the management because it involves the process of decision making about the investment in a

particular plan. This includes allocation of funds to a specific project for a specific period of

time in order to achieve the goals and objectives of the organization. A company can choose

its investment proposal on the basis of capital budgeting methods. Cost- Volume Profit

analysis is a method of determining changes in cost and volume which directly affect

operating profit of an organization. The analysis also helps in calculating contribution per

unit, analysis of limiting factor and to identify the profit maximising sales mix.

Dangerous Dessert Company (DDC) is an enterprise that deals in the production of desserts

and offers a wide range of products like bakery items, fresh fruit products, dairy products and

ice creams. The company has set a division range for one of its product that is vanilla ice

cream. The division range of the ice cream is Single Whammy, Double Whammy and Triple

Whammy. Recently the company has opted for an investment proposal for delivering vanilla

ice cream directly to the general public. It has also prepared a budget for the same product.

Bespoke Golf Club is an organization which is financed by the employees of Bespoke Built

Ltd. Peter Kwok has recently joined the club and want to know about the final accounts of the

club. The report presented by the treasurer in the meeting did not show a clear picture of the

financial position of the club and was not according to the rules of accounting. Peter wanted

the accounts to be reported in a proper format and also according to standard rules and

guidelines.

This report consist of the analysis of the investment proposal chosen by DDC and the

calculation of contribution per unit, sales mix and analysis of limiting factor as per the budget

prepared by DDC. The report also contains the information about the accounting rules which

are required to be adopted by the treasurer of Bespoke along with their explanation.

Preparation of club’s accounts in proper format and as per rules is also done in this report.

Scenario I

Investment Appraisal

DDC is evaluating an investment proposal which is concerned with the direct delivery of ice-

creams to the public. NPV method and Pay-Back Period method is used to evaluate this

project.

Calculation of Net Present Value

Cash Outflows ($ million)

Years 0 1 2 3 4 5

Cost of Vans 60000

Pre-launch advertising 100000

Salary of van drivers 50000 50000 125000 125000 125000

Van running cost 10000 12000 14000 16000 18000

cost of running central services 60000 60000 80000 80000 80000

Advertising Budget cost 50000 50000 50000 50000 50000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance 3

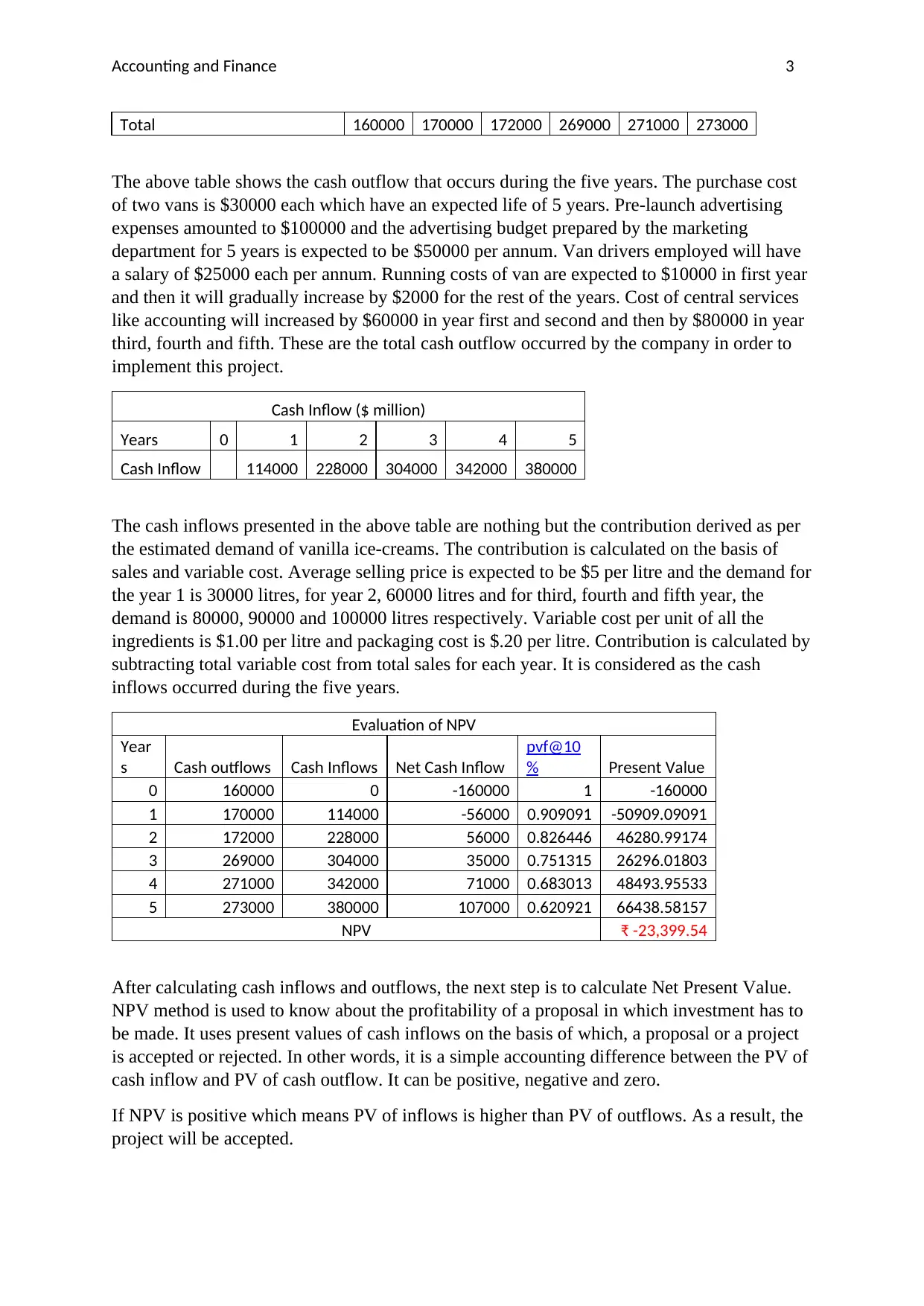

Total 160000 170000 172000 269000 271000 273000

The above table shows the cash outflow that occurs during the five years. The purchase cost

of two vans is $30000 each which have an expected life of 5 years. Pre-launch advertising

expenses amounted to $100000 and the advertising budget prepared by the marketing

department for 5 years is expected to be $50000 per annum. Van drivers employed will have

a salary of $25000 each per annum. Running costs of van are expected to $10000 in first year

and then it will gradually increase by $2000 for the rest of the years. Cost of central services

like accounting will increased by $60000 in year first and second and then by $80000 in year

third, fourth and fifth. These are the total cash outflow occurred by the company in order to

implement this project.

Cash Inflow ($ million)

Years 0 1 2 3 4 5

Cash Inflow 114000 228000 304000 342000 380000

The cash inflows presented in the above table are nothing but the contribution derived as per

the estimated demand of vanilla ice-creams. The contribution is calculated on the basis of

sales and variable cost. Average selling price is expected to be $5 per litre and the demand for

the year 1 is 30000 litres, for year 2, 60000 litres and for third, fourth and fifth year, the

demand is 80000, 90000 and 100000 litres respectively. Variable cost per unit of all the

ingredients is $1.00 per litre and packaging cost is $.20 per litre. Contribution is calculated by

subtracting total variable cost from total sales for each year. It is considered as the cash

inflows occurred during the five years.

Evaluation of NPV

Year

s Cash outflows Cash Inflows Net Cash Inflow

pvf@10

% Present Value

0 160000 0 -160000 1 -160000

1 170000 114000 -56000 0.909091 -50909.09091

2 172000 228000 56000 0.826446 46280.99174

3 269000 304000 35000 0.751315 26296.01803

4 271000 342000 71000 0.683013 48493.95533

5 273000 380000 107000 0.620921 66438.58157

NPV ₹ -23,399.54

After calculating cash inflows and outflows, the next step is to calculate Net Present Value.

NPV method is used to know about the profitability of a proposal in which investment has to

be made. It uses present values of cash inflows on the basis of which, a proposal or a project

is accepted or rejected. In other words, it is a simple accounting difference between the PV of

cash inflow and PV of cash outflow. It can be positive, negative and zero.

If NPV is positive which means PV of inflows is higher than PV of outflows. As a result, the

project will be accepted.

Total 160000 170000 172000 269000 271000 273000

The above table shows the cash outflow that occurs during the five years. The purchase cost

of two vans is $30000 each which have an expected life of 5 years. Pre-launch advertising

expenses amounted to $100000 and the advertising budget prepared by the marketing

department for 5 years is expected to be $50000 per annum. Van drivers employed will have

a salary of $25000 each per annum. Running costs of van are expected to $10000 in first year

and then it will gradually increase by $2000 for the rest of the years. Cost of central services

like accounting will increased by $60000 in year first and second and then by $80000 in year

third, fourth and fifth. These are the total cash outflow occurred by the company in order to

implement this project.

Cash Inflow ($ million)

Years 0 1 2 3 4 5

Cash Inflow 114000 228000 304000 342000 380000

The cash inflows presented in the above table are nothing but the contribution derived as per

the estimated demand of vanilla ice-creams. The contribution is calculated on the basis of

sales and variable cost. Average selling price is expected to be $5 per litre and the demand for

the year 1 is 30000 litres, for year 2, 60000 litres and for third, fourth and fifth year, the

demand is 80000, 90000 and 100000 litres respectively. Variable cost per unit of all the

ingredients is $1.00 per litre and packaging cost is $.20 per litre. Contribution is calculated by

subtracting total variable cost from total sales for each year. It is considered as the cash

inflows occurred during the five years.

Evaluation of NPV

Year

s Cash outflows Cash Inflows Net Cash Inflow

pvf@10

% Present Value

0 160000 0 -160000 1 -160000

1 170000 114000 -56000 0.909091 -50909.09091

2 172000 228000 56000 0.826446 46280.99174

3 269000 304000 35000 0.751315 26296.01803

4 271000 342000 71000 0.683013 48493.95533

5 273000 380000 107000 0.620921 66438.58157

NPV ₹ -23,399.54

After calculating cash inflows and outflows, the next step is to calculate Net Present Value.

NPV method is used to know about the profitability of a proposal in which investment has to

be made. It uses present values of cash inflows on the basis of which, a proposal or a project

is accepted or rejected. In other words, it is a simple accounting difference between the PV of

cash inflow and PV of cash outflow. It can be positive, negative and zero.

If NPV is positive which means PV of inflows is higher than PV of outflows. As a result, the

project will be accepted.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance 4

If it is negative, then the proposal is rejected because the PV of cash outflows is more than

the PV of cash inflows.

And if, NPV is equal to zero it means the present values of both inflow and outflow are equal

and the project is accepted (Bierman Jr, & Smidt, 2012).

Advantages and Disadvantages

Merits:

The method helps in determining that whether the proposed project will increase the

value of firm or not.

NPV reveals that when the project will produce income and how important that

income will be.

It is used in calculating time value of money.

Helps in comparing different projects.

Evaluation of NPV always provide a correct decision regarding investments.

Demerits:

NPV is difficult to use.

When the projects are of unequal life, NPV can provide incorrect decision.

Appropriate discount rate cannot be calculated.

The method is based on assumptions

It is a very difficult task to determine the value of a project because there are many method to

measure that. The time value of money factor is considered by the managers and for that they

used NPV method. As this is based on predicted cash flows, the accounting practices like

depreciation and many more does not affect the decision. So it is very important to use this

method for knowing the profitability of a project. In the above table, NPV is evaluated at a

discount rate of 10% and on the basis of the information provided in the scenario. The above

table shows a negative NPV which means that the amount of present values of cash outflow

is more than the cash inflow, so this project should be rejected.

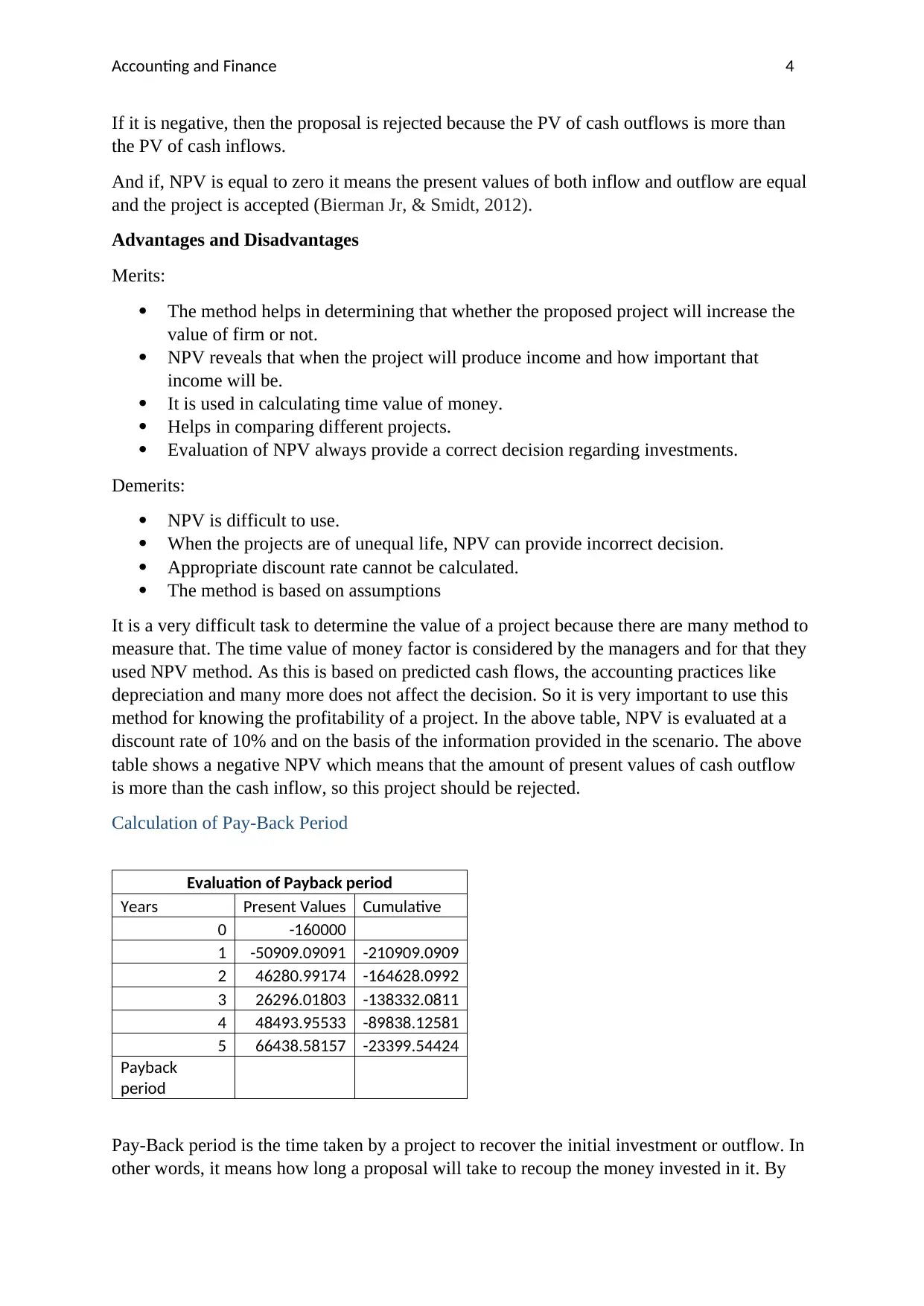

Calculation of Pay-Back Period

Evaluation of Payback period

Years Present Values Cumulative

0 -160000

1 -50909.09091 -210909.0909

2 46280.99174 -164628.0992

3 26296.01803 -138332.0811

4 48493.95533 -89838.12581

5 66438.58157 -23399.54424

Payback

period

Pay-Back period is the time taken by a project to recover the initial investment or outflow. In

other words, it means how long a proposal will take to recoup the money invested in it. By

If it is negative, then the proposal is rejected because the PV of cash outflows is more than

the PV of cash inflows.

And if, NPV is equal to zero it means the present values of both inflow and outflow are equal

and the project is accepted (Bierman Jr, & Smidt, 2012).

Advantages and Disadvantages

Merits:

The method helps in determining that whether the proposed project will increase the

value of firm or not.

NPV reveals that when the project will produce income and how important that

income will be.

It is used in calculating time value of money.

Helps in comparing different projects.

Evaluation of NPV always provide a correct decision regarding investments.

Demerits:

NPV is difficult to use.

When the projects are of unequal life, NPV can provide incorrect decision.

Appropriate discount rate cannot be calculated.

The method is based on assumptions

It is a very difficult task to determine the value of a project because there are many method to

measure that. The time value of money factor is considered by the managers and for that they

used NPV method. As this is based on predicted cash flows, the accounting practices like

depreciation and many more does not affect the decision. So it is very important to use this

method for knowing the profitability of a project. In the above table, NPV is evaluated at a

discount rate of 10% and on the basis of the information provided in the scenario. The above

table shows a negative NPV which means that the amount of present values of cash outflow

is more than the cash inflow, so this project should be rejected.

Calculation of Pay-Back Period

Evaluation of Payback period

Years Present Values Cumulative

0 -160000

1 -50909.09091 -210909.0909

2 46280.99174 -164628.0992

3 26296.01803 -138332.0811

4 48493.95533 -89838.12581

5 66438.58157 -23399.54424

Payback

period

Pay-Back period is the time taken by a project to recover the initial investment or outflow. In

other words, it means how long a proposal will take to recoup the money invested in it. By

Accounting and Finance 5

knowing the payback period, investors can decide whether to invest in the desired proposal or

not (Bierman Jr, & Smidt, 2012).

The above table shows that the project is not able to retrieve the amount invested in it during

its life of 5 years. The amount gained from the project during the five years is not enough to

meet the initial cash outlay. So it is suggested not to opt for this project.

Analysis of the methods used

The evaluation of both the methods shows that the proposal opted by DDC is not a desired

one. Investing in it will not provide profits to the company. The NPV table shows that the

project will not earn profits during its life span of five years. As the theory says that the

investor should invest only in those projects that have a positive NPV. On the other hand,

Payback period table represents that the project is not capable enough to recover the cash

outlays incurred on it during its life span of 5 years. On the basis of above analysis, the

proposal of purchasing two vans should not be accepted by DDC as it will result in creating

loss for the company. So it is better for the company to avoid investing in this project.

Budget

DDC has prepared a budget for the production of range of vanilla ice-cream. It shows the

consumption and cost of required ingredients per kilogram. Fixed and variable overheads

along with the selling price per unit and quantity demanded for all three ranges is also

mentioned in the budget. Contribution per unit, sales mix and analysis of limiting factor is

done on the basis of provided budget.

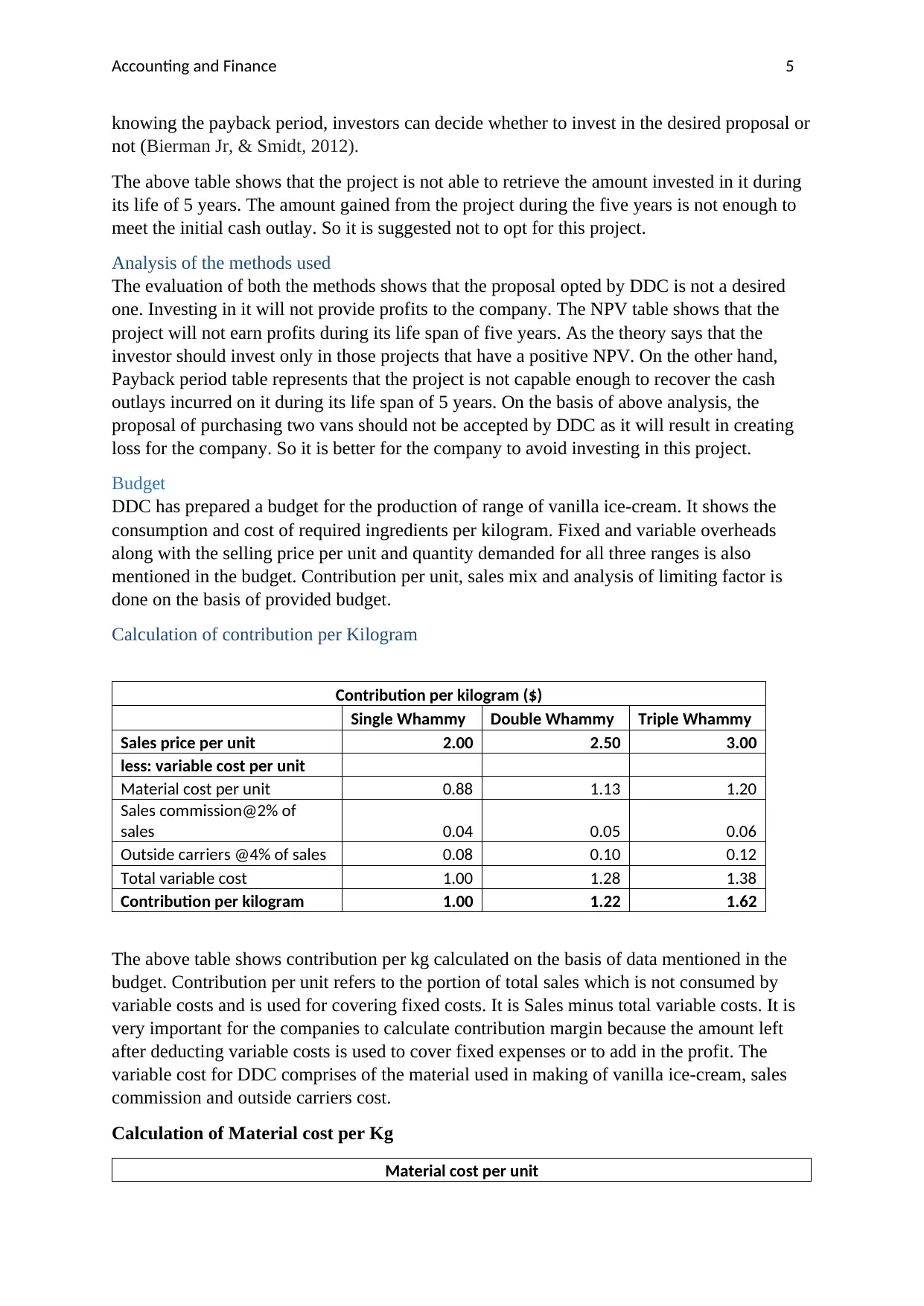

Calculation of contribution per Kilogram

Contribution per kilogram ($)

Single Whammy Double Whammy Triple Whammy

Sales price per unit 2.00 2.50 3.00

less: variable cost per unit

Material cost per unit 0.88 1.13 1.20

Sales commission@2% of

sales 0.04 0.05 0.06

Outside carriers @4% of sales 0.08 0.10 0.12

Total variable cost 1.00 1.28 1.38

Contribution per kilogram 1.00 1.22 1.62

The above table shows contribution per kg calculated on the basis of data mentioned in the

budget. Contribution per unit refers to the portion of total sales which is not consumed by

variable costs and is used for covering fixed costs. It is Sales minus total variable costs. It is

very important for the companies to calculate contribution margin because the amount left

after deducting variable costs is used to cover fixed expenses or to add in the profit. The

variable cost for DDC comprises of the material used in making of vanilla ice-cream, sales

commission and outside carriers cost.

Calculation of Material cost per Kg

Material cost per unit

knowing the payback period, investors can decide whether to invest in the desired proposal or

not (Bierman Jr, & Smidt, 2012).

The above table shows that the project is not able to retrieve the amount invested in it during

its life of 5 years. The amount gained from the project during the five years is not enough to

meet the initial cash outlay. So it is suggested not to opt for this project.

Analysis of the methods used

The evaluation of both the methods shows that the proposal opted by DDC is not a desired

one. Investing in it will not provide profits to the company. The NPV table shows that the

project will not earn profits during its life span of five years. As the theory says that the

investor should invest only in those projects that have a positive NPV. On the other hand,

Payback period table represents that the project is not capable enough to recover the cash

outlays incurred on it during its life span of 5 years. On the basis of above analysis, the

proposal of purchasing two vans should not be accepted by DDC as it will result in creating

loss for the company. So it is better for the company to avoid investing in this project.

Budget

DDC has prepared a budget for the production of range of vanilla ice-cream. It shows the

consumption and cost of required ingredients per kilogram. Fixed and variable overheads

along with the selling price per unit and quantity demanded for all three ranges is also

mentioned in the budget. Contribution per unit, sales mix and analysis of limiting factor is

done on the basis of provided budget.

Calculation of contribution per Kilogram

Contribution per kilogram ($)

Single Whammy Double Whammy Triple Whammy

Sales price per unit 2.00 2.50 3.00

less: variable cost per unit

Material cost per unit 0.88 1.13 1.20

Sales commission@2% of

sales 0.04 0.05 0.06

Outside carriers @4% of sales 0.08 0.10 0.12

Total variable cost 1.00 1.28 1.38

Contribution per kilogram 1.00 1.22 1.62

The above table shows contribution per kg calculated on the basis of data mentioned in the

budget. Contribution per unit refers to the portion of total sales which is not consumed by

variable costs and is used for covering fixed costs. It is Sales minus total variable costs. It is

very important for the companies to calculate contribution margin because the amount left

after deducting variable costs is used to cover fixed expenses or to add in the profit. The

variable cost for DDC comprises of the material used in making of vanilla ice-cream, sales

commission and outside carriers cost.

Calculation of Material cost per Kg

Material cost per unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance 6

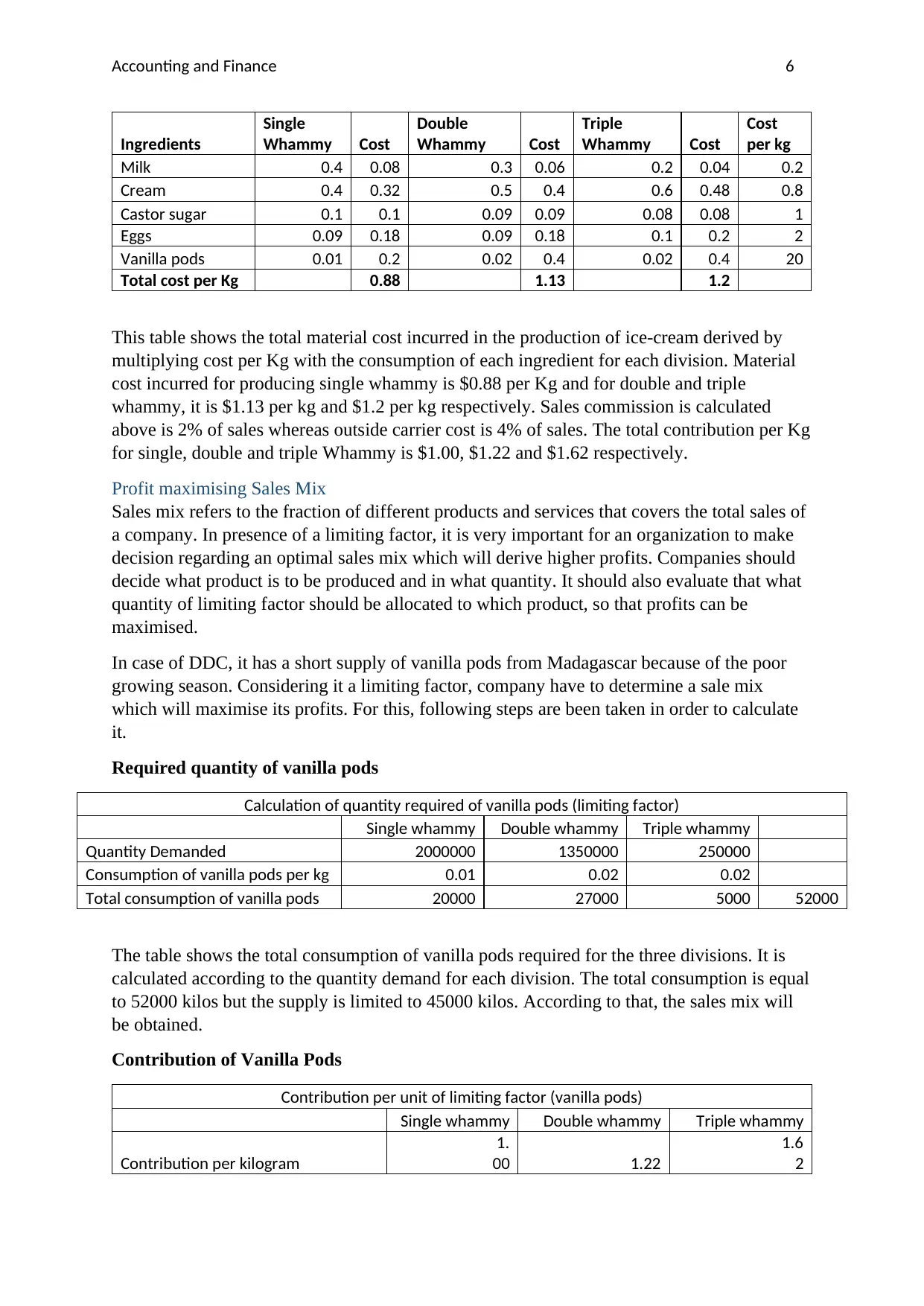

Ingredients

Single

Whammy Cost

Double

Whammy Cost

Triple

Whammy Cost

Cost

per kg

Milk 0.4 0.08 0.3 0.06 0.2 0.04 0.2

Cream 0.4 0.32 0.5 0.4 0.6 0.48 0.8

Castor sugar 0.1 0.1 0.09 0.09 0.08 0.08 1

Eggs 0.09 0.18 0.09 0.18 0.1 0.2 2

Vanilla pods 0.01 0.2 0.02 0.4 0.02 0.4 20

Total cost per Kg 0.88 1.13 1.2

This table shows the total material cost incurred in the production of ice-cream derived by

multiplying cost per Kg with the consumption of each ingredient for each division. Material

cost incurred for producing single whammy is $0.88 per Kg and for double and triple

whammy, it is $1.13 per kg and $1.2 per kg respectively. Sales commission is calculated

above is 2% of sales whereas outside carrier cost is 4% of sales. The total contribution per Kg

for single, double and triple Whammy is $1.00, $1.22 and $1.62 respectively.

Profit maximising Sales Mix

Sales mix refers to the fraction of different products and services that covers the total sales of

a company. In presence of a limiting factor, it is very important for an organization to make

decision regarding an optimal sales mix which will derive higher profits. Companies should

decide what product is to be produced and in what quantity. It should also evaluate that what

quantity of limiting factor should be allocated to which product, so that profits can be

maximised.

In case of DDC, it has a short supply of vanilla pods from Madagascar because of the poor

growing season. Considering it a limiting factor, company have to determine a sale mix

which will maximise its profits. For this, following steps are been taken in order to calculate

it.

Required quantity of vanilla pods

Calculation of quantity required of vanilla pods (limiting factor)

Single whammy Double whammy Triple whammy

Quantity Demanded 2000000 1350000 250000

Consumption of vanilla pods per kg 0.01 0.02 0.02

Total consumption of vanilla pods 20000 27000 5000 52000

The table shows the total consumption of vanilla pods required for the three divisions. It is

calculated according to the quantity demand for each division. The total consumption is equal

to 52000 kilos but the supply is limited to 45000 kilos. According to that, the sales mix will

be obtained.

Contribution of Vanilla Pods

Contribution per unit of limiting factor (vanilla pods)

Single whammy Double whammy Triple whammy

Contribution per kilogram

1.

00 1.22

1.6

2

Ingredients

Single

Whammy Cost

Double

Whammy Cost

Triple

Whammy Cost

Cost

per kg

Milk 0.4 0.08 0.3 0.06 0.2 0.04 0.2

Cream 0.4 0.32 0.5 0.4 0.6 0.48 0.8

Castor sugar 0.1 0.1 0.09 0.09 0.08 0.08 1

Eggs 0.09 0.18 0.09 0.18 0.1 0.2 2

Vanilla pods 0.01 0.2 0.02 0.4 0.02 0.4 20

Total cost per Kg 0.88 1.13 1.2

This table shows the total material cost incurred in the production of ice-cream derived by

multiplying cost per Kg with the consumption of each ingredient for each division. Material

cost incurred for producing single whammy is $0.88 per Kg and for double and triple

whammy, it is $1.13 per kg and $1.2 per kg respectively. Sales commission is calculated

above is 2% of sales whereas outside carrier cost is 4% of sales. The total contribution per Kg

for single, double and triple Whammy is $1.00, $1.22 and $1.62 respectively.

Profit maximising Sales Mix

Sales mix refers to the fraction of different products and services that covers the total sales of

a company. In presence of a limiting factor, it is very important for an organization to make

decision regarding an optimal sales mix which will derive higher profits. Companies should

decide what product is to be produced and in what quantity. It should also evaluate that what

quantity of limiting factor should be allocated to which product, so that profits can be

maximised.

In case of DDC, it has a short supply of vanilla pods from Madagascar because of the poor

growing season. Considering it a limiting factor, company have to determine a sale mix

which will maximise its profits. For this, following steps are been taken in order to calculate

it.

Required quantity of vanilla pods

Calculation of quantity required of vanilla pods (limiting factor)

Single whammy Double whammy Triple whammy

Quantity Demanded 2000000 1350000 250000

Consumption of vanilla pods per kg 0.01 0.02 0.02

Total consumption of vanilla pods 20000 27000 5000 52000

The table shows the total consumption of vanilla pods required for the three divisions. It is

calculated according to the quantity demand for each division. The total consumption is equal

to 52000 kilos but the supply is limited to 45000 kilos. According to that, the sales mix will

be obtained.

Contribution of Vanilla Pods

Contribution per unit of limiting factor (vanilla pods)

Single whammy Double whammy Triple whammy

Contribution per kilogram

1.

00 1.22

1.6

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance 7

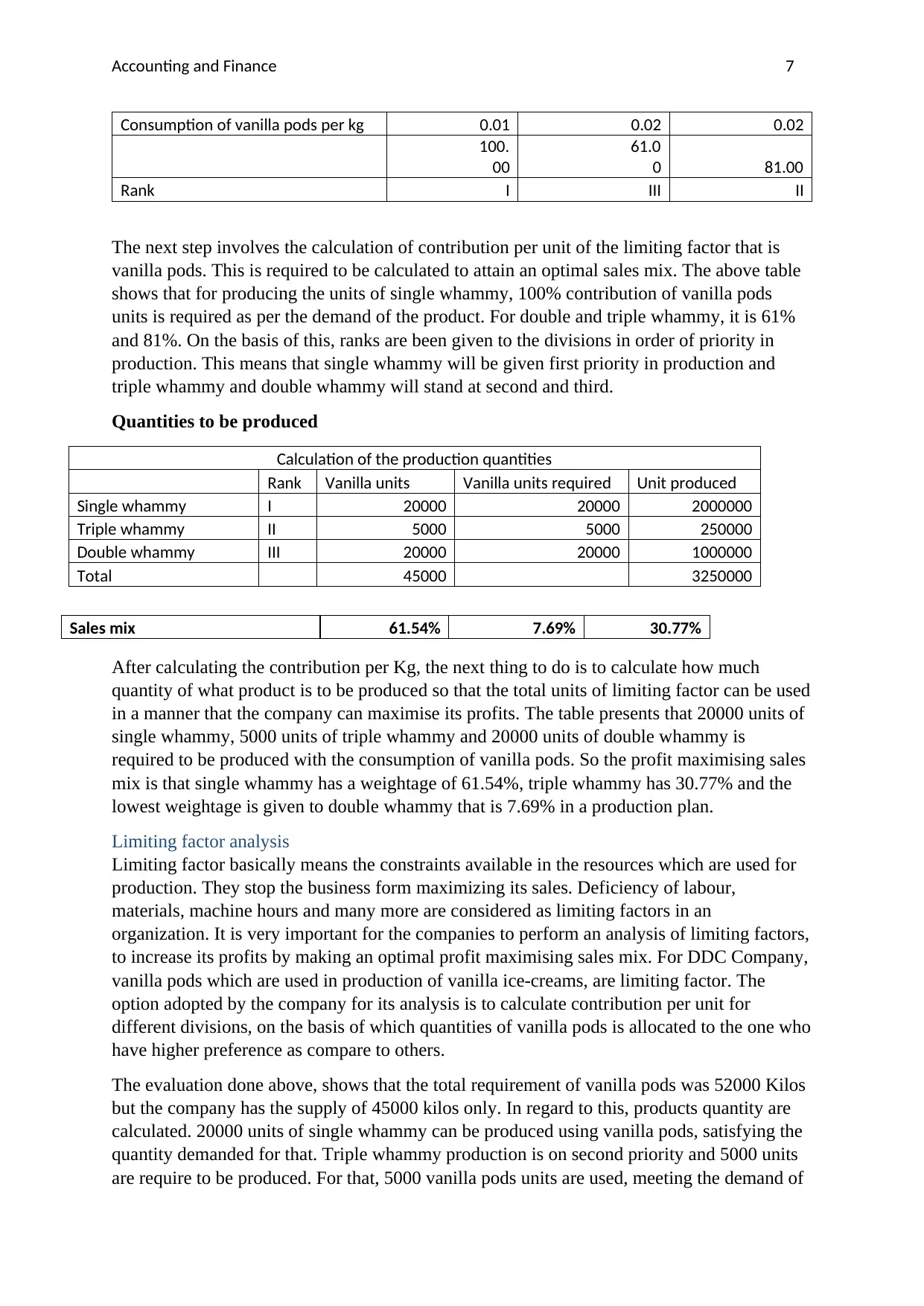

Consumption of vanilla pods per kg 0.01 0.02 0.02

100.

00

61.0

0 81.00

Rank I III II

The next step involves the calculation of contribution per unit of the limiting factor that is

vanilla pods. This is required to be calculated to attain an optimal sales mix. The above table

shows that for producing the units of single whammy, 100% contribution of vanilla pods

units is required as per the demand of the product. For double and triple whammy, it is 61%

and 81%. On the basis of this, ranks are been given to the divisions in order of priority in

production. This means that single whammy will be given first priority in production and

triple whammy and double whammy will stand at second and third.

Quantities to be produced

Calculation of the production quantities

Rank Vanilla units Vanilla units required Unit produced

Single whammy I 20000 20000 2000000

Triple whammy II 5000 5000 250000

Double whammy III 20000 20000 1000000

Total 45000 3250000

After calculating the contribution per Kg, the next thing to do is to calculate how much

quantity of what product is to be produced so that the total units of limiting factor can be used

in a manner that the company can maximise its profits. The table presents that 20000 units of

single whammy, 5000 units of triple whammy and 20000 units of double whammy is

required to be produced with the consumption of vanilla pods. So the profit maximising sales

mix is that single whammy has a weightage of 61.54%, triple whammy has 30.77% and the

lowest weightage is given to double whammy that is 7.69% in a production plan.

Limiting factor analysis

Limiting factor basically means the constraints available in the resources which are used for

production. They stop the business form maximizing its sales. Deficiency of labour,

materials, machine hours and many more are considered as limiting factors in an

organization. It is very important for the companies to perform an analysis of limiting factors,

to increase its profits by making an optimal profit maximising sales mix. For DDC Company,

vanilla pods which are used in production of vanilla ice-creams, are limiting factor. The

option adopted by the company for its analysis is to calculate contribution per unit for

different divisions, on the basis of which quantities of vanilla pods is allocated to the one who

have higher preference as compare to others.

The evaluation done above, shows that the total requirement of vanilla pods was 52000 Kilos

but the company has the supply of 45000 kilos only. In regard to this, products quantity are

calculated. 20000 units of single whammy can be produced using vanilla pods, satisfying the

quantity demanded for that. Triple whammy production is on second priority and 5000 units

are require to be produced. For that, 5000 vanilla pods units are used, meeting the demand of

Sales mix 61.54% 7.69% 30.77%

Consumption of vanilla pods per kg 0.01 0.02 0.02

100.

00

61.0

0 81.00

Rank I III II

The next step involves the calculation of contribution per unit of the limiting factor that is

vanilla pods. This is required to be calculated to attain an optimal sales mix. The above table

shows that for producing the units of single whammy, 100% contribution of vanilla pods

units is required as per the demand of the product. For double and triple whammy, it is 61%

and 81%. On the basis of this, ranks are been given to the divisions in order of priority in

production. This means that single whammy will be given first priority in production and

triple whammy and double whammy will stand at second and third.

Quantities to be produced

Calculation of the production quantities

Rank Vanilla units Vanilla units required Unit produced

Single whammy I 20000 20000 2000000

Triple whammy II 5000 5000 250000

Double whammy III 20000 20000 1000000

Total 45000 3250000

After calculating the contribution per Kg, the next thing to do is to calculate how much

quantity of what product is to be produced so that the total units of limiting factor can be used

in a manner that the company can maximise its profits. The table presents that 20000 units of

single whammy, 5000 units of triple whammy and 20000 units of double whammy is

required to be produced with the consumption of vanilla pods. So the profit maximising sales

mix is that single whammy has a weightage of 61.54%, triple whammy has 30.77% and the

lowest weightage is given to double whammy that is 7.69% in a production plan.

Limiting factor analysis

Limiting factor basically means the constraints available in the resources which are used for

production. They stop the business form maximizing its sales. Deficiency of labour,

materials, machine hours and many more are considered as limiting factors in an

organization. It is very important for the companies to perform an analysis of limiting factors,

to increase its profits by making an optimal profit maximising sales mix. For DDC Company,

vanilla pods which are used in production of vanilla ice-creams, are limiting factor. The

option adopted by the company for its analysis is to calculate contribution per unit for

different divisions, on the basis of which quantities of vanilla pods is allocated to the one who

have higher preference as compare to others.

The evaluation done above, shows that the total requirement of vanilla pods was 52000 Kilos

but the company has the supply of 45000 kilos only. In regard to this, products quantity are

calculated. 20000 units of single whammy can be produced using vanilla pods, satisfying the

quantity demanded for that. Triple whammy production is on second priority and 5000 units

are require to be produced. For that, 5000 vanilla pods units are used, meeting the demand of

Sales mix 61.54% 7.69% 30.77%

Accounting and Finance 8

250,000 Kg. For the production of double whammy, only 20000 units of vanilla pods are left

to produce double whammy units. The units made, meet only the demand of 1000000 kilos,

while initial demand for double whammy was 13500000 kilos. As this product has lowest

contribution per unit, that is why it has given less priority and the demand is also reduced

because there was not enough supply of vanilla pods to produce all the required units of

double whammy which satisfies its initial demand.

Scenario II

Accounting rules adopted by the treasurer

Accounting rules are list of rules explain in detail and are required to be followed by

accountants and treasurers in preparing final accounts of companies. Recording of

transactions and creation of journal entries needed some rules that are known as three golden

rules of accounting standards. These rules are classified according to the three different types

of accounts named as Personal Account, Real Account and Nominal Account. The three

golden rules are adopted by the treasures while preparing his report (Rajni, 2016). The three

golden rules are:

Debit the receiver, Credit the giver

This rule is for personal account. It means that when an individual give some amount to the

company, it is treated as an inflow and that individual becomes giver and his account is

credited in the books of company. Similarly, if a person receives something form the

company, then he is called a receiver and stands on the debit side of the books of business.

Debit what comes in, Credit what goes out

This rule is applicable for real account. Real account includes any property or goods which

are either coming into the business or going out of the business. The rule states that if any

property comes into the business, the account of that property will be debited in the books

and similarly if any goods or property goes out of the business, the account of the same will

be credited.

The deposits done by the club for New Year and slide show are been credited in the books of

accounts as per this rule.

Debit all expenses and losses and Credit all incomes and gains

This golden rule is for nominal account. This account generally includes business income,

losses, expenses and gains. According to the rules, the account of expenses and losses

incurred by the business will stand on the debit side of the accounts books. On the other hand,

if business earns income and gains, the account of the same will have a credit balance.

All the profit gained by the golf club from its activities have a credit balance and all the

expenses incurred on the different events by the club are debited in its books of accounts

Accounting rules should be adopted by treasurer

The treasurer should use a proper format in presenting the financial statements of the club.

The information presented by her in the balance sheet of accounts can be bifurcated into two

accounts which are mandatory to be maintained as per accounting rules and standards. These

accounts are Income and Expenditure account and Balance sheet.

250,000 Kg. For the production of double whammy, only 20000 units of vanilla pods are left

to produce double whammy units. The units made, meet only the demand of 1000000 kilos,

while initial demand for double whammy was 13500000 kilos. As this product has lowest

contribution per unit, that is why it has given less priority and the demand is also reduced

because there was not enough supply of vanilla pods to produce all the required units of

double whammy which satisfies its initial demand.

Scenario II

Accounting rules adopted by the treasurer

Accounting rules are list of rules explain in detail and are required to be followed by

accountants and treasurers in preparing final accounts of companies. Recording of

transactions and creation of journal entries needed some rules that are known as three golden

rules of accounting standards. These rules are classified according to the three different types

of accounts named as Personal Account, Real Account and Nominal Account. The three

golden rules are adopted by the treasures while preparing his report (Rajni, 2016). The three

golden rules are:

Debit the receiver, Credit the giver

This rule is for personal account. It means that when an individual give some amount to the

company, it is treated as an inflow and that individual becomes giver and his account is

credited in the books of company. Similarly, if a person receives something form the

company, then he is called a receiver and stands on the debit side of the books of business.

Debit what comes in, Credit what goes out

This rule is applicable for real account. Real account includes any property or goods which

are either coming into the business or going out of the business. The rule states that if any

property comes into the business, the account of that property will be debited in the books

and similarly if any goods or property goes out of the business, the account of the same will

be credited.

The deposits done by the club for New Year and slide show are been credited in the books of

accounts as per this rule.

Debit all expenses and losses and Credit all incomes and gains

This golden rule is for nominal account. This account generally includes business income,

losses, expenses and gains. According to the rules, the account of expenses and losses

incurred by the business will stand on the debit side of the accounts books. On the other hand,

if business earns income and gains, the account of the same will have a credit balance.

All the profit gained by the golf club from its activities have a credit balance and all the

expenses incurred on the different events by the club are debited in its books of accounts

Accounting rules should be adopted by treasurer

The treasurer should use a proper format in presenting the financial statements of the club.

The information presented by her in the balance sheet of accounts can be bifurcated into two

accounts which are mandatory to be maintained as per accounting rules and standards. These

accounts are Income and Expenditure account and Balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance 9

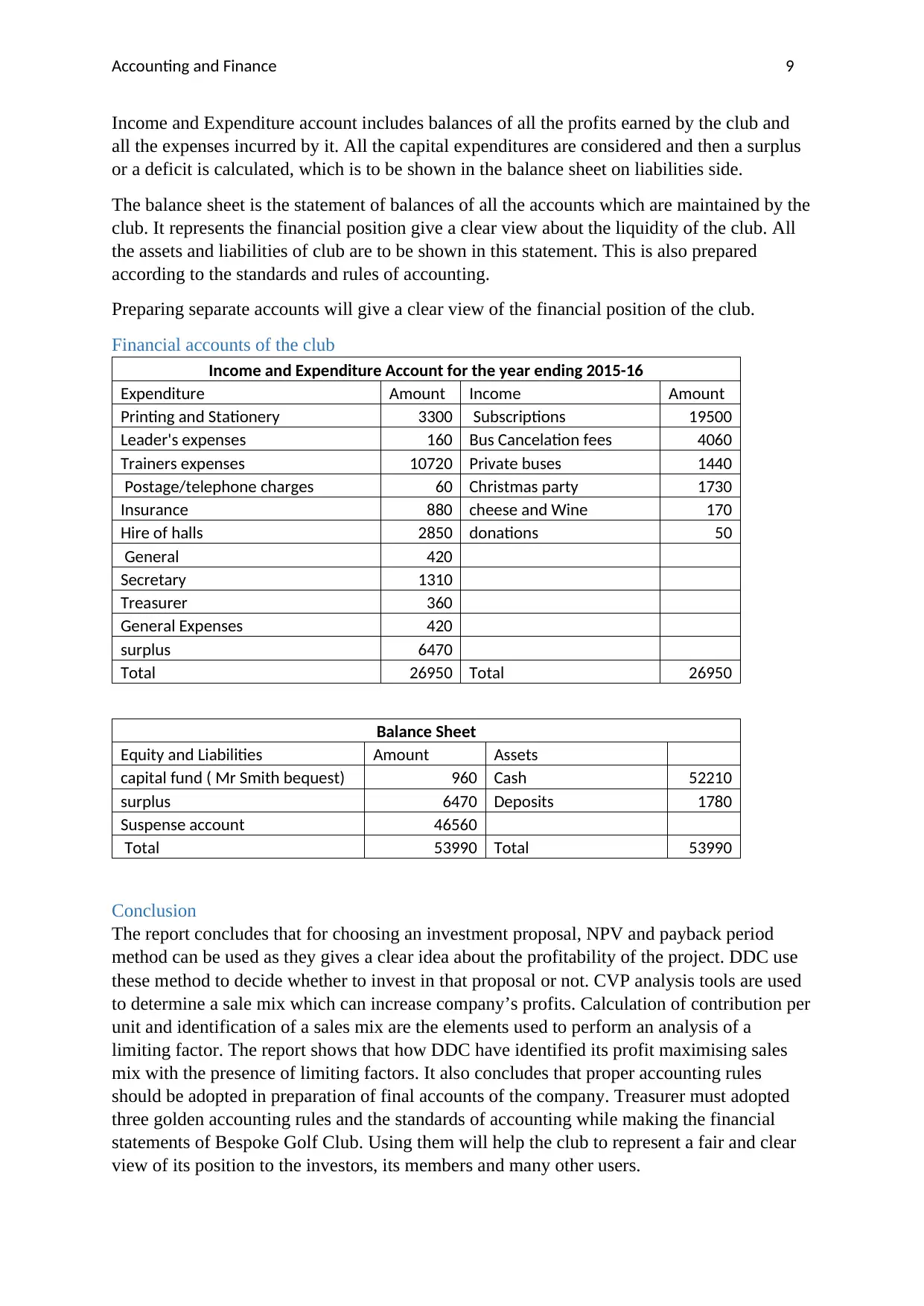

Income and Expenditure account includes balances of all the profits earned by the club and

all the expenses incurred by it. All the capital expenditures are considered and then a surplus

or a deficit is calculated, which is to be shown in the balance sheet on liabilities side.

The balance sheet is the statement of balances of all the accounts which are maintained by the

club. It represents the financial position give a clear view about the liquidity of the club. All

the assets and liabilities of club are to be shown in this statement. This is also prepared

according to the standards and rules of accounting.

Preparing separate accounts will give a clear view of the financial position of the club.

Financial accounts of the club

Income and Expenditure Account for the year ending 2015-16

Expenditure Amount Income Amount

Printing and Stationery 3300 Subscriptions 19500

Leader's expenses 160 Bus Cancelation fees 4060

Trainers expenses 10720 Private buses 1440

Postage/telephone charges 60 Christmas party 1730

Insurance 880 cheese and Wine 170

Hire of halls 2850 donations 50

General 420

Secretary 1310

Treasurer 360

General Expenses 420

surplus 6470

Total 26950 Total 26950

Balance Sheet

Equity and Liabilities Amount Assets

capital fund ( Mr Smith bequest) 960 Cash 52210

surplus 6470 Deposits 1780

Suspense account 46560

Total 53990 Total 53990

Conclusion

The report concludes that for choosing an investment proposal, NPV and payback period

method can be used as they gives a clear idea about the profitability of the project. DDC use

these method to decide whether to invest in that proposal or not. CVP analysis tools are used

to determine a sale mix which can increase company’s profits. Calculation of contribution per

unit and identification of a sales mix are the elements used to perform an analysis of a

limiting factor. The report shows that how DDC have identified its profit maximising sales

mix with the presence of limiting factors. It also concludes that proper accounting rules

should be adopted in preparation of final accounts of the company. Treasurer must adopted

three golden accounting rules and the standards of accounting while making the financial

statements of Bespoke Golf Club. Using them will help the club to represent a fair and clear

view of its position to the investors, its members and many other users.

Income and Expenditure account includes balances of all the profits earned by the club and

all the expenses incurred by it. All the capital expenditures are considered and then a surplus

or a deficit is calculated, which is to be shown in the balance sheet on liabilities side.

The balance sheet is the statement of balances of all the accounts which are maintained by the

club. It represents the financial position give a clear view about the liquidity of the club. All

the assets and liabilities of club are to be shown in this statement. This is also prepared

according to the standards and rules of accounting.

Preparing separate accounts will give a clear view of the financial position of the club.

Financial accounts of the club

Income and Expenditure Account for the year ending 2015-16

Expenditure Amount Income Amount

Printing and Stationery 3300 Subscriptions 19500

Leader's expenses 160 Bus Cancelation fees 4060

Trainers expenses 10720 Private buses 1440

Postage/telephone charges 60 Christmas party 1730

Insurance 880 cheese and Wine 170

Hire of halls 2850 donations 50

General 420

Secretary 1310

Treasurer 360

General Expenses 420

surplus 6470

Total 26950 Total 26950

Balance Sheet

Equity and Liabilities Amount Assets

capital fund ( Mr Smith bequest) 960 Cash 52210

surplus 6470 Deposits 1780

Suspense account 46560

Total 53990 Total 53990

Conclusion

The report concludes that for choosing an investment proposal, NPV and payback period

method can be used as they gives a clear idea about the profitability of the project. DDC use

these method to decide whether to invest in that proposal or not. CVP analysis tools are used

to determine a sale mix which can increase company’s profits. Calculation of contribution per

unit and identification of a sales mix are the elements used to perform an analysis of a

limiting factor. The report shows that how DDC have identified its profit maximising sales

mix with the presence of limiting factors. It also concludes that proper accounting rules

should be adopted in preparation of final accounts of the company. Treasurer must adopted

three golden accounting rules and the standards of accounting while making the financial

statements of Bespoke Golf Club. Using them will help the club to represent a fair and clear

view of its position to the investors, its members and many other users.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance 10

References

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects. Routledge.

Rajni, S. (2016). Basic accounting. [S.l.]: Prentice-Hall Of India.

References

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects. Routledge.

Rajni, S. (2016). Basic accounting. [S.l.]: Prentice-Hall Of India.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.