Corporate Financial Accounting Assessment Task 2022

VerifiedAdded on 2022/10/14

|16

|2449

|10

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE FINANCIAL ACCOUNTING

Corporate Financial Accounting

Name of the Student

Name of the University

Author Note

Corporate Financial Accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CORPORATE FINANCIAL ACCOUNTING

Table of Contents

Case Studies.....................................................................................................................................3

Task 1...........................................................................................................................................3

Task 2...........................................................................................................................................3

Task 3...........................................................................................................................................4

Task 4...........................................................................................................................................5

Task 5...........................................................................................................................................6

Task 6...........................................................................................................................................7

Task 7...........................................................................................................................................8

Part 2..............................................................................................................................................10

Answer to question 1..................................................................................................................10

Answer to Question 2.................................................................................................................10

Answer to Question 3.................................................................................................................10

Answer to Question 4.................................................................................................................10

Answer to Question 5.................................................................................................................11

Answer to Question 6.................................................................................................................11

Answer to Question 7.................................................................................................................11

Answer to Question 8.................................................................................................................11

Answer to Question 9.................................................................................................................11

Answer to Question 10...............................................................................................................12

Answer to Question 11...............................................................................................................12

Answer to Question 12...............................................................................................................12

Answer to Question 13...............................................................................................................12

Answer to Question 14...............................................................................................................13

Answer to Question 15...............................................................................................................13

References..................................................................................................................................14

CORPORATE FINANCIAL ACCOUNTING

Table of Contents

Case Studies.....................................................................................................................................3

Task 1...........................................................................................................................................3

Task 2...........................................................................................................................................3

Task 3...........................................................................................................................................4

Task 4...........................................................................................................................................5

Task 5...........................................................................................................................................6

Task 6...........................................................................................................................................7

Task 7...........................................................................................................................................8

Part 2..............................................................................................................................................10

Answer to question 1..................................................................................................................10

Answer to Question 2.................................................................................................................10

Answer to Question 3.................................................................................................................10

Answer to Question 4.................................................................................................................10

Answer to Question 5.................................................................................................................11

Answer to Question 6.................................................................................................................11

Answer to Question 7.................................................................................................................11

Answer to Question 8.................................................................................................................11

Answer to Question 9.................................................................................................................11

Answer to Question 10...............................................................................................................12

Answer to Question 11...............................................................................................................12

Answer to Question 12...............................................................................................................12

Answer to Question 13...............................................................................................................12

Answer to Question 14...............................................................................................................13

Answer to Question 15...............................................................................................................13

References..................................................................................................................................14

2

CORPORATE FINANCIAL ACCOUNTING

Case Studies

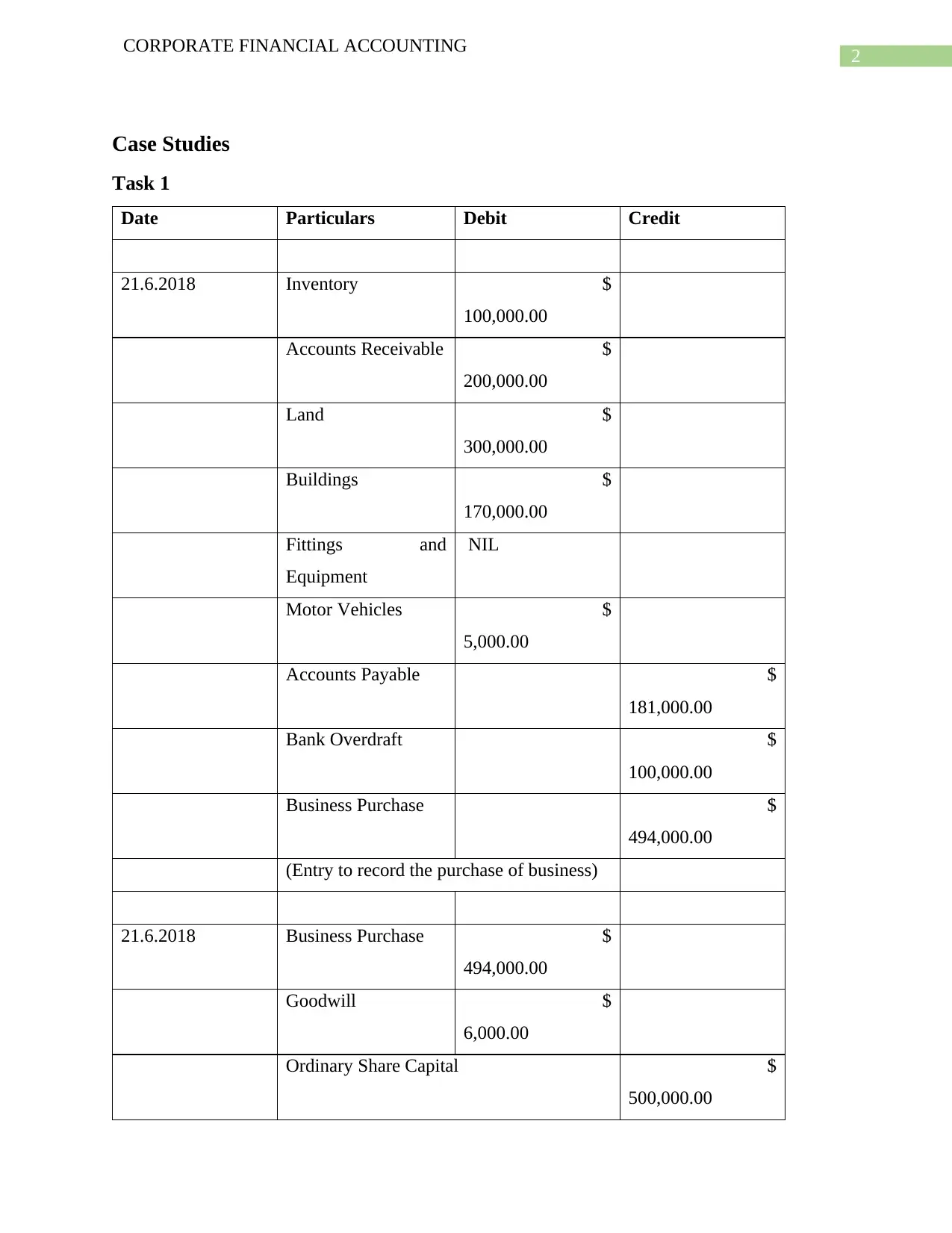

Task 1

Date Particulars Debit Credit

21.6.2018 Inventory $

100,000.00

Accounts Receivable $

200,000.00

Land $

300,000.00

Buildings $

170,000.00

Fittings and

Equipment

NIL

Motor Vehicles $

5,000.00

Accounts Payable $

181,000.00

Bank Overdraft $

100,000.00

Business Purchase $

494,000.00

(Entry to record the purchase of business)

21.6.2018 Business Purchase $

494,000.00

Goodwill $

6,000.00

Ordinary Share Capital $

500,000.00

CORPORATE FINANCIAL ACCOUNTING

Case Studies

Task 1

Date Particulars Debit Credit

21.6.2018 Inventory $

100,000.00

Accounts Receivable $

200,000.00

Land $

300,000.00

Buildings $

170,000.00

Fittings and

Equipment

NIL

Motor Vehicles $

5,000.00

Accounts Payable $

181,000.00

Bank Overdraft $

100,000.00

Business Purchase $

494,000.00

(Entry to record the purchase of business)

21.6.2018 Business Purchase $

494,000.00

Goodwill $

6,000.00

Ordinary Share Capital $

500,000.00

3

CORPORATE FINANCIAL ACCOUNTING

(Entry to settle the purchase consideration)

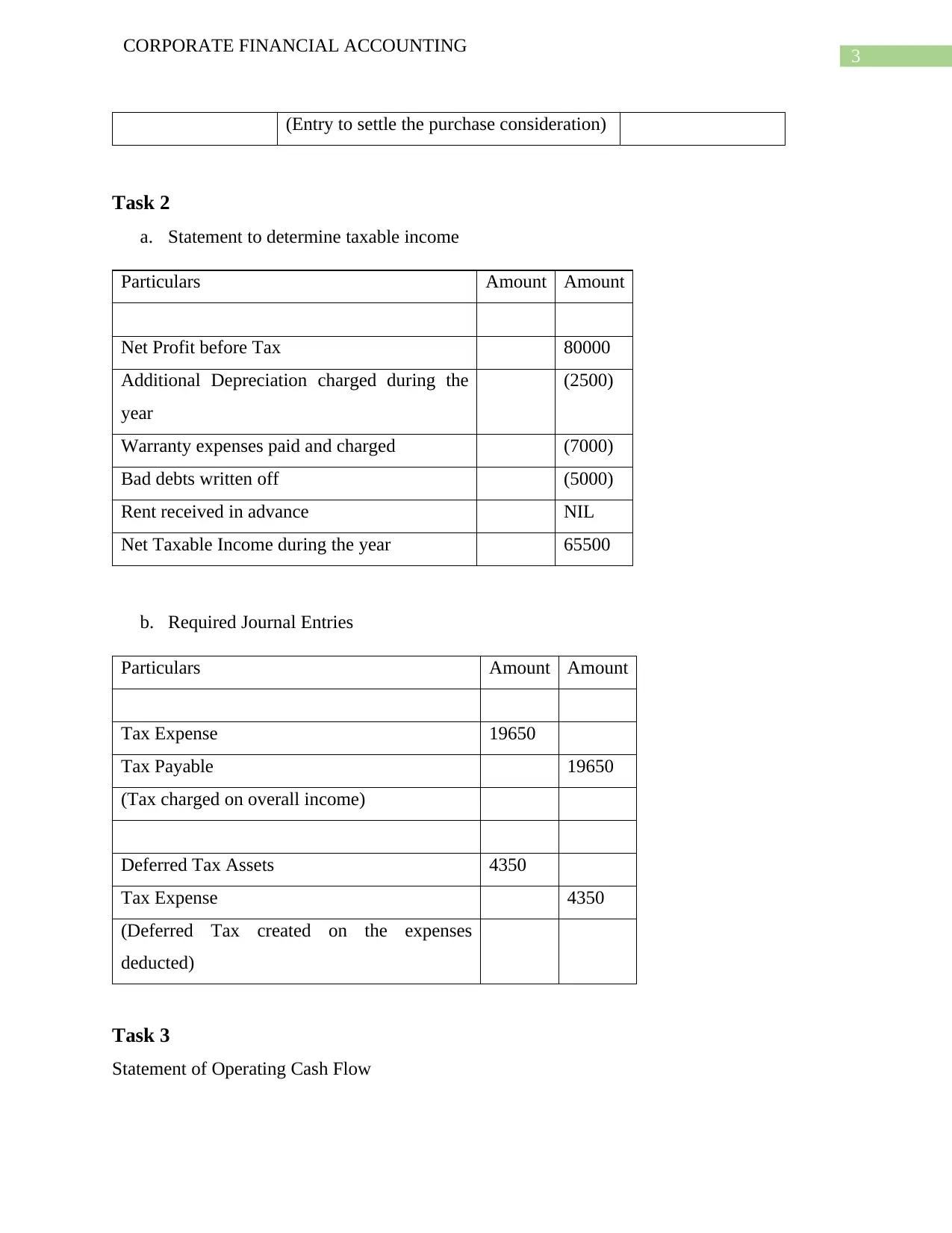

Task 2

a. Statement to determine taxable income

Particulars Amount Amount

Net Profit before Tax 80000

Additional Depreciation charged during the

year

(2500)

Warranty expenses paid and charged (7000)

Bad debts written off (5000)

Rent received in advance NIL

Net Taxable Income during the year 65500

b. Required Journal Entries

Particulars Amount Amount

Tax Expense 19650

Tax Payable 19650

(Tax charged on overall income)

Deferred Tax Assets 4350

Tax Expense 4350

(Deferred Tax created on the expenses

deducted)

Task 3

Statement of Operating Cash Flow

CORPORATE FINANCIAL ACCOUNTING

(Entry to settle the purchase consideration)

Task 2

a. Statement to determine taxable income

Particulars Amount Amount

Net Profit before Tax 80000

Additional Depreciation charged during the

year

(2500)

Warranty expenses paid and charged (7000)

Bad debts written off (5000)

Rent received in advance NIL

Net Taxable Income during the year 65500

b. Required Journal Entries

Particulars Amount Amount

Tax Expense 19650

Tax Payable 19650

(Tax charged on overall income)

Deferred Tax Assets 4350

Tax Expense 4350

(Deferred Tax created on the expenses

deducted)

Task 3

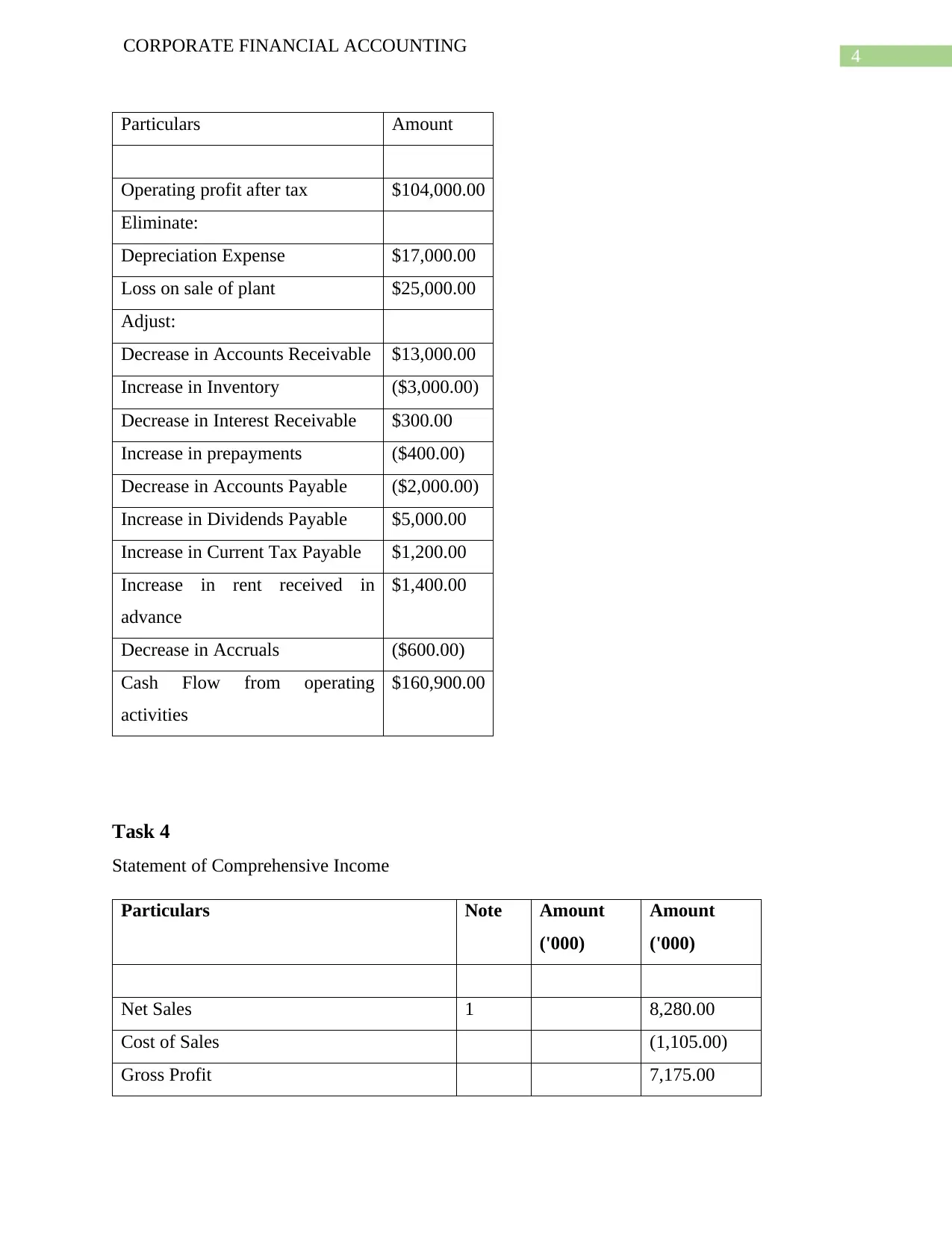

Statement of Operating Cash Flow

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CORPORATE FINANCIAL ACCOUNTING

Particulars Amount

Operating profit after tax $104,000.00

Eliminate:

Depreciation Expense $17,000.00

Loss on sale of plant $25,000.00

Adjust:

Decrease in Accounts Receivable $13,000.00

Increase in Inventory ($3,000.00)

Decrease in Interest Receivable $300.00

Increase in prepayments ($400.00)

Decrease in Accounts Payable ($2,000.00)

Increase in Dividends Payable $5,000.00

Increase in Current Tax Payable $1,200.00

Increase in rent received in

advance

$1,400.00

Decrease in Accruals ($600.00)

Cash Flow from operating

activities

$160,900.00

Task 4

Statement of Comprehensive Income

Particulars Note Amount

('000)

Amount

('000)

Net Sales 1 8,280.00

Cost of Sales (1,105.00)

Gross Profit 7,175.00

CORPORATE FINANCIAL ACCOUNTING

Particulars Amount

Operating profit after tax $104,000.00

Eliminate:

Depreciation Expense $17,000.00

Loss on sale of plant $25,000.00

Adjust:

Decrease in Accounts Receivable $13,000.00

Increase in Inventory ($3,000.00)

Decrease in Interest Receivable $300.00

Increase in prepayments ($400.00)

Decrease in Accounts Payable ($2,000.00)

Increase in Dividends Payable $5,000.00

Increase in Current Tax Payable $1,200.00

Increase in rent received in

advance

$1,400.00

Decrease in Accruals ($600.00)

Cash Flow from operating

activities

$160,900.00

Task 4

Statement of Comprehensive Income

Particulars Note Amount

('000)

Amount

('000)

Net Sales 1 8,280.00

Cost of Sales (1,105.00)

Gross Profit 7,175.00

5

CORPORATE FINANCIAL ACCOUNTING

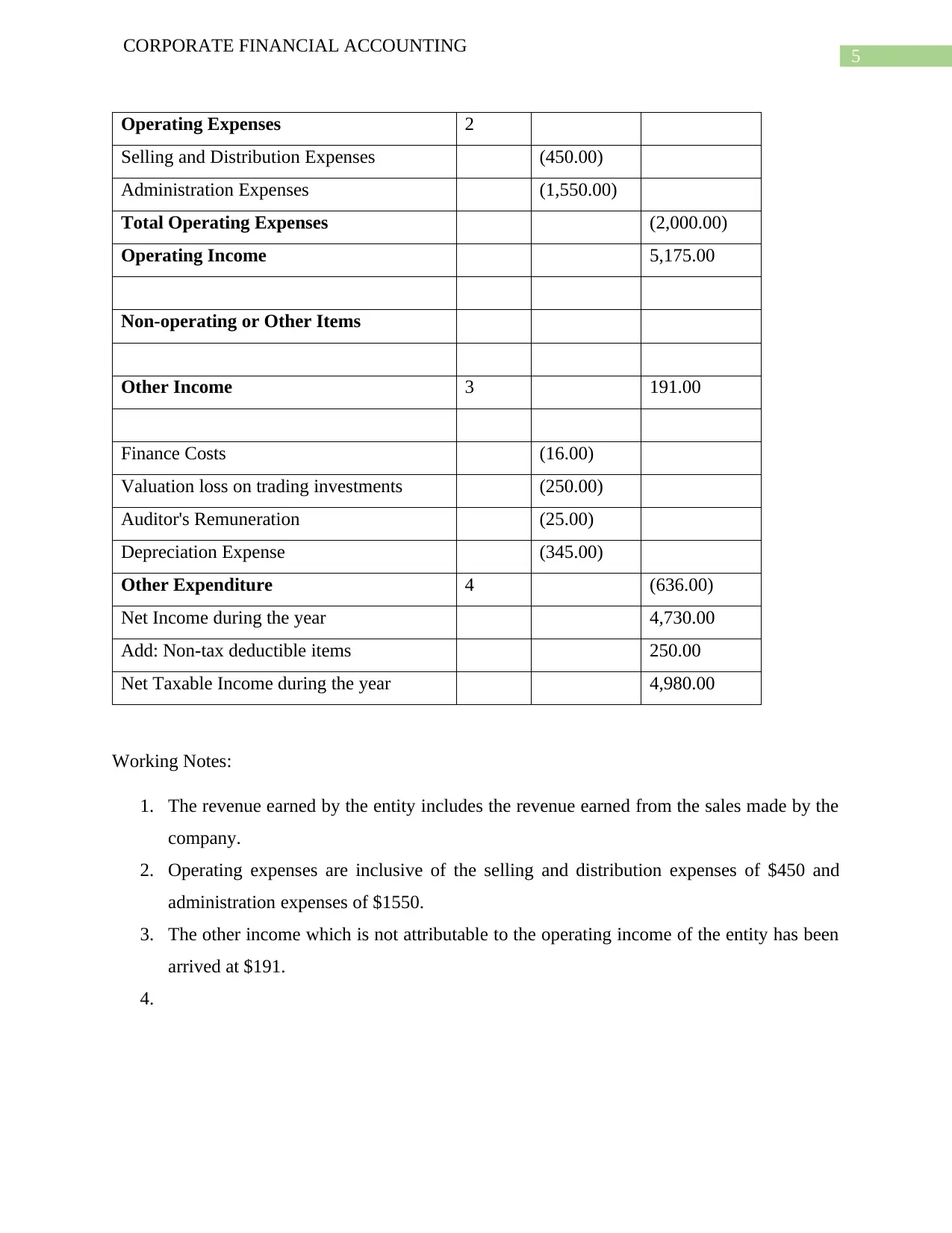

Operating Expenses 2

Selling and Distribution Expenses (450.00)

Administration Expenses (1,550.00)

Total Operating Expenses (2,000.00)

Operating Income 5,175.00

Non-operating or Other Items

Other Income 3 191.00

Finance Costs (16.00)

Valuation loss on trading investments (250.00)

Auditor's Remuneration (25.00)

Depreciation Expense (345.00)

Other Expenditure 4 (636.00)

Net Income during the year 4,730.00

Add: Non-tax deductible items 250.00

Net Taxable Income during the year 4,980.00

Working Notes:

1. The revenue earned by the entity includes the revenue earned from the sales made by the

company.

2. Operating expenses are inclusive of the selling and distribution expenses of $450 and

administration expenses of $1550.

3. The other income which is not attributable to the operating income of the entity has been

arrived at $191.

4.

CORPORATE FINANCIAL ACCOUNTING

Operating Expenses 2

Selling and Distribution Expenses (450.00)

Administration Expenses (1,550.00)

Total Operating Expenses (2,000.00)

Operating Income 5,175.00

Non-operating or Other Items

Other Income 3 191.00

Finance Costs (16.00)

Valuation loss on trading investments (250.00)

Auditor's Remuneration (25.00)

Depreciation Expense (345.00)

Other Expenditure 4 (636.00)

Net Income during the year 4,730.00

Add: Non-tax deductible items 250.00

Net Taxable Income during the year 4,980.00

Working Notes:

1. The revenue earned by the entity includes the revenue earned from the sales made by the

company.

2. Operating expenses are inclusive of the selling and distribution expenses of $450 and

administration expenses of $1550.

3. The other income which is not attributable to the operating income of the entity has been

arrived at $191.

4.

6

CORPORATE FINANCIAL ACCOUNTING

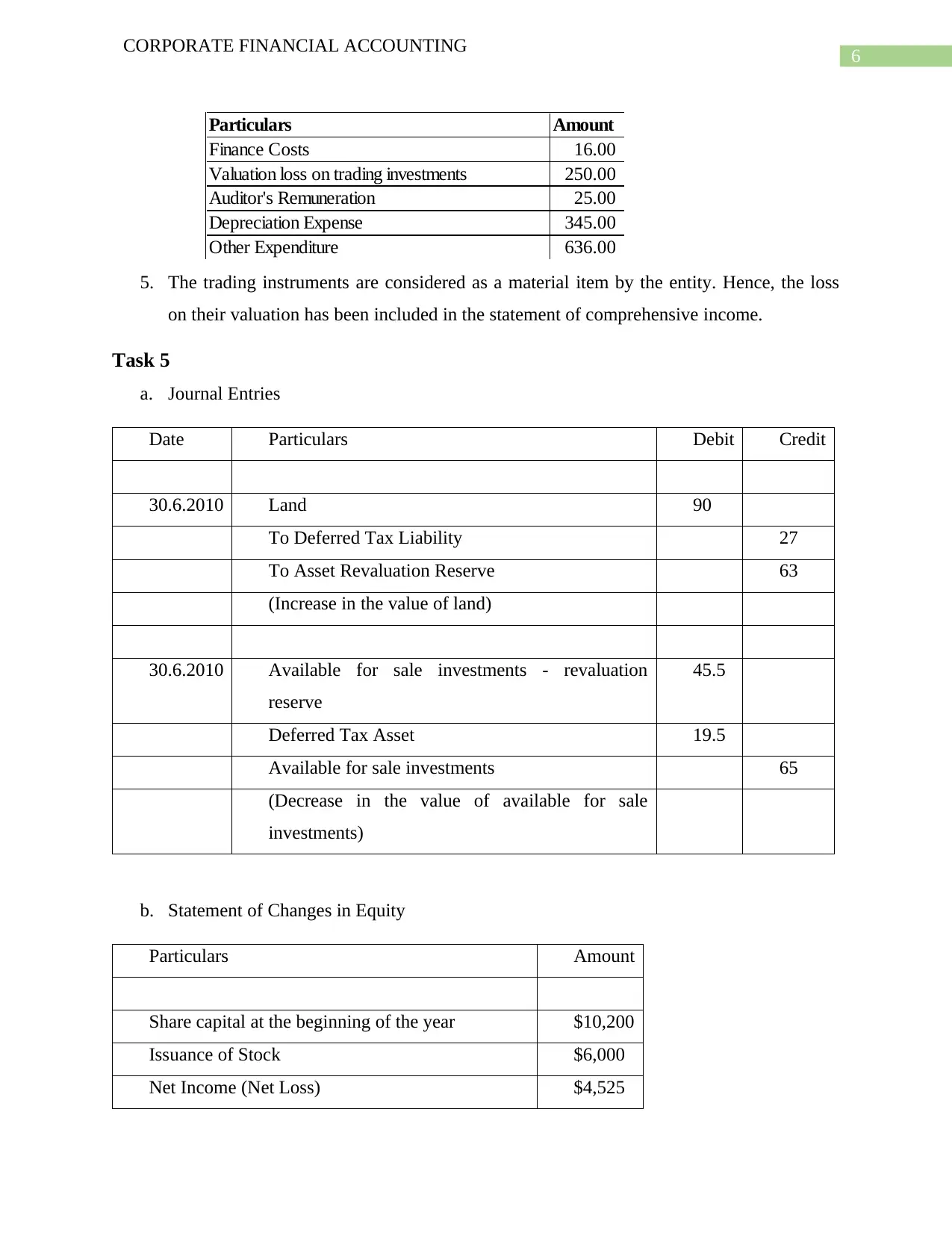

Particulars Amount

Finance Costs 16.00

Valuation loss on trading investments 250.00

Auditor's Remuneration 25.00

Depreciation Expense 345.00

Other Expenditure 636.00

5. The trading instruments are considered as a material item by the entity. Hence, the loss

on their valuation has been included in the statement of comprehensive income.

Task 5

a. Journal Entries

Date Particulars Debit Credit

30.6.2010 Land 90

To Deferred Tax Liability 27

To Asset Revaluation Reserve 63

(Increase in the value of land)

30.6.2010 Available for sale investments - revaluation

reserve

45.5

Deferred Tax Asset 19.5

Available for sale investments 65

(Decrease in the value of available for sale

investments)

b. Statement of Changes in Equity

Particulars Amount

Share capital at the beginning of the year $10,200

Issuance of Stock $6,000

Net Income (Net Loss) $4,525

CORPORATE FINANCIAL ACCOUNTING

Particulars Amount

Finance Costs 16.00

Valuation loss on trading investments 250.00

Auditor's Remuneration 25.00

Depreciation Expense 345.00

Other Expenditure 636.00

5. The trading instruments are considered as a material item by the entity. Hence, the loss

on their valuation has been included in the statement of comprehensive income.

Task 5

a. Journal Entries

Date Particulars Debit Credit

30.6.2010 Land 90

To Deferred Tax Liability 27

To Asset Revaluation Reserve 63

(Increase in the value of land)

30.6.2010 Available for sale investments - revaluation

reserve

45.5

Deferred Tax Asset 19.5

Available for sale investments 65

(Decrease in the value of available for sale

investments)

b. Statement of Changes in Equity

Particulars Amount

Share capital at the beginning of the year $10,200

Issuance of Stock $6,000

Net Income (Net Loss) $4,525

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE FINANCIAL ACCOUNTING

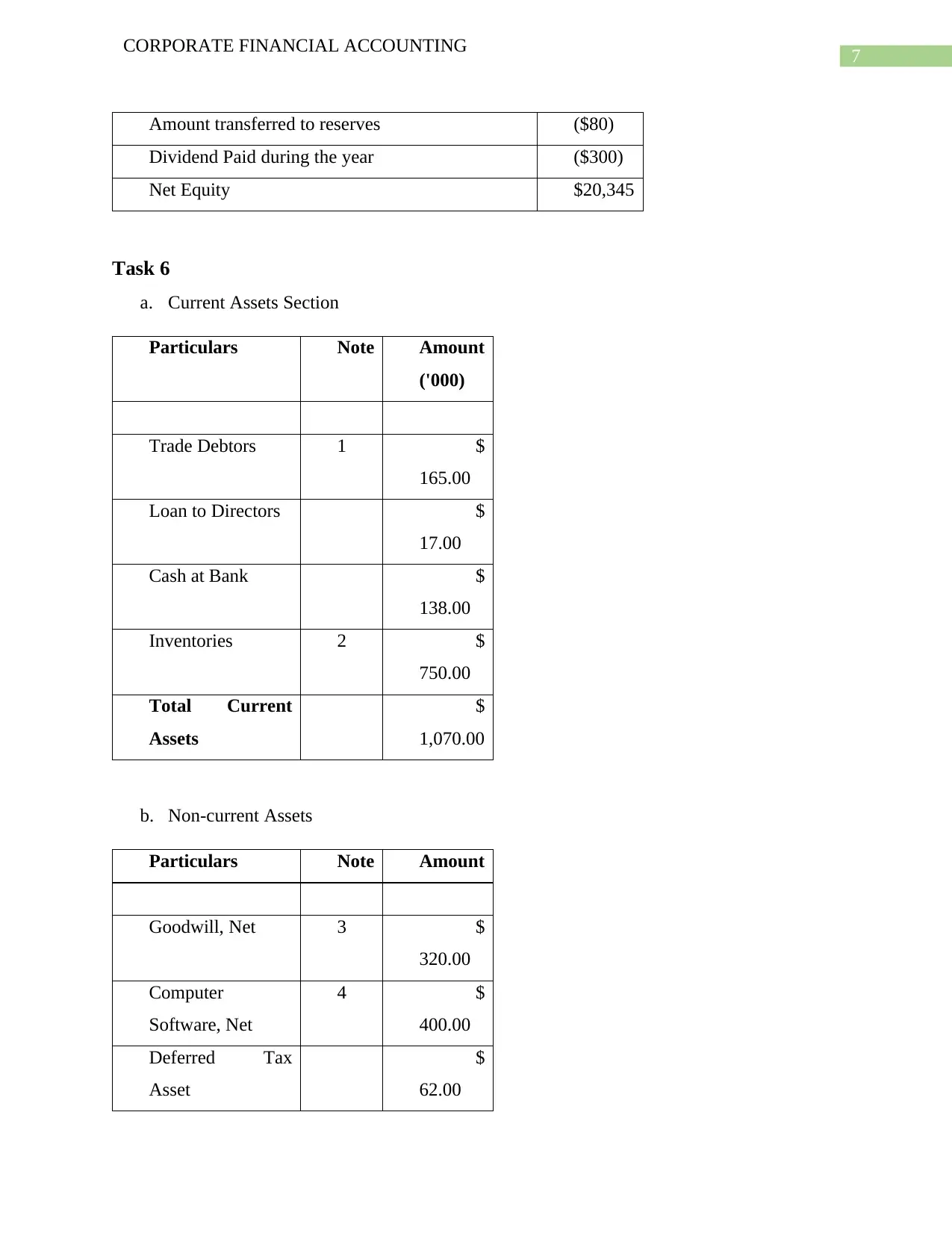

Amount transferred to reserves ($80)

Dividend Paid during the year ($300)

Net Equity $20,345

Task 6

a. Current Assets Section

Particulars Note Amount

('000)

Trade Debtors 1 $

165.00

Loan to Directors $

17.00

Cash at Bank $

138.00

Inventories 2 $

750.00

Total Current

Assets

$

1,070.00

b. Non-current Assets

Particulars Note Amount

Goodwill, Net 3 $

320.00

Computer

Software, Net

4 $

400.00

Deferred Tax

Asset

$

62.00

CORPORATE FINANCIAL ACCOUNTING

Amount transferred to reserves ($80)

Dividend Paid during the year ($300)

Net Equity $20,345

Task 6

a. Current Assets Section

Particulars Note Amount

('000)

Trade Debtors 1 $

165.00

Loan to Directors $

17.00

Cash at Bank $

138.00

Inventories 2 $

750.00

Total Current

Assets

$

1,070.00

b. Non-current Assets

Particulars Note Amount

Goodwill, Net 3 $

320.00

Computer

Software, Net

4 $

400.00

Deferred Tax

Asset

$

62.00

8

CORPORATE FINANCIAL ACCOUNTING

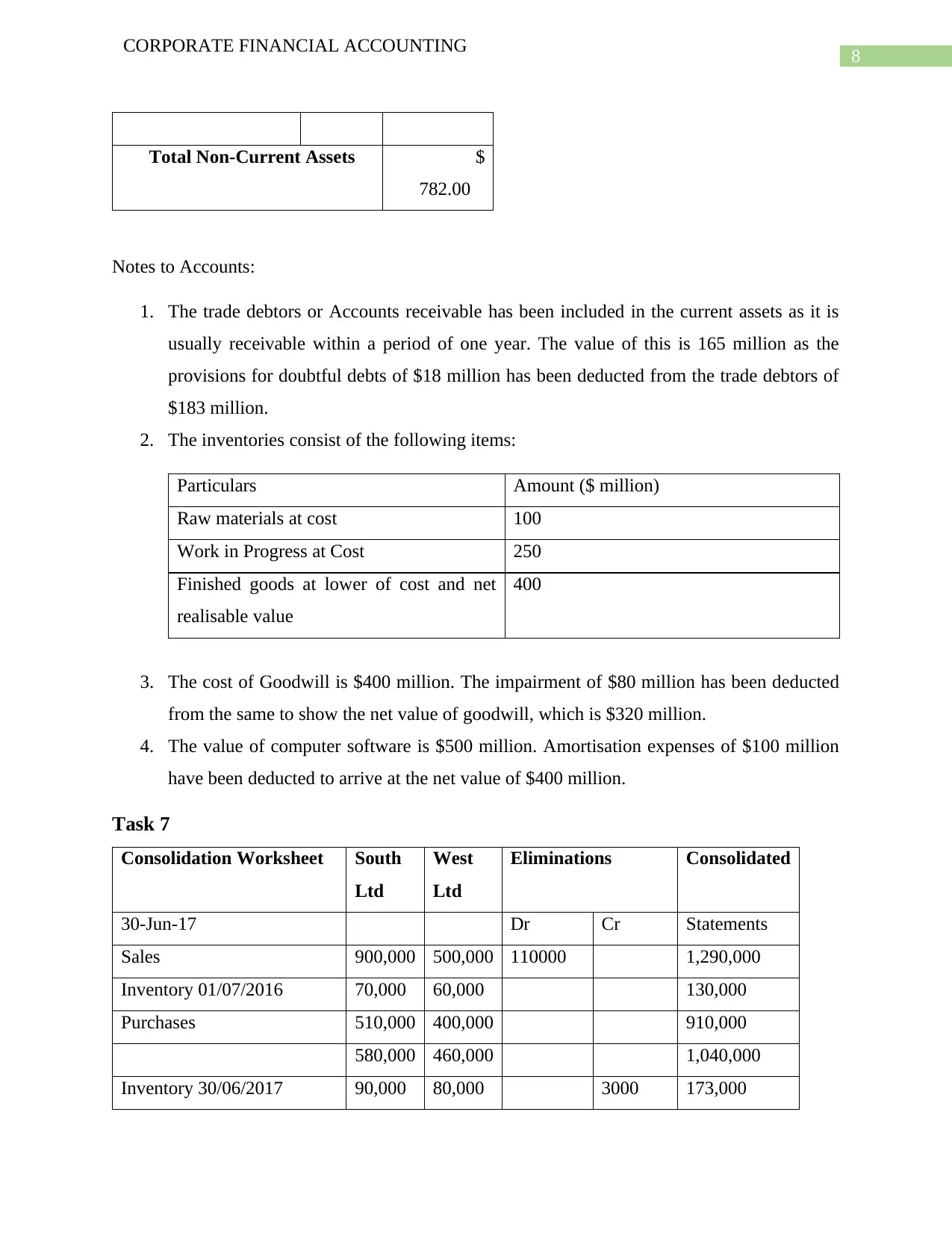

Total Non-Current Assets $

782.00

Notes to Accounts:

1. The trade debtors or Accounts receivable has been included in the current assets as it is

usually receivable within a period of one year. The value of this is 165 million as the

provisions for doubtful debts of $18 million has been deducted from the trade debtors of

$183 million.

2. The inventories consist of the following items:

Particulars Amount ($ million)

Raw materials at cost 100

Work in Progress at Cost 250

Finished goods at lower of cost and net

realisable value

400

3. The cost of Goodwill is $400 million. The impairment of $80 million has been deducted

from the same to show the net value of goodwill, which is $320 million.

4. The value of computer software is $500 million. Amortisation expenses of $100 million

have been deducted to arrive at the net value of $400 million.

Task 7

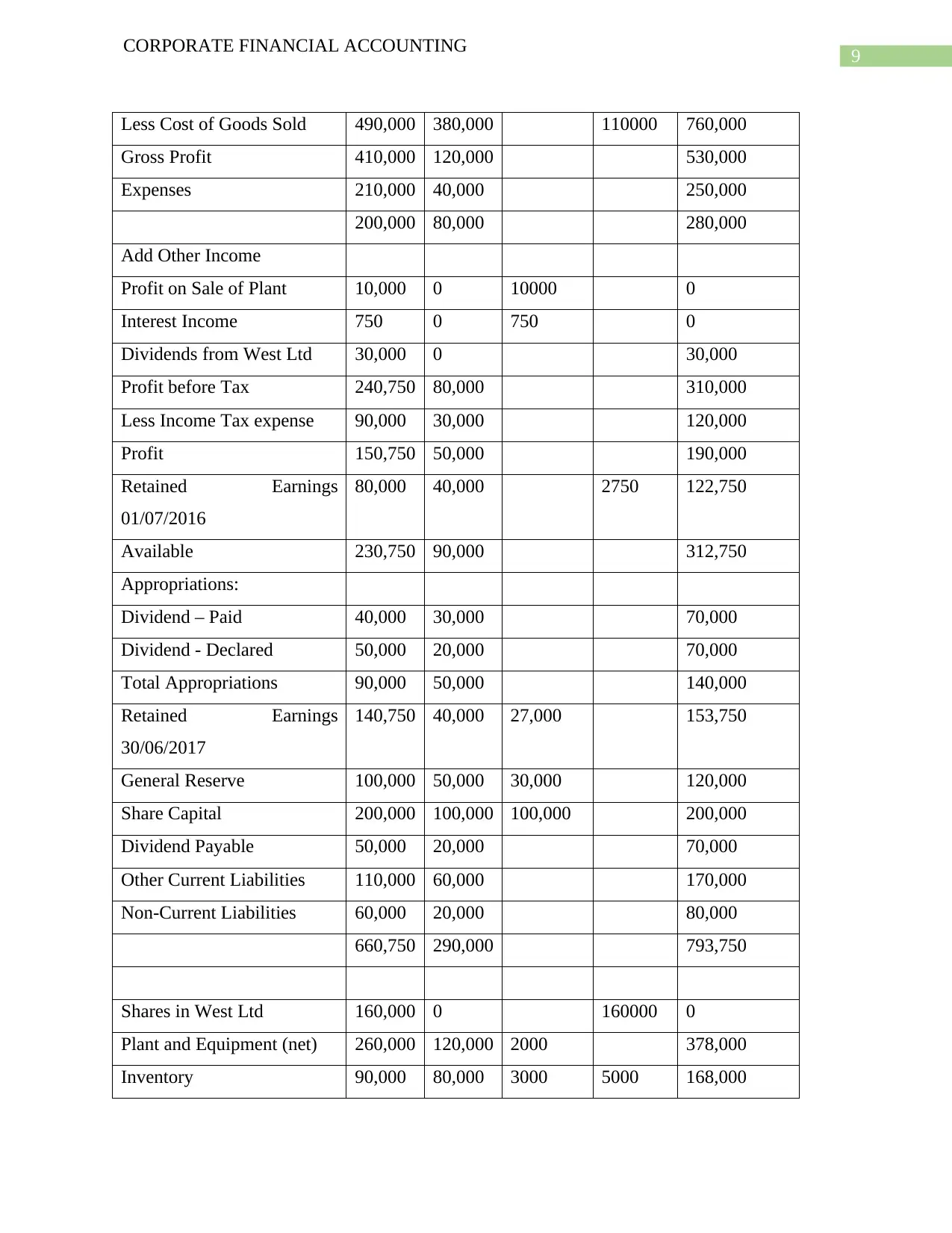

Consolidation Worksheet South

Ltd

West

Ltd

Eliminations Consolidated

30-Jun-17 Dr Cr Statements

Sales 900,000 500,000 110000 1,290,000

Inventory 01/07/2016 70,000 60,000 130,000

Purchases 510,000 400,000 910,000

580,000 460,000 1,040,000

Inventory 30/06/2017 90,000 80,000 3000 173,000

CORPORATE FINANCIAL ACCOUNTING

Total Non-Current Assets $

782.00

Notes to Accounts:

1. The trade debtors or Accounts receivable has been included in the current assets as it is

usually receivable within a period of one year. The value of this is 165 million as the

provisions for doubtful debts of $18 million has been deducted from the trade debtors of

$183 million.

2. The inventories consist of the following items:

Particulars Amount ($ million)

Raw materials at cost 100

Work in Progress at Cost 250

Finished goods at lower of cost and net

realisable value

400

3. The cost of Goodwill is $400 million. The impairment of $80 million has been deducted

from the same to show the net value of goodwill, which is $320 million.

4. The value of computer software is $500 million. Amortisation expenses of $100 million

have been deducted to arrive at the net value of $400 million.

Task 7

Consolidation Worksheet South

Ltd

West

Ltd

Eliminations Consolidated

30-Jun-17 Dr Cr Statements

Sales 900,000 500,000 110000 1,290,000

Inventory 01/07/2016 70,000 60,000 130,000

Purchases 510,000 400,000 910,000

580,000 460,000 1,040,000

Inventory 30/06/2017 90,000 80,000 3000 173,000

9

CORPORATE FINANCIAL ACCOUNTING

Less Cost of Goods Sold 490,000 380,000 110000 760,000

Gross Profit 410,000 120,000 530,000

Expenses 210,000 40,000 250,000

200,000 80,000 280,000

Add Other Income

Profit on Sale of Plant 10,000 0 10000 0

Interest Income 750 0 750 0

Dividends from West Ltd 30,000 0 30,000

Profit before Tax 240,750 80,000 310,000

Less Income Tax expense 90,000 30,000 120,000

Profit 150,750 50,000 190,000

Retained Earnings

01/07/2016

80,000 40,000 2750 122,750

Available 230,750 90,000 312,750

Appropriations:

Dividend – Paid 40,000 30,000 70,000

Dividend - Declared 50,000 20,000 70,000

Total Appropriations 90,000 50,000 140,000

Retained Earnings

30/06/2017

140,750 40,000 27,000 153,750

General Reserve 100,000 50,000 30,000 120,000

Share Capital 200,000 100,000 100,000 200,000

Dividend Payable 50,000 20,000 70,000

Other Current Liabilities 110,000 60,000 170,000

Non-Current Liabilities 60,000 20,000 80,000

660,750 290,000 793,750

Shares in West Ltd 160,000 0 160000 0

Plant and Equipment (net) 260,000 120,000 2000 378,000

Inventory 90,000 80,000 3000 5000 168,000

CORPORATE FINANCIAL ACCOUNTING

Less Cost of Goods Sold 490,000 380,000 110000 760,000

Gross Profit 410,000 120,000 530,000

Expenses 210,000 40,000 250,000

200,000 80,000 280,000

Add Other Income

Profit on Sale of Plant 10,000 0 10000 0

Interest Income 750 0 750 0

Dividends from West Ltd 30,000 0 30,000

Profit before Tax 240,750 80,000 310,000

Less Income Tax expense 90,000 30,000 120,000

Profit 150,750 50,000 190,000

Retained Earnings

01/07/2016

80,000 40,000 2750 122,750

Available 230,750 90,000 312,750

Appropriations:

Dividend – Paid 40,000 30,000 70,000

Dividend - Declared 50,000 20,000 70,000

Total Appropriations 90,000 50,000 140,000

Retained Earnings

30/06/2017

140,750 40,000 27,000 153,750

General Reserve 100,000 50,000 30,000 120,000

Share Capital 200,000 100,000 100,000 200,000

Dividend Payable 50,000 20,000 70,000

Other Current Liabilities 110,000 60,000 170,000

Non-Current Liabilities 60,000 20,000 80,000

660,750 290,000 793,750

Shares in West Ltd 160,000 0 160000 0

Plant and Equipment (net) 260,000 120,000 2000 378,000

Inventory 90,000 80,000 3000 5000 168,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CORPORATE FINANCIAL ACCOUNTING

Other Assets 150,750 90,000 240,750

Goodwill on Consolidation 0 10000 10000

Accum Impairment –

Goodwill

-3000

660,750 290,000 793,750

Part 2

Answer to question 1

The three types of coding systems that can be used by a business to systematically

classify, code and checking the data are source coding, channel coding, cryptographic coding and

line coding. These systems are helpful in compressing the data and making it more useful in

being used as a part of the business (Shkvir and Borshchuk 2018).

Answer to Question 2

Some of the computerized accounting systems that could be used for accounting for data

include ready-to-use software, customised software and tailored software. Some of the prominent

software that are available in the market for businesses include QuickBooks, Sage and

Bookkeeper. These software are essential in breaking down vast amounts of data and using it in

the preparation of the financial statements.

Answer to Question 3

The first step in preparing a consolidated statement is to combine the assets and liabilities

of both the entities. Any prior investment of the parent company in the subsidiary should be

eliminated. The profits or losses of the non-controlling interest should then be separated. Their

share in the assets and liabilities should also be separated. The combined balances form the

consolidated account (Miller Jr and Segall 2017).

CORPORATE FINANCIAL ACCOUNTING

Other Assets 150,750 90,000 240,750

Goodwill on Consolidation 0 10000 10000

Accum Impairment –

Goodwill

-3000

660,750 290,000 793,750

Part 2

Answer to question 1

The three types of coding systems that can be used by a business to systematically

classify, code and checking the data are source coding, channel coding, cryptographic coding and

line coding. These systems are helpful in compressing the data and making it more useful in

being used as a part of the business (Shkvir and Borshchuk 2018).

Answer to Question 2

Some of the computerized accounting systems that could be used for accounting for data

include ready-to-use software, customised software and tailored software. Some of the prominent

software that are available in the market for businesses include QuickBooks, Sage and

Bookkeeper. These software are essential in breaking down vast amounts of data and using it in

the preparation of the financial statements.

Answer to Question 3

The first step in preparing a consolidated statement is to combine the assets and liabilities

of both the entities. Any prior investment of the parent company in the subsidiary should be

eliminated. The profits or losses of the non-controlling interest should then be separated. Their

share in the assets and liabilities should also be separated. The combined balances form the

consolidated account (Miller Jr and Segall 2017).

11

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 4

Fair value measures are used in the valuation of the assets at the time of preparing the

consolidated financial statements. These values are used to reflect the existing market conditions

and the position of the business at the time of undertaking the business. This also helps the parent

company in avoiding the undervaluation and overvaluation of the business at the time of merger

(Palea 2014).

Answer to Question 5

The various effects of taxation that need to be considered are the amount of income tax

related to the comprehensive income after making necessary adjustments to the profits and losses

of the entities. The consolidated entity can either show the net tax effect or show the entire tax

amount and allocate it between the pre-adjustment and post-adjustment comprehensive income.

Answer to Question 6

The types of charts that can be used for a report include a pie chart, horizontal and

vertical bar charts and a histogram. These are useful in simplifying the data and representing the

results visually. The diagrams that can be used in reports include a flowchart diagram, object

diagram and a component diagram. A profile and package diagram are also useful in a report

(Blanchette et al. 2013).

Answer to Question 7

One of the major requirements that needs to be followed at the time of preparing the

financial statements is the rules and regulations prescribed by the Accounting Standards. These

financial statements should also be audited on an annual basis and certified by a qualified

auditor. Sufficient disclosures should also be made suggesting the reliability of the financial

statements.

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 4

Fair value measures are used in the valuation of the assets at the time of preparing the

consolidated financial statements. These values are used to reflect the existing market conditions

and the position of the business at the time of undertaking the business. This also helps the parent

company in avoiding the undervaluation and overvaluation of the business at the time of merger

(Palea 2014).

Answer to Question 5

The various effects of taxation that need to be considered are the amount of income tax

related to the comprehensive income after making necessary adjustments to the profits and losses

of the entities. The consolidated entity can either show the net tax effect or show the entire tax

amount and allocate it between the pre-adjustment and post-adjustment comprehensive income.

Answer to Question 6

The types of charts that can be used for a report include a pie chart, horizontal and

vertical bar charts and a histogram. These are useful in simplifying the data and representing the

results visually. The diagrams that can be used in reports include a flowchart diagram, object

diagram and a component diagram. A profile and package diagram are also useful in a report

(Blanchette et al. 2013).

Answer to Question 7

One of the major requirements that needs to be followed at the time of preparing the

financial statements is the rules and regulations prescribed by the Accounting Standards. These

financial statements should also be audited on an annual basis and certified by a qualified

auditor. Sufficient disclosures should also be made suggesting the reliability of the financial

statements.

12

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 8

Financial statements are the only source of information about the financial performance

and health of an organisation to most of the stakeholders. Hence, they should be consistent with

the information available to the management at the time of their preparation. This also avoids

any unnecessary sanctions and penalties from the statutory authorities in the future (Handley

2013).

Answer to Question 9

The current taxation requirements suggest that every entity should prepare the financial

statements in accordance with the Australian Accounting Standards. The cash flows of the entity

should be presented separately from other parts of financial statements. Other important items

include the interest, income tax paid, dividends received and other expenses paid. The notes to

accounts and various registers should also be appropriately maintained.

Answer to Question 10

In Australia, the entities should identify the taxation and financial reporting requirements

before the preparation of the financial statements. The financial statements are then prepared in

accordance with the requirements. Other acts like the Corporations Act 2001, regulations of

ATO, ASIC, Financial Reporting Council and the AASB should all be followed in preparing the

financial statements of an entity.

Answer to Question 11

In case of a relation between a service provider and an adviser, the adviser is likely to

provide an advice which will benefit the service provider. However, this should be avoided. If

sensitive information like the product design and policies of the entity are not stored properly,

then they can be accessed by outsiders. This should be avoided by the organisation (Fung 2014).

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 8

Financial statements are the only source of information about the financial performance

and health of an organisation to most of the stakeholders. Hence, they should be consistent with

the information available to the management at the time of their preparation. This also avoids

any unnecessary sanctions and penalties from the statutory authorities in the future (Handley

2013).

Answer to Question 9

The current taxation requirements suggest that every entity should prepare the financial

statements in accordance with the Australian Accounting Standards. The cash flows of the entity

should be presented separately from other parts of financial statements. Other important items

include the interest, income tax paid, dividends received and other expenses paid. The notes to

accounts and various registers should also be appropriately maintained.

Answer to Question 10

In Australia, the entities should identify the taxation and financial reporting requirements

before the preparation of the financial statements. The financial statements are then prepared in

accordance with the requirements. Other acts like the Corporations Act 2001, regulations of

ATO, ASIC, Financial Reporting Council and the AASB should all be followed in preparing the

financial statements of an entity.

Answer to Question 11

In case of a relation between a service provider and an adviser, the adviser is likely to

provide an advice which will benefit the service provider. However, this should be avoided. If

sensitive information like the product design and policies of the entity are not stored properly,

then they can be accessed by outsiders. This should be avoided by the organisation (Fung 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 12

The industry-standard methods include the usage of coding to simplify and record

necessary data. The financial statements are prepared using the Accounting Standards suggested

by AASB. Presentation of the financial results and their interpretation is done through different

charts and diagrams to visually represent the data.

Answer to Question 13

A depreciation schedule, also known as the fixed asset register should be maintained by

the entities to record their fixed assets at cost. The depreciation on these assets is then charged

over the lifetime of the asset or until they are sold by the business. The depreciation on the assets

is calculated either by using the straight line method or the written down value method of

depreciation.

Answer to Question 14

The general requirements that should be included in the organisational policies include

the adoption of the Generally Accepted Accounting Standards in the preparation of the financial

statements. The accounting policies should be selected on the basis of the size, business and the

requirements of the entity. The policies should also comply with all the statutory requirements

guiding the corporate entities (Anić-Antić and Konsuo 2015).

Answer to Question 15

The Directors of an entity can delegate their power but not their responsibilities to others.

The financial reports should be prepared on both annual and half-yearly basis. Both should

contain important financial results of the entity. The tax payment timings should be followed on

the basis of the information gathered from the Corporations Law.

CORPORATE FINANCIAL ACCOUNTING

Answer to Question 12

The industry-standard methods include the usage of coding to simplify and record

necessary data. The financial statements are prepared using the Accounting Standards suggested

by AASB. Presentation of the financial results and their interpretation is done through different

charts and diagrams to visually represent the data.

Answer to Question 13

A depreciation schedule, also known as the fixed asset register should be maintained by

the entities to record their fixed assets at cost. The depreciation on these assets is then charged

over the lifetime of the asset or until they are sold by the business. The depreciation on the assets

is calculated either by using the straight line method or the written down value method of

depreciation.

Answer to Question 14

The general requirements that should be included in the organisational policies include

the adoption of the Generally Accepted Accounting Standards in the preparation of the financial

statements. The accounting policies should be selected on the basis of the size, business and the

requirements of the entity. The policies should also comply with all the statutory requirements

guiding the corporate entities (Anić-Antić and Konsuo 2015).

Answer to Question 15

The Directors of an entity can delegate their power but not their responsibilities to others.

The financial reports should be prepared on both annual and half-yearly basis. Both should

contain important financial results of the entity. The tax payment timings should be followed on

the basis of the information gathered from the Corporations Law.

14

CORPORATE FINANCIAL ACCOUNTING

CORPORATE FINANCIAL ACCOUNTING

15

CORPORATE FINANCIAL ACCOUNTING

References

Anić-Antić, P. and Konsuo, D., 2015. THE IMPORTANCE OF CONVERGENCE BETWEEN

US GAAP AND IFRS FOR PUBLICLY LISTED COMPANIES. Ekonomski pregled, 66(4),

pp.358-383.

Blanchette, M., Racicot, F.É., Sedzro, K. and Simonova, E., 2013. IFRS adoption in Canada: An

empirical analysis of the impact on financial statements. Certified General Accountants

Association of Canada, pp.1-68.

Fung, B., 2014. The demand and need for transparency and disclosure in corporate

governance. Universal Journal of Management, 2(2), pp.72-80.

Handley, K., 2013. Accounting standards for Australian SMEs: identifying, considering and

incorporating the needs of users into financial statements. Macquarie University, Faculty of

Business and Economics, Department of Accounting and Corporate Governance.

Miller Jr, E.L. and Segall, L.N., 2017. Mergers and Acquisitions,+ Website: A Step-by-Step

Legal and Practical Guide. John Wiley & Sons.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement users. Journal of

Financial Reporting and Accounting, 12(2), pp.102-116.

Shkvir, V. and Borshchuk, I., 2018, February. Methodology of construction accounting

nomenclature codes of non-automatic informational base of computer accounting system.

In Economics, Entrepreneurship, Management (Vol. 5, No. 2, pp. 51-58). Lviv Politechnic

Publishing House.

CORPORATE FINANCIAL ACCOUNTING

References

Anić-Antić, P. and Konsuo, D., 2015. THE IMPORTANCE OF CONVERGENCE BETWEEN

US GAAP AND IFRS FOR PUBLICLY LISTED COMPANIES. Ekonomski pregled, 66(4),

pp.358-383.

Blanchette, M., Racicot, F.É., Sedzro, K. and Simonova, E., 2013. IFRS adoption in Canada: An

empirical analysis of the impact on financial statements. Certified General Accountants

Association of Canada, pp.1-68.

Fung, B., 2014. The demand and need for transparency and disclosure in corporate

governance. Universal Journal of Management, 2(2), pp.72-80.

Handley, K., 2013. Accounting standards for Australian SMEs: identifying, considering and

incorporating the needs of users into financial statements. Macquarie University, Faculty of

Business and Economics, Department of Accounting and Corporate Governance.

Miller Jr, E.L. and Segall, L.N., 2017. Mergers and Acquisitions,+ Website: A Step-by-Step

Legal and Practical Guide. John Wiley & Sons.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement users. Journal of

Financial Reporting and Accounting, 12(2), pp.102-116.

Shkvir, V. and Borshchuk, I., 2018, February. Methodology of construction accounting

nomenclature codes of non-automatic informational base of computer accounting system.

In Economics, Entrepreneurship, Management (Vol. 5, No. 2, pp. 51-58). Lviv Politechnic

Publishing House.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.