Tax Law Assignment: Taxation of Patent Infringement and Land Sale

VerifiedAdded on 2023/01/03

|16

|4674

|81

Homework Assignment

AI Summary

This assignment analyzes two key tax law questions. The first question focuses on Our Earth Pty Ltd, a company that received compensation for patent infringement and lost revenue. The assignment examines whether the compensation for patent infringement is taxable, considering its capital nature, and whether the lost revenue and interest received are assessable income. It also considers the tax treatment of reimbursed legal fees. The second question addresses the sale of land, determining if the land is a pre-CGT asset and whether the sale of subdivided land constitutes carrying on a business, impacting how profits are assessed under section 25(1) of the ITAA 1936. The assignment applies relevant case law and legislation to determine the tax implications of these scenarios, providing a detailed analysis of assessable income, capital gains tax, and relevant tax provisions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1.................................................................................................................2

Issues......................................................................................................................................2

Rules.......................................................................................................................................2

Application.............................................................................................................................4

Conclusion..................................................................................................................................6

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................9

Conclusion:..........................................................................................................................12

Reference..................................................................................................................................13

Table of Contents

Answer to Question 1.................................................................................................................2

Issues......................................................................................................................................2

Rules.......................................................................................................................................2

Application.............................................................................................................................4

Conclusion..................................................................................................................................6

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................9

Conclusion:..........................................................................................................................12

Reference..................................................................................................................................13

2TAXATION LAW

Answer to Question 1

Issues

Is the amount $ 300,000 which is received by the taxpayer as compensation damage

for breach of rights of patents be considered taxable?

Will the taxpayer be held liable for tax considering ordinary concepts of “section 6-5,

ITAA 1936” for the loss of income due to breach of patent rights?

Will the taxpayer be considered liable for the interest which is received for successful

outcome of the judicial case as per “section 6-5, ITAA 1936”?

Will reimbursement of legal expenses be considered in assessable income?

Rules

Any amount which is received for partial damage caused to the assets or effective

operations of asset or for some revenue generating activities would then be considered as

capital receipts. As per the opinion of the court in the case “Glenboig Union Fireclay Co Ltd

v IRC (1921)” the nature of the payment which was made as compensation was made for the

loss of capital asset and how the same was used (Bankman et al., 2018). The amount which

was received represents profits for the business and was considered to be immaterial in

nature.

In general taxation rulings when a taxpayer receives payments which is compensation

for some in lumpsum that the same can be considered as ordinary income of capital receipts

judging from the nature of the payment. It was held in the case of “Federal Wharf Co Ltd v

FCT” that the compensation which was received was to be held as income provided that the

same was received in lumpsum and for some losses which is incurred (Murphy & Lederman,

2018). The term compensatory payments reflects any payments which is received for right of

seeking compensation or as a result of cause of action bought forward by the taxpayer for any

Answer to Question 1

Issues

Is the amount $ 300,000 which is received by the taxpayer as compensation damage

for breach of rights of patents be considered taxable?

Will the taxpayer be held liable for tax considering ordinary concepts of “section 6-5,

ITAA 1936” for the loss of income due to breach of patent rights?

Will the taxpayer be considered liable for the interest which is received for successful

outcome of the judicial case as per “section 6-5, ITAA 1936”?

Will reimbursement of legal expenses be considered in assessable income?

Rules

Any amount which is received for partial damage caused to the assets or effective

operations of asset or for some revenue generating activities would then be considered as

capital receipts. As per the opinion of the court in the case “Glenboig Union Fireclay Co Ltd

v IRC (1921)” the nature of the payment which was made as compensation was made for the

loss of capital asset and how the same was used (Bankman et al., 2018). The amount which

was received represents profits for the business and was considered to be immaterial in

nature.

In general taxation rulings when a taxpayer receives payments which is compensation

for some in lumpsum that the same can be considered as ordinary income of capital receipts

judging from the nature of the payment. It was held in the case of “Federal Wharf Co Ltd v

FCT” that the compensation which was received was to be held as income provided that the

same was received in lumpsum and for some losses which is incurred (Murphy & Lederman,

2018). The term compensatory payments reflects any payments which is received for right of

seeking compensation or as a result of cause of action bought forward by the taxpayer for any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

underlying asset. The amount of compensatory payment would be considered as income

eligible for tax under “Division 6 of the ITAA 1997” or the same can also be treated as

statutory income for the purpose of tax.

It is clearly stated in “section 25 (1), ITAA 1997” that compensation payments which

is received by taxpayers for loss of income during the previous years would be considered for

taxation under Australian law (Braithwaite, 2017). This provision can be tested in the case

laws of “Mc Laurin v FC of T (1961)” where judgement was passed that sum of

compensation which was received was held as taxable income under “subsection 25 (1),

ITAA 1936” to the extent that the income is appropriately recognizable.

In many situations, it has been noticed that taxpayers try to get compensations for any

loss which is caused to their capital assets. In general scenarios, the compensation which is

received for loss caused to an asset or changes in terms of contract or termination of contract

are considered to be income generated from ordinary income (Jones & Rhoades-Catanach,

2015). It is therefore this reason the compensation which is derived due to loss of income

would be considered as just substitute income of lost earnings.

As per the verdict of the federal commissioner in “Californian Oil Products Ltd v

FCT (1934)” held that the compensation which is received by taxpayer for substitutes for

normal income would be treated as ordinary income under “section 6-5, ITAA 1997”

(Braithwaite et al., 2017). The income was derived in uncertain circumstances but the same

was within the scope of normal business activities.

In another case which was filed under the federal court “CT (Vic) v Phillips (1936)”,

verdict was provided that receipt of any compensation for any damages that is closely

associated with business loss and is related to the close business activities then such

compensation would be regarded as loss caused to capital asset (Sharkey, & Murray, 2016).

underlying asset. The amount of compensatory payment would be considered as income

eligible for tax under “Division 6 of the ITAA 1997” or the same can also be treated as

statutory income for the purpose of tax.

It is clearly stated in “section 25 (1), ITAA 1997” that compensation payments which

is received by taxpayers for loss of income during the previous years would be considered for

taxation under Australian law (Braithwaite, 2017). This provision can be tested in the case

laws of “Mc Laurin v FC of T (1961)” where judgement was passed that sum of

compensation which was received was held as taxable income under “subsection 25 (1),

ITAA 1936” to the extent that the income is appropriately recognizable.

In many situations, it has been noticed that taxpayers try to get compensations for any

loss which is caused to their capital assets. In general scenarios, the compensation which is

received for loss caused to an asset or changes in terms of contract or termination of contract

are considered to be income generated from ordinary income (Jones & Rhoades-Catanach,

2015). It is therefore this reason the compensation which is derived due to loss of income

would be considered as just substitute income of lost earnings.

As per the verdict of the federal commissioner in “Californian Oil Products Ltd v

FCT (1934)” held that the compensation which is received by taxpayer for substitutes for

normal income would be treated as ordinary income under “section 6-5, ITAA 1997”

(Braithwaite et al., 2017). The income was derived in uncertain circumstances but the same

was within the scope of normal business activities.

In another case which was filed under the federal court “CT (Vic) v Phillips (1936)”,

verdict was provided that receipt of any compensation for any damages that is closely

associated with business loss and is related to the close business activities then such

compensation would be regarded as loss caused to capital asset (Sharkey, & Murray, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

In a similar case law of “FCT v Spedley Securities Ltd (1988)” decision was provided that

compensation received for loss of business goodwill was considered as capital receipts in

nature.

In case the taxpayer receives interest as compensation for losses than the same would

be considered as assessable under the legislations of “section 6-5, ITAA 1997”. In the case of

“Whitaker v DFCT (1998)” verdict was given that post-judgement interest would be treated

as ordinary income under “section 6-5, ITAA 1997” (Lymer & Hasseldine, 2014). The

amount which is received as interest by the taxpayer for compensation due to loss would be

treated as ordinary income considering the period that was ascertainable and outstanding

(Basu, 2016).

The taxpayer is also eligible for claiming deduction for the purpose of tax considering

the provisions which are stated under “section 8-1 of the ITAA 1997” and then the same

amount that is paid or awarded relating to the legal expenses would also be included in

assessable income under the provisions of “subdivision 20-A”. The payments which is

received for legal proceedings is mainly for indemnifying the receiver for the expenses

occurred on the legal proceedings (Braithwaite & Reinhart, 2019). The legal fees which is

received by the taxpayer would not be considered as ordinary income in ordinary concepts

but the same would be considered as assessable recoupment within the “subsection 20-20

(2)”.

Application

The company which is considered in the case study is Our Earth Pty Ltd, reflects a

business which is engaged in the business of producing and designing coffee cups. The

special feature of the company is that it uses biodegradable materials for producing the cups.

It came to the attention of Our Earth Pty Ltd that Coffee Beans Pty Ltd has copied the design

In a similar case law of “FCT v Spedley Securities Ltd (1988)” decision was provided that

compensation received for loss of business goodwill was considered as capital receipts in

nature.

In case the taxpayer receives interest as compensation for losses than the same would

be considered as assessable under the legislations of “section 6-5, ITAA 1997”. In the case of

“Whitaker v DFCT (1998)” verdict was given that post-judgement interest would be treated

as ordinary income under “section 6-5, ITAA 1997” (Lymer & Hasseldine, 2014). The

amount which is received as interest by the taxpayer for compensation due to loss would be

treated as ordinary income considering the period that was ascertainable and outstanding

(Basu, 2016).

The taxpayer is also eligible for claiming deduction for the purpose of tax considering

the provisions which are stated under “section 8-1 of the ITAA 1997” and then the same

amount that is paid or awarded relating to the legal expenses would also be included in

assessable income under the provisions of “subdivision 20-A”. The payments which is

received for legal proceedings is mainly for indemnifying the receiver for the expenses

occurred on the legal proceedings (Braithwaite & Reinhart, 2019). The legal fees which is

received by the taxpayer would not be considered as ordinary income in ordinary concepts

but the same would be considered as assessable recoupment within the “subsection 20-20

(2)”.

Application

The company which is considered in the case study is Our Earth Pty Ltd, reflects a

business which is engaged in the business of producing and designing coffee cups. The

special feature of the company is that it uses biodegradable materials for producing the cups.

It came to the attention of Our Earth Pty Ltd that Coffee Beans Pty Ltd has copied the design

5TAXATION LAW

of coffee cups from Our Earth Pty Ltd which is causing losses to the business. The

management of Coffee Beans Pty Ltd has effectively offered the products to overseas

markets and that too at a lower price. The management of Our Earth Pty Ltd decided to file

legal suits where a sum of $ 300,000 was recovered from Coffee Beans Pty Ltd as

compensation for breach of patent rights. The first step to ascertain whether the compensation

would be included in assessable income is to identify the nature of the receipts. The decision

which was made in the case of “CT (Vic) v Phillips (1936)” is applied which shows that $

300,000 is received by the business as loss caused to business and can be mainly treated as an

attempt to cause injury to the asset (Novak, 2018). The compensation amount which is

received is for the breach of patents and therefore the nature of the receipt is of capital nature

and cannot be held as taxable income.

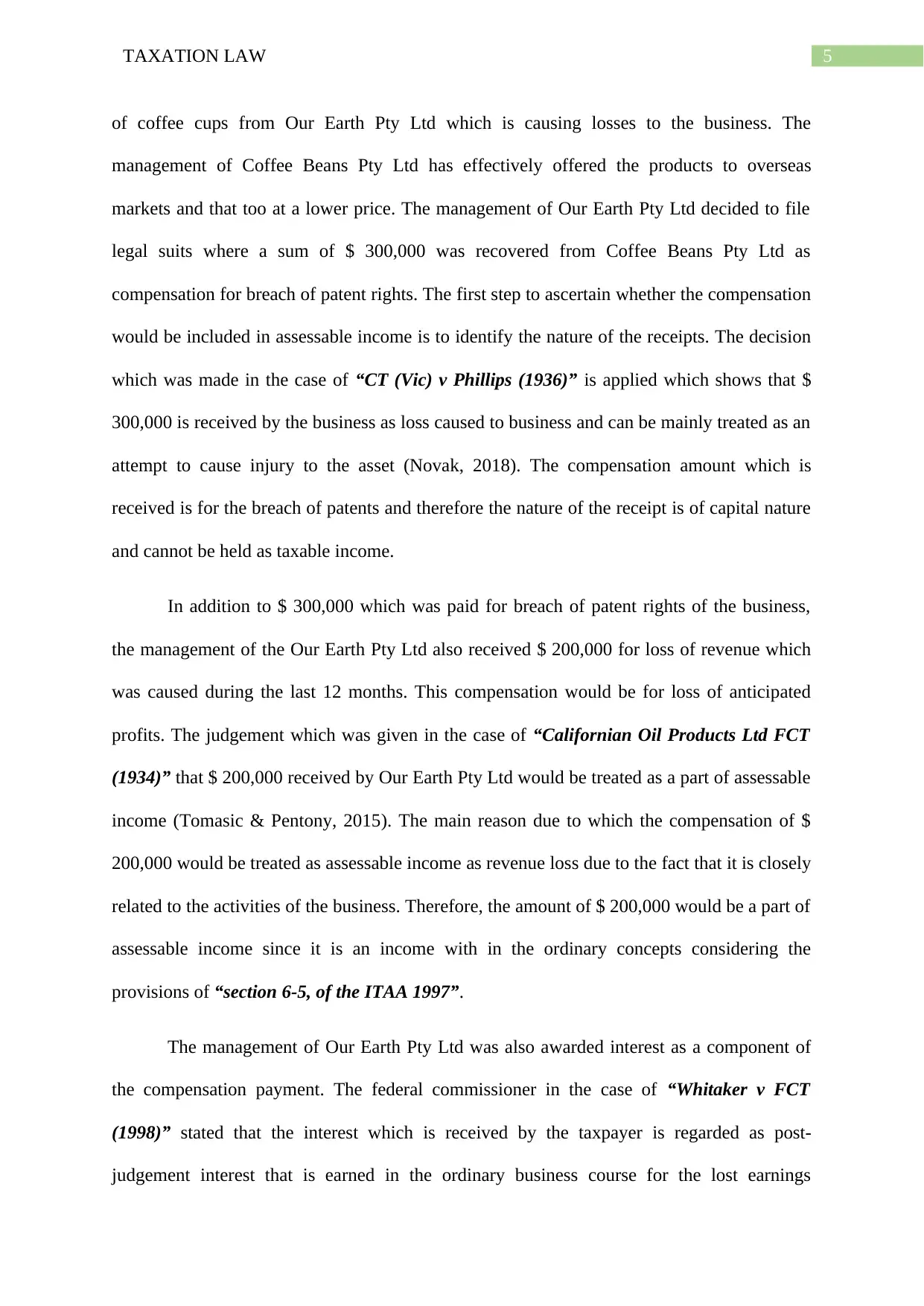

In addition to $ 300,000 which was paid for breach of patent rights of the business,

the management of the Our Earth Pty Ltd also received $ 200,000 for loss of revenue which

was caused during the last 12 months. This compensation would be for loss of anticipated

profits. The judgement which was given in the case of “Californian Oil Products Ltd FCT

(1934)” that $ 200,000 received by Our Earth Pty Ltd would be treated as a part of assessable

income (Tomasic & Pentony, 2015). The main reason due to which the compensation of $

200,000 would be treated as assessable income as revenue loss due to the fact that it is closely

related to the activities of the business. Therefore, the amount of $ 200,000 would be a part of

assessable income since it is an income with in the ordinary concepts considering the

provisions of “section 6-5, of the ITAA 1997”.

The management of Our Earth Pty Ltd was also awarded interest as a component of

the compensation payment. The federal commissioner in the case of “Whitaker v FCT

(1998)” stated that the interest which is received by the taxpayer is regarded as post-

judgement interest that is earned in the ordinary business course for the lost earnings

of coffee cups from Our Earth Pty Ltd which is causing losses to the business. The

management of Coffee Beans Pty Ltd has effectively offered the products to overseas

markets and that too at a lower price. The management of Our Earth Pty Ltd decided to file

legal suits where a sum of $ 300,000 was recovered from Coffee Beans Pty Ltd as

compensation for breach of patent rights. The first step to ascertain whether the compensation

would be included in assessable income is to identify the nature of the receipts. The decision

which was made in the case of “CT (Vic) v Phillips (1936)” is applied which shows that $

300,000 is received by the business as loss caused to business and can be mainly treated as an

attempt to cause injury to the asset (Novak, 2018). The compensation amount which is

received is for the breach of patents and therefore the nature of the receipt is of capital nature

and cannot be held as taxable income.

In addition to $ 300,000 which was paid for breach of patent rights of the business,

the management of the Our Earth Pty Ltd also received $ 200,000 for loss of revenue which

was caused during the last 12 months. This compensation would be for loss of anticipated

profits. The judgement which was given in the case of “Californian Oil Products Ltd FCT

(1934)” that $ 200,000 received by Our Earth Pty Ltd would be treated as a part of assessable

income (Tomasic & Pentony, 2015). The main reason due to which the compensation of $

200,000 would be treated as assessable income as revenue loss due to the fact that it is closely

related to the activities of the business. Therefore, the amount of $ 200,000 would be a part of

assessable income since it is an income with in the ordinary concepts considering the

provisions of “section 6-5, of the ITAA 1997”.

The management of Our Earth Pty Ltd was also awarded interest as a component of

the compensation payment. The federal commissioner in the case of “Whitaker v FCT

(1998)” stated that the interest which is received by the taxpayer is regarded as post-

judgement interest that is earned in the ordinary business course for the lost earnings

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

(Woellner et al., 2016). The income which is generated from interest would be included

within the meaning of “section 6-5, ITAA 1997” for assessment purpose.

The taxpayer which is Our Earth Pty Ltd also received legal fees which was received

in the form of reimbursement. The legal fees amount was received along with compensation

for the successful party. Therefore, it can be said that the amount which is received by Our

Earth Pty Ltd would be included in the assessable income of the business under the

legislation of “subdivision 20-A”.

Conclusion

The analysis which is conducted above effectively shows that the case of Our Earth

Pty Ltd where the business has incurred losses due to infringement of patent rights of the

business. The amount of $ 300,000 which is received for breach of patent rights would be

treated as receipt of capital nature and therefore is not subjected for tax under the legislation.

In addition to this, the management of Our Earth Pty Ltd also received $ 200,000 which is for

loss of revenue during the last 12 months period and the same would be considered as taxable

income. In addition to this post-judgement interest should also be incorporated in taxable

income within the ordinary meaning of section 6-5, ITAA 1997. The legal fees would also be

included in the assessable income of the business under the provisions of “subdivision 20-A”.

(Woellner et al., 2016). The income which is generated from interest would be included

within the meaning of “section 6-5, ITAA 1997” for assessment purpose.

The taxpayer which is Our Earth Pty Ltd also received legal fees which was received

in the form of reimbursement. The legal fees amount was received along with compensation

for the successful party. Therefore, it can be said that the amount which is received by Our

Earth Pty Ltd would be included in the assessable income of the business under the

legislation of “subdivision 20-A”.

Conclusion

The analysis which is conducted above effectively shows that the case of Our Earth

Pty Ltd where the business has incurred losses due to infringement of patent rights of the

business. The amount of $ 300,000 which is received for breach of patent rights would be

treated as receipt of capital nature and therefore is not subjected for tax under the legislation.

In addition to this, the management of Our Earth Pty Ltd also received $ 200,000 which is for

loss of revenue during the last 12 months period and the same would be considered as taxable

income. In addition to this post-judgement interest should also be incorporated in taxable

income within the ordinary meaning of section 6-5, ITAA 1997. The legal fees would also be

included in the assessable income of the business under the provisions of “subdivision 20-A”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

a. Is the sale of land that was bought in May 1984 amounts to a pre-CGT asset?

a. Is the sale of subdivided land amounts to carrying the business the business and land

development and the profits derived thereon are treated for assessment under “section

25 (1), ITAA 1936”?

Rule:

The capital gains can be defined as the system that is contained under the part 3-1 and

part 3-3 of the chapter 3 of the 1997 Act (Blakelock & King, 2017). The concept of capital

gains tax was announced in the year 1985-86 income so that it can overcome the deficiencies

contained in the income tax system as the outcome of capital gains escaping the tax. Under

the CGT, where a taxpayer makes net capital gains during the particular income year, then

the capital gains is included into the taxable income of the taxpayer.

Capital gains is generally imposed on those assets that is purchased by the taxpayer or

any other events that are taking place on or following the 20th September 1985 (Anderson et

al., 2016). Accordingly, the taxpayer should denote the word pre-CGT and post-CGT asset

which is regularly used to assets acquired or events that takes place prior to or following the

introduction of CGT date. The primary step in ascertaining whether the transaction or the

event will be subjected to the CGT it is necessary to ascertain whether any kind of CGT event

has happened.

A capital gains or the capital loss might take place if a CGT event takes place to the

CGT asset. According to the “section 108-5 (1), ITAA 1997” a CGT asset is defined as the

asset or property that are having the legal and equitable rights which is not held as property.

Land is treated as capital asset and its sale will be regarded as the CGT event A1 (Fry, 2017).

Answer to question 2:

Issues:

a. Is the sale of land that was bought in May 1984 amounts to a pre-CGT asset?

a. Is the sale of subdivided land amounts to carrying the business the business and land

development and the profits derived thereon are treated for assessment under “section

25 (1), ITAA 1936”?

Rule:

The capital gains can be defined as the system that is contained under the part 3-1 and

part 3-3 of the chapter 3 of the 1997 Act (Blakelock & King, 2017). The concept of capital

gains tax was announced in the year 1985-86 income so that it can overcome the deficiencies

contained in the income tax system as the outcome of capital gains escaping the tax. Under

the CGT, where a taxpayer makes net capital gains during the particular income year, then

the capital gains is included into the taxable income of the taxpayer.

Capital gains is generally imposed on those assets that is purchased by the taxpayer or

any other events that are taking place on or following the 20th September 1985 (Anderson et

al., 2016). Accordingly, the taxpayer should denote the word pre-CGT and post-CGT asset

which is regularly used to assets acquired or events that takes place prior to or following the

introduction of CGT date. The primary step in ascertaining whether the transaction or the

event will be subjected to the CGT it is necessary to ascertain whether any kind of CGT event

has happened.

A capital gains or the capital loss might take place if a CGT event takes place to the

CGT asset. According to the “section 108-5 (1), ITAA 1997” a CGT asset is defined as the

asset or property that are having the legal and equitable rights which is not held as property.

Land is treated as capital asset and its sale will be regarded as the CGT event A1 (Fry, 2017).

8TAXATION LAW

“Section 104-10, ITAA 1997” provides the taxpayers with the guidelines that the CGT event

A1 is triggered when the taxpayer sells the CGT asset. Nonetheless, the legislative provision

of “subsection 104-10 (5), ITAA 1997” explains that the capital gains or capital loss which is

made by the taxpayer should be disregarded if the taxpayer purchases the asset before the 20th

September 1985.

Accordingly, subdividing the land does not imply the sale of land within the meaning

of “section 104-10, ITAA 1997”. As stated by the “Taxation Determination TD 97/3” it

explains that impact of registering the new titles under the subdivision is with the purpose of

the CGT provisions, to divide the original parcel of land in the two or more assets (James,

2016). Consequently, subdivided blocks of lands are considered to have been purchased by

the owner of the actual parcel of land when actual parcel of land was acquired.

As explained under the CGT regimes, if the disposal of land amounts to business or

the portion of business then the proceeds that are obtained will be considered taxable in the

form of ordinary income under “section 6-5, ITAA 1997”. There are large number of

instances where the owners of the land possess the chance of subdivision and sell of land

which they have owned for the long span of time (Burton, 2017). This kind of situation

happens with the primary producers of the land that owns the asset on the outskirts of the

urban centres and they consider the residential expansion as the best means of using the land

rather than using the land for the purpose of farming. In some of the situation the property

development can be regarded as very much substantial where the taxpayer possesses the large

prospect of making income from the subdivided land.

As held in the case of “Scottish Australia Mining Co Ltd v FCT (1950)” the decision

handed by the court stated that the taxpayer realised a considerable amount of profit.

According to the commissioner, the taxpayer was held taxable in respect of the profits that

“Section 104-10, ITAA 1997” provides the taxpayers with the guidelines that the CGT event

A1 is triggered when the taxpayer sells the CGT asset. Nonetheless, the legislative provision

of “subsection 104-10 (5), ITAA 1997” explains that the capital gains or capital loss which is

made by the taxpayer should be disregarded if the taxpayer purchases the asset before the 20th

September 1985.

Accordingly, subdividing the land does not imply the sale of land within the meaning

of “section 104-10, ITAA 1997”. As stated by the “Taxation Determination TD 97/3” it

explains that impact of registering the new titles under the subdivision is with the purpose of

the CGT provisions, to divide the original parcel of land in the two or more assets (James,

2016). Consequently, subdivided blocks of lands are considered to have been purchased by

the owner of the actual parcel of land when actual parcel of land was acquired.

As explained under the CGT regimes, if the disposal of land amounts to business or

the portion of business then the proceeds that are obtained will be considered taxable in the

form of ordinary income under “section 6-5, ITAA 1997”. There are large number of

instances where the owners of the land possess the chance of subdivision and sell of land

which they have owned for the long span of time (Burton, 2017). This kind of situation

happens with the primary producers of the land that owns the asset on the outskirts of the

urban centres and they consider the residential expansion as the best means of using the land

rather than using the land for the purpose of farming. In some of the situation the property

development can be regarded as very much substantial where the taxpayer possesses the large

prospect of making income from the subdivided land.

As held in the case of “Scottish Australia Mining Co Ltd v FCT (1950)” the decision

handed by the court stated that the taxpayer realised a considerable amount of profit.

According to the commissioner, the taxpayer was held taxable in respect of the profits that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

was derived following the subdivision of many lots (Maley & Maley, 2018). The profit was

considered taxable under the “section 25 (1) of the ITAA 1936” in the form of income for the

profits that are derived by the taxpayer from carrying the business of profit making scheme.

The commissioner assessed the taxpayer for realising the capital asset in the most

advantageous manner because it carried out extensive amount of work on the land so that the

taxpayer can obtain the best possible price.

In another case of “FCT v Whitfords Beach Pty Ltd (1982)”, the taxation

commissioner considered the issues relating to the business income and whether the

subdivision and disposal of land was treated as the ordinary income or was it of capital in

nature (Glover, 2018). The decision handed by the law court explained that the disposal of

land and the gains which were made by the taxpayer from the disposal of land was assessable

under “section 25 (1)” because the taxpayer has gone more than the simple sale of the capital

asset and its activities amounts to carrying the business of land development (Morgan et al.,

2018). The taxpayer carried out the extensive amount of work on the land so that it can get

the possible price and the taxpayer was considered taxable on the profits that was made from

the extensive amount of subdivision and sale of land.

Application:

Sam here purchased an 80 acres of farmland back in 1984 for the amount of

$270,000. Sam used the land for the purpose of cattle breeding. Later in the year February

1995, Sam bought an additional plot of land that has 20 acres of adjoining farmland for the

amount of $110,000 so that he can expand the business operations. Sam however decided to

retire from the farming business and considered selling the land as the sub-divided plots to

produce higher amount of profit.

was derived following the subdivision of many lots (Maley & Maley, 2018). The profit was

considered taxable under the “section 25 (1) of the ITAA 1936” in the form of income for the

profits that are derived by the taxpayer from carrying the business of profit making scheme.

The commissioner assessed the taxpayer for realising the capital asset in the most

advantageous manner because it carried out extensive amount of work on the land so that the

taxpayer can obtain the best possible price.

In another case of “FCT v Whitfords Beach Pty Ltd (1982)”, the taxation

commissioner considered the issues relating to the business income and whether the

subdivision and disposal of land was treated as the ordinary income or was it of capital in

nature (Glover, 2018). The decision handed by the law court explained that the disposal of

land and the gains which were made by the taxpayer from the disposal of land was assessable

under “section 25 (1)” because the taxpayer has gone more than the simple sale of the capital

asset and its activities amounts to carrying the business of land development (Morgan et al.,

2018). The taxpayer carried out the extensive amount of work on the land so that it can get

the possible price and the taxpayer was considered taxable on the profits that was made from

the extensive amount of subdivision and sale of land.

Application:

Sam here purchased an 80 acres of farmland back in 1984 for the amount of

$270,000. Sam used the land for the purpose of cattle breeding. Later in the year February

1995, Sam bought an additional plot of land that has 20 acres of adjoining farmland for the

amount of $110,000 so that he can expand the business operations. Sam however decided to

retire from the farming business and considered selling the land as the sub-divided plots to

produce higher amount of profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

In agreement with the “section 108-5 (1), ITAA 1997” it can be stated that land that is

owned by Sam is a CGT asset. Therefore, the selling of land has triggered the CGT event A1

under the “section 104-10, ITAA 1997”. Nevertheless, it is noteworthy to denote that the 80

acres of land which is purchased by Sam way back in the year 1984 should be viewed as the

pre-CGT asset (Black, 2018). This is because the 80 acres of farmland that was bought by

Sam in 1984 is the pre-CGT asset that is bought before the system of CGT was introduced.

Therefore, the 80 acres of farm being a pre-CGT asset is exempted from the capital gains tax

under “subsection 104-10 (5) of the ITAA 1997”.

Apart from this, Sam also bought the 20 acre of additional farm land which was

adjacent to the previous lot in 1995. This 20 acre of farmland should be treated as the post-

CGT asset since the land was purchased by Sam after the CGT system was introduced

(Robin, 2019). Sam re-zoned the subdivided land and spend additional costs on the

subdivision and surveyor fees. The land was eventually sold on April 2018 for a sum of

$1,100,000.

In light of the “Taxation Determination TD 97/3” Sam registered the new titles on

the land subdivided lots mostly for deriving capital gains (Long et al., 2016). As a result, the

subdivision of land by Sam is treated as the land obtained through the original parcel

ownership. In addition to this, to ascertain the applicability of the capital gains tax on the

subdivided plot of land it is necessary to determine whether the property was acquired for

performing the business of agriculture or for making profit. The intention of deriving

substantial amount of profit was formed in the later stages.

By noting the decision that was given by the federal commissioner in the event of

“FCT v Scottish Australian Mining Co Ltd (1950)” it should be noted that Sam has made a

considerable amount of capital gains from the sale of subdivided allotments (Tran-Nam,

In agreement with the “section 108-5 (1), ITAA 1997” it can be stated that land that is

owned by Sam is a CGT asset. Therefore, the selling of land has triggered the CGT event A1

under the “section 104-10, ITAA 1997”. Nevertheless, it is noteworthy to denote that the 80

acres of land which is purchased by Sam way back in the year 1984 should be viewed as the

pre-CGT asset (Black, 2018). This is because the 80 acres of farmland that was bought by

Sam in 1984 is the pre-CGT asset that is bought before the system of CGT was introduced.

Therefore, the 80 acres of farm being a pre-CGT asset is exempted from the capital gains tax

under “subsection 104-10 (5) of the ITAA 1997”.

Apart from this, Sam also bought the 20 acre of additional farm land which was

adjacent to the previous lot in 1995. This 20 acre of farmland should be treated as the post-

CGT asset since the land was purchased by Sam after the CGT system was introduced

(Robin, 2019). Sam re-zoned the subdivided land and spend additional costs on the

subdivision and surveyor fees. The land was eventually sold on April 2018 for a sum of

$1,100,000.

In light of the “Taxation Determination TD 97/3” Sam registered the new titles on

the land subdivided lots mostly for deriving capital gains (Long et al., 2016). As a result, the

subdivision of land by Sam is treated as the land obtained through the original parcel

ownership. In addition to this, to ascertain the applicability of the capital gains tax on the

subdivided plot of land it is necessary to determine whether the property was acquired for

performing the business of agriculture or for making profit. The intention of deriving

substantial amount of profit was formed in the later stages.

By noting the decision that was given by the federal commissioner in the event of

“FCT v Scottish Australian Mining Co Ltd (1950)” it should be noted that Sam has made a

considerable amount of capital gains from the sale of subdivided allotments (Tran-Nam,

11TAXATION LAW

2016). Therefore, Sam will be considered taxable on the capital gains from the sale of

subdivided lots. The profits will be treated under the legislative provision of “section 25 (1),

ITAA 1936” in the form of income which is earned by the taxpayer from performing the

business of land development (Black, 2017). In addition to this the gains that is derived by

Sam has mainly originated from carrying on the profit making undertaking or scheme.

Sam in the present situation has realised the capital asset in the most advantageous

way and was carrying the business activities. The gains made thereof will be considered

assessable as ordinary income (Basak, 2016). The activities of Sam can be contented as the

mere realisation of the asset and the extensive amount of work in the form of re-zoning of

land was mainly directed to fetch the best possible price.

Additional orientation to the decision handed in “FCT v Whitfords Beach Pty Ltd

(1982)” can be referred to explain that capital gains that are made from the selling of

subdivided land is taxable under the “section 25 (1) of the ITAA 1997” in the form of

income from performing the business activities of land development (Chardon et al., 2016).

Furthermore, the capital gains made thereof were as the outcome of carrying the profit

deriving scheme. The extensive amount of work done by Sam was primarily directed towards

getting the best possible price and the situation of Sam was not indistinguishable from the

“FCT v Scottish Australian Mining Co Ltd (1950)” (Martin, 2019). Therefore, the profit

will be considered taxable arising out of the extensive amount of subdivision and sale of land.

2016). Therefore, Sam will be considered taxable on the capital gains from the sale of

subdivided lots. The profits will be treated under the legislative provision of “section 25 (1),

ITAA 1936” in the form of income which is earned by the taxpayer from performing the

business of land development (Black, 2017). In addition to this the gains that is derived by

Sam has mainly originated from carrying on the profit making undertaking or scheme.

Sam in the present situation has realised the capital asset in the most advantageous

way and was carrying the business activities. The gains made thereof will be considered

assessable as ordinary income (Basak, 2016). The activities of Sam can be contented as the

mere realisation of the asset and the extensive amount of work in the form of re-zoning of

land was mainly directed to fetch the best possible price.

Additional orientation to the decision handed in “FCT v Whitfords Beach Pty Ltd

(1982)” can be referred to explain that capital gains that are made from the selling of

subdivided land is taxable under the “section 25 (1) of the ITAA 1997” in the form of

income from performing the business activities of land development (Chardon et al., 2016).

Furthermore, the capital gains made thereof were as the outcome of carrying the profit

deriving scheme. The extensive amount of work done by Sam was primarily directed towards

getting the best possible price and the situation of Sam was not indistinguishable from the

“FCT v Scottish Australian Mining Co Ltd (1950)” (Martin, 2019). Therefore, the profit

will be considered taxable arising out of the extensive amount of subdivision and sale of land.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.