Tax Consultation Report: Jack Jones' Tax Residency and Income

VerifiedAdded on 2020/07/22

|11

|3023

|45

Report

AI Summary

This report provides a tax consultation for Jack Jones, analyzing his residential status and taxable income for the income tax year ending June 30, 2016. The report begins with an introduction to taxation and the importance of residential status, discussing relevant conditions issued by Canada and Australia. The main body delves into Jack Jones' case scenario, outlining his movements between Australia and Canada, and examines relevant legislation and case laws. It covers the domicile test, 183-day test, and superannuation test for Australian residency, as well as residency requirements in Canada. The report includes a detailed calculation of Jack Jones' taxable income, considering various income sources such as salary, rental income, and benefits. It also addresses deductions and foreign tax credits, providing a comprehensive analysis of Jack Jones' tax liabilities. The conclusion summarizes the findings and references relevant sources.

Tax Consultation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Main Body.......................................................................................................................................1

Legislation advice on taxation residency status..........................................................................1

Calculation of taxable income of Jack Jones..............................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Main Body.......................................................................................................................................1

Legislation advice on taxation residency status..........................................................................1

Calculation of taxable income of Jack Jones..............................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

Index of Tables

Table 1: Calculation of taxable income...........................................................................................4

Table 1: Calculation of taxable income...........................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Taxation is a compulsory amount collected by the government. Residential status is an

important aspect which is required to be considered while assessing the taxable income of the

person (Hogg, Magee, and Li, 2013). An individual is considered to be resident based on the

certain conditions that are laid downs by the tax department of that country. The report discusses

relevant conditions issued by Canada and Australia in case of residential status. It further

discusses the case laws that are related to the given case scenario of jack Jones. In the end,

taxable income of Jack will be calculated considering him as a resident of Australia.

Main Body

As per the given case scenario, Jack Jones owns visa to live in Australia from 2nd

December 2012 to 30th June 2016. He came in contract with Peterson Marine Industries Pty Ltd

for which he arrived in the country. The company got leased to an American company with the

name of Samsak marine whose vessel was used to conduct oil exploration from Canada. It

compelled the client to shift to Canada. Therefore, he joined Samsak and left Australia on 1st

August 2015 to settle down in Canada. He worked for 9 months there and then terminates the

contract and returned to Australia on 1st May 2016. Then he remained in Australia upto rest of

the income tax year, that is, upto 30th June 2016.

Jack was able to lived in the accommodation provided by the company when he used to

work in Samsak for the first three months. He then lived with his sister where he used to live in

childhood. It shows that Jack was born and brought in Canada. He also has permanent house in

Vancouver Canada. It shows that he was already having residence ship of Canada once when he

used to live in the country.

Jack was in Australia and in Canada both ion the tax year. Hence, ii is difficult to decide

his residential status. It is important to analyse the legal rule issued by both the countries with

respect to residential status and reach to a conclusion. It is an important aspect as on the basis of

residential status, taxable income for the person is calculated.

Legislation advice on taxation residency status

Residential status is an important aspect which is to be considered while calculating

taxable income of a person (Hopkins, 2016). It has not important that the person must be

domicile of that nation. He can be resident of a particular country for a certain tax year as well.

Conditions for resident of Australia

1

Taxation is a compulsory amount collected by the government. Residential status is an

important aspect which is required to be considered while assessing the taxable income of the

person (Hogg, Magee, and Li, 2013). An individual is considered to be resident based on the

certain conditions that are laid downs by the tax department of that country. The report discusses

relevant conditions issued by Canada and Australia in case of residential status. It further

discusses the case laws that are related to the given case scenario of jack Jones. In the end,

taxable income of Jack will be calculated considering him as a resident of Australia.

Main Body

As per the given case scenario, Jack Jones owns visa to live in Australia from 2nd

December 2012 to 30th June 2016. He came in contract with Peterson Marine Industries Pty Ltd

for which he arrived in the country. The company got leased to an American company with the

name of Samsak marine whose vessel was used to conduct oil exploration from Canada. It

compelled the client to shift to Canada. Therefore, he joined Samsak and left Australia on 1st

August 2015 to settle down in Canada. He worked for 9 months there and then terminates the

contract and returned to Australia on 1st May 2016. Then he remained in Australia upto rest of

the income tax year, that is, upto 30th June 2016.

Jack was able to lived in the accommodation provided by the company when he used to

work in Samsak for the first three months. He then lived with his sister where he used to live in

childhood. It shows that Jack was born and brought in Canada. He also has permanent house in

Vancouver Canada. It shows that he was already having residence ship of Canada once when he

used to live in the country.

Jack was in Australia and in Canada both ion the tax year. Hence, ii is difficult to decide

his residential status. It is important to analyse the legal rule issued by both the countries with

respect to residential status and reach to a conclusion. It is an important aspect as on the basis of

residential status, taxable income for the person is calculated.

Legislation advice on taxation residency status

Residential status is an important aspect which is to be considered while calculating

taxable income of a person (Hopkins, 2016). It has not important that the person must be

domicile of that nation. He can be resident of a particular country for a certain tax year as well.

Conditions for resident of Australia

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The test that is performed to calculate the residency is known as resides test. In order to

become a resident of Australia, it is important to fulfil one of the following three statutory

conditions issued by Australian Tax office (ATO):

Domicile test: A person is considered as an Australian resident if one is domicile of that

country (Gitman, Juchau and Flanagan, 2015). It means the place which is his permanent

home. It is important to satisfy the officials of ATO that the person do not have any

permanent residence other than Australia.

183 days test: A person must be present in Australian territory for more than half of the

income year. It can be a continuous stay or in breaks it is considered as a constructive

residence in the country. However, the condition is that the person must not be planning

to shift in the other country and have no intention for the same (What income you pay tax

on, 2017).

Superannuation test: The Australian government employees working of the country's

post in different countries are considered as a resident of Australia.

Conditions for resident in Canada

In order to be considered as a resident of Canada; the person must be present in the

Canadian territory for more than 183 days. Otherwise, he will be considered as non resident of

Canada. However, it is important to develop residential ties with the country otherwise the

person will be called as deemed resident of Canada even if he has stayed in the territory for more

than 183 days. It is important to have significant ties with the country in order to become resident

of the country (Income Tax Folio S5-F1-C1, Determining an Individual’s Residence Status,

2017).

In the given case scenario, jack lived in Australia for 92 days and he was present in

Canada for 274 days. The days of presence in the country will help in deciding that whether he

will be considered as resident in Australia or in Canada.

A case law of taxpayer and Commissioner of taxation where the payer was an engineer

living in Australia since 1989. He bought a property and set up his home in the country.

However, in 2010 and 2011 he was in Singapore and India (Braithwaite, 2017). It was

determined by the verdict of the court that the person will be treated as a resident of Australia

and not for Singapore and India as he was on passenger permit during that time.

2

become a resident of Australia, it is important to fulfil one of the following three statutory

conditions issued by Australian Tax office (ATO):

Domicile test: A person is considered as an Australian resident if one is domicile of that

country (Gitman, Juchau and Flanagan, 2015). It means the place which is his permanent

home. It is important to satisfy the officials of ATO that the person do not have any

permanent residence other than Australia.

183 days test: A person must be present in Australian territory for more than half of the

income year. It can be a continuous stay or in breaks it is considered as a constructive

residence in the country. However, the condition is that the person must not be planning

to shift in the other country and have no intention for the same (What income you pay tax

on, 2017).

Superannuation test: The Australian government employees working of the country's

post in different countries are considered as a resident of Australia.

Conditions for resident in Canada

In order to be considered as a resident of Canada; the person must be present in the

Canadian territory for more than 183 days. Otherwise, he will be considered as non resident of

Canada. However, it is important to develop residential ties with the country otherwise the

person will be called as deemed resident of Canada even if he has stayed in the territory for more

than 183 days. It is important to have significant ties with the country in order to become resident

of the country (Income Tax Folio S5-F1-C1, Determining an Individual’s Residence Status,

2017).

In the given case scenario, jack lived in Australia for 92 days and he was present in

Canada for 274 days. The days of presence in the country will help in deciding that whether he

will be considered as resident in Australia or in Canada.

A case law of taxpayer and Commissioner of taxation where the payer was an engineer

living in Australia since 1989. He bought a property and set up his home in the country.

However, in 2010 and 2011 he was in Singapore and India (Braithwaite, 2017). It was

determined by the verdict of the court that the person will be treated as a resident of Australia

and not for Singapore and India as he was on passenger permit during that time.

2

As per the case Q95 83 ATC 472, a missionary of Australia went to other country for 4 to

6 years (Taylor and Richardson, 2012). She has a office in the country which she got rented for

that period during their absence. She and her husband came back to Australia after the

completion of missionary work. As per the judgement of the court, they will be considered as

non resident at the time of absence.

Based on the above two cases, it can be interpreted that only remaining in the country for

specified number of days is not important. The person must be able to satisfy the other

conditions as well. Further, a person, who is living in one country will be treated as a resident if

he went to other country on work permit (Harrison, 2012). Moreover, if a person owns a house

must live in it. Only owning a house will not be considered an important aspect while

determining residential status of a person. The person must be physically present in the country

in order to determine his actual number of days while determining residential status.

In some cases, the person take post in other countries but remain domicile for the same

country. In that cases rules issued by ATO will be considered while determining hos taxable

income. In case of Jack, he took permission to go to Canada on post for 5 months but he returned

in 9 months. In that case he will not be considered as resident for Australia. It shows that jack

will not be considered as resident of Australia and will be termed as non resident in that case.

If the person have stayed in two countries in the same taxable year; it is important to

consider that how much tax will be paid by the person in aforesaid countries. In case of jack, he

lived in Australia and in Canada during the taxable year. Tax residency is the important factor

that is required to be considered in that case. If he person is resident of Australia, he will be

considered taxable in that country and if his residential status stated that the person belongs to

Canada in that particular year (Taylor, and Richardson, 2012). Then he will be liable to pay tax

in Canada only.

Another important factor that come into light is the Double Tax Avoidance Agreement

(DTAA) between the two countries. It is the agreement between the two countries which decides

that what income will be taxed in the one country and what will be taxed in the other country in

certain circumstances. It helps in avoiding to pay tax in two countries on the same amount. It

also saves the person from any double effect of tax on the individual (Guide to foreign income

tax offset rules, 2017).

3

6 years (Taylor and Richardson, 2012). She has a office in the country which she got rented for

that period during their absence. She and her husband came back to Australia after the

completion of missionary work. As per the judgement of the court, they will be considered as

non resident at the time of absence.

Based on the above two cases, it can be interpreted that only remaining in the country for

specified number of days is not important. The person must be able to satisfy the other

conditions as well. Further, a person, who is living in one country will be treated as a resident if

he went to other country on work permit (Harrison, 2012). Moreover, if a person owns a house

must live in it. Only owning a house will not be considered an important aspect while

determining residential status of a person. The person must be physically present in the country

in order to determine his actual number of days while determining residential status.

In some cases, the person take post in other countries but remain domicile for the same

country. In that cases rules issued by ATO will be considered while determining hos taxable

income. In case of Jack, he took permission to go to Canada on post for 5 months but he returned

in 9 months. In that case he will not be considered as resident for Australia. It shows that jack

will not be considered as resident of Australia and will be termed as non resident in that case.

If the person have stayed in two countries in the same taxable year; it is important to

consider that how much tax will be paid by the person in aforesaid countries. In case of jack, he

lived in Australia and in Canada during the taxable year. Tax residency is the important factor

that is required to be considered in that case. If he person is resident of Australia, he will be

considered taxable in that country and if his residential status stated that the person belongs to

Canada in that particular year (Taylor, and Richardson, 2012). Then he will be liable to pay tax

in Canada only.

Another important factor that come into light is the Double Tax Avoidance Agreement

(DTAA) between the two countries. It is the agreement between the two countries which decides

that what income will be taxed in the one country and what will be taxed in the other country in

certain circumstances. It helps in avoiding to pay tax in two countries on the same amount. It

also saves the person from any double effect of tax on the individual (Guide to foreign income

tax offset rules, 2017).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Any income that has been generated from outside the country, which includes, salary,

wages, commission, allowances and bonus, is called as foreign employment income. This

income will be taxable in Australia if the person is a resident of the country. Hence, it will be

included in Australian tax return of the individual. However, if the tax has already been paid in

the foreign country (Lang, 2014). The person is eligible to get foreign tax credit on the same

amount. It helps in ensuring that the person is not doubly taxed in the country. The person is

eligible to get foreign tax credit in the below two conditions:

If the person have actually paid or deemed to have paid an amount of tax in the foreign

country.

Income or gain on which the tax has been paid in foreign must be included in assessable

income for the purpose of Australian tax (Tanzi, 2014).

The person who live normal customary life in Canada is only considered as its resident.

Otherwise, he is considered as a deemed resident. A factual resident is one who have maintained

some residential ties with the country while he was in abroad. Residential ties refers to having

personal property, social ties in the form of recreational or religious organisation and economic

ties in the form of employment. The person is also considered as factual resident to Canada if he

holds a Canadian passport.

Jack took permission for overseas employment from Australian government for 5

months. However, he returned in 9 months which made him non resident to the country. Further,

he was physically present in Australia for 92 days only. It shows that Jack will be considered as a

non resident to Australia.

Moreover, in case of Canada, the person tend to have a Canadian passport which helps in

maintaining secondary ties with the country. Further, he did not permanently shift there which

don't make him common resident of Canada. He was born and brought up there and also own a

permanent property. It can be concluded from the available facts that Jack will be considered as a

factual resident to Canada as he stayed for more that 183 days in the geographical territory, that

is for 274 days. He also holds a Canadian passport and a permanent property in Canada. He is

able to satisfy all the rules and regulations of factual resident of Canada.

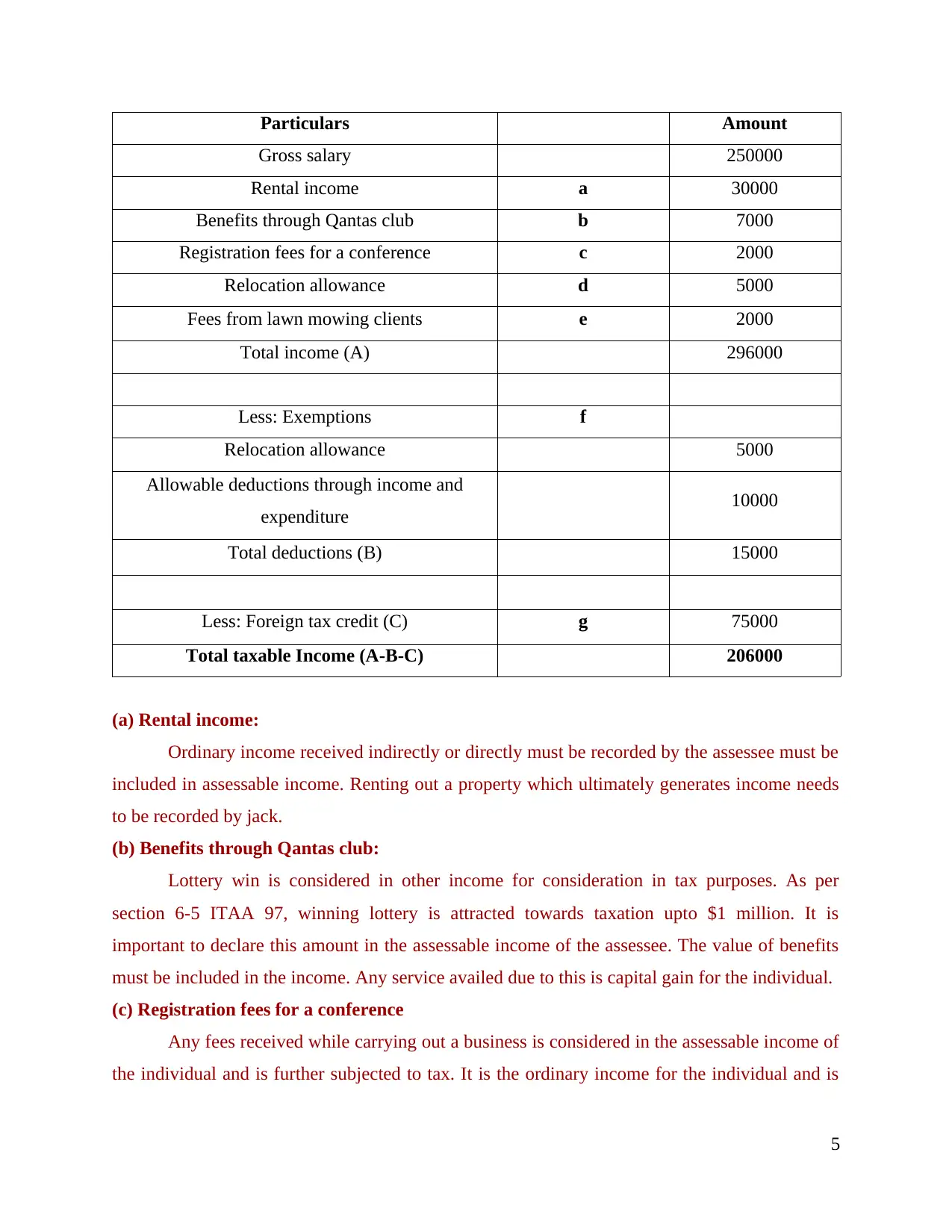

Calculation of taxable income of Jack Jones

Computation of taxable income for the income tax year ended 30 June 2016.

Table 1: Calculation of taxable income

4

wages, commission, allowances and bonus, is called as foreign employment income. This

income will be taxable in Australia if the person is a resident of the country. Hence, it will be

included in Australian tax return of the individual. However, if the tax has already been paid in

the foreign country (Lang, 2014). The person is eligible to get foreign tax credit on the same

amount. It helps in ensuring that the person is not doubly taxed in the country. The person is

eligible to get foreign tax credit in the below two conditions:

If the person have actually paid or deemed to have paid an amount of tax in the foreign

country.

Income or gain on which the tax has been paid in foreign must be included in assessable

income for the purpose of Australian tax (Tanzi, 2014).

The person who live normal customary life in Canada is only considered as its resident.

Otherwise, he is considered as a deemed resident. A factual resident is one who have maintained

some residential ties with the country while he was in abroad. Residential ties refers to having

personal property, social ties in the form of recreational or religious organisation and economic

ties in the form of employment. The person is also considered as factual resident to Canada if he

holds a Canadian passport.

Jack took permission for overseas employment from Australian government for 5

months. However, he returned in 9 months which made him non resident to the country. Further,

he was physically present in Australia for 92 days only. It shows that Jack will be considered as a

non resident to Australia.

Moreover, in case of Canada, the person tend to have a Canadian passport which helps in

maintaining secondary ties with the country. Further, he did not permanently shift there which

don't make him common resident of Canada. He was born and brought up there and also own a

permanent property. It can be concluded from the available facts that Jack will be considered as a

factual resident to Canada as he stayed for more that 183 days in the geographical territory, that

is for 274 days. He also holds a Canadian passport and a permanent property in Canada. He is

able to satisfy all the rules and regulations of factual resident of Canada.

Calculation of taxable income of Jack Jones

Computation of taxable income for the income tax year ended 30 June 2016.

Table 1: Calculation of taxable income

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

Gross salary 250000

Rental income a 30000

Benefits through Qantas club b 7000

Registration fees for a conference c 2000

Relocation allowance d 5000

Fees from lawn mowing clients e 2000

Total income (A) 296000

Less: Exemptions f

Relocation allowance 5000

Allowable deductions through income and

expenditure 10000

Total deductions (B) 15000

Less: Foreign tax credit (C) g 75000

Total taxable Income (A-B-C) 206000

(a) Rental income:

Ordinary income received indirectly or directly must be recorded by the assessee must be

included in assessable income. Renting out a property which ultimately generates income needs

to be recorded by jack.

(b) Benefits through Qantas club:

Lottery win is considered in other income for consideration in tax purposes. As per

section 6-5 ITAA 97, winning lottery is attracted towards taxation upto $1 million. It is

important to declare this amount in the assessable income of the assessee. The value of benefits

must be included in the income. Any service availed due to this is capital gain for the individual.

(c) Registration fees for a conference

Any fees received while carrying out a business is considered in the assessable income of

the individual and is further subjected to tax. It is the ordinary income for the individual and is

5

Gross salary 250000

Rental income a 30000

Benefits through Qantas club b 7000

Registration fees for a conference c 2000

Relocation allowance d 5000

Fees from lawn mowing clients e 2000

Total income (A) 296000

Less: Exemptions f

Relocation allowance 5000

Allowable deductions through income and

expenditure 10000

Total deductions (B) 15000

Less: Foreign tax credit (C) g 75000

Total taxable Income (A-B-C) 206000

(a) Rental income:

Ordinary income received indirectly or directly must be recorded by the assessee must be

included in assessable income. Renting out a property which ultimately generates income needs

to be recorded by jack.

(b) Benefits through Qantas club:

Lottery win is considered in other income for consideration in tax purposes. As per

section 6-5 ITAA 97, winning lottery is attracted towards taxation upto $1 million. It is

important to declare this amount in the assessable income of the assessee. The value of benefits

must be included in the income. Any service availed due to this is capital gain for the individual.

(c) Registration fees for a conference

Any fees received while carrying out a business is considered in the assessable income of

the individual and is further subjected to tax. It is the ordinary income for the individual and is

5

considered under 'salary' head or 'Profits and gain from business and profession'. It is considered

as personal income if the services are provided without the partnership any firm or the company.

(d) Relocation allowance

It is a type of compensation provided by the employer in case of location shift to the

employee. It helps the employee to cover the cost of removal and storage. It is considered in

s136 (1) which is with respect to living away from home allowance. Since, it is a fringe benefit

provided by the employer it is considered as tax deductible and exemption is provided to the

client on the same.

(e) Fees from lawn mowing clients:

It is a Personal service income which is required to be included while calculating taxable

income. It is derives by the client with his personal skills or efforts. Jack has received this

amount due to his lawn mowing services. It will be treated as individual income of Jack.

(f) Exemptions:

Taxable income jack have been calculated considering all the provisions issued by

Australian Tax Office. According to the deductions issued by ATO, the allowable deduction

amount that have been mentioned in the income and expenditure statement is $10000. Moreover,

he also earned relocation allowance from his employer which is a fringe benefit. Hence, it is also

taken into consideration of exempted in come for the employee. Hence, the two deductions have

been taken into consideration while calculating taxable income.

(g) Further, the amount of foreign tax credit have been deducted as the person have already paid

tax on the amount in Canada. It helps in eliminating the double taxation impact on the income

earned by the assessee. It is included by the individual while calculating assessable income as per

the rules laid down in Section 23AI or 23AK of ITAA 1936 for Australian tax purposes.

Moreover, all the income that has been received and are not attracted to deductions must

be included while calculating total income of Jack.

CONCLUSION

Based on the above report, it can be concluded that, Jack will be considered as a factual

resident of Canada as he was physical present for 264 days in that country. Further, all the

important provisions of Canada and Australia with respect to residential status have been studied

in the report. Moreover, it can be inferred that the person must be more than 183 days physically

6

as personal income if the services are provided without the partnership any firm or the company.

(d) Relocation allowance

It is a type of compensation provided by the employer in case of location shift to the

employee. It helps the employee to cover the cost of removal and storage. It is considered in

s136 (1) which is with respect to living away from home allowance. Since, it is a fringe benefit

provided by the employer it is considered as tax deductible and exemption is provided to the

client on the same.

(e) Fees from lawn mowing clients:

It is a Personal service income which is required to be included while calculating taxable

income. It is derives by the client with his personal skills or efforts. Jack has received this

amount due to his lawn mowing services. It will be treated as individual income of Jack.

(f) Exemptions:

Taxable income jack have been calculated considering all the provisions issued by

Australian Tax Office. According to the deductions issued by ATO, the allowable deduction

amount that have been mentioned in the income and expenditure statement is $10000. Moreover,

he also earned relocation allowance from his employer which is a fringe benefit. Hence, it is also

taken into consideration of exempted in come for the employee. Hence, the two deductions have

been taken into consideration while calculating taxable income.

(g) Further, the amount of foreign tax credit have been deducted as the person have already paid

tax on the amount in Canada. It helps in eliminating the double taxation impact on the income

earned by the assessee. It is included by the individual while calculating assessable income as per

the rules laid down in Section 23AI or 23AK of ITAA 1936 for Australian tax purposes.

Moreover, all the income that has been received and are not attracted to deductions must

be included while calculating total income of Jack.

CONCLUSION

Based on the above report, it can be concluded that, Jack will be considered as a factual

resident of Canada as he was physical present for 264 days in that country. Further, all the

important provisions of Canada and Australia with respect to residential status have been studied

in the report. Moreover, it can be inferred that the person must be more than 183 days physically

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

present in order to become resident of that country. In the end, the calculated taxable amount of

Jack is 206,000.

7

Jack is 206,000.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Harrison, K. (2012). A tale of two taxes: The fate of environmental tax reform in Canada. Review

of Policy Research. 29(3). 383-407.

Hogg, P. W., Magee, J. E., & Li, J. (2013). Principles of Canadian income tax law. Carswell.

Hopkins, B. R. (2016). The Law of Tax-Exempt Organizations+ Website, 2016 Supplement. John

Wiley & Sons.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Tanzi, V. (2014). Inflation, indexation and interest income taxation. PSL Quarterly

Review. 29(116).

Taylor, G., & Richardson, G. (2012). International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting. 47(4). 469-496.

Online

What income you pay tax on. (2017). [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Coming-to-

Australia/Paying-tax-and-lodging-a-tax-return/What-income-you-pay-tax-on/>.

[Accessed on 15th September 2017].

Income Tax Folio S5-F1-C1, Determining an Individual’s Residence Status. (2017). [Online].

Available through <https://www.canada.ca/en/revenue-agency/services/tax/technical-

information/income-tax/income-tax-folios-index/series-5-international-residency/folio-

1-residency/income-tax-folio-s5-f1-c1-determining-individual-s-residence-status.html>.

[Accessed on 15th September 2017].

Guide to foreign income tax offset rules. (2017). Available through

<https://www.ato.gov.au/Individuals/Tax-return/2017/In-detail/Publications/Guide-to-

foreign-income-tax-offset-rules-2017/?=redirected>. [Accessed on 15th September

2017].

8

Books and Journals

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Harrison, K. (2012). A tale of two taxes: The fate of environmental tax reform in Canada. Review

of Policy Research. 29(3). 383-407.

Hogg, P. W., Magee, J. E., & Li, J. (2013). Principles of Canadian income tax law. Carswell.

Hopkins, B. R. (2016). The Law of Tax-Exempt Organizations+ Website, 2016 Supplement. John

Wiley & Sons.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Tanzi, V. (2014). Inflation, indexation and interest income taxation. PSL Quarterly

Review. 29(116).

Taylor, G., & Richardson, G. (2012). International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting. 47(4). 469-496.

Online

What income you pay tax on. (2017). [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Coming-to-

Australia/Paying-tax-and-lodging-a-tax-return/What-income-you-pay-tax-on/>.

[Accessed on 15th September 2017].

Income Tax Folio S5-F1-C1, Determining an Individual’s Residence Status. (2017). [Online].

Available through <https://www.canada.ca/en/revenue-agency/services/tax/technical-

information/income-tax/income-tax-folios-index/series-5-international-residency/folio-

1-residency/income-tax-folio-s5-f1-c1-determining-individual-s-residence-status.html>.

[Accessed on 15th September 2017].

Guide to foreign income tax offset rules. (2017). Available through

<https://www.ato.gov.au/Individuals/Tax-return/2017/In-detail/Publications/Guide-to-

foreign-income-tax-offset-rules-2017/?=redirected>. [Accessed on 15th September

2017].

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.