Supply Chain Financial Analysis: Evaluating NikoTech's Performance

VerifiedAdded on 2023/06/05

|16

|3494

|77

Homework Assignment

AI Summary

This assignment provides a detailed financial analysis of NikoTech's supply chain management performance across two years. It calculates and interprets key performance indicators such as Days of Inventory (DOI), Days of Receivables (DRO), length of the operating cycle, days of payables, and cash-to-cash cycle. The analysis identifies factors driving changes in these metrics, including the impact of cost of goods sold and average receivables. Furthermore, the assignment evaluates the implications of inventory turnover and net profit margin, offering insights into the company's efficiency and profitability. The document concludes by assessing whether changes in inventory turnover indicate positive management performance and how average turnover can help managers.

Running head: SUPPLY CHAIN MANAGEMENT 1

Supply Chain Management

Name of the student:

Name of the University:

Authors Note:

Supply Chain Management

Name of the student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1SUPPLY CHAIN MANAGEMENT

Assignment Questions: Part 1

Question 1.

a) Days of inventory. (DOI). This measures the performance of the business through

using the annual costs from the sales and mean of inventory. Days of receivables

are equal to the company’s year end account receivables divided by the daily

average sales made by the business (Barroso e tal. 2016).

Year 1

Therefore, DOI = (average inventory/COGS) *365

DoI = (495/3266) *365(Natarajarathinam e t al., 2009).

= 55.3

Therefore, it takes the company 55.3 days to sell its average inventory.

Year 2.

DOI = (789/5426) *365

DOI = 53.1.

Thus, it takes the company 53.1 days to sell its average inventory.

b)Days of receivables (DRO).

It simply measures the number of days taken by the company to get all its cash from

the credit sales. It also shows the efficiency and the liquidity of a firm’s collection

departments.

Year 2.

Days of receivables equals to the mean of all the sales divided by the receivables.

DRO = 450/ (1698/365)

DRO = 97 days (Musanzikwa., and Ramchander, 2018).

Therefore, it takes 97 days for the company to get its cash from its credit sales.

Assignment Questions: Part 1

Question 1.

a) Days of inventory. (DOI). This measures the performance of the business through

using the annual costs from the sales and mean of inventory. Days of receivables

are equal to the company’s year end account receivables divided by the daily

average sales made by the business (Barroso e tal. 2016).

Year 1

Therefore, DOI = (average inventory/COGS) *365

DoI = (495/3266) *365(Natarajarathinam e t al., 2009).

= 55.3

Therefore, it takes the company 55.3 days to sell its average inventory.

Year 2.

DOI = (789/5426) *365

DOI = 53.1.

Thus, it takes the company 53.1 days to sell its average inventory.

b)Days of receivables (DRO).

It simply measures the number of days taken by the company to get all its cash from

the credit sales. It also shows the efficiency and the liquidity of a firm’s collection

departments.

Year 2.

Days of receivables equals to the mean of all the sales divided by the receivables.

DRO = 450/ (1698/365)

DRO = 97 days (Musanzikwa., and Ramchander, 2018).

Therefore, it takes 97 days for the company to get its cash from its credit sales.

2SUPPLY CHAIN MANAGEMENT

Year 1.

DRO = 285/ (1440/365)

DRO = 72 days.

Thus, it takes 72 days for the company to get its cash from its credit sales.

C) Length of the Operating cycle (John and Gardner, 2003).

This simply means the time taken for an inventory to be turned into cash by the

retailers.

Length of the Operating Cycle can be obtained by the summation of receivables and

average inventory.

Year 1.

Inventory turnover = 2.06

Inventory period = 365/2.06 = 177.18

Receivables turnover = 1440/285 = 5.05

Accounts receivable period = 365/5.05 = 72.278

Hence, length of operating cycle = 177.18 + 72.278 = 249.457

Hence, it takes 249 days for the company to get its inventories and real money.

Inventory turnover = 1239/360 = 1.9

Inventory period = 365/1.9 = 192.105 (John and Gardner, 2003).

Receivables turnover = 1698/450 = 3.8

Accounts receivable period = 365/3.8 = 96.052

Hence, length of operating cycle = 1.9 + 96.052 = 97.95

Therefore, it takes approximately 98 days for the company’s inventories and money

from the sales to be received.

Year 1.

DRO = 285/ (1440/365)

DRO = 72 days.

Thus, it takes 72 days for the company to get its cash from its credit sales.

C) Length of the Operating cycle (John and Gardner, 2003).

This simply means the time taken for an inventory to be turned into cash by the

retailers.

Length of the Operating Cycle can be obtained by the summation of receivables and

average inventory.

Year 1.

Inventory turnover = 2.06

Inventory period = 365/2.06 = 177.18

Receivables turnover = 1440/285 = 5.05

Accounts receivable period = 365/5.05 = 72.278

Hence, length of operating cycle = 177.18 + 72.278 = 249.457

Hence, it takes 249 days for the company to get its inventories and real money.

Inventory turnover = 1239/360 = 1.9

Inventory period = 365/1.9 = 192.105 (John and Gardner, 2003).

Receivables turnover = 1698/450 = 3.8

Accounts receivable period = 365/3.8 = 96.052

Hence, length of operating cycle = 1.9 + 96.052 = 97.95

Therefore, it takes approximately 98 days for the company’s inventories and money

from the sales to be received.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3SUPPLY CHAIN MANAGEMENT

Question 2.

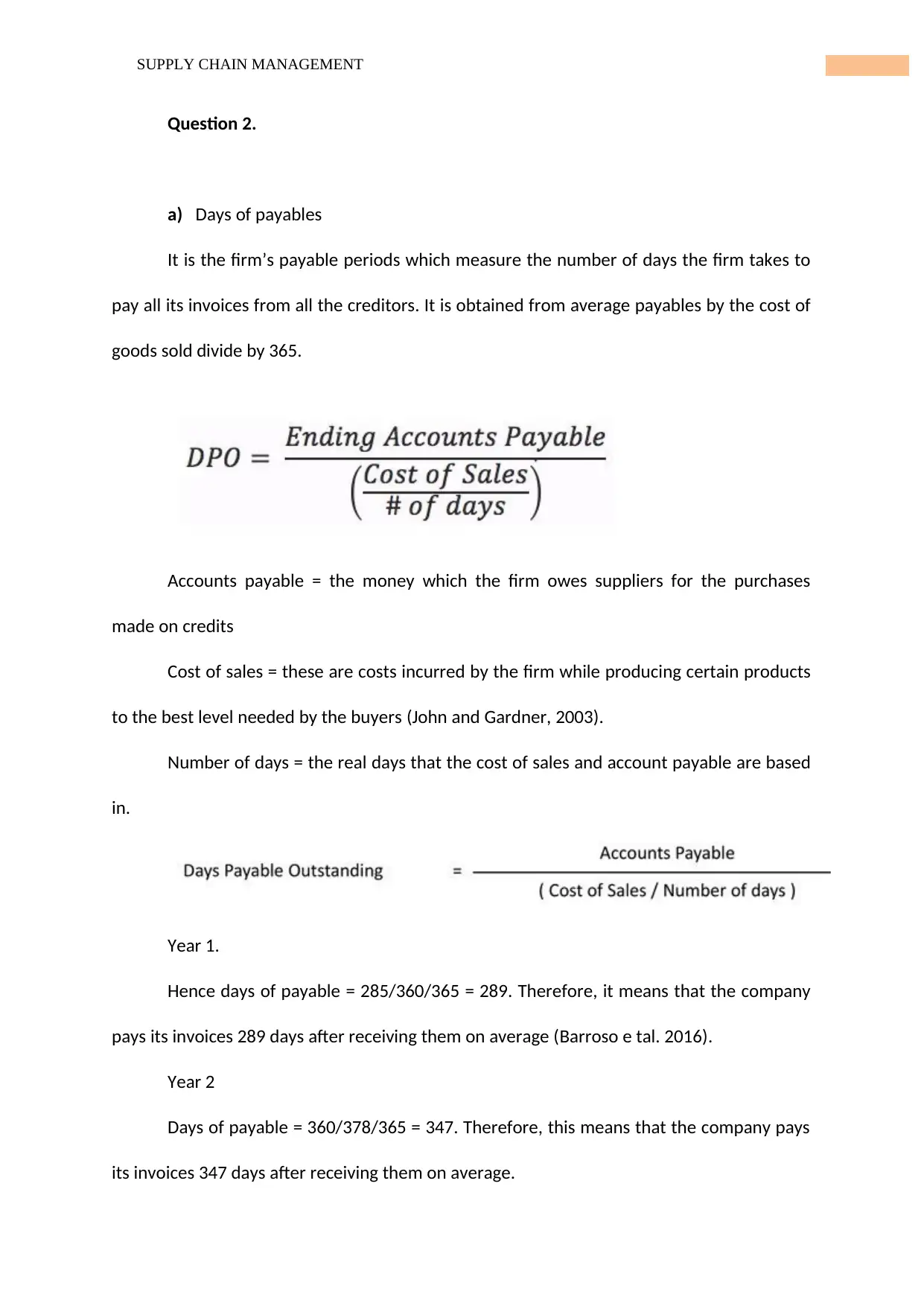

a) Days of payables

It is the firm’s payable periods which measure the number of days the firm takes to

pay all its invoices from all the creditors. It is obtained from average payables by the cost of

goods sold divide by 365.

Accounts payable = the money which the firm owes suppliers for the purchases

made on credits

Cost of sales = these are costs incurred by the firm while producing certain products

to the best level needed by the buyers (John and Gardner, 2003).

Number of days = the real days that the cost of sales and account payable are based

in.

Year 1.

Hence days of payable = 285/360/365 = 289. Therefore, it means that the company

pays its invoices 289 days after receiving them on average (Barroso e tal. 2016).

Year 2

Days of payable = 360/378/365 = 347. Therefore, this means that the company pays

its invoices 347 days after receiving them on average.

Question 2.

a) Days of payables

It is the firm’s payable periods which measure the number of days the firm takes to

pay all its invoices from all the creditors. It is obtained from average payables by the cost of

goods sold divide by 365.

Accounts payable = the money which the firm owes suppliers for the purchases

made on credits

Cost of sales = these are costs incurred by the firm while producing certain products

to the best level needed by the buyers (John and Gardner, 2003).

Number of days = the real days that the cost of sales and account payable are based

in.

Year 1.

Hence days of payable = 285/360/365 = 289. Therefore, it means that the company

pays its invoices 289 days after receiving them on average (Barroso e tal. 2016).

Year 2

Days of payable = 360/378/365 = 347. Therefore, this means that the company pays

its invoices 347 days after receiving them on average.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4SUPPLY CHAIN MANAGEMENT

b)

It measures time when the real money is out of reach for productive uses by the

firm. When the speed of the cash to cash cycle increases, implies that there are few days

when the firm’s cash is not available for productive activities (Eicker and Cilliers, 2018).

Year 1.

Length of the cash - cash cycles in the business can be obtained by deducting the

number of days when money is not in use from the summation of the locked money days in

the business and receivables (Natarajarathinam e t al., 2009).

Inventory -Average number of days = (raw and fini9shed goods inventory + gross

margins/2)/ (cost of goods /365) =480/450/365 = 389.3

The receivable money can be obtained from the mean of receivable accounts +

(sales/365)

=285/ (1500/365) = 69.343

Time when money is not in use can be obtained as mean of the accounts payable +

(COG /365) = 285/ (990/365) = 105.077.

Therefore, Length of cash to cash cycle = 389.3 + 69.343 - 105.077 = 354.566.

Year 2.

Inventory -Average number of days = {(660 + 459)/2}/ (1239/365) = 164.8012

Days cash is locked up in receivables = 450/ (1845/365) = 89.021

Days cash is free because the business has not paid its bills = 360/ (1239/365) =

106.038(Natarajarathinam e t al., 2009).

Therefore, Length of cash to cash cycle = 164.8012 + 89.021 - 106.038 = 147.739

days

b)

It measures time when the real money is out of reach for productive uses by the

firm. When the speed of the cash to cash cycle increases, implies that there are few days

when the firm’s cash is not available for productive activities (Eicker and Cilliers, 2018).

Year 1.

Length of the cash - cash cycles in the business can be obtained by deducting the

number of days when money is not in use from the summation of the locked money days in

the business and receivables (Natarajarathinam e t al., 2009).

Inventory -Average number of days = (raw and fini9shed goods inventory + gross

margins/2)/ (cost of goods /365) =480/450/365 = 389.3

The receivable money can be obtained from the mean of receivable accounts +

(sales/365)

=285/ (1500/365) = 69.343

Time when money is not in use can be obtained as mean of the accounts payable +

(COG /365) = 285/ (990/365) = 105.077.

Therefore, Length of cash to cash cycle = 389.3 + 69.343 - 105.077 = 354.566.

Year 2.

Inventory -Average number of days = {(660 + 459)/2}/ (1239/365) = 164.8012

Days cash is locked up in receivables = 450/ (1845/365) = 89.021

Days cash is free because the business has not paid its bills = 360/ (1239/365) =

106.038(Natarajarathinam e t al., 2009).

Therefore, Length of cash to cash cycle = 164.8012 + 89.021 - 106.038 = 147.739

days

5SUPPLY CHAIN MANAGEMENT

Question 3.

a) Cost of goods sold for NikoTech appear not to be increasing under

the right reasons. The costs involved in selling the goods sold for NikoTech appear

are increasing from one year to another due to pressure from other competitors.

Since cost of goods sold is that amount of money paid by the firm after acquiring its

inventories for sell. When cost of goods sold is subtracted from the other expenses

incurred results into the operating profit (Saunders e t al., 2011). This implies that as

COG increases, there is a decline in company’s revenues. Therefore, the cost of

goods sold for NikoTech were not increasing under right reasons but rather due to

expenses incurred in acquiring goods (Musanzikwa., and Ramchander, 2018).

I think if the cost of goods sold were increasing for the right reasons then its cost in

the year 2 would relatively be $1000 which would indicate there is a slight and reasonable

increase. It implies that the costs involved in selling the goods from year 1 to year 2 would

increase with a relatively small margin just to increase that there was an increase in

commodities purchased (Saunders e t al., 2011).For example, for a reasonable increase in

the COG would be obtained in what a firm pays to acquire inventories for sell (Sibanda and

Pooe, 2018).

b) ). Supposing the firm is required to pay $1000 for all its inventories

required for sell, then the cost of goods sold would be $1000 (Musanzikwa., and

Ramchander, 2018).

c) .Question 4.

Question 3.

a) Cost of goods sold for NikoTech appear not to be increasing under

the right reasons. The costs involved in selling the goods sold for NikoTech appear

are increasing from one year to another due to pressure from other competitors.

Since cost of goods sold is that amount of money paid by the firm after acquiring its

inventories for sell. When cost of goods sold is subtracted from the other expenses

incurred results into the operating profit (Saunders e t al., 2011). This implies that as

COG increases, there is a decline in company’s revenues. Therefore, the cost of

goods sold for NikoTech were not increasing under right reasons but rather due to

expenses incurred in acquiring goods (Musanzikwa., and Ramchander, 2018).

I think if the cost of goods sold were increasing for the right reasons then its cost in

the year 2 would relatively be $1000 which would indicate there is a slight and reasonable

increase. It implies that the costs involved in selling the goods from year 1 to year 2 would

increase with a relatively small margin just to increase that there was an increase in

commodities purchased (Saunders e t al., 2011).For example, for a reasonable increase in

the COG would be obtained in what a firm pays to acquire inventories for sell (Sibanda and

Pooe, 2018).

b) ). Supposing the firm is required to pay $1000 for all its inventories

required for sell, then the cost of goods sold would be $1000 (Musanzikwa., and

Ramchander, 2018).

c) .Question 4.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6SUPPLY CHAIN MANAGEMENT

Costs involved in selling goods are responsible factor from year 1 to year 2 trends in

days of inventory for NikoTech since it is the major factor in calculating the days of

inventory (Eicker and Cilliers, 2018). It is known that days of inventory helps the business to

measure its performance by using average inventories and costs involved in selling goods

sold. It implies that days of inventory from year 1 are calculated as follows;

DOI = (average inventory/COGS) *365

DoI = (495/3266) *365

= 55.3

While the days of inventory in year 2;

DOI = (789/5426) *365

DOI = 53.1.

Therefore, form the calculations above it observed that, as cost of goods sold

increase, days of inventory decreases which implies that for better performance of the

business more emphasis has to be put under reducing cost of goods sold (Saunders e t al.,

2011). Because when cost of goods sold reduces days of inventory will increase with no

doubt. Finally, costs involved in seeeling goods are primarily responsible in trends for the

NikoTech Company (Natarajarathinam e t al., 2009).

Question 5.

a) Average receivables are primarily driving the year 1 to year 2 in the

days of receivables since it is also involved while calculating the days of receivables.

Costs involved in selling goods are responsible factor from year 1 to year 2 trends in

days of inventory for NikoTech since it is the major factor in calculating the days of

inventory (Eicker and Cilliers, 2018). It is known that days of inventory helps the business to

measure its performance by using average inventories and costs involved in selling goods

sold. It implies that days of inventory from year 1 are calculated as follows;

DOI = (average inventory/COGS) *365

DoI = (495/3266) *365

= 55.3

While the days of inventory in year 2;

DOI = (789/5426) *365

DOI = 53.1.

Therefore, form the calculations above it observed that, as cost of goods sold

increase, days of inventory decreases which implies that for better performance of the

business more emphasis has to be put under reducing cost of goods sold (Saunders e t al.,

2011). Because when cost of goods sold reduces days of inventory will increase with no

doubt. Finally, costs involved in seeeling goods are primarily responsible in trends for the

NikoTech Company (Natarajarathinam e t al., 2009).

Question 5.

a) Average receivables are primarily driving the year 1 to year 2 in the

days of receivables since it is also involved while calculating the days of receivables.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SUPPLY CHAIN MANAGEMENT

Simply means that the firm uses the average receivables in measuring the number of

days it will take to get is cash from its credit sales. Which implies average receivable

is driving factor in calculating the days of receivable for the firm (Diane and

Mollenkopf, 2018).

For example,

Year 1.

DRO = 285/ (1440/365)

DRO = 72 days.

Therefore, it takes 72 days for the company to get its cash from its credit sales.

Also considering;

Year 2.

DRO = 450/ (1698/365)

DRO = 97 days

Therefore, it takes 97 days for the company to get its cash from its credit sales.

Hence from the above calculations, it is noted that when average receivables

increase, leads the days of receivables to also increase. Hence average receivable is directly

proportional to days of receivable (Diane and Mollenkopf, 2018).

b) When there is a change in the returns and allowances, also the days

of receivables change appropriately. For example, returns from the customers

increase the average receivables of the firm which in turn increases the days of

Simply means that the firm uses the average receivables in measuring the number of

days it will take to get is cash from its credit sales. Which implies average receivable

is driving factor in calculating the days of receivable for the firm (Diane and

Mollenkopf, 2018).

For example,

Year 1.

DRO = 285/ (1440/365)

DRO = 72 days.

Therefore, it takes 72 days for the company to get its cash from its credit sales.

Also considering;

Year 2.

DRO = 450/ (1698/365)

DRO = 97 days

Therefore, it takes 97 days for the company to get its cash from its credit sales.

Hence from the above calculations, it is noted that when average receivables

increase, leads the days of receivables to also increase. Hence average receivable is directly

proportional to days of receivable (Diane and Mollenkopf, 2018).

b) When there is a change in the returns and allowances, also the days

of receivables change appropriately. For example, returns from the customers

increase the average receivables of the firm which in turn increases the days of

8SUPPLY CHAIN MANAGEMENT

receivables. However, the days of receivables decrease with no returns from the

buyers.

On the other hand, an increase in the sales allowances reduce the average

sales which increase the days of receivables (Eicker and Cilliers, 2018).

Assignment questions: Part 2.

Question 1.

Days payable outstanding is not contributing significantly to the change in the value

of NikoTech’s cash to cash cycle since it is not involved in the calculation (Sibanda and Pooe,

2018).

From the formula of the length of cash-to-cash above; It implies that days payable

outstanding has no significant to the cash to cash cycle (Sibanda and Pooe, 2018).

Question 2.

a) Average turnover helps the manager to find out how high his costs per hire

figures are. For its calculation, it is the summation of annual average of the turnover rates.

The Turnover Inventory is obtained by COG by the mean of inventory (Musanzikwa.,

and Ramchander, 2018).

Year 1;

Inventory Turnover = 3266/495 = 6.6. Therefore, it takes 6.6 days for the inventory

to be used up in the business (Keely e t al., 2012).

Year 2;

Inventory Turnover = 5426/789 = 6.9. therefore, it takes 6.6 days for the inventory to

be used up (Diane and Mollenkopf, 2018).

receivables. However, the days of receivables decrease with no returns from the

buyers.

On the other hand, an increase in the sales allowances reduce the average

sales which increase the days of receivables (Eicker and Cilliers, 2018).

Assignment questions: Part 2.

Question 1.

Days payable outstanding is not contributing significantly to the change in the value

of NikoTech’s cash to cash cycle since it is not involved in the calculation (Sibanda and Pooe,

2018).

From the formula of the length of cash-to-cash above; It implies that days payable

outstanding has no significant to the cash to cash cycle (Sibanda and Pooe, 2018).

Question 2.

a) Average turnover helps the manager to find out how high his costs per hire

figures are. For its calculation, it is the summation of annual average of the turnover rates.

The Turnover Inventory is obtained by COG by the mean of inventory (Musanzikwa.,

and Ramchander, 2018).

Year 1;

Inventory Turnover = 3266/495 = 6.6. Therefore, it takes 6.6 days for the inventory

to be used up in the business (Keely e t al., 2012).

Year 2;

Inventory Turnover = 5426/789 = 6.9. therefore, it takes 6.6 days for the inventory to

be used up (Diane and Mollenkopf, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9SUPPLY CHAIN MANAGEMENT

b)

Inventory turnover is the ratio which measures the rate of inventory use in a

measurement period of the business (Barroso e tal.,2016). The division between the costs

involved in selling the goods with the inventories in the firm gives the turnover inventory.

Also, dividing the inventory by the COG gives the days of inventories and tking its

recipricol

(1/inventory turnover)365 is obtained from dividing the inventories by the COG and

multiplying by 365.

365/Inventory Turnover = (inventory / COG) 365…….1

Where equation 1 is the days of inventory. Implying that equation 1 becomes;

365/ Inventory turnover = days of inventory. By taking the reciprocal again and

multiplying 365 gives;

Inventory Turnover = 365/Days of Inventory (Diane and Mollenkopf, 2018).

c) I would consider the change in inventory turnover from year 1 to year 2 as a

positive indication of the inventory management performance for NikoTech company

(Barroso e tal., 2016). Since a positive change results into increase in the inventory turnover

ratio meaning the rate at which the inventory is being used up in the business is high. It

implies that the business would order more inventory from the suppliers since the inventory

turnover is going on well and positive (Eicker and Cilliers, 2018). Any increase in demand by

the customers increases the inventory turnover of the firm.

Question 3.

b)

Inventory turnover is the ratio which measures the rate of inventory use in a

measurement period of the business (Barroso e tal.,2016). The division between the costs

involved in selling the goods with the inventories in the firm gives the turnover inventory.

Also, dividing the inventory by the COG gives the days of inventories and tking its

recipricol

(1/inventory turnover)365 is obtained from dividing the inventories by the COG and

multiplying by 365.

365/Inventory Turnover = (inventory / COG) 365…….1

Where equation 1 is the days of inventory. Implying that equation 1 becomes;

365/ Inventory turnover = days of inventory. By taking the reciprocal again and

multiplying 365 gives;

Inventory Turnover = 365/Days of Inventory (Diane and Mollenkopf, 2018).

c) I would consider the change in inventory turnover from year 1 to year 2 as a

positive indication of the inventory management performance for NikoTech company

(Barroso e tal., 2016). Since a positive change results into increase in the inventory turnover

ratio meaning the rate at which the inventory is being used up in the business is high. It

implies that the business would order more inventory from the suppliers since the inventory

turnover is going on well and positive (Eicker and Cilliers, 2018). Any increase in demand by

the customers increases the inventory turnover of the firm.

Question 3.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10SUPPLY CHAIN MANAGEMENT

a) Net profit margin obtained after subtracting the expenses, taxes, interests

and dividends from revenues and expressing it as a percentage. The Net income margin

comes from the revenues minus the expenses divide by (total revenues) times 100

Net profit margin = 100,000.0 - 30000/ (100000) *100 = 70%. Therefore, the net

profit margin is 70.0% (Eicker and Cilliers, 2018).

For year 2.

Net profit margin = 120,000 – 35000/120,000 *100 = 70.83% (Keely e t al.,2012).

b) Asset turnover helps in determining the firm’s asset efficiency in generating

sales or

revenues. It calculates the net sales of the firm as a percentage of the total assets

year 1

Asset turnover = (285/1239) *100 = 23.0. therefore, the asset turnover is 23.0%

Year 2;

Asset turnover = (450/990) *100 = 45.45. hence the asset turnover for the year2 is 45.45%

(Keely e t al.,2012).

c) Return on assets

This is a ratio which determines the total assets’ income in a particular period by

comparing the net income with the average total assets of the firm(Barroso and Maschado,

2016).

Return on assets = (Net income/ Average total assets0*100

For year 1;

Return on assets = 285/1500*100 = 19.0%. therefore, the return on asset is 19.0%.

a) Net profit margin obtained after subtracting the expenses, taxes, interests

and dividends from revenues and expressing it as a percentage. The Net income margin

comes from the revenues minus the expenses divide by (total revenues) times 100

Net profit margin = 100,000.0 - 30000/ (100000) *100 = 70%. Therefore, the net

profit margin is 70.0% (Eicker and Cilliers, 2018).

For year 2.

Net profit margin = 120,000 – 35000/120,000 *100 = 70.83% (Keely e t al.,2012).

b) Asset turnover helps in determining the firm’s asset efficiency in generating

sales or

revenues. It calculates the net sales of the firm as a percentage of the total assets

year 1

Asset turnover = (285/1239) *100 = 23.0. therefore, the asset turnover is 23.0%

Year 2;

Asset turnover = (450/990) *100 = 45.45. hence the asset turnover for the year2 is 45.45%

(Keely e t al.,2012).

c) Return on assets

This is a ratio which determines the total assets’ income in a particular period by

comparing the net income with the average total assets of the firm(Barroso and Maschado,

2016).

Return on assets = (Net income/ Average total assets0*100

For year 1;

Return on assets = 285/1500*100 = 19.0%. therefore, the return on asset is 19.0%.

11SUPPLY CHAIN MANAGEMENT

Year 2;

Return on assets = 450/1845 *100 = 24.4%. hence the return on asset by that year is

24.4% (Keely e t al.,2012).

Question 4.

a) Net profit is not primarily driving factor for the change in year 1 to year 2 for

the return on assets simply because it does not have any effect on the calculations of the

return on assets. Return on assets only considers net income and total assets in its

calculations.

b) The factors that could have caused the deteriorating trend are changes in

demand by the customers, price increase of the goods by the suppliers and inflation. All

these could have contributed to the deteriorating of the trends (Elize and Trollip, 2018).

Question 5.

a) The supply chain velocity is improving from the year1 to year 2 as calculated

below;

Year 1

Inventory turnover = 2.06 (Musanzikwa., and Ramchander, 2018).

Inventory period = 365/2.06 = 177.18 (Natarajarathinam e t al.,2009).

Receivables turnover = 1440/285 = 5.05

Accounts receivable period = 365/5.05 = 72.278

Hence, length of operating cycle = 177.18 + 72.278 = 249.457(Keely e t al.,2012).

Therefore, it takes 249 days for the company’s inventories to be received.

Year 2;

Return on assets = 450/1845 *100 = 24.4%. hence the return on asset by that year is

24.4% (Keely e t al.,2012).

Question 4.

a) Net profit is not primarily driving factor for the change in year 1 to year 2 for

the return on assets simply because it does not have any effect on the calculations of the

return on assets. Return on assets only considers net income and total assets in its

calculations.

b) The factors that could have caused the deteriorating trend are changes in

demand by the customers, price increase of the goods by the suppliers and inflation. All

these could have contributed to the deteriorating of the trends (Elize and Trollip, 2018).

Question 5.

a) The supply chain velocity is improving from the year1 to year 2 as calculated

below;

Year 1

Inventory turnover = 2.06 (Musanzikwa., and Ramchander, 2018).

Inventory period = 365/2.06 = 177.18 (Natarajarathinam e t al.,2009).

Receivables turnover = 1440/285 = 5.05

Accounts receivable period = 365/5.05 = 72.278

Hence, length of operating cycle = 177.18 + 72.278 = 249.457(Keely e t al.,2012).

Therefore, it takes 249 days for the company’s inventories to be received.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.