Contemporary Issues in Accounting - Assignment

VerifiedAdded on 2020/04/15

|12

|2321

|67

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The study discusses on the important aspects of the study has been seen to identify the various

types of factors which has been seen to be related to ascertain whether the Newcrest Limited is

able to meet the objectives of the conceptual framework with its reporting. The study also able to

assesses the recognition criteria to report Assets, Liabilities, Equity, Revenue and Expenses.

Some of the other aspects of the study have been also able to present central qualitative

enhancing features of financial reporting and discern the improving characteristics of financial

reportage. The main findings have been able to discern that the selected company is seen to

comply with CG framework complying with Corporate Governance Values and suggestions

“(3rd edition)” published as per “ASX Corporate Governance Council”. LTI Plan has been seen

to be included with the calculation as per “Australian Accounting Standard AASB 2 Share Based

Payments”. The granted in 2017 have been seen to be value as per the non-IFRS financial

measures throughout the annual report.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The study discusses on the important aspects of the study has been seen to identify the various

types of factors which has been seen to be related to ascertain whether the Newcrest Limited is

able to meet the objectives of the conceptual framework with its reporting. The study also able to

assesses the recognition criteria to report Assets, Liabilities, Equity, Revenue and Expenses.

Some of the other aspects of the study have been also able to present central qualitative

enhancing features of financial reporting and discern the improving characteristics of financial

reportage. The main findings have been able to discern that the selected company is seen to

comply with CG framework complying with Corporate Governance Values and suggestions

“(3rd edition)” published as per “ASX Corporate Governance Council”. LTI Plan has been seen

to be included with the calculation as per “Australian Accounting Standard AASB 2 Share Based

Payments”. The granted in 2017 have been seen to be value as per the non-IFRS financial

measures throughout the annual report.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................6

Adherence with enhancing characteristics of financial reporting....................................................7

Conclusions and Recommendations................................................................................................7

References........................................................................................................................................9

List of Appendix............................................................................................................................10

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................6

Adherence with enhancing characteristics of financial reporting....................................................7

Conclusions and Recommendations................................................................................................7

References........................................................................................................................................9

List of Appendix............................................................................................................................10

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Newcrest is identified as one of the largest producers of gold as per the Australian

Security exchange and recognised as world’s largest gold mining company. The main mission of

the company has been seen with the various types of services which have been seen to be related

to developing, finding and operation as one of the pioneers in gold/copper mines. Some of the

most noted mines of the company have been seen to be located in areas such as “Cadia Valley

Operations (New South Wales, Australia), Telfer (Western Australia), Gosowong (Halmahera

Island, Indonesia), Lihir (New Ireland Province, PNG) and Bonikro” (Côte d’Ivoire) (Milnes et

al. 2015).

The important aspects of the study is identified with the factors which has been seen to be

related to ascertain whether the Newcrest Limited is able to meet the objectives of the conceptual

framework with its reporting. The study also able to assesses the recognition criteria to report

Assets, Liabilities, Equity, Revenue and Expenses. Some of the other aspects of the study have

been also able to present fundamental qualitative enhancing features of financial reporting and

discern the enhancing features of financial reporting (Lukasiewicz et al. 2013).

Adherence to the objectives of the conceptual framework with its reporting

The company is seen to act in accordance with corporate governance framework

complying with CG “Principles and Recommendations (3rd edition)” published as per “ASX

Corporate Governance Council”. The information provided as per the Newcrest’s governance

framework has been seen to be provided with the Corporate Governance Statement which has

been seen to be lodged as per ASX lodgement date and compliance with the relevant practices.

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Newcrest is identified as one of the largest producers of gold as per the Australian

Security exchange and recognised as world’s largest gold mining company. The main mission of

the company has been seen with the various types of services which have been seen to be related

to developing, finding and operation as one of the pioneers in gold/copper mines. Some of the

most noted mines of the company have been seen to be located in areas such as “Cadia Valley

Operations (New South Wales, Australia), Telfer (Western Australia), Gosowong (Halmahera

Island, Indonesia), Lihir (New Ireland Province, PNG) and Bonikro” (Côte d’Ivoire) (Milnes et

al. 2015).

The important aspects of the study is identified with the factors which has been seen to be

related to ascertain whether the Newcrest Limited is able to meet the objectives of the conceptual

framework with its reporting. The study also able to assesses the recognition criteria to report

Assets, Liabilities, Equity, Revenue and Expenses. Some of the other aspects of the study have

been also able to present fundamental qualitative enhancing features of financial reporting and

discern the enhancing features of financial reporting (Lukasiewicz et al. 2013).

Adherence to the objectives of the conceptual framework with its reporting

The company is seen to act in accordance with corporate governance framework

complying with CG “Principles and Recommendations (3rd edition)” published as per “ASX

Corporate Governance Council”. The information provided as per the Newcrest’s governance

framework has been seen to be provided with the Corporate Governance Statement which has

been seen to be lodged as per ASX lodgement date and compliance with the relevant practices.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CONTEMPORARY ISSUES IN ACCOUNTING

The relevant factors may be seen with the limited to the changes in the commodity prices. Some

of the other relevant factors which has been seen with general economic conditions and projected

nature of examination and project expansion containing the risks of attaining the important

licenses and permits along with regulatory framework in terms of retaining of personnel,

industrial relations issues and lawsuit (Frühling 2014).

There have been several numbers of jurisdictions where Newcrest has been seen with the

various types of the interest which are associated to the increasingly composite change and

becoming more onerous. The report has further aimed to link the executive remuneration

framework of Newcrest with the appropriate strategy and performance (Wiewiora et al. 2013).

The framework for the executive remuneration has been seen to be conducive with Changes in

STI Measures. Some of the core form of the other changes has been further seen to be based on

deviations in the “LTI measures and vesting schedules”. The various types of the considerations

for the remuneration framework has been identified with fully informing the stakeholders about

the governance and compliance practices. Organisational and workforce diversity is created on

the various types of elements which have been seen to be linked to the detailed risk management

and the internal control framework (Kingsley et al. 2013).

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The “Return on Capital Employed (ROCE)” is seen as the divergence of the average

capital employed among the shareholder’s equity. The representation of the fair value rights has

been considered with the agreement with the “Australian Accounting Standard AASB 2 Share

Based Payments”. Based on the assessment of the annual report it has been further discerned that

CONTEMPORARY ISSUES IN ACCOUNTING

The relevant factors may be seen with the limited to the changes in the commodity prices. Some

of the other relevant factors which has been seen with general economic conditions and projected

nature of examination and project expansion containing the risks of attaining the important

licenses and permits along with regulatory framework in terms of retaining of personnel,

industrial relations issues and lawsuit (Frühling 2014).

There have been several numbers of jurisdictions where Newcrest has been seen with the

various types of the interest which are associated to the increasingly composite change and

becoming more onerous. The report has further aimed to link the executive remuneration

framework of Newcrest with the appropriate strategy and performance (Wiewiora et al. 2013).

The framework for the executive remuneration has been seen to be conducive with Changes in

STI Measures. Some of the core form of the other changes has been further seen to be based on

deviations in the “LTI measures and vesting schedules”. The various types of the considerations

for the remuneration framework has been identified with fully informing the stakeholders about

the governance and compliance practices. Organisational and workforce diversity is created on

the various types of elements which have been seen to be linked to the detailed risk management

and the internal control framework (Kingsley et al. 2013).

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The “Return on Capital Employed (ROCE)” is seen as the divergence of the average

capital employed among the shareholder’s equity. The representation of the fair value rights has

been considered with the agreement with the “Australian Accounting Standard AASB 2 Share

Based Payments”. Based on the assessment of the annual report it has been further discerned that

5

CONTEMPORARY ISSUES IN ACCOUNTING

the company has been able to prepare financial report as per profit for entity and in agreement

with the “Corporations Act 2001” and “Australian Accounting Standards” and other

“authoritative pronouncements of the Australian Accounting Standards Board (AASB)”. The

recognition of the Assets, Liabilities, Equity, Revenue and Expenses along with the profit for

entity has been prepared with “International Financial Reporting Standards (IFRS)”, which is

interpreted with “International Accounting Standards Board (IASB)”. The numerous

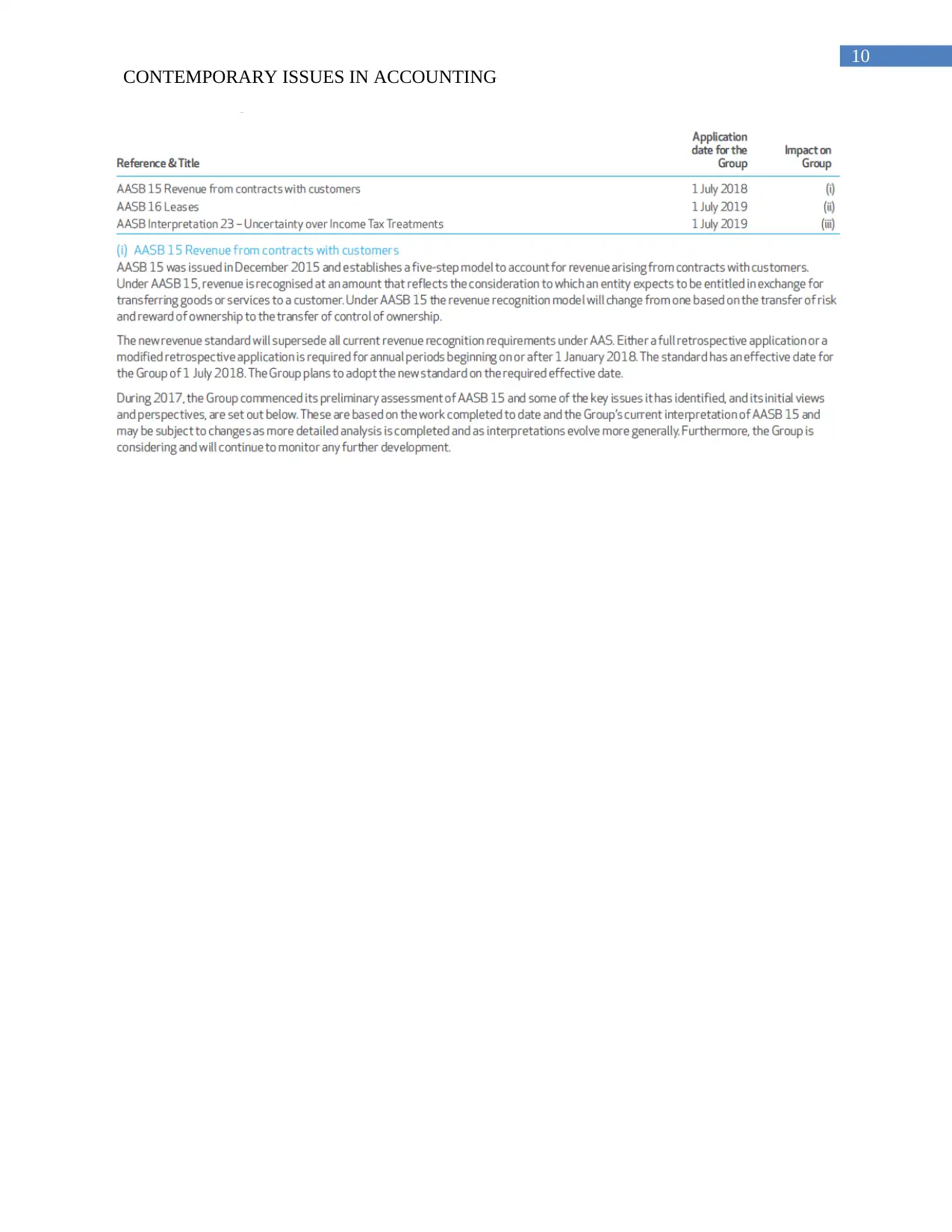

considerations are taken into account with “AASB 15 Revenue from contracts with customers”,

“AASB 16 Leases” and “AASB Interpretation 23 – Uncertainty over Income Tax Treatments 1

July”. The issue of “AASB 15 Revenue from contracts with customers” in December 2015 has

been seen to be established with a five step model and account for the number of factors which

his seen to be associated to the contracts taken from the customers (Fielding 2015). The

introduction of “AASB 16 Leases” has been able to introduce “single lessee accounting model”.

The interpretation of the AASB 23 has been seen to account for the income tax treatments and

also consider the ambiguity that affects the application of “AASB 112 Income Taxes”. The main

form of the Interpretation does not consider the duties or levies outside the scope of “AABS

112”. This has been seen to be based on requirements as per interest and penalties associated

with indefinite tax treatments. The early adoption of the accounting standard has been further

discerned with bookkeeping standard “AASB 9 Financial Instruments” in the previous financial

year. The representation of the “fair value of the Rights, comprising Rights over unissued shares,

granted under the LTI Plan” has been seen to be included with the calculation as per “Australian

Accounting Standard AASB 2 Share Based Payments”. The granted rights in 2017 have been

seen to be value as per the “non-IFRS” financial procedures throughout the annual report. The

non-IFRS information has been further seen to be taken onto consideration with financial

CONTEMPORARY ISSUES IN ACCOUNTING

the company has been able to prepare financial report as per profit for entity and in agreement

with the “Corporations Act 2001” and “Australian Accounting Standards” and other

“authoritative pronouncements of the Australian Accounting Standards Board (AASB)”. The

recognition of the Assets, Liabilities, Equity, Revenue and Expenses along with the profit for

entity has been prepared with “International Financial Reporting Standards (IFRS)”, which is

interpreted with “International Accounting Standards Board (IASB)”. The numerous

considerations are taken into account with “AASB 15 Revenue from contracts with customers”,

“AASB 16 Leases” and “AASB Interpretation 23 – Uncertainty over Income Tax Treatments 1

July”. The issue of “AASB 15 Revenue from contracts with customers” in December 2015 has

been seen to be established with a five step model and account for the number of factors which

his seen to be associated to the contracts taken from the customers (Fielding 2015). The

introduction of “AASB 16 Leases” has been able to introduce “single lessee accounting model”.

The interpretation of the AASB 23 has been seen to account for the income tax treatments and

also consider the ambiguity that affects the application of “AASB 112 Income Taxes”. The main

form of the Interpretation does not consider the duties or levies outside the scope of “AABS

112”. This has been seen to be based on requirements as per interest and penalties associated

with indefinite tax treatments. The early adoption of the accounting standard has been further

discerned with bookkeeping standard “AASB 9 Financial Instruments” in the previous financial

year. The representation of the “fair value of the Rights, comprising Rights over unissued shares,

granted under the LTI Plan” has been seen to be included with the calculation as per “Australian

Accounting Standard AASB 2 Share Based Payments”. The granted rights in 2017 have been

seen to be value as per the “non-IFRS” financial procedures throughout the annual report. The

non-IFRS information has been further seen to be taken onto consideration with financial

6

CONTEMPORARY ISSUES IN ACCOUNTING

information as per the review of the financial review of the non-IFRS financial information. The

different types of the explanations and the reconciliations for the non-IFRS financial information

for the computation reporting Assets, Liabilities, Equity, Revenue and Expenses has been further

seen to be encompassed in Section 6 of the financial and operating review (Troy and Walsh

2013).

Adherence with the qualitative enhancing characteristics of financial reporting

The consideration of the Newcrest’s economic metrics has improved considerably

improved in the last 3 years and led to put the company in a strong profitable position and the

capability to fund immediate term options for growth. The dividend policy of Newcrest has been

further considered on the option which has been seen to be associated to the ability to fund in the

near term growth options (Shah and Jarzabkowski 2013). The board has been further able to

announce the dividends as per the 12 months summing up to US 15 cents per share. Newcrest

looks has been seen with the payment of ordinary level of dividends as per the containing

balance of the financial performance and capital commitment has been discerned with careful

leverage and gearing level for the corporation (Hollis et al. 2015).

Adherence with enhancing characteristics of financial reporting

The enhancing of the ordinary dividends has been seen to be associated with the

consideration of the ordinary dividends. As per going forward Newcrest targeting of the total

annual dividend payment with least amount 10-30% as per free cash flow generated in the

particular financial year and seen to be less than US 15c for each share on a full year basis.

Based on the enhancing characteristics it has been discerned that the company has been able to

CONTEMPORARY ISSUES IN ACCOUNTING

information as per the review of the financial review of the non-IFRS financial information. The

different types of the explanations and the reconciliations for the non-IFRS financial information

for the computation reporting Assets, Liabilities, Equity, Revenue and Expenses has been further

seen to be encompassed in Section 6 of the financial and operating review (Troy and Walsh

2013).

Adherence with the qualitative enhancing characteristics of financial reporting

The consideration of the Newcrest’s economic metrics has improved considerably

improved in the last 3 years and led to put the company in a strong profitable position and the

capability to fund immediate term options for growth. The dividend policy of Newcrest has been

further considered on the option which has been seen to be associated to the ability to fund in the

near term growth options (Shah and Jarzabkowski 2013). The board has been further able to

announce the dividends as per the 12 months summing up to US 15 cents per share. Newcrest

looks has been seen with the payment of ordinary level of dividends as per the containing

balance of the financial performance and capital commitment has been discerned with careful

leverage and gearing level for the corporation (Hollis et al. 2015).

Adherence with enhancing characteristics of financial reporting

The enhancing of the ordinary dividends has been seen to be associated with the

consideration of the ordinary dividends. As per going forward Newcrest targeting of the total

annual dividend payment with least amount 10-30% as per free cash flow generated in the

particular financial year and seen to be less than US 15c for each share on a full year basis.

Based on the enhancing characteristics it has been discerned that the company has been able to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

significant factors which has been related to increasing leverage ratio of “1.1x and gearing ratio

of 16.6%” (Department of Natural Resources 2013).

Conclusions and Recommendations

As per the various consideration of the study it has been discerned that the adherence to

the objectives of the conceptual framework with its reporting has been seen that Newcrest is seen

to comply with CG framework complying with “Corporate Governance Principles” and

Recommendations (3rd edition) published as per “ASX Corporate Governance Council”. The

recognition of the Assets, Liabilities, Equity, Revenue and Expenses along with the profit for

entity has been prepared with “International Financial Reporting Standards (IFRS)”, is

interpreted with “International Accounting Standards Board (IASB)”. The financial report is

prepared based on the various types of the considerations further seen to be based on “AASB 15

Revenue from contracts with customers”, “AASB 16 Leases” and “AASB Interpretation 23 –

Uncertainty over Income Tax Treatments 1 July”. “Newcrest’s financial metrics” has enhanced

considerably improved in the last three years and led to put the company in a strong profitable

position and the capability to fund near term options for growth. The dividend policy of

Newcrest is seen with the option which are associated to the ability to fund in the near-term

growth options.

CONTEMPORARY ISSUES IN ACCOUNTING

significant factors which has been related to increasing leverage ratio of “1.1x and gearing ratio

of 16.6%” (Department of Natural Resources 2013).

Conclusions and Recommendations

As per the various consideration of the study it has been discerned that the adherence to

the objectives of the conceptual framework with its reporting has been seen that Newcrest is seen

to comply with CG framework complying with “Corporate Governance Principles” and

Recommendations (3rd edition) published as per “ASX Corporate Governance Council”. The

recognition of the Assets, Liabilities, Equity, Revenue and Expenses along with the profit for

entity has been prepared with “International Financial Reporting Standards (IFRS)”, is

interpreted with “International Accounting Standards Board (IASB)”. The financial report is

prepared based on the various types of the considerations further seen to be based on “AASB 15

Revenue from contracts with customers”, “AASB 16 Leases” and “AASB Interpretation 23 –

Uncertainty over Income Tax Treatments 1 July”. “Newcrest’s financial metrics” has enhanced

considerably improved in the last three years and led to put the company in a strong profitable

position and the capability to fund near term options for growth. The dividend policy of

Newcrest is seen with the option which are associated to the ability to fund in the near-term

growth options.

8

CONTEMPORARY ISSUES IN ACCOUNTING

References

Department of Natural Resources, Q. (2013) ‘Geological framework North Australian Craton’,

Queensland Minerals.

Fielding, R. (2015) Multilingualism in the Australian suburbs: A framework for exploring

bilingual identity, Multilingualism in the Australian Suburbs: A Framework for Exploring

Bilingual Identity. doi: 10.1007/978-981-287-453-5.

Frühling, S. (2014) ‘Australian defence policy and the concept of self-reliance’, Australian

Journal of International Affairs, 68(5), pp. 531–547. doi: 10.1080/10357718.2014.899310.

Hollis, J. J., Gould, J. S., Cruz, M. G. and McCaw, W. L. (2015) ‘Framework for an Australian

fuel classification to support bushfire management’, Australian Forestry, pp. 1–17. doi:

10.1080/00049158.2014.999186.

Kingsley, J., Townsend, M., Henderson-Wilson, C. and Bolam, B. (2013) ‘Developing an

exploratory framework linking australian aboriginal peoples’ connection to country and concepts

of wellbeing’, International Journal of Environmental Research and Public Health, 10(2), pp.

678–698. doi: 10.3390/ijerph10020678.

Lukasiewicz, A., Bowmer, K., Syme, G. J. and Davidson, P. (2013) ‘Assessing Government

Intentions for Australian Water Reform Using a Social Justice Framework’, Society and Natural

Resources, 26(11), pp. 1314–1329. doi: 10.1080/08941920.2013.791903.

Milnes, S., Orford, N. R., Berkeley, L., Lambert, N., Simpson, N., Elderkin, T., Corke, C. and

Bailey, M. (2015) ‘A prospective observational study of prevalence and outcomes of patients

with Gold Standard Framework criteria in a tertiary regional Australian Hospital’, BMJ

Supportive & Palliative Care, p. bmjspcare-2015-000864. doi: 10.1136/bmjspcare-2015-000864.

Shah, M. and Jarzabkowski, L. (2013) ‘The Australian higher education quality assurance

framework’, Perspectives: Policy and Practice in Higher Education, 17(3), pp. 96–106. doi:

10.1080/13603108.2013.794168.

Troy, J. and Walsh, M. (2013) ‘Embracing Babel: The “Framework for Australian Languages”’,

Babel, 48(2/3), pp. 14–19.

Wiewiora, A., Trigunarsyah, B., Murphy, G. and Coffey, V. (2013) ‘Organizational culture and

willingness to share knowledge: A competing values perspective in Australian context’,

International Journal of Project Management, 31(8), pp. 1163–1174. doi:

10.1016/j.ijproman.2012.12.014.

CONTEMPORARY ISSUES IN ACCOUNTING

References

Department of Natural Resources, Q. (2013) ‘Geological framework North Australian Craton’,

Queensland Minerals.

Fielding, R. (2015) Multilingualism in the Australian suburbs: A framework for exploring

bilingual identity, Multilingualism in the Australian Suburbs: A Framework for Exploring

Bilingual Identity. doi: 10.1007/978-981-287-453-5.

Frühling, S. (2014) ‘Australian defence policy and the concept of self-reliance’, Australian

Journal of International Affairs, 68(5), pp. 531–547. doi: 10.1080/10357718.2014.899310.

Hollis, J. J., Gould, J. S., Cruz, M. G. and McCaw, W. L. (2015) ‘Framework for an Australian

fuel classification to support bushfire management’, Australian Forestry, pp. 1–17. doi:

10.1080/00049158.2014.999186.

Kingsley, J., Townsend, M., Henderson-Wilson, C. and Bolam, B. (2013) ‘Developing an

exploratory framework linking australian aboriginal peoples’ connection to country and concepts

of wellbeing’, International Journal of Environmental Research and Public Health, 10(2), pp.

678–698. doi: 10.3390/ijerph10020678.

Lukasiewicz, A., Bowmer, K., Syme, G. J. and Davidson, P. (2013) ‘Assessing Government

Intentions for Australian Water Reform Using a Social Justice Framework’, Society and Natural

Resources, 26(11), pp. 1314–1329. doi: 10.1080/08941920.2013.791903.

Milnes, S., Orford, N. R., Berkeley, L., Lambert, N., Simpson, N., Elderkin, T., Corke, C. and

Bailey, M. (2015) ‘A prospective observational study of prevalence and outcomes of patients

with Gold Standard Framework criteria in a tertiary regional Australian Hospital’, BMJ

Supportive & Palliative Care, p. bmjspcare-2015-000864. doi: 10.1136/bmjspcare-2015-000864.

Shah, M. and Jarzabkowski, L. (2013) ‘The Australian higher education quality assurance

framework’, Perspectives: Policy and Practice in Higher Education, 17(3), pp. 96–106. doi:

10.1080/13603108.2013.794168.

Troy, J. and Walsh, M. (2013) ‘Embracing Babel: The “Framework for Australian Languages”’,

Babel, 48(2/3), pp. 14–19.

Wiewiora, A., Trigunarsyah, B., Murphy, G. and Coffey, V. (2013) ‘Organizational culture and

willingness to share knowledge: A competing values perspective in Australian context’,

International Journal of Project Management, 31(8), pp. 1163–1174. doi:

10.1016/j.ijproman.2012.12.014.

9

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

11

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.