Janice Brown’s “net capital gain

Calculate Janice Brown's net capital gain for the 2018/19 income year.

9 Pages2065 Words13 Views

Added on 2022-09-08

Janice Brown’s “net capital gain

Calculate Janice Brown's net capital gain for the 2018/19 income year.

Added on 2022-09-08

ShareRelated Documents

Tax Law

30 June 2019

Seminar Number 7

Question 1

You are required to just calculate Janice Brown’s “net capital gain” for the 2018/19 income

year. Assume Janice is not entitled to use any of the small business concessions in Division 152

ITAA 1997.

In addition to the transactions listed below, Janice also received salary income of $150,000 in

the 2018/19 and an unfranked divided of $3,000 from BHP shares. Janice also has carried

forward capital losses from:

the sale of a coin collection of $3,500, and

the sale of shares in Rio Tinto of $10,000

Janice had the following capital gains and/or losses (prior to considering any capital losses,

indexation method or discount method

Initial capital loss of $7,000 on Jet Ski (acquired 3 March 2014; disposed 12 June 2019);

Initial exempt capital gain of $1150 on a Painting (acquired 19 May 1990; disposed 12

June 2019);

Initial capital gain of $1,200 on Rare Book (acquired 5 April 2003; disposed 12 June

2019); and

Initial capital gain of $159,900 on Investment House (acquired 16 October 2010;

disposed 12 May 2019)

Initial capital gain of $340,000 on Telstra Shares (acquired 16 July 2016; disposed 6

April 2019).

Rainbow Bay Property

Janice signed a contract to purchase a house (on 0.2 hectares) at 19 Finders Street Rainbow

Bay on the Gold Coast on 15 August 2008 for $350,000. Ownership transferred to her on 15

September 2008. Janice lived in Rainbow Bay Property as her home from the 15th September

2008 until to 20th November 2014.

On 21st November 2014, Janice decided to move to Brisbane so that her children could attend

an exclusive private school. She rented the Rainbow Bay house to tenants from the 21st

November 2014 and received approximately $35,000 per year in rent. The family moved into an

apartment at Kangaroo Point which they rented through a local real estate agent.

In April 2019 Janice decided that her family had settled well into the Brisbane lifestyle and as a

result she would buy a home in Brisbane. As a consequence, she had to sell the Rainbow Bay

house to fund the purchase. She placed the property on the market and sold the Rainbow Bay

house for $800,000 under a contract dated 13 June 2019. In relation to the sale, she paid a

$16,000 commission to the real estate agent and $2,500 in legal fees to her lawyer. The

ownership of the Rainbow Bay house transferred to the new owner on 13 July 2019.

1

30 June 2019

Seminar Number 7

Question 1

You are required to just calculate Janice Brown’s “net capital gain” for the 2018/19 income

year. Assume Janice is not entitled to use any of the small business concessions in Division 152

ITAA 1997.

In addition to the transactions listed below, Janice also received salary income of $150,000 in

the 2018/19 and an unfranked divided of $3,000 from BHP shares. Janice also has carried

forward capital losses from:

the sale of a coin collection of $3,500, and

the sale of shares in Rio Tinto of $10,000

Janice had the following capital gains and/or losses (prior to considering any capital losses,

indexation method or discount method

Initial capital loss of $7,000 on Jet Ski (acquired 3 March 2014; disposed 12 June 2019);

Initial exempt capital gain of $1150 on a Painting (acquired 19 May 1990; disposed 12

June 2019);

Initial capital gain of $1,200 on Rare Book (acquired 5 April 2003; disposed 12 June

2019); and

Initial capital gain of $159,900 on Investment House (acquired 16 October 2010;

disposed 12 May 2019)

Initial capital gain of $340,000 on Telstra Shares (acquired 16 July 2016; disposed 6

April 2019).

Rainbow Bay Property

Janice signed a contract to purchase a house (on 0.2 hectares) at 19 Finders Street Rainbow

Bay on the Gold Coast on 15 August 2008 for $350,000. Ownership transferred to her on 15

September 2008. Janice lived in Rainbow Bay Property as her home from the 15th September

2008 until to 20th November 2014.

On 21st November 2014, Janice decided to move to Brisbane so that her children could attend

an exclusive private school. She rented the Rainbow Bay house to tenants from the 21st

November 2014 and received approximately $35,000 per year in rent. The family moved into an

apartment at Kangaroo Point which they rented through a local real estate agent.

In April 2019 Janice decided that her family had settled well into the Brisbane lifestyle and as a

result she would buy a home in Brisbane. As a consequence, she had to sell the Rainbow Bay

house to fund the purchase. She placed the property on the market and sold the Rainbow Bay

house for $800,000 under a contract dated 13 June 2019. In relation to the sale, she paid a

$16,000 commission to the real estate agent and $2,500 in legal fees to her lawyer. The

ownership of the Rainbow Bay house transferred to the new owner on 13 July 2019.

1

Tax Law

30 June 2019

Springwood Property

On 10 January 1984 Janice Brown purchased a block of land for $20,000 in

Springwood on which to build a house. After receiving many quotations, Janice signed a

contract on 21 April 1988 with Construct with Us Pty Ltd to construct the house. The

house construction began on 1 July 1988 and was completed on the 31st October 1988 at

a cost of $95,000.

Instead of moving into the house, Janice rented it out to tenants. She continued to do this

until she eventually sold the property for $720,000 under a contract dated 11 June 2019

with the ownership transferring on 11 July 2019. An independent valuation revealed that

the land was worth $550,000 at the time of sale. (Hint! Could the house be considered

as separate asset to the land?)

===================

2

30 June 2019

Springwood Property

On 10 January 1984 Janice Brown purchased a block of land for $20,000 in

Springwood on which to build a house. After receiving many quotations, Janice signed a

contract on 21 April 1988 with Construct with Us Pty Ltd to construct the house. The

house construction began on 1 July 1988 and was completed on the 31st October 1988 at

a cost of $95,000.

Instead of moving into the house, Janice rented it out to tenants. She continued to do this

until she eventually sold the property for $720,000 under a contract dated 11 June 2019

with the ownership transferring on 11 July 2019. An independent valuation revealed that

the land was worth $550,000 at the time of sale. (Hint! Could the house be considered

as separate asset to the land?)

===================

2

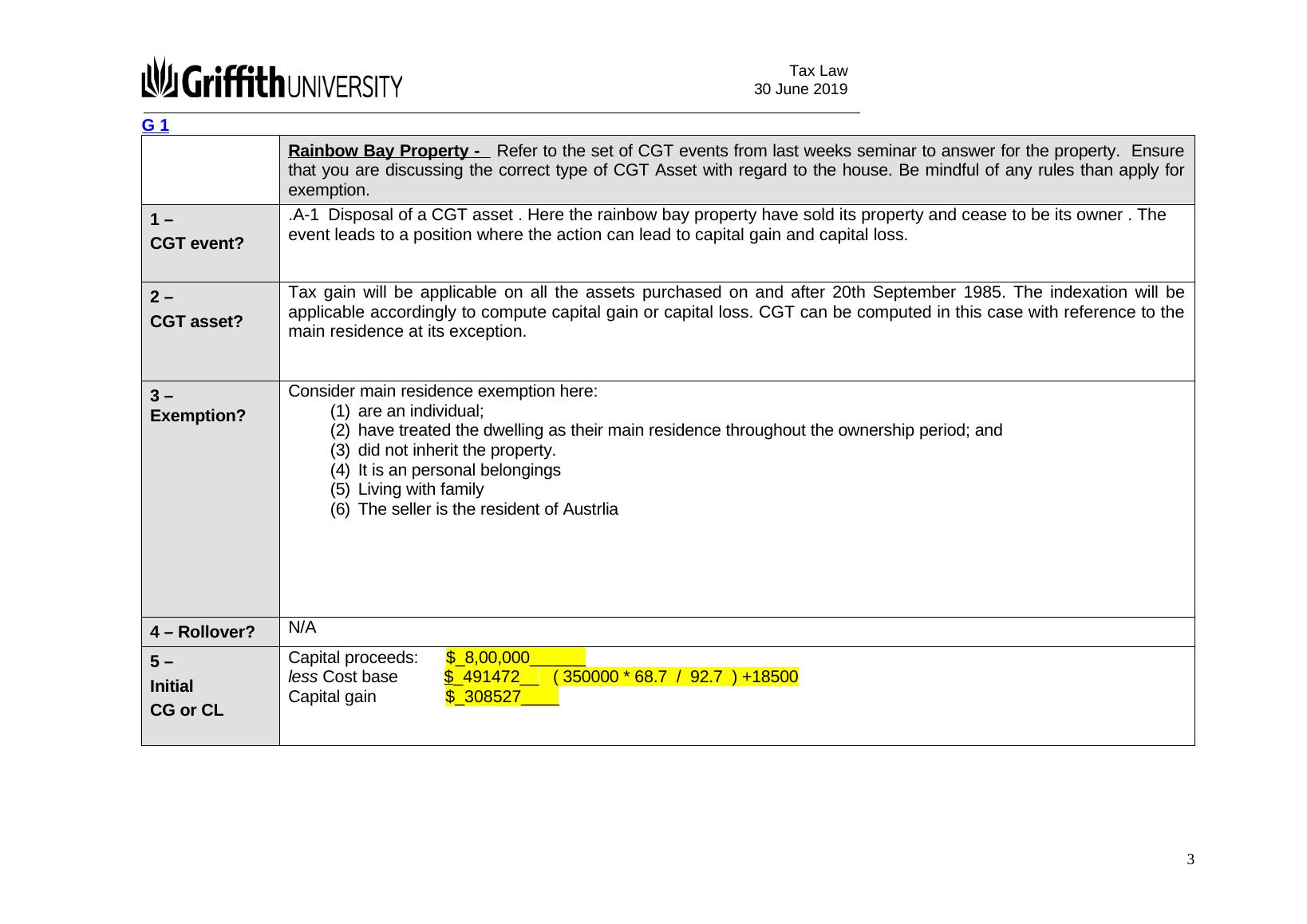

Tax Law

30 June 2019

G 1

Rainbow Bay Property - Refer to the set of CGT events from last weeks seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

.A-1 Disposal of a CGT asset . Here the rainbow bay property have sold its property and cease to be its owner . The

event leads to a position where the action can lead to capital gain and capital loss.

2 –

CGT asset?

Tax gain will be applicable on all the assets purchased on and after 20th September 1985. The indexation will be

applicable accordingly to compute capital gain or capital loss. CGT can be computed in this case with reference to the

main residence at its exception.

3 –

Exemption?

Consider main residence exemption here:

(1) are an individual;

(2) have treated the dwelling as their main residence throughout the ownership period; and

(3) did not inherit the property.

(4) It is an personal belongings

(5) Living with family

(6) The seller is the resident of Austrlia

4 – Rollover? N/A

5 –

Initial

CG or CL

Capital proceeds: $_8,00,000______

less Cost base $_491472__ ( 350000 * 68.7 / 92.7 ) +18500

Capital gain $_308527____

3

30 June 2019

G 1

Rainbow Bay Property - Refer to the set of CGT events from last weeks seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

.A-1 Disposal of a CGT asset . Here the rainbow bay property have sold its property and cease to be its owner . The

event leads to a position where the action can lead to capital gain and capital loss.

2 –

CGT asset?

Tax gain will be applicable on all the assets purchased on and after 20th September 1985. The indexation will be

applicable accordingly to compute capital gain or capital loss. CGT can be computed in this case with reference to the

main residence at its exception.

3 –

Exemption?

Consider main residence exemption here:

(1) are an individual;

(2) have treated the dwelling as their main residence throughout the ownership period; and

(3) did not inherit the property.

(4) It is an personal belongings

(5) Living with family

(6) The seller is the resident of Austrlia

4 – Rollover? N/A

5 –

Initial

CG or CL

Capital proceeds: $_8,00,000______

less Cost base $_491472__ ( 350000 * 68.7 / 92.7 ) +18500

Capital gain $_308527____

3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Calculating Janice Brown's Net Capital Gain for 2018/19 Income Yearlg...

|13

|2478

|427

Calculating Janice's Net Capital Gain in Tax Lawlg...

|9

|1841

|78

Calculating Janice's Net Capital Gain for the 2018/19 Income Yearlg...

|9

|1859

|72

Tax Law Assignment Assesmentslg...

|11

|2039

|13

Tax Assignment Question Answer 2022lg...

|14

|3806

|14