ACC30005 Taxation Law: VFA Tax Advice - Swinburne University 2018

VerifiedAdded on 2023/06/04

|13

|3865

|383

Case Study

AI Summary

This assignment provides tax advice to VFA for the year ending June 30, 2018, addressing key issues such as income recognition methods (accrual vs. cash basis), the nature of proceeds from land sales (capital vs. revenue), deductibility of solicitor and court fees, tax implications of land sales intended for expansion, treatment of lease incentives (cash and non-cash), deductibility of lease payments for flight simulators, tax deductibility of restrictive covenant payments, assessability of compensation payments, and appropriate taxation treatment of various expenses (bank charges, car expenses, education expenses, entertainment, furniture, marketing costs, telephone, travel expenses) under ITAA 1997 and FBTAA 1986, referencing relevant case laws and tax rulings to provide comprehensive recommendations.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date: October 8, 2018

Dear Ross & Dale

I have reviewed the information that has been provided pertaining to the company. I have

referred to the relevant case laws, legislation and tax rulings in order to provide

recommendation with regards to the various items. The same has been carried out in manner

where the issues are firstly identified, followed by the discussion of the applicable law which

leads to application of the same for generation of advice. These can be found in the

attachment commencing from next page.

Feel free to address any further or follow-up queries that you may have regarding the

recommendations.

Yours Faithfully

STUDENT NAME

Dear Ross & Dale

I have reviewed the information that has been provided pertaining to the company. I have

referred to the relevant case laws, legislation and tax rulings in order to provide

recommendation with regards to the various items. The same has been carried out in manner

where the issues are firstly identified, followed by the discussion of the applicable law which

leads to application of the same for generation of advice. These can be found in the

attachment commencing from next page.

Feel free to address any further or follow-up queries that you may have regarding the

recommendations.

Yours Faithfully

STUDENT NAME

Issue

The key objective in the given case is to extend tax advice with regards to the taxpayer

(VFA) in relation to the year ending June 30, 2018. The critical issues that need to addressed

are as following.

1) The revenues obtained from TCA airways as part of pilot training contract would be

recognised on accrual basis or cash basis.

2) With regards to the proceeds from the sale of land, it needs to be highlighted whether the

same would be capital receipts or revenue receipts.

3) The possible tax deduction of the solicitor and court fees incurred by VFA in relation to

build a large training facility with reference to s. 8-1 ITAA 1997.

4) The tax implications of the sale of land which was intended to expand the operations to

training of commercial pilots and had to be closed later.

5) To ascertain whether the cash incentives for entering the lease can be treated as assessable

income under s. 6-5 or s 6-10. The same needs to also be performed for the rent free use of

the new facility by Chandler Airport Corporation for a period of one year.

6) The tax deductibility of the annual lease payments made with regards to the special flight

simulator procured from Flight Services Ltd in the light of s. 8-1 ITAA 1997 or any other

clause.

7) The tax deductibility of the payment for restrictive covenant to the tune of $ 350,000 for a

period of four years.

8) The assessability of the compensation payment to the tune of $ 750,000 that has been

provided by FlyHigh on account of cancellation of the service agreement which would have

brought in assessable income for VFA over the next four years.

9) The appropriate taxation treatment of the following expenses need to be considered with

reference to Income Tax Assessment Act 1997 (ITAA 1997) and also Fringe Benefit Tax

Assessment Act 1986 (FBTAA 1986).

Bank Charges

Car Expenses

The key objective in the given case is to extend tax advice with regards to the taxpayer

(VFA) in relation to the year ending June 30, 2018. The critical issues that need to addressed

are as following.

1) The revenues obtained from TCA airways as part of pilot training contract would be

recognised on accrual basis or cash basis.

2) With regards to the proceeds from the sale of land, it needs to be highlighted whether the

same would be capital receipts or revenue receipts.

3) The possible tax deduction of the solicitor and court fees incurred by VFA in relation to

build a large training facility with reference to s. 8-1 ITAA 1997.

4) The tax implications of the sale of land which was intended to expand the operations to

training of commercial pilots and had to be closed later.

5) To ascertain whether the cash incentives for entering the lease can be treated as assessable

income under s. 6-5 or s 6-10. The same needs to also be performed for the rent free use of

the new facility by Chandler Airport Corporation for a period of one year.

6) The tax deductibility of the annual lease payments made with regards to the special flight

simulator procured from Flight Services Ltd in the light of s. 8-1 ITAA 1997 or any other

clause.

7) The tax deductibility of the payment for restrictive covenant to the tune of $ 350,000 for a

period of four years.

8) The assessability of the compensation payment to the tune of $ 750,000 that has been

provided by FlyHigh on account of cancellation of the service agreement which would have

brought in assessable income for VFA over the next four years.

9) The appropriate taxation treatment of the following expenses need to be considered with

reference to Income Tax Assessment Act 1997 (ITAA 1997) and also Fringe Benefit Tax

Assessment Act 1986 (FBTAA 1986).

Bank Charges

Car Expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Education Expenses

Entertainment

Furniture

Marketing Costs

Telephone

Travel Expenses

The deductibility of the above expenses and potential liability for the company ought to be

highlighted.

Rule

Ordinary income

The income derived from ordinary income sources are termed as ordinary income and

contributes to assessable income as per s.6-5 ITAA 1997. As per tax ruling TR 92/7,

assessable income would include various income such as employment income, business

income, investment income and income from personal exertion (Reuters, 2017).

Basis for Income Recognition

In accordance with tax ruling TR 98/1, a taxpayer has a choice with regards to choosing an

appropriate means for income recognition in the form of accrual (earnings) basis or cash

(receipts) basis. The taxpayer has the choice but the same should be exhibited in a manner

that presents the most accurate representation of the income. TR 98/1 highlights that the

receipts or cash method is preferable in instances where the income is derived on providing

services or where income is the result of skill possessed by the underlying income. On the

other hand, trading income or income from manufacturing operations is preferred to be

recorded on the earnings method (Barkoczy, 2017).

However, as indicated in Carden v FCT (1938) 63 CLR 108, the decision with regards to

appropriate basis for income recognition should not be based on rigid rule and must be driven

by the underlying circumstances of the business. In this regards, the size of the business plays

a crucial role and typically when the size of a business expands and there is use of other

employees for revenue generation, then the appropriate basis to be deployed is accrual basis

as indicated in the verdict of the Henderson v. Federal Commissioner of Taxation (1970) 119

CLR case (Sadiq et. al., 2015).

Entertainment

Furniture

Marketing Costs

Telephone

Travel Expenses

The deductibility of the above expenses and potential liability for the company ought to be

highlighted.

Rule

Ordinary income

The income derived from ordinary income sources are termed as ordinary income and

contributes to assessable income as per s.6-5 ITAA 1997. As per tax ruling TR 92/7,

assessable income would include various income such as employment income, business

income, investment income and income from personal exertion (Reuters, 2017).

Basis for Income Recognition

In accordance with tax ruling TR 98/1, a taxpayer has a choice with regards to choosing an

appropriate means for income recognition in the form of accrual (earnings) basis or cash

(receipts) basis. The taxpayer has the choice but the same should be exhibited in a manner

that presents the most accurate representation of the income. TR 98/1 highlights that the

receipts or cash method is preferable in instances where the income is derived on providing

services or where income is the result of skill possessed by the underlying income. On the

other hand, trading income or income from manufacturing operations is preferred to be

recorded on the earnings method (Barkoczy, 2017).

However, as indicated in Carden v FCT (1938) 63 CLR 108, the decision with regards to

appropriate basis for income recognition should not be based on rigid rule and must be driven

by the underlying circumstances of the business. In this regards, the size of the business plays

a crucial role and typically when the size of a business expands and there is use of other

employees for revenue generation, then the appropriate basis to be deployed is accrual basis

as indicated in the verdict of the Henderson v. Federal Commissioner of Taxation (1970) 119

CLR case (Sadiq et. al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

General Deduction

General deduction is available for business expenses under s. 8-1 ITAA 1997. As per ss. 8(1)

ITAA 1997, the necessary positive limb for claiming tax deduction for outgoings or losses is

that the underlying outgoing or expenditure must have been incurred with regards to

producing assessable income and there should be sufficient nexus between the outgoing and

the assessable income production (Woellner, 2015). Further, there are three negative limbs in

relation to ss. 8-1(2) that are outlined as follows (Krever, 2017).

The expenditure cannot be capital in nature and has to be revenue. In case of capital

expenditure no deduction can be availed.

The expenditure should be business expenditure and must not domestic expenditure

since no deduction is available for private expenditure.

The expenditure should be done for assessable income and any expenditure incurred

for producing tax exempt income or non-assessable income would not be able to

claim deduction under this section.

Capital or Revenue Nature of Expenses/Outgoings

A key concern with regards to expenditure or outgoing is to determine the underlying nature

of the same which is of special information to s. 8-1 deduction and also other sections which

provide deduction only belonging to revenue nature. A suitable case law for indicating the

difference between the two is Sun Newspapers Ltd and Associated Newspapers Ltd v.

Federal Commissioner of Taxation (1938) 61 CLR 33 case. In this particular case, Dixon J

highlighted a test to differentiate between the two which focused on the advantage produced

from the underlying outgoing (Deutsch et. al., 2015). If the advantage that is procured from

the outgoing has an enduring effect, then the underlying expenditure would be capital in

nature. However, if the advantage would be realised in the current tax year and would not be

long term, then the expenditure would be revenue. A similar stance has also been assumed in

the Carden v FCT (1938) 63 CLR 108 case (Coleman, 2015). For instance, any payment

related to restrictive covenant would be capital expenditure and not revenue expenditure as

the underlying positive effect in terms of lower competition is not limited to the current tax

period but tends to extend in the future and hence the nature of the advantage would be

termed as enduring (Gilders et. al., 2016).

Deduction for capital expenses

General deduction is available for business expenses under s. 8-1 ITAA 1997. As per ss. 8(1)

ITAA 1997, the necessary positive limb for claiming tax deduction for outgoings or losses is

that the underlying outgoing or expenditure must have been incurred with regards to

producing assessable income and there should be sufficient nexus between the outgoing and

the assessable income production (Woellner, 2015). Further, there are three negative limbs in

relation to ss. 8-1(2) that are outlined as follows (Krever, 2017).

The expenditure cannot be capital in nature and has to be revenue. In case of capital

expenditure no deduction can be availed.

The expenditure should be business expenditure and must not domestic expenditure

since no deduction is available for private expenditure.

The expenditure should be done for assessable income and any expenditure incurred

for producing tax exempt income or non-assessable income would not be able to

claim deduction under this section.

Capital or Revenue Nature of Expenses/Outgoings

A key concern with regards to expenditure or outgoing is to determine the underlying nature

of the same which is of special information to s. 8-1 deduction and also other sections which

provide deduction only belonging to revenue nature. A suitable case law for indicating the

difference between the two is Sun Newspapers Ltd and Associated Newspapers Ltd v.

Federal Commissioner of Taxation (1938) 61 CLR 33 case. In this particular case, Dixon J

highlighted a test to differentiate between the two which focused on the advantage produced

from the underlying outgoing (Deutsch et. al., 2015). If the advantage that is procured from

the outgoing has an enduring effect, then the underlying expenditure would be capital in

nature. However, if the advantage would be realised in the current tax year and would not be

long term, then the expenditure would be revenue. A similar stance has also been assumed in

the Carden v FCT (1938) 63 CLR 108 case (Coleman, 2015). For instance, any payment

related to restrictive covenant would be capital expenditure and not revenue expenditure as

the underlying positive effect in terms of lower competition is not limited to the current tax

period but tends to extend in the future and hence the nature of the advantage would be

termed as enduring (Gilders et. al., 2016).

Deduction for capital expenses

With regards to capital expenses, deduction can be availed in accordance with s. 40-880

ITAA 1997 where any business related capital expense can be deducted completely over a

five year period with equal deductions applicable every year (Krever, 2017).

Capital Gains Tax

It is noteworthy that when there is a sale of assets, then the underlying proceeds are capital in

nature and exempted from tax. However, any capital gains that are obtained in the process

would be taxed in accordance with Capital Gains Tax (CGT). The CGT needs to be charged

on the capital gains which are required to be computed once a CGT event takes place as per s.

104-5 ITAA 1997. A prominent CGT event is A1 event which is triggered whenever there is

a disposal of any asset. In accordance with this the capital gains can be computed by

subtracted the asset cost base from the proceeds realised on asset case (Reuters, 2016).

The cost base of the asset is determined in accordance with s. 110-25 ITAA 1997. As per ss.

110-25(1) ITAA 1997, there are five elements which tend to contribute to the asset cost base

as highlighted below (Barkoczy, 2017).

ss. 110-25(2) – The price for which the asset has been purchased.

ss. 110-25(3) – The incidental costs which are related to either the asset purchase or sale and

are necessary.

ss. 110-25(3) – The ownership costs for the asset including the payment of certain taxes along

with the payment of interest on any loan assumed for the asset purchase.

ss. 110-25(4) – The capital costs in regards to the preservation or enhancement of asset value.

ss. 110-25(5) – The capital costs incurred by the taxpayer in relation to the title preservation

of the asset.

The capital gains thus determined considering the cost base and sales proceeds can further be

reduced through the application of discount method or indexation method. The discount

method is outlined in s. 115-25 ITAA 1997 and offers 50% discount on the capital gains

provided these are long term. For long term capital gains, it is imperative that the underlying

asset has been held for a period of more than one year. However, this discount cannot be

availed by companies and restricted only to individuals and small businesses. Hence, the only

alternative remains in the form of indexation method which is applicable only for assets

ITAA 1997 where any business related capital expense can be deducted completely over a

five year period with equal deductions applicable every year (Krever, 2017).

Capital Gains Tax

It is noteworthy that when there is a sale of assets, then the underlying proceeds are capital in

nature and exempted from tax. However, any capital gains that are obtained in the process

would be taxed in accordance with Capital Gains Tax (CGT). The CGT needs to be charged

on the capital gains which are required to be computed once a CGT event takes place as per s.

104-5 ITAA 1997. A prominent CGT event is A1 event which is triggered whenever there is

a disposal of any asset. In accordance with this the capital gains can be computed by

subtracted the asset cost base from the proceeds realised on asset case (Reuters, 2016).

The cost base of the asset is determined in accordance with s. 110-25 ITAA 1997. As per ss.

110-25(1) ITAA 1997, there are five elements which tend to contribute to the asset cost base

as highlighted below (Barkoczy, 2017).

ss. 110-25(2) – The price for which the asset has been purchased.

ss. 110-25(3) – The incidental costs which are related to either the asset purchase or sale and

are necessary.

ss. 110-25(3) – The ownership costs for the asset including the payment of certain taxes along

with the payment of interest on any loan assumed for the asset purchase.

ss. 110-25(4) – The capital costs in regards to the preservation or enhancement of asset value.

ss. 110-25(5) – The capital costs incurred by the taxpayer in relation to the title preservation

of the asset.

The capital gains thus determined considering the cost base and sales proceeds can further be

reduced through the application of discount method or indexation method. The discount

method is outlined in s. 115-25 ITAA 1997 and offers 50% discount on the capital gains

provided these are long term. For long term capital gains, it is imperative that the underlying

asset has been held for a period of more than one year. However, this discount cannot be

availed by companies and restricted only to individuals and small businesses. Hence, the only

alternative remains in the form of indexation method which is applicable only for assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purchased prior to September 1999. Finally, the capital gains remaining after this would be

levied CGT at the rate of 30% (Sadiq et. al., 2015).

Fringe Benefit Tax

Fringe benefits are those benefits that are extended to the employees by the employers and

are provided not in form of cash besides being personal in nature. The legislation for the tax

treatment of these benefits is Fringe Benefit Tax Assessment Act 1986 (FBTAA 1986). The

discussion on the key aspects is indicated below (Gilders et. al., 2016).

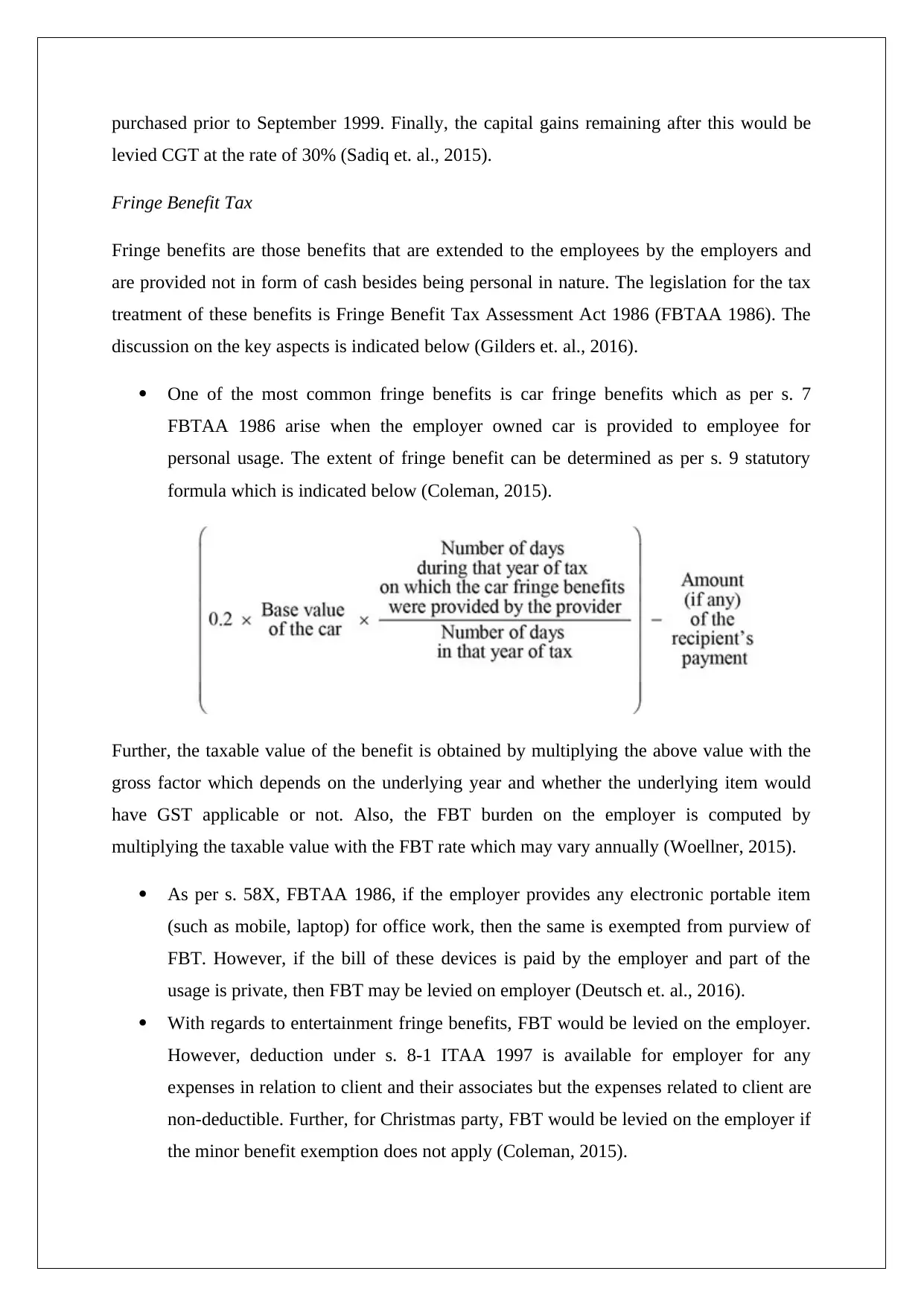

One of the most common fringe benefits is car fringe benefits which as per s. 7

FBTAA 1986 arise when the employer owned car is provided to employee for

personal usage. The extent of fringe benefit can be determined as per s. 9 statutory

formula which is indicated below (Coleman, 2015).

Further, the taxable value of the benefit is obtained by multiplying the above value with the

gross factor which depends on the underlying year and whether the underlying item would

have GST applicable or not. Also, the FBT burden on the employer is computed by

multiplying the taxable value with the FBT rate which may vary annually (Woellner, 2015).

As per s. 58X, FBTAA 1986, if the employer provides any electronic portable item

(such as mobile, laptop) for office work, then the same is exempted from purview of

FBT. However, if the bill of these devices is paid by the employer and part of the

usage is private, then FBT may be levied on employer (Deutsch et. al., 2016).

With regards to entertainment fringe benefits, FBT would be levied on the employer.

However, deduction under s. 8-1 ITAA 1997 is available for employer for any

expenses in relation to client and their associates but the expenses related to client are

non-deductible. Further, for Christmas party, FBT would be levied on the employer if

the minor benefit exemption does not apply (Coleman, 2015).

levied CGT at the rate of 30% (Sadiq et. al., 2015).

Fringe Benefit Tax

Fringe benefits are those benefits that are extended to the employees by the employers and

are provided not in form of cash besides being personal in nature. The legislation for the tax

treatment of these benefits is Fringe Benefit Tax Assessment Act 1986 (FBTAA 1986). The

discussion on the key aspects is indicated below (Gilders et. al., 2016).

One of the most common fringe benefits is car fringe benefits which as per s. 7

FBTAA 1986 arise when the employer owned car is provided to employee for

personal usage. The extent of fringe benefit can be determined as per s. 9 statutory

formula which is indicated below (Coleman, 2015).

Further, the taxable value of the benefit is obtained by multiplying the above value with the

gross factor which depends on the underlying year and whether the underlying item would

have GST applicable or not. Also, the FBT burden on the employer is computed by

multiplying the taxable value with the FBT rate which may vary annually (Woellner, 2015).

As per s. 58X, FBTAA 1986, if the employer provides any electronic portable item

(such as mobile, laptop) for office work, then the same is exempted from purview of

FBT. However, if the bill of these devices is paid by the employer and part of the

usage is private, then FBT may be levied on employer (Deutsch et. al., 2016).

With regards to entertainment fringe benefits, FBT would be levied on the employer.

However, deduction under s. 8-1 ITAA 1997 is available for employer for any

expenses in relation to client and their associates but the expenses related to client are

non-deductible. Further, for Christmas party, FBT would be levied on the employer if

the minor benefit exemption does not apply (Coleman, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Compensation Receipts

In accordance with tax ruling TR 95/35, the compensation receipts would be considered to

have the same nature as the underlying loss that they are replacing. Hence, if the

compensation receipts are provided for revenue receipts, then the income would be assessable

else not (Krever, 2017).

Lease Incentives

The tax implications of cash and non-cash lease incentives are highlighted as per IT 2631. In

accordance with this any cash incentive would be treated as income for the taxpayer. This is

also vindicated from the decision in the F.C. of T. v. Cooling 90 ATC 4472 case where it was

highlighted that these incentives tend to result from the normal business activity of shifting

premises and would be income in character. In relation to the non-cash incentive, if the same

is convertible into cash, then the same would also be included in the assessable income of the

taxpayer (Sadiq et. al., 2015).

Depreciation

The depreciation on various depreciable business assets can be computed using the prime

cost method as indicated in s. 40-75 ITAA 1997. To the extent that the asset is used for

generation of assessable income, deduction would be available to the taxpayer. However, no

deduction for the personal use of asset is permissible (Coleman, 2015).

Application

Ordinary Income

The taxpayer in this case is the company VFA which is providing services to various airlines

in regards to training their pilots and the money received on account of the same would be

considered as ordinary income as per s. 6-5. Thus, the proceeds from TCA Airways contract

would be considered as ordinary income. Considering the size and scale of business, the

relevant basis would be accrual basis, hence the complete cash receipts received in October

of each year would not be recognised. The revenue for each year would be recognised to the

extent that services have been provided to the TCA Airways and remaining revenues would

remain unearned. Further, the debtors to the extent that

Compensation Receipts

In accordance with tax ruling TR 95/35, the compensation receipts would be considered to

have the same nature as the underlying loss that they are replacing. Hence, if the

compensation receipts are provided for revenue receipts, then the income would be assessable

else not (Krever, 2017).

Lease Incentives

The tax implications of cash and non-cash lease incentives are highlighted as per IT 2631. In

accordance with this any cash incentive would be treated as income for the taxpayer. This is

also vindicated from the decision in the F.C. of T. v. Cooling 90 ATC 4472 case where it was

highlighted that these incentives tend to result from the normal business activity of shifting

premises and would be income in character. In relation to the non-cash incentive, if the same

is convertible into cash, then the same would also be included in the assessable income of the

taxpayer (Sadiq et. al., 2015).

Depreciation

The depreciation on various depreciable business assets can be computed using the prime

cost method as indicated in s. 40-75 ITAA 1997. To the extent that the asset is used for

generation of assessable income, deduction would be available to the taxpayer. However, no

deduction for the personal use of asset is permissible (Coleman, 2015).

Application

Ordinary Income

The taxpayer in this case is the company VFA which is providing services to various airlines

in regards to training their pilots and the money received on account of the same would be

considered as ordinary income as per s. 6-5. Thus, the proceeds from TCA Airways contract

would be considered as ordinary income. Considering the size and scale of business, the

relevant basis would be accrual basis, hence the complete cash receipts received in October

of each year would not be recognised. The revenue for each year would be recognised to the

extent that services have been provided to the TCA Airways and remaining revenues would

remain unearned. Further, the debtors to the extent that

Compensation Receipts

The settlement amount to the tune of $ 750,000 obtained during the year from FlyHigh Ltd

would be considered as ordinary income since the settlement amount has been received in

exchange of the loss on the future ordinary income that could have been earned had the

contract not been terminated.

Lease Incentives

The cash lease incentive offered by CAC in relation to shifting the base to their airport would

be considered as ordinary income for VFA considering that this payment has been derived in

the ordinary course of shifting business premises by the company. Additionally, the

assessability of the non-cash benefit would also be considered as the rent free place would

result in cash savings for the company to the extent of $ 100,000 over the given tax year.

Thus, both cash and non-cash incentives would contribute to the ordinary income.

Sale of Land

Land had been acquired by the company for the purpose of expansion but was liquidated later

when the permission for commercial flight testing was not provided. Considering that the

taxpayer is a company, hence discount method is not available. Further, indexation method

cannot be used as the land has been acquired on October 1, 2017.

Purchase cost of land = $ 6 million

Interest paid for holding period of 4 months from October 1, 2017 to January 31, 2018 =

0.9*6 million*(6.8/100)*(123/365) = $ 123,741

Hence, cost base of the land = $ 6,000,000 + $ 123,741 = $ 6,123,741

Selling price of the land = $ 6,850,000

Capital gains that are subject to CGT = (6850000 – 6123741) = $ 726,259

CGT obligation (assumed no previous CGT loss and no other transactions) = 0.3*726259 = $

217,878

However, it is noteworthy that the proceeds of $ 6.85 million from land would not be taxable

since it is capital in nature.

Expenses

would be considered as ordinary income since the settlement amount has been received in

exchange of the loss on the future ordinary income that could have been earned had the

contract not been terminated.

Lease Incentives

The cash lease incentive offered by CAC in relation to shifting the base to their airport would

be considered as ordinary income for VFA considering that this payment has been derived in

the ordinary course of shifting business premises by the company. Additionally, the

assessability of the non-cash benefit would also be considered as the rent free place would

result in cash savings for the company to the extent of $ 100,000 over the given tax year.

Thus, both cash and non-cash incentives would contribute to the ordinary income.

Sale of Land

Land had been acquired by the company for the purpose of expansion but was liquidated later

when the permission for commercial flight testing was not provided. Considering that the

taxpayer is a company, hence discount method is not available. Further, indexation method

cannot be used as the land has been acquired on October 1, 2017.

Purchase cost of land = $ 6 million

Interest paid for holding period of 4 months from October 1, 2017 to January 31, 2018 =

0.9*6 million*(6.8/100)*(123/365) = $ 123,741

Hence, cost base of the land = $ 6,000,000 + $ 123,741 = $ 6,123,741

Selling price of the land = $ 6,850,000

Capital gains that are subject to CGT = (6850000 – 6123741) = $ 726,259

CGT obligation (assumed no previous CGT loss and no other transactions) = 0.3*726259 = $

217,878

However, it is noteworthy that the proceeds of $ 6.85 million from land would not be taxable

since it is capital in nature.

Expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The tax treatment of various expenses is indicated as follows.

Solicitor and Court Fees ($380,000) – The given legal expense is capital in nature

since the benefit derived from the same would have brought incremental income for

the taxpayer over several years and hence the benefit would have been enduring.

100% deduction can be claimed under s. 24-440 ITAA over a five year period.

Lease payment to Flight Services for simulator ($150,000) – Assuming that the given

expense is operating, tax deduction under s. 8-1 ITAA 1997 would be available since

the given equipment is necessary for producing assessable income.

Payment for restrictive covenant ($350,000) – Since the benefits derived for the

business are enduring, hence the given expense would be termed as a capital expense

for the company. Thus, 100% deduction can be claimed under s. 24-440 ITAA over a

five year period.

Bank charges – The card transaction fees would be revenue in nature and hence

deduction under s. 8-1 ITAA 1997 is available as these are required for payments.

Car expenses – Since personal use is allowed on the car, hence FBT liability would be

computed on the company (Taxpayer) as per s. 9 FBTAA 1986. Further, for the

operating expenses, deduction to the extent of 77% can be availed under s. 8-1 ITAA

1997 since it relates to production of assessable income.

Education Expenses – These are requisite expenses for the business since it is

imperative to train the staff and also the instructor. Hence, the nature of the business

expense is revenue owing to which deduction as per s. 8-1 ITAA 1997 is permissible.

Employee Remuneration – These are deductible revenue business costs and thereby

deductible in accordance with s. 8-1 ITAA 1997.

Lunches and Christmas – Depending on the availability of the minimum exemption

rebate, FBT would be levied on the employer in relation to the entertainment and

meal fringe benefits that are extended. However, the amount of spending would be

deductible under s. 8-1 ITAA 1997 as the employees produce assessable income for

taxpayer.

Furniture – The expenditure on furniture would be capital in nature and hence non-

deductible under s. 8-1 ITAA 1997. However, over the useful life depreciation would

be charged on the same and this amount would be available for deduction from

taxable income.

Solicitor and Court Fees ($380,000) – The given legal expense is capital in nature

since the benefit derived from the same would have brought incremental income for

the taxpayer over several years and hence the benefit would have been enduring.

100% deduction can be claimed under s. 24-440 ITAA over a five year period.

Lease payment to Flight Services for simulator ($150,000) – Assuming that the given

expense is operating, tax deduction under s. 8-1 ITAA 1997 would be available since

the given equipment is necessary for producing assessable income.

Payment for restrictive covenant ($350,000) – Since the benefits derived for the

business are enduring, hence the given expense would be termed as a capital expense

for the company. Thus, 100% deduction can be claimed under s. 24-440 ITAA over a

five year period.

Bank charges – The card transaction fees would be revenue in nature and hence

deduction under s. 8-1 ITAA 1997 is available as these are required for payments.

Car expenses – Since personal use is allowed on the car, hence FBT liability would be

computed on the company (Taxpayer) as per s. 9 FBTAA 1986. Further, for the

operating expenses, deduction to the extent of 77% can be availed under s. 8-1 ITAA

1997 since it relates to production of assessable income.

Education Expenses – These are requisite expenses for the business since it is

imperative to train the staff and also the instructor. Hence, the nature of the business

expense is revenue owing to which deduction as per s. 8-1 ITAA 1997 is permissible.

Employee Remuneration – These are deductible revenue business costs and thereby

deductible in accordance with s. 8-1 ITAA 1997.

Lunches and Christmas – Depending on the availability of the minimum exemption

rebate, FBT would be levied on the employer in relation to the entertainment and

meal fringe benefits that are extended. However, the amount of spending would be

deductible under s. 8-1 ITAA 1997 as the employees produce assessable income for

taxpayer.

Furniture – The expenditure on furniture would be capital in nature and hence non-

deductible under s. 8-1 ITAA 1997. However, over the useful life depreciation would

be charged on the same and this amount would be available for deduction from

taxable income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fuel and Airplane Maintenance cost - These are essential costs for the company as

airplane are required for training and fuel would be incurred. For these regular

business expenses, deduction is available under s. 8-1 ITAA 1997.

Marketing and advertising costs are also business expenses that are regularly incurred

for attracting new clients and hence these are revenue expenses with deduction under

s. 8-1 ITAA 1997.

In relation to mobile phone provided to instructors, no FBT would be levied but

depreciation on the same may be claimed over the useful life of the asset.

Solicitor fees with regards to lease for Simulator would be a revenue expense and

hence general deduction would apply for this case.

The amount spent by the company on the travel and stay of Dale Wise would be

deductible under s. 8-1 ITAA 1997 since it is an imperative expenditure related to

training and production of assessable income through upgrading and entering new

business avenues.

Conclusion

On the basis of the above discussion, the following recommendations may be offered.

The ordinary income would be derived on accrual basis from the services offered to

various airlines. Also, the cash and non-cash based lease incentives obtained from

CAC for changing the base would be considered as ordinary income. Additionally, the

compensation receipts from the settlement (i.e. $ 750,000) would be considered as

ordinary income and thereby assessable in the given tax year.

On the sale of land, while the proceeds would not be taxable but on account of capital

gains, CGT liability to the tune of $217,878 would le levied. Further, the interest

charges on loan are adjusted in the land cost base.

Also, the company would have FBT liability arising from extension of lunches,

Christmas party and car fringe benefits.

The solicitor expenses related to settlement case along with payment of restrictive

covenant proceeds would be capital expenditure and hence deduction would be

available over a five year period.

For furniture and mobile phone, depreciation related deduction may be permissible

provided the same is used for business.

airplane are required for training and fuel would be incurred. For these regular

business expenses, deduction is available under s. 8-1 ITAA 1997.

Marketing and advertising costs are also business expenses that are regularly incurred

for attracting new clients and hence these are revenue expenses with deduction under

s. 8-1 ITAA 1997.

In relation to mobile phone provided to instructors, no FBT would be levied but

depreciation on the same may be claimed over the useful life of the asset.

Solicitor fees with regards to lease for Simulator would be a revenue expense and

hence general deduction would apply for this case.

The amount spent by the company on the travel and stay of Dale Wise would be

deductible under s. 8-1 ITAA 1997 since it is an imperative expenditure related to

training and production of assessable income through upgrading and entering new

business avenues.

Conclusion

On the basis of the above discussion, the following recommendations may be offered.

The ordinary income would be derived on accrual basis from the services offered to

various airlines. Also, the cash and non-cash based lease incentives obtained from

CAC for changing the base would be considered as ordinary income. Additionally, the

compensation receipts from the settlement (i.e. $ 750,000) would be considered as

ordinary income and thereby assessable in the given tax year.

On the sale of land, while the proceeds would not be taxable but on account of capital

gains, CGT liability to the tune of $217,878 would le levied. Further, the interest

charges on loan are adjusted in the land cost base.

Also, the company would have FBT liability arising from extension of lunches,

Christmas party and car fringe benefits.

The solicitor expenses related to settlement case along with payment of restrictive

covenant proceeds would be capital expenditure and hence deduction would be

available over a five year period.

For furniture and mobile phone, depreciation related deduction may be permissible

provided the same is used for business.

The remaining expenses are considered as deductible expenses under s. 8-1 ITAA

1997 owing to there being a direct nexus between these expenses and assessable

income production. Also, these expenses are revenue in nature.

1997 owing to there being a direct nexus between these expenses and assessable

income production. Also, these expenses are revenue in nature.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.