Financial Report: Option Pricing and Hedging Strategies in Finance

VerifiedAdded on 2022/08/27

|6

|1696

|15

Report

AI Summary

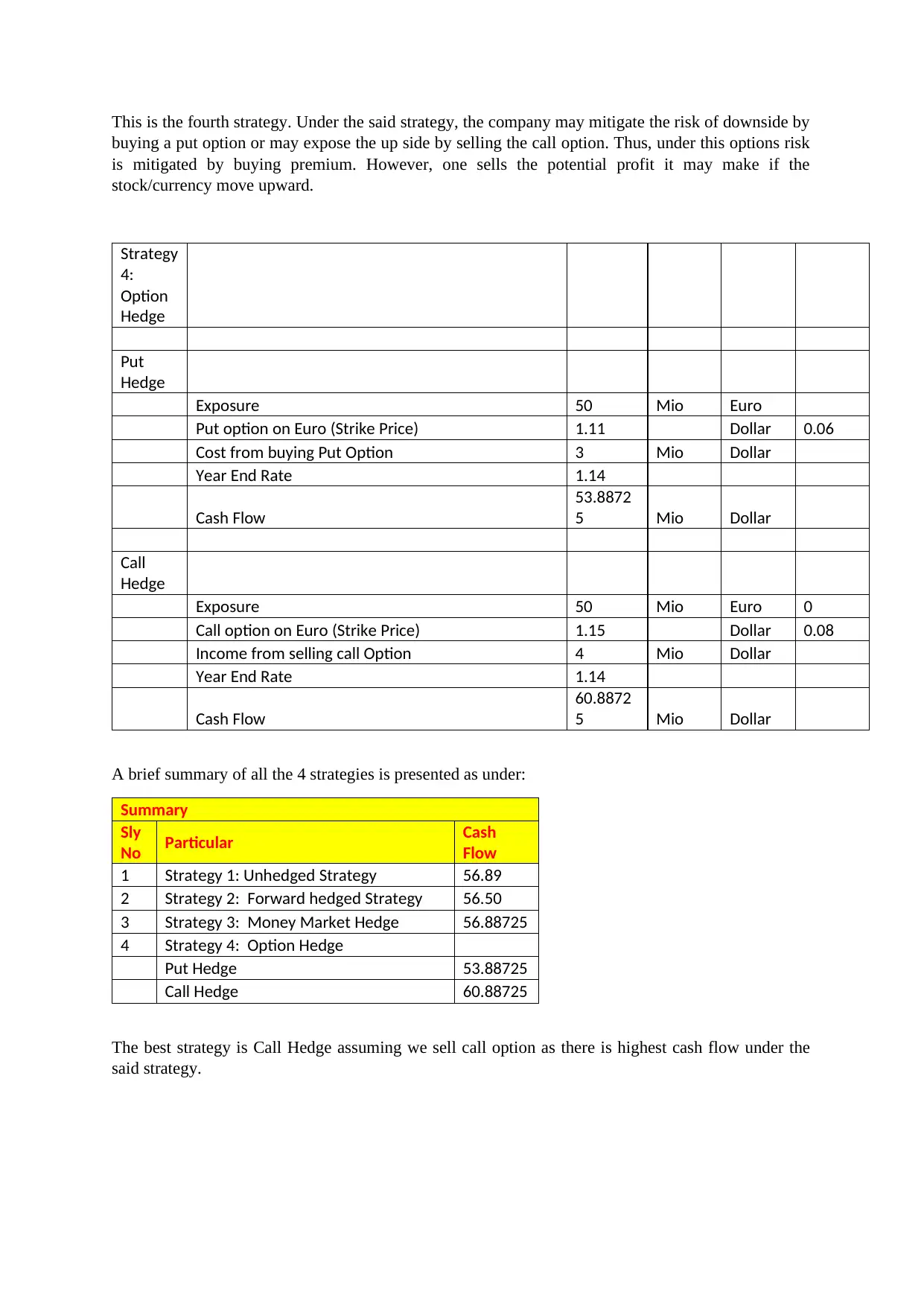

This report provides a comprehensive analysis of option pricing and hedging strategies, using a real-world example of the Swiss National Bank's decision to de-peg the Swiss Franc from the Euro. The report explores the rationale behind the bank's actions and the impact on Swiss exporters. It then delves into various hedging strategies, including forward contracts, future contracts, and currency options, that businesses can employ to mitigate currency risk. The core of the report is a detailed examination of four hedging strategies (unhedged, forward hedged, money market hedge, and option hedge) applied to a scenario involving Euro and US Dollar currency exposure. It calculates the expected cash flows under each strategy, comparing the outcomes of put and call options, and concludes with a recommendation of the optimal strategy based on the highest potential cash flow. The report includes references to relevant financial sources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.