Tax Law Analysis: Income Tax, Medicare Levy, and Surcharge 2018

VerifiedAdded on 2023/06/04

|8

|944

|376

Homework Assignment

AI Summary

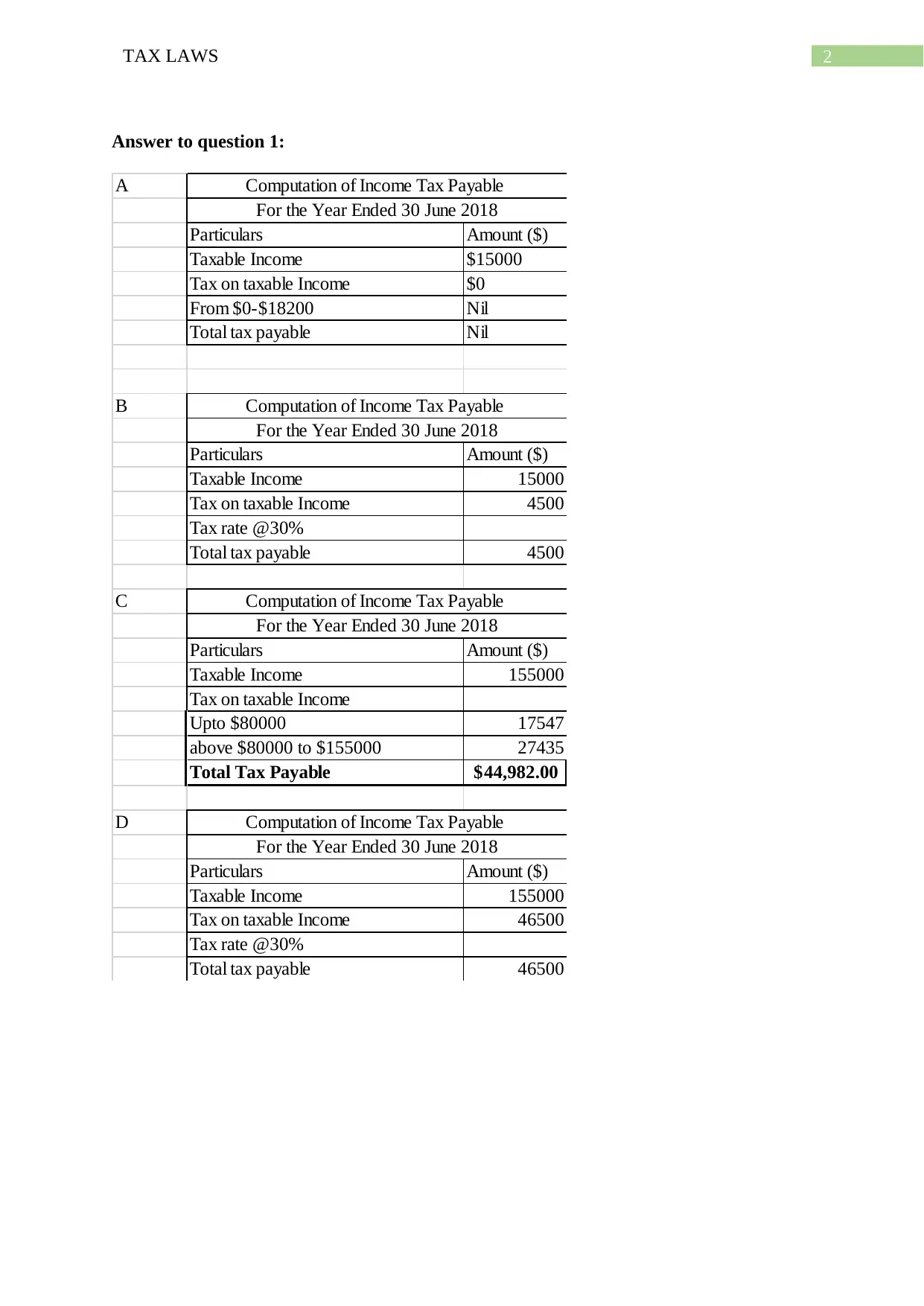

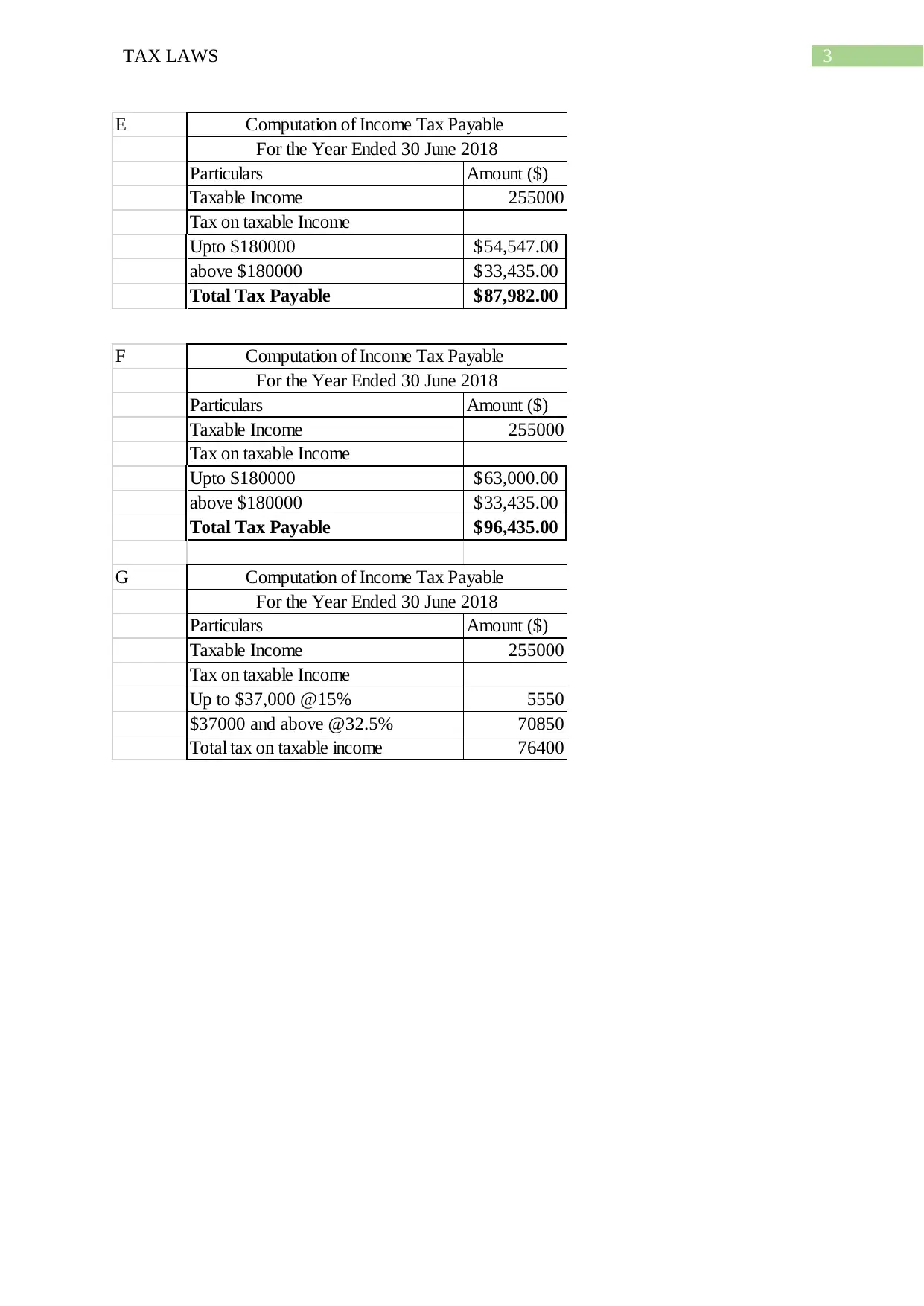

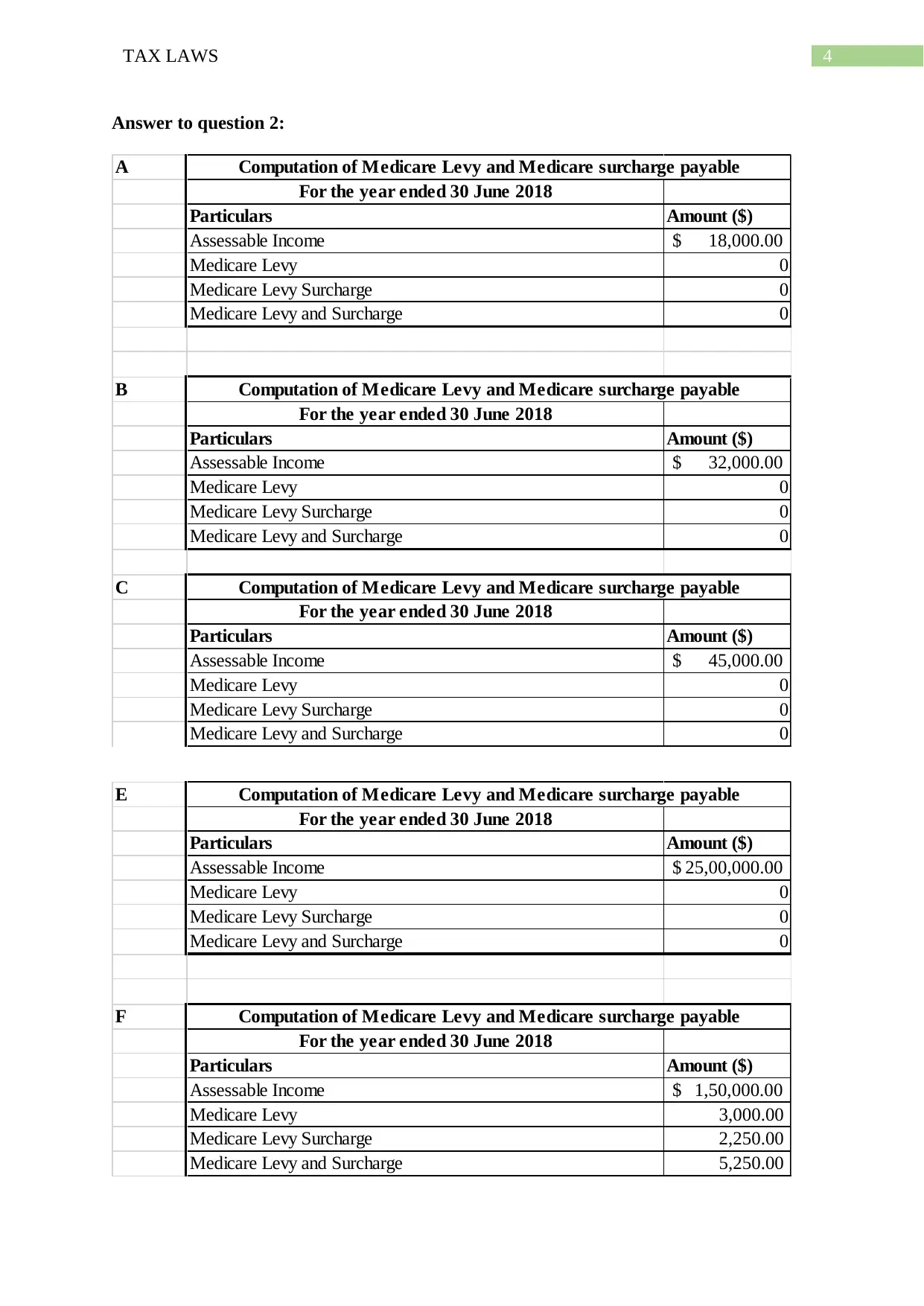

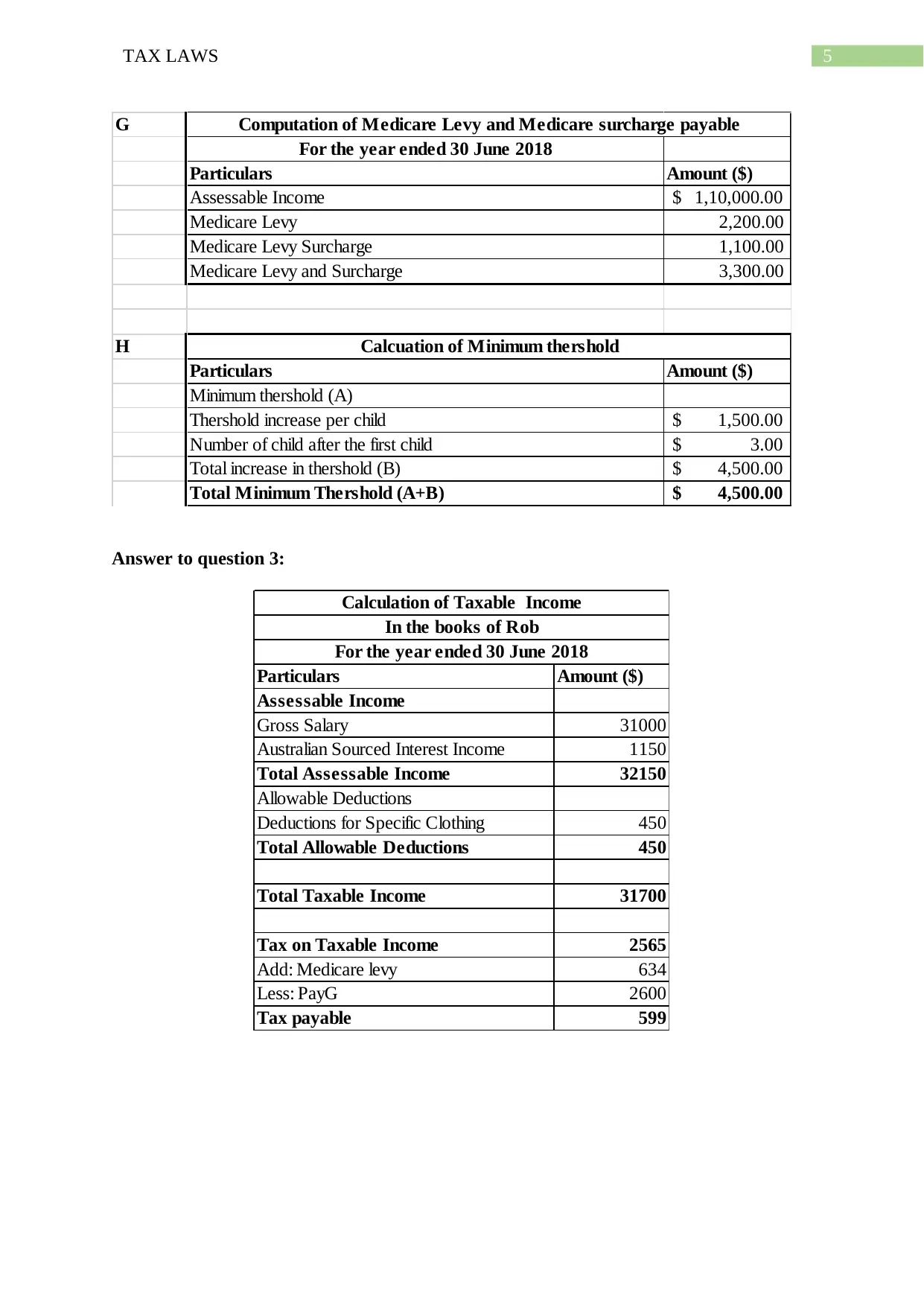

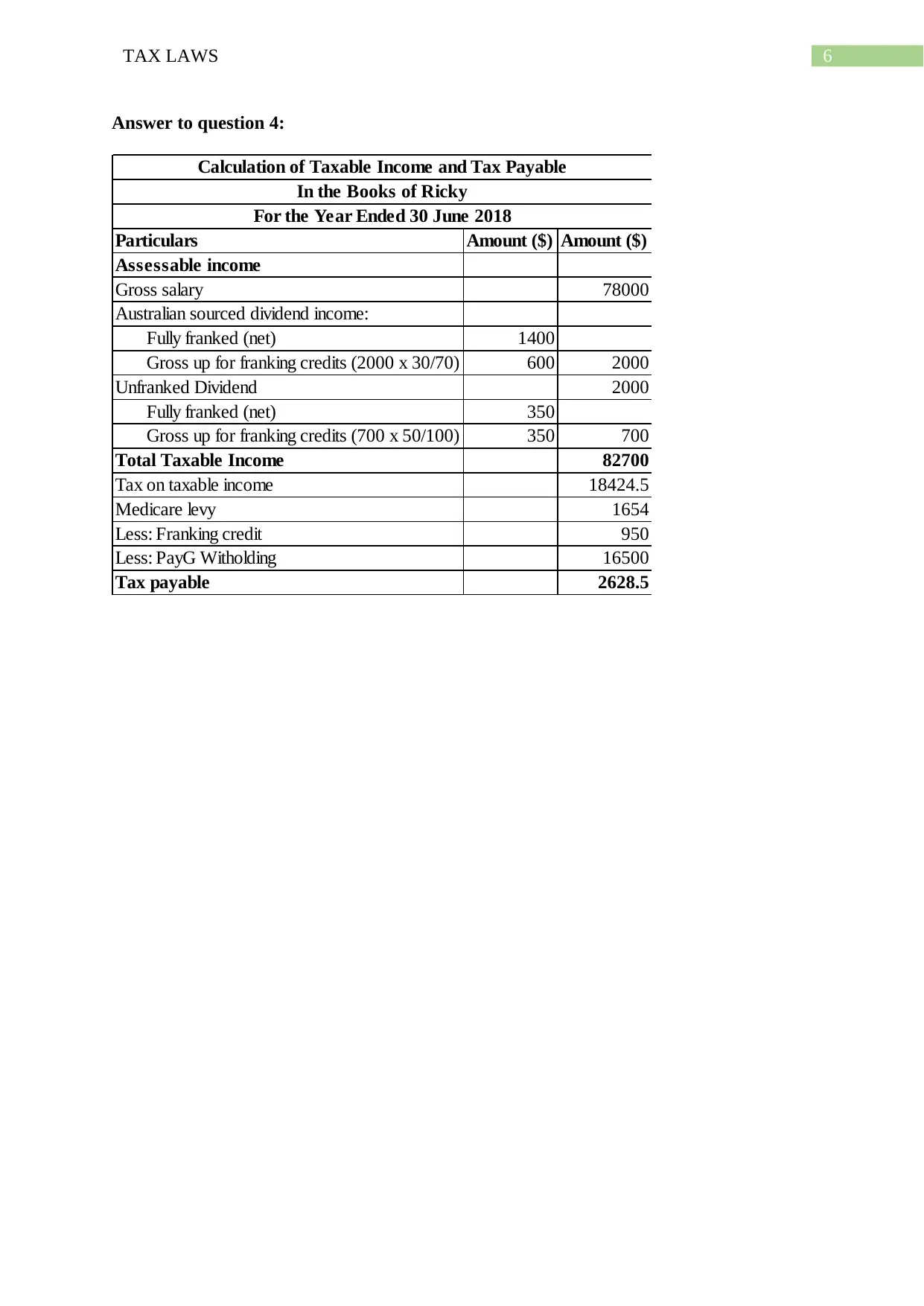

This assignment provides detailed calculations related to Australian tax law for the year ended June 30, 2018. It includes computations of income tax payable under various taxable income scenarios, considering different tax rates and thresholds. Additionally, it covers the calculation of Medicare levy and Medicare levy surcharge based on assessable income, demonstrating how these levies are determined for different income levels. The assignment also includes calculations of taxable income, taking into account assessable income, allowable deductions, and pay-as-you-go (PAYG) tax payable. Finally, it addresses the calculation of taxable income and tax payable, incorporating franked and unfranked dividend income, franking credits, and Medicare levy, providing a comprehensive overview of key tax concepts and calculations. Desklib provides access to this and similar solved assignments.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.