Group Presentation: Australian Supermarkets and Grocery Store Analysis

VerifiedAdded on 2023/06/04

|14

|2133

|424

Presentation

AI Summary

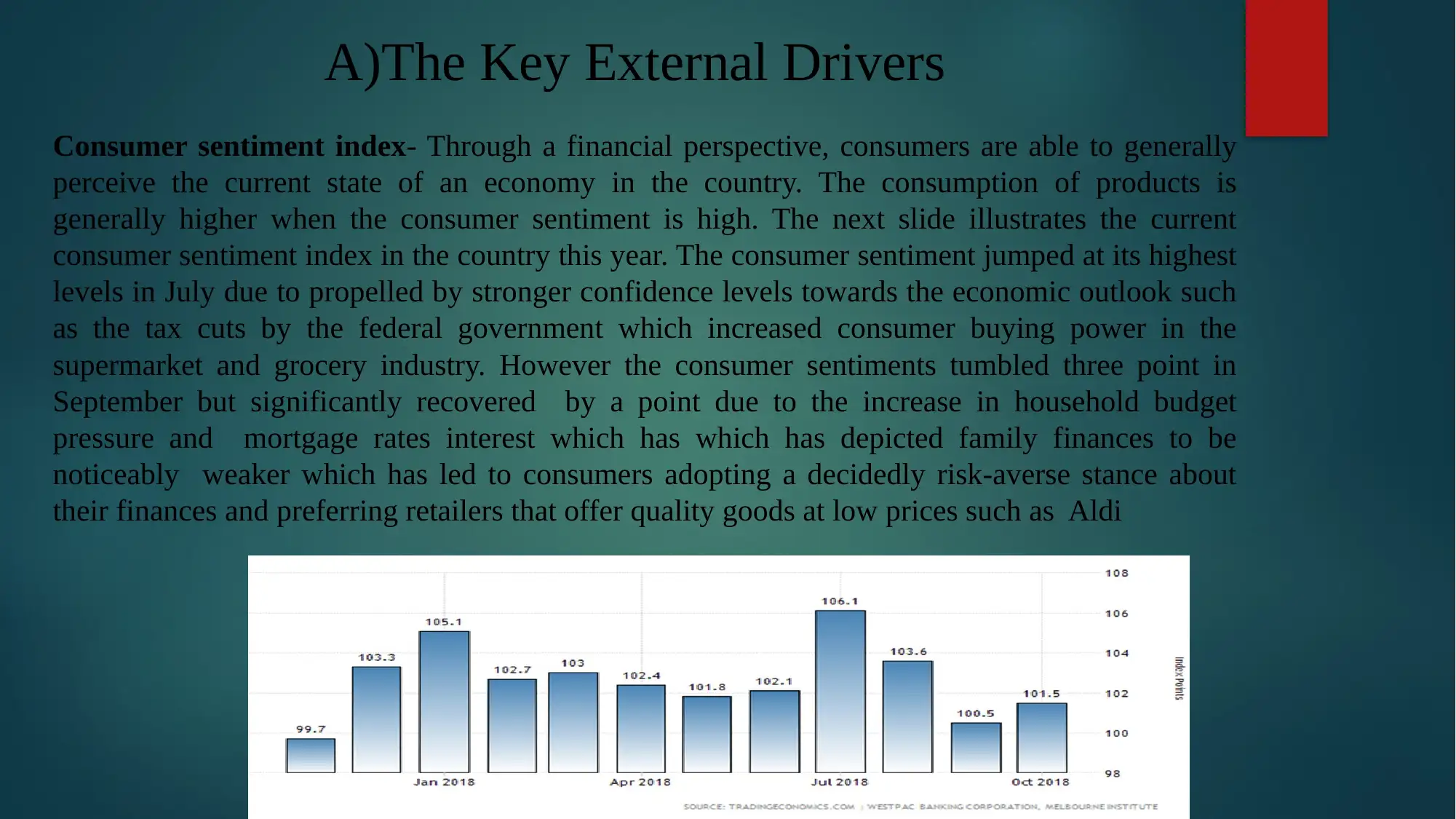

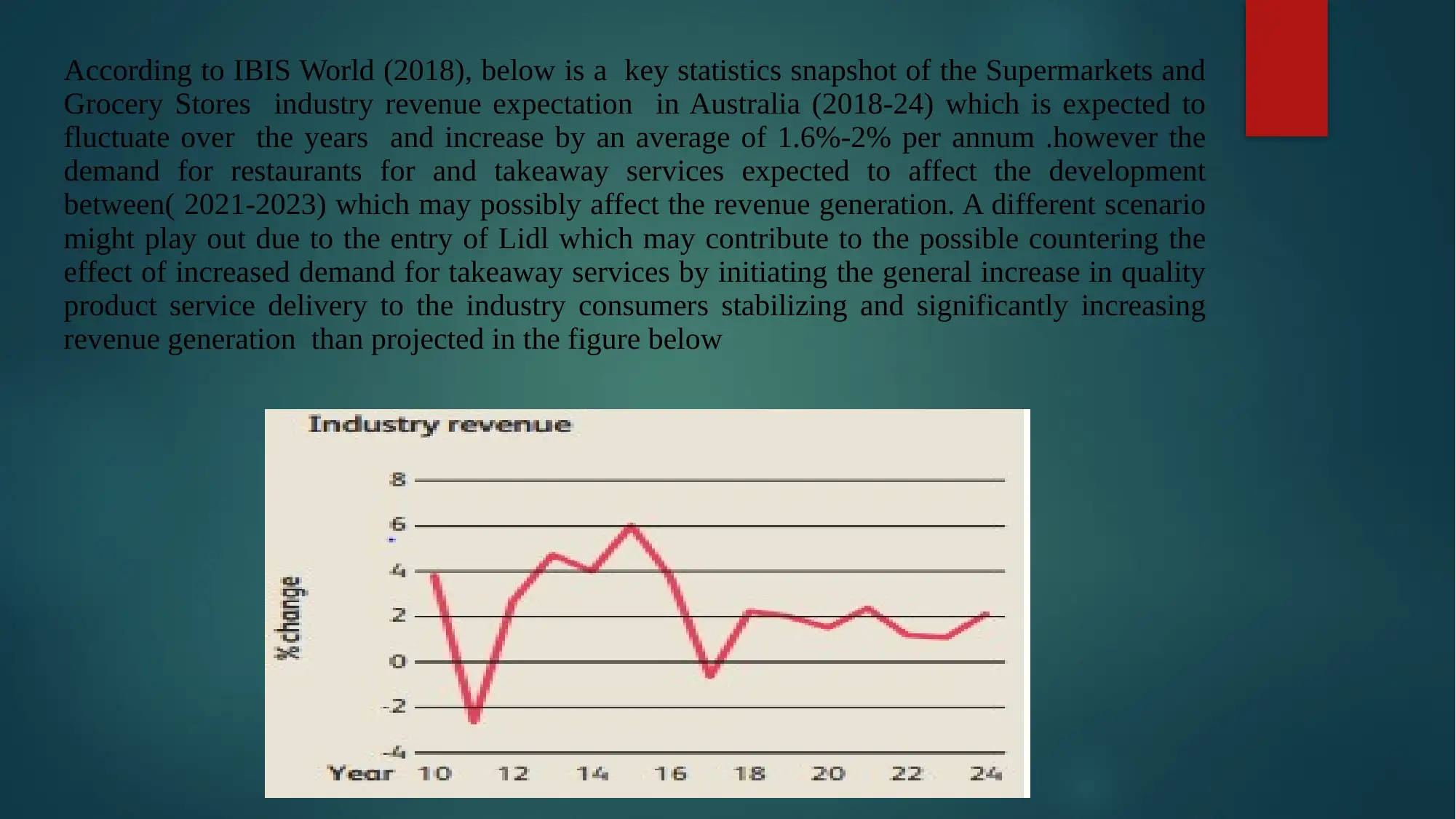

This presentation provides an in-depth analysis of the Australian supermarket and grocery store industry, focusing on its growth, key players, and competitive dynamics. The introduction highlights the industry's recent revenue and the major firms: IGA, Coles, Woolworths, and Aldi, as well as the potential entry of Lidl. The presentation examines key external drivers such as consumer sentiment, the increasing demand for takeaway food services, and population growth, and their impact on the industry. It details the current performance and market share of major supermarkets, including the impact of Aldi's entry and the anticipated effects of Lidl. The analysis explores the basis of competition, highlighting the strategies employed by different players, particularly the price wars initiated by Aldi and the responses of Coles and Woolworths. The conclusion summarizes the key findings, emphasizing the market share of Woolworths and Coles, the impact of Aldi, the challenges posed by the rise in takeaway food demand, and the potential effects of Lidl's entry. The presentation references relevant academic sources to support its claims and provides a comprehensive overview of the industry's current state and future prospects.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.