Factors Influencing Superannuation Plan Choices in Australia

VerifiedAdded on 2022/11/16

|11

|3034

|125

Report

AI Summary

This report provides a comprehensive analysis of superannuation in Australia, focusing on the factors that tertiary sector employees should consider when choosing between a Defined Benefit Plan and an Investment Choice Plan. It delves into the specifics of superannuation, including preserved, restricted non-preserved, and unrestricted non-preserved benefits, as well as different plan types like Defined Benefit and Investment Choice plans. The report also explores the various types of superannuation funds, such as public sector, corporate, industry, self-managed, and public offer funds. Furthermore, it highlights the key factors influencing employees' choices, including the impact of taxes, opportunity cost, and the time value of money. The report includes relevant graphs, a conclusion, and recommendations, and is supported by numerous references from peer-reviewed journals and articles, adhering to the specified formatting guidelines.

Superannuation in Australia 1

SUPERANNUATION IN AUSTRALIAN

By Students Name

Course Code

Professor

City, State

Date

SUPERANNUATION IN AUSTRALIAN

By Students Name

Course Code

Professor

City, State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation in Australia 2

Table of Contents

Executive Summary.........................................................................................................................3

Superannuation................................................................................................................................3

Introduction......................................................................................................................................3

Superannuation in Australia............................................................................................................3

Preserved benefits:................................................................................................................5

Restricted non-preserved benefits:.......................................................................................5

Unrestricted non-preserved benefits:....................................................................................5

Types of superannuation Plans........................................................................................................5

Defined benefits plan...................................................................................................................5

Investment Choice Plan...............................................................................................................6

Types of Funds................................................................................................................................6

Factors Considered by Tertiary Employees in Choosing Benefits Scheme....................................7

Taxes............................................................................................................................................7

Opportunity cost...........................................................................................................................7

Time value of money...................................................................................................................7

Conclusion.......................................................................................................................................8

Recommendation.............................................................................................................................8

References........................................................................................................................................9

Table of Contents

Executive Summary.........................................................................................................................3

Superannuation................................................................................................................................3

Introduction......................................................................................................................................3

Superannuation in Australia............................................................................................................3

Preserved benefits:................................................................................................................5

Restricted non-preserved benefits:.......................................................................................5

Unrestricted non-preserved benefits:....................................................................................5

Types of superannuation Plans........................................................................................................5

Defined benefits plan...................................................................................................................5

Investment Choice Plan...............................................................................................................6

Types of Funds................................................................................................................................6

Factors Considered by Tertiary Employees in Choosing Benefits Scheme....................................7

Taxes............................................................................................................................................7

Opportunity cost...........................................................................................................................7

Time value of money...................................................................................................................7

Conclusion.......................................................................................................................................8

Recommendation.............................................................................................................................8

References........................................................................................................................................9

Superannuation in Australia 3

Executive Summary

Every individual is wary of a rocky retirement based on the fact that at retirement, one will stop

working, and as a result, the flow of income will stop. This is a problem to governments as well

who struggle to provide retirement pension to its employees. This retirement security has made

individual forgo part of their current income in order to secure their future. Governments have

also been involved through legislation passing on saving and regulation of the funds. In this case,

the main aim of the savings is to secure the future and ensure decent retirement benefits that will

enable individual to afford basic amenities. This reduces the burden for the government since

individuals are responsible for their own retirement benefits.

Superannuation

Introduction

Superannuation refers to contribution to pension plans for purposes of saving for retirement. The

contribution can either be made by the individual employed or by the employer. Policies and

regulations exist in most countries that govern super annunciation. The policies in some

countries include the minimum contribution and the contributor. Some policies require the

employer to make the contribution while for some, both the employer and employee contribute

(Gallery, Newton, and Palm, 2011). The money contributed are deposited in funds that are

managed and invested in order to earn interest, which is paid to the contributors to compensate

for the time value of money. The funds contributed to superannuation are not drawable until

retirement. However, these funds can be withdrawn when the contributor is diagnosed with

terminal illnesses or any other genuine reasons that render the contributor incapable of

continuing with the scheme (Kristjanpoller, and Olson, 2015). The body charged with ensuring

compliance is the Australian Prudential Regulatory Authority while conflict resolutions are

channeled through the Superannuation Complaints Tribunal. Compliance in the investment of

funds falls under the jurisdiction of The Australian Securities and Investment Commission

(ASIC). These are the main bodies involved in the superannuation regulation, although there

exists’ other bodies that work in hand with the three.

Executive Summary

Every individual is wary of a rocky retirement based on the fact that at retirement, one will stop

working, and as a result, the flow of income will stop. This is a problem to governments as well

who struggle to provide retirement pension to its employees. This retirement security has made

individual forgo part of their current income in order to secure their future. Governments have

also been involved through legislation passing on saving and regulation of the funds. In this case,

the main aim of the savings is to secure the future and ensure decent retirement benefits that will

enable individual to afford basic amenities. This reduces the burden for the government since

individuals are responsible for their own retirement benefits.

Superannuation

Introduction

Superannuation refers to contribution to pension plans for purposes of saving for retirement. The

contribution can either be made by the individual employed or by the employer. Policies and

regulations exist in most countries that govern super annunciation. The policies in some

countries include the minimum contribution and the contributor. Some policies require the

employer to make the contribution while for some, both the employer and employee contribute

(Gallery, Newton, and Palm, 2011). The money contributed are deposited in funds that are

managed and invested in order to earn interest, which is paid to the contributors to compensate

for the time value of money. The funds contributed to superannuation are not drawable until

retirement. However, these funds can be withdrawn when the contributor is diagnosed with

terminal illnesses or any other genuine reasons that render the contributor incapable of

continuing with the scheme (Kristjanpoller, and Olson, 2015). The body charged with ensuring

compliance is the Australian Prudential Regulatory Authority while conflict resolutions are

channeled through the Superannuation Complaints Tribunal. Compliance in the investment of

funds falls under the jurisdiction of The Australian Securities and Investment Commission

(ASIC). These are the main bodies involved in the superannuation regulation, although there

exists’ other bodies that work in hand with the three.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation in Australia 4

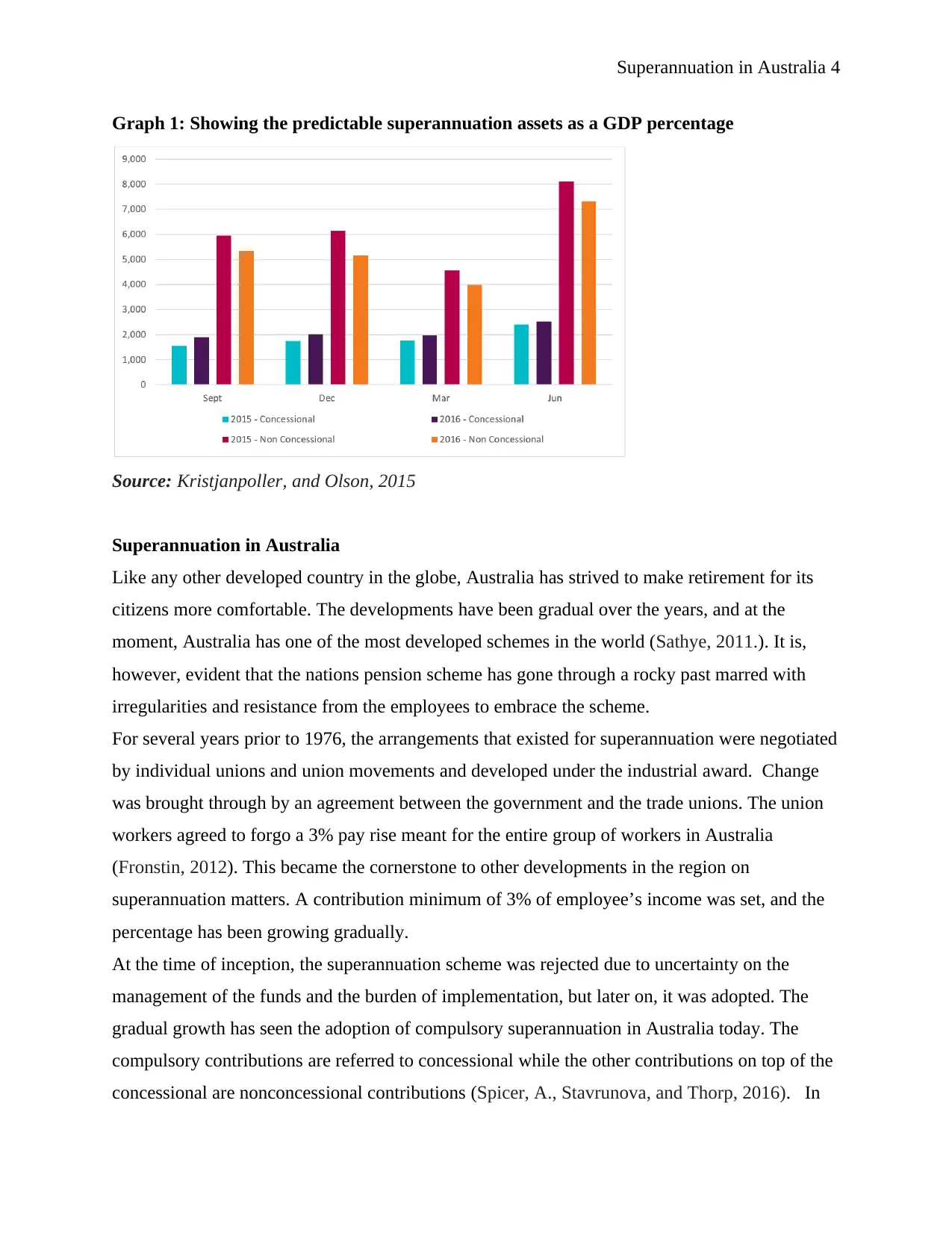

Graph 1: Showing the predictable superannuation assets as a GDP percentage

Source: Kristjanpoller, and Olson, 2015

Superannuation in Australia

Like any other developed country in the globe, Australia has strived to make retirement for its

citizens more comfortable. The developments have been gradual over the years, and at the

moment, Australia has one of the most developed schemes in the world (Sathye, 2011.). It is,

however, evident that the nations pension scheme has gone through a rocky past marred with

irregularities and resistance from the employees to embrace the scheme.

For several years prior to 1976, the arrangements that existed for superannuation were negotiated

by individual unions and union movements and developed under the industrial award. Change

was brought through by an agreement between the government and the trade unions. The union

workers agreed to forgo a 3% pay rise meant for the entire group of workers in Australia

(Fronstin, 2012). This became the cornerstone to other developments in the region on

superannuation matters. A contribution minimum of 3% of employee’s income was set, and the

percentage has been growing gradually.

At the time of inception, the superannuation scheme was rejected due to uncertainty on the

management of the funds and the burden of implementation, but later on, it was adopted. The

gradual growth has seen the adoption of compulsory superannuation in Australia today. The

compulsory contributions are referred to concessional while the other contributions on top of the

concessional are nonconcessional contributions (Spicer, A., Stavrunova, and Thorp, 2016). In

Graph 1: Showing the predictable superannuation assets as a GDP percentage

Source: Kristjanpoller, and Olson, 2015

Superannuation in Australia

Like any other developed country in the globe, Australia has strived to make retirement for its

citizens more comfortable. The developments have been gradual over the years, and at the

moment, Australia has one of the most developed schemes in the world (Sathye, 2011.). It is,

however, evident that the nations pension scheme has gone through a rocky past marred with

irregularities and resistance from the employees to embrace the scheme.

For several years prior to 1976, the arrangements that existed for superannuation were negotiated

by individual unions and union movements and developed under the industrial award. Change

was brought through by an agreement between the government and the trade unions. The union

workers agreed to forgo a 3% pay rise meant for the entire group of workers in Australia

(Fronstin, 2012). This became the cornerstone to other developments in the region on

superannuation matters. A contribution minimum of 3% of employee’s income was set, and the

percentage has been growing gradually.

At the time of inception, the superannuation scheme was rejected due to uncertainty on the

management of the funds and the burden of implementation, but later on, it was adopted. The

gradual growth has seen the adoption of compulsory superannuation in Australia today. The

compulsory contributions are referred to concessional while the other contributions on top of the

concessional are nonconcessional contributions (Spicer, A., Stavrunova, and Thorp, 2016). In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation in Australia 5

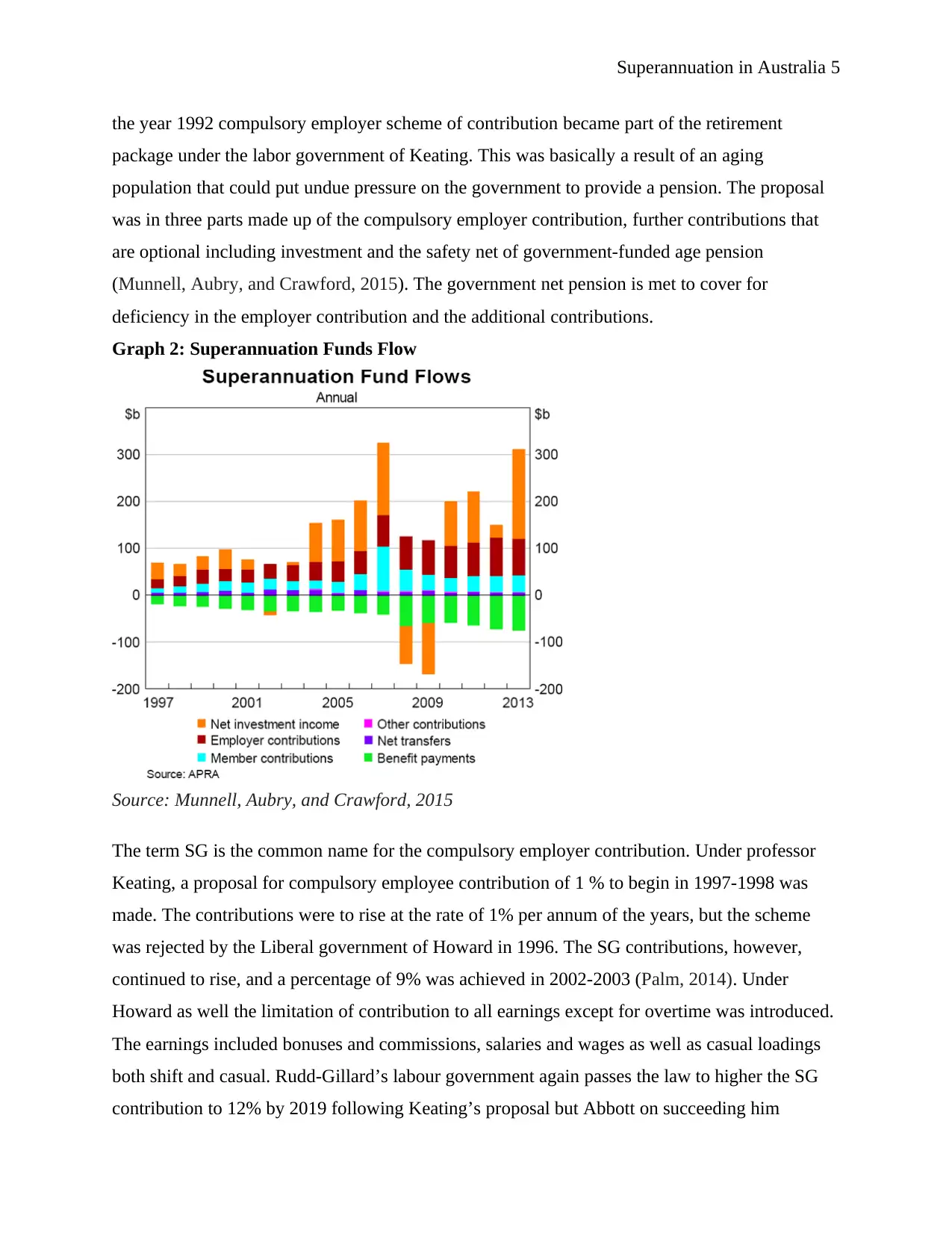

the year 1992 compulsory employer scheme of contribution became part of the retirement

package under the labor government of Keating. This was basically a result of an aging

population that could put undue pressure on the government to provide a pension. The proposal

was in three parts made up of the compulsory employer contribution, further contributions that

are optional including investment and the safety net of government-funded age pension

(Munnell, Aubry, and Crawford, 2015). The government net pension is met to cover for

deficiency in the employer contribution and the additional contributions.

Graph 2: Superannuation Funds Flow

Source: Munnell, Aubry, and Crawford, 2015

The term SG is the common name for the compulsory employer contribution. Under professor

Keating, a proposal for compulsory employee contribution of 1 % to begin in 1997-1998 was

made. The contributions were to rise at the rate of 1% per annum of the years, but the scheme

was rejected by the Liberal government of Howard in 1996. The SG contributions, however,

continued to rise, and a percentage of 9% was achieved in 2002-2003 (Palm, 2014). Under

Howard as well the limitation of contribution to all earnings except for overtime was introduced.

The earnings included bonuses and commissions, salaries and wages as well as casual loadings

both shift and casual. Rudd-Gillard’s labour government again passes the law to higher the SG

contribution to 12% by 2019 following Keating’s proposal but Abbott on succeeding him

the year 1992 compulsory employer scheme of contribution became part of the retirement

package under the labor government of Keating. This was basically a result of an aging

population that could put undue pressure on the government to provide a pension. The proposal

was in three parts made up of the compulsory employer contribution, further contributions that

are optional including investment and the safety net of government-funded age pension

(Munnell, Aubry, and Crawford, 2015). The government net pension is met to cover for

deficiency in the employer contribution and the additional contributions.

Graph 2: Superannuation Funds Flow

Source: Munnell, Aubry, and Crawford, 2015

The term SG is the common name for the compulsory employer contribution. Under professor

Keating, a proposal for compulsory employee contribution of 1 % to begin in 1997-1998 was

made. The contributions were to rise at the rate of 1% per annum of the years, but the scheme

was rejected by the Liberal government of Howard in 1996. The SG contributions, however,

continued to rise, and a percentage of 9% was achieved in 2002-2003 (Palm, 2014). Under

Howard as well the limitation of contribution to all earnings except for overtime was introduced.

The earnings included bonuses and commissions, salaries and wages as well as casual loadings

both shift and casual. Rudd-Gillard’s labour government again passes the law to higher the SG

contribution to 12% by 2019 following Keating’s proposal but Abbott on succeeding him

Superannuation in Australia 6

deferred the commencement of the increase by six years. This made the year 1st July 2021

instead of the early planned 1st July 2015. The rate has, therefore, stood at 9.5% since the year

2014.

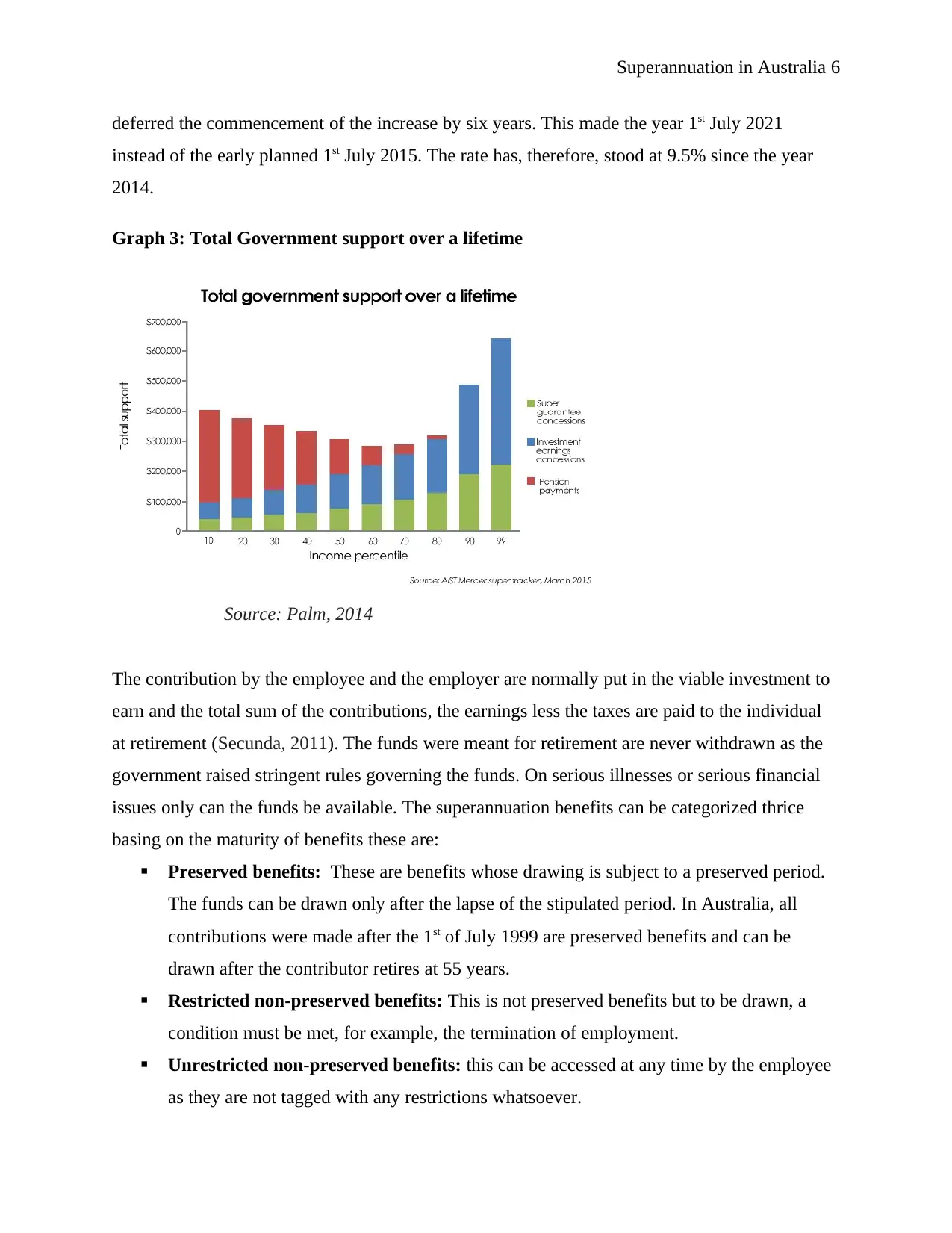

Graph 3: Total Government support over a lifetime

Source: Palm, 2014

The contribution by the employee and the employer are normally put in the viable investment to

earn and the total sum of the contributions, the earnings less the taxes are paid to the individual

at retirement (Secunda, 2011). The funds were meant for retirement are never withdrawn as the

government raised stringent rules governing the funds. On serious illnesses or serious financial

issues only can the funds be available. The superannuation benefits can be categorized thrice

basing on the maturity of benefits these are:

Preserved benefits: These are benefits whose drawing is subject to a preserved period.

The funds can be drawn only after the lapse of the stipulated period. In Australia, all

contributions were made after the 1st of July 1999 are preserved benefits and can be

drawn after the contributor retires at 55 years.

Restricted non-preserved benefits: This is not preserved benefits but to be drawn, a

condition must be met, for example, the termination of employment.

Unrestricted non-preserved benefits: this can be accessed at any time by the employee

as they are not tagged with any restrictions whatsoever.

deferred the commencement of the increase by six years. This made the year 1st July 2021

instead of the early planned 1st July 2015. The rate has, therefore, stood at 9.5% since the year

2014.

Graph 3: Total Government support over a lifetime

Source: Palm, 2014

The contribution by the employee and the employer are normally put in the viable investment to

earn and the total sum of the contributions, the earnings less the taxes are paid to the individual

at retirement (Secunda, 2011). The funds were meant for retirement are never withdrawn as the

government raised stringent rules governing the funds. On serious illnesses or serious financial

issues only can the funds be available. The superannuation benefits can be categorized thrice

basing on the maturity of benefits these are:

Preserved benefits: These are benefits whose drawing is subject to a preserved period.

The funds can be drawn only after the lapse of the stipulated period. In Australia, all

contributions were made after the 1st of July 1999 are preserved benefits and can be

drawn after the contributor retires at 55 years.

Restricted non-preserved benefits: This is not preserved benefits but to be drawn, a

condition must be met, for example, the termination of employment.

Unrestricted non-preserved benefits: this can be accessed at any time by the employee

as they are not tagged with any restrictions whatsoever.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation in Australia 7

Types of superannuation Plans

The superannuation can be categorized based on the characteristics of the scheme in terms of the

structure and how the benefits are determined. There are basically two categories one is based on

the certainty of the vested benefit while the other is based on the contributions made

(Wiatrowski, 2012.). The two schemes are that an employee should choose are; Defined benefits

scheme and the Investment choice plan.

Defined benefits plan

This is a scheme that is common with employees with high income. It is a scheme whose

benefits at retirement. They are known because of the amount to be contributed at any given

point is certain. The figures for the contributions to be made are determined actuarially, and the

risk factors in the market are factored (Sy, 2011). In this case, the contributor is not responsible

for market risk or any other occurrence, but the amount of contribution changes according to the

market. The changes made in the contributions are in line with changes in market risk of the

investment and the inflation, including other factors that affect interest earnings and the time

value of money. In this type of scheme, the contribution is majorly based on the length of time an

employee has been in service as well as the expected final salary (Gerrans, 2012). The scheme is

less common these days as it was in the previous years. The contributions are mainly employer

contributions and vest to the employee upon meeting some requirements, which are commonly

an agreed period.

Investment Choice Plan

For this type of superannuation, the benefits that will vest at the end of employment is unknown,

and there is no method to determine it certainly. The uncertainty is as a result of the inability to

determine the contribution that will be made to the scheme. The certain part for this kind of

superannuation is basically the periodic contributions made by the contributor (Dushi, and Iams,

2015.). Due to the inability to the uncertainty in the contributions, the market risks cannot be

predicted, and as a result, the contributor bears major of the risks inherent in the investments.

This plan is characterized by flexibility as the contributor can make contributions based on the

fund’s availability. The contribution is periodical mostly monthly or at least quarterly.

Types of Funds

Plan funds can be classified based on contributors. In most cases, a fund will have contributors in

the same field of employment or income generation. The funds constitute;

Types of superannuation Plans

The superannuation can be categorized based on the characteristics of the scheme in terms of the

structure and how the benefits are determined. There are basically two categories one is based on

the certainty of the vested benefit while the other is based on the contributions made

(Wiatrowski, 2012.). The two schemes are that an employee should choose are; Defined benefits

scheme and the Investment choice plan.

Defined benefits plan

This is a scheme that is common with employees with high income. It is a scheme whose

benefits at retirement. They are known because of the amount to be contributed at any given

point is certain. The figures for the contributions to be made are determined actuarially, and the

risk factors in the market are factored (Sy, 2011). In this case, the contributor is not responsible

for market risk or any other occurrence, but the amount of contribution changes according to the

market. The changes made in the contributions are in line with changes in market risk of the

investment and the inflation, including other factors that affect interest earnings and the time

value of money. In this type of scheme, the contribution is majorly based on the length of time an

employee has been in service as well as the expected final salary (Gerrans, 2012). The scheme is

less common these days as it was in the previous years. The contributions are mainly employer

contributions and vest to the employee upon meeting some requirements, which are commonly

an agreed period.

Investment Choice Plan

For this type of superannuation, the benefits that will vest at the end of employment is unknown,

and there is no method to determine it certainly. The uncertainty is as a result of the inability to

determine the contribution that will be made to the scheme. The certain part for this kind of

superannuation is basically the periodic contributions made by the contributor (Dushi, and Iams,

2015.). Due to the inability to the uncertainty in the contributions, the market risks cannot be

predicted, and as a result, the contributor bears major of the risks inherent in the investments.

This plan is characterized by flexibility as the contributor can make contributions based on the

fund’s availability. The contribution is periodical mostly monthly or at least quarterly.

Types of Funds

Plan funds can be classified based on contributors. In most cases, a fund will have contributors in

the same field of employment or income generation. The funds constitute;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation in Australia 8

Public sector funds which are funds developed specifically for the employees for the

Australian state government and the federal government. Commonwealth superannuation

scheme and the Queensland Government super are the two main examples of the public

sector funds.

Corporate funds, these are funds established by large and medium private sector

businesses for their employees. Westpac superannuation is an example of corporate

funds.

Industry funds, this type of fund are also referred to as multi-employer fund. They are the

superannuation paid by the employer to specific funds for particular care of the

employee, for example, medical care. Host plus is an example of an industry fund.

Self-managed superannuation funds are funds that are typically managed by family

members. For it to be self-managed, it has to have less than five members.

Public offer funds are superannuation that is generally available to the public.

Factors Considered by Tertiary Employees in Choosing Benefits Scheme

In making investments, employees have a number of factors to consider. The factors include

taxes, opportunity cost, and the time value of money. A contributor should analyze the factors in

order to come up with the best plan.

Taxes

Taxes are deductions from income imposed by the government. The Australian Tax Office

(ATO) is the body in charge of taxes in Australia. Through tax incentive, the government of

Australia has encouraged retirement saving by making the amounts put to superannuation tax

deductible. Benefits are also tax-free (de Zwaan, L., Brimble, and Stewart2015). In order to

utilize the tax deduction, the contributor is required to write to the fund manager concerning the

intention to make use of the incentive. With Defined benefits plans the tax liability the

contributor is liable can be determined and factored in during contribution determination. For the

investment benefits scheme, the tax liability cannot be determined. In this case, a contributor

who wants a certain amount of benefit should choose the defined benefits scheme.

Opportunity cost

Opportunity cost can be defined as the benefit of the next best alternative sacrificed in order to

take the opportunity (Benson, K.L., Hutchinson, and Sriram, 2011). In this case, in choosing a

particular scheme, the benefits derived from that particular scheme should be higher than the

Public sector funds which are funds developed specifically for the employees for the

Australian state government and the federal government. Commonwealth superannuation

scheme and the Queensland Government super are the two main examples of the public

sector funds.

Corporate funds, these are funds established by large and medium private sector

businesses for their employees. Westpac superannuation is an example of corporate

funds.

Industry funds, this type of fund are also referred to as multi-employer fund. They are the

superannuation paid by the employer to specific funds for particular care of the

employee, for example, medical care. Host plus is an example of an industry fund.

Self-managed superannuation funds are funds that are typically managed by family

members. For it to be self-managed, it has to have less than five members.

Public offer funds are superannuation that is generally available to the public.

Factors Considered by Tertiary Employees in Choosing Benefits Scheme

In making investments, employees have a number of factors to consider. The factors include

taxes, opportunity cost, and the time value of money. A contributor should analyze the factors in

order to come up with the best plan.

Taxes

Taxes are deductions from income imposed by the government. The Australian Tax Office

(ATO) is the body in charge of taxes in Australia. Through tax incentive, the government of

Australia has encouraged retirement saving by making the amounts put to superannuation tax

deductible. Benefits are also tax-free (de Zwaan, L., Brimble, and Stewart2015). In order to

utilize the tax deduction, the contributor is required to write to the fund manager concerning the

intention to make use of the incentive. With Defined benefits plans the tax liability the

contributor is liable can be determined and factored in during contribution determination. For the

investment benefits scheme, the tax liability cannot be determined. In this case, a contributor

who wants a certain amount of benefit should choose the defined benefits scheme.

Opportunity cost

Opportunity cost can be defined as the benefit of the next best alternative sacrificed in order to

take the opportunity (Benson, K.L., Hutchinson, and Sriram, 2011). In this case, in choosing a

particular scheme, the benefits derived from that particular scheme should be higher than the

Superannuation in Australia 9

benefits from the second-best scheme that was not chosen. Based on opportunity cost, a

contributor should pick an alternative that guarantees a good return.

Time value of money

The cost of postponing consumption to a future date is referred to as the time value of money.

For a contributor, the earnings from the investment by funds are the time value of the

contribution. In choosing a scheme, the contributor should choose a scheme that compensates for

the time value of the contribution and is prudent in holding the fund to prevent losses (Bateman,

Eckert, Geweke, Louviere, Thorp, and Satchell, 2012). In this case, the return from the savings in

the fund should be high enough to compensate for the time the contributor has saved. For the

defined benefits schemes the figure is already calculated and ascertained while for the vested

investment choice, the figure will never be determined.

Conclusion

In choosing a scheme, a contributor must be very keen to come up with the best available

scheme. Due diligence analysis is the best way to come up with the best of all the schemes. The

choice should, therefore, not only a stable fund but a reliable scheme as well. Following the

previous misappropriation, the contributor should find a fund with proper regulation and known

channels of arbitration in case of breach of the agreement.

Recommendation

It is highly recommended that the employees chose defined benefits scheme in a move to save on

costs as it considers the consolidation of funds. The consolidation will result in savings in terms

of funds management. The stability of contributor’s income is another determiner since defined

benefits scheme does not provide flexible contributions.

benefits from the second-best scheme that was not chosen. Based on opportunity cost, a

contributor should pick an alternative that guarantees a good return.

Time value of money

The cost of postponing consumption to a future date is referred to as the time value of money.

For a contributor, the earnings from the investment by funds are the time value of the

contribution. In choosing a scheme, the contributor should choose a scheme that compensates for

the time value of the contribution and is prudent in holding the fund to prevent losses (Bateman,

Eckert, Geweke, Louviere, Thorp, and Satchell, 2012). In this case, the return from the savings in

the fund should be high enough to compensate for the time the contributor has saved. For the

defined benefits schemes the figure is already calculated and ascertained while for the vested

investment choice, the figure will never be determined.

Conclusion

In choosing a scheme, a contributor must be very keen to come up with the best available

scheme. Due diligence analysis is the best way to come up with the best of all the schemes. The

choice should, therefore, not only a stable fund but a reliable scheme as well. Following the

previous misappropriation, the contributor should find a fund with proper regulation and known

channels of arbitration in case of breach of the agreement.

Recommendation

It is highly recommended that the employees chose defined benefits scheme in a move to save on

costs as it considers the consolidation of funds. The consolidation will result in savings in terms

of funds management. The stability of contributor’s income is another determiner since defined

benefits scheme does not provide flexible contributions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation in Australia 10

References

Bateman, H., Eckert, C., Geweke, J., Louviere, J., Thorp, S., and Satchell, S., 2012. Financial

competence and expectations formation: Evidence from Australia. Economic Record, 88(280),

pp.39-63.

Benson, K.L., Hutchinson, M., and Sriram, A., 2011. Governance in the Australian

superannuation industry. Journal of business ethics, 99(2), pp.183-200.

De Zwaan, L., Brimble, M., and Stewart, J., 2015. Member perceptions of ESG investing

through superannuation. Sustainability Accounting, Management and Policy Journal, 6(1),

pp.79-102.

Dushi, I. and Iams, H.M., 2015. The Impact of Employment and Earnings Shocks on

Contribution Behavior in Defined Contribution Plans: 2005–2009. The Journal of

Retirement, 2(4), pp.86-104.

Fronstin, P., 2012. Private health insurance exchanges and defined contribution health plans: is it

déjà vu all over again?.

Gallery, N., Newton, C. and Palm, C., 2011. Framework for assessing financial literacy and

superannuation investment choice decisions. Australasian Accounting, Business and Finance

Journal, 5(2), pp.3-22.

Gerrans, P., 2012. Retirement savings investment choices in response to the global financial

crisis: Australian evidence. Australian Journal of Management, 37(3), pp.415-439.

Kristjanpoller, W.D., and Olson, J.E., 2015. The effect of financial knowledge and demographic

variables on passive and active investment in Chile's pension plan. Journal of Pension

Economics & Finance, 14(3), pp.293-314.

Palm, C.T., 2014. Financial Literacy and Superannuation Investment Decision-making in a

choice environment: An exploratory study (Doctoral dissertation, Queensland University of

Technology).

Sathye, M., 2011. The impact of the financial crisis on the efficiency of superannuation funds:

Evidence from Australia. Journal of Law and Financial Management, 10(2), pp.16-27

Secunda, P.M., 2011. The forgotten employee benefit crisis: Multiemployer benefit plans on the

brink. Cornell JL & Pub. Poly, 21, p.77.

Spicer, A., Stavrunova, O., and Thorp, S., 2016. How portfolios evolve after retirement:

evidence from Australia. Economic Record, 92(297), pp.241-267.

References

Bateman, H., Eckert, C., Geweke, J., Louviere, J., Thorp, S., and Satchell, S., 2012. Financial

competence and expectations formation: Evidence from Australia. Economic Record, 88(280),

pp.39-63.

Benson, K.L., Hutchinson, M., and Sriram, A., 2011. Governance in the Australian

superannuation industry. Journal of business ethics, 99(2), pp.183-200.

De Zwaan, L., Brimble, M., and Stewart, J., 2015. Member perceptions of ESG investing

through superannuation. Sustainability Accounting, Management and Policy Journal, 6(1),

pp.79-102.

Dushi, I. and Iams, H.M., 2015. The Impact of Employment and Earnings Shocks on

Contribution Behavior in Defined Contribution Plans: 2005–2009. The Journal of

Retirement, 2(4), pp.86-104.

Fronstin, P., 2012. Private health insurance exchanges and defined contribution health plans: is it

déjà vu all over again?.

Gallery, N., Newton, C. and Palm, C., 2011. Framework for assessing financial literacy and

superannuation investment choice decisions. Australasian Accounting, Business and Finance

Journal, 5(2), pp.3-22.

Gerrans, P., 2012. Retirement savings investment choices in response to the global financial

crisis: Australian evidence. Australian Journal of Management, 37(3), pp.415-439.

Kristjanpoller, W.D., and Olson, J.E., 2015. The effect of financial knowledge and demographic

variables on passive and active investment in Chile's pension plan. Journal of Pension

Economics & Finance, 14(3), pp.293-314.

Palm, C.T., 2014. Financial Literacy and Superannuation Investment Decision-making in a

choice environment: An exploratory study (Doctoral dissertation, Queensland University of

Technology).

Sathye, M., 2011. The impact of the financial crisis on the efficiency of superannuation funds:

Evidence from Australia. Journal of Law and Financial Management, 10(2), pp.16-27

Secunda, P.M., 2011. The forgotten employee benefit crisis: Multiemployer benefit plans on the

brink. Cornell JL & Pub. Poly, 21, p.77.

Spicer, A., Stavrunova, O., and Thorp, S., 2016. How portfolios evolve after retirement:

evidence from Australia. Economic Record, 92(297), pp.241-267.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Superannuation in Australia 11

Sy, W.N., 2011. Redesigning choice and competition in Australian superannuation. Rotman

International Journal of Pension Management, 4(1), pp.52-61.

Mohan, N., and Zhang, T., 2014. An analysis of risk-taking behavior for public defined benefit

pension plans. Journal of Banking & Finance, 40, pp.403-419.

Munnell, A.H., Aubry, J.P., and Crawford, C.V., 2015. How has a shift to defined contribution

plans affected saving?. Center for Retirement Research at Boston College, (15-16).

Wiatrowski, W.J., 2012. The last private industry pension plans: A visual essay. Monthly Lab.

Rev., 135, p.3.

Sy, W.N., 2011. Redesigning choice and competition in Australian superannuation. Rotman

International Journal of Pension Management, 4(1), pp.52-61.

Mohan, N., and Zhang, T., 2014. An analysis of risk-taking behavior for public defined benefit

pension plans. Journal of Banking & Finance, 40, pp.403-419.

Munnell, A.H., Aubry, J.P., and Crawford, C.V., 2015. How has a shift to defined contribution

plans affected saving?. Center for Retirement Research at Boston College, (15-16).

Wiatrowski, W.J., 2012. The last private industry pension plans: A visual essay. Monthly Lab.

Rev., 135, p.3.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.