Tax Law 30 June 2019 Assignment: Seminar 5 - Tax Deductions & Expenses

VerifiedAdded on 2023/01/18

|11

|2795

|99

Homework Assignment

AI Summary

This assignment solution addresses two tax law questions concerning rental property expenses and car expenses. Question 1 analyzes Jayson Jones' tax deductions for his Brisbane investment property, including interest, legal fees, bathroom vanity replacement, and depreciation of a chemical blower. The solution details the deductibility of interest expenses, the treatment of borrowing costs, and the application of relevant tax rulings (TR97/23, TR 2018/4) to determine depreciation. It also examines the tax treatment of repairs versus capital improvements. Question 2 concerns Ben, an area manager, and his car expenses. It requires calculating his car expense deductions under Division 28 ITAA 97, considering car allowance, lease, and logbook records of business versus personal use. The solution evaluates the appropriate deduction method and substantiation requirements for car expenses.

Tax Law

30 June 2019

Seminar Number 5

[The focus of this seminar is Chapter 6 of the Study Guide]

Question 1

Jayson Jones, a self-employed plumber, purchased a house in Brisbane as an investment for

$430,000 on 1 September 2018. He rented out the house from that date to the existing tenant

for $410 per week.

Jayson seeks your advice as to whether he might be able to claim any tax deductions

for the following expenses:

Jayson took out a loan of $350,000 on 1 September 2018 for 20 years to purchase

the house. Interest paid on the loan for the tax year ended 30 June 2019 was $23,630.

The legal fees, loan charges and stamp duty paid in relation to the loan were $5,460.

On 10 March 2019 Jayson paid $1,400 to replace the entire bathroom vanity unit,

which was badly damaged by a burst water pipe. The new vanity was made of similar

material to the original. He was able to re-use the original tapware [Hint: research the

tax treatment of this expenditure].

In regards to the burst water pipe above, Jayson fixed it himself. He estimates that if

he performed that work for a paying customer he would have charged $450 for his

labour. Jayson spent $35 on rubber seals to fix the water pipe.

Jayson would also like some tax advice on the following transaction:

Jayson sold a chemical blower on 15 June 2019 for $24,000 that he had been using

solely for work purposes, but no longer needed. He bought the chemical blower on 1

October 2017 for $30,000 and has been using it since that date. He has been using

the diminishing value method to claim the decline in value of the equipment (and using

the Commissioner’s estimate of effective life). Assume that Jayson is NOT a small

business entity and please ignore the effect of GST.

[Hint: you need to find the appropriate tax ruling that contains the Commissioner’s

estimate of effective life for depreciating assets – note that date of acquisition is

relevant].

1

30 June 2019

Seminar Number 5

[The focus of this seminar is Chapter 6 of the Study Guide]

Question 1

Jayson Jones, a self-employed plumber, purchased a house in Brisbane as an investment for

$430,000 on 1 September 2018. He rented out the house from that date to the existing tenant

for $410 per week.

Jayson seeks your advice as to whether he might be able to claim any tax deductions

for the following expenses:

Jayson took out a loan of $350,000 on 1 September 2018 for 20 years to purchase

the house. Interest paid on the loan for the tax year ended 30 June 2019 was $23,630.

The legal fees, loan charges and stamp duty paid in relation to the loan were $5,460.

On 10 March 2019 Jayson paid $1,400 to replace the entire bathroom vanity unit,

which was badly damaged by a burst water pipe. The new vanity was made of similar

material to the original. He was able to re-use the original tapware [Hint: research the

tax treatment of this expenditure].

In regards to the burst water pipe above, Jayson fixed it himself. He estimates that if

he performed that work for a paying customer he would have charged $450 for his

labour. Jayson spent $35 on rubber seals to fix the water pipe.

Jayson would also like some tax advice on the following transaction:

Jayson sold a chemical blower on 15 June 2019 for $24,000 that he had been using

solely for work purposes, but no longer needed. He bought the chemical blower on 1

October 2017 for $30,000 and has been using it since that date. He has been using

the diminishing value method to claim the decline in value of the equipment (and using

the Commissioner’s estimate of effective life). Assume that Jayson is NOT a small

business entity and please ignore the effect of GST.

[Hint: you need to find the appropriate tax ruling that contains the Commissioner’s

estimate of effective life for depreciating assets – note that date of acquisition is

relevant].

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

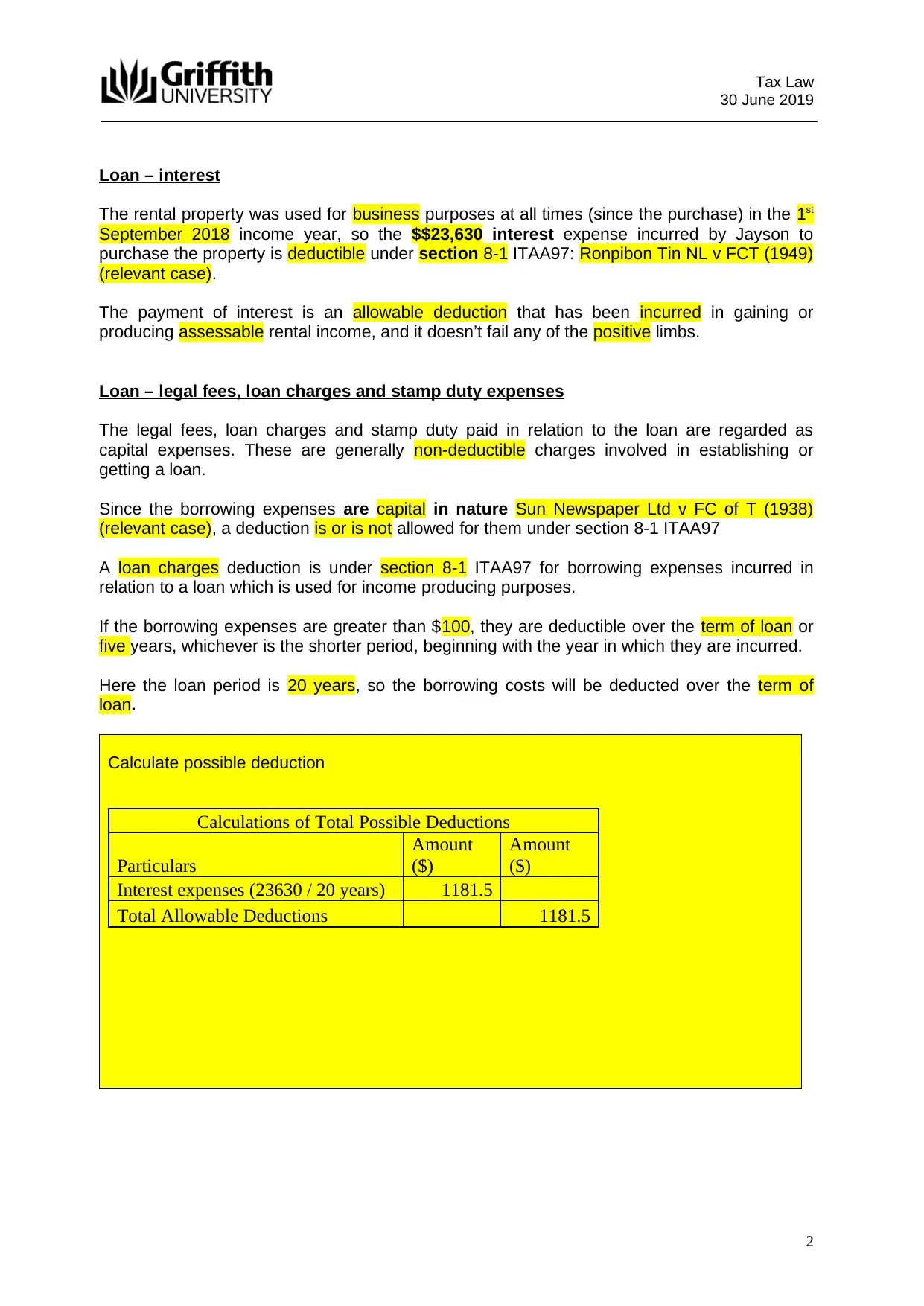

Loan – interest

The rental property was used for business purposes at all times (since the purchase) in the 1st

September 2018 income year, so the $$23,630 interest expense incurred by Jayson to

purchase the property is deductible under section 8-1 ITAA97: Ronpibon Tin NL v FCT (1949)

(relevant case).

The payment of interest is an allowable deduction that has been incurred in gaining or

producing assessable rental income, and it doesn’t fail any of the positive limbs.

Loan – legal fees, loan charges and stamp duty expenses

The legal fees, loan charges and stamp duty paid in relation to the loan are regarded as

capital expenses. These are generally non-deductible charges involved in establishing or

getting a loan.

Since the borrowing expenses are capital in nature Sun Newspaper Ltd v FC of T (1938)

(relevant case), a deduction is or is not allowed for them under section 8-1 ITAA97

A loan charges deduction is under section 8-1 ITAA97 for borrowing expenses incurred in

relation to a loan which is used for income producing purposes.

If the borrowing expenses are greater than $100, they are deductible over the term of loan or

five years, whichever is the shorter period, beginning with the year in which they are incurred.

Here the loan period is 20 years, so the borrowing costs will be deducted over the term of

loan.

Calculate possible deduction

Calculations of Total Possible Deductions

Particulars

Amount

($)

Amount

($)

Interest expenses (23630 / 20 years) 1181.5

Total Allowable Deductions 1181.5

2

30 June 2019

Loan – interest

The rental property was used for business purposes at all times (since the purchase) in the 1st

September 2018 income year, so the $$23,630 interest expense incurred by Jayson to

purchase the property is deductible under section 8-1 ITAA97: Ronpibon Tin NL v FCT (1949)

(relevant case).

The payment of interest is an allowable deduction that has been incurred in gaining or

producing assessable rental income, and it doesn’t fail any of the positive limbs.

Loan – legal fees, loan charges and stamp duty expenses

The legal fees, loan charges and stamp duty paid in relation to the loan are regarded as

capital expenses. These are generally non-deductible charges involved in establishing or

getting a loan.

Since the borrowing expenses are capital in nature Sun Newspaper Ltd v FC of T (1938)

(relevant case), a deduction is or is not allowed for them under section 8-1 ITAA97

A loan charges deduction is under section 8-1 ITAA97 for borrowing expenses incurred in

relation to a loan which is used for income producing purposes.

If the borrowing expenses are greater than $100, they are deductible over the term of loan or

five years, whichever is the shorter period, beginning with the year in which they are incurred.

Here the loan period is 20 years, so the borrowing costs will be deducted over the term of

loan.

Calculate possible deduction

Calculations of Total Possible Deductions

Particulars

Amount

($)

Amount

($)

Interest expenses (23630 / 20 years) 1181.5

Total Allowable Deductions 1181.5

2

Tax Law

30 June 2019

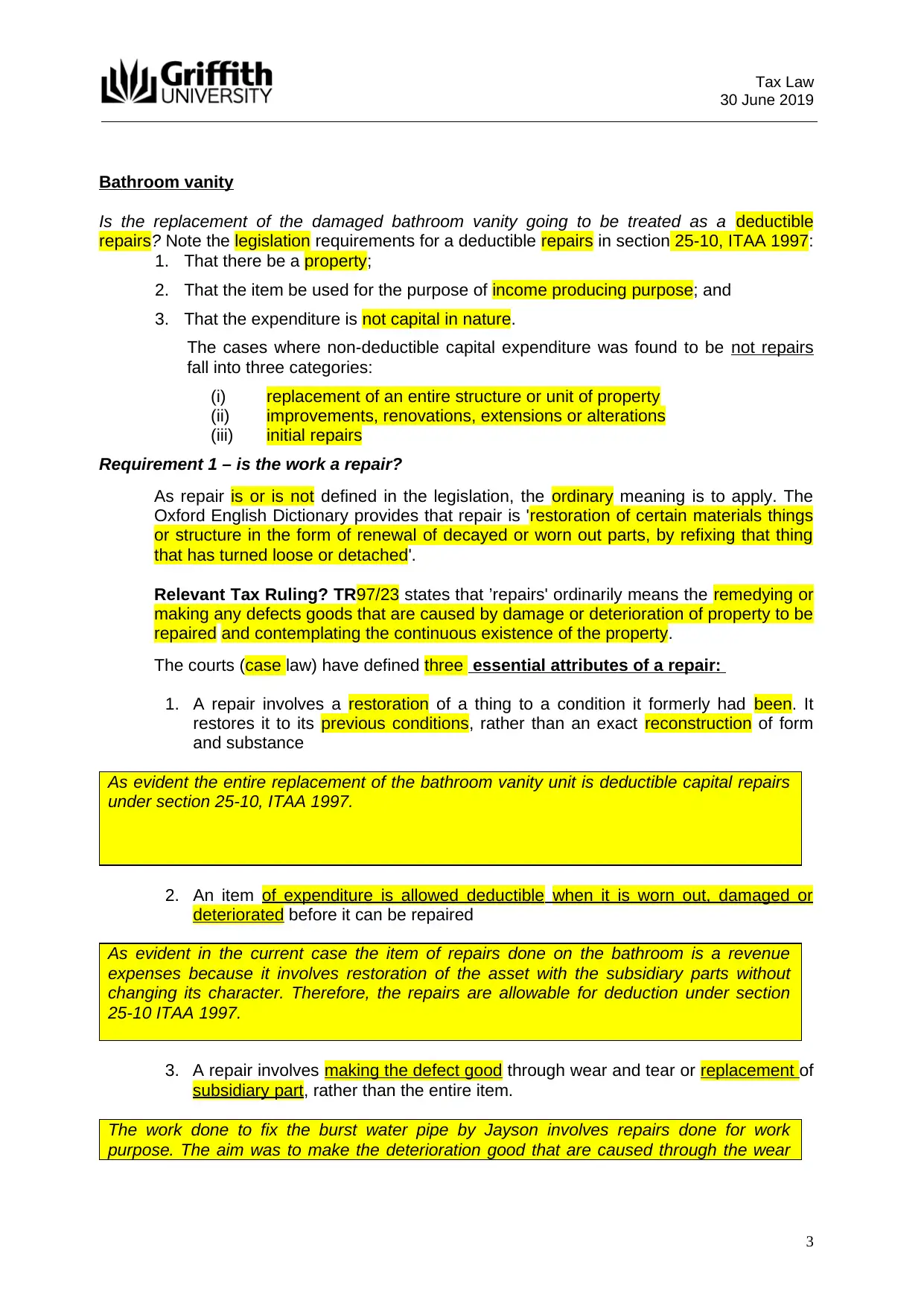

Bathroom vanity

Is the replacement of the damaged bathroom vanity going to be treated as a deductible

repairs? Note the legislation requirements for a deductible repairs in section 25-10, ITAA 1997:

1. That there be a property;

2. That the item be used for the purpose of income producing purpose; and

3. That the expenditure is not capital in nature.

The cases where non-deductible capital expenditure was found to be not repairs

fall into three categories:

(i) replacement of an entire structure or unit of property

(ii) improvements, renovations, extensions or alterations

(iii) initial repairs

Requirement 1 – is the work a repair?

As repair is or is not defined in the legislation, the ordinary meaning is to apply. The

Oxford English Dictionary provides that repair is 'restoration of certain materials things

or structure in the form of renewal of decayed or worn out parts, by refixing that thing

that has turned loose or detached'.

Relevant Tax Ruling? TR97/23 states that ’repairs' ordinarily means the remedying or

making any defects goods that are caused by damage or deterioration of property to be

repaired and contemplating the continuous existence of the property.

The courts (case law) have defined three essential attributes of a repair:

1. A repair involves a restoration of a thing to a condition it formerly had been. It

restores it to its previous conditions, rather than an exact reconstruction of form

and substance

As evident the entire replacement of the bathroom vanity unit is deductible capital repairs

under section 25-10, ITAA 1997.

2. An item of expenditure is allowed deductible when it is worn out, damaged or

deteriorated before it can be repaired

As evident in the current case the item of repairs done on the bathroom is a revenue

expenses because it involves restoration of the asset with the subsidiary parts without

changing its character. Therefore, the repairs are allowable for deduction under section

25-10 ITAA 1997.

3. A repair involves making the defect good through wear and tear or replacement of

subsidiary part, rather than the entire item.

The work done to fix the burst water pipe by Jayson involves repairs done for work

purpose. The aim was to make the deterioration good that are caused through the wear

3

30 June 2019

Bathroom vanity

Is the replacement of the damaged bathroom vanity going to be treated as a deductible

repairs? Note the legislation requirements for a deductible repairs in section 25-10, ITAA 1997:

1. That there be a property;

2. That the item be used for the purpose of income producing purpose; and

3. That the expenditure is not capital in nature.

The cases where non-deductible capital expenditure was found to be not repairs

fall into three categories:

(i) replacement of an entire structure or unit of property

(ii) improvements, renovations, extensions or alterations

(iii) initial repairs

Requirement 1 – is the work a repair?

As repair is or is not defined in the legislation, the ordinary meaning is to apply. The

Oxford English Dictionary provides that repair is 'restoration of certain materials things

or structure in the form of renewal of decayed or worn out parts, by refixing that thing

that has turned loose or detached'.

Relevant Tax Ruling? TR97/23 states that ’repairs' ordinarily means the remedying or

making any defects goods that are caused by damage or deterioration of property to be

repaired and contemplating the continuous existence of the property.

The courts (case law) have defined three essential attributes of a repair:

1. A repair involves a restoration of a thing to a condition it formerly had been. It

restores it to its previous conditions, rather than an exact reconstruction of form

and substance

As evident the entire replacement of the bathroom vanity unit is deductible capital repairs

under section 25-10, ITAA 1997.

2. An item of expenditure is allowed deductible when it is worn out, damaged or

deteriorated before it can be repaired

As evident in the current case the item of repairs done on the bathroom is a revenue

expenses because it involves restoration of the asset with the subsidiary parts without

changing its character. Therefore, the repairs are allowable for deduction under section

25-10 ITAA 1997.

3. A repair involves making the defect good through wear and tear or replacement of

subsidiary part, rather than the entire item.

The work done to fix the burst water pipe by Jayson involves repairs done for work

purpose. The aim was to make the deterioration good that are caused through the wear

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

and tear. The work done by Jayson involved the replacement of subsidiary part of a whole

but does not involves the reconstruction of the entirety. Therefore, it is an allowable

deduction under section 25-10.

4

30 June 2019

and tear. The work done by Jayson involved the replacement of subsidiary part of a whole

but does not involves the reconstruction of the entirety. Therefore, it is an allowable

deduction under section 25-10.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

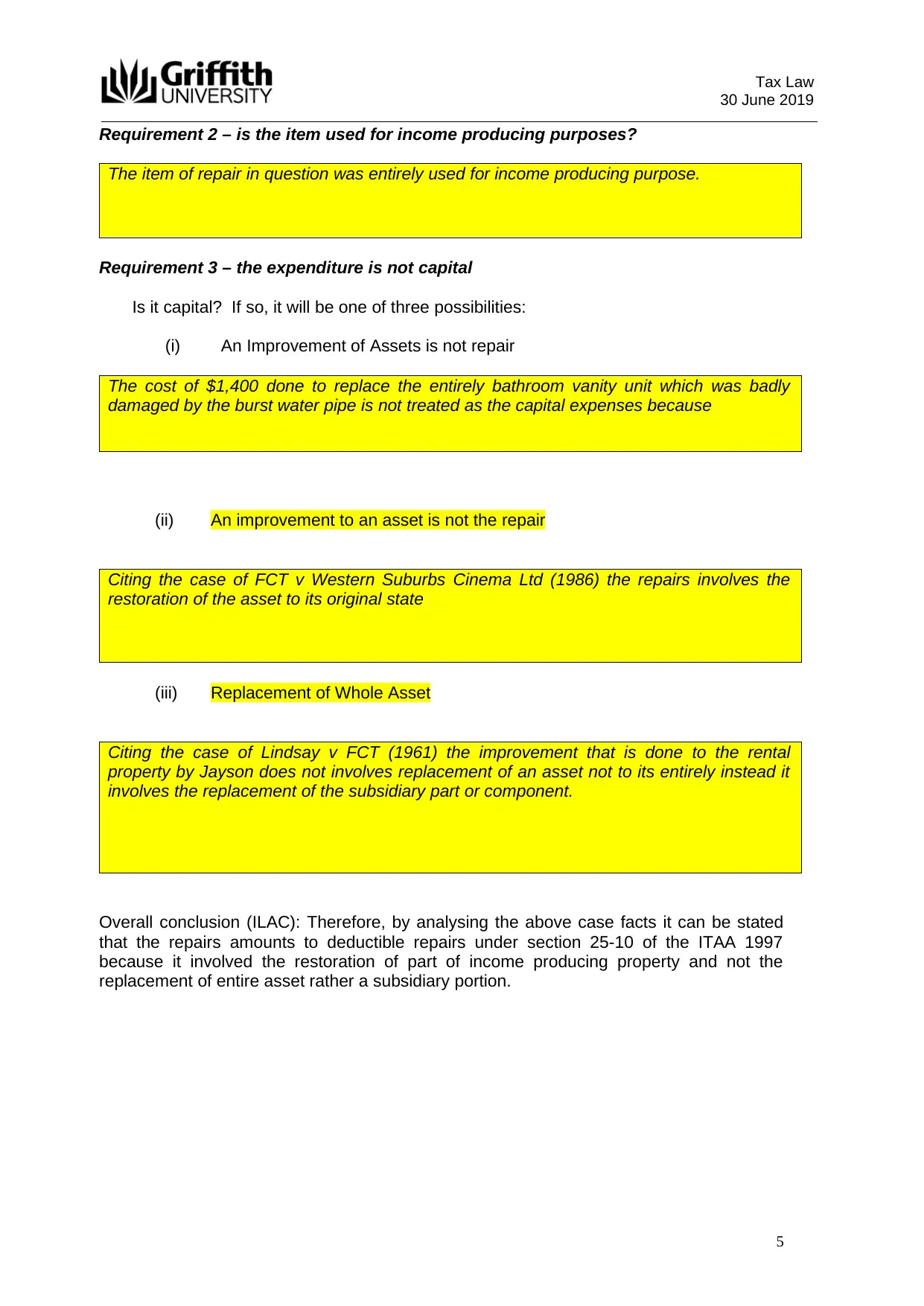

Requirement 2 – is the item used for income producing purposes?

The item of repair in question was entirely used for income producing purpose.

Requirement 3 – the expenditure is not capital

Is it capital? If so, it will be one of three possibilities:

(i) An Improvement of Assets is not repair

The cost of $1,400 done to replace the entirely bathroom vanity unit which was badly

damaged by the burst water pipe is not treated as the capital expenses because

(ii) An improvement to an asset is not the repair

Citing the case of FCT v Western Suburbs Cinema Ltd (1986) the repairs involves the

restoration of the asset to its original state

(iii) Replacement of Whole Asset

Citing the case of Lindsay v FCT (1961) the improvement that is done to the rental

property by Jayson does not involves replacement of an asset not to its entirely instead it

involves the replacement of the subsidiary part or component.

Overall conclusion (ILAC): Therefore, by analysing the above case facts it can be stated

that the repairs amounts to deductible repairs under section 25-10 of the ITAA 1997

because it involved the restoration of part of income producing property and not the

replacement of entire asset rather a subsidiary portion.

5

30 June 2019

Requirement 2 – is the item used for income producing purposes?

The item of repair in question was entirely used for income producing purpose.

Requirement 3 – the expenditure is not capital

Is it capital? If so, it will be one of three possibilities:

(i) An Improvement of Assets is not repair

The cost of $1,400 done to replace the entirely bathroom vanity unit which was badly

damaged by the burst water pipe is not treated as the capital expenses because

(ii) An improvement to an asset is not the repair

Citing the case of FCT v Western Suburbs Cinema Ltd (1986) the repairs involves the

restoration of the asset to its original state

(iii) Replacement of Whole Asset

Citing the case of Lindsay v FCT (1961) the improvement that is done to the rental

property by Jayson does not involves replacement of an asset not to its entirely instead it

involves the replacement of the subsidiary part or component.

Overall conclusion (ILAC): Therefore, by analysing the above case facts it can be stated

that the repairs amounts to deductible repairs under section 25-10 of the ITAA 1997

because it involved the restoration of part of income producing property and not the

replacement of entire asset rather a subsidiary portion.

5

Tax Law

30 June 2019

Jayson’s labour $450

Fixing the plumbing (burst water pipe) would amount to a revenue expenses but

deductions are or are not is allowed for capital costs (what the work would have cost):

“Day v Harland and Wolff (1953)”

Rubber seals $35

Here there has been revenue expenditure. Are the rubber seals a deductible to the burst

water pipes?

Note the 3 requirements for a deductible repair in section 25-10:

1. An individual is allowed to claim deduction for expenses occurred on repairs to

premises or the depreciating asset that held for generating assessable income.

2. If a taxpayer held the property or used the property only partially then one can

claim deduction for expenses up to the reasonable circumstances; and

3. No deduction is allowed under this section for capital expenses

Overall conclusion (ILAC): Therefore it can be stated that rubber seals are revenue

expenses and it is occurred entirely for the revenue producing asset. The expenses are

allowed for deduction under section 25-10, ITAA 1997.

6

30 June 2019

Jayson’s labour $450

Fixing the plumbing (burst water pipe) would amount to a revenue expenses but

deductions are or are not is allowed for capital costs (what the work would have cost):

“Day v Harland and Wolff (1953)”

Rubber seals $35

Here there has been revenue expenditure. Are the rubber seals a deductible to the burst

water pipes?

Note the 3 requirements for a deductible repair in section 25-10:

1. An individual is allowed to claim deduction for expenses occurred on repairs to

premises or the depreciating asset that held for generating assessable income.

2. If a taxpayer held the property or used the property only partially then one can

claim deduction for expenses up to the reasonable circumstances; and

3. No deduction is allowed under this section for capital expenses

Overall conclusion (ILAC): Therefore it can be stated that rubber seals are revenue

expenses and it is occurred entirely for the revenue producing asset. The expenses are

allowed for deduction under section 25-10, ITAA 1997.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

Chemical blower

The chemical blower would be a depreciating asset - has a 15 years of effective life and is

reasonably expected to decline in value: s 40-30.

Jayson owns the chemical blower so he holds it for the purpose of s 40-40.

He uses the chemical blower in rental property to produce assessable income so he has a

100% work purpose deduction: s 40-25(7).

Start time would be 1st October 2017, when Jayson first held for any purpose: s 40-60.

Calculate days: 622 days_

Cost: the acquisition costs (includes capital costs) and then any ongoing improvement

costs: ss 40-100 (1) . Here $

Effective life: under s 40-60 if using the Commissioner’s effective life, need to use the

ruling in force at the time acquired.

TR 2018/4 applied to assets acquired from 1 July 2017 to 30 June 2018 the effective

life of a chemical blower is 15 years

2017/18:

Post 9 May 2006 assets s 40-72

Base Value x Days Held x 200%

365 effective life

Decline in value for 2017/18 is:

Calculate decline in value for 2018 year? (why do you have do this when we are looking at

the 2019 year?)

30000 x 272 / 365 x 200% / 15 years = $2,981

2018/19

Calculate decline in value for 2019 year?

27019 x 273/365 x 200% / 15 years = $2,695

7

30 June 2019

Chemical blower

The chemical blower would be a depreciating asset - has a 15 years of effective life and is

reasonably expected to decline in value: s 40-30.

Jayson owns the chemical blower so he holds it for the purpose of s 40-40.

He uses the chemical blower in rental property to produce assessable income so he has a

100% work purpose deduction: s 40-25(7).

Start time would be 1st October 2017, when Jayson first held for any purpose: s 40-60.

Calculate days: 622 days_

Cost: the acquisition costs (includes capital costs) and then any ongoing improvement

costs: ss 40-100 (1) . Here $

Effective life: under s 40-60 if using the Commissioner’s effective life, need to use the

ruling in force at the time acquired.

TR 2018/4 applied to assets acquired from 1 July 2017 to 30 June 2018 the effective

life of a chemical blower is 15 years

2017/18:

Post 9 May 2006 assets s 40-72

Base Value x Days Held x 200%

365 effective life

Decline in value for 2017/18 is:

Calculate decline in value for 2018 year? (why do you have do this when we are looking at

the 2019 year?)

30000 x 272 / 365 x 200% / 15 years = $2,981

2018/19

Calculate decline in value for 2019 year?

27019 x 273/365 x 200% / 15 years = $2,695

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

(Assume the depreciation claimed on the chemical up to 15 June 2019 is $6,445)

On disposal – must calculate total days held. Section 40-102

Jayson stops ‘holding’ the depreciating asset (chemical blower) on 15 June 2019.

The termination value of a sold depreciating asset is $24,000: Section 40-300

Adjustable value means as the asset’s cost less the decline in value Section 40-85.

So we need to calculate the decline in value attributable to the chemical blower from the

start time on 1 October 2017 to the date of the balancing adjustment event on 15 June

2019.

So the adjustable value for the chemical blower will be:

Calculate adjustable value

30,000 x (622 days / 365 days) x (200% / 15) = $6,816

We need to compare the termination value to the adjustable value:

$24,000 (Termination value) [is < or >] $2,3184 (Adjustable value)

The difference of $816 will be carry forward under s 104-10 (4).

Therefore Jayson will need to in respect of the blower to quarantined the capital loss or

carry forward the loss.

8

30 June 2019

(Assume the depreciation claimed on the chemical up to 15 June 2019 is $6,445)

On disposal – must calculate total days held. Section 40-102

Jayson stops ‘holding’ the depreciating asset (chemical blower) on 15 June 2019.

The termination value of a sold depreciating asset is $24,000: Section 40-300

Adjustable value means as the asset’s cost less the decline in value Section 40-85.

So we need to calculate the decline in value attributable to the chemical blower from the

start time on 1 October 2017 to the date of the balancing adjustment event on 15 June

2019.

So the adjustable value for the chemical blower will be:

Calculate adjustable value

30,000 x (622 days / 365 days) x (200% / 15) = $6,816

We need to compare the termination value to the adjustable value:

$24,000 (Termination value) [is < or >] $2,3184 (Adjustable value)

The difference of $816 will be carry forward under s 104-10 (4).

Therefore Jayson will need to in respect of the blower to quarantined the capital loss or

carry forward the loss.

8

Tax Law

30 June 2019

Question 2

Ben is an area manager for a retail chain. He needs to travel frequently between the head

office, the warehouse, and the retail stores in the area. His employer does not provide him

with a vehicle, but gives him a car allowance of $5,000 per year.

Ben leased a BMW car (engine size 2700CC) valued at $52,000 on 1 February 2019. It

has a 2.7 litre engine. He kept a logbook that showed that his travel from 1 February

2019 to 30 June 2019 consisted of the following:

1,400 km travelling between home and his office

400 km travelling between home and Woolworths to buy personal groceries

5,300 km travelling from his office to the warehouse and/or the retail stores, and

back again.

He incurred the following car expenses (which he can substantiate):

- Registration $ 700

- Insurance $1,300

- Fuel $2,400

- Lease $5,600

a) What would be his deduction for car expenses under Div 28 ITAA 97 for the

2018/19 income year? Which method should he claim under?

Ben is an employee so he must calculate his car expenses under Division 28 ITAA97

Ben’s business kms will be 5300 km – which represents the distance he travelled from

his office to the warehouse and retail stores.

Which travel is not business kilometres? Discuss with reference to case law.

Travelling from home to office and travel between home and Woolworths to purchase

personal groceries.

9

30 June 2019

Question 2

Ben is an area manager for a retail chain. He needs to travel frequently between the head

office, the warehouse, and the retail stores in the area. His employer does not provide him

with a vehicle, but gives him a car allowance of $5,000 per year.

Ben leased a BMW car (engine size 2700CC) valued at $52,000 on 1 February 2019. It

has a 2.7 litre engine. He kept a logbook that showed that his travel from 1 February

2019 to 30 June 2019 consisted of the following:

1,400 km travelling between home and his office

400 km travelling between home and Woolworths to buy personal groceries

5,300 km travelling from his office to the warehouse and/or the retail stores, and

back again.

He incurred the following car expenses (which he can substantiate):

- Registration $ 700

- Insurance $1,300

- Fuel $2,400

- Lease $5,600

a) What would be his deduction for car expenses under Div 28 ITAA 97 for the

2018/19 income year? Which method should he claim under?

Ben is an employee so he must calculate his car expenses under Division 28 ITAA97

Ben’s business kms will be 5300 km – which represents the distance he travelled from

his office to the warehouse and retail stores.

Which travel is not business kilometres? Discuss with reference to case law.

Travelling from home to office and travel between home and Woolworths to purchase

personal groceries.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

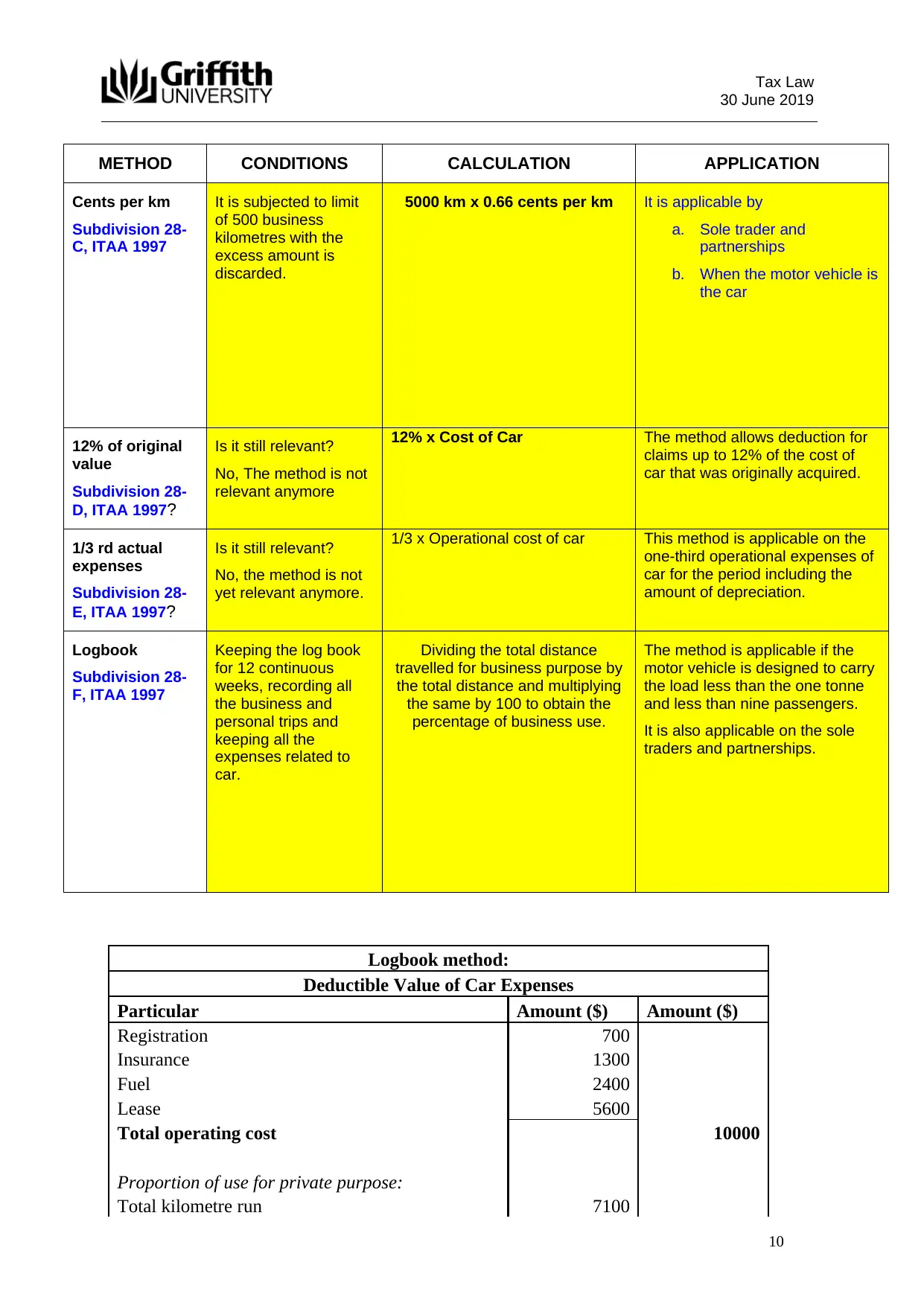

METHOD CONDITIONS CALCULATION APPLICATION

Cents per km

Subdivision 28-

C, ITAA 1997

It is subjected to limit

of 500 business

kilometres with the

excess amount is

discarded.

5000 km x 0.66 cents per km It is applicable by

a. Sole trader and

partnerships

b. When the motor vehicle is

the car

12% of original

value

Subdivision 28-

D, ITAA 1997?

Is it still relevant?

No, The method is not

relevant anymore

12% x Cost of Car The method allows deduction for

claims up to 12% of the cost of

car that was originally acquired.

1/3 rd actual

expenses

Subdivision 28-

E, ITAA 1997?

Is it still relevant?

No, the method is not

yet relevant anymore.

1/3 x Operational cost of car This method is applicable on the

one-third operational expenses of

car for the period including the

amount of depreciation.

Logbook

Subdivision 28-

F, ITAA 1997

Keeping the log book

for 12 continuous

weeks, recording all

the business and

personal trips and

keeping all the

expenses related to

car.

Dividing the total distance

travelled for business purpose by

the total distance and multiplying

the same by 100 to obtain the

percentage of business use.

The method is applicable if the

motor vehicle is designed to carry

the load less than the one tonne

and less than nine passengers.

It is also applicable on the sole

traders and partnerships.

Logbook method:

Deductible Value of Car Expenses

Particular Amount ($) Amount ($)

Registration 700

Insurance 1300

Fuel 2400

Lease 5600

Total operating cost 10000

Proportion of use for private purpose:

Total kilometre run 7100

10

30 June 2019

METHOD CONDITIONS CALCULATION APPLICATION

Cents per km

Subdivision 28-

C, ITAA 1997

It is subjected to limit

of 500 business

kilometres with the

excess amount is

discarded.

5000 km x 0.66 cents per km It is applicable by

a. Sole trader and

partnerships

b. When the motor vehicle is

the car

12% of original

value

Subdivision 28-

D, ITAA 1997?

Is it still relevant?

No, The method is not

relevant anymore

12% x Cost of Car The method allows deduction for

claims up to 12% of the cost of

car that was originally acquired.

1/3 rd actual

expenses

Subdivision 28-

E, ITAA 1997?

Is it still relevant?

No, the method is not

yet relevant anymore.

1/3 x Operational cost of car This method is applicable on the

one-third operational expenses of

car for the period including the

amount of depreciation.

Logbook

Subdivision 28-

F, ITAA 1997

Keeping the log book

for 12 continuous

weeks, recording all

the business and

personal trips and

keeping all the

expenses related to

car.

Dividing the total distance

travelled for business purpose by

the total distance and multiplying

the same by 100 to obtain the

percentage of business use.

The method is applicable if the

motor vehicle is designed to carry

the load less than the one tonne

and less than nine passengers.

It is also applicable on the sole

traders and partnerships.

Logbook method:

Deductible Value of Car Expenses

Particular Amount ($) Amount ($)

Registration 700

Insurance 1300

Fuel 2400

Lease 5600

Total operating cost 10000

Proportion of use for private purpose:

Total kilometre run 7100

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

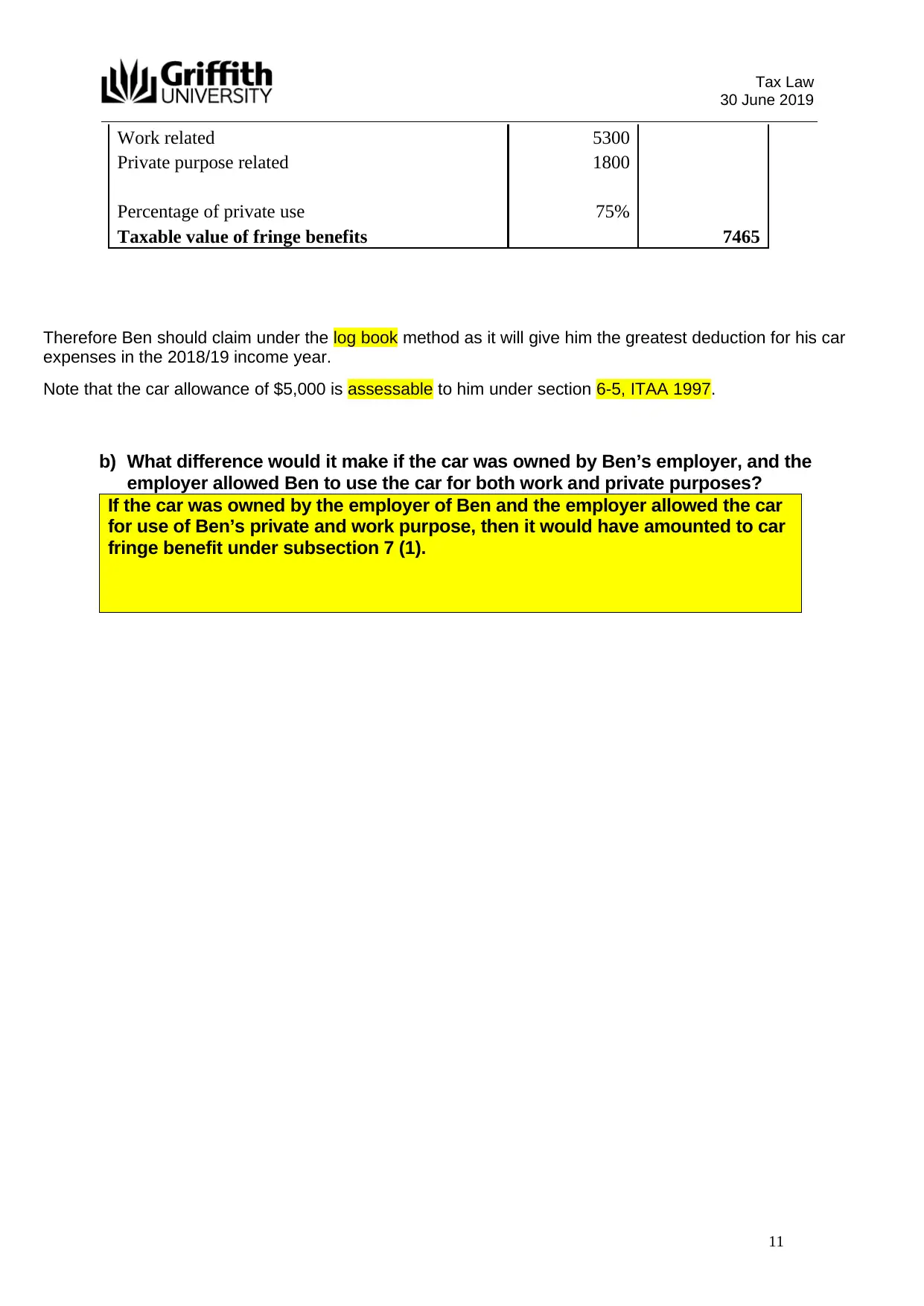

Work related 5300

Private purpose related 1800

Percentage of private use 75%

Taxable value of fringe benefits 7465

Therefore Ben should claim under the log book method as it will give him the greatest deduction for his car

expenses in the 2018/19 income year.

Note that the car allowance of $5,000 is assessable to him under section 6-5, ITAA 1997.

b) What difference would it make if the car was owned by Ben’s employer, and the

employer allowed Ben to use the car for both work and private purposes?

If the car was owned by the employer of Ben and the employer allowed the car

for use of Ben’s private and work purpose, then it would have amounted to car

fringe benefit under subsection 7 (1).

11

30 June 2019

Work related 5300

Private purpose related 1800

Percentage of private use 75%

Taxable value of fringe benefits 7465

Therefore Ben should claim under the log book method as it will give him the greatest deduction for his car

expenses in the 2018/19 income year.

Note that the car allowance of $5,000 is assessable to him under section 6-5, ITAA 1997.

b) What difference would it make if the car was owned by Ben’s employer, and the

employer allowed Ben to use the car for both work and private purposes?

If the car was owned by the employer of Ben and the employer allowed the car

for use of Ben’s private and work purpose, then it would have amounted to car

fringe benefit under subsection 7 (1).

11

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.