Swanston Banking Group Ltd. Report 2022

Conduct research analysis in the superannuation industry for the Diploma of Financial Planning and RG146 Compliance Programs.

13 Pages2557 Words17 Views

Added on 2022-10-08

Swanston Banking Group Ltd. Report 2022

Conduct research analysis in the superannuation industry for the Diploma of Financial Planning and RG146 Compliance Programs.

Added on 2022-10-08

ShareRelated Documents

Client File Note

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

Client Goals

The objective and goals of the clients are the most important elements considered while recommending a

strategy for the clients. The reason that the clients hire the services of an expert in financial matter is to

achieve their goals and objectives. The constraint of resources makes it difficult for a client to use the

resources to achieve all of his or her goals and objectives. The financial experts by providing expertise

advice helps to optimize the use of client’s resources to help him achieve his goals and objectives in the

future. The report in this document detailed out a proper strategy for Johhny Wilson and Julia Wilson to

ensure they achieve their financial goals and objectives including securing the future of their family.

Taking into consideration the current state of finance of the couple including their current income and

expenditures let us now recommend appropriate courses of actions for the couple to achieve their

financial goals in the future. Firstly let us discuss about the goals and objectives of the couple.

Clearing debts:

Firstly, the couple is looking to clear their debts immediately. Since, it is not possible to clear the debt of

$327,032 (mortgage amount as per the asset and liabilities statement of the couple) hence, the couple is

looking to clear the debts by repaying the mortgage as soon as practically possible. Thus, clearing the

debts is of utmost importance to the couple.

Protection:

Taking different policies such as life insurance policies, medical policies and other health policies to

protect the couple and their family is also included in the overall objectives of the couple. Thus, the couple

is looking to take necessary protection to provide for the future.

Stable financial condition:

One of the most important objectives of the couple is to have a stable financial condition in the future.

Constant worrying about the future is something that couple would like to avoid by ensuring that there will

be substantial funds to provide for the future expenses of the couple and the family.

Providing for day to day expenses of the household:

The day to day expenses of the couple and the family shall be available after making all necessary

investment decisions. Thus, recommendations of the financial expert should not only about

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

Client Goals

The objective and goals of the clients are the most important elements considered while recommending a

strategy for the clients. The reason that the clients hire the services of an expert in financial matter is to

achieve their goals and objectives. The constraint of resources makes it difficult for a client to use the

resources to achieve all of his or her goals and objectives. The financial experts by providing expertise

advice helps to optimize the use of client’s resources to help him achieve his goals and objectives in the

future. The report in this document detailed out a proper strategy for Johhny Wilson and Julia Wilson to

ensure they achieve their financial goals and objectives including securing the future of their family.

Taking into consideration the current state of finance of the couple including their current income and

expenditures let us now recommend appropriate courses of actions for the couple to achieve their

financial goals in the future. Firstly let us discuss about the goals and objectives of the couple.

Clearing debts:

Firstly, the couple is looking to clear their debts immediately. Since, it is not possible to clear the debt of

$327,032 (mortgage amount as per the asset and liabilities statement of the couple) hence, the couple is

looking to clear the debts by repaying the mortgage as soon as practically possible. Thus, clearing the

debts is of utmost importance to the couple.

Protection:

Taking different policies such as life insurance policies, medical policies and other health policies to

protect the couple and their family is also included in the overall objectives of the couple. Thus, the couple

is looking to take necessary protection to provide for the future.

Stable financial condition:

One of the most important objectives of the couple is to have a stable financial condition in the future.

Constant worrying about the future is something that couple would like to avoid by ensuring that there will

be substantial funds to provide for the future expenses of the couple and the family.

Providing for day to day expenses of the household:

The day to day expenses of the couple and the family shall be available after making all necessary

investment decisions. Thus, recommendations of the financial expert should not only about

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Client File Note

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

recommending on investment options but also to ensure that after making necessary investments the

couple shall left with necessary funds to meet the day to day expenses of the family.

Acquisition of new home:

The couple is aiming to acquire a new home by the end of 2020. Thus, the experts must recommend an

appropriate strategy to the couple to ensure that the couple is able to buy a new home by the end of

2020.

Providing for the education of the children:

The couple wants set up a fund to ensure that the children have necessary funds to finance their

education. Both secondary and higher education of the children should be completed without any financial

problem is another goal of the couple.

Providing for travelling expenses:

The couple travels inter-state as well as out of the countries quite often for both vacation and professional

purposes. Thus, the goals and objectives of the couple include financing the travelling expenses of the

couple in the future.

Planning the retirement:

Johhny Wilosn planning to retire at the age of 55 years and he does not wish to work after attaining the

age of 55 years thus, the goals of the couple include an effective retirement plan that will help Johhny to

take retirement from his occupation by the age of 55 years and he would not have to work again to meet

his and his family’s financial needs.

Acquisition of a new bike:

Johhny is also considering acquiring a new bike within next 12 months period. Thus, it is again one of the

goals of the couple to have a new bike by the end of next 12 months.

Advice

In order to achieve the above goals and objectives the couple should comply with the following

recommendations of the financial expert.

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

recommending on investment options but also to ensure that after making necessary investments the

couple shall left with necessary funds to meet the day to day expenses of the family.

Acquisition of new home:

The couple is aiming to acquire a new home by the end of 2020. Thus, the experts must recommend an

appropriate strategy to the couple to ensure that the couple is able to buy a new home by the end of

2020.

Providing for the education of the children:

The couple wants set up a fund to ensure that the children have necessary funds to finance their

education. Both secondary and higher education of the children should be completed without any financial

problem is another goal of the couple.

Providing for travelling expenses:

The couple travels inter-state as well as out of the countries quite often for both vacation and professional

purposes. Thus, the goals and objectives of the couple include financing the travelling expenses of the

couple in the future.

Planning the retirement:

Johhny Wilosn planning to retire at the age of 55 years and he does not wish to work after attaining the

age of 55 years thus, the goals of the couple include an effective retirement plan that will help Johhny to

take retirement from his occupation by the age of 55 years and he would not have to work again to meet

his and his family’s financial needs.

Acquisition of a new bike:

Johhny is also considering acquiring a new bike within next 12 months period. Thus, it is again one of the

goals of the couple to have a new bike by the end of next 12 months.

Advice

In order to achieve the above goals and objectives the couple should comply with the following

recommendations of the financial expert.

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Client File Note

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

Rescheduling the loan repayment:

Firstly, the couple should reschedule the loan repayment by increasing the annual mortgage payment.

This would help the couple to reduce the time to clear the entire debt in shorter time than the current time

required to repay the entire mortgage. Considering that the client is having substantial amount of surplus

at present thus, it would not be difficult to increase the annual repayment amount of mortgage.

Taking new protection policies:

The couple should take new life and medical insurance policies to increase the protection against life and

medical issues in the future.

Stability in financial condition:

The couple should invest in government bonds and fixed interest bearing securities to ensure

that there is stability at least about certain monthly and annual income as these

investments generally provide stable rate of return to the investors without default. Thus,

financial stability would be achieved by making such investments.

Household expenses:

The couple shall keep the household expenses separately to ensure there is no compromise with the

household requirements. Thus, after keeping the amount of household expenses separately from the net

income of the couple, they should invest on the recommended assets and securities.

Salary sacrifice and increase contribution to super funds:

The couple should seriously consider sacrificing certain portion of their salaries to increase their

contribution to the superannuation funds. Sacrificing salary to the extent of 15% of gross salary will help

the couple to reduce their income tax liability. In addition the contribution in superannuation fund would be

significantly higher resulting accumulation of larger amount in respective superannuation funds of the

couples. The combined gross salary of Johhnny and Julia is $286,000 ($180,000 + $106,000 thus,

contribution to the superannuation fund by maximum possible amount, i.e. 15% of gross salary of the

couple would help the couple to accumulate significant amount of money in the fund. This will have

multiple benefits for the couple as not only they will contribute significant amount in superannuation fund

but they will also get equal contribution form the employer. In addition the clients’ taxable income would

also be lowered by the amount of salary sacrifice which will reduce the tax liability of the couple.

Hence, Johhnny and Julia should sacrifice 15% of their respective salaries to contribute the same into the

superannuation fund. Thus, the couple in combination should sacrifice $42,900 (286000 x15 %) to

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

Rescheduling the loan repayment:

Firstly, the couple should reschedule the loan repayment by increasing the annual mortgage payment.

This would help the couple to reduce the time to clear the entire debt in shorter time than the current time

required to repay the entire mortgage. Considering that the client is having substantial amount of surplus

at present thus, it would not be difficult to increase the annual repayment amount of mortgage.

Taking new protection policies:

The couple should take new life and medical insurance policies to increase the protection against life and

medical issues in the future.

Stability in financial condition:

The couple should invest in government bonds and fixed interest bearing securities to ensure

that there is stability at least about certain monthly and annual income as these

investments generally provide stable rate of return to the investors without default. Thus,

financial stability would be achieved by making such investments.

Household expenses:

The couple shall keep the household expenses separately to ensure there is no compromise with the

household requirements. Thus, after keeping the amount of household expenses separately from the net

income of the couple, they should invest on the recommended assets and securities.

Salary sacrifice and increase contribution to super funds:

The couple should seriously consider sacrificing certain portion of their salaries to increase their

contribution to the superannuation funds. Sacrificing salary to the extent of 15% of gross salary will help

the couple to reduce their income tax liability. In addition the contribution in superannuation fund would be

significantly higher resulting accumulation of larger amount in respective superannuation funds of the

couples. The combined gross salary of Johhnny and Julia is $286,000 ($180,000 + $106,000 thus,

contribution to the superannuation fund by maximum possible amount, i.e. 15% of gross salary of the

couple would help the couple to accumulate significant amount of money in the fund. This will have

multiple benefits for the couple as not only they will contribute significant amount in superannuation fund

but they will also get equal contribution form the employer. In addition the clients’ taxable income would

also be lowered by the amount of salary sacrifice which will reduce the tax liability of the couple.

Hence, Johhnny and Julia should sacrifice 15% of their respective salaries to contribute the same into the

superannuation fund. Thus, the couple in combination should sacrifice $42,900 (286000 x15 %) to

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Client File Note

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

contribute the same into superannuation fund. The employers of the couple will also make equal

contribution in the superannuation fund. Thus, in each year the couple will have $85,800 contributed to

the superannuation funds due to sacrificing 15% of their gross salaries. Thus, if the fund is expected to

provide a normal 3% rate of return on the funds invested then within a period of next 10 years the couple

will have significant amount of money in their respective superannuation funds.

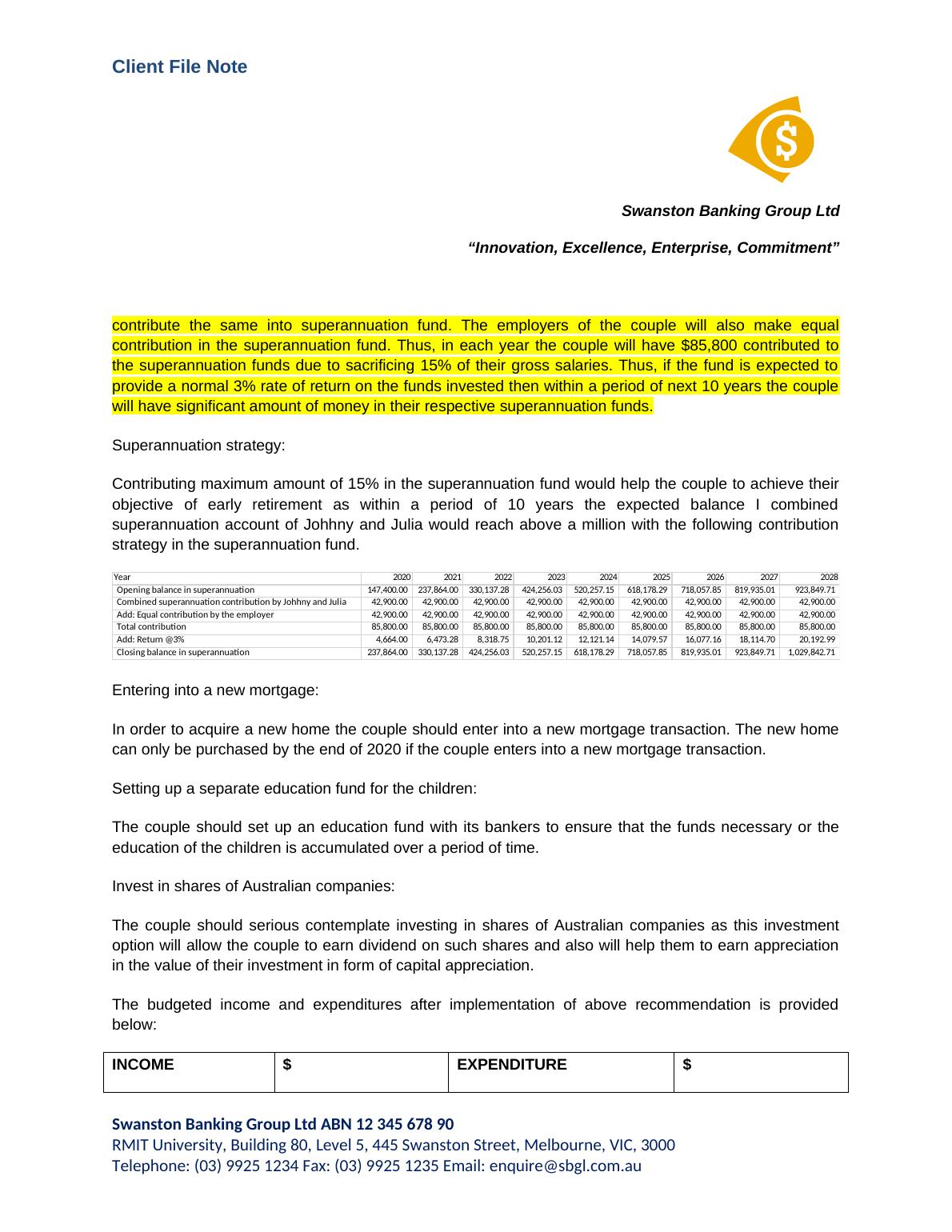

Superannuation strategy:

Contributing maximum amount of 15% in the superannuation fund would help the couple to achieve their

objective of early retirement as within a period of 10 years the expected balance I combined

superannuation account of Johhny and Julia would reach above a million with the following contribution

strategy in the superannuation fund.

Year 2020 2021 2022 2023 2024 2025 2026 2027 2028

Opening balance in superannuation 147,400.00 237,864.00 330,137.28 424,256.03 520,257.15 618,178.29 718,057.85 819,935.01 923,849.71

Combined superannuation contribution by Johhny and Julia 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00

Add: Equal contribution by the employer 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00

Total contribution 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00

Add: Return @3% 4,664.00 6,473.28 8,318.75 10,201.12 12,121.14 14,079.57 16,077.16 18,114.70 20,192.99

Closingbalance in superannuation 237,864.00 330,137.28 424,256.03 520,257.15 618,178.29 718,057.85 819,935.01 923,849.71 1,029,842.71

Entering into a new mortgage:

In order to acquire a new home the couple should enter into a new mortgage transaction. The new home

can only be purchased by the end of 2020 if the couple enters into a new mortgage transaction.

Setting up a separate education fund for the children:

The couple should set up an education fund with its bankers to ensure that the funds necessary or the

education of the children is accumulated over a period of time.

Invest in shares of Australian companies:

The couple should serious contemplate investing in shares of Australian companies as this investment

option will allow the couple to earn dividend on such shares and also will help them to earn appreciation

in the value of their investment in form of capital appreciation.

The budgeted income and expenditures after implementation of above recommendation is provided

below:

INCOME $ EXPENDITURE $

(Average Monthly) (Average Monthly)

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

Swanston Banking Group Ltd

“Innovation, Excellence, Enterprise, Commitment”

contribute the same into superannuation fund. The employers of the couple will also make equal

contribution in the superannuation fund. Thus, in each year the couple will have $85,800 contributed to

the superannuation funds due to sacrificing 15% of their gross salaries. Thus, if the fund is expected to

provide a normal 3% rate of return on the funds invested then within a period of next 10 years the couple

will have significant amount of money in their respective superannuation funds.

Superannuation strategy:

Contributing maximum amount of 15% in the superannuation fund would help the couple to achieve their

objective of early retirement as within a period of 10 years the expected balance I combined

superannuation account of Johhny and Julia would reach above a million with the following contribution

strategy in the superannuation fund.

Year 2020 2021 2022 2023 2024 2025 2026 2027 2028

Opening balance in superannuation 147,400.00 237,864.00 330,137.28 424,256.03 520,257.15 618,178.29 718,057.85 819,935.01 923,849.71

Combined superannuation contribution by Johhny and Julia 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00

Add: Equal contribution by the employer 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00 42,900.00

Total contribution 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00 85,800.00

Add: Return @3% 4,664.00 6,473.28 8,318.75 10,201.12 12,121.14 14,079.57 16,077.16 18,114.70 20,192.99

Closingbalance in superannuation 237,864.00 330,137.28 424,256.03 520,257.15 618,178.29 718,057.85 819,935.01 923,849.71 1,029,842.71

Entering into a new mortgage:

In order to acquire a new home the couple should enter into a new mortgage transaction. The new home

can only be purchased by the end of 2020 if the couple enters into a new mortgage transaction.

Setting up a separate education fund for the children:

The couple should set up an education fund with its bankers to ensure that the funds necessary or the

education of the children is accumulated over a period of time.

Invest in shares of Australian companies:

The couple should serious contemplate investing in shares of Australian companies as this investment

option will allow the couple to earn dividend on such shares and also will help them to earn appreciation

in the value of their investment in form of capital appreciation.

The budgeted income and expenditures after implementation of above recommendation is provided

below:

INCOME $ EXPENDITURE $

(Average Monthly) (Average Monthly)

Swanston Banking Group Ltd ABN 12 345 678 90

RMIT University, Building 80, Level 5, 445 Swanston Street, Melbourne, VIC, 3000

Telephone: (03) 9925 1234 Fax: (03) 9925 1235 Email: enquire@sbgl.com.au

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Assignment about What is Transcript?lg...

|8

|1478

|20

Personal Finance - An Introductionlg...

|11

|517

|98

Personal Finance: Retirement Planning and Financial Objectiveslg...

|25

|4361

|468

Financial Planning TABLE OF CONTENTS INTRODUCTIONlg...

|6

|979

|130

Financial Planning: Statement of Advicelg...

|24

|5058

|394

Assignment On The Presentationlg...

|21

|1818

|23