ACC302 Auditing & Assurance: Practical Audit Scenario of Woolworths

VerifiedAdded on 2023/03/20

|13

|2435

|97

Report

AI Summary

This report presents a comprehensive audit scenario for Woolworths, a company listed on the ASX. It begins with an executive summary and table of contents, followed by an introduction outlining the importance of audit planning and the identification of areas of concern within Woolworths' financial statements. The report conducts an analytical review of the company's financial performance, focusing on areas such as supplier rebates, total shareholders' returns, and foreign currency risk. It then details relevant audit procedures for each area of concern, including the verification of rebate figures, analysis of shareholder returns calculations, and assessment of foreign currency rate changes. The report also examines Woolworths' corporate governance practices, including its reporting under corporate governance and the role and benefits of its audit committee. The report concludes with an overall analysis of the company's financial performance and corporate governance, highlighting areas for improvement and disclosure. References and an appendix with profitability and liquidity ratios are also provided.

Subject Code: ACC302

Subject Name: Auditing & Assurance

Assessment Title: Assessment 3: A Practical Audit Scenario

Subject Name: Auditing & Assurance

Assessment Title: Assessment 3: A Practical Audit Scenario

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

Executive Summary

The analytical overview of the company can be done with the aid of the annual report

provided by the company. The area of concern can be easily checked with the aid of the

report. In this report, the major emphasis is on the area of concern and assertions. To conduct

this study, Woolworths has been selected, listed on the ASX. The report revolves around the

analytical review of the financial report followed by the relevant audit procedure taken by the

auditor. Further, the corporate governance of the company is dealt with in an effective

manner

2

Executive Summary

The analytical overview of the company can be done with the aid of the annual report

provided by the company. The area of concern can be easily checked with the aid of the

report. In this report, the major emphasis is on the area of concern and assertions. To conduct

this study, Woolworths has been selected, listed on the ASX. The report revolves around the

analytical review of the financial report followed by the relevant audit procedure taken by the

auditor. Further, the corporate governance of the company is dealt with in an effective

manner

2

Woolworths

Contents

Introduction................................................................................................................................4

1. Analytical Review...............................................................................................................4

Assumption, Assertions & Judgements......................................................................................6

2. Relevant Audit Procedure..................................................................................................7

B. Corporate Governance...........................................................................................................8

1. Reporting under corporate governance..................................................................................8

2. Audit Committee....................................................................................................................8

3. Benefits of Audit Committee...........................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

3

Contents

Introduction................................................................................................................................4

1. Analytical Review...............................................................................................................4

Assumption, Assertions & Judgements......................................................................................6

2. Relevant Audit Procedure..................................................................................................7

B. Corporate Governance...........................................................................................................8

1. Reporting under corporate governance..................................................................................8

2. Audit Committee....................................................................................................................8

3. Benefits of Audit Committee...........................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

Introduction

The first step in an audit process is audit planning which includes various steps like

understanding the client and nature of their business, assessing risks and materiality,

formulating an audit strategy and deciding on the type of evidence to be collected on the basis

of risk levels (Merchant, 2012). Audit planning is important for identification of the areas

where there may exist the risk of material misstatements, for designing audit procedures to

address those risks and obtaining sufficient audit evidence, for minimizing audit costs, etc

(Osuala, 2015).

1. Analytical Review

In the case of Woolworths Group Limited for the year ended 2018, following are few of the

areas of concern which were noted while doing audit planning:

a. Area of Concern-

Rebates from the suppliers – the Group receives rebates from the suppliers which include

normal purchase discounts, discounts based on purchase or sales volume and based on

contribution towards any product promotions done for the suppliers. Such discounts need to

be shown either as reduction from the inventory value or reduction from the cost of sales as

per the nature of rebate received.

The main concern in this account is the authenticity and accuracy of rebate figures which

need to be checked, especially those of nonstandard nature. Also, the recording and

accounting treatment of the rebates are of concern matter.

Further, the Group has shown the Supplier Rebates as an inclusion in the trade receivables of

an amount equal to $100m which is a very substantial amount. The inclusion of supplier

rebate indicates that the rebates have only been booked as receivable and have not been

received in the current financial year. The rebates receivable should have been shown as a

separate figure in the balance sheet to encourage transparency in the balance sheet items.

The supplier rebates are likely to affect the trade and other receivables account, inventories

account, cost of sales (CAANZ, 2016).

b. Area of Concern-

4

Introduction

The first step in an audit process is audit planning which includes various steps like

understanding the client and nature of their business, assessing risks and materiality,

formulating an audit strategy and deciding on the type of evidence to be collected on the basis

of risk levels (Merchant, 2012). Audit planning is important for identification of the areas

where there may exist the risk of material misstatements, for designing audit procedures to

address those risks and obtaining sufficient audit evidence, for minimizing audit costs, etc

(Osuala, 2015).

1. Analytical Review

In the case of Woolworths Group Limited for the year ended 2018, following are few of the

areas of concern which were noted while doing audit planning:

a. Area of Concern-

Rebates from the suppliers – the Group receives rebates from the suppliers which include

normal purchase discounts, discounts based on purchase or sales volume and based on

contribution towards any product promotions done for the suppliers. Such discounts need to

be shown either as reduction from the inventory value or reduction from the cost of sales as

per the nature of rebate received.

The main concern in this account is the authenticity and accuracy of rebate figures which

need to be checked, especially those of nonstandard nature. Also, the recording and

accounting treatment of the rebates are of concern matter.

Further, the Group has shown the Supplier Rebates as an inclusion in the trade receivables of

an amount equal to $100m which is a very substantial amount. The inclusion of supplier

rebate indicates that the rebates have only been booked as receivable and have not been

received in the current financial year. The rebates receivable should have been shown as a

separate figure in the balance sheet to encourage transparency in the balance sheet items.

The supplier rebates are likely to affect the trade and other receivables account, inventories

account, cost of sales (CAANZ, 2016).

b. Area of Concern-

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

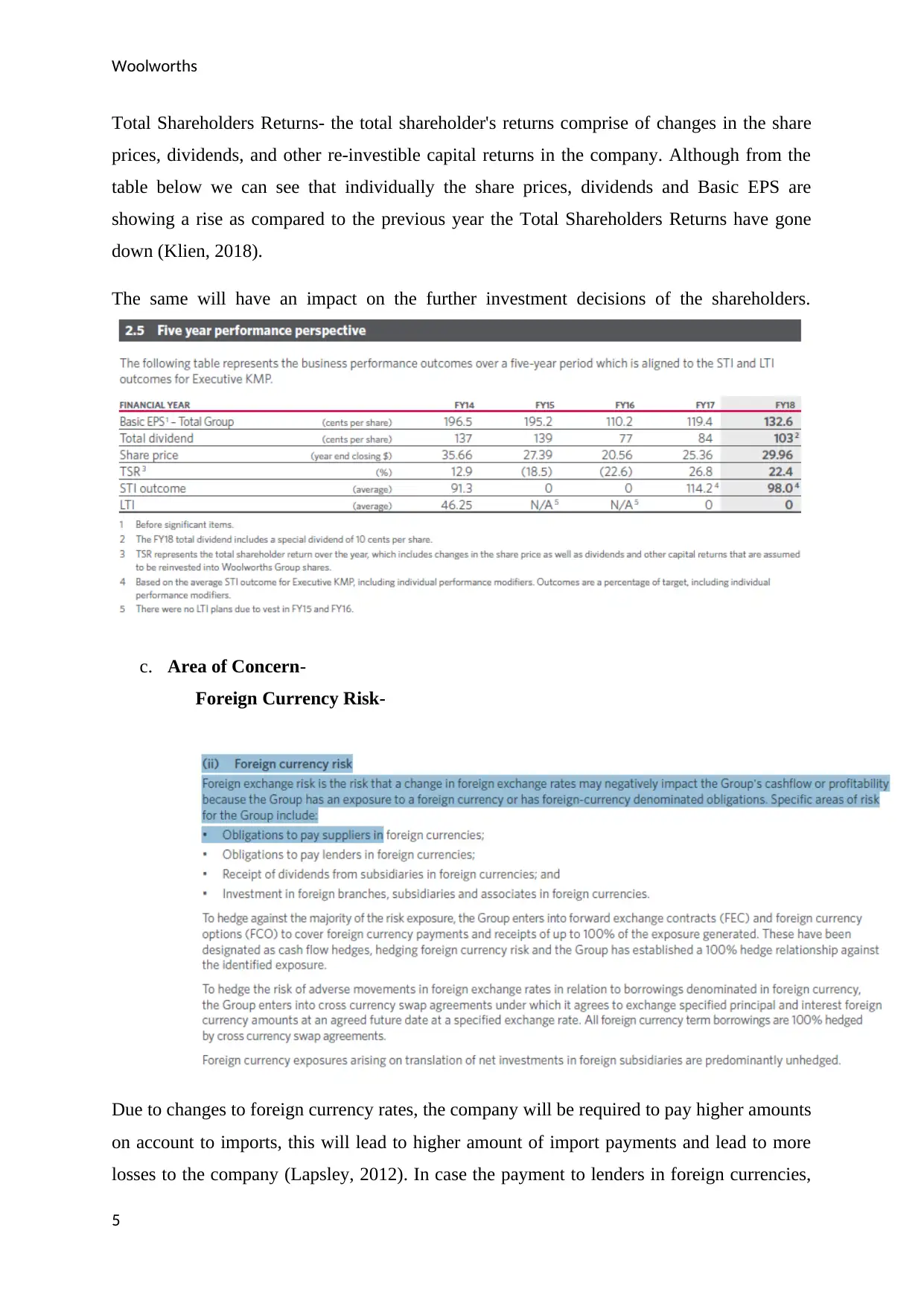

Total Shareholders Returns- the total shareholder's returns comprise of changes in the share

prices, dividends, and other re-investible capital returns in the company. Although from the

table below we can see that individually the share prices, dividends and Basic EPS are

showing a rise as compared to the previous year the Total Shareholders Returns have gone

down (Klien, 2018).

The same will have an impact on the further investment decisions of the shareholders.

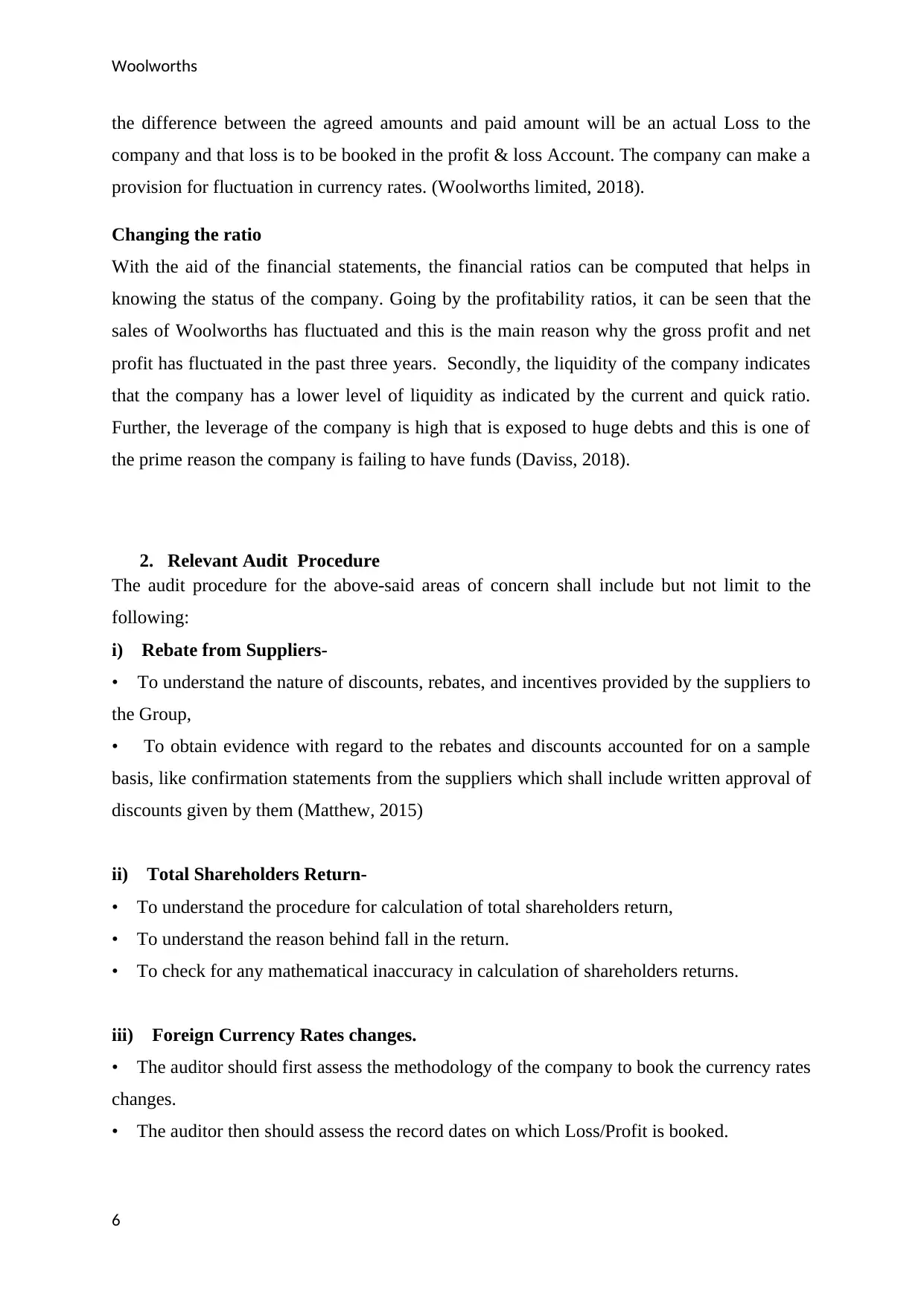

c. Area of Concern-

Foreign Currency Risk-

Due to changes to foreign currency rates, the company will be required to pay higher amounts

on account to imports, this will lead to higher amount of import payments and lead to more

losses to the company (Lapsley, 2012). In case the payment to lenders in foreign currencies,

5

Total Shareholders Returns- the total shareholder's returns comprise of changes in the share

prices, dividends, and other re-investible capital returns in the company. Although from the

table below we can see that individually the share prices, dividends and Basic EPS are

showing a rise as compared to the previous year the Total Shareholders Returns have gone

down (Klien, 2018).

The same will have an impact on the further investment decisions of the shareholders.

c. Area of Concern-

Foreign Currency Risk-

Due to changes to foreign currency rates, the company will be required to pay higher amounts

on account to imports, this will lead to higher amount of import payments and lead to more

losses to the company (Lapsley, 2012). In case the payment to lenders in foreign currencies,

5

Woolworths

the difference between the agreed amounts and paid amount will be an actual Loss to the

company and that loss is to be booked in the profit & loss Account. The company can make a

provision for fluctuation in currency rates. (Woolworths limited, 2018).

Changing the ratio

With the aid of the financial statements, the financial ratios can be computed that helps in

knowing the status of the company. Going by the profitability ratios, it can be seen that the

sales of Woolworths has fluctuated and this is the main reason why the gross profit and net

profit has fluctuated in the past three years. Secondly, the liquidity of the company indicates

that the company has a lower level of liquidity as indicated by the current and quick ratio.

Further, the leverage of the company is high that is exposed to huge debts and this is one of

the prime reason the company is failing to have funds (Daviss, 2018).

2. Relevant Audit Procedure

The audit procedure for the above-said areas of concern shall include but not limit to the

following:

i) Rebate from Suppliers-

• To understand the nature of discounts, rebates, and incentives provided by the suppliers to

the Group,

• To obtain evidence with regard to the rebates and discounts accounted for on a sample

basis, like confirmation statements from the suppliers which shall include written approval of

discounts given by them (Matthew, 2015)

ii) Total Shareholders Return-

• To understand the procedure for calculation of total shareholders return,

• To understand the reason behind fall in the return.

• To check for any mathematical inaccuracy in calculation of shareholders returns.

iii) Foreign Currency Rates changes.

• The auditor should first assess the methodology of the company to book the currency rates

changes.

• The auditor then should assess the record dates on which Loss/Profit is booked.

6

the difference between the agreed amounts and paid amount will be an actual Loss to the

company and that loss is to be booked in the profit & loss Account. The company can make a

provision for fluctuation in currency rates. (Woolworths limited, 2018).

Changing the ratio

With the aid of the financial statements, the financial ratios can be computed that helps in

knowing the status of the company. Going by the profitability ratios, it can be seen that the

sales of Woolworths has fluctuated and this is the main reason why the gross profit and net

profit has fluctuated in the past three years. Secondly, the liquidity of the company indicates

that the company has a lower level of liquidity as indicated by the current and quick ratio.

Further, the leverage of the company is high that is exposed to huge debts and this is one of

the prime reason the company is failing to have funds (Daviss, 2018).

2. Relevant Audit Procedure

The audit procedure for the above-said areas of concern shall include but not limit to the

following:

i) Rebate from Suppliers-

• To understand the nature of discounts, rebates, and incentives provided by the suppliers to

the Group,

• To obtain evidence with regard to the rebates and discounts accounted for on a sample

basis, like confirmation statements from the suppliers which shall include written approval of

discounts given by them (Matthew, 2015)

ii) Total Shareholders Return-

• To understand the procedure for calculation of total shareholders return,

• To understand the reason behind fall in the return.

• To check for any mathematical inaccuracy in calculation of shareholders returns.

iii) Foreign Currency Rates changes.

• The auditor should first assess the methodology of the company to book the currency rates

changes.

• The auditor then should assess the record dates on which Loss/Profit is booked.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

• In case the change in currency is permanent, the asset or Liability can be written off. The

procedure should be well documented and disclosed in notes to accounts.

• The effect of changes in foreign currency rates should be properly disclosed in the

financial statements. The stakeholders are entitled to know the extent of Losses or profits on

this font .

iv) Analysis of the ratio

The auditor should check the sales pattern and the reason why the sales increased with the

increment in inventory level. This difference should be ascertained by having an insight on

the sales made by the company and the stock left behind. The drop in the liquidity ratio

should be provided adequate attention and the reason for the falling current assets should be

traced by comparison with the old figures (Melville, 2013)

B. Corporate Governance.

1. Reporting under corporate governance

Yes, Woolworths Group Limited has a process of Corporate Governance. The Group’s

Board & its Management team are deeply committed to policies and practices that can be

seen from its level of disclosures and compliances. The Group follows all the

recommendations of ASX Corporate Council’s Corporate Governance Principles &

Recommendations which it has followed throughout the year ended 2018 which can be

seen from the Corporate Governance Statement issued by the Group (Woolworths limited

CG, 2018).

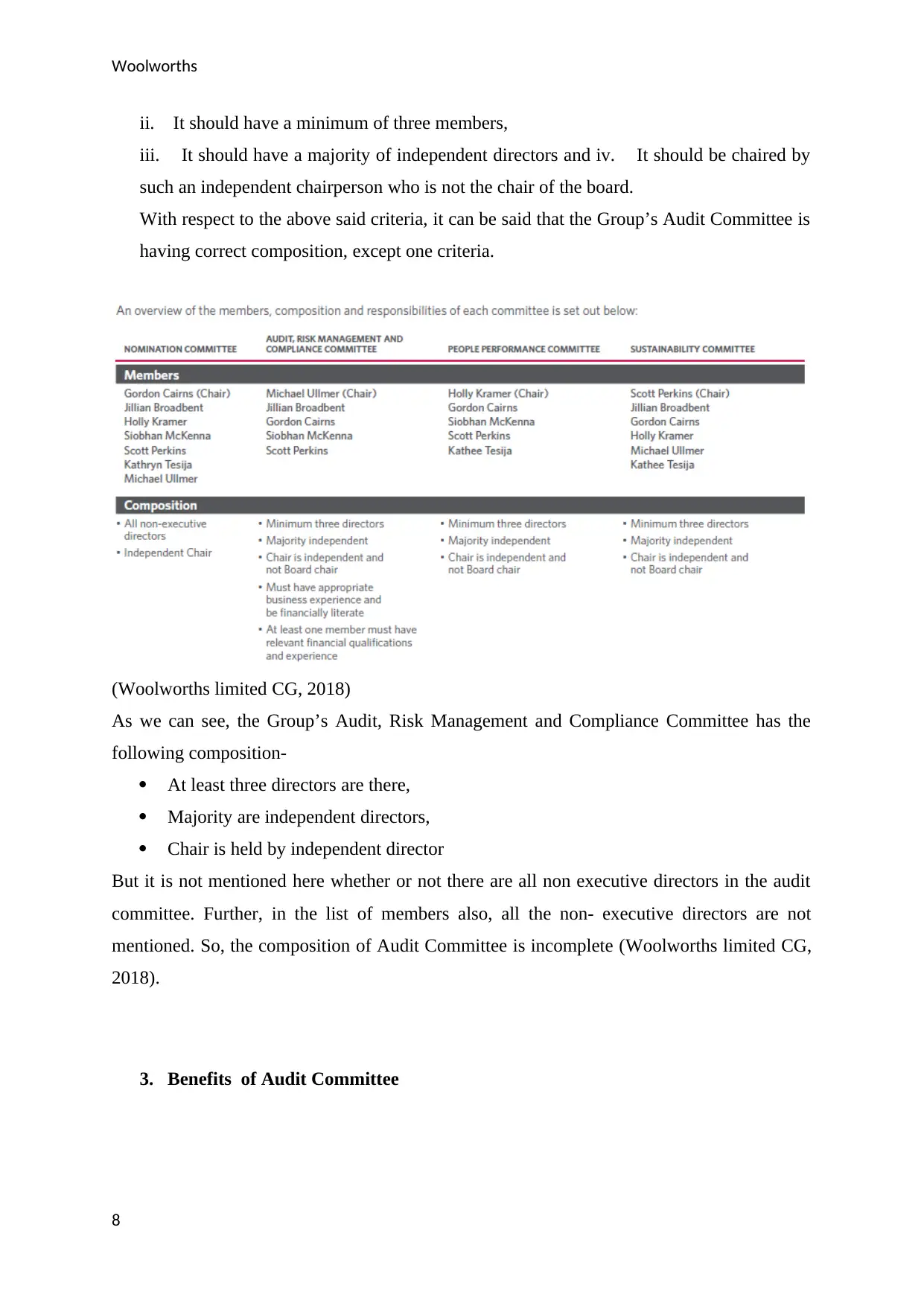

2. Audit Committee

Yes, the Group has an Audit committee with the name Audit, Risk Management &

Compliance Committee.

Under the ASX Listing Rules and Corporate Governance Guidelines, there are various

recommendations for the listed companies on the Australian Stock Exchange. One of the

recommendations of ASX Rules namely Principle 4 states that a listed company needs to

have formal and set processes for independent verification and safeguarding of the

integrity of its corporate reporting (Woolworths limited CG, 2018). For this an Audit

Committee is formed which should meet the following composition criteria:

i. The audit committee should consist of only non-executive directors,

7

• In case the change in currency is permanent, the asset or Liability can be written off. The

procedure should be well documented and disclosed in notes to accounts.

• The effect of changes in foreign currency rates should be properly disclosed in the

financial statements. The stakeholders are entitled to know the extent of Losses or profits on

this font .

iv) Analysis of the ratio

The auditor should check the sales pattern and the reason why the sales increased with the

increment in inventory level. This difference should be ascertained by having an insight on

the sales made by the company and the stock left behind. The drop in the liquidity ratio

should be provided adequate attention and the reason for the falling current assets should be

traced by comparison with the old figures (Melville, 2013)

B. Corporate Governance.

1. Reporting under corporate governance

Yes, Woolworths Group Limited has a process of Corporate Governance. The Group’s

Board & its Management team are deeply committed to policies and practices that can be

seen from its level of disclosures and compliances. The Group follows all the

recommendations of ASX Corporate Council’s Corporate Governance Principles &

Recommendations which it has followed throughout the year ended 2018 which can be

seen from the Corporate Governance Statement issued by the Group (Woolworths limited

CG, 2018).

2. Audit Committee

Yes, the Group has an Audit committee with the name Audit, Risk Management &

Compliance Committee.

Under the ASX Listing Rules and Corporate Governance Guidelines, there are various

recommendations for the listed companies on the Australian Stock Exchange. One of the

recommendations of ASX Rules namely Principle 4 states that a listed company needs to

have formal and set processes for independent verification and safeguarding of the

integrity of its corporate reporting (Woolworths limited CG, 2018). For this an Audit

Committee is formed which should meet the following composition criteria:

i. The audit committee should consist of only non-executive directors,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

ii. It should have a minimum of three members,

iii. It should have a majority of independent directors and iv. It should be chaired by

such an independent chairperson who is not the chair of the board.

With respect to the above said criteria, it can be said that the Group’s Audit Committee is

having correct composition, except one criteria.

(Woolworths limited CG, 2018)

As we can see, the Group’s Audit, Risk Management and Compliance Committee has the

following composition-

At least three directors are there,

Majority are independent directors,

Chair is held by independent director

But it is not mentioned here whether or not there are all non executive directors in the audit

committee. Further, in the list of members also, all the non- executive directors are not

mentioned. So, the composition of Audit Committee is incomplete (Woolworths limited CG,

2018).

3. Benefits of Audit Committee

8

ii. It should have a minimum of three members,

iii. It should have a majority of independent directors and iv. It should be chaired by

such an independent chairperson who is not the chair of the board.

With respect to the above said criteria, it can be said that the Group’s Audit Committee is

having correct composition, except one criteria.

(Woolworths limited CG, 2018)

As we can see, the Group’s Audit, Risk Management and Compliance Committee has the

following composition-

At least three directors are there,

Majority are independent directors,

Chair is held by independent director

But it is not mentioned here whether or not there are all non executive directors in the audit

committee. Further, in the list of members also, all the non- executive directors are not

mentioned. So, the composition of Audit Committee is incomplete (Woolworths limited CG,

2018).

3. Benefits of Audit Committee

8

Woolworths

The Audit Committee has various roles and responsibilities which provides benefits to

various persons like auditors, company, the auditing profession and the society as a whole

(Oshry, Hermalin & Weisbach, 2010).

The roles and responsibilities of the Audit Committee have been mentioned in the Corporate

Governance Statement by the Company which directly or indirectly benefit the auditors,

company board, society, etc (Woolworths limited CG, 2018). The audit committee makes

recommendations about the external auditors and about the lead audit partner for the audit of

the relevant period to the Board of the company. Further, the committee is responsible for

monitoring and reviewing of the key policies of the company which benefits the company

(Woolworths limited CG, 2018). The committee reviews and monitors the internal control

processes for its nature, extent, and effectiveness. The committee helps the Board by

reviewing the performance of external auditors on an annual basis. With regard to the internal

audit, the committee keeps a check on the quality of work and effectiveness of work of the

internal audit team.

Conclusion

From the overall analysis, a clear picture about Woolworths that the financial report provides

a complete information regarding the company’s functioning. Furthermore, from the analysis

it is clear that the financial performance of the company is lacking the momentum as all ratios

are not able to perform or meet the desired target. Hence, it is imperative for the management

to spot the weak areas and work on it in an effective manner. In terms of disclosure, the

company has provided adequate data and the corporate governance of the company is

effectively laid down.

9

The Audit Committee has various roles and responsibilities which provides benefits to

various persons like auditors, company, the auditing profession and the society as a whole

(Oshry, Hermalin & Weisbach, 2010).

The roles and responsibilities of the Audit Committee have been mentioned in the Corporate

Governance Statement by the Company which directly or indirectly benefit the auditors,

company board, society, etc (Woolworths limited CG, 2018). The audit committee makes

recommendations about the external auditors and about the lead audit partner for the audit of

the relevant period to the Board of the company. Further, the committee is responsible for

monitoring and reviewing of the key policies of the company which benefits the company

(Woolworths limited CG, 2018). The committee reviews and monitors the internal control

processes for its nature, extent, and effectiveness. The committee helps the Board by

reviewing the performance of external auditors on an annual basis. With regard to the internal

audit, the committee keeps a check on the quality of work and effectiveness of work of the

internal audit team.

Conclusion

From the overall analysis, a clear picture about Woolworths that the financial report provides

a complete information regarding the company’s functioning. Furthermore, from the analysis

it is clear that the financial performance of the company is lacking the momentum as all ratios

are not able to perform or meet the desired target. Hence, it is imperative for the management

to spot the weak areas and work on it in an effective manner. In terms of disclosure, the

company has provided adequate data and the corporate governance of the company is

effectively laid down.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

References

CAANZ. (2016) Auditing, and Assurance Handbook 2016 Australia. Australia: John Wiley

& Sons.

Cooper , B. and Coram, P. (2015) Modern Auditing & Assurance Services. 6th ed. Australia:

Wiley.

Daviss, A. (2018) Woolworths Growth Hits Two-Year Low. Available from:

https://www.powerretail.com.au/news/woolworths-growth-slows/ [Accessed 15 May 2019]

Klien, M. (2018) Woolies showing signs of better performance. Available from:

https://www.moneyweb.co.za/news/companies-and-deals/woolies-showing-signs-of-better-

performance/ [Accessed 15 May 2019]

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. 9(3), pp. 291-292. https://doi.org/10.1111/1468-

0408.00081

Leo, K. J. (2011). Company Accounting. Boston:McGraw Hill

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. 90(2), p. 495-527. Available from:

https://doi.org/10.2308/accr-50871 [Accessed 16 May 2019]

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. 24(3), 1-34. Available from

https://pdfs.semanticscholar.org/6ccf/f78a452763f17ed5e4f4ddc6b96703801403.pdf

[Accessed 16 May 2019]

Oshry, B., Hermalin, B.E. & Weisbach, M.S. (2010) The role of boards of directors in

corporate governance: A conceptual framework and survey. Journal of Economic Literature,

48(1), 58-107. Available from:

https://cpb-us-w2.wpmucdn.com/u.osu.edu/dist/8/7843/files/2015/01/AdamsHWJEL2010-

2ff7jzc.pdf [Accessed 15 May 2019]

Osuala, C. (2015) Introduction to accounting theory, 3rd Edition. Enugu, Africana First

Publishers Limited

10

References

CAANZ. (2016) Auditing, and Assurance Handbook 2016 Australia. Australia: John Wiley

& Sons.

Cooper , B. and Coram, P. (2015) Modern Auditing & Assurance Services. 6th ed. Australia:

Wiley.

Daviss, A. (2018) Woolworths Growth Hits Two-Year Low. Available from:

https://www.powerretail.com.au/news/woolworths-growth-slows/ [Accessed 15 May 2019]

Klien, M. (2018) Woolies showing signs of better performance. Available from:

https://www.moneyweb.co.za/news/companies-and-deals/woolies-showing-signs-of-better-

performance/ [Accessed 15 May 2019]

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. 9(3), pp. 291-292. https://doi.org/10.1111/1468-

0408.00081

Leo, K. J. (2011). Company Accounting. Boston:McGraw Hill

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. 90(2), p. 495-527. Available from:

https://doi.org/10.2308/accr-50871 [Accessed 16 May 2019]

Melville, A. (2013) International Financial Reporting – A Practical Guide. 4th edition.

Merchant, K. A. (2012) Making Management Accounting Research More Useful. Pacific

Accounting Review. 24(3), 1-34. Available from

https://pdfs.semanticscholar.org/6ccf/f78a452763f17ed5e4f4ddc6b96703801403.pdf

[Accessed 16 May 2019]

Oshry, B., Hermalin, B.E. & Weisbach, M.S. (2010) The role of boards of directors in

corporate governance: A conceptual framework and survey. Journal of Economic Literature,

48(1), 58-107. Available from:

https://cpb-us-w2.wpmucdn.com/u.osu.edu/dist/8/7843/files/2015/01/AdamsHWJEL2010-

2ff7jzc.pdf [Accessed 15 May 2019]

Osuala, C. (2015) Introduction to accounting theory, 3rd Edition. Enugu, Africana First

Publishers Limited

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

Parrino, R, Kidwell, D. and Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

NJ: Wiley. Pearson, Education Limited, UK

Woolworths limited CG. (2018) Woolworths limited Corporate governance 2018. Available

from: https://www.woolworthsgroup.com.au/content/Document/2018%20Corporate

%20Governance%20Statement.pdf [Accessed 16 May 2019]

Woolworths limited. (2018) Woolworths limited Annual Report and accounts 2018. Available

from: https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/

Reports/Annual_Reports [Accessed 16 May 2019]

11

Parrino, R, Kidwell, D. and Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

NJ: Wiley. Pearson, Education Limited, UK

Woolworths limited CG. (2018) Woolworths limited Corporate governance 2018. Available

from: https://www.woolworthsgroup.com.au/content/Document/2018%20Corporate

%20Governance%20Statement.pdf [Accessed 16 May 2019]

Woolworths limited. (2018) Woolworths limited Annual Report and accounts 2018. Available

from: https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/

Reports/Annual_Reports [Accessed 16 May 2019]

11

Woolworths

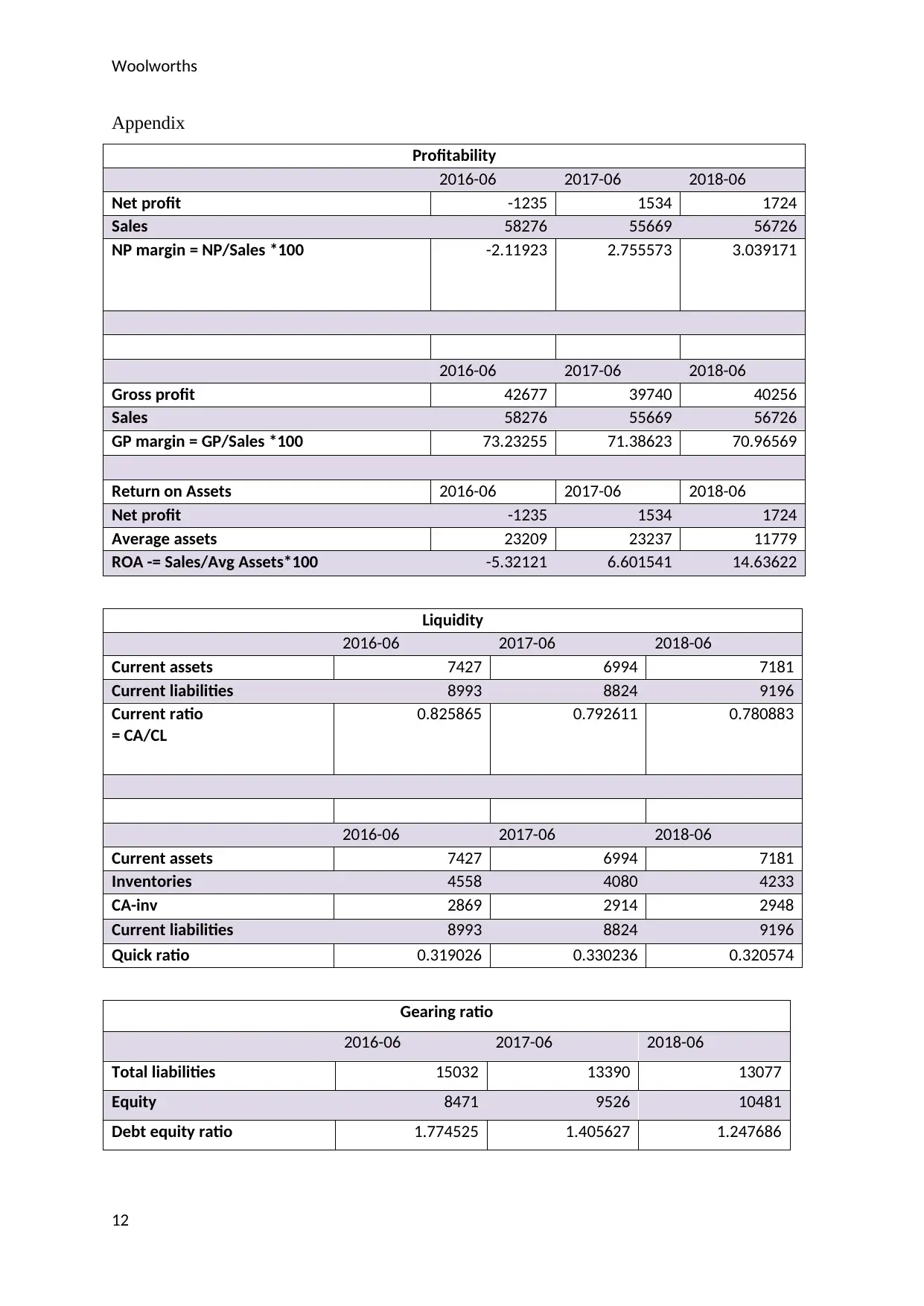

Appendix

Profitability

2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Sales 58276 55669 56726

NP margin = NP/Sales *100 -2.11923 2.755573 3.039171

2016-06 2017-06 2018-06

Gross profit 42677 39740 40256

Sales 58276 55669 56726

GP margin = GP/Sales *100 73.23255 71.38623 70.96569

Return on Assets 2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Average assets 23209 23237 11779

ROA -= Sales/Avg Assets*100 -5.32121 6.601541 14.63622

Liquidity

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

Current liabilities 8993 8824 9196

Current ratio

= CA/CL

0.825865 0.792611 0.780883

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

Inventories 4558 4080 4233

CA-inv 2869 2914 2948

Current liabilities 8993 8824 9196

Quick ratio 0.319026 0.330236 0.320574

Gearing ratio

2016-06 2017-06 2018-06

Total liabilities 15032 13390 13077

Equity 8471 9526 10481

Debt equity ratio 1.774525 1.405627 1.247686

12

Appendix

Profitability

2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Sales 58276 55669 56726

NP margin = NP/Sales *100 -2.11923 2.755573 3.039171

2016-06 2017-06 2018-06

Gross profit 42677 39740 40256

Sales 58276 55669 56726

GP margin = GP/Sales *100 73.23255 71.38623 70.96569

Return on Assets 2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Average assets 23209 23237 11779

ROA -= Sales/Avg Assets*100 -5.32121 6.601541 14.63622

Liquidity

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

Current liabilities 8993 8824 9196

Current ratio

= CA/CL

0.825865 0.792611 0.780883

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

Inventories 4558 4080 4233

CA-inv 2869 2914 2948

Current liabilities 8993 8824 9196

Quick ratio 0.319026 0.330236 0.320574

Gearing ratio

2016-06 2017-06 2018-06

Total liabilities 15032 13390 13077

Equity 8471 9526 10481

Debt equity ratio 1.774525 1.405627 1.247686

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.