Tax Report Project: Partnership and Corporate Tax Analysis

VerifiedAdded on 2022/08/27

|12

|1372

|38

Report

AI Summary

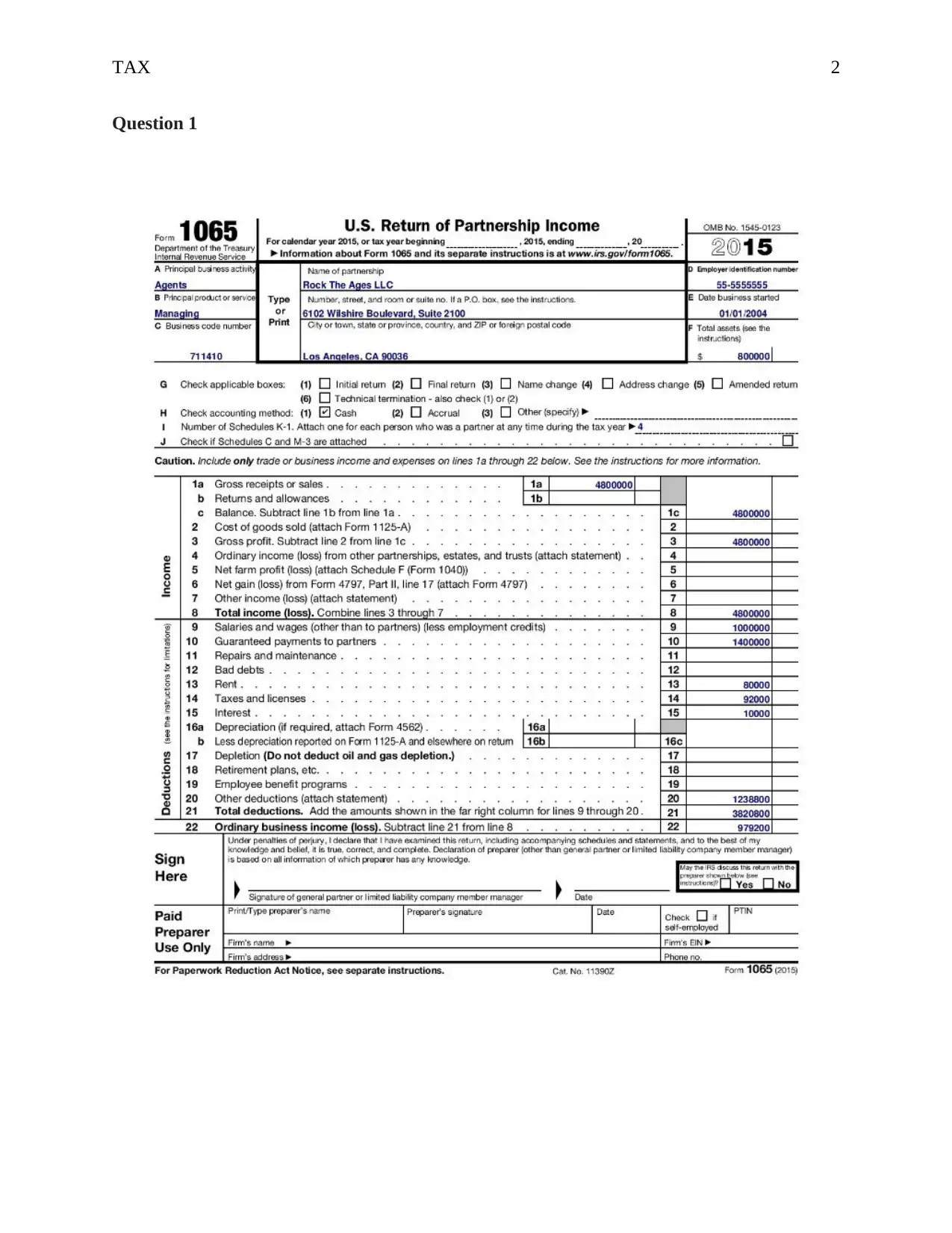

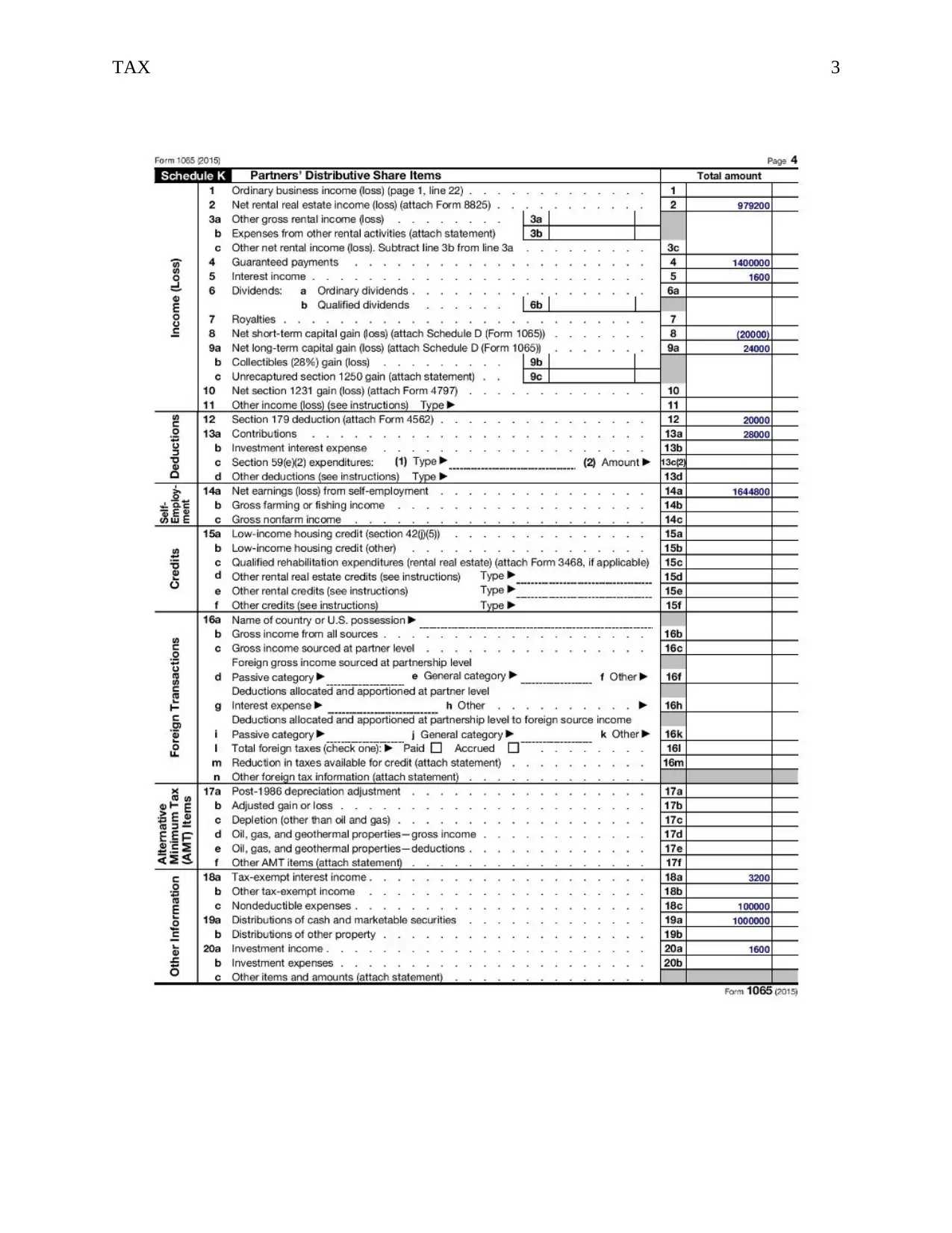

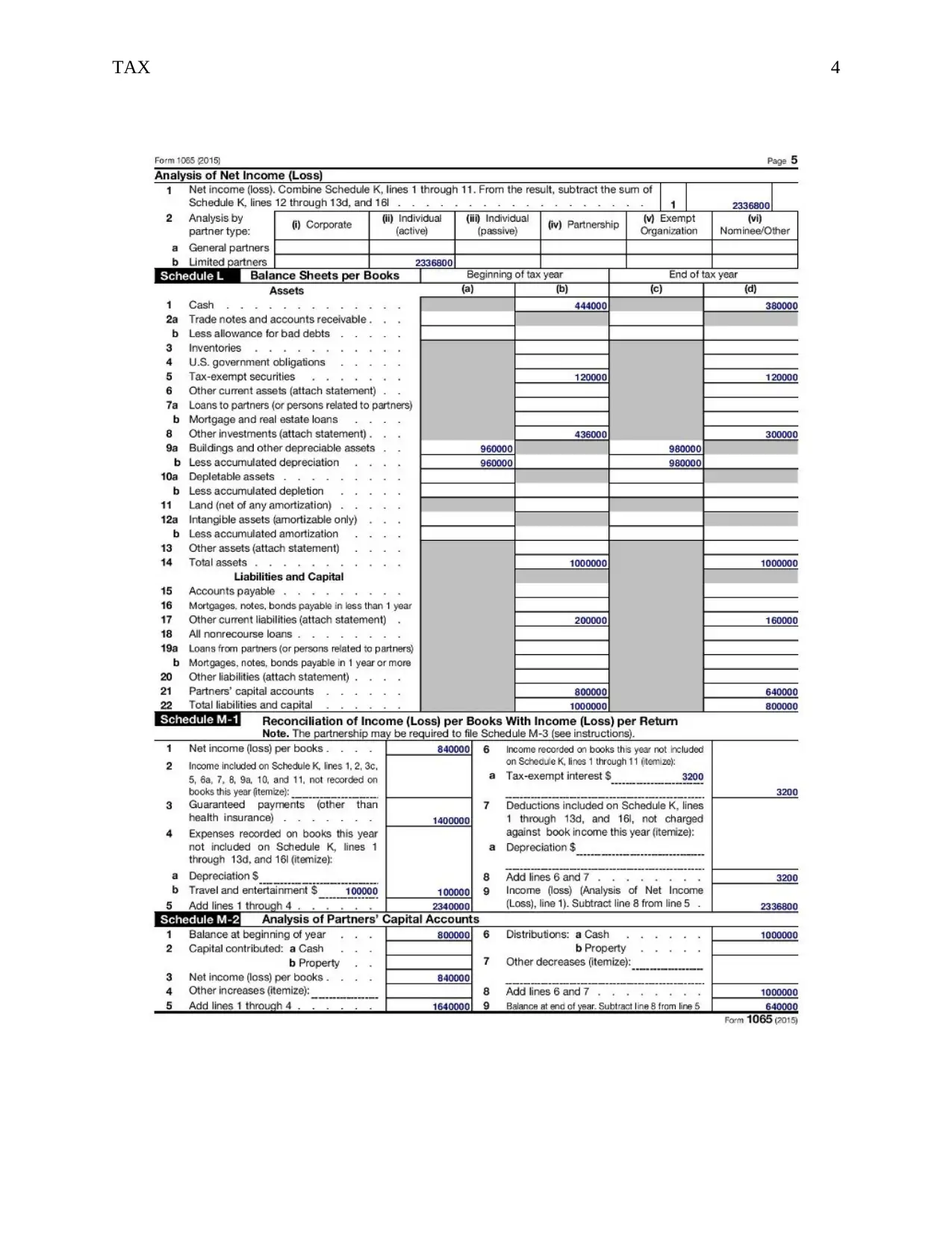

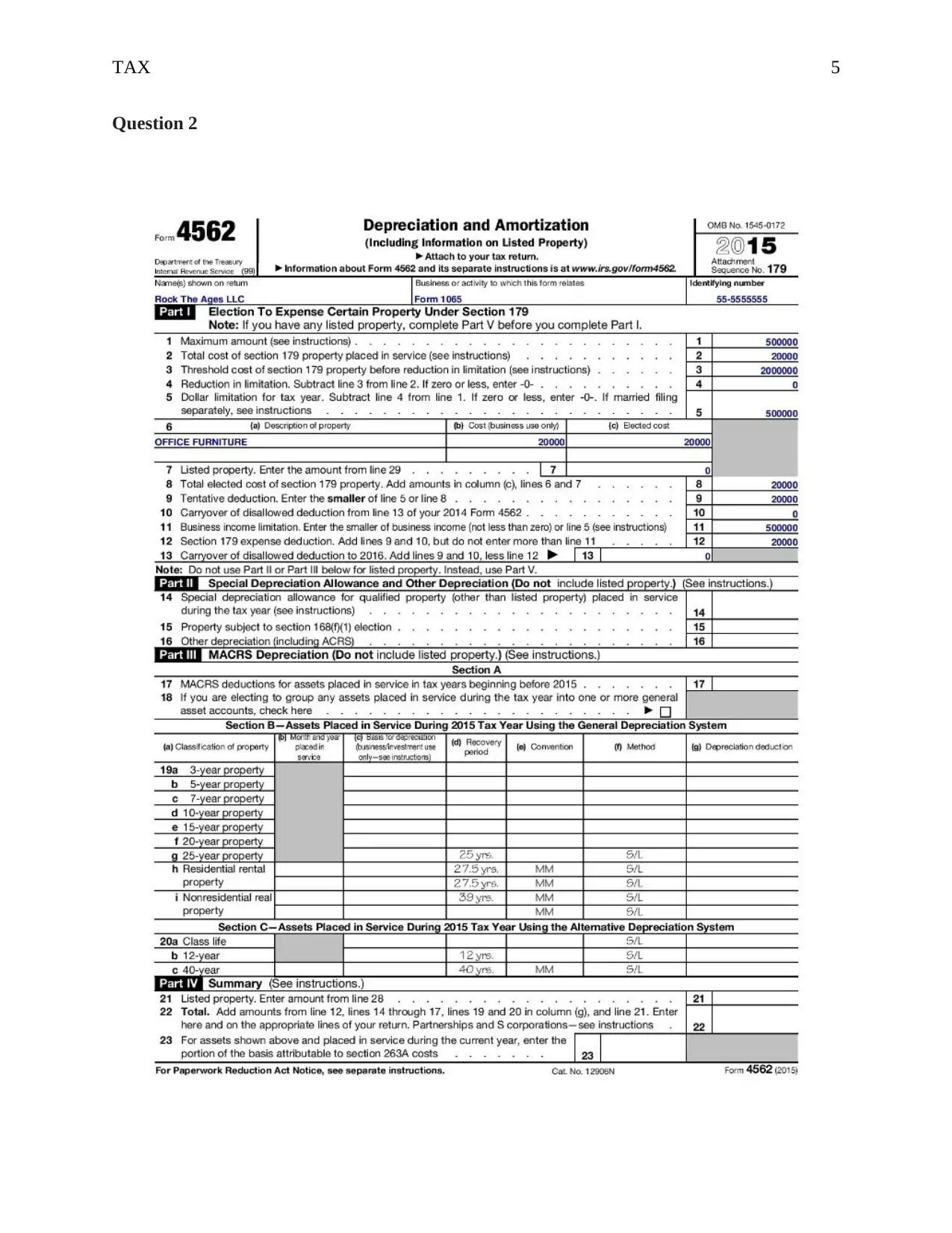

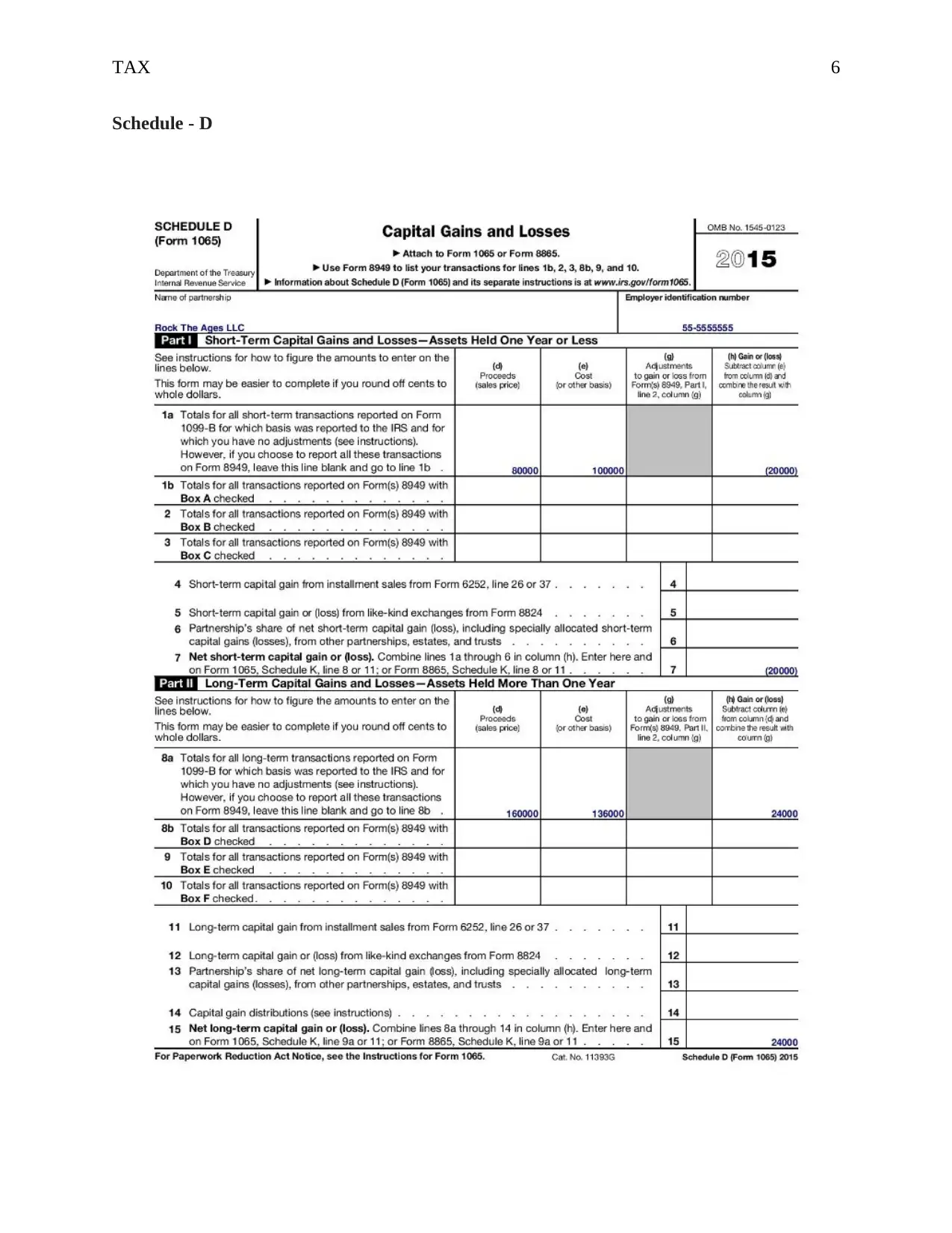

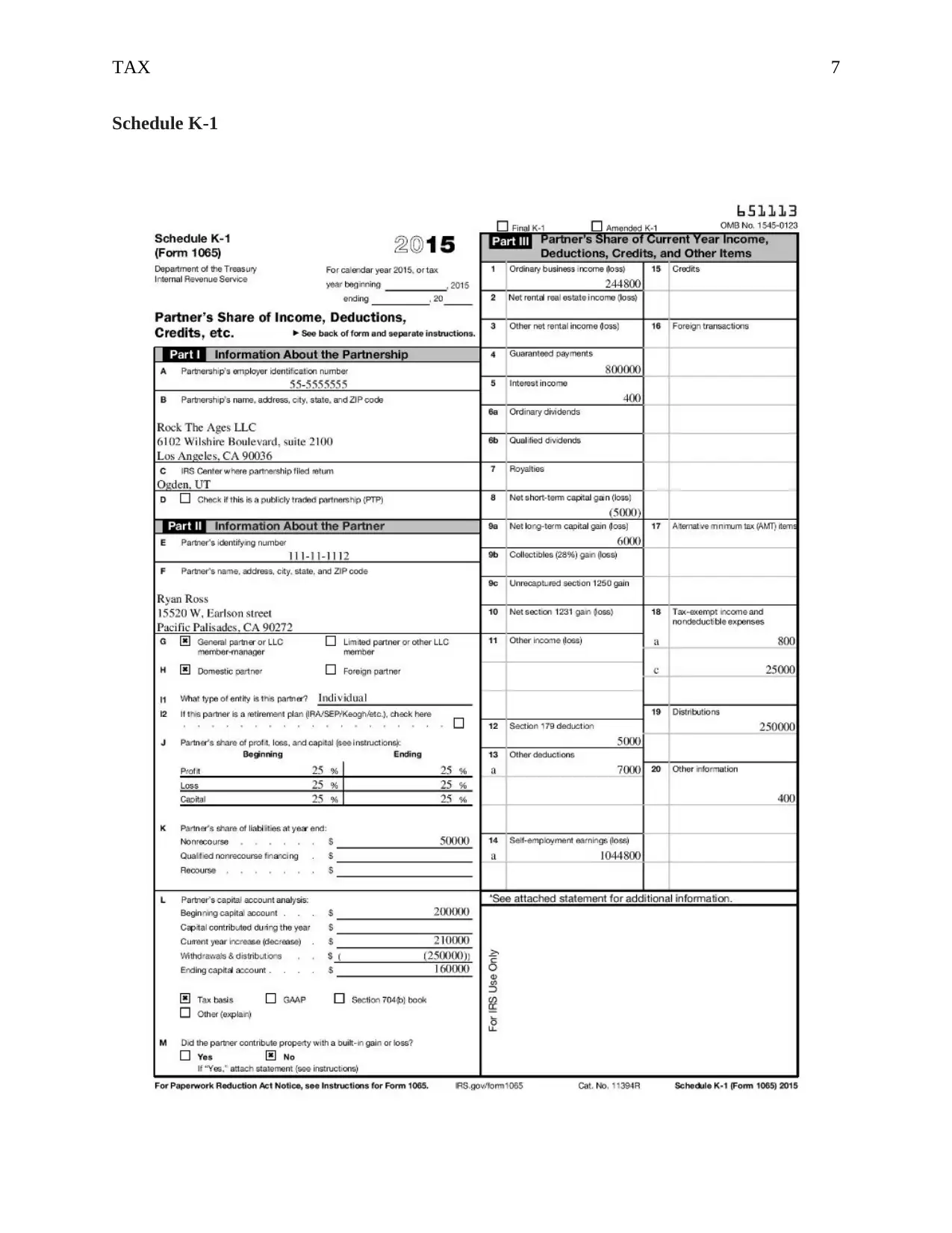

This report analyzes the tax implications for the Rock Ages, LLC, a partnership, and compares it to corporate tax structures. The report includes a letter to a partner, Ryan Ross, explaining the Schedule K-1 and its impact on his individual tax return, detailing the treatment of business income, guaranteed payments, capital losses, and other relevant items. It emphasizes the need for professional tax assistance and the importance of timely filing. The report then contrasts partnership and corporate tax returns, highlighting differences in taxation, liability, profit allocation, and dividend payments. It explains the 'pass-through' taxation mechanism for LLCs and its similarities to corporate structures. Finally, the report offers recommendations for Rock Ages, LLC, including adhering to tax deadlines, minimizing capital losses, and properly utilizing the tax pass-through mechanism. The report covers the use of Form 1065, Schedule K-1 and Form 1120.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.