FIN10002: Financial Statistics Report - ASX Company Data Analysis

VerifiedAdded on 2022/11/01

|18

|3489

|444

Report

AI Summary

This report analyzes the financial performance of companies listed on the ASX, utilizing a dataset of 50 randomly selected companies from a pool of 1536. The analysis encompasses descriptive statistics, including distributions of sector, status, market capitalization, total assets, total revenue, and net profit after tax. The study employs confidence intervals to assess the reliability of sample data in estimating population parameters for total revenue and total assets, specifically within the materials sector and for all trading companies. Hypothesis testing, using independent sample t-tests, examines differences in total revenue between the financial and healthcare sectors, and market capitalization differences between financial and materials sectors. A linear regression model is fitted to explore the relationship between total assets and net profit after tax, revealing a strong positive correlation. The report concludes with limitations stemming from the small sample size and highlights key findings regarding sector distribution, financial performance, and the relationship between assets and profitability.

Surname: 1

FIN10002: Financial Statistics

Name

The Name of the Class (Course)

Professor (Tutor)

The Name of the School (University)

The City and State where it is located

Date

FIN10002: Financial Statistics

Name

The Name of the Class (Course)

Professor (Tutor)

The Name of the School (University)

The City and State where it is located

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Surname: 2

Executive Summary

The research was focused on assessing the companies listed on the ASX with their sector area

and financial information. It was established that most of the companies listed on the ASX

were from the material sector, although about 52.00% were either suspended or delisted. All

the continuous variables in the sample data were highly positively skewed. The analysis

indicated that the sample data used could not estimate the population parameter for the total

asset for all companies that are trading. However, the sample could

estimate the population parameter for the total revenue for the GICS

sector of material only. It was found that total revenue for financial (GICS) is not

more than the average total revenue for Health Care (GICS) and the average market

capitalization, for financial and materials, did not differ. Lastly, it was found that

there a significant relationship between net profit after tax and total assets.

Executive Summary

The research was focused on assessing the companies listed on the ASX with their sector area

and financial information. It was established that most of the companies listed on the ASX

were from the material sector, although about 52.00% were either suspended or delisted. All

the continuous variables in the sample data were highly positively skewed. The analysis

indicated that the sample data used could not estimate the population parameter for the total

asset for all companies that are trading. However, the sample could

estimate the population parameter for the total revenue for the GICS

sector of material only. It was found that total revenue for financial (GICS) is not

more than the average total revenue for Health Care (GICS) and the average market

capitalization, for financial and materials, did not differ. Lastly, it was found that

there a significant relationship between net profit after tax and total assets.

Surname: 3

Introduction

In this study, the focus was on assessing the companies listed on the ASX with their sector

area and financial information. The main objective was to determine the distribution of the

data. Both descriptive statistics and plots will be used to illustrate how the variables were

distributed. For the nominal variables, pie chart and bar plots will be used. A histogram will

be used to show the distribution of the continuous variables (Lowry, 2014). The independent

sample t-test will be carried out to determine whether the mean difference between two

groups is different. Lastly, a regression model will be fitted to determine whether there exists

a significant relationship between net profit after tax and total assets.

To achieve this, the sample data of companies listed on the ASX (n = 50) was used. A simple

random process was used to select a random sample size 50 of customers from the 1536

companies in the Major Assignment Data Company Profits file. The sample data are located

in .

Analysis

Using this sample data, we carry out data analysis as follows:

Descriptive analysis

The distribution of Status was carried out and the summary table is as follows:

Row Labels Count of Status

Delisted 44.00%

Suspended 8.00%

Trading 48.00%

Grand Total 100.00%

Introduction

In this study, the focus was on assessing the companies listed on the ASX with their sector

area and financial information. The main objective was to determine the distribution of the

data. Both descriptive statistics and plots will be used to illustrate how the variables were

distributed. For the nominal variables, pie chart and bar plots will be used. A histogram will

be used to show the distribution of the continuous variables (Lowry, 2014). The independent

sample t-test will be carried out to determine whether the mean difference between two

groups is different. Lastly, a regression model will be fitted to determine whether there exists

a significant relationship between net profit after tax and total assets.

To achieve this, the sample data of companies listed on the ASX (n = 50) was used. A simple

random process was used to select a random sample size 50 of customers from the 1536

companies in the Major Assignment Data Company Profits file. The sample data are located

in .

Analysis

Using this sample data, we carry out data analysis as follows:

Descriptive analysis

The distribution of Status was carried out and the summary table is as follows:

Row Labels Count of Status

Delisted 44.00%

Suspended 8.00%

Trading 48.00%

Grand Total 100.00%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Surname: 4

Delisted

44%

Suspended

8%

Trading

48%

Status Distibution

Delisted

Suspended

Trading

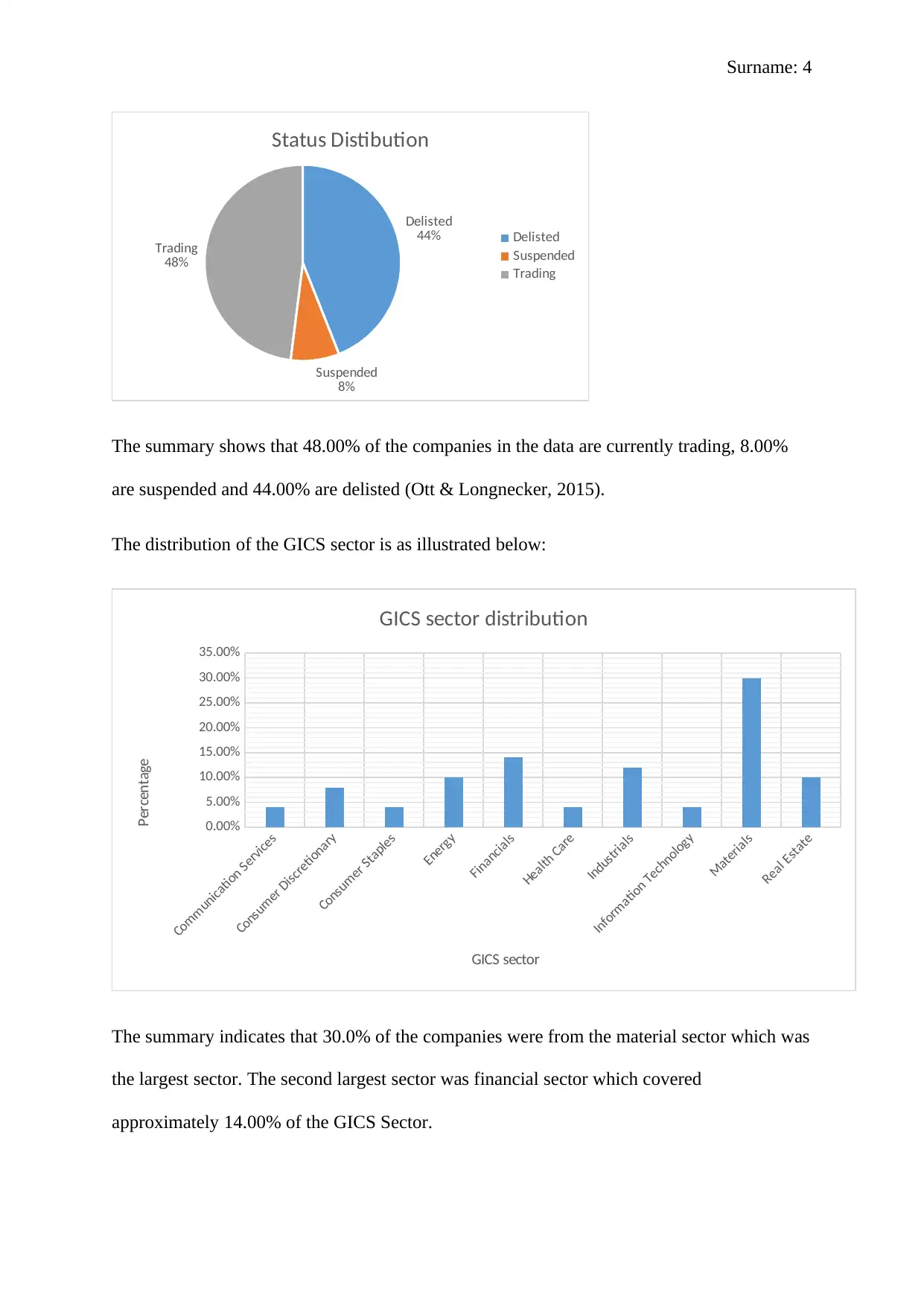

The summary shows that 48.00% of the companies in the data are currently trading, 8.00%

are suspended and 44.00% are delisted (Ott & Longnecker, 2015).

The distribution of the GICS sector is as illustrated below:

Communication Services

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Real Estate

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

GICS sector distribution

GICS sector

Percentage

The summary indicates that 30.0% of the companies were from the material sector which was

the largest sector. The second largest sector was financial sector which covered

approximately 14.00% of the GICS Sector.

Delisted

44%

Suspended

8%

Trading

48%

Status Distibution

Delisted

Suspended

Trading

The summary shows that 48.00% of the companies in the data are currently trading, 8.00%

are suspended and 44.00% are delisted (Ott & Longnecker, 2015).

The distribution of the GICS sector is as illustrated below:

Communication Services

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Real Estate

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

GICS sector distribution

GICS sector

Percentage

The summary indicates that 30.0% of the companies were from the material sector which was

the largest sector. The second largest sector was financial sector which covered

approximately 14.00% of the GICS Sector.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Surname: 5

Materials

Diversified Financials

Real Estate

Commercial & Professional Services

Energy

Consumer Services

Telecommunication Services

Pharmaceuticals, Biotechnology & Life Sciences

Software & Services

Capital Goods

Retailing

Household & Personal Products

Technology Hardware & Equipment

Food, Beverage & Tobacco

Automobiles & Components

Health Care Equipment & Services

0.0%

10.0%

20.0%

30.0% 30.0%

14.0%10.0%10.0%10.0%

4.0% 4.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

GICS Industry group distribution

Total

GICS Industry group

Percentage

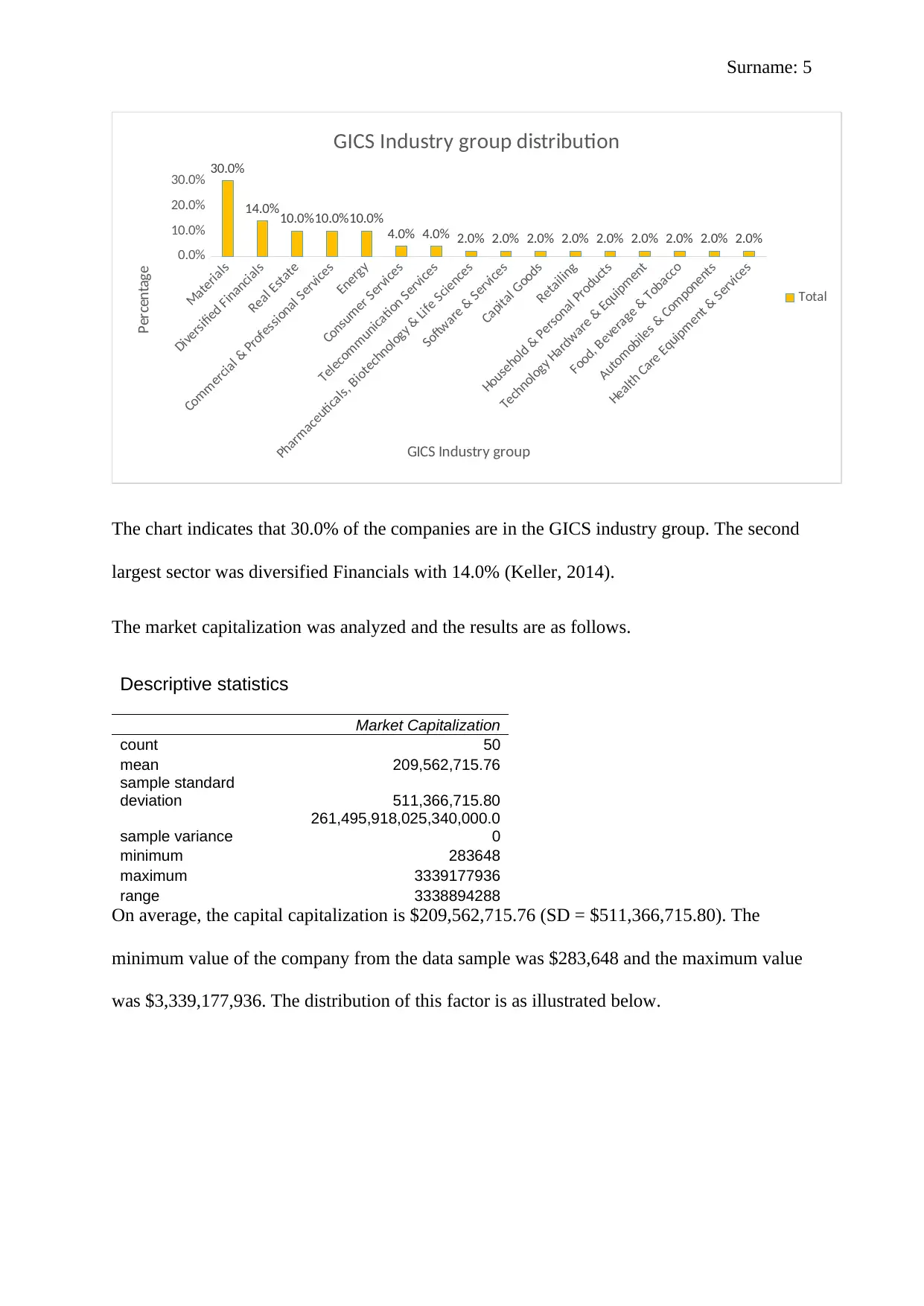

The chart indicates that 30.0% of the companies are in the GICS industry group. The second

largest sector was diversified Financials with 14.0% (Keller, 2014).

The market capitalization was analyzed and the results are as follows.

Descriptive statistics

Market Capitalization

count 50

mean 209,562,715.76

sample standard

deviation 511,366,715.80

sample variance

261,495,918,025,340,000.0

0

minimum 283648

maximum 3339177936

range 3338894288

On average, the capital capitalization is $209,562,715.76 (SD = $511,366,715.80). The

minimum value of the company from the data sample was $283,648 and the maximum value

was $3,339,177,936. The distribution of this factor is as illustrated below.

Materials

Diversified Financials

Real Estate

Commercial & Professional Services

Energy

Consumer Services

Telecommunication Services

Pharmaceuticals, Biotechnology & Life Sciences

Software & Services

Capital Goods

Retailing

Household & Personal Products

Technology Hardware & Equipment

Food, Beverage & Tobacco

Automobiles & Components

Health Care Equipment & Services

0.0%

10.0%

20.0%

30.0% 30.0%

14.0%10.0%10.0%10.0%

4.0% 4.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

GICS Industry group distribution

Total

GICS Industry group

Percentage

The chart indicates that 30.0% of the companies are in the GICS industry group. The second

largest sector was diversified Financials with 14.0% (Keller, 2014).

The market capitalization was analyzed and the results are as follows.

Descriptive statistics

Market Capitalization

count 50

mean 209,562,715.76

sample standard

deviation 511,366,715.80

sample variance

261,495,918,025,340,000.0

0

minimum 283648

maximum 3339177936

range 3338894288

On average, the capital capitalization is $209,562,715.76 (SD = $511,366,715.80). The

minimum value of the company from the data sample was $283,648 and the maximum value

was $3,339,177,936. The distribution of this factor is as illustrated below.

Surname: 6

0

300,000,000

600,000,000

900,000,000

1,200,000,000

1,500,000,000

1,800,000,000

2,100,000,000

2,400,000,000

2,700,000,000

3,000,000,000

3,300,000,000

0

10

20

30

40

50

60

70

80

Histogram of Market capitalization

Market Capitalisation

Percent

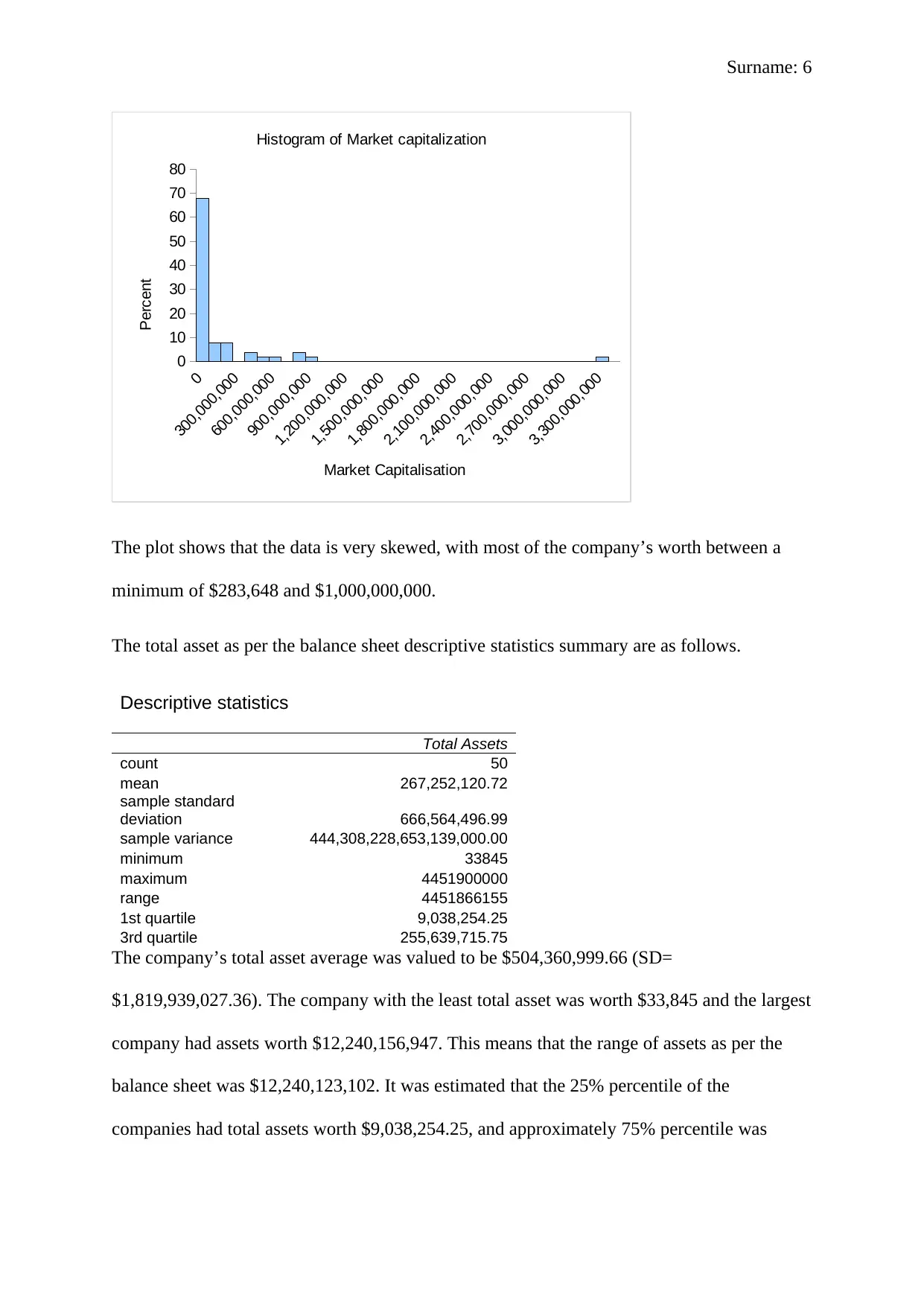

The plot shows that the data is very skewed, with most of the company’s worth between a

minimum of $283,648 and $1,000,000,000.

The total asset as per the balance sheet descriptive statistics summary are as follows.

Descriptive statistics

Total Assets

count 50

mean 267,252,120.72

sample standard

deviation 666,564,496.99

sample variance 444,308,228,653,139,000.00

minimum 33845

maximum 4451900000

range 4451866155

1st quartile 9,038,254.25

3rd quartile 255,639,715.75

The company’s total asset average was valued to be $504,360,999.66 (SD=

$1,819,939,027.36). The company with the least total asset was worth $33,845 and the largest

company had assets worth $12,240,156,947. This means that the range of assets as per the

balance sheet was $12,240,123,102. It was estimated that the 25% percentile of the

companies had total assets worth $9,038,254.25, and approximately 75% percentile was

0

300,000,000

600,000,000

900,000,000

1,200,000,000

1,500,000,000

1,800,000,000

2,100,000,000

2,400,000,000

2,700,000,000

3,000,000,000

3,300,000,000

0

10

20

30

40

50

60

70

80

Histogram of Market capitalization

Market Capitalisation

Percent

The plot shows that the data is very skewed, with most of the company’s worth between a

minimum of $283,648 and $1,000,000,000.

The total asset as per the balance sheet descriptive statistics summary are as follows.

Descriptive statistics

Total Assets

count 50

mean 267,252,120.72

sample standard

deviation 666,564,496.99

sample variance 444,308,228,653,139,000.00

minimum 33845

maximum 4451900000

range 4451866155

1st quartile 9,038,254.25

3rd quartile 255,639,715.75

The company’s total asset average was valued to be $504,360,999.66 (SD=

$1,819,939,027.36). The company with the least total asset was worth $33,845 and the largest

company had assets worth $12,240,156,947. This means that the range of assets as per the

balance sheet was $12,240,123,102. It was estimated that the 25% percentile of the

companies had total assets worth $9,038,254.25, and approximately 75% percentile was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Surname: 7

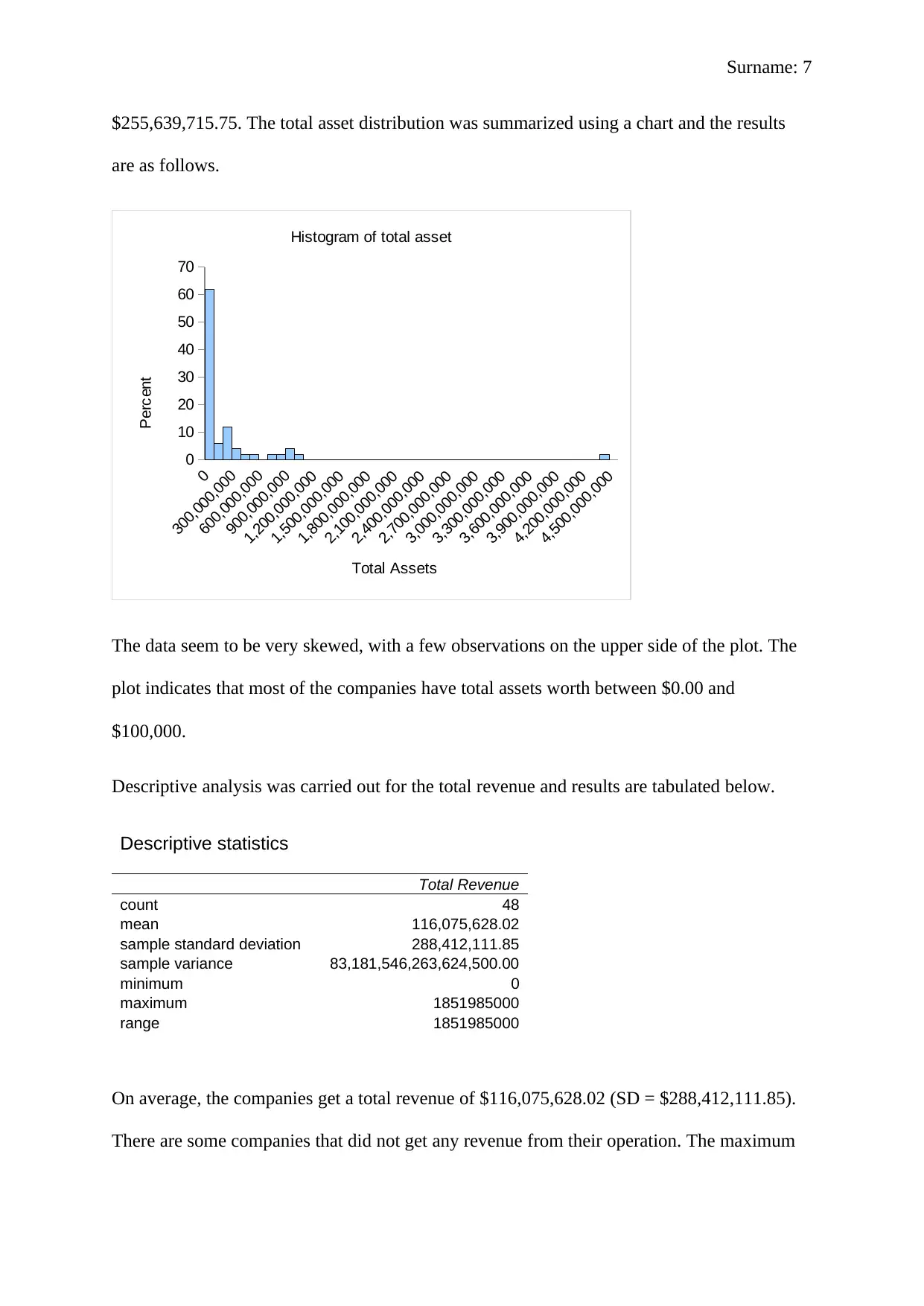

$255,639,715.75. The total asset distribution was summarized using a chart and the results

are as follows.

0

300,000,000

600,000,000

900,000,000

1,200,000,000

1,500,000,000

1,800,000,000

2,100,000,000

2,400,000,000

2,700,000,000

3,000,000,000

3,300,000,000

3,600,000,000

3,900,000,000

4,200,000,000

4,500,000,000

0

10

20

30

40

50

60

70

Histogram of total asset

Total Assets

Percent

The data seem to be very skewed, with a few observations on the upper side of the plot. The

plot indicates that most of the companies have total assets worth between $0.00 and

$100,000.

Descriptive analysis was carried out for the total revenue and results are tabulated below.

Descriptive statistics

Total Revenue

count 48

mean 116,075,628.02

sample standard deviation 288,412,111.85

sample variance 83,181,546,263,624,500.00

minimum 0

maximum 1851985000

range 1851985000

On average, the companies get a total revenue of $116,075,628.02 (SD = $288,412,111.85).

There are some companies that did not get any revenue from their operation. The maximum

$255,639,715.75. The total asset distribution was summarized using a chart and the results

are as follows.

0

300,000,000

600,000,000

900,000,000

1,200,000,000

1,500,000,000

1,800,000,000

2,100,000,000

2,400,000,000

2,700,000,000

3,000,000,000

3,300,000,000

3,600,000,000

3,900,000,000

4,200,000,000

4,500,000,000

0

10

20

30

40

50

60

70

Histogram of total asset

Total Assets

Percent

The data seem to be very skewed, with a few observations on the upper side of the plot. The

plot indicates that most of the companies have total assets worth between $0.00 and

$100,000.

Descriptive analysis was carried out for the total revenue and results are tabulated below.

Descriptive statistics

Total Revenue

count 48

mean 116,075,628.02

sample standard deviation 288,412,111.85

sample variance 83,181,546,263,624,500.00

minimum 0

maximum 1851985000

range 1851985000

On average, the companies get a total revenue of $116,075,628.02 (SD = $288,412,111.85).

There are some companies that did not get any revenue from their operation. The maximum

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Surname: 8

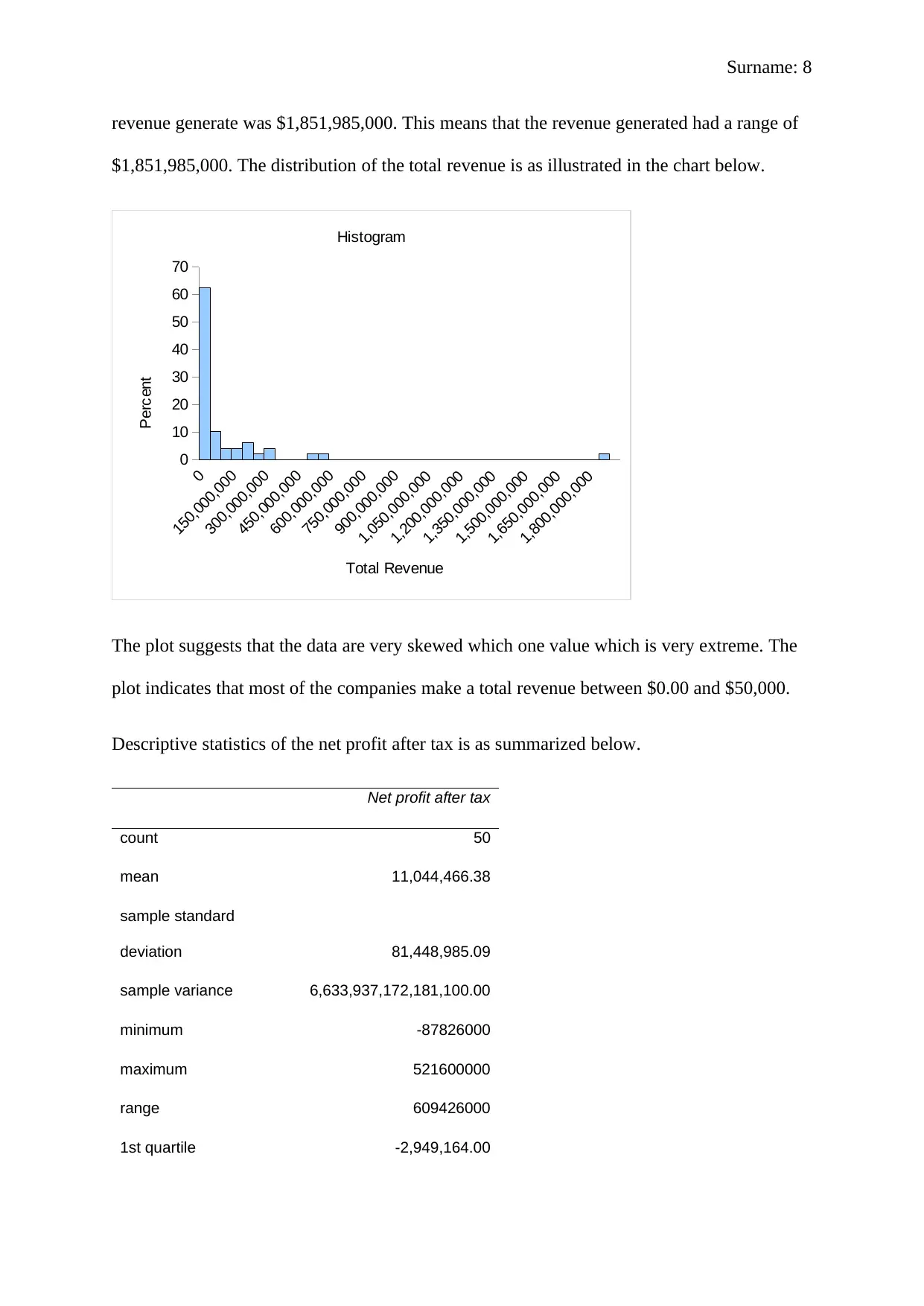

revenue generate was $1,851,985,000. This means that the revenue generated had a range of

$1,851,985,000. The distribution of the total revenue is as illustrated in the chart below.

0

150,000,000

300,000,000

450,000,000

600,000,000

750,000,000

900,000,000

1,050,000,000

1,200,000,000

1,350,000,000

1,500,000,000

1,650,000,000

1,800,000,000

0

10

20

30

40

50

60

70

Histogram

Total Revenue

Percent

The plot suggests that the data are very skewed which one value which is very extreme. The

plot indicates that most of the companies make a total revenue between $0.00 and $50,000.

Descriptive statistics of the net profit after tax is as summarized below.

Net profit after tax

count 50

mean 11,044,466.38

sample standard

deviation 81,448,985.09

sample variance 6,633,937,172,181,100.00

minimum -87826000

maximum 521600000

range 609426000

1st quartile -2,949,164.00

revenue generate was $1,851,985,000. This means that the revenue generated had a range of

$1,851,985,000. The distribution of the total revenue is as illustrated in the chart below.

0

150,000,000

300,000,000

450,000,000

600,000,000

750,000,000

900,000,000

1,050,000,000

1,200,000,000

1,350,000,000

1,500,000,000

1,650,000,000

1,800,000,000

0

10

20

30

40

50

60

70

Histogram

Total Revenue

Percent

The plot suggests that the data are very skewed which one value which is very extreme. The

plot indicates that most of the companies make a total revenue between $0.00 and $50,000.

Descriptive statistics of the net profit after tax is as summarized below.

Net profit after tax

count 50

mean 11,044,466.38

sample standard

deviation 81,448,985.09

sample variance 6,633,937,172,181,100.00

minimum -87826000

maximum 521600000

range 609426000

1st quartile -2,949,164.00

Surname: 9

3rd quartile 3,761,688.75

interquartile range 6,710,852.75

The summary indicates that on average companies made $11,044,466.38 net profit after tax

(SD = $81,448,985.09). The company that made the largest loss made a loss of $87,826,000

and the highest profit was $521,600,000. This means that the range of the net profit after tax

was $609,426,000. The 25th percent of the company made a loss of $2,949,164.00 and the 75th

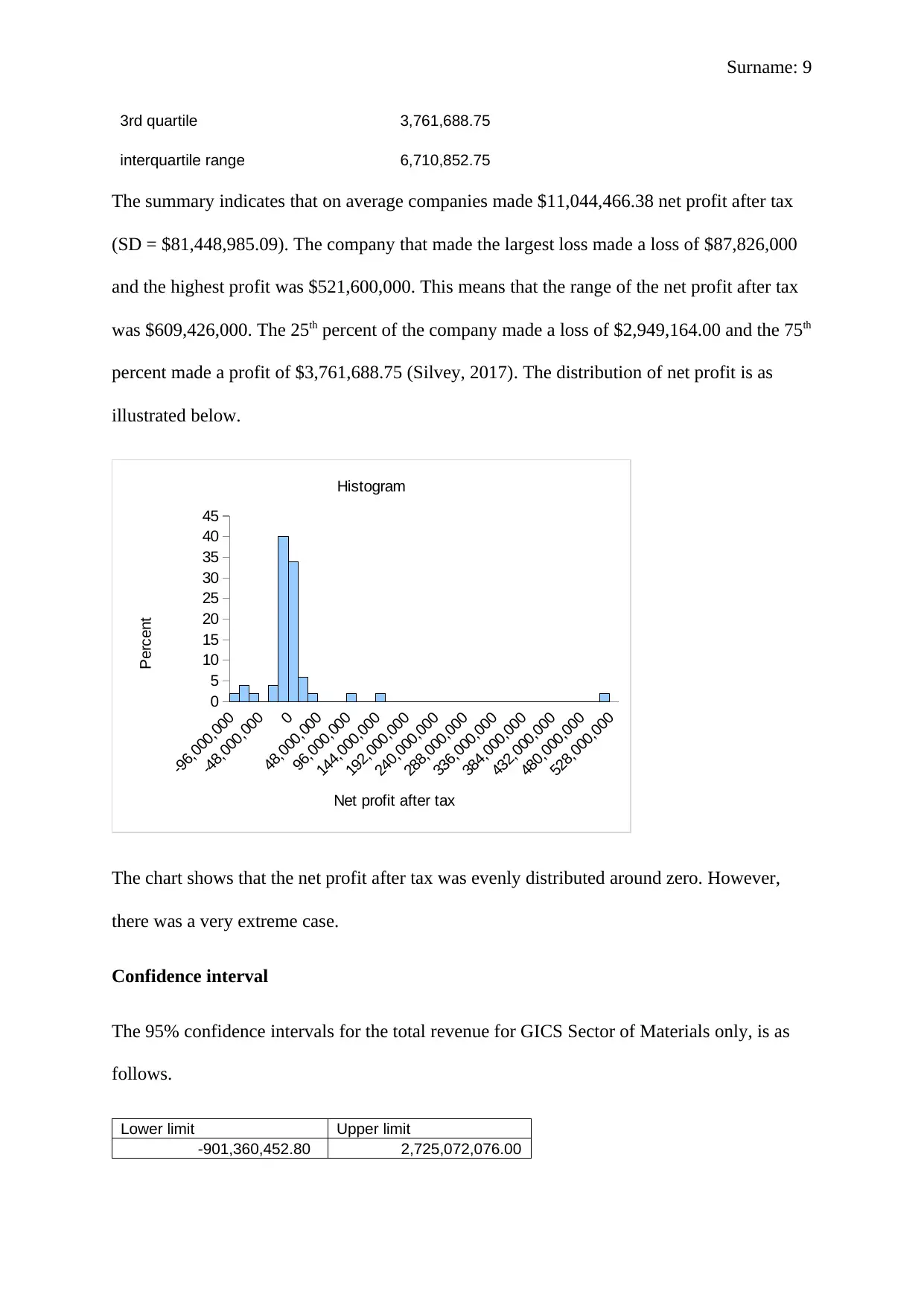

percent made a profit of $3,761,688.75 (Silvey, 2017). The distribution of net profit is as

illustrated below.

-96,000,000

-48,000,000

0

48,000,000

96,000,000

144,000,000

192,000,000

240,000,000

288,000,000

336,000,000

384,000,000

432,000,000

480,000,000

528,000,000

0

5

10

15

20

25

30

35

40

45

Histogram

Net profit after tax

Percent

The chart shows that the net profit after tax was evenly distributed around zero. However,

there was a very extreme case.

Confidence interval

The 95% confidence intervals for the total revenue for GICS Sector of Materials only, is as

follows.

Lower limit Upper limit

-901,360,452.80 2,725,072,076.00

3rd quartile 3,761,688.75

interquartile range 6,710,852.75

The summary indicates that on average companies made $11,044,466.38 net profit after tax

(SD = $81,448,985.09). The company that made the largest loss made a loss of $87,826,000

and the highest profit was $521,600,000. This means that the range of the net profit after tax

was $609,426,000. The 25th percent of the company made a loss of $2,949,164.00 and the 75th

percent made a profit of $3,761,688.75 (Silvey, 2017). The distribution of net profit is as

illustrated below.

-96,000,000

-48,000,000

0

48,000,000

96,000,000

144,000,000

192,000,000

240,000,000

288,000,000

336,000,000

384,000,000

432,000,000

480,000,000

528,000,000

0

5

10

15

20

25

30

35

40

45

Histogram

Net profit after tax

Percent

The chart shows that the net profit after tax was evenly distributed around zero. However,

there was a very extreme case.

Confidence interval

The 95% confidence intervals for the total revenue for GICS Sector of Materials only, is as

follows.

Lower limit Upper limit

-901,360,452.80 2,725,072,076.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Surname: 10

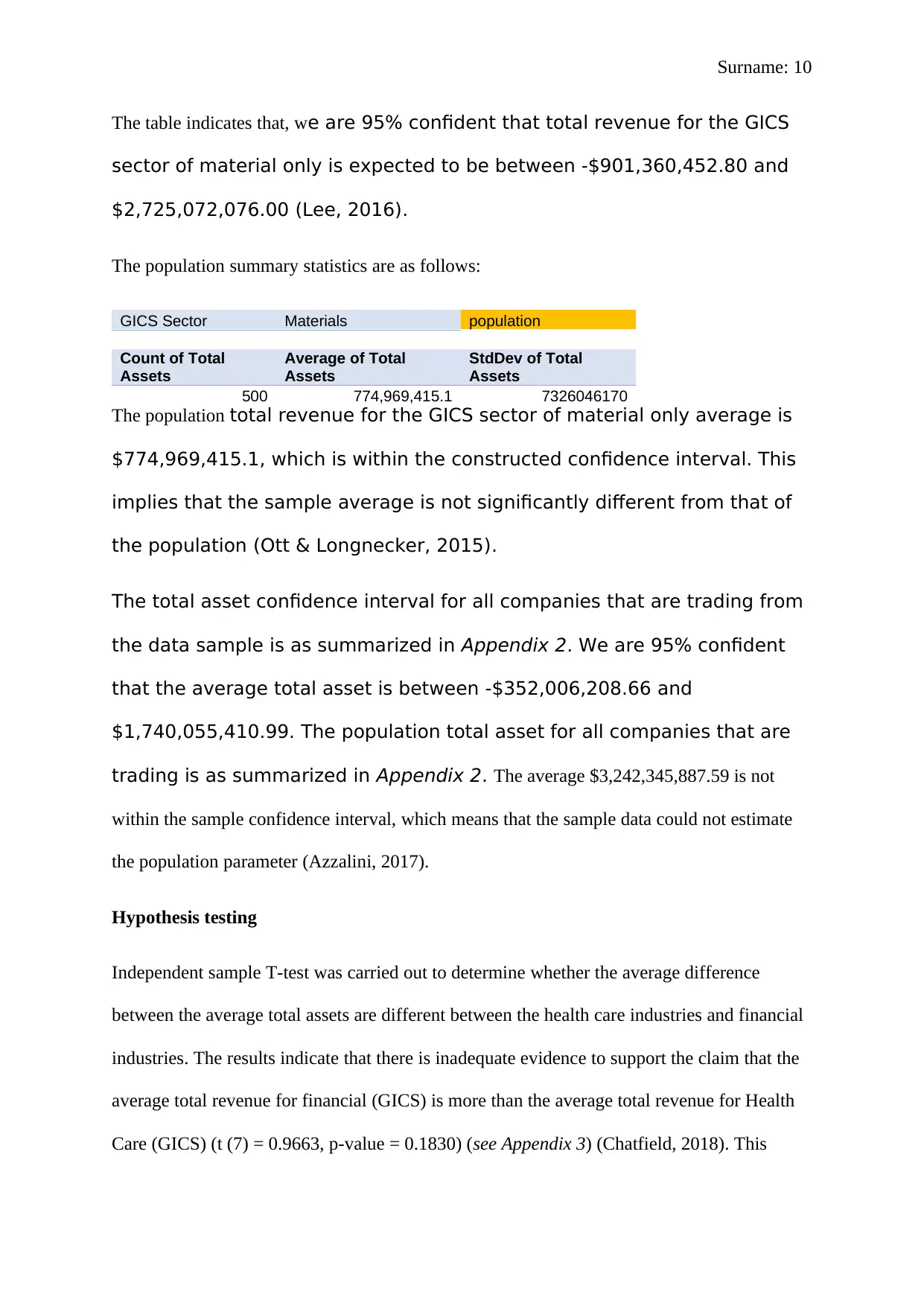

The table indicates that, we are 95% confident that total revenue for the GICS

sector of material only is expected to be between -$901,360,452.80 and

$2,725,072,076.00 (Lee, 2016).

The population summary statistics are as follows:

GICS Sector Materials population

Count of Total

Assets

Average of Total

Assets

StdDev of Total

Assets

500 774,969,415.1 7326046170

The population total revenue for the GICS sector of material only average is

$774,969,415.1, which is within the constructed confidence interval. This

implies that the sample average is not significantly different from that of

the population (Ott & Longnecker, 2015).

The total asset confidence interval for all companies that are trading from

the data sample is as summarized in Appendix 2. We are 95% confident

that the average total asset is between -$352,006,208.66 and

$1,740,055,410.99. The population total asset for all companies that are

trading is as summarized in Appendix 2. The average $3,242,345,887.59 is not

within the sample confidence interval, which means that the sample data could not estimate

the population parameter (Azzalini, 2017).

Hypothesis testing

Independent sample T-test was carried out to determine whether the average difference

between the average total assets are different between the health care industries and financial

industries. The results indicate that there is inadequate evidence to support the claim that the

average total revenue for financial (GICS) is more than the average total revenue for Health

Care (GICS) (t (7) = 0.9663, p-value = 0.1830) (see Appendix 3) (Chatfield, 2018). This

The table indicates that, we are 95% confident that total revenue for the GICS

sector of material only is expected to be between -$901,360,452.80 and

$2,725,072,076.00 (Lee, 2016).

The population summary statistics are as follows:

GICS Sector Materials population

Count of Total

Assets

Average of Total

Assets

StdDev of Total

Assets

500 774,969,415.1 7326046170

The population total revenue for the GICS sector of material only average is

$774,969,415.1, which is within the constructed confidence interval. This

implies that the sample average is not significantly different from that of

the population (Ott & Longnecker, 2015).

The total asset confidence interval for all companies that are trading from

the data sample is as summarized in Appendix 2. We are 95% confident

that the average total asset is between -$352,006,208.66 and

$1,740,055,410.99. The population total asset for all companies that are

trading is as summarized in Appendix 2. The average $3,242,345,887.59 is not

within the sample confidence interval, which means that the sample data could not estimate

the population parameter (Azzalini, 2017).

Hypothesis testing

Independent sample T-test was carried out to determine whether the average difference

between the average total assets are different between the health care industries and financial

industries. The results indicate that there is inadequate evidence to support the claim that the

average total revenue for financial (GICS) is more than the average total revenue for Health

Care (GICS) (t (7) = 0.9663, p-value = 0.1830) (see Appendix 3) (Chatfield, 2018). This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Surname: 11

means that the average between the average total asset for the health care industries and

financial industries is not different. However, the test, in this case, might be unreliable since

the sample used was too small. Nonetheless, one can conclude that the average total revenue

for Financials (GICS) is not more than the average total revenue for Health Care (GICS).

An analysis was carried out to determine whether the average market capitalization, differs

for financial and materials. The results indicate that there is inadequate evidence to support

that claim (t (20) = -0.7233, p-value = 0.4779) (see Appendix 4) (Sullivan III, 2015). This

implies that the average market capitalization does not differ for Financials and materials.

Therefore, when an investor is planning to venture into either of the two, he/she should know

that the two require an equal amount of capital.

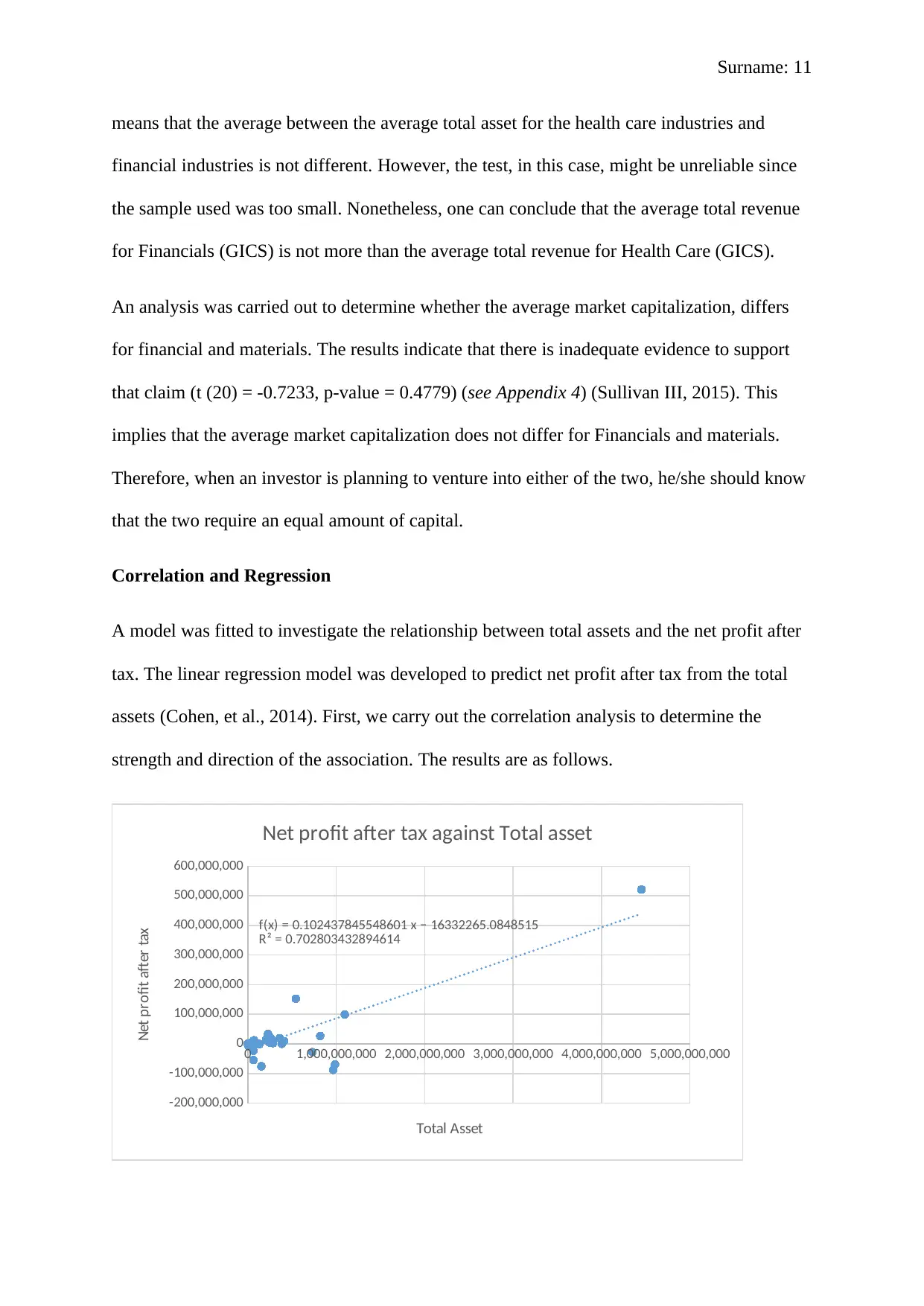

Correlation and Regression

A model was fitted to investigate the relationship between total assets and the net profit after

tax. The linear regression model was developed to predict net profit after tax from the total

assets (Cohen, et al., 2014). First, we carry out the correlation analysis to determine the

strength and direction of the association. The results are as follows.

0 1,000,000,000 2,000,000,000 3,000,000,000 4,000,000,000 5,000,000,000

-200,000,000

-100,000,000

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

f(x) = 0.102437845548601 x − 16332265.0848515

R² = 0.702803432894614

Net profit after tax against Total asset

Total Asset

Net profit after tax

means that the average between the average total asset for the health care industries and

financial industries is not different. However, the test, in this case, might be unreliable since

the sample used was too small. Nonetheless, one can conclude that the average total revenue

for Financials (GICS) is not more than the average total revenue for Health Care (GICS).

An analysis was carried out to determine whether the average market capitalization, differs

for financial and materials. The results indicate that there is inadequate evidence to support

that claim (t (20) = -0.7233, p-value = 0.4779) (see Appendix 4) (Sullivan III, 2015). This

implies that the average market capitalization does not differ for Financials and materials.

Therefore, when an investor is planning to venture into either of the two, he/she should know

that the two require an equal amount of capital.

Correlation and Regression

A model was fitted to investigate the relationship between total assets and the net profit after

tax. The linear regression model was developed to predict net profit after tax from the total

assets (Cohen, et al., 2014). First, we carry out the correlation analysis to determine the

strength and direction of the association. The results are as follows.

0 1,000,000,000 2,000,000,000 3,000,000,000 4,000,000,000 5,000,000,000

-200,000,000

-100,000,000

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

f(x) = 0.102437845548601 x − 16332265.0848515

R² = 0.702803432894614

Net profit after tax against Total asset

Total Asset

Net profit after tax

Surname: 12

The plot indicates that there is a strong positive relationship between total assets and net

profit after tax (Bland, 2015). Further, an analysis was carried out to determine whether there

is a linear relationship between total assets and net profit after tax. The hypothesis was as

follows:

H0: there is no linear relationship between total assets and net profit after tax.

Ha: there is a linear relationship between total assets and net profit after tax.

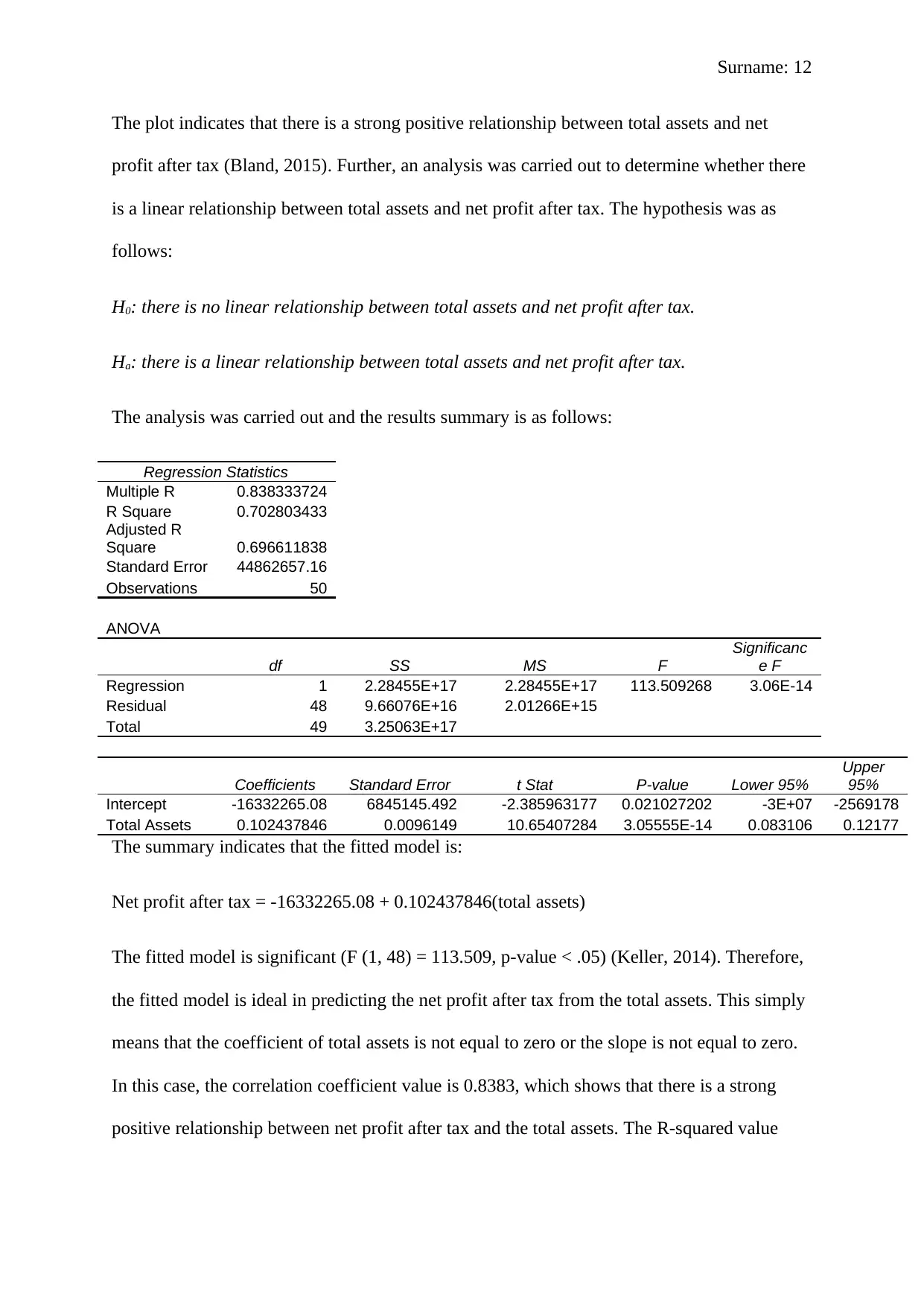

The analysis was carried out and the results summary is as follows:

Regression Statistics

Multiple R 0.838333724

R Square 0.702803433

Adjusted R

Square 0.696611838

Standard Error 44862657.16

Observations 50

ANOVA

df SS MS F

Significanc

e F

Regression 1 2.28455E+17 2.28455E+17 113.509268 3.06E-14

Residual 48 9.66076E+16 2.01266E+15

Total 49 3.25063E+17

Coefficients Standard Error t Stat P-value Lower 95%

Upper

95%

Intercept -16332265.08 6845145.492 -2.385963177 0.021027202 -3E+07 -2569178

Total Assets 0.102437846 0.0096149 10.65407284 3.05555E-14 0.083106 0.12177

The summary indicates that the fitted model is:

Net profit after tax = -16332265.08 + 0.102437846(total assets)

The fitted model is significant (F (1, 48) = 113.509, p-value < .05) (Keller, 2014). Therefore,

the fitted model is ideal in predicting the net profit after tax from the total assets. This simply

means that the coefficient of total assets is not equal to zero or the slope is not equal to zero.

In this case, the correlation coefficient value is 0.8383, which shows that there is a strong

positive relationship between net profit after tax and the total assets. The R-squared value

The plot indicates that there is a strong positive relationship between total assets and net

profit after tax (Bland, 2015). Further, an analysis was carried out to determine whether there

is a linear relationship between total assets and net profit after tax. The hypothesis was as

follows:

H0: there is no linear relationship between total assets and net profit after tax.

Ha: there is a linear relationship between total assets and net profit after tax.

The analysis was carried out and the results summary is as follows:

Regression Statistics

Multiple R 0.838333724

R Square 0.702803433

Adjusted R

Square 0.696611838

Standard Error 44862657.16

Observations 50

ANOVA

df SS MS F

Significanc

e F

Regression 1 2.28455E+17 2.28455E+17 113.509268 3.06E-14

Residual 48 9.66076E+16 2.01266E+15

Total 49 3.25063E+17

Coefficients Standard Error t Stat P-value Lower 95%

Upper

95%

Intercept -16332265.08 6845145.492 -2.385963177 0.021027202 -3E+07 -2569178

Total Assets 0.102437846 0.0096149 10.65407284 3.05555E-14 0.083106 0.12177

The summary indicates that the fitted model is:

Net profit after tax = -16332265.08 + 0.102437846(total assets)

The fitted model is significant (F (1, 48) = 113.509, p-value < .05) (Keller, 2014). Therefore,

the fitted model is ideal in predicting the net profit after tax from the total assets. This simply

means that the coefficient of total assets is not equal to zero or the slope is not equal to zero.

In this case, the correlation coefficient value is 0.8383, which shows that there is a strong

positive relationship between net profit after tax and the total assets. The R-squared value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.