Accounting 217 Personal Taxation: Individual Tax Computation 2017

VerifiedAdded on 2023/06/13

|14

|1143

|95

Homework Assignment

AI Summary

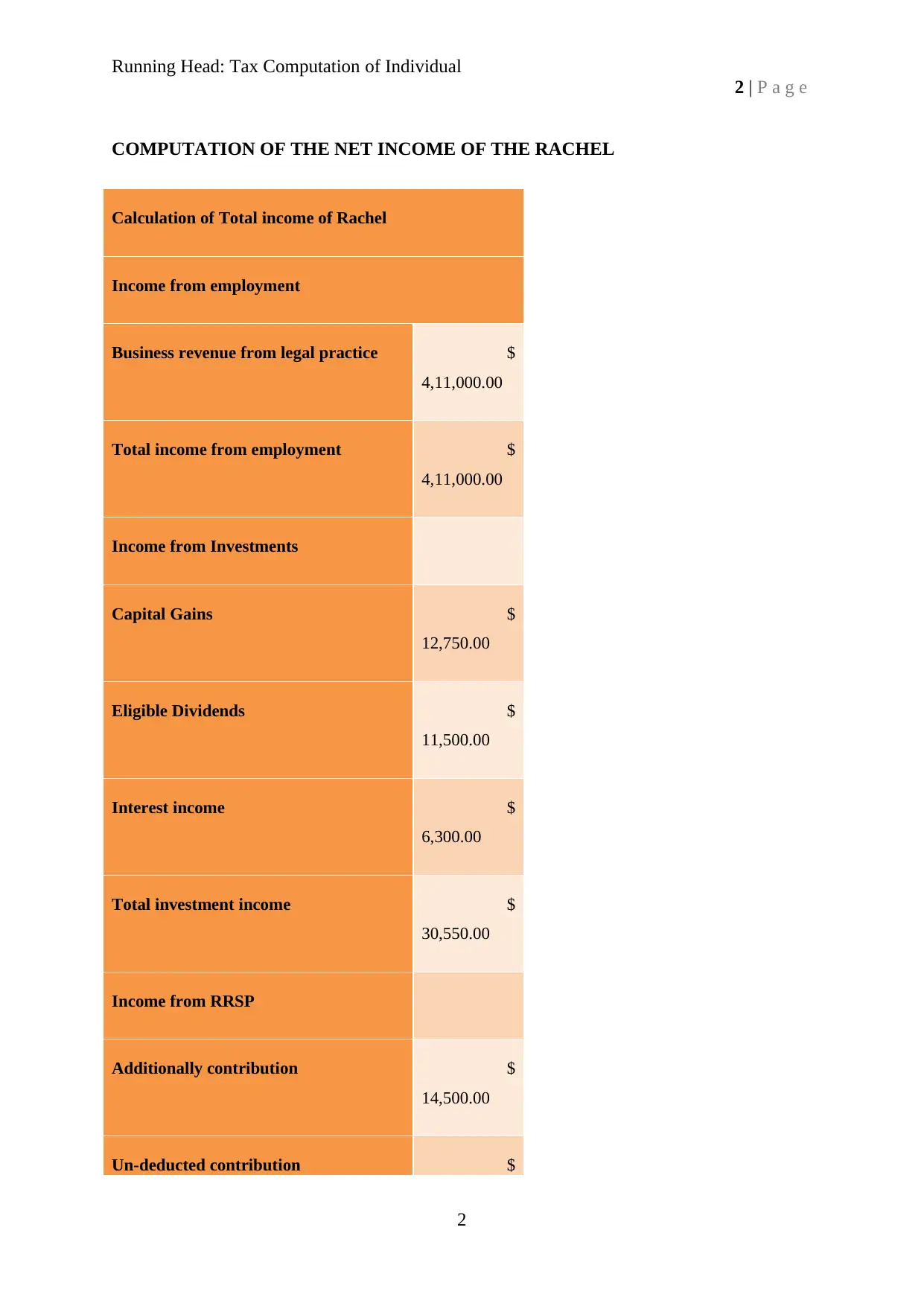

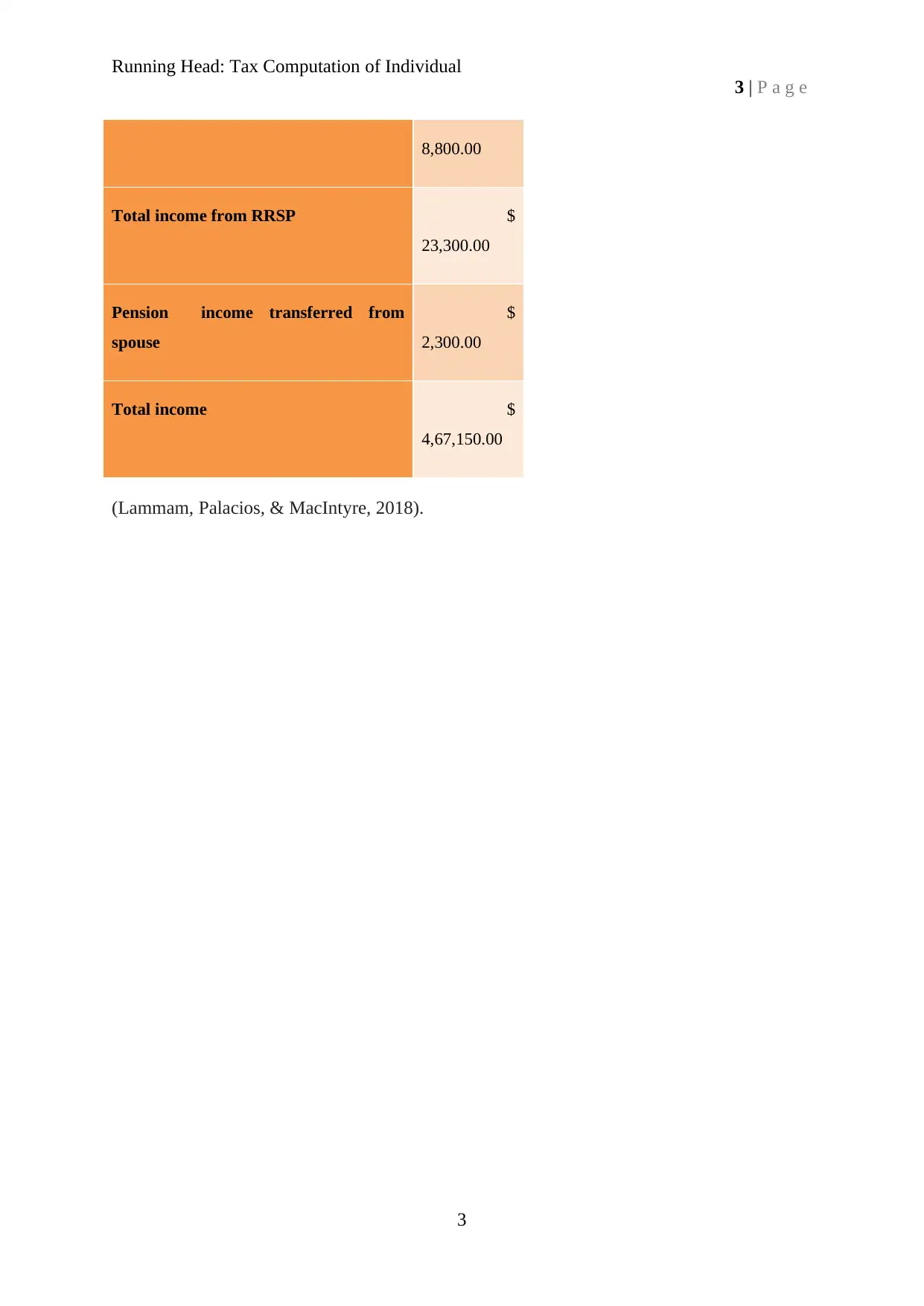

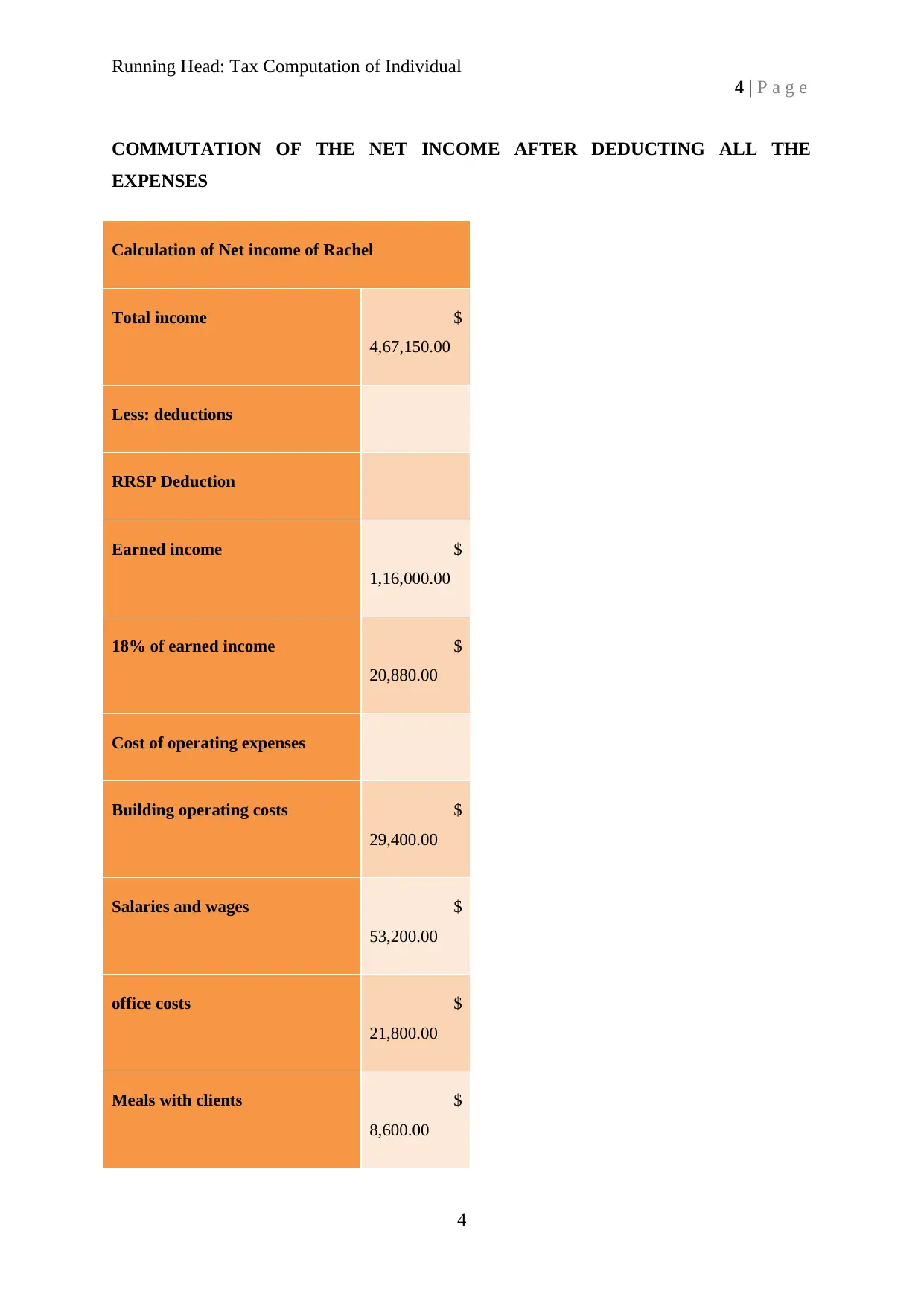

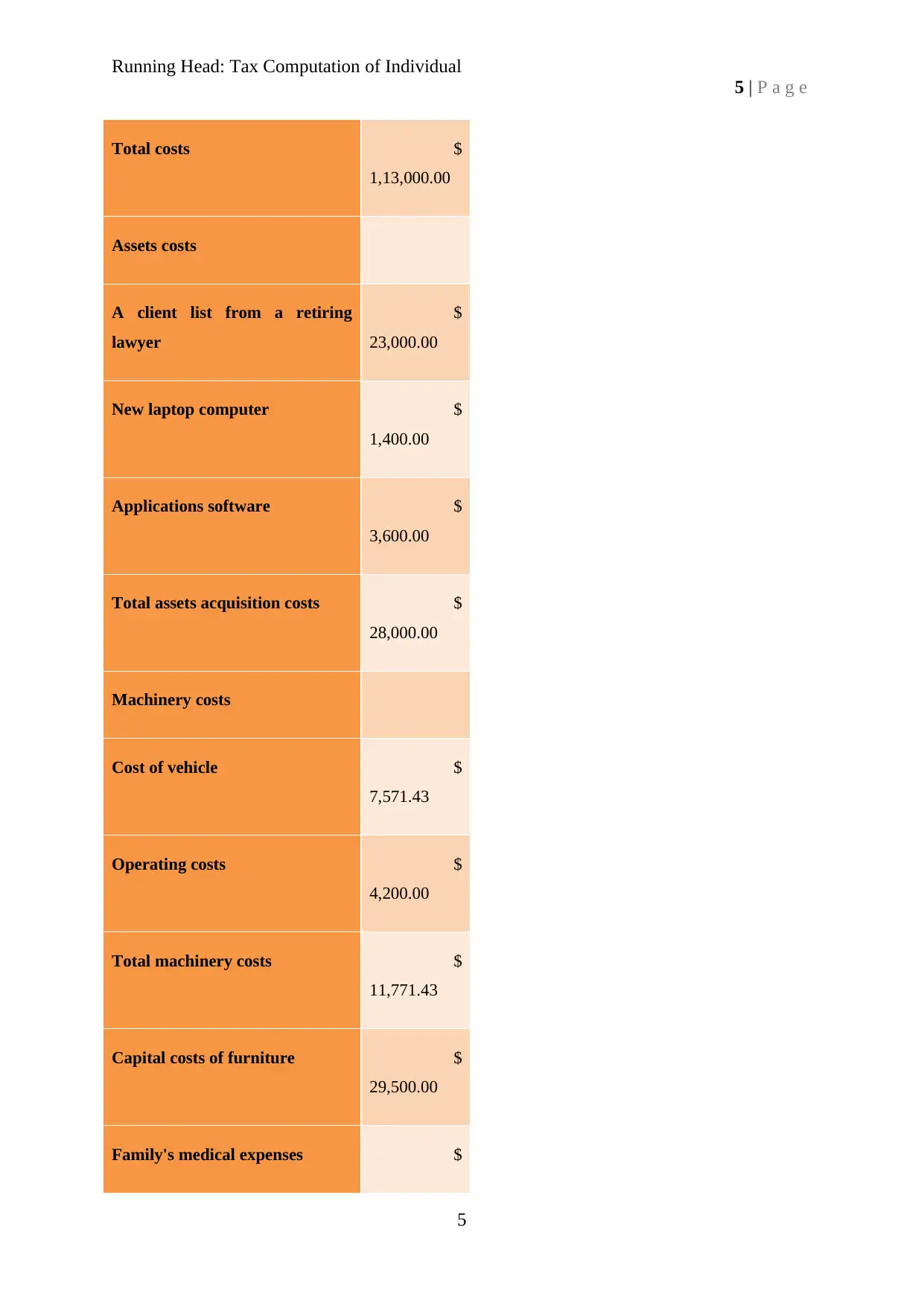

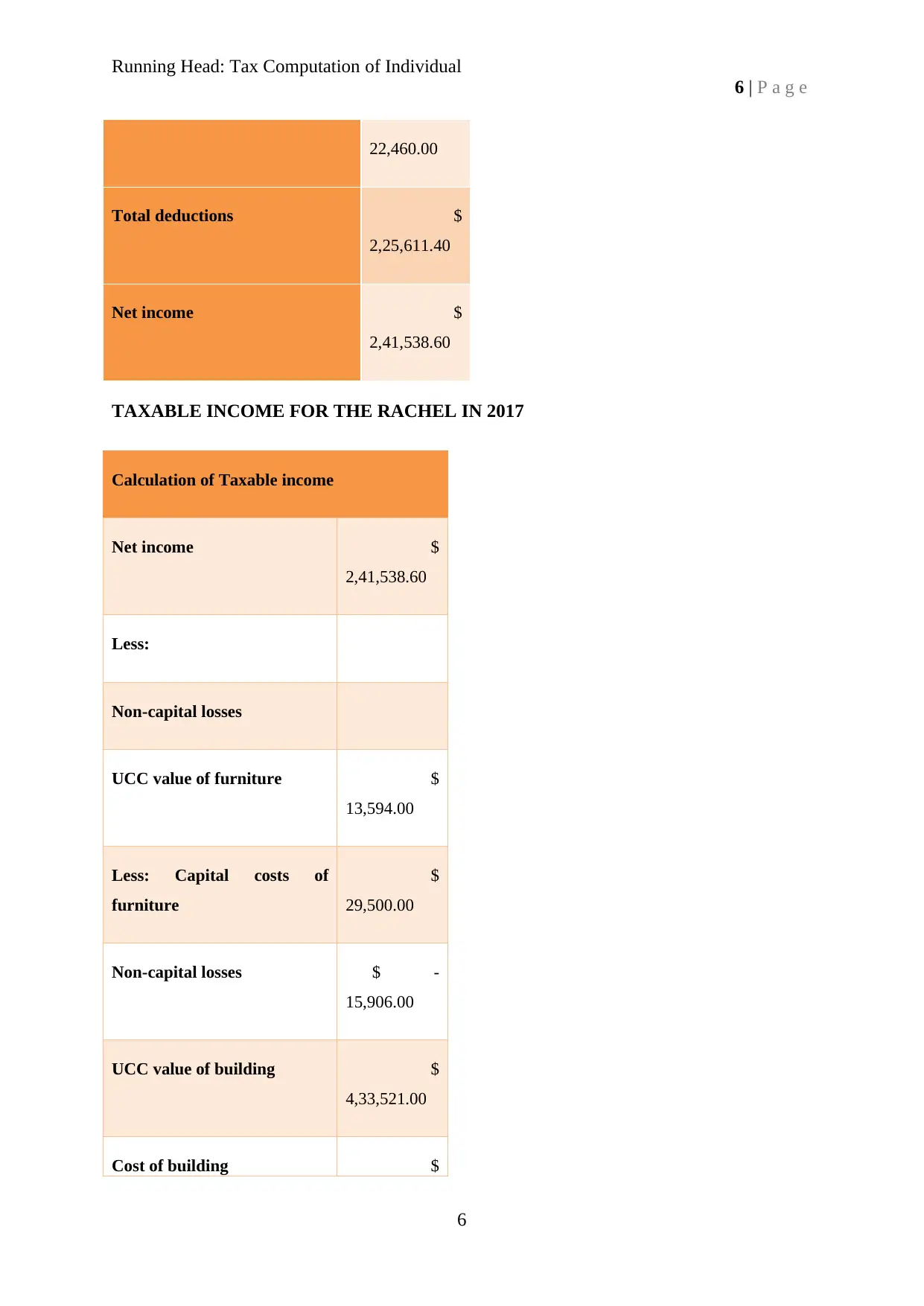

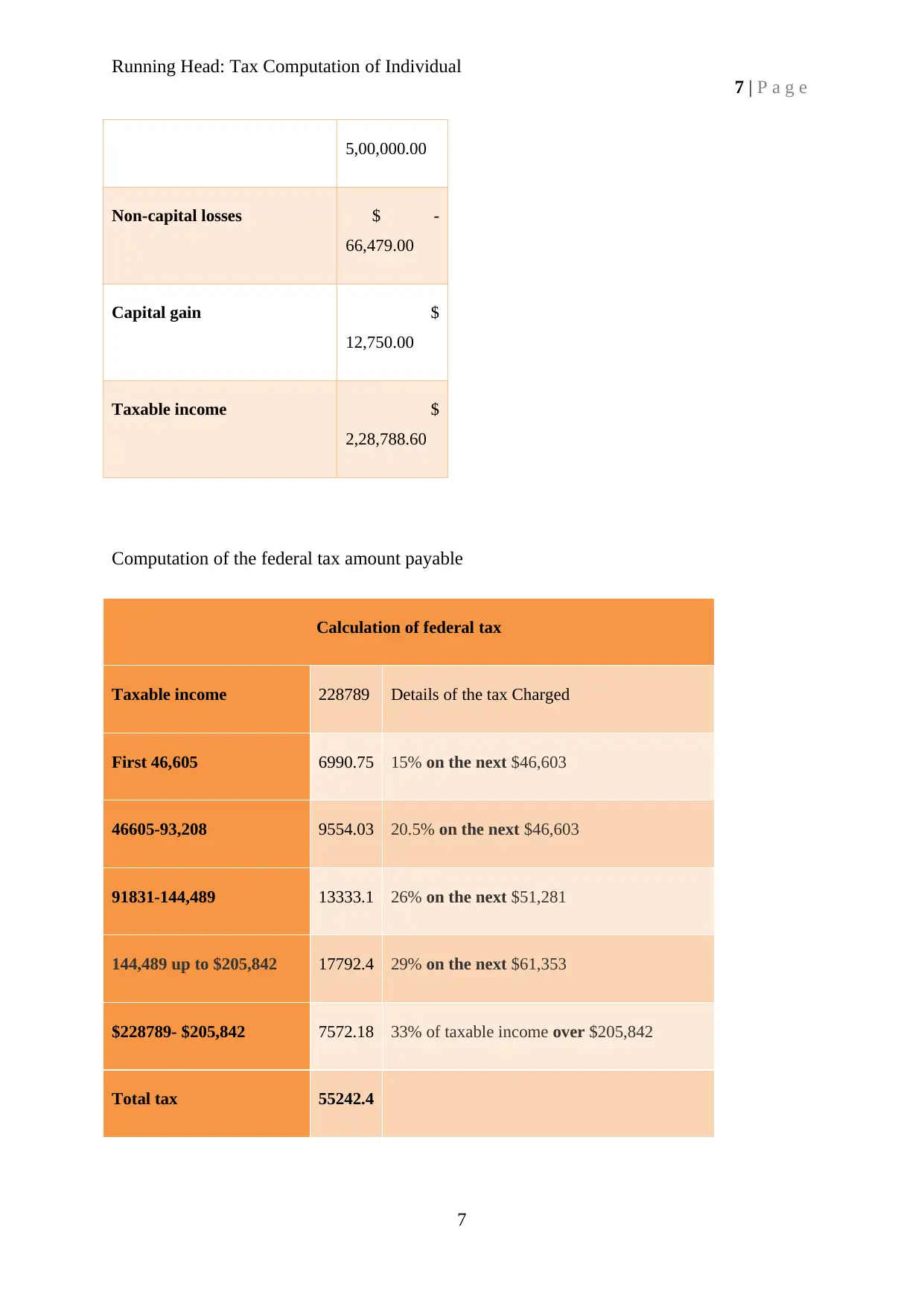

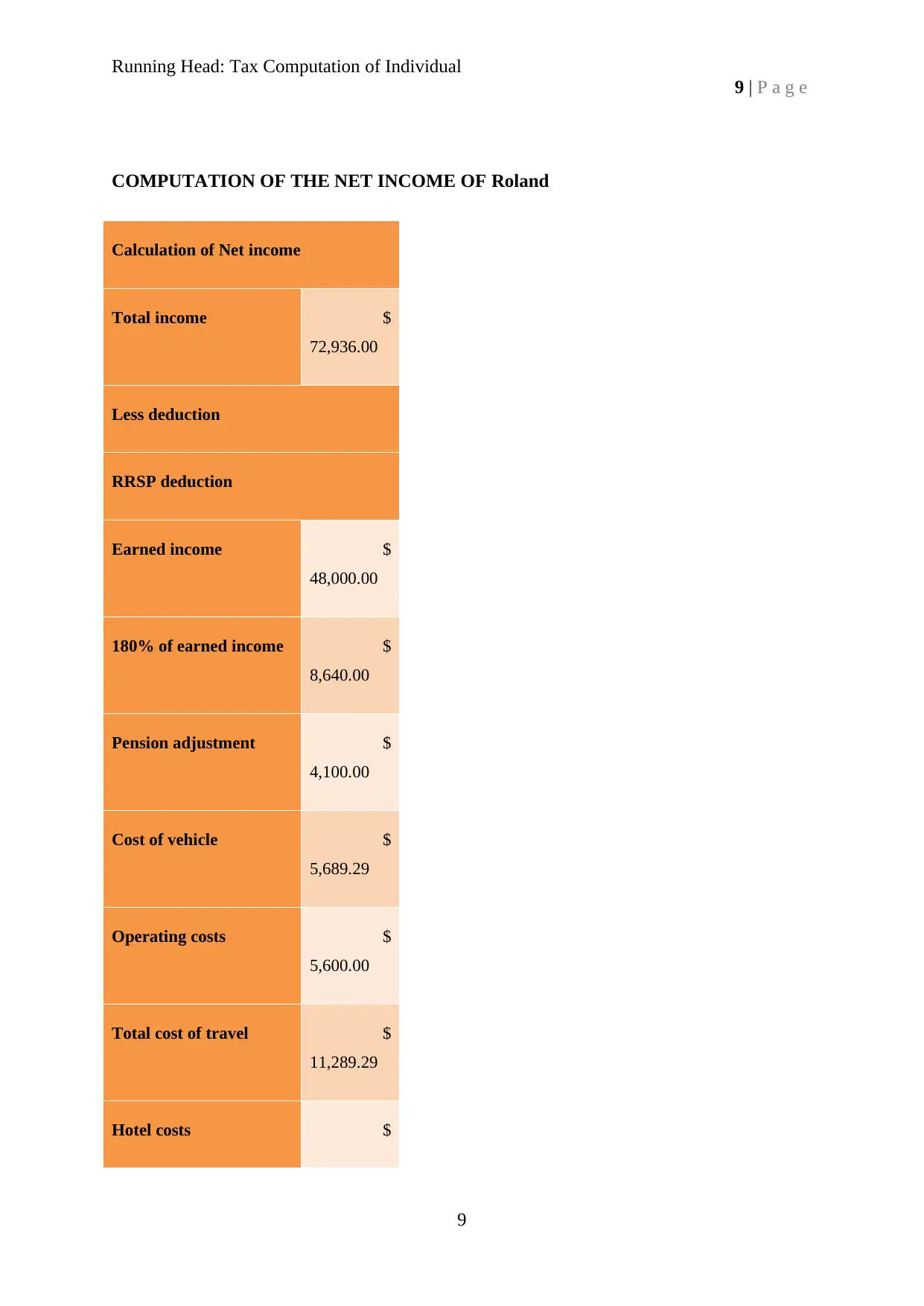

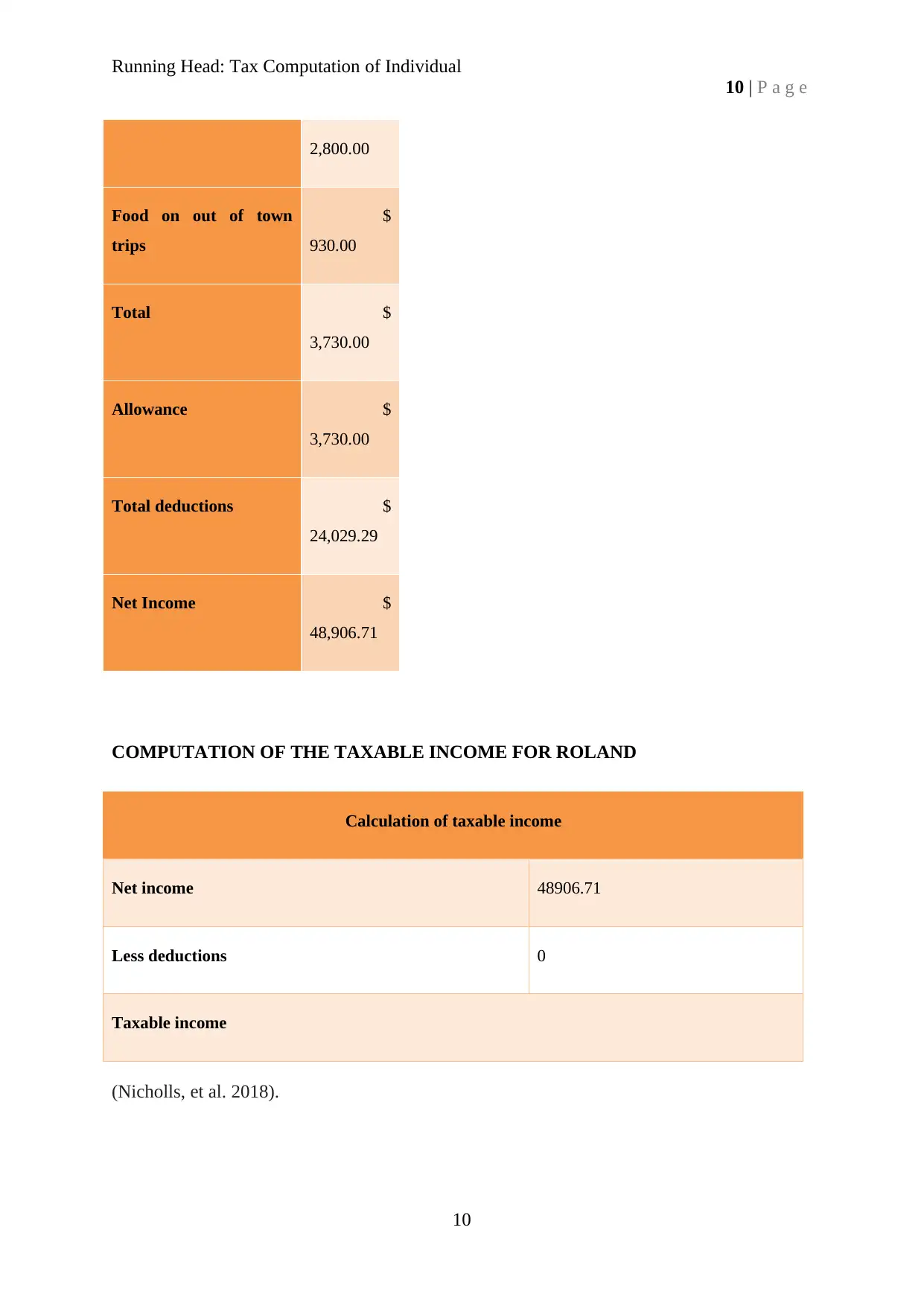

This assignment solution provides a detailed computation of federal taxes payable for Mr. and Mrs. Sorter for the 2017 taxation year, as per the requirements of Accounting 217 Personal Taxation. It includes the calculation of Rachel's total income from employment, investments, RRSP, and pension, followed by deductions for RRSP, operating expenses, asset costs, and machinery costs to arrive at her net income and taxable income. The federal tax amount payable by Rachel is then computed based on the applicable tax brackets. Similarly, the assignment calculates Roland's total income from employment and RRSP, followed by deductions for RRSP and vehicle costs to determine his net income and taxable income. Finally, the federal tax payable by Roland is computed based on his taxable income. The document is formatted as a memo to the clients, providing a clear and concise overview of their tax obligations.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.