Tax Effects and Journal Entries

VerifiedAdded on 2020/05/04

|7

|495

|60

AI Summary

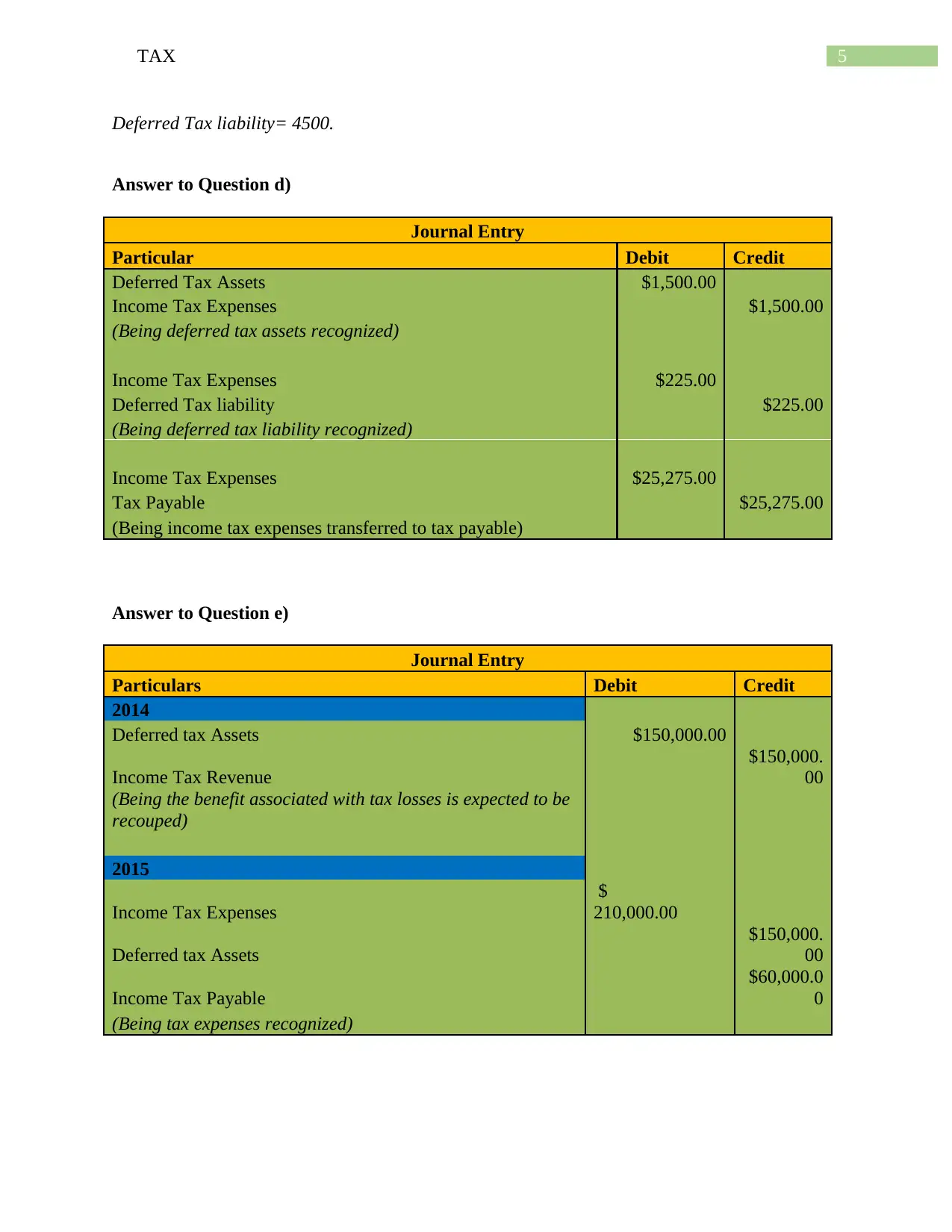

The assignment delves into the complexities of income tax accounting, specifically focusing on the treatment of temporary differences. It requires students to calculate a temporal difference, determine the associated tax expense, and record appropriate journal entries for both deferred tax assets and liabilities. The example provided showcases the impact of these transactions in 2014 and 2015.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.