Corporate Finance Assignment - [University Name], [Course Name]

VerifiedAdded on 2020/04/13

|11

|2000

|324

Homework Assignment

AI Summary

This document provides a comprehensive solution to a corporate finance assignment, addressing key concepts such as managerial flexibility, capital budgeting techniques, and real options. It analyzes different methods of shareholder wealth distribution, including extra dividends and share repurchases, and offers insights into the Modigliani and Miller theory of capital structure. The assignment also explores futures contracts, rights issuance, and the implications of debt financing on a company's risk and value. The solution includes detailed explanations, calculations, and advantages and disadvantages of different financial strategies. The assignment also discusses the differences between short-term and long-term debt securities and the factors affecting future prices.

CORPORATE FINANCE

ASSIGNMENT

[Pick the date]

STUDENT ID & NAME

ASSIGNMENT

[Pick the date]

STUDENT ID & NAME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The term managerial flexibility refers to the ability of the management to modify or change

decisions as there is material change in the market scenario or environmental factors thereby

impacting the underlying decision. This is quite imperative in the modern business world where

there is plethora of factors that tend to impact a given decision and most of these tend to quite

dynamic making the underlying decision highly sensitive to these changes (Lasher, 2007).

For evaluation of a given project, managerial flexibility becomes important as the presence of the

same would lead to decision making being superior along with improved returns on investment

in comparison with peer group players. The valuation techniques that are commonly endorsed in

capital budgeting are static and based on the future cash flows which can essentially alter in a

manner which might not have been foreseen before. This potentially can have significant

implications for a given project and thereby it is imperative that real options be inserted whereby

even after commencement of the project management can either abandon or step up the capacity

based on the underlying environment. It is imperative to ascertain the impact of these options in

the traditional capital budgeting tools so as to make a prudent decision maximizing the wealth of

the shareholders (Damodaran, 2010).

Question 2

a) The two options to be discussed are highlighted below.

Extra Dividend

Extra dividend on each share = Total amount to be given as dividend / Outstanding Shares =

13325/5125 = $ 2.6

Since neither earnings change nor outstanding shares, hence EPS alteration does not take place.

But the distribution of the dividend would lead to incremental shareholder wealth of $ 13325 as

dividend income.

Share Repurchase

1

The term managerial flexibility refers to the ability of the management to modify or change

decisions as there is material change in the market scenario or environmental factors thereby

impacting the underlying decision. This is quite imperative in the modern business world where

there is plethora of factors that tend to impact a given decision and most of these tend to quite

dynamic making the underlying decision highly sensitive to these changes (Lasher, 2007).

For evaluation of a given project, managerial flexibility becomes important as the presence of the

same would lead to decision making being superior along with improved returns on investment

in comparison with peer group players. The valuation techniques that are commonly endorsed in

capital budgeting are static and based on the future cash flows which can essentially alter in a

manner which might not have been foreseen before. This potentially can have significant

implications for a given project and thereby it is imperative that real options be inserted whereby

even after commencement of the project management can either abandon or step up the capacity

based on the underlying environment. It is imperative to ascertain the impact of these options in

the traditional capital budgeting tools so as to make a prudent decision maximizing the wealth of

the shareholders (Damodaran, 2010).

Question 2

a) The two options to be discussed are highlighted below.

Extra Dividend

Extra dividend on each share = Total amount to be given as dividend / Outstanding Shares =

13325/5125 = $ 2.6

Since neither earnings change nor outstanding shares, hence EPS alteration does not take place.

But the distribution of the dividend would lead to incremental shareholder wealth of $ 13325 as

dividend income.

Share Repurchase

1

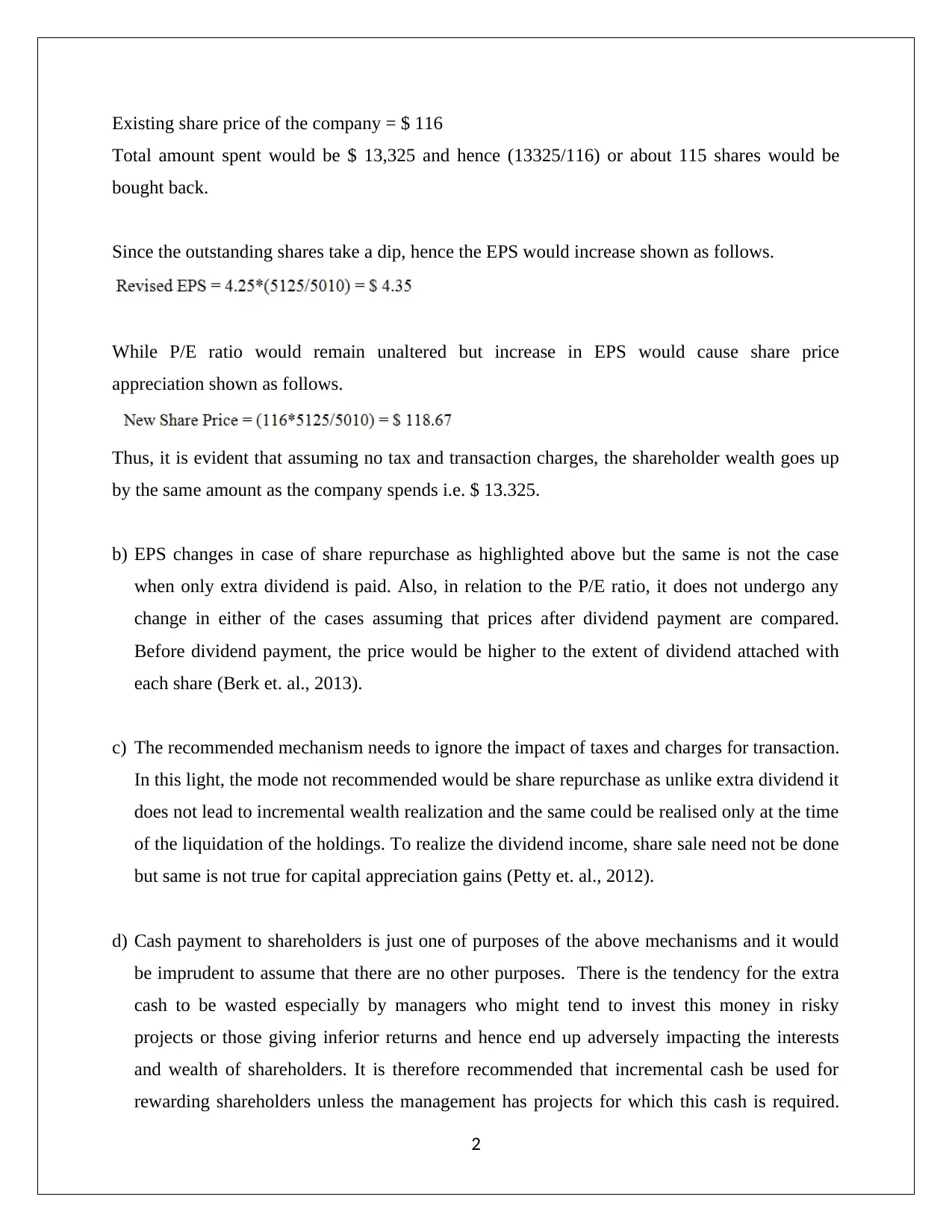

Existing share price of the company = $ 116

Total amount spent would be $ 13,325 and hence (13325/116) or about 115 shares would be

bought back.

Since the outstanding shares take a dip, hence the EPS would increase shown as follows.

While P/E ratio would remain unaltered but increase in EPS would cause share price

appreciation shown as follows.

Thus, it is evident that assuming no tax and transaction charges, the shareholder wealth goes up

by the same amount as the company spends i.e. $ 13.325.

b) EPS changes in case of share repurchase as highlighted above but the same is not the case

when only extra dividend is paid. Also, in relation to the P/E ratio, it does not undergo any

change in either of the cases assuming that prices after dividend payment are compared.

Before dividend payment, the price would be higher to the extent of dividend attached with

each share (Berk et. al., 2013).

c) The recommended mechanism needs to ignore the impact of taxes and charges for transaction.

In this light, the mode not recommended would be share repurchase as unlike extra dividend it

does not lead to incremental wealth realization and the same could be realised only at the time

of the liquidation of the holdings. To realize the dividend income, share sale need not be done

but same is not true for capital appreciation gains (Petty et. al., 2012).

d) Cash payment to shareholders is just one of purposes of the above mechanisms and it would

be imprudent to assume that there are no other purposes. There is the tendency for the extra

cash to be wasted especially by managers who might tend to invest this money in risky

projects or those giving inferior returns and hence end up adversely impacting the interests

and wealth of shareholders. It is therefore recommended that incremental cash be used for

rewarding shareholders unless the management has projects for which this cash is required.

2

Total amount spent would be $ 13,325 and hence (13325/116) or about 115 shares would be

bought back.

Since the outstanding shares take a dip, hence the EPS would increase shown as follows.

While P/E ratio would remain unaltered but increase in EPS would cause share price

appreciation shown as follows.

Thus, it is evident that assuming no tax and transaction charges, the shareholder wealth goes up

by the same amount as the company spends i.e. $ 13.325.

b) EPS changes in case of share repurchase as highlighted above but the same is not the case

when only extra dividend is paid. Also, in relation to the P/E ratio, it does not undergo any

change in either of the cases assuming that prices after dividend payment are compared.

Before dividend payment, the price would be higher to the extent of dividend attached with

each share (Berk et. al., 2013).

c) The recommended mechanism needs to ignore the impact of taxes and charges for transaction.

In this light, the mode not recommended would be share repurchase as unlike extra dividend it

does not lead to incremental wealth realization and the same could be realised only at the time

of the liquidation of the holdings. To realize the dividend income, share sale need not be done

but same is not true for capital appreciation gains (Petty et. al., 2012).

d) Cash payment to shareholders is just one of purposes of the above mechanisms and it would

be imprudent to assume that there are no other purposes. There is the tendency for the extra

cash to be wasted especially by managers who might tend to invest this money in risky

projects or those giving inferior returns and hence end up adversely impacting the interests

and wealth of shareholders. It is therefore recommended that incremental cash be used for

rewarding shareholders unless the management has projects for which this cash is required.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Also, taking these measures in the interest of the shareholders also leads to an opinion that the

management is investor friendly (Brealey and Myers, 2007).

Question 3

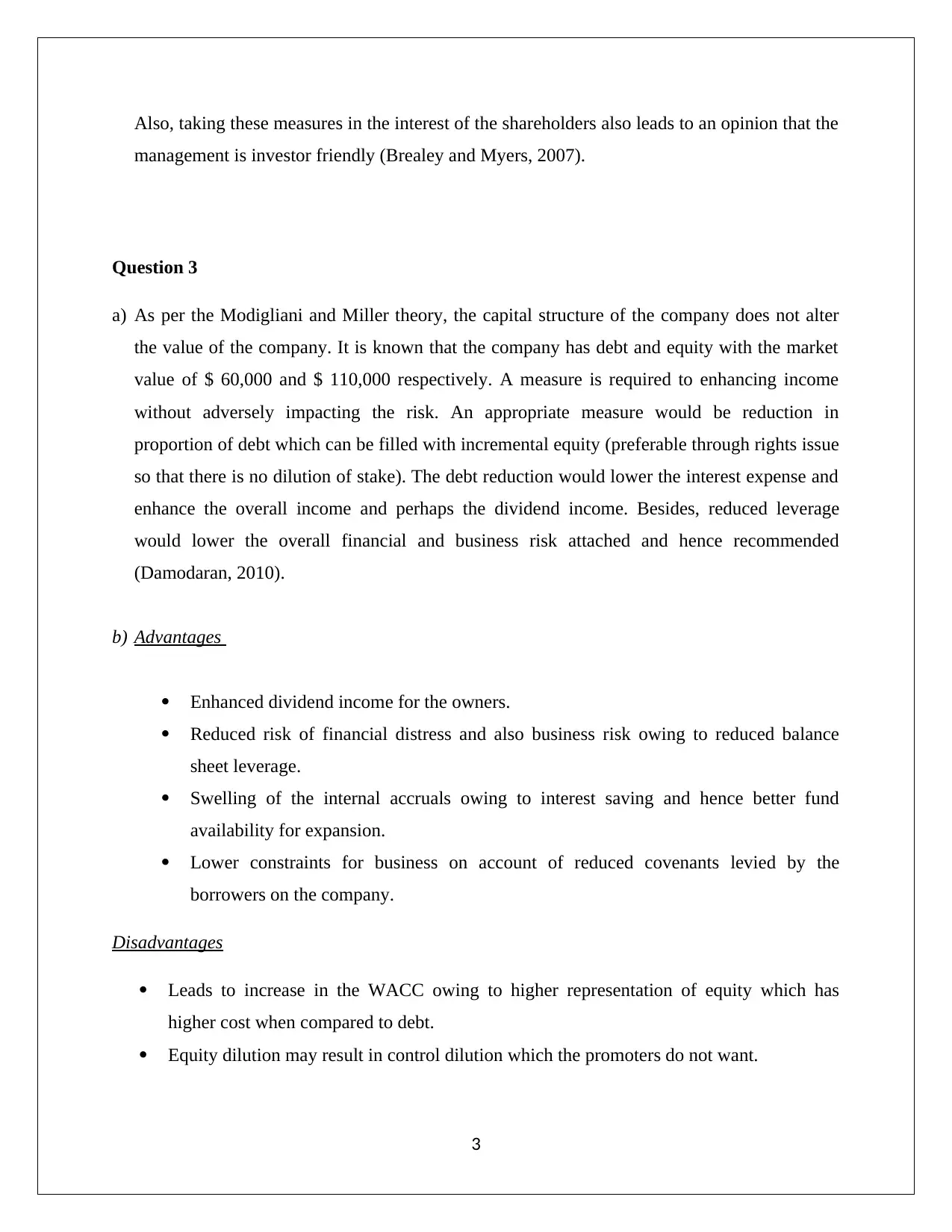

a) As per the Modigliani and Miller theory, the capital structure of the company does not alter

the value of the company. It is known that the company has debt and equity with the market

value of $ 60,000 and $ 110,000 respectively. A measure is required to enhancing income

without adversely impacting the risk. An appropriate measure would be reduction in

proportion of debt which can be filled with incremental equity (preferable through rights issue

so that there is no dilution of stake). The debt reduction would lower the interest expense and

enhance the overall income and perhaps the dividend income. Besides, reduced leverage

would lower the overall financial and business risk attached and hence recommended

(Damodaran, 2010).

b) Advantages

Enhanced dividend income for the owners.

Reduced risk of financial distress and also business risk owing to reduced balance

sheet leverage.

Swelling of the internal accruals owing to interest saving and hence better fund

availability for expansion.

Lower constraints for business on account of reduced covenants levied by the

borrowers on the company.

Disadvantages

Leads to increase in the WACC owing to higher representation of equity which has

higher cost when compared to debt.

Equity dilution may result in control dilution which the promoters do not want.

3

management is investor friendly (Brealey and Myers, 2007).

Question 3

a) As per the Modigliani and Miller theory, the capital structure of the company does not alter

the value of the company. It is known that the company has debt and equity with the market

value of $ 60,000 and $ 110,000 respectively. A measure is required to enhancing income

without adversely impacting the risk. An appropriate measure would be reduction in

proportion of debt which can be filled with incremental equity (preferable through rights issue

so that there is no dilution of stake). The debt reduction would lower the interest expense and

enhance the overall income and perhaps the dividend income. Besides, reduced leverage

would lower the overall financial and business risk attached and hence recommended

(Damodaran, 2010).

b) Advantages

Enhanced dividend income for the owners.

Reduced risk of financial distress and also business risk owing to reduced balance

sheet leverage.

Swelling of the internal accruals owing to interest saving and hence better fund

availability for expansion.

Lower constraints for business on account of reduced covenants levied by the

borrowers on the company.

Disadvantages

Leads to increase in the WACC owing to higher representation of equity which has

higher cost when compared to debt.

Equity dilution may result in control dilution which the promoters do not want.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The tax savings reaped due to the interest expense would be adversely impacted leading

to higher tax expense as a proportion of revenue.

Increased shares would lead to reduction in EPS and hence lower the company share

price.

Question 4

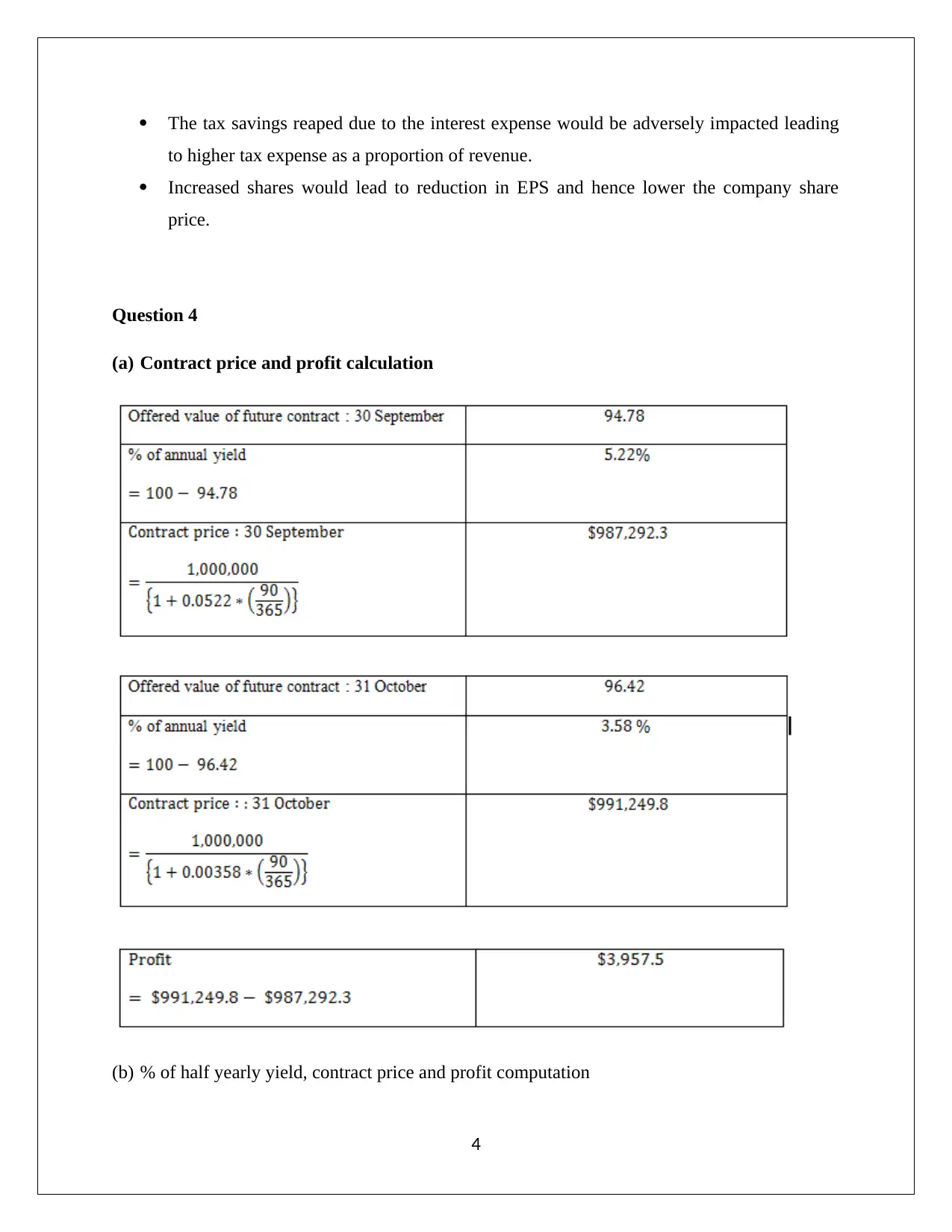

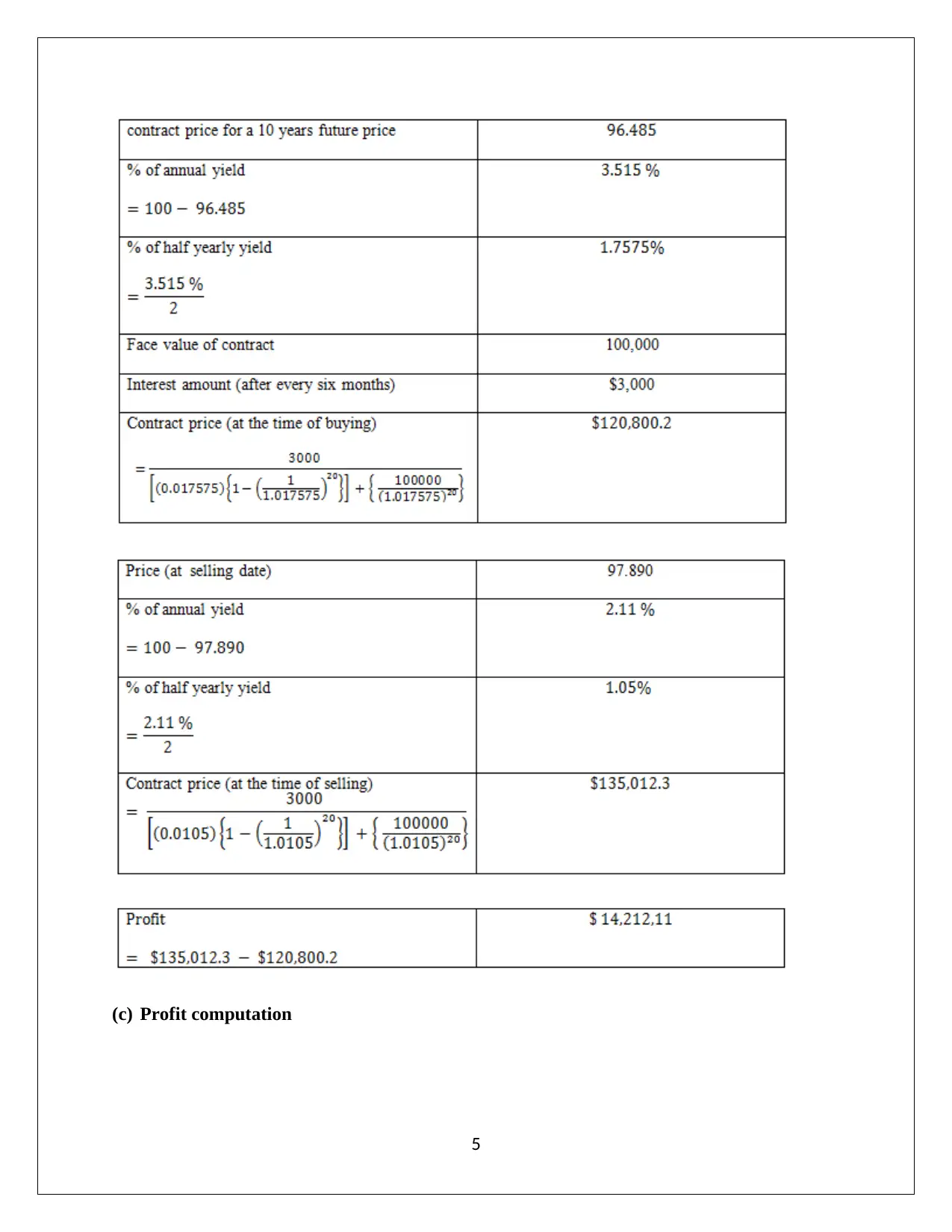

(a) Contract price and profit calculation

(b) % of half yearly yield, contract price and profit computation

4

to higher tax expense as a proportion of revenue.

Increased shares would lead to reduction in EPS and hence lower the company share

price.

Question 4

(a) Contract price and profit calculation

(b) % of half yearly yield, contract price and profit computation

4

(c) Profit computation

5

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

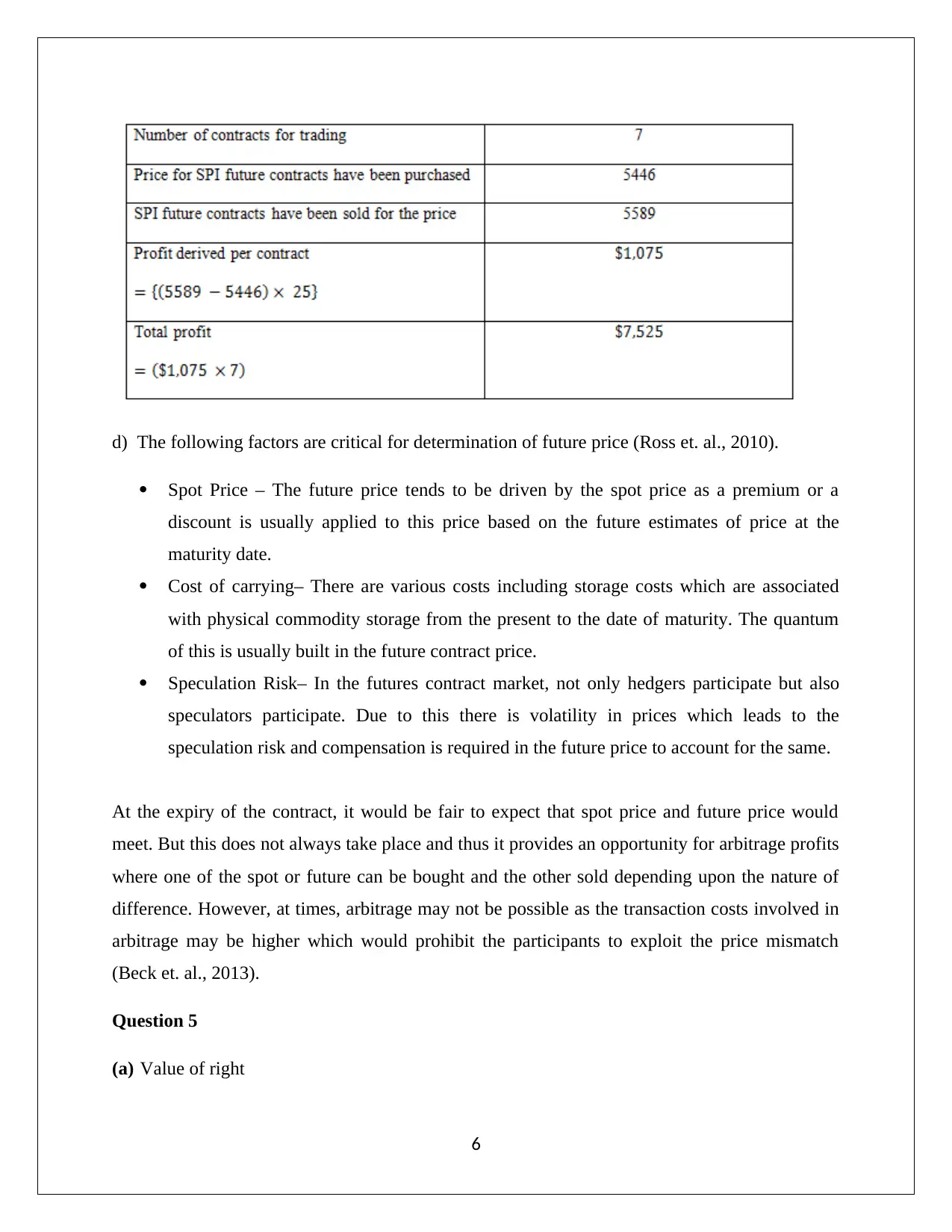

d) The following factors are critical for determination of future price (Ross et. al., 2010).

Spot Price – The future price tends to be driven by the spot price as a premium or a

discount is usually applied to this price based on the future estimates of price at the

maturity date.

Cost of carrying– There are various costs including storage costs which are associated

with physical commodity storage from the present to the date of maturity. The quantum

of this is usually built in the future contract price.

Speculation Risk– In the futures contract market, not only hedgers participate but also

speculators participate. Due to this there is volatility in prices which leads to the

speculation risk and compensation is required in the future price to account for the same.

At the expiry of the contract, it would be fair to expect that spot price and future price would

meet. But this does not always take place and thus it provides an opportunity for arbitrage profits

where one of the spot or future can be bought and the other sold depending upon the nature of

difference. However, at times, arbitrage may not be possible as the transaction costs involved in

arbitrage may be higher which would prohibit the participants to exploit the price mismatch

(Beck et. al., 2013).

Question 5

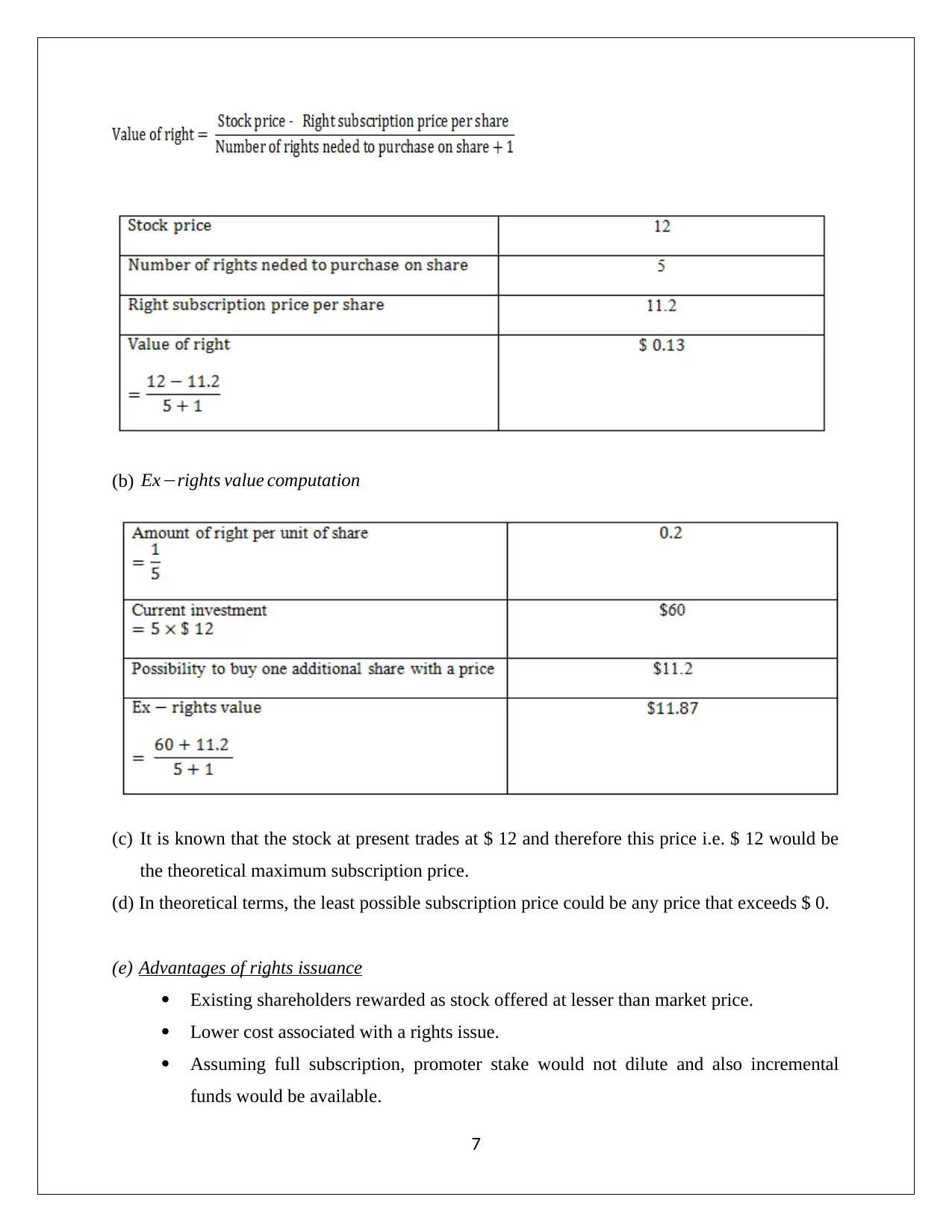

(a) Value of right

6

Spot Price – The future price tends to be driven by the spot price as a premium or a

discount is usually applied to this price based on the future estimates of price at the

maturity date.

Cost of carrying– There are various costs including storage costs which are associated

with physical commodity storage from the present to the date of maturity. The quantum

of this is usually built in the future contract price.

Speculation Risk– In the futures contract market, not only hedgers participate but also

speculators participate. Due to this there is volatility in prices which leads to the

speculation risk and compensation is required in the future price to account for the same.

At the expiry of the contract, it would be fair to expect that spot price and future price would

meet. But this does not always take place and thus it provides an opportunity for arbitrage profits

where one of the spot or future can be bought and the other sold depending upon the nature of

difference. However, at times, arbitrage may not be possible as the transaction costs involved in

arbitrage may be higher which would prohibit the participants to exploit the price mismatch

(Beck et. al., 2013).

Question 5

(a) Value of right

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Ex−rights value computation

(c) It is known that the stock at present trades at $ 12 and therefore this price i.e. $ 12 would be

the theoretical maximum subscription price.

(d) In theoretical terms, the least possible subscription price could be any price that exceeds $ 0.

(e) Advantages of rights issuance

Existing shareholders rewarded as stock offered at lesser than market price.

Lower cost associated with a rights issue.

Assuming full subscription, promoter stake would not dilute and also incremental

funds would be available.

7

(c) It is known that the stock at present trades at $ 12 and therefore this price i.e. $ 12 would be

the theoretical maximum subscription price.

(d) In theoretical terms, the least possible subscription price could be any price that exceeds $ 0.

(e) Advantages of rights issuance

Existing shareholders rewarded as stock offered at lesser than market price.

Lower cost associated with a rights issue.

Assuming full subscription, promoter stake would not dilute and also incremental

funds would be available.

7

Financial risk can be lowered and also the balance sheet could be strengthened on

greater equity.

Disadvantages of rights issuance

Limits on funding that potentially can be availed in this manner.

It leads to a decrease in EPS as the share outstanding increase due to issue of new shares.

May lead to dilution of control if promoters do not fully subscribe to the rights issue.

It is used by companies that have an overleveraged balance sheet to buy some more time

and hence leads to a negative image especially in case of leverage being high.

Rights issuance can potentially lead to enhancement of the value of the firm as it enhances the

overall equity contribution and hence lead to improvement in the various ratios. Thus, it leads to

lower financial and business risk and thereby leads to creation of value (Lasher, 2007).

Question 6

(a) The relevant aspects are highlighted below (Damodaran, 2010).

Risk- Increasing debt proportion leads to higher financial risk due to higher probability of

financial distress. Also, owing to increasing balance sheet leveraging, it is potential that higher

returns may be demanded by the equity holders. Further, periodic obligations for principal

repayments along with interest payments also arise leading to default risk.

Control – With regards to assuming incremental risk, covenants are levied to secure the rights of

the lenders which tend to reduce business flexibility to an extent but the control does not dilute

which tends to arise in equity issuance as voting rights get diluted. Thus, from control

perspective increase debt proportion is preferable.

Intrinsic Value – The exact impact would depend on the debt level originally. If the original debt

proportion was less than the optimal levels, then incremental debt would enhance intrinsic value

or else the intrinsic value would decrease. However, in general debt lowers the WACC and is

positive for intrinsic value assuming debt is not very high.

8

greater equity.

Disadvantages of rights issuance

Limits on funding that potentially can be availed in this manner.

It leads to a decrease in EPS as the share outstanding increase due to issue of new shares.

May lead to dilution of control if promoters do not fully subscribe to the rights issue.

It is used by companies that have an overleveraged balance sheet to buy some more time

and hence leads to a negative image especially in case of leverage being high.

Rights issuance can potentially lead to enhancement of the value of the firm as it enhances the

overall equity contribution and hence lead to improvement in the various ratios. Thus, it leads to

lower financial and business risk and thereby leads to creation of value (Lasher, 2007).

Question 6

(a) The relevant aspects are highlighted below (Damodaran, 2010).

Risk- Increasing debt proportion leads to higher financial risk due to higher probability of

financial distress. Also, owing to increasing balance sheet leveraging, it is potential that higher

returns may be demanded by the equity holders. Further, periodic obligations for principal

repayments along with interest payments also arise leading to default risk.

Control – With regards to assuming incremental risk, covenants are levied to secure the rights of

the lenders which tend to reduce business flexibility to an extent but the control does not dilute

which tends to arise in equity issuance as voting rights get diluted. Thus, from control

perspective increase debt proportion is preferable.

Intrinsic Value – The exact impact would depend on the debt level originally. If the original debt

proportion was less than the optimal levels, then incremental debt would enhance intrinsic value

or else the intrinsic value would decrease. However, in general debt lowers the WACC and is

positive for intrinsic value assuming debt is not very high.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

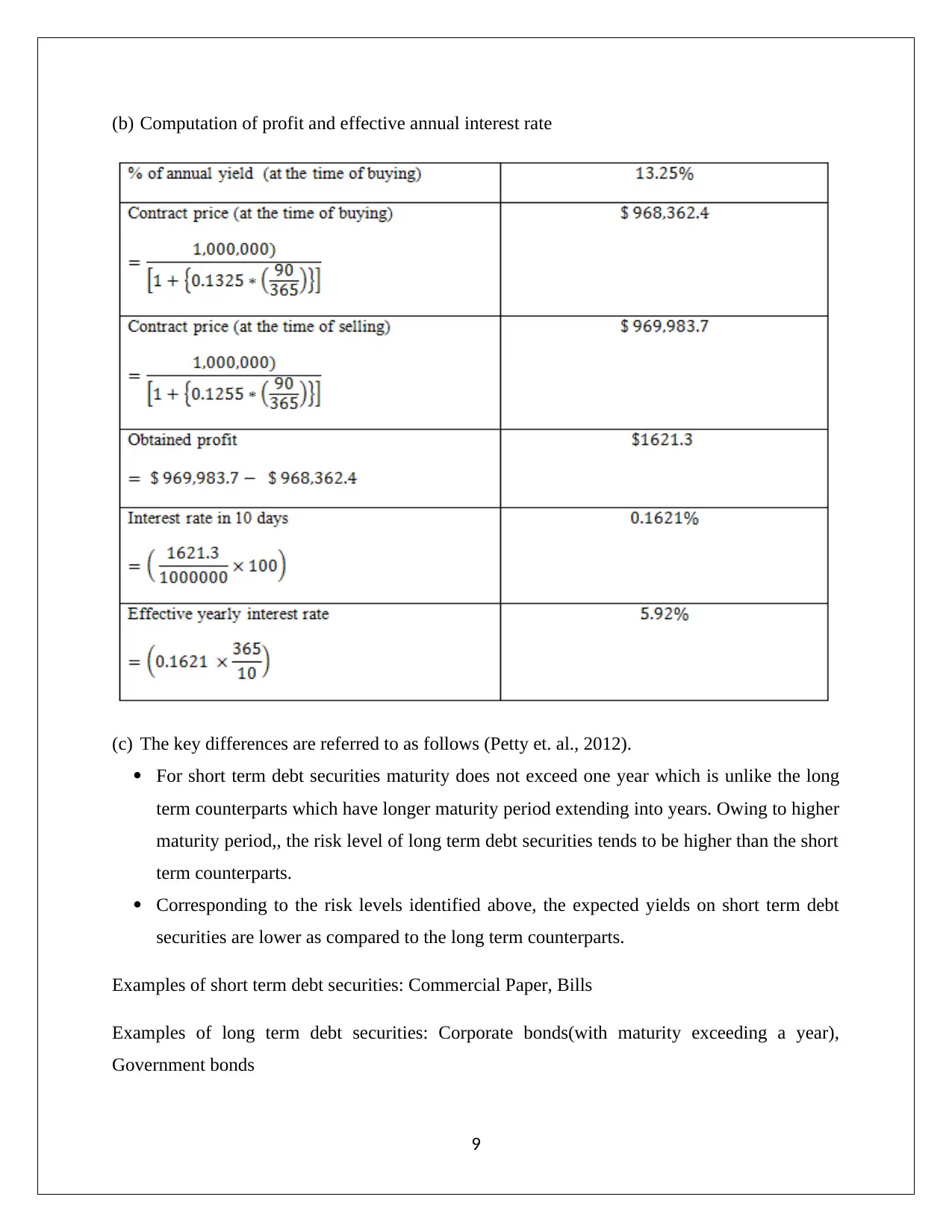

(b) Computation of profit and effective annual interest rate

(c) The key differences are referred to as follows (Petty et. al., 2012).

For short term debt securities maturity does not exceed one year which is unlike the long

term counterparts which have longer maturity period extending into years. Owing to higher

maturity period,, the risk level of long term debt securities tends to be higher than the short

term counterparts.

Corresponding to the risk levels identified above, the expected yields on short term debt

securities are lower as compared to the long term counterparts.

Examples of short term debt securities: Commercial Paper, Bills

Examples of long term debt securities: Corporate bonds(with maturity exceeding a year),

Government bonds

9

(c) The key differences are referred to as follows (Petty et. al., 2012).

For short term debt securities maturity does not exceed one year which is unlike the long

term counterparts which have longer maturity period extending into years. Owing to higher

maturity period,, the risk level of long term debt securities tends to be higher than the short

term counterparts.

Corresponding to the risk levels identified above, the expected yields on short term debt

securities are lower as compared to the long term counterparts.

Examples of short term debt securities: Commercial Paper, Bills

Examples of long term debt securities: Corporate bonds(with maturity exceeding a year),

Government bonds

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2013) Fundamentals of

corporate finance. London: Pearson Higher Education

Brealey, R., and Myers, S., (2007) Principles of Corporate Finance. 9th edn. New York City:

McGraw –Hill.

Damodaran, A. (2010) Applied corporate finance: A user’s manual. 3rd edn. New York: Wiley,

John & Sons.

Lasher, W. R., (2007) Practical Financial Management. 5th edn. London: South- Western

College Publisher

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th edn. NSW: Pearson Education, French

Forest Australia.

Ross,S.A., Tryaler,R., Bird, R.,Westerfield, R.W. and Jorden,B.D. (2010) Essentials of Corporate

Finance. 2nd edn. New York City: McGraw-Hill.

10

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2013) Fundamentals of

corporate finance. London: Pearson Higher Education

Brealey, R., and Myers, S., (2007) Principles of Corporate Finance. 9th edn. New York City:

McGraw –Hill.

Damodaran, A. (2010) Applied corporate finance: A user’s manual. 3rd edn. New York: Wiley,

John & Sons.

Lasher, W. R., (2007) Practical Financial Management. 5th edn. London: South- Western

College Publisher

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th edn. NSW: Pearson Education, French

Forest Australia.

Ross,S.A., Tryaler,R., Bird, R.,Westerfield, R.W. and Jorden,B.D. (2010) Essentials of Corporate

Finance. 2nd edn. New York City: McGraw-Hill.

10

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.