Managerial Accounting Report for Swipe 50 Limited: Profit Analysis

VerifiedAdded on 2021/10/06

|12

|4823

|208

Report

AI Summary

This report provides a detailed analysis of managerial accounting processes for Swipe 50 Limited, focusing on profit statements prepared using absorption and variable costing methods for February and March. The report includes profit reconciliation statements, comparing the results from both costing methods, and explains the differences and importance of each method. It also explores how fixed overhead expenses are treated. Further, the report examines three ways Swipe 50 Limited can improve its accounting systems and discusses the importance of a managing accountant within a manufacturing company. The report also includes calculations of cost of goods sold, gross margin, operating income, and contribution margin. The conclusion summarizes the key findings and provides recommendations for the company to enhance its financial reporting and decision-making processes.

1

Table of Contents

Table of Contents...........................................................................................................1

Introduction...........................................................................................................2

Part 1. Profit Statements for Swipe 50 Limited for the months of February and March

1)Profit Statements using Absorption Costing for February and March....................3

2)Profit Statements using Variable Costing for February and March........................4

Part 2. Profit Reconciliation Statement calculated using Absorption Costing to that

using Variable costing..........................................................................................4

Part 3. How each method differs from the other method and also explain in the

importance of each of the methods..................................................................5-7

Part 4. Three ways that Swipes 50 Limited can improve its accounting systems......7-10

Part 5. Why the managing accountant job are important within a manufacturing

company........................................................................................................10-11

Conclusion....................................................................................................................12

References....................................................................................................................12

Table of Contents

Table of Contents...........................................................................................................1

Introduction...........................................................................................................2

Part 1. Profit Statements for Swipe 50 Limited for the months of February and March

1)Profit Statements using Absorption Costing for February and March....................3

2)Profit Statements using Variable Costing for February and March........................4

Part 2. Profit Reconciliation Statement calculated using Absorption Costing to that

using Variable costing..........................................................................................4

Part 3. How each method differs from the other method and also explain in the

importance of each of the methods..................................................................5-7

Part 4. Three ways that Swipes 50 Limited can improve its accounting systems......7-10

Part 5. Why the managing accountant job are important within a manufacturing

company........................................................................................................10-11

Conclusion....................................................................................................................12

References....................................................................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Introduction

There is large importance of managerial accounting processes for a company as it helps

in collecting, recording, analyzing and interpreting the internal accounting information

that assists the business managers to take important decisions regarding its future growth

and development. In this context, the present report is being undertaken for the purpose

of providing an adequate understanding of the managerial accounting processes for

evaluation of a company internal business processes and developing future strategic

action plan. The use of different accounting methods adopted by a company for

preparation of internal accounting information is explained adequately within the report.

Managerial accounting is the branch of accounting that deals with providing accounting

information that is useful to managers in decision-making. Unlike financial accounting, it

does not focus on following reporting standards. Rather, it makes use of principles from

different fields of business to cater to management needs.

Managerial accounting involves budgeting and forecasting, performance evaluation,

financial analysis, product costing and pricing, evaluation of business decisions,

governance, corporate finance, and other areas.

Introduction

There is large importance of managerial accounting processes for a company as it helps

in collecting, recording, analyzing and interpreting the internal accounting information

that assists the business managers to take important decisions regarding its future growth

and development. In this context, the present report is being undertaken for the purpose

of providing an adequate understanding of the managerial accounting processes for

evaluation of a company internal business processes and developing future strategic

action plan. The use of different accounting methods adopted by a company for

preparation of internal accounting information is explained adequately within the report.

Managerial accounting is the branch of accounting that deals with providing accounting

information that is useful to managers in decision-making. Unlike financial accounting, it

does not focus on following reporting standards. Rather, it makes use of principles from

different fields of business to cater to management needs.

Managerial accounting involves budgeting and forecasting, performance evaluation,

financial analysis, product costing and pricing, evaluation of business decisions,

governance, corporate finance, and other areas.

3

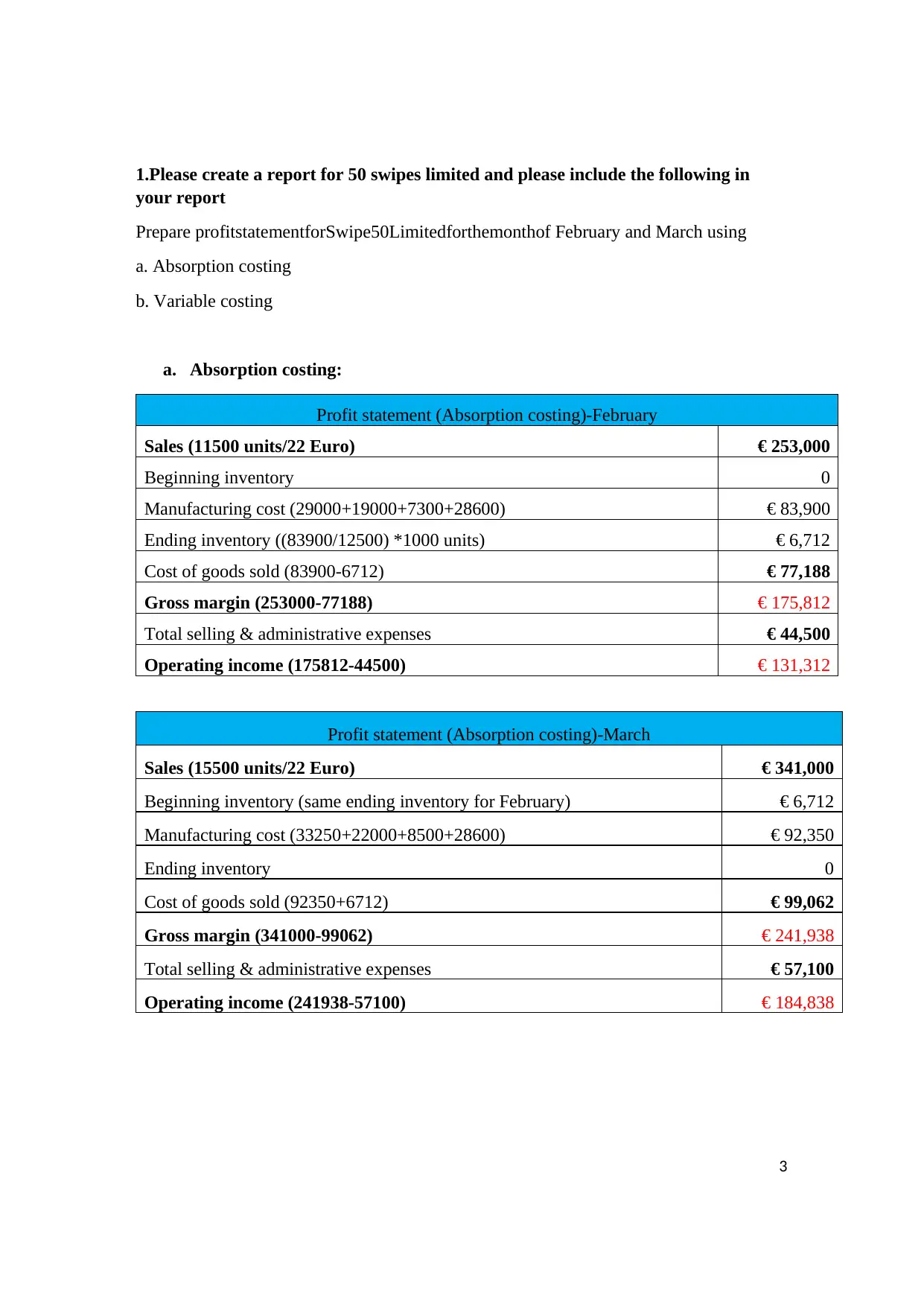

1.Please create a report for 50 swipes limited and please include the following in

your report

Prepare profitstatementforSwipe50Limitedforthemonthof February and March using

a. Absorption costing

b. Variable costing

a. Absorption costing:

Profit statement (Absorption costing)-February

Sales (11500 units/22 Euro) € 253,000

Beginning inventory 0

Manufacturing cost (29000+19000+7300+28600) € 83,900

Ending inventory ((83900/12500) *1000 units) € 6,712

Cost of goods sold (83900-6712) € 77,188

Gross margin (253000-77188) € 175,812

Total selling & administrative expenses € 44,500

Operating income (175812-44500) € 131,312

Profit statement (Absorption costing)-March

Sales (15500 units/22 Euro) € 341,000

Beginning inventory (same ending inventory for February) € 6,712

Manufacturing cost (33250+22000+8500+28600) € 92,350

Ending inventory 0

Cost of goods sold (92350+6712) € 99,062

Gross margin (341000-99062) € 241,938

Total selling & administrative expenses € 57,100

Operating income (241938-57100) € 184,838

1.Please create a report for 50 swipes limited and please include the following in

your report

Prepare profitstatementforSwipe50Limitedforthemonthof February and March using

a. Absorption costing

b. Variable costing

a. Absorption costing:

Profit statement (Absorption costing)-February

Sales (11500 units/22 Euro) € 253,000

Beginning inventory 0

Manufacturing cost (29000+19000+7300+28600) € 83,900

Ending inventory ((83900/12500) *1000 units) € 6,712

Cost of goods sold (83900-6712) € 77,188

Gross margin (253000-77188) € 175,812

Total selling & administrative expenses € 44,500

Operating income (175812-44500) € 131,312

Profit statement (Absorption costing)-March

Sales (15500 units/22 Euro) € 341,000

Beginning inventory (same ending inventory for February) € 6,712

Manufacturing cost (33250+22000+8500+28600) € 92,350

Ending inventory 0

Cost of goods sold (92350+6712) € 99,062

Gross margin (341000-99062) € 241,938

Total selling & administrative expenses € 57,100

Operating income (241938-57100) € 184,838

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

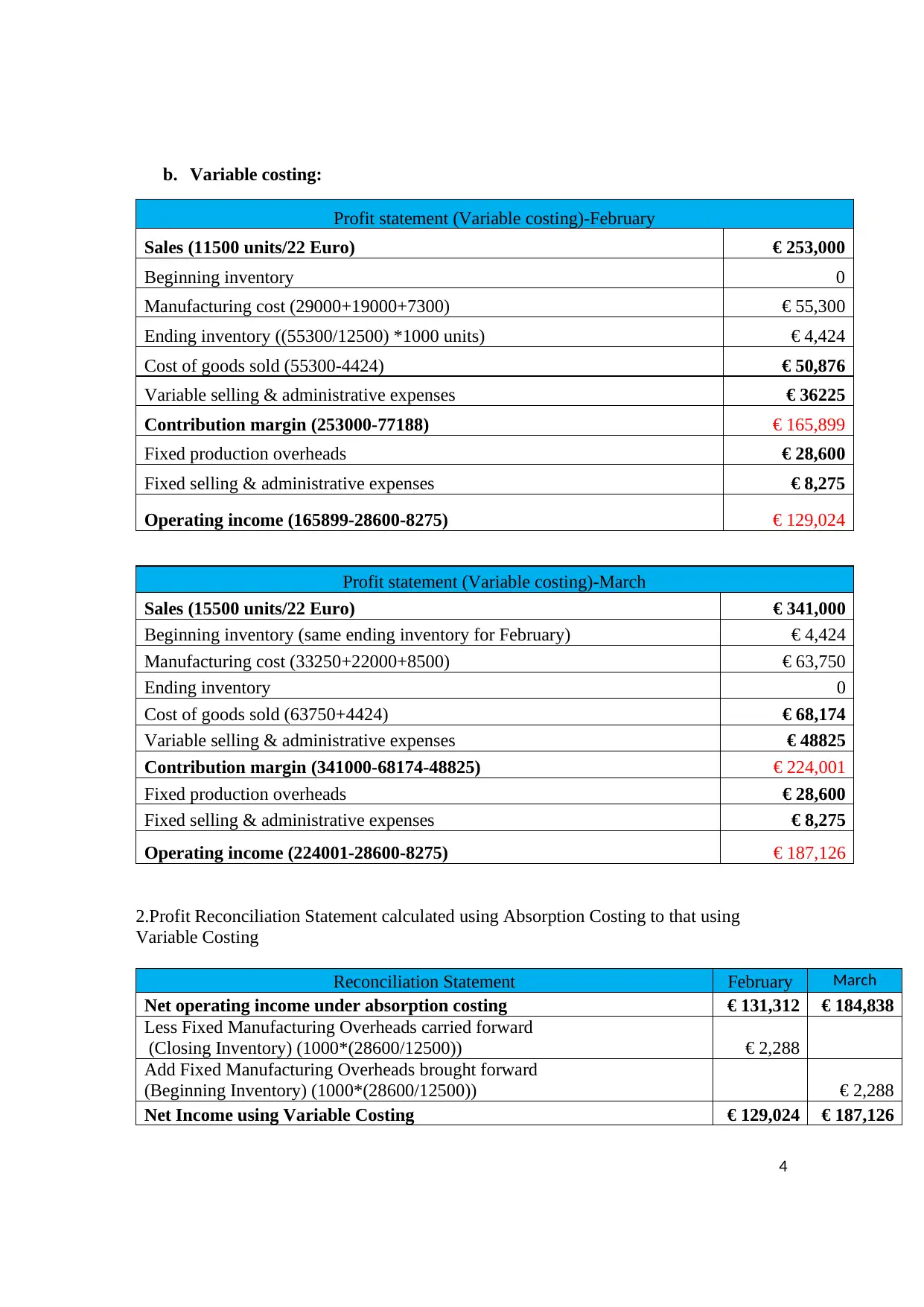

b. Variable costing:

Profit statement (Variable costing)-February

Sales (11500 units/22 Euro) € 253,000

Beginning inventory 0

Manufacturing cost (29000+19000+7300) € 55,300

Ending inventory ((55300/12500) *1000 units) € 4,424

Cost of goods sold (55300-4424) € 50,876

Variable selling & administrative expenses € 36225

Contribution margin (253000-77188) € 165,899

Fixed production overheads € 28,600

Fixed selling & administrative expenses € 8,275

Operating income (165899-28600-8275) € 129,024

Profit statement (Variable costing)-March

Sales (15500 units/22 Euro) € 341,000

Beginning inventory (same ending inventory for February) € 4,424

Manufacturing cost (33250+22000+8500) € 63,750

Ending inventory 0

Cost of goods sold (63750+4424) € 68,174

Variable selling & administrative expenses € 48825

Contribution margin (341000-68174-48825) € 224,001

Fixed production overheads € 28,600

Fixed selling & administrative expenses € 8,275

Operating income (224001-28600-8275) € 187,126

2.Profit Reconciliation Statement calculated using Absorption Costing to that using

Variable Costing

Reconciliation Statement February March

Net operating income under absorption costing € 131,312 € 184,838

Less Fixed Manufacturing Overheads carried forward

(Closing Inventory) (1000*(28600/12500)) € 2,288

Add Fixed Manufacturing Overheads brought forward

(Beginning Inventory) (1000*(28600/12500)) € 2,288

Net Income using Variable Costing € 129,024 € 187,126

b. Variable costing:

Profit statement (Variable costing)-February

Sales (11500 units/22 Euro) € 253,000

Beginning inventory 0

Manufacturing cost (29000+19000+7300) € 55,300

Ending inventory ((55300/12500) *1000 units) € 4,424

Cost of goods sold (55300-4424) € 50,876

Variable selling & administrative expenses € 36225

Contribution margin (253000-77188) € 165,899

Fixed production overheads € 28,600

Fixed selling & administrative expenses € 8,275

Operating income (165899-28600-8275) € 129,024

Profit statement (Variable costing)-March

Sales (15500 units/22 Euro) € 341,000

Beginning inventory (same ending inventory for February) € 4,424

Manufacturing cost (33250+22000+8500) € 63,750

Ending inventory 0

Cost of goods sold (63750+4424) € 68,174

Variable selling & administrative expenses € 48825

Contribution margin (341000-68174-48825) € 224,001

Fixed production overheads € 28,600

Fixed selling & administrative expenses € 8,275

Operating income (224001-28600-8275) € 187,126

2.Profit Reconciliation Statement calculated using Absorption Costing to that using

Variable Costing

Reconciliation Statement February March

Net operating income under absorption costing € 131,312 € 184,838

Less Fixed Manufacturing Overheads carried forward

(Closing Inventory) (1000*(28600/12500)) € 2,288

Add Fixed Manufacturing Overheads brought forward

(Beginning Inventory) (1000*(28600/12500)) € 2,288

Net Income using Variable Costing € 129,024 € 187,126

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

3. Explain how each method differs from the other method and also explain the

importance of each methods.

To better understand Absorption and Variable Costing, its first important to know what is

meant by Managerial Accounting. Sometimes called Management Accounting, it’s also

known as Cost Accounting but regardless of the title used, it’s a process of analyzing

business costs and operations in order to prepare internal financial reports that are used to

aid management decision making processes in achieving the business strategic and other

goals. The word internal is important, as these reports are typically not seen or used by

others outside the company (Noreen, et al., 2016).

However, it’s worthwhile noting early, that under Generally Accepted Accounting

Principles (GAAP), only Absorption Costing is allowed for any company external

financial statement reporting. However, within the business there is a choice of using

either absorption costing or variable costing in determining profits and profit reporting.

Before we look at a comparison of both methods, we must firstly understand the meaning

and importance of fixed overhead expenses and this leads us to an understanding of how

absorption costing and variable costing differs and compares. By most definitions fixed

overhead expenses are things that don’t change regardless of production levels. Fixed

overhead expenses examples include such items as: rent, insurance, full time employee

salaries and/or equipment leasing charges. Note: in other words, these expenses continue

regardless of the volumes of sales or production output (Noreen, et al., 2016).

The method of absorption costing involves only allocating the fixed costs across all the

units produced over an accounting period, this type of costing is also known as full

costing and it involves treating the costs of all manufacturing components such as direct

material, direct labor, variable overhead and fixed overhead in the product costs as per

the generally accepted accounting principles (GAAP) (Lalli, 2011).

This method of costing allocates the fixed overhead costs across all the units

manufactured and thus helps in determining of per-unit cost, it generally results in

identifying the two categories of fixed overhead costs, that includes cost of goods sold

and inventory costs (Lalli, 2011).

The major importance of using absorption costing method:

It enables the companies to develop a suitable pricing policy that includes fixed

and variable manufacturing costs (Lalli, 2011).

It ensures that prices are determines on the basis of all the cost incurred in the

production process (Lalli, 2011).

It avoids the separation of costs into fixed and variable that cannot be done in an

easy and accurate manner (Lalli, 2011).

3. Explain how each method differs from the other method and also explain the

importance of each methods.

To better understand Absorption and Variable Costing, its first important to know what is

meant by Managerial Accounting. Sometimes called Management Accounting, it’s also

known as Cost Accounting but regardless of the title used, it’s a process of analyzing

business costs and operations in order to prepare internal financial reports that are used to

aid management decision making processes in achieving the business strategic and other

goals. The word internal is important, as these reports are typically not seen or used by

others outside the company (Noreen, et al., 2016).

However, it’s worthwhile noting early, that under Generally Accepted Accounting

Principles (GAAP), only Absorption Costing is allowed for any company external

financial statement reporting. However, within the business there is a choice of using

either absorption costing or variable costing in determining profits and profit reporting.

Before we look at a comparison of both methods, we must firstly understand the meaning

and importance of fixed overhead expenses and this leads us to an understanding of how

absorption costing and variable costing differs and compares. By most definitions fixed

overhead expenses are things that don’t change regardless of production levels. Fixed

overhead expenses examples include such items as: rent, insurance, full time employee

salaries and/or equipment leasing charges. Note: in other words, these expenses continue

regardless of the volumes of sales or production output (Noreen, et al., 2016).

The method of absorption costing involves only allocating the fixed costs across all the

units produced over an accounting period, this type of costing is also known as full

costing and it involves treating the costs of all manufacturing components such as direct

material, direct labor, variable overhead and fixed overhead in the product costs as per

the generally accepted accounting principles (GAAP) (Lalli, 2011).

This method of costing allocates the fixed overhead costs across all the units

manufactured and thus helps in determining of per-unit cost, it generally results in

identifying the two categories of fixed overhead costs, that includes cost of goods sold

and inventory costs (Lalli, 2011).

The major importance of using absorption costing method:

It enables the companies to develop a suitable pricing policy that includes fixed

and variable manufacturing costs (Lalli, 2011).

It ensures that prices are determines on the basis of all the cost incurred in the

production process (Lalli, 2011).

It avoids the separation of costs into fixed and variable that cannot be done in an

easy and accurate manner (Lalli, 2011).

6

The method of accounting also helps in determining accurate profitability as all

the sales and marketing expenses are recorded under the same period. However,

the major drawback associated with this method is that some of the period costs

does not have any future relevance and thus should not be included within the cost

of product and inventory (Lalli, 2011).

The Absorption Costing method offers the advantage when you have finished

goods in inventory during the reporting period, but which were not sold. Because

each product in inventory has per unit amount assigned for fixed expenses, each

item in inventory stock has a value assigned that also includes a part of the fixed

overhead expense. Therefore, until sold, a product is not reported as an expense

until it is actually sold and removed from inventory (Noreen, et al., 2016).

Difference to Absorption Costing, Variable Costing accounts for fixed overheads in a

lump sum, rather than a per unit, expense. Additionally, under this costing method, all

variable costs including production supplies such as raw materials, packaging and

shipping is included. The full cost of fixed overheads for the reporting period is added.

Specifically, these expenses are not added on a per unit as sold basis instead, these

expenses are subtracted from the revenue amount as a lump Sum expense. (Noreen, et al.,

2016)

Variable costing involves including only the variable costs that is incurred in the

production process. This type of costing method involves emphasizing only variable

production costs for costing of products and valuation of inventory. This type pf costing

unlike absorption costing integrates all fixed overhead costs into a single expense and

reports them into a single line item on the balance sheet (Maingi, 2013).

The major benefit of using variable costing as compared to the absorption costing is that:

It enables only in identifying the significant costs that were actually incurred in

developing a product or service (Maingi, 2013).

It helps in developing income statement by the use of contribution margin that

leads in attaining better information in context of cost volume profit analysis

(CVP) analysis. The absorption costing does not help in undertaking a CVP

analysis. However, the major drawbacks associated with the use of this method is

that it does not help in determination of actual process of products for companies

as it does not involve allocation of fixed costs to the production. Also, the use of

this costing method leads in attaining lower net income for a company because all

fixed costs are reported in the same period in which they are incurred (Maingi,

2013).

It can be stated on the basis of analysis of difference between the above two methods of

cost accounting that variable costs accounting seems to be more adequate for decision-

making purposes of the business managers. This is because it helps in providing an

adequate analysis of cost and volume as it adequately helps in determining the variation

in costs that can occur at different levels of production. Thus, largely assist the business

The method of accounting also helps in determining accurate profitability as all

the sales and marketing expenses are recorded under the same period. However,

the major drawback associated with this method is that some of the period costs

does not have any future relevance and thus should not be included within the cost

of product and inventory (Lalli, 2011).

The Absorption Costing method offers the advantage when you have finished

goods in inventory during the reporting period, but which were not sold. Because

each product in inventory has per unit amount assigned for fixed expenses, each

item in inventory stock has a value assigned that also includes a part of the fixed

overhead expense. Therefore, until sold, a product is not reported as an expense

until it is actually sold and removed from inventory (Noreen, et al., 2016).

Difference to Absorption Costing, Variable Costing accounts for fixed overheads in a

lump sum, rather than a per unit, expense. Additionally, under this costing method, all

variable costs including production supplies such as raw materials, packaging and

shipping is included. The full cost of fixed overheads for the reporting period is added.

Specifically, these expenses are not added on a per unit as sold basis instead, these

expenses are subtracted from the revenue amount as a lump Sum expense. (Noreen, et al.,

2016)

Variable costing involves including only the variable costs that is incurred in the

production process. This type of costing method involves emphasizing only variable

production costs for costing of products and valuation of inventory. This type pf costing

unlike absorption costing integrates all fixed overhead costs into a single expense and

reports them into a single line item on the balance sheet (Maingi, 2013).

The major benefit of using variable costing as compared to the absorption costing is that:

It enables only in identifying the significant costs that were actually incurred in

developing a product or service (Maingi, 2013).

It helps in developing income statement by the use of contribution margin that

leads in attaining better information in context of cost volume profit analysis

(CVP) analysis. The absorption costing does not help in undertaking a CVP

analysis. However, the major drawbacks associated with the use of this method is

that it does not help in determination of actual process of products for companies

as it does not involve allocation of fixed costs to the production. Also, the use of

this costing method leads in attaining lower net income for a company because all

fixed costs are reported in the same period in which they are incurred (Maingi,

2013).

It can be stated on the basis of analysis of difference between the above two methods of

cost accounting that variable costs accounting seems to be more adequate for decision-

making purposes of the business managers. This is because it helps in providing an

adequate analysis of cost and volume as it adequately helps in determining the variation

in costs that can occur at different levels of production. Thus, largely assist the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

managers to analyze the operational efficiency and develop future strategies to improve

the operational effectiveness. Also, the method of costing can be regarded as more

suitable for the companies that are involved in manufacturing of different line of product

(Maingi, 2013).

This is because it is largely easy to identify the differences in profits involved in

producing one items to that of another by only analyzing the differences in the variable

costs of production. It is also associated with less chances of causing manipulation in the

financial reporting for the general users as it does not result in inflating a higher net

income that generally results in using the method of absorption costing. On the other

hand, some of the accountant argues that absorption costing takes into account all the cost

of production that includes fixed and variable and therefore helps in providing a better

picture of production cost that can better help the company management in valuating

profitability and determining process. Also, the method of costing is in compliance with

IFRS and GAAP and therefore regarded to be more suitable to be used in financial

reporting as compared with that of variable costing (McWatters and Zimmerman, 2015).

However, the business managers still largely adopt the use of variable costing for

conducting break-even analysis, determining the contribution margin and enhancing the

decision-making in context of improving the operational efficiency. It can be stated on

the basis of analyzing the important characteristics of both the costing method that

variable costing should largely be applied by the business companies that are involved in

manufacturing of diversified product lines. This is because it largely assists in

determining the profits attained from each of the product line in an accurate manner. On

the other hand, the firms that are involved in developing a single product line can adopt

the use of absorption costing as the method help in determining accurate price level on

per unit basis of products manufactured. This is because all costs are absorbed by the

products that are manufactured in the method of absorption costing. However, as per the

accounting’s standards firms are allowed only for adopting the sue of absorption costing

as variable costing seems to contradict the matching principle which states that all related

revenue and expenses should be recognized within the same accounting period. However,

in the method of variable costing does not involve allocation of fixed manufacturing

overhead and thus is not allowed for external reporting purpose. As such, it is largely

used by the business managers for decision-making purposes related to improving the

operational effectiveness (Moles and Kidwekk, 2011).

4. Explain three ways through that Swipe 50 Ltd can improve its accounting system.

Management accounting system is an important category of complete accounting system

and improving the process of management accounting system will directly improve the

accounting performance of an entity. The main purpose of management accounting

system is to provide sufficient quantitative and qualitative information on company’s

operational as well as financial performance. Management accounting provides

managers to analyze the operational efficiency and develop future strategies to improve

the operational effectiveness. Also, the method of costing can be regarded as more

suitable for the companies that are involved in manufacturing of different line of product

(Maingi, 2013).

This is because it is largely easy to identify the differences in profits involved in

producing one items to that of another by only analyzing the differences in the variable

costs of production. It is also associated with less chances of causing manipulation in the

financial reporting for the general users as it does not result in inflating a higher net

income that generally results in using the method of absorption costing. On the other

hand, some of the accountant argues that absorption costing takes into account all the cost

of production that includes fixed and variable and therefore helps in providing a better

picture of production cost that can better help the company management in valuating

profitability and determining process. Also, the method of costing is in compliance with

IFRS and GAAP and therefore regarded to be more suitable to be used in financial

reporting as compared with that of variable costing (McWatters and Zimmerman, 2015).

However, the business managers still largely adopt the use of variable costing for

conducting break-even analysis, determining the contribution margin and enhancing the

decision-making in context of improving the operational efficiency. It can be stated on

the basis of analyzing the important characteristics of both the costing method that

variable costing should largely be applied by the business companies that are involved in

manufacturing of diversified product lines. This is because it largely assists in

determining the profits attained from each of the product line in an accurate manner. On

the other hand, the firms that are involved in developing a single product line can adopt

the use of absorption costing as the method help in determining accurate price level on

per unit basis of products manufactured. This is because all costs are absorbed by the

products that are manufactured in the method of absorption costing. However, as per the

accounting’s standards firms are allowed only for adopting the sue of absorption costing

as variable costing seems to contradict the matching principle which states that all related

revenue and expenses should be recognized within the same accounting period. However,

in the method of variable costing does not involve allocation of fixed manufacturing

overhead and thus is not allowed for external reporting purpose. As such, it is largely

used by the business managers for decision-making purposes related to improving the

operational effectiveness (Moles and Kidwekk, 2011).

4. Explain three ways through that Swipe 50 Ltd can improve its accounting system.

Management accounting system is an important category of complete accounting system

and improving the process of management accounting system will directly improve the

accounting performance of an entity. The main purpose of management accounting

system is to provide sufficient quantitative and qualitative information on company’s

operational as well as financial performance. Management accounting provides

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

information to the managers or owners of the company and helps them to make the

economic decisions through use of budgeting technique and apply controls on the

variances noticed from actual result and budgeted results. So, company can use

management accounting as a resource planning tool as it focuses on future and it can also

be used as instrument for controlling resources due to its ability to focus on present. So, it

can be said that way to success and to increase profitability performance of any entity it is

important to build rigorous management accounting system that ensure all the cost

elements are in place and are properly controlled (Rasmussen, 2013).

Managerial Accounting provides valuable production performance data to the business

management; and so, helping them to make vital economic decisions the areas of

forecasting and planning. Managerial Accounting is effectively a control technique used

on any variances from the comparison of the actual results against budgeted results.

Therefore, this makes Managerial Accounting a very effective resource planning tool

when it is used to focus on longer term planning. Additionally, it can be used as an

effective tool for resource control due to its ability to focus on present results. (Warren, et

al., 2019)

So, as a performance measurement method, the use of Managerial Accounting could be

said to be an invaluable tool to try and ensure manufacturing success and profitability,

especially in manufacturing, it’s important to, as early as possible, introduce a rigorous

management accounting system that is used to ensure that all costs and expenses are

properly accounted for and controlled (Patankar, 2019).

In the given case it was clear that Swipes 50 Limited has already implemented the

management accounting system that provide required information to managers for

making important economic decisions. Although not much detail has been provided by

the company about its management accounting system but it is assumed that company

uses simpler form of management accounting system which is not providing detailed

information to improve the profitability performance. Three important ways through

which Swipes 50 Limited can improve its management accounting system is given

below:

A. Implementation of activity-based costing system:

As it is clearly reflected from given information that company manufactures only one

product and all the overhead cost have to be directly applied to that one product but there

might be chance that some of overhead costs are not linked with product and take place

with no reason. So, after implementation of activity-based costing system, cost from each

department will be separated and only those overhead costs are being added to the

product that has any relation with product. It will help to separate value added costs and

non-value-added costs from the total overhead costs. Through the application various

costing techniques non value-added activities can be reduced and it will help to improve

the overall profitability of the company. In addition to this activity-based costing will

provide information that can used to calculate the exact profitability of each of product

information to the managers or owners of the company and helps them to make the

economic decisions through use of budgeting technique and apply controls on the

variances noticed from actual result and budgeted results. So, company can use

management accounting as a resource planning tool as it focuses on future and it can also

be used as instrument for controlling resources due to its ability to focus on present. So, it

can be said that way to success and to increase profitability performance of any entity it is

important to build rigorous management accounting system that ensure all the cost

elements are in place and are properly controlled (Rasmussen, 2013).

Managerial Accounting provides valuable production performance data to the business

management; and so, helping them to make vital economic decisions the areas of

forecasting and planning. Managerial Accounting is effectively a control technique used

on any variances from the comparison of the actual results against budgeted results.

Therefore, this makes Managerial Accounting a very effective resource planning tool

when it is used to focus on longer term planning. Additionally, it can be used as an

effective tool for resource control due to its ability to focus on present results. (Warren, et

al., 2019)

So, as a performance measurement method, the use of Managerial Accounting could be

said to be an invaluable tool to try and ensure manufacturing success and profitability,

especially in manufacturing, it’s important to, as early as possible, introduce a rigorous

management accounting system that is used to ensure that all costs and expenses are

properly accounted for and controlled (Patankar, 2019).

In the given case it was clear that Swipes 50 Limited has already implemented the

management accounting system that provide required information to managers for

making important economic decisions. Although not much detail has been provided by

the company about its management accounting system but it is assumed that company

uses simpler form of management accounting system which is not providing detailed

information to improve the profitability performance. Three important ways through

which Swipes 50 Limited can improve its management accounting system is given

below:

A. Implementation of activity-based costing system:

As it is clearly reflected from given information that company manufactures only one

product and all the overhead cost have to be directly applied to that one product but there

might be chance that some of overhead costs are not linked with product and take place

with no reason. So, after implementation of activity-based costing system, cost from each

department will be separated and only those overhead costs are being added to the

product that has any relation with product. It will help to separate value added costs and

non-value-added costs from the total overhead costs. Through the application various

costing techniques non value-added activities can be reduced and it will help to improve

the overall profitability of the company. In addition to this activity-based costing will

provide information that can used to calculate the exact profitability of each of product

9

manufactured by an organization. So, in case if Swipes 50 Ltd adds one more line of

product it will be easy for the company to distribute the overhead costs on the basis of

usage by each one of product (Scheller-Kreinsen and Geissler, 2009).

Activity based costing is much more reliable and accurate cost allocation method as

compared to absorption costing. Absorption costing takes the full amount of

manufacturing overhead and spread evenly to the production quantities of all products

taken together. So, there may be case that certain products have utilized only some of

overhead costs as compared to other. This issue can be easily resolved through use of

activity-based costing system. Activity based costing help to calculate the accurate

product cost as it makes focus on the cause-and-effect relationship of cost incurred. It

takes into accounts the activities that are taken place within the organization and calculate

per unit cost of overhead through use of suitable cost driver. Cost driver is selected on the

ground that it can be quantified and relate to respective overhead cost. ABC costing

makes use of cost driver to allocate the overhead costs to each product on the basis of

number of driver units absorbed by respective product. Overall, it can be said that ABC

costing is superior as compared to absorption costing method as it makes use of relevant

cost drivers for allocating overhead costs. On the other hand, absorption costing makes

use of only single cost driver to allocate the overall manufacturing overheads (Shim,

Siegel and Shim, 2011).

B. Preparation of budgets and evaluating the actual results with budgeted results:

Management accounting system is not a one-day process and no company can succeed

without proper budgets and future plan. Budgeting is an important part in the process of

planning and control of management accounting system. Management accounting system

requires a base to evaluate the actual results in order to evaluate the performance of each

department and take actions to eliminate the variance. In other words, it can be said that

budget provide a regulatory framework that can be used to develop the plan of action, to

minimize the future uncertainties, to calculate the future costs and revenue and to think to

future events. Budget is an integral part of management accounting system and it is

essential to achieve the goals and objectives of an organization (Tănase, 2013).

Budgeting or Forecasting are integral parts of an effective Managerial Accounting

System and it is essential to achieve the goals and objectives of the business. It can be

used to achieve targeted profits through controlling added and possible wasteful costs

incurred through the budgeted year and focusing on quality. Budgeting ensures that costs

are allocated to those activities that help to achieve the strategic objectives of the business

and can play an important role in building key performance indicators (KPI’s) for

individual staff, managers and departments as a whole (Noreen, et al., 2016)

Budgeting will improve accounting system as it is the most important part of internal

control system and can be used to compare the actual results with budgeted results to

calculate the variance. It will help managers to take further steps to eliminate the

manufactured by an organization. So, in case if Swipes 50 Ltd adds one more line of

product it will be easy for the company to distribute the overhead costs on the basis of

usage by each one of product (Scheller-Kreinsen and Geissler, 2009).

Activity based costing is much more reliable and accurate cost allocation method as

compared to absorption costing. Absorption costing takes the full amount of

manufacturing overhead and spread evenly to the production quantities of all products

taken together. So, there may be case that certain products have utilized only some of

overhead costs as compared to other. This issue can be easily resolved through use of

activity-based costing system. Activity based costing help to calculate the accurate

product cost as it makes focus on the cause-and-effect relationship of cost incurred. It

takes into accounts the activities that are taken place within the organization and calculate

per unit cost of overhead through use of suitable cost driver. Cost driver is selected on the

ground that it can be quantified and relate to respective overhead cost. ABC costing

makes use of cost driver to allocate the overhead costs to each product on the basis of

number of driver units absorbed by respective product. Overall, it can be said that ABC

costing is superior as compared to absorption costing method as it makes use of relevant

cost drivers for allocating overhead costs. On the other hand, absorption costing makes

use of only single cost driver to allocate the overall manufacturing overheads (Shim,

Siegel and Shim, 2011).

B. Preparation of budgets and evaluating the actual results with budgeted results:

Management accounting system is not a one-day process and no company can succeed

without proper budgets and future plan. Budgeting is an important part in the process of

planning and control of management accounting system. Management accounting system

requires a base to evaluate the actual results in order to evaluate the performance of each

department and take actions to eliminate the variance. In other words, it can be said that

budget provide a regulatory framework that can be used to develop the plan of action, to

minimize the future uncertainties, to calculate the future costs and revenue and to think to

future events. Budget is an integral part of management accounting system and it is

essential to achieve the goals and objectives of an organization (Tănase, 2013).

Budgeting or Forecasting are integral parts of an effective Managerial Accounting

System and it is essential to achieve the goals and objectives of the business. It can be

used to achieve targeted profits through controlling added and possible wasteful costs

incurred through the budgeted year and focusing on quality. Budgeting ensures that costs

are allocated to those activities that help to achieve the strategic objectives of the business

and can play an important role in building key performance indicators (KPI’s) for

individual staff, managers and departments as a whole (Noreen, et al., 2016)

Budgeting will improve accounting system as it is the most important part of internal

control system and can be used to compare the actual results with budgeted results to

calculate the variance. It will help managers to take further steps to eliminate the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

unfavorable variances and try to achieve the favorable variances to improve the

profitability performance (Vanderbeck, 2012).

The process of drafting a budget provides an opportunity for each department to provide

their recommendations and contribute towards the business vision but the budget must be

well planned and properly indicate the duties and responsibilities for each staff member.

Finally, budgeting will greatly improve the Managerial Accounting System as it is one of

the most important facets of the businesses internal control system mechanisms and

therefore can be used to compare the actual results with budgeted results to calculate any

variances against actual performance. Effective budgeting / forecasting will provide

enormously helpful feedback to management and so help eliminate or at least minimize

any variance and therefore to help improve the business profitability performance

(Warren, et al., 2019).

C. Use of management accounting techniques to improve accounting system

There are many management accounting techniques that can be implemented to integrate

the management performance with the financial performance of the company.

Management accounting techniques such as variance costing, cost volume profit,

standard costing, and marginal costing and cash flow management will help Swipes 50

Limited to evaluate different aspects of costing information and integrate resultant data

with the financial performance of company. For example, cost volume profit analysis

with provide information on breakeven units and also provide numbers of units required

to be sold to achieve the target profit (Warren, et al., 2019).

5. State why the managing accountant’s job are important in manufacturing

company.

The role of a management accountant is not only important, it is very important, as it

covers the entirety of an organization (Kulkarni, et al., 2018).

The job of the management accountant includes the collection, recording and reporting of

financial data from, perhaps, several business units throughout the organization. The job

also involves the observation and analysis of budgets / forecasts; and then to understand

and recommend their funding. This last section includes an estimation of the cost of raw

materials, labor, production, sales, marketing, sales, advertising and the businesses

internal operational costs.

Additionally, the management accountant needs to coordinate with all relevant business

units in order to make an overall analysis of the company’s functioning capital and

availability of funds and then to report all this information to senior management and the

Board of directors. Thus, the management accountant is the key source of information

required by Directors and CEOs that they then use to make decisions.

unfavorable variances and try to achieve the favorable variances to improve the

profitability performance (Vanderbeck, 2012).

The process of drafting a budget provides an opportunity for each department to provide

their recommendations and contribute towards the business vision but the budget must be

well planned and properly indicate the duties and responsibilities for each staff member.

Finally, budgeting will greatly improve the Managerial Accounting System as it is one of

the most important facets of the businesses internal control system mechanisms and

therefore can be used to compare the actual results with budgeted results to calculate any

variances against actual performance. Effective budgeting / forecasting will provide

enormously helpful feedback to management and so help eliminate or at least minimize

any variance and therefore to help improve the business profitability performance

(Warren, et al., 2019).

C. Use of management accounting techniques to improve accounting system

There are many management accounting techniques that can be implemented to integrate

the management performance with the financial performance of the company.

Management accounting techniques such as variance costing, cost volume profit,

standard costing, and marginal costing and cash flow management will help Swipes 50

Limited to evaluate different aspects of costing information and integrate resultant data

with the financial performance of company. For example, cost volume profit analysis

with provide information on breakeven units and also provide numbers of units required

to be sold to achieve the target profit (Warren, et al., 2019).

5. State why the managing accountant’s job are important in manufacturing

company.

The role of a management accountant is not only important, it is very important, as it

covers the entirety of an organization (Kulkarni, et al., 2018).

The job of the management accountant includes the collection, recording and reporting of

financial data from, perhaps, several business units throughout the organization. The job

also involves the observation and analysis of budgets / forecasts; and then to understand

and recommend their funding. This last section includes an estimation of the cost of raw

materials, labor, production, sales, marketing, sales, advertising and the businesses

internal operational costs.

Additionally, the management accountant needs to coordinate with all relevant business

units in order to make an overall analysis of the company’s functioning capital and

availability of funds and then to report all this information to senior management and the

Board of directors. Thus, the management accountant is the key source of information

required by Directors and CEOs that they then use to make decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Input to the decision-making process by the management accountant is the function of

tracking internal costs on any business process that helps a company make decisions

related to the production, operation and investments. Companies need management

accounting and the management accountant to be able to understand the efficiency of

their budget, the cost of their operations and then allocate funds accordingly in

production, sales and investment (Noreen, et al., 2016).

The role of a management accountant is thus, very crucial for a company’s success.

Their role and responsibilities are so huge that even a single miscalculation or

underestimation of any business plan by a management accountant can put a company’s

future in danger.

The management accountant enforces both internal costing procedures and generally

accepted accounting practices to ensure ongoing compliance.

Timing is an important factor for making all plans for a company’s management. A

management accountant’s functions are time related as they need to make predictions,

budgets and report within a stipulated period so that they can be implemented quickly

without delay at a time of need. Timely forecasting is particularly needed in order to take

into consideration market uncertainties. The budget needs to be according to the available

working capital and exposure to market risks thus a certain amount of accuracy is very

necessary. Before reporting, a management accountant has to ensure accuracy of all

information gathered to help incorrect decision making.

Finally, a management accountant needs to be aware of everything, be it political

situation that could affect market, inflation, other exposures in the market, competition,

cost of labor, raw material, internal operations, coordination among different departments

within a company as well as its interaction with rest of the business world in order that

they can inform company management in advance so that they can take financial

decisions with consideration of available funds and requirements (Kulkarni, et al., 2018).

Input to the decision-making process by the management accountant is the function of

tracking internal costs on any business process that helps a company make decisions

related to the production, operation and investments. Companies need management

accounting and the management accountant to be able to understand the efficiency of

their budget, the cost of their operations and then allocate funds accordingly in

production, sales and investment (Noreen, et al., 2016).

The role of a management accountant is thus, very crucial for a company’s success.

Their role and responsibilities are so huge that even a single miscalculation or

underestimation of any business plan by a management accountant can put a company’s

future in danger.

The management accountant enforces both internal costing procedures and generally

accepted accounting practices to ensure ongoing compliance.

Timing is an important factor for making all plans for a company’s management. A

management accountant’s functions are time related as they need to make predictions,

budgets and report within a stipulated period so that they can be implemented quickly

without delay at a time of need. Timely forecasting is particularly needed in order to take

into consideration market uncertainties. The budget needs to be according to the available

working capital and exposure to market risks thus a certain amount of accuracy is very

necessary. Before reporting, a management accountant has to ensure accuracy of all

information gathered to help incorrect decision making.

Finally, a management accountant needs to be aware of everything, be it political

situation that could affect market, inflation, other exposures in the market, competition,

cost of labor, raw material, internal operations, coordination among different departments

within a company as well as its interaction with rest of the business world in order that

they can inform company management in advance so that they can take financial

decisions with consideration of available funds and requirements (Kulkarni, et al., 2018).

12

Conclusion

Management accounting is most important part of accounting system as it helps to

formulate the budgets, calculate variance and determine products cost. Management

accounting comprises of various costing techniques such as make or buy decisions, target

costing, cost volume profit analysis, activity-based costing, inventory management and

many other that helps to improve the accounting system.

References

1. Noreen, E.W., Brewer, P.C., Garrison, R.H. (2016) Managerial Accounting for

Managers 4thEd.

2. Lalli, W. (2011) Handbook of Budgeting.

3. Maingi, J. (2013) Advantages & Disadvantages of activity-based costing with

reference to economic value addition. Germany: GRIN Verlag.

4. McWatters, C., & Zimmerman, J. (2015) Management Accounting in a Dynamic

Environment.

5. Moles, P. & Kidwekk, D. (2011) Corporate finance.

6. Rasmussen, N. et al. (2013) Process Improvement for Effective Budgeting and

Financial Reporting.

7. Warren, C.S., Jones, J.P., Tayler, W.B. (2019) Financial and Managerial

Accounting 15thEd.Boston.

8. Patankar Dr. B.S. (2019). Managerial Accounting. Pune.

9. Scheller-Kreinsen, D. & Geissler, A. (2009) The ABC of DRGs.

10. Shim, J.K., Siegel, J.G. & Shim, A.L. (2011) Budgeting Basics and Beyond.

11. Tănase, G.L. (2013). An Overall Analysis of Participatory Budgeting: Advantages

and Essential Factors for an Effective Implementation in Economic Entities.

12. Vanderbeck, E. (2012) Principles of Cost Accounting. Cengage Learning.

13. Kulkarni M., Mahajan S. (2018). Management Accounting.

Conclusion

Management accounting is most important part of accounting system as it helps to

formulate the budgets, calculate variance and determine products cost. Management

accounting comprises of various costing techniques such as make or buy decisions, target

costing, cost volume profit analysis, activity-based costing, inventory management and

many other that helps to improve the accounting system.

References

1. Noreen, E.W., Brewer, P.C., Garrison, R.H. (2016) Managerial Accounting for

Managers 4thEd.

2. Lalli, W. (2011) Handbook of Budgeting.

3. Maingi, J. (2013) Advantages & Disadvantages of activity-based costing with

reference to economic value addition. Germany: GRIN Verlag.

4. McWatters, C., & Zimmerman, J. (2015) Management Accounting in a Dynamic

Environment.

5. Moles, P. & Kidwekk, D. (2011) Corporate finance.

6. Rasmussen, N. et al. (2013) Process Improvement for Effective Budgeting and

Financial Reporting.

7. Warren, C.S., Jones, J.P., Tayler, W.B. (2019) Financial and Managerial

Accounting 15thEd.Boston.

8. Patankar Dr. B.S. (2019). Managerial Accounting. Pune.

9. Scheller-Kreinsen, D. & Geissler, A. (2009) The ABC of DRGs.

10. Shim, J.K., Siegel, J.G. & Shim, A.L. (2011) Budgeting Basics and Beyond.

11. Tănase, G.L. (2013). An Overall Analysis of Participatory Budgeting: Advantages

and Essential Factors for an Effective Implementation in Economic Entities.

12. Vanderbeck, E. (2012) Principles of Cost Accounting. Cengage Learning.

13. Kulkarni M., Mahajan S. (2018). Management Accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.