Management Accounting: A Framework

VerifiedAdded on 2020/02/03

|21

|5286

|38

Essay

AI Summary

This assignment delves into the core principles of management accounting, emphasizing its role in strategic decision-making, performance assessment, and risk management. It explores various techniques and tools employed in management accounting, such as cash budgeting, cost analysis, and activity-based costing. The assignment aims to provide a framework for understanding how management accounting contributes to organizational success.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting Systems.........................................................................................1

P2 Methods Used for Management Accounting Reporting........................................................3

TASK 2............................................................................................................................................4

P3 Calculation of Costs and Difference between Marginal and Absorption Costing.................4

TASK 3............................................................................................................................................9

P4 Advantages and Disadvantages of Budgets which is used for Budgetary Control................9

M3 Planning Tools & Forecasting Techniques used in Budget................................................12

P5 Ways Management Accounting can be used to respond to Financial Problems ................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting Systems.........................................................................................1

P2 Methods Used for Management Accounting Reporting........................................................3

TASK 2............................................................................................................................................4

P3 Calculation of Costs and Difference between Marginal and Absorption Costing.................4

TASK 3............................................................................................................................................9

P4 Advantages and Disadvantages of Budgets which is used for Budgetary Control................9

M3 Planning Tools & Forecasting Techniques used in Budget................................................12

P5 Ways Management Accounting can be used to respond to Financial Problems ................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INDEX OF TABLES

Table 1: Calculation of cost of production.....................................................................................6

Table 2: Income Statement As per Marginal Costing......................................................................7

Table 3: Income Statement As per Absorption Costing..................................................................8

Table 4: Sales Budget....................................................................................................................12

Table 1: Calculation of cost of production.....................................................................................6

Table 2: Income Statement As per Marginal Costing......................................................................7

Table 3: Income Statement As per Absorption Costing..................................................................8

Table 4: Sales Budget....................................................................................................................12

ILLUSTRATION INDEX

Illustration 1: Cash budget for organisation...................................................................................11

Illustration 1: Cash budget for organisation...................................................................................11

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management accounting is key in developing a business as a whole. When it is talked

about management accounting, there also some discussions about cost and financial accounting

because they both are the part of management accounting(Bryer, 2013). Managers need to

evaluate the performance of the particular plant considering the performance of various costs

into it then here comes the role of cost accounting in which various costs helps a mangers to

make decisions on the working of the plant. In management accounting recording, classification,

evaluation and interpretation of data take place.

Same is in the case of financial accounting as well here financial matters are discussed so

that managers can strategically use those data and then can make necessary decisions in order to

make fruitful decisions which can impact the company in a positive way. In this report various

management techniques and its implication plus how a management accounting is carried out in

the retail sector is undertaken with point of view of providing an insight on management

accounting practices in an organization(A. Hammad, Jusoh and Ghozali, 2013). The company

taken here is M & S Ltd. which is doing business in retail sector.

TASK 1

P1 Management Accounting Systems

For the purpose of study abc company here is undertaken because as world is moving fast

retail sector is developing too and thus the increase in retail industry practices in the recent times

it is important to take an analysis of the retail management techniques and how they handle the

pressure of decision making and controlling. Since they have to deal every day with lots of

inventory in order to keep attracting customers towards their retail outlets. Thus, different

aspects of management accounting for decision making regarding effective business operations

can understand through this report.

This approach is nothing but the process of evaluating the operations of business of

different departments(A. Hammad, Jusoh and Ghozali, 2013). However, it is considered as a

process for analysing, interpreting and sharing information related to business operations for

used by the managers in due course of the organizational workings. Management accounting is

combination of financial accounting and cost accounting. Though it is some what different from

both of the said accounting. That's why management accounting is more preferred over different

1

Management accounting is key in developing a business as a whole. When it is talked

about management accounting, there also some discussions about cost and financial accounting

because they both are the part of management accounting(Bryer, 2013). Managers need to

evaluate the performance of the particular plant considering the performance of various costs

into it then here comes the role of cost accounting in which various costs helps a mangers to

make decisions on the working of the plant. In management accounting recording, classification,

evaluation and interpretation of data take place.

Same is in the case of financial accounting as well here financial matters are discussed so

that managers can strategically use those data and then can make necessary decisions in order to

make fruitful decisions which can impact the company in a positive way. In this report various

management techniques and its implication plus how a management accounting is carried out in

the retail sector is undertaken with point of view of providing an insight on management

accounting practices in an organization(A. Hammad, Jusoh and Ghozali, 2013). The company

taken here is M & S Ltd. which is doing business in retail sector.

TASK 1

P1 Management Accounting Systems

For the purpose of study abc company here is undertaken because as world is moving fast

retail sector is developing too and thus the increase in retail industry practices in the recent times

it is important to take an analysis of the retail management techniques and how they handle the

pressure of decision making and controlling. Since they have to deal every day with lots of

inventory in order to keep attracting customers towards their retail outlets. Thus, different

aspects of management accounting for decision making regarding effective business operations

can understand through this report.

This approach is nothing but the process of evaluating the operations of business of

different departments(A. Hammad, Jusoh and Ghozali, 2013). However, it is considered as a

process for analysing, interpreting and sharing information related to business operations for

used by the managers in due course of the organizational workings. Management accounting is

combination of financial accounting and cost accounting. Though it is some what different from

both of the said accounting. That's why management accounting is more preferred over different

1

types of accounting. Management accounting has wider coverage area of the organization. This

accounting technique is beneficial to generate ideas for optimum utilization of organizational

resources to support managers in their task and through it the managers wants to enhance both

the customer and shareholder value. Their are different objectives and benefits of management

accounting and they are:

It facilitates Organizational Planning in which selection of best alternatives take place.

M.A used to keep a monitoring and control over the organizational activities.

Performance Measurement is the key towards achieving the vision and mission of the

organization and thus M.A helps in that(Myrelid and Olhager, 2015).

Through management accounting a manager is able to make sound strategies and

decisions.

Management accounting Systems is kind of an information system which facilitate a

manager in making sound decisions and create value for the company. The information provided

in this is based on ad hoc and fulfill both the short-term as well long-term needs of management.

There are different systems which managers take into account for better understanding and they

are:1. Cost Accounting System: abc company have a practice of using this system very often

because in this system the cost of goods and services as well as the cost of different

departments is taken into consideration to know actually how much the expenses are.

This accounting system provides a detailed cost data which helps the management of abc

to control its operations and plan for the future(Du and Taylor, 2013). It is one of the

most effective system to creating balance between production and distribution system of

the organization adequately.2. Inventory Management System: It is one of the main source to manage inventories of the

entity and improving its liquidity position. In this regard, managers analyses all

inventories and further make decisions for its effectiveness. Including this, it also employ

and undertakes this type of system into recording to implement all action plans in proper

time.

2

accounting technique is beneficial to generate ideas for optimum utilization of organizational

resources to support managers in their task and through it the managers wants to enhance both

the customer and shareholder value. Their are different objectives and benefits of management

accounting and they are:

It facilitates Organizational Planning in which selection of best alternatives take place.

M.A used to keep a monitoring and control over the organizational activities.

Performance Measurement is the key towards achieving the vision and mission of the

organization and thus M.A helps in that(Myrelid and Olhager, 2015).

Through management accounting a manager is able to make sound strategies and

decisions.

Management accounting Systems is kind of an information system which facilitate a

manager in making sound decisions and create value for the company. The information provided

in this is based on ad hoc and fulfill both the short-term as well long-term needs of management.

There are different systems which managers take into account for better understanding and they

are:1. Cost Accounting System: abc company have a practice of using this system very often

because in this system the cost of goods and services as well as the cost of different

departments is taken into consideration to know actually how much the expenses are.

This accounting system provides a detailed cost data which helps the management of abc

to control its operations and plan for the future(Du and Taylor, 2013). It is one of the

most effective system to creating balance between production and distribution system of

the organization adequately.2. Inventory Management System: It is one of the main source to manage inventories of the

entity and improving its liquidity position. In this regard, managers analyses all

inventories and further make decisions for its effectiveness. Including this, it also employ

and undertakes this type of system into recording to implement all action plans in proper

time.

2

3. Job-costing Systems: Under this management accounting system, costs incurred for

manufacturing of products are analysed that affects its production effectively. That means

for fulfilling requirements of all customers regarding set of product produced by entity.

Here firstly the customer makes the order as per his liking and then a company prepares

him the product(Ghasemi and et.al, 2016). It is appropriate technique to reach out

customers' expectations and satisfying them with product services provided by

organization.

4. Price-Optimizing Systems: It is best tool for optimizing price and cost effectiveness to

produce goods and services provided by entity (Hopper, 2013). In accordance to this,

several tools are applied for setting price regarding business operations also impacts on

profitability of organisation. In this system different customer groups are taken into

consideration as per their income levels so that pricing decisions can be made as per the

purchasing powers.

P2 Methods Used for Management Accounting Reporting

Management accounting reporting can be understood as the reporting of operations of the

businesses which makes or helps management of organizations to make decisions which

remains vital for the operations of the company. It is considered that preparing and maintaining

report presents different business operations which is analyzed for decision-making process

(Smith, Brännström and Jansson, 2015). The reports are of different types in management

accounting which contain different information's related to different operations and the data

collected in this reports is from financial and non-financial sources and facilitate in decision-

making. There are different reports and they are:

Job Cost Reports: This report shows how much cost has been incurred in particular

period by the organization to carry out the operations. In this report usually the cost is

matched with an estimate of revenue to draw conclusions on the profitability of the

company. It is helpful to analyse higher earning area and costs incurred for

manufacturing of products. Therefore, preparing job cost report is analyzed for further

business operations.

Inventory Management Reports: Preparing and maintaining this report is suitable to

manage all inventories of the organisation as well generating ideas for improving its

3

manufacturing of products are analysed that affects its production effectively. That means

for fulfilling requirements of all customers regarding set of product produced by entity.

Here firstly the customer makes the order as per his liking and then a company prepares

him the product(Ghasemi and et.al, 2016). It is appropriate technique to reach out

customers' expectations and satisfying them with product services provided by

organization.

4. Price-Optimizing Systems: It is best tool for optimizing price and cost effectiveness to

produce goods and services provided by entity (Hopper, 2013). In accordance to this,

several tools are applied for setting price regarding business operations also impacts on

profitability of organisation. In this system different customer groups are taken into

consideration as per their income levels so that pricing decisions can be made as per the

purchasing powers.

P2 Methods Used for Management Accounting Reporting

Management accounting reporting can be understood as the reporting of operations of the

businesses which makes or helps management of organizations to make decisions which

remains vital for the operations of the company. It is considered that preparing and maintaining

report presents different business operations which is analyzed for decision-making process

(Smith, Brännström and Jansson, 2015). The reports are of different types in management

accounting which contain different information's related to different operations and the data

collected in this reports is from financial and non-financial sources and facilitate in decision-

making. There are different reports and they are:

Job Cost Reports: This report shows how much cost has been incurred in particular

period by the organization to carry out the operations. In this report usually the cost is

matched with an estimate of revenue to draw conclusions on the profitability of the

company. It is helpful to analyse higher earning area and costs incurred for

manufacturing of products. Therefore, preparing job cost report is analyzed for further

business operations.

Inventory Management Reports: Preparing and maintaining this report is suitable to

manage all inventories of the organisation as well generating ideas for improving its

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liquidity. Including this, it also helps in maintaining the levels of inventory in the

situations of immediate needs(Orelli, Padovani and Katsikas, 2016). These reports

generally include items such as inventory waste, O/H costs, Labor costs, etc.

Operating Budget Report: Operating reports will help abc to make decisions on the

performance as a whole and each department has to enable monitoring and proper control

costs of operations. Through these reports every individual employee is tracked in terms

of his performance and thus by the help of budget reports is easy for management to

calculate the incentives of employees.

Accounts Receivable Reports: This report is vital tool which enables managers to

manage cash transactions in the organization with relation to credit it offers to customers.

The report identify the problem related to collection process and it facilitate in making

necessary regulations or rules for further operations. It also enables accounts departments

to look at old debts(Orelli, Padovani and Katsikas, 2016).

TASK 2

P3 Calculation of Costs and Difference between Marginal and Absorption Costing

Price determination is one the essential tool for cost effectiveness and proper

management of production and distribution system of the organisation. It is used to measure the

cost which is incurred in a particular period for activities that are being performed in an

organization. An inappropriate cost identification will affects abc in a negative and a major way

(Luft, 2016). There are different costs which is used in management accounting and they are:

opportunity costs, sunk costs, Direct expenses and Overheads. For price determination process,

various costing methods are used such as; marginal, absorption, activity based costing and so on.

However, in all of these methods, preparing income statement from marginal and absorption

costing can understand as below:

Marginal Costing: Under this costing method, for evaluating net profit, gross profit of

the entity is deducted with expenditures incurred on variable operations only. Therefore, it is

suitable for short term decision making process and preparing strategies for reducing issues

occur in the entity. However, proper ideas are generated for further decision making and

implementing activities for its improvement effectively. The name itself suggest that cost which

has established by incurring one additional unit of output.

4

situations of immediate needs(Orelli, Padovani and Katsikas, 2016). These reports

generally include items such as inventory waste, O/H costs, Labor costs, etc.

Operating Budget Report: Operating reports will help abc to make decisions on the

performance as a whole and each department has to enable monitoring and proper control

costs of operations. Through these reports every individual employee is tracked in terms

of his performance and thus by the help of budget reports is easy for management to

calculate the incentives of employees.

Accounts Receivable Reports: This report is vital tool which enables managers to

manage cash transactions in the organization with relation to credit it offers to customers.

The report identify the problem related to collection process and it facilitate in making

necessary regulations or rules for further operations. It also enables accounts departments

to look at old debts(Orelli, Padovani and Katsikas, 2016).

TASK 2

P3 Calculation of Costs and Difference between Marginal and Absorption Costing

Price determination is one the essential tool for cost effectiveness and proper

management of production and distribution system of the organisation. It is used to measure the

cost which is incurred in a particular period for activities that are being performed in an

organization. An inappropriate cost identification will affects abc in a negative and a major way

(Luft, 2016). There are different costs which is used in management accounting and they are:

opportunity costs, sunk costs, Direct expenses and Overheads. For price determination process,

various costing methods are used such as; marginal, absorption, activity based costing and so on.

However, in all of these methods, preparing income statement from marginal and absorption

costing can understand as below:

Marginal Costing: Under this costing method, for evaluating net profit, gross profit of

the entity is deducted with expenditures incurred on variable operations only. Therefore, it is

suitable for short term decision making process and preparing strategies for reducing issues

occur in the entity. However, proper ideas are generated for further decision making and

implementing activities for its improvement effectively. The name itself suggest that cost which

has established by incurring one additional unit of output.

4

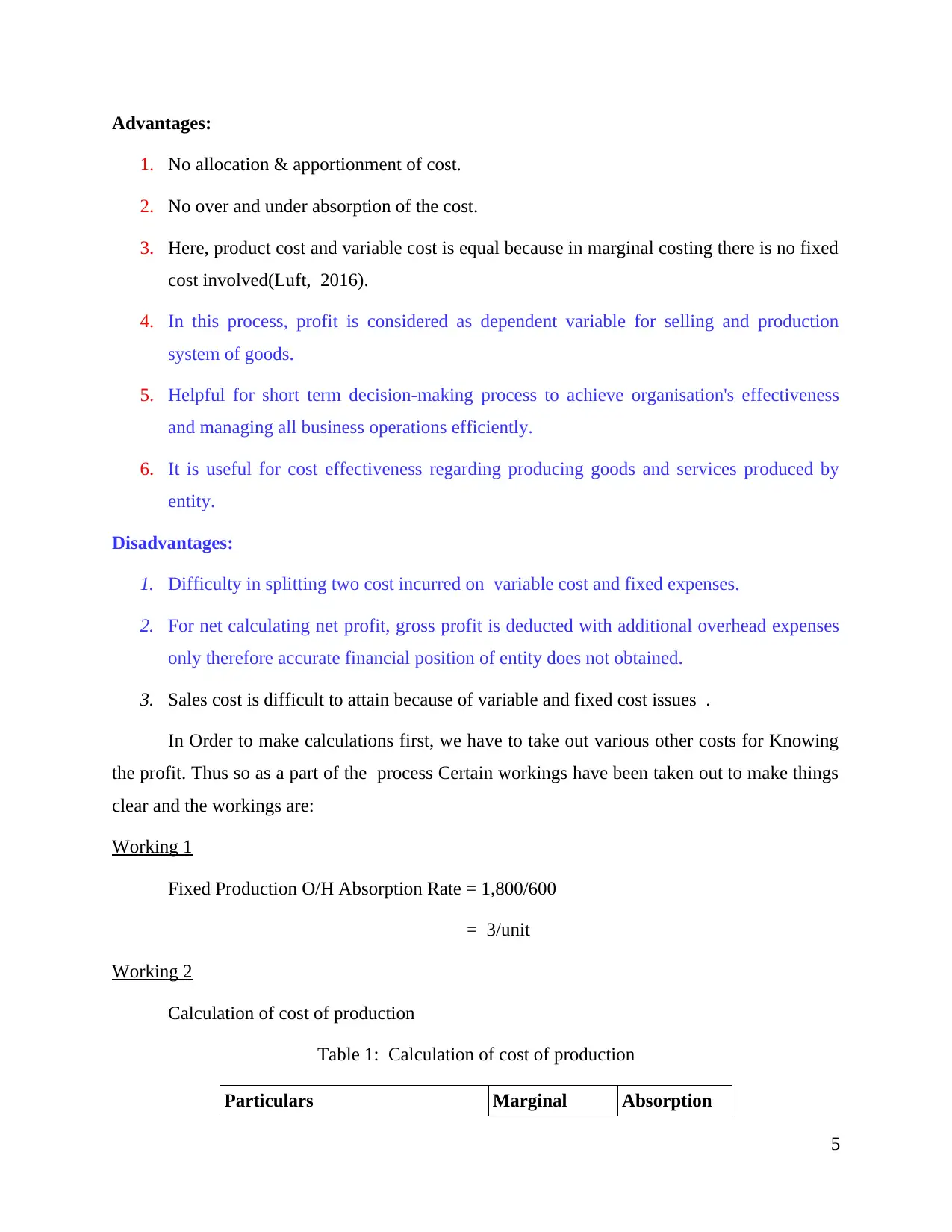

Advantages:

1. No allocation & apportionment of cost.

2. No over and under absorption of the cost.

3. Here, product cost and variable cost is equal because in marginal costing there is no fixed

cost involved(Luft, 2016).

4. In this process, profit is considered as dependent variable for selling and production

system of goods.

5. Helpful for short term decision-making process to achieve organisation's effectiveness

and managing all business operations efficiently.

6. It is useful for cost effectiveness regarding producing goods and services produced by

entity.

Disadvantages:

1. Difficulty in splitting two cost incurred on variable cost and fixed expenses.

2. For net calculating net profit, gross profit is deducted with additional overhead expenses

only therefore accurate financial position of entity does not obtained.

3. Sales cost is difficult to attain because of variable and fixed cost issues .

In Order to make calculations first, we have to take out various other costs for Knowing

the profit. Thus so as a part of the process Certain workings have been taken out to make things

clear and the workings are:

Working 1

Fixed Production O/H Absorption Rate = 1,800/600

= 3/unit

Working 2

Calculation of cost of production

Table 1: Calculation of cost of production

Particulars Marginal Absorption

5

1. No allocation & apportionment of cost.

2. No over and under absorption of the cost.

3. Here, product cost and variable cost is equal because in marginal costing there is no fixed

cost involved(Luft, 2016).

4. In this process, profit is considered as dependent variable for selling and production

system of goods.

5. Helpful for short term decision-making process to achieve organisation's effectiveness

and managing all business operations efficiently.

6. It is useful for cost effectiveness regarding producing goods and services produced by

entity.

Disadvantages:

1. Difficulty in splitting two cost incurred on variable cost and fixed expenses.

2. For net calculating net profit, gross profit is deducted with additional overhead expenses

only therefore accurate financial position of entity does not obtained.

3. Sales cost is difficult to attain because of variable and fixed cost issues .

In Order to make calculations first, we have to take out various other costs for Knowing

the profit. Thus so as a part of the process Certain workings have been taken out to make things

clear and the workings are:

Working 1

Fixed Production O/H Absorption Rate = 1,800/600

= 3/unit

Working 2

Calculation of cost of production

Table 1: Calculation of cost of production

Particulars Marginal Absorption

5

Direct Material 6 6

Direct Labour 5 5

Variable O/H 2 2

Fixed Production O/H 0 3

Cost of Production/Unit 13 16

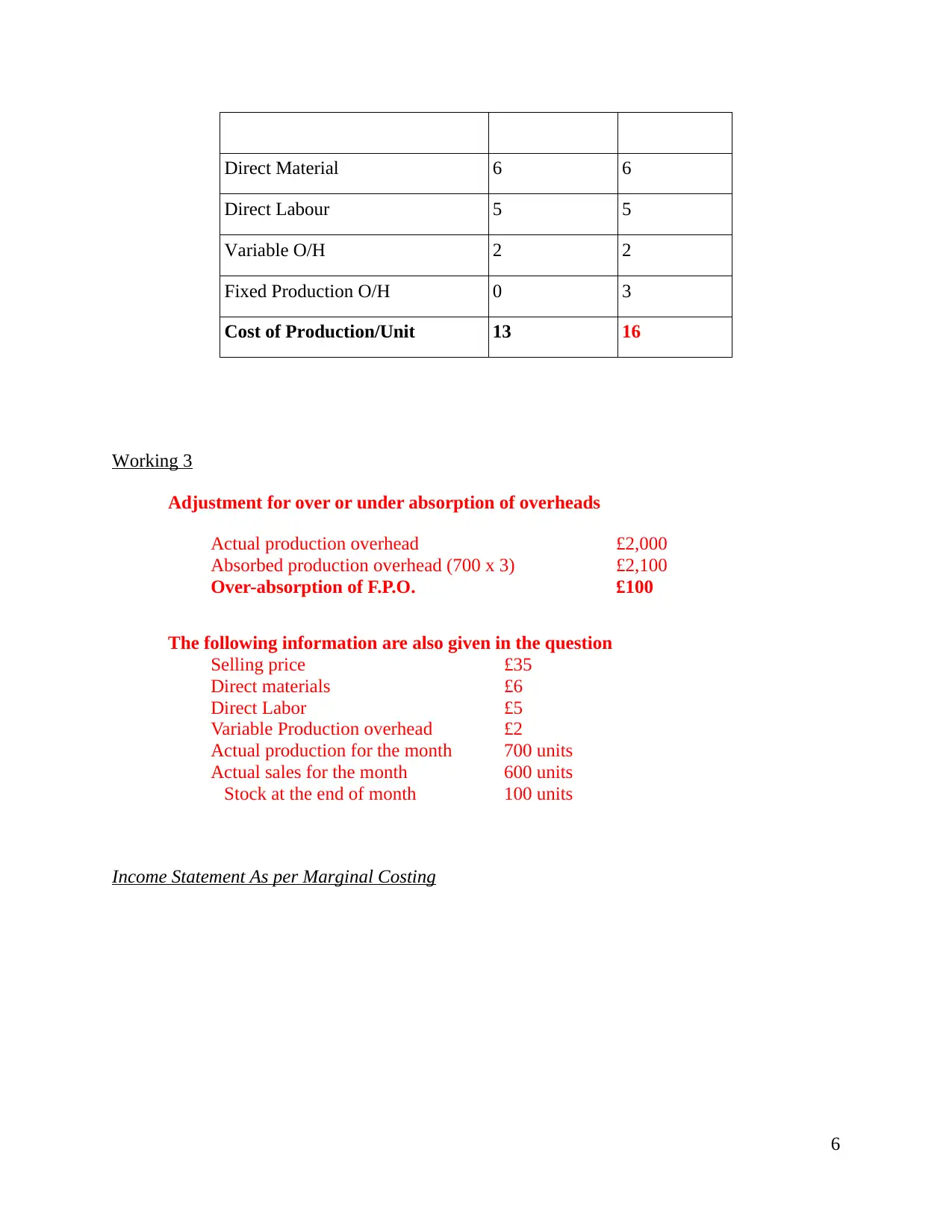

Working 3

Adjustment for over or under absorption of overheads

Actual production overhead £2,000

Absorbed production overhead (700 x 3) £2,100

Over-absorption of F.P.O. £100

The following information are also given in the question

Selling price £35

Direct materials £6

Direct Labor £5

Variable Production overhead £2

Actual production for the month 700 units

Actual sales for the month 600 units

Stock at the end of month 100 units

Income Statement As per Marginal Costing

6

Direct Labour 5 5

Variable O/H 2 2

Fixed Production O/H 0 3

Cost of Production/Unit 13 16

Working 3

Adjustment for over or under absorption of overheads

Actual production overhead £2,000

Absorbed production overhead (700 x 3) £2,100

Over-absorption of F.P.O. £100

The following information are also given in the question

Selling price £35

Direct materials £6

Direct Labor £5

Variable Production overhead £2

Actual production for the month 700 units

Actual sales for the month 600 units

Stock at the end of month 100 units

Income Statement As per Marginal Costing

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table 2: Income Statement As per Marginal Costing

Particulars £ £

Sales (700 x 35) 21,000

Cost of Production (13 x 700) 9,100

Less: Closing stock (13 x 100) (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales O/H (1 x 600) 600

Less: Fixed Costs; Production O/H 2,000

Admin cost 700

Selling cost 600 3,900

Profit 9,300

Absorption Costing: It is different from marginal costing in which net profit is

evaluated through deducting gross profit with allover the expenses incurred on variable and fixed

expenditures. Thus, it is beneficial for long term decision-making process regarding business

operations. Including this, actual financial position of entity is analyzed that affects further

business operations and its profitability. In this process, calculation for absorption costing of the

organisation can understand as follows including its advantages and limitations:

7

Particulars £ £

Sales (700 x 35) 21,000

Cost of Production (13 x 700) 9,100

Less: Closing stock (13 x 100) (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales O/H (1 x 600) 600

Less: Fixed Costs; Production O/H 2,000

Admin cost 700

Selling cost 600 3,900

Profit 9,300

Absorption Costing: It is different from marginal costing in which net profit is

evaluated through deducting gross profit with allover the expenses incurred on variable and fixed

expenditures. Thus, it is beneficial for long term decision-making process regarding business

operations. Including this, actual financial position of entity is analyzed that affects further

business operations and its profitability. In this process, calculation for absorption costing of the

organisation can understand as follows including its advantages and limitations:

7

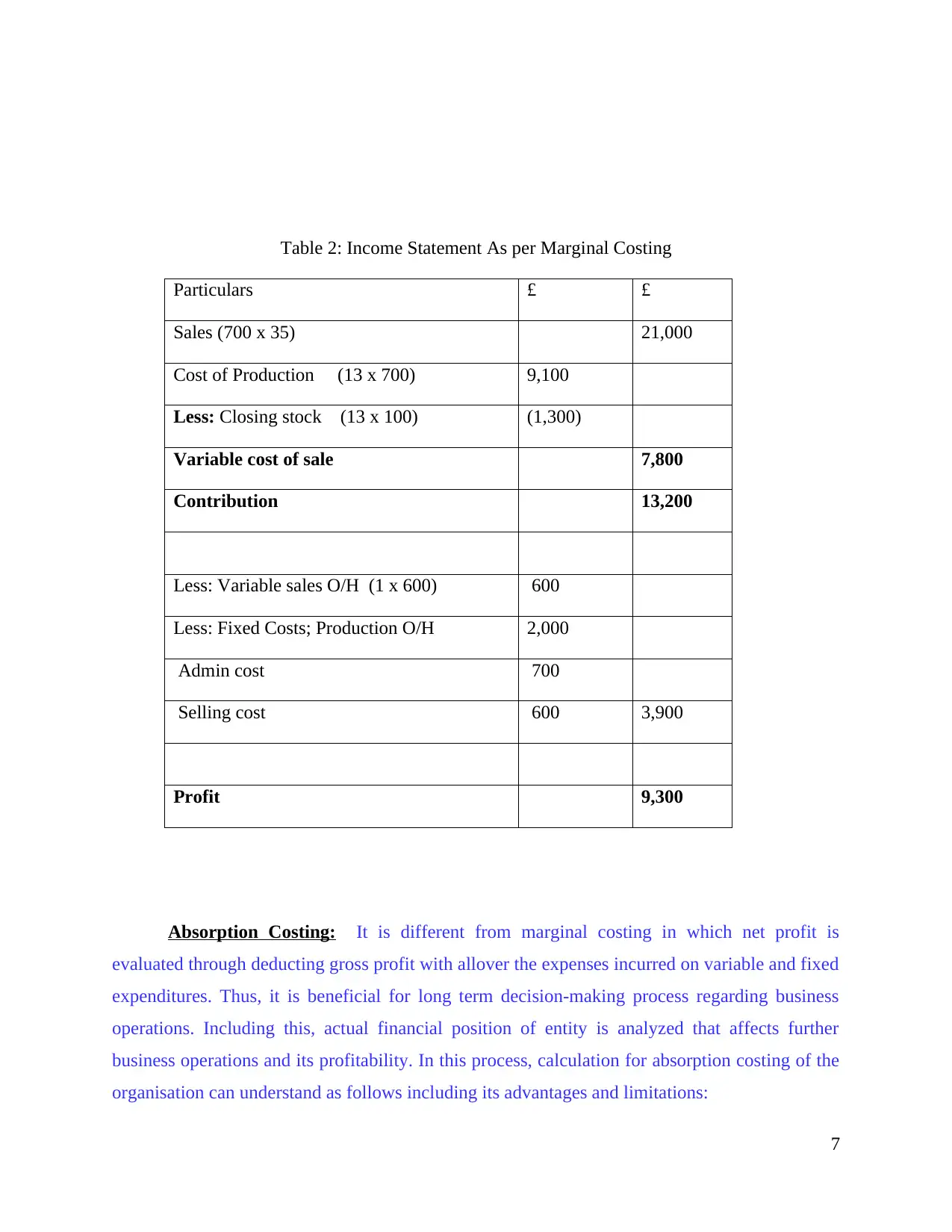

Advantages:1. Under absorption costing method, competitive selling price is evaluated for long term

decision-making process.2. It is helpful for optimum utilization of resources and fund efficiently (Aouni, McGillis

and Abdulkarim, 2015).3. Cost is charged in an efficient manner to the product.4. This costing is emphasis for business operations for long time periodicity.

Disadvantages:

1. Cost apportionment is not easy to implement.

2. Over and under absorbed cost should be included at the year end. It should not be

included directly.

3. Profits is affected by the volumes of production.

Income Statement As per Absorption Costing

Table 3: Income Statement As per Absorption Costing

Particulars £ £

Sales (700 x 35) 21,000

Less: Cost of Production (16 x 700) 11,200

Less: Closing stock (16 x 100) (1,600)

9,600

Less: Over-absorption of F.O.H -100

Production cost of sale 9,500

Gross Profit 11,500

Less: Variable sales O/H (1 x 600) 600

8

decision-making process.2. It is helpful for optimum utilization of resources and fund efficiently (Aouni, McGillis

and Abdulkarim, 2015).3. Cost is charged in an efficient manner to the product.4. This costing is emphasis for business operations for long time periodicity.

Disadvantages:

1. Cost apportionment is not easy to implement.

2. Over and under absorbed cost should be included at the year end. It should not be

included directly.

3. Profits is affected by the volumes of production.

Income Statement As per Absorption Costing

Table 3: Income Statement As per Absorption Costing

Particulars £ £

Sales (700 x 35) 21,000

Less: Cost of Production (16 x 700) 11,200

Less: Closing stock (16 x 100) (1,600)

9,600

Less: Over-absorption of F.O.H -100

Production cost of sale 9,500

Gross Profit 11,500

Less: Variable sales O/H (1 x 600) 600

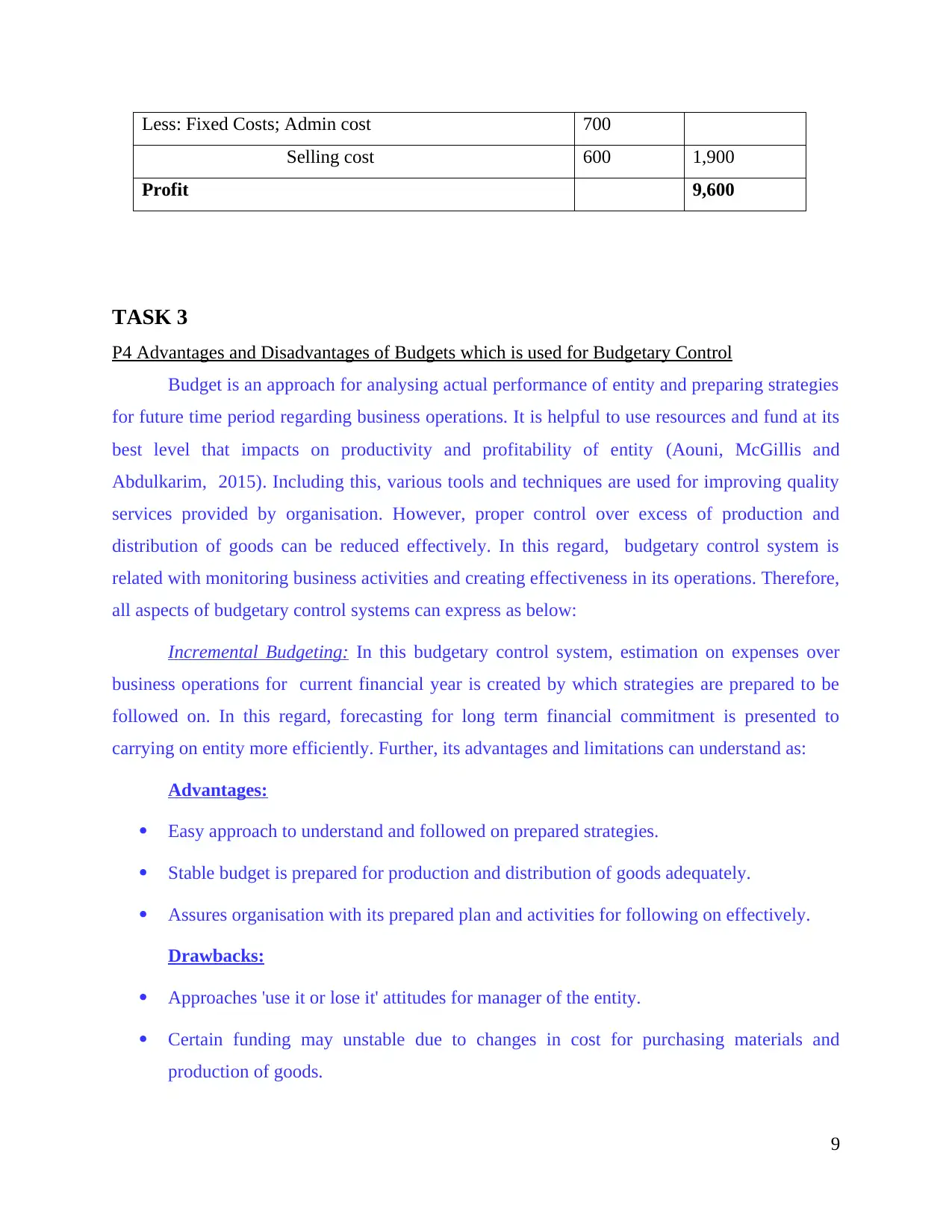

8

Less: Fixed Costs; Admin cost 700

Selling cost 600 1,900

Profit 9,600

TASK 3

P4 Advantages and Disadvantages of Budgets which is used for Budgetary Control

Budget is an approach for analysing actual performance of entity and preparing strategies

for future time period regarding business operations. It is helpful to use resources and fund at its

best level that impacts on productivity and profitability of entity (Aouni, McGillis and

Abdulkarim, 2015). Including this, various tools and techniques are used for improving quality

services provided by organisation. However, proper control over excess of production and

distribution of goods can be reduced effectively. In this regard, budgetary control system is

related with monitoring business activities and creating effectiveness in its operations. Therefore,

all aspects of budgetary control systems can express as below:

Incremental Budgeting: In this budgetary control system, estimation on expenses over

business operations for current financial year is created by which strategies are prepared to be

followed on. In this regard, forecasting for long term financial commitment is presented to

carrying on entity more efficiently. Further, its advantages and limitations can understand as:

Advantages:

Easy approach to understand and followed on prepared strategies.

Stable budget is prepared for production and distribution of goods adequately.

Assures organisation with its prepared plan and activities for following on effectively.

Drawbacks:

Approaches 'use it or lose it' attitudes for manager of the entity.

Certain funding may unstable due to changes in cost for purchasing materials and

production of goods.

9

Selling cost 600 1,900

Profit 9,600

TASK 3

P4 Advantages and Disadvantages of Budgets which is used for Budgetary Control

Budget is an approach for analysing actual performance of entity and preparing strategies

for future time period regarding business operations. It is helpful to use resources and fund at its

best level that impacts on productivity and profitability of entity (Aouni, McGillis and

Abdulkarim, 2015). Including this, various tools and techniques are used for improving quality

services provided by organisation. However, proper control over excess of production and

distribution of goods can be reduced effectively. In this regard, budgetary control system is

related with monitoring business activities and creating effectiveness in its operations. Therefore,

all aspects of budgetary control systems can express as below:

Incremental Budgeting: In this budgetary control system, estimation on expenses over

business operations for current financial year is created by which strategies are prepared to be

followed on. In this regard, forecasting for long term financial commitment is presented to

carrying on entity more efficiently. Further, its advantages and limitations can understand as:

Advantages:

Easy approach to understand and followed on prepared strategies.

Stable budget is prepared for production and distribution of goods adequately.

Assures organisation with its prepared plan and activities for following on effectively.

Drawbacks:

Approaches 'use it or lose it' attitudes for manager of the entity.

Certain funding may unstable due to changes in cost for purchasing materials and

production of goods.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero-based Budgeting: It is useful approach to maintain finance and preparing certain

strategies to be followed on for organisation's effectiveness (Ahmad and Leftesi, 2014). In

addition to this, decisions are made regarding starting operations for business entity and

improving its services for increasing efficiencies at higher level.

Advantages:

It is simple and convenient to understand all processes of budget.

Helpful to maintain finance and funding for further operations efficiently.

Disadvantages

Response over business activities are obtained slowly.

Expenses to be incurred on additional operations like; advertisement etc are not

considered for preparing budget. Therefore, financial management get disturbed.

Fixed Budgeting: In this budgetary control system, prepared strategies remains constant

whether market price and distribution of goods changes. Therefore, due to changes in market

prices and expenses over business operations, decided plan get stable.

Advantages:

Fixed and stable budget

No changes in prices for producing goods and crevices according to competitive

strategies and fluctuations in market price.

Disadvantages:

It is difficult to sustain in competitive market.

Imbalanced production and distribution of goods and services.

Flexible Budgeting: In flexible budget companies are more flexible because here the

budget can be changed as per the requirements of the companies.

Advantages:

For making place in market, price for production and distribution of goods and services

produced by entity get flexible.

10

strategies to be followed on for organisation's effectiveness (Ahmad and Leftesi, 2014). In

addition to this, decisions are made regarding starting operations for business entity and

improving its services for increasing efficiencies at higher level.

Advantages:

It is simple and convenient to understand all processes of budget.

Helpful to maintain finance and funding for further operations efficiently.

Disadvantages

Response over business activities are obtained slowly.

Expenses to be incurred on additional operations like; advertisement etc are not

considered for preparing budget. Therefore, financial management get disturbed.

Fixed Budgeting: In this budgetary control system, prepared strategies remains constant

whether market price and distribution of goods changes. Therefore, due to changes in market

prices and expenses over business operations, decided plan get stable.

Advantages:

Fixed and stable budget

No changes in prices for producing goods and crevices according to competitive

strategies and fluctuations in market price.

Disadvantages:

It is difficult to sustain in competitive market.

Imbalanced production and distribution of goods and services.

Flexible Budgeting: In flexible budget companies are more flexible because here the

budget can be changed as per the requirements of the companies.

Advantages:

For making place in market, price for production and distribution of goods and services

produced by entity get flexible.

10

Able to gain customer satisfaction and providing services according to their requirements.

Disadvantages:

Inaccurate adjustments for getting changes according to situations occurred.

Lack of information regarding market position and competitiveness.

Quite complex and difficult to access.

There are several kinds of budgets prepared by a business entity in order to assess

financial data for the further period. Moreover, the budget section is one of the important part of

management accounting. Basic two types of budgets along with illustration are such as follows:

Cash budget- This kind of budget provides information to the management regarding to

the cash position at the end of every month. On the basis of this, company able to predetermine

that how much amount of incomes as well as expenses will be incur at the workplace. Generally

it includes two values like cash inflows and cash outflows and whatever difference comes is

considered as net cash balance. It supports to the entity in order to assess that in case of lack of

capital which source of financing will be suitable for it. Most of the firms use the cash budget

because it supports to manage as well as allocate financial resources within workplace and utilise

in optimum ways.

However, it is based on the assumptions due to which sometimes data and figures not

assumed properly which lead to make business decisions ineffectual. Along with this, highly

qualified as well as finance expertise required to prepare cash budget who create monetary

burden on the firm.

Example of the cash budget is given as below:

11

Disadvantages:

Inaccurate adjustments for getting changes according to situations occurred.

Lack of information regarding market position and competitiveness.

Quite complex and difficult to access.

There are several kinds of budgets prepared by a business entity in order to assess

financial data for the further period. Moreover, the budget section is one of the important part of

management accounting. Basic two types of budgets along with illustration are such as follows:

Cash budget- This kind of budget provides information to the management regarding to

the cash position at the end of every month. On the basis of this, company able to predetermine

that how much amount of incomes as well as expenses will be incur at the workplace. Generally

it includes two values like cash inflows and cash outflows and whatever difference comes is

considered as net cash balance. It supports to the entity in order to assess that in case of lack of

capital which source of financing will be suitable for it. Most of the firms use the cash budget

because it supports to manage as well as allocate financial resources within workplace and utilise

in optimum ways.

However, it is based on the assumptions due to which sometimes data and figures not

assumed properly which lead to make business decisions ineffectual. Along with this, highly

qualified as well as finance expertise required to prepare cash budget who create monetary

burden on the firm.

Example of the cash budget is given as below:

11

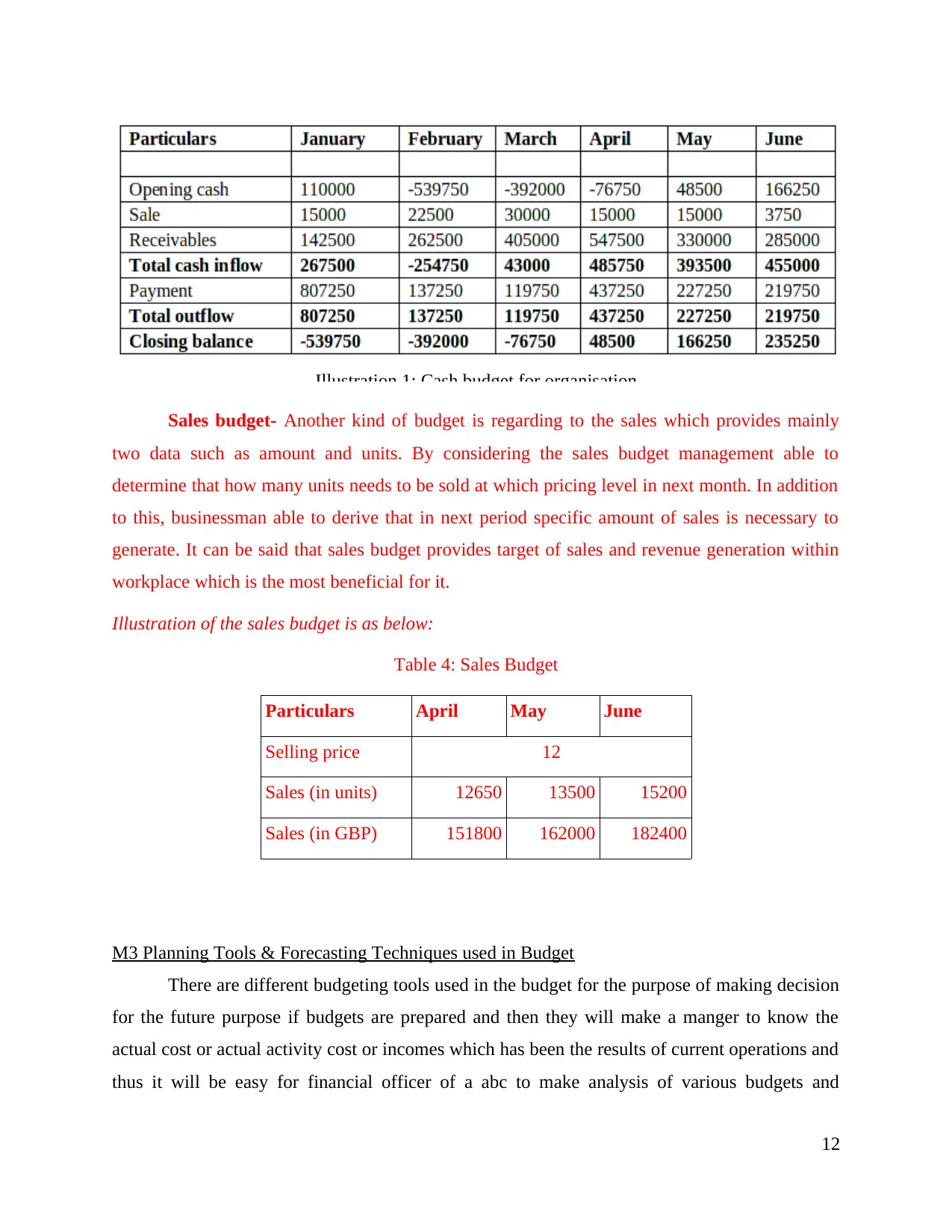

Illustration 1: Cash budget for organisation

Sales budget- Another kind of budget is regarding to the sales which provides mainly

two data such as amount and units. By considering the sales budget management able to

determine that how many units needs to be sold at which pricing level in next month. In addition

to this, businessman able to derive that in next period specific amount of sales is necessary to

generate. It can be said that sales budget provides target of sales and revenue generation within

workplace which is the most beneficial for it.

Illustration of the sales budget is as below:

Table 4: Sales Budget

Particulars April May June

Selling price 12

Sales (in units) 12650 13500 15200

Sales (in GBP) 151800 162000 182400

M3 Planning Tools & Forecasting Techniques used in Budget

There are different budgeting tools used in the budget for the purpose of making decision

for the future purpose if budgets are prepared and then they will make a manger to know the

actual cost or actual activity cost or incomes which has been the results of current operations and

thus it will be easy for financial officer of a abc to make analysis of various budgets and

12

Sales budget- Another kind of budget is regarding to the sales which provides mainly

two data such as amount and units. By considering the sales budget management able to

determine that how many units needs to be sold at which pricing level in next month. In addition

to this, businessman able to derive that in next period specific amount of sales is necessary to

generate. It can be said that sales budget provides target of sales and revenue generation within

workplace which is the most beneficial for it.

Illustration of the sales budget is as below:

Table 4: Sales Budget

Particulars April May June

Selling price 12

Sales (in units) 12650 13500 15200

Sales (in GBP) 151800 162000 182400

M3 Planning Tools & Forecasting Techniques used in Budget

There are different budgeting tools used in the budget for the purpose of making decision

for the future purpose if budgets are prepared and then they will make a manger to know the

actual cost or actual activity cost or incomes which has been the results of current operations and

thus it will be easy for financial officer of a abc to make analysis of various budgets and

12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

comparing the standards with actual will make them take capable decisions and thus making it

more growth prospective for the firm(Ossadnik and Kaspar, 2013). There are different planning

tools which are:

Budgetary Control: Budgets formed as per the requirements of executives to make

different policies and to make the policies they need to have a different set of thinking

capabilities and the data and that data is collected from different people over the others.

Forecasting: Forecasting is also another technique of budgeting which helps in making

different decisions for the future purpose(Wickramasinghe, 2015). As the name suggest different

people. Through forecasting results are expected which are based on the latest experience and

circumstances at the hand. Therefore, on the basis of actual position of entity, predictions on

further business operations are created that affects further business operations. Forecast also

enables a manager to predict the results by adjusting their existing plans according to the at least

information. Forecasting is helpful for a company to make necessary adjustments regarding

expenses for production and distribution system.

Capital Acquisition Budgets: Acquisitions of capital assets including buildings,

renovations, automobiles, software systems, furniture must be carefully planned because they

consume substantial cash reserves. The purpose is to allocate funds, control risks in decision

making, and set priorities. It aims to allocate resources and fund of the entity of entity for further

operations and improvements in its quality services (Tucker and Parker, 2014). By using this

budgeting approach, organisation remains suitable to achieve competitive advantages and further

business operations. It also enable the business plan for the acquisition of capital equipment for

expansion and/or replacement.

Cash Budgets: Cash budgets are the tools which determine the cash requirements of the

firm in the near future. It determines whether cash balances remain sufficient to fulfill regular

obligations. In accordance to this, it is useful for cost effectiveness and balancing all cash and

maintaining fund efficiently. In addition to this, cash required to operate business activities and

reducing losses are obtained through this process in a systematic manner.

P5 Ways Management Accounting can be used to respond to Financial Problems

There are different way through which by applying management accounting at the

workplace abc's financial problems can be solved up to an extent there are different techniques or

13

more growth prospective for the firm(Ossadnik and Kaspar, 2013). There are different planning

tools which are:

Budgetary Control: Budgets formed as per the requirements of executives to make

different policies and to make the policies they need to have a different set of thinking

capabilities and the data and that data is collected from different people over the others.

Forecasting: Forecasting is also another technique of budgeting which helps in making

different decisions for the future purpose(Wickramasinghe, 2015). As the name suggest different

people. Through forecasting results are expected which are based on the latest experience and

circumstances at the hand. Therefore, on the basis of actual position of entity, predictions on

further business operations are created that affects further business operations. Forecast also

enables a manager to predict the results by adjusting their existing plans according to the at least

information. Forecasting is helpful for a company to make necessary adjustments regarding

expenses for production and distribution system.

Capital Acquisition Budgets: Acquisitions of capital assets including buildings,

renovations, automobiles, software systems, furniture must be carefully planned because they

consume substantial cash reserves. The purpose is to allocate funds, control risks in decision

making, and set priorities. It aims to allocate resources and fund of the entity of entity for further

operations and improvements in its quality services (Tucker and Parker, 2014). By using this

budgeting approach, organisation remains suitable to achieve competitive advantages and further

business operations. It also enable the business plan for the acquisition of capital equipment for

expansion and/or replacement.

Cash Budgets: Cash budgets are the tools which determine the cash requirements of the

firm in the near future. It determines whether cash balances remain sufficient to fulfill regular

obligations. In accordance to this, it is useful for cost effectiveness and balancing all cash and

maintaining fund efficiently. In addition to this, cash required to operate business activities and

reducing losses are obtained through this process in a systematic manner.

P5 Ways Management Accounting can be used to respond to Financial Problems

There are different way through which by applying management accounting at the

workplace abc's financial problems can be solved up to an extent there are different techniques or

13

ways through which a company can make difference in the market and thus making it more

dynamic and reliable brand in the minds of customers(Tucker and Parker, 2014). There are three

ways through which by management accounting can be used to respond to financial problems

and they are:

Key Performance Indicators: These indicators depicts or show the performance levels

of different individuals and operations of the business. In this process, competitive strategies of

all organizations and market positions are analyzed that generates ideas to make position in

market for long time period. It enables organizations to understand where the progress is being

made towards achieving strategic aims and those areas which need to be addressed. Key

performance indicators are qualitative and quantitative measures used to review the companies

progress against its goals(Zaleha Abdul Rasid and et.al, 2014). These indicators help managers in

making sound decisions which keeps reflecting a positive and good financial health of abc.

Several kinds of problems comes into existence at the workplace which lead to hamper

the smooth functioning of business and reduce its performance within industry. With the help of

key performance indicators management able to depict that which are problems arise and due to

which condition. Various KPIs used by firm are relating to the performance, costing, financial,

employees, productivity etc. Moreover, in this firm use various measurement criteria are like

quality, cost, net profit, employee efficiency etc. For example, cost of the overall production

enhance and profit reduce then entity will determine that it performing poor within industry.

Bench marking: It is comparative tool that shows market position of entity and potential

to face competition. However, actual market position is recognize by which further

improvements in quality services regarding business operations are made effectively (Adrian,

2014). For example; analysing market position of ABC with its competitive entity therefore ideas

are generated related to improving its quality services. This is a process which involves

comparing one's firm performance on a set of measurable parameters against firms known to

have achieved against firms known to achieved best performance on those indicators. Here

specific criteria and standards are settled by the management as well as external business

authorities. In this, actual data compared with the benchmark or standard value and then analyse

that whether it performs well or poor in the market segment. The company set benchmark for

further accounting year that profit must be improve by 12.5%. At the end of year if it founds that

14

dynamic and reliable brand in the minds of customers(Tucker and Parker, 2014). There are three

ways through which by management accounting can be used to respond to financial problems

and they are:

Key Performance Indicators: These indicators depicts or show the performance levels

of different individuals and operations of the business. In this process, competitive strategies of

all organizations and market positions are analyzed that generates ideas to make position in

market for long time period. It enables organizations to understand where the progress is being

made towards achieving strategic aims and those areas which need to be addressed. Key

performance indicators are qualitative and quantitative measures used to review the companies

progress against its goals(Zaleha Abdul Rasid and et.al, 2014). These indicators help managers in

making sound decisions which keeps reflecting a positive and good financial health of abc.

Several kinds of problems comes into existence at the workplace which lead to hamper

the smooth functioning of business and reduce its performance within industry. With the help of

key performance indicators management able to depict that which are problems arise and due to

which condition. Various KPIs used by firm are relating to the performance, costing, financial,

employees, productivity etc. Moreover, in this firm use various measurement criteria are like

quality, cost, net profit, employee efficiency etc. For example, cost of the overall production

enhance and profit reduce then entity will determine that it performing poor within industry.

Bench marking: It is comparative tool that shows market position of entity and potential

to face competition. However, actual market position is recognize by which further

improvements in quality services regarding business operations are made effectively (Adrian,

2014). For example; analysing market position of ABC with its competitive entity therefore ideas

are generated related to improving its quality services. This is a process which involves

comparing one's firm performance on a set of measurable parameters against firms known to

have achieved against firms known to achieved best performance on those indicators. Here

specific criteria and standards are settled by the management as well as external business

authorities. In this, actual data compared with the benchmark or standard value and then analyse

that whether it performs well or poor in the market segment. The company set benchmark for

further accounting year that profit must be improve by 12.5%. At the end of year if it founds that

14

from previous to next period it achieves target then it has been said that performance is better.

Apart from this, as per the industry standard current ratio must be 2:1 and after completion of

year in case entity achieves the standards then it can be said that it performing well in its

respective industry.

Financial Governance: It is one of the essential decision-making tool to building up

different sets of traits regarding business operations (Adrian, 2014). Thus, financial data is so

important Dior the organization that it should be made. Governance is an important element in

mankind strategic tactical and operational decisions thus making it more reluctant. Financial

governance is small segment of the corporate governance where it has been evaluated that

business enterprise is achieving the targets or not. In this, several financial transactions are also

checked out by the financial governance which helps to assess accountable reasons of occurring

financial shortfalls.

CONCLUSION

From this report it can be concluded that management accounting has played an

important part in making an organization work smoothly and with the efficient and effective way

inn order to make the operations achieve the desired goals and objectives, Further the report

discussed the scenario of cost accounting factors which can impact the decision making of

managers in the organization and for this purpose a company taken here was abc company who

is retail sector company which has calculated the cost on two basis that is absorption costing and

marginal costing in which it is identified that in a way of the making different judgments

managers have to make use of different set of techniques. In this report it is founded that there

are various budgeting techniques from which a particular activity budget can also be made and

that are: Incremental budgeting, activity based budgeting, Zero-based budgeting and many more.

Further the financial problem evaluation of abc is done which ensures that making a move will

make difference in decision making scenario.

15

Apart from this, as per the industry standard current ratio must be 2:1 and after completion of

year in case entity achieves the standards then it can be said that it performing well in its

respective industry.

Financial Governance: It is one of the essential decision-making tool to building up

different sets of traits regarding business operations (Adrian, 2014). Thus, financial data is so

important Dior the organization that it should be made. Governance is an important element in

mankind strategic tactical and operational decisions thus making it more reluctant. Financial

governance is small segment of the corporate governance where it has been evaluated that

business enterprise is achieving the targets or not. In this, several financial transactions are also

checked out by the financial governance which helps to assess accountable reasons of occurring

financial shortfalls.

CONCLUSION

From this report it can be concluded that management accounting has played an

important part in making an organization work smoothly and with the efficient and effective way

inn order to make the operations achieve the desired goals and objectives, Further the report

discussed the scenario of cost accounting factors which can impact the decision making of

managers in the organization and for this purpose a company taken here was abc company who

is retail sector company which has calculated the cost on two basis that is absorption costing and

marginal costing in which it is identified that in a way of the making different judgments

managers have to make use of different set of techniques. In this report it is founded that there

are various budgeting techniques from which a particular activity budget can also be made and

that are: Incremental budgeting, activity based budgeting, Zero-based budgeting and many more.

Further the financial problem evaluation of abc is done which ensures that making a move will

make difference in decision making scenario.

15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

A. Hammad, S., Jusoh, R. and Ghozali, I., 2013. Decentralization, perceived environmental

uncertainty, managerial performance and management accounting system information in

Egyptian hospitals. International Journal of Accounting and Information Management.

21(4). pp.314-330.

Adrian, T., 2014. Directions for improving management accounting in the textile industry

enterprises/Directii de perfectionare a contabiliatii de gestiune în întreprinderile din

industria textila. Industria Textila. 65(2). pp.101.

Ahmad, N. S. M. and Leftesi, A., 2014. An exploratory study of the level of sophistication of

management accounting practices in Libyan manufacturing companies. International

Journal of Business and Management. 2(2). pp.1.

Aouni, B., McGillis, S. and Abdulkarim, M. E., 2015. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. pp.1-14.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4). pp.273-318.

Chiekezie, N. R., Egbunike, P. A. and Odum, A. N., 2014. Adoption of competitor focused

accounting methods in selected manufacturing companies in Nigeria. Asian Journal of

Economic Modelling. 2(3). pp.128-140.

Du, X. and Taylor, S., 2013. Flipped classroom in first year management accounting unit–a case

study. Electric Dreams. Proceedings 30th ascilite. pp.252-256.

Ghasemi, R. and et.al.,, 2016. The mediating effect of management accounting system on the

relationship between competition and managerial performance. International Journal of

Accounting and Information Management. 24(3). pp.272-295.

Hopper, T., 2013. Management Accounting: Strategic Decision Making, Performance and

Risk. Journal of Accounting & Organizational Change.

Luft, J., 2016. Cooperation and competition among employees: Experimental evidence on the

role of management control systems. Management Accounting Research. 31. pp.75-85.

Myrelid, A. and Olhager, J., 2015. Applying modern accounting techniques in complex

manufacturing. Industrial Management & Data Systems. 115(3). pp.402-418.

16

Books & Journals

A. Hammad, S., Jusoh, R. and Ghozali, I., 2013. Decentralization, perceived environmental

uncertainty, managerial performance and management accounting system information in

Egyptian hospitals. International Journal of Accounting and Information Management.

21(4). pp.314-330.

Adrian, T., 2014. Directions for improving management accounting in the textile industry

enterprises/Directii de perfectionare a contabiliatii de gestiune în întreprinderile din

industria textila. Industria Textila. 65(2). pp.101.

Ahmad, N. S. M. and Leftesi, A., 2014. An exploratory study of the level of sophistication of

management accounting practices in Libyan manufacturing companies. International

Journal of Business and Management. 2(2). pp.1.

Aouni, B., McGillis, S. and Abdulkarim, M. E., 2015. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. pp.1-14.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4). pp.273-318.

Chiekezie, N. R., Egbunike, P. A. and Odum, A. N., 2014. Adoption of competitor focused

accounting methods in selected manufacturing companies in Nigeria. Asian Journal of

Economic Modelling. 2(3). pp.128-140.

Du, X. and Taylor, S., 2013. Flipped classroom in first year management accounting unit–a case

study. Electric Dreams. Proceedings 30th ascilite. pp.252-256.

Ghasemi, R. and et.al.,, 2016. The mediating effect of management accounting system on the

relationship between competition and managerial performance. International Journal of

Accounting and Information Management. 24(3). pp.272-295.

Hopper, T., 2013. Management Accounting: Strategic Decision Making, Performance and

Risk. Journal of Accounting & Organizational Change.

Luft, J., 2016. Cooperation and competition among employees: Experimental evidence on the

role of management control systems. Management Accounting Research. 31. pp.75-85.

Myrelid, A. and Olhager, J., 2015. Applying modern accounting techniques in complex

manufacturing. Industrial Management & Data Systems. 115(3). pp.402-418.

16

Orelli, R.L., Padovani, E. and Katsikas, E., 2016. NPM Reforms in Napoleonic Countries: A

Comparative Study of Management Accounting Innovations in Greek and Italian

Municipalities. International Journal of Public Administration. 39(10). pp.778-789.

Ossadnik, W. and Kaspar, R., 2013. Evaluation of AHP software from a management accounting

perspective. Journal of Modelling in Management. 8(3). pp.305-319.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Tucker, B. P. and Parker, L. D., 2014. Comparing Interview Interaction Modes in Management

Accounting Research: A Case to Answer?.

Wickramasinghe, D., 2015. Getting management accounting off the ground: post-colonial

neoliberalism in healthcare budgets. Accounting and Business Research. 45(3). pp.323-

355.

Zaleha Abdul Rasid, S. and et.al., 2014. Management accounting systems, enterprise risk

management and organizational performance in financial institutions. Asian Review of

Accounting. 22(2). pp.128-144.

17

Comparative Study of Management Accounting Innovations in Greek and Italian

Municipalities. International Journal of Public Administration. 39(10). pp.778-789.

Ossadnik, W. and Kaspar, R., 2013. Evaluation of AHP software from a management accounting

perspective. Journal of Modelling in Management. 8(3). pp.305-319.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Tucker, B. P. and Parker, L. D., 2014. Comparing Interview Interaction Modes in Management

Accounting Research: A Case to Answer?.

Wickramasinghe, D., 2015. Getting management accounting off the ground: post-colonial

neoliberalism in healthcare budgets. Accounting and Business Research. 45(3). pp.323-

355.

Zaleha Abdul Rasid, S. and et.al., 2014. Management accounting systems, enterprise risk

management and organizational performance in financial institutions. Asian Review of

Accounting. 22(2). pp.128-144.

17

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.