Understanding Trading Stock Regulations & Income Tax Assessment 1997

VerifiedAdded on 2023/06/18

|5

|1020

|63

Homework Assignment

AI Summary

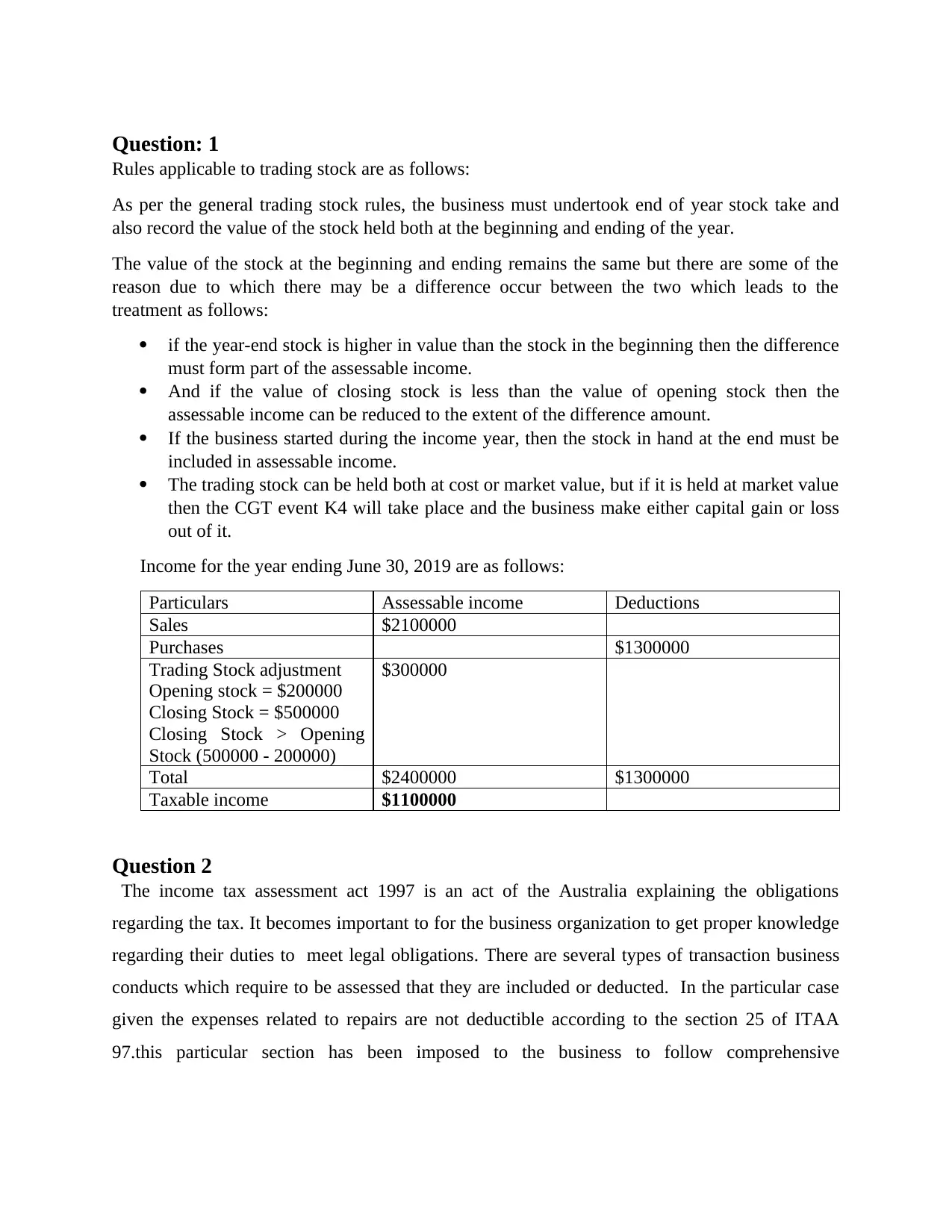

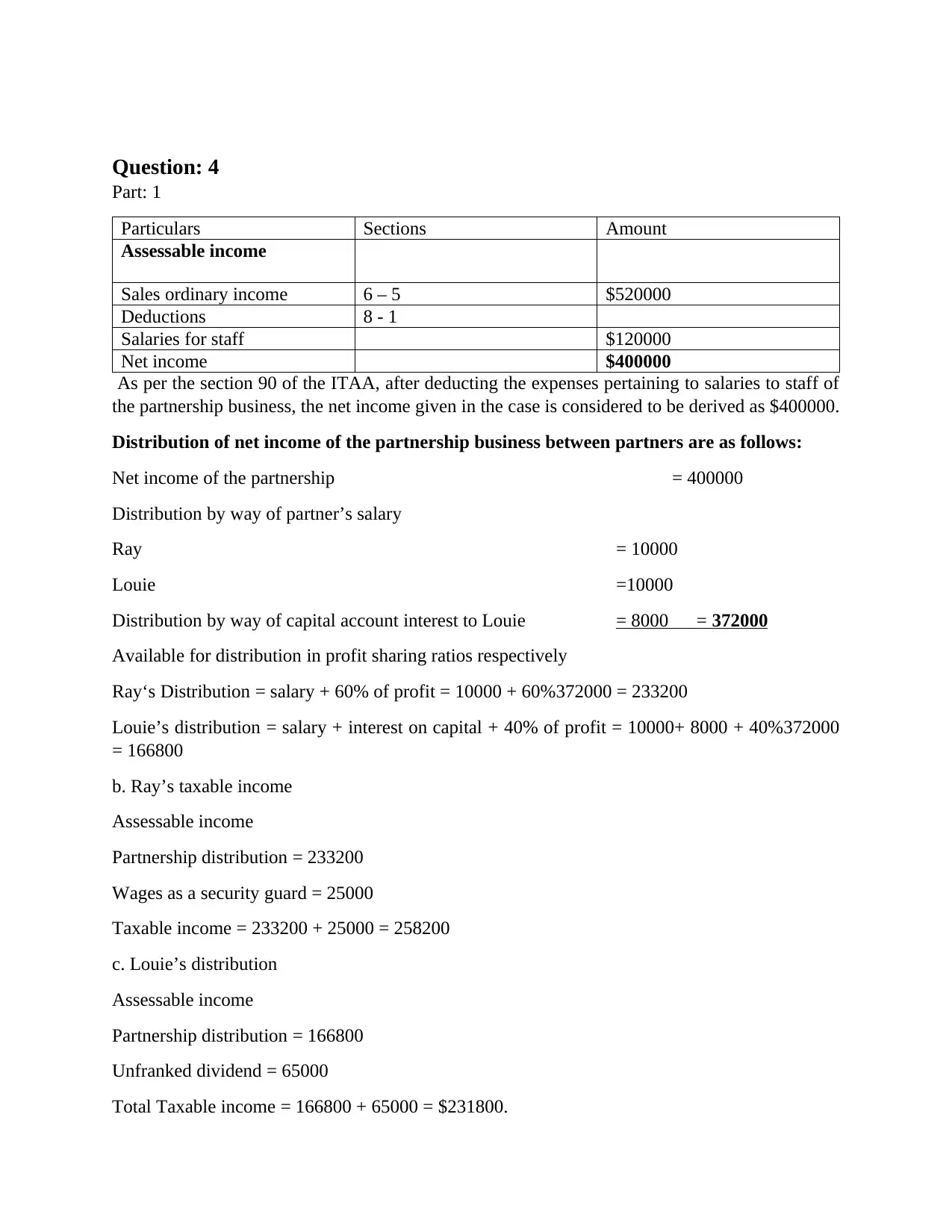

This assignment provides a detailed analysis of trading stock rules and the Income Tax Assessment Act 1997, focusing on assessable income, tax deductions, and partnership income distribution. It explains the implications of year-end stock adjustments, deductibility of business expenses, and the treatment of legal fees and employee wages. The assignment also includes a breakdown of partnership income distribution between partners, considering salaries, capital account interest, and profit-sharing ratios, along with the calculation of individual partners' taxable income based on their respective distributions and other income sources. Desklib offers a wealth of study resources, including solved assignments and past papers, to support students in mastering these complex topics.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.