THE TAX PLAN AND COMPLIANCE

VerifiedAdded on 2022/08/11

|14

|1607

|34

AI Summary

This unit requires the application of skills and knowledge required to implement tax plans and to evaluate organisation's taxation compliance. The unit encompasses assessing taxation liabilities, optimising tax position, establishing processes and plans, evaluating tax policies and reviewing taxation compliance. The unit can be applied across the financial services sector, and is appropriate for a person with suitable qualifications and experience such as an accountant and taxation specialist that is responsible for implementing tax plans and evaluating compliance with taxation requirements

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAX PLAN AND COMPLIANCE

Tax Plan and Compliance

Name of the Student

Name of the University

Authors Note

Course ID

Tax Plan and Compliance

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAX PLAN AND COMPLIANCE

Table of Contents

Part a: Scenario 1:......................................................................................................................3

Answer to question A:................................................................................................................3

Answer to question B:................................................................................................................4

Answer to question II:................................................................................................................4

Answer to question III:...............................................................................................................4

Answer to question IV:..............................................................................................................5

Answer to question V:................................................................................................................5

Answer to question VI:..............................................................................................................5

Answer to question VII:.............................................................................................................6

Answer to VIII:..........................................................................................................................6

Answer to question IX:..............................................................................................................7

Part B: Scenario 2:.....................................................................................................................8

Answer to requirement A:..........................................................................................................8

Answer to question II:................................................................................................................9

Answer to A:..............................................................................................................................9

Answer to B:............................................................................................................................10

Answer to C:............................................................................................................................10

Answer to D:............................................................................................................................10

Answer to requirement III:.......................................................................................................10

Part C: Scenario 3:...................................................................................................................11

Table of Contents

Part a: Scenario 1:......................................................................................................................3

Answer to question A:................................................................................................................3

Answer to question B:................................................................................................................4

Answer to question II:................................................................................................................4

Answer to question III:...............................................................................................................4

Answer to question IV:..............................................................................................................5

Answer to question V:................................................................................................................5

Answer to question VI:..............................................................................................................5

Answer to question VII:.............................................................................................................6

Answer to VIII:..........................................................................................................................6

Answer to question IX:..............................................................................................................7

Part B: Scenario 2:.....................................................................................................................8

Answer to requirement A:..........................................................................................................8

Answer to question II:................................................................................................................9

Answer to A:..............................................................................................................................9

Answer to B:............................................................................................................................10

Answer to C:............................................................................................................................10

Answer to D:............................................................................................................................10

Answer to requirement III:.......................................................................................................10

Part C: Scenario 3:...................................................................................................................11

2TAX PLAN AND COMPLIANCE

Answer to question I:...............................................................................................................11

Answer to question II:..............................................................................................................11

Bibliographies:.........................................................................................................................13

Answer to question I:...............................................................................................................11

Answer to question II:..............................................................................................................11

Bibliographies:.........................................................................................................................13

3TAX PLAN AND COMPLIANCE

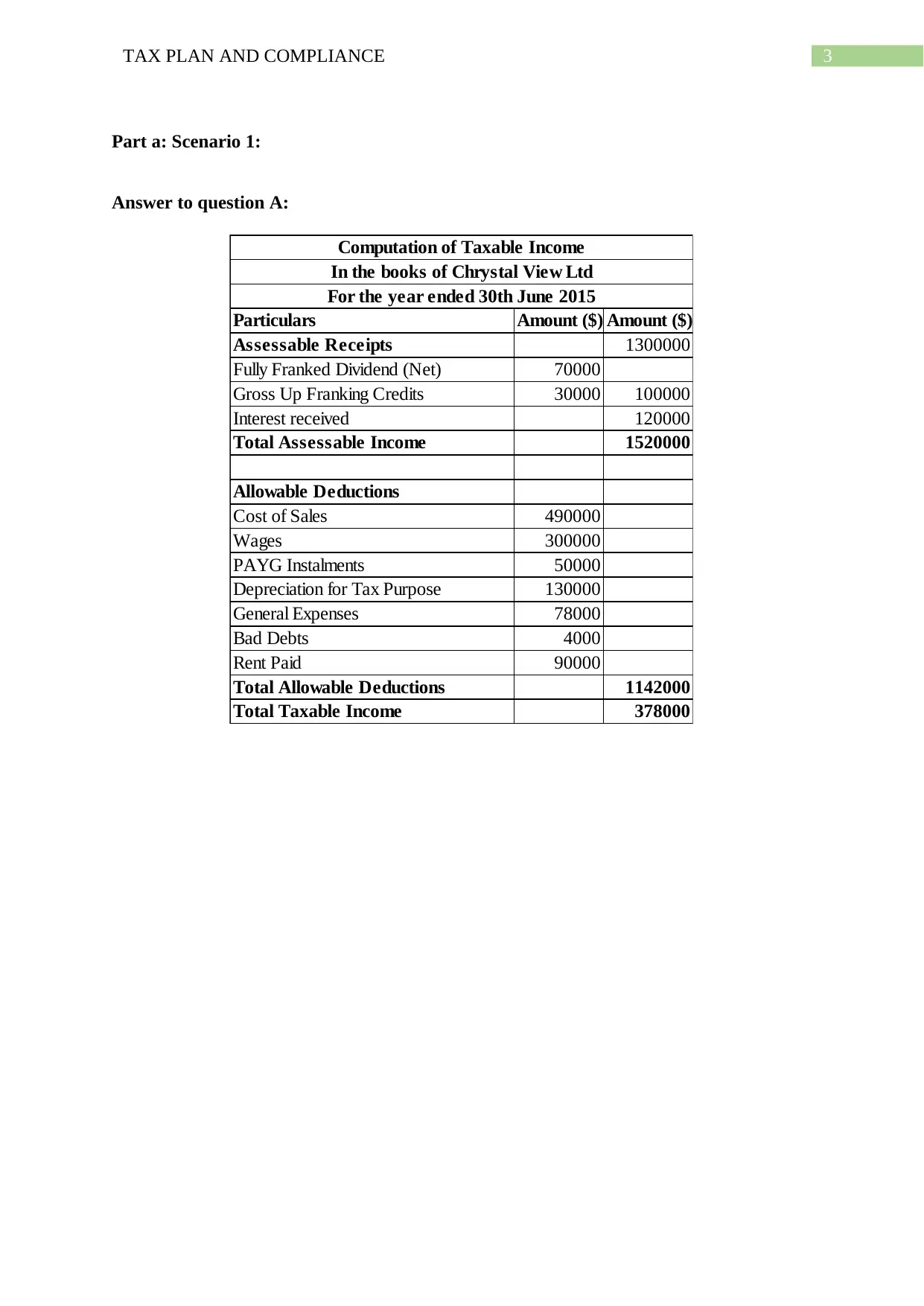

Part a: Scenario 1:

Answer to question A:

Particulars Amount ($) Amount ($)

Assessable Receipts 1300000

Fully Franked Dividend (Net) 70000

Gross Up Franking Credits 30000 100000

Interest received 120000

Total Assessable Income 1520000

Allowable Deductions

Cost of Sales 490000

Wages 300000

PAYG Instalments 50000

Depreciation for Tax Purpose 130000

General Expenses 78000

Bad Debts 4000

Rent Paid 90000

Total Allowable Deductions 1142000

Total Taxable Income 378000

Computation of Taxable Income

In the books of Chrystal View Ltd

For the year ended 30th June 2015

Part a: Scenario 1:

Answer to question A:

Particulars Amount ($) Amount ($)

Assessable Receipts 1300000

Fully Franked Dividend (Net) 70000

Gross Up Franking Credits 30000 100000

Interest received 120000

Total Assessable Income 1520000

Allowable Deductions

Cost of Sales 490000

Wages 300000

PAYG Instalments 50000

Depreciation for Tax Purpose 130000

General Expenses 78000

Bad Debts 4000

Rent Paid 90000

Total Allowable Deductions 1142000

Total Taxable Income 378000

Computation of Taxable Income

In the books of Chrystal View Ltd

For the year ended 30th June 2015

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAX PLAN AND COMPLIANCE

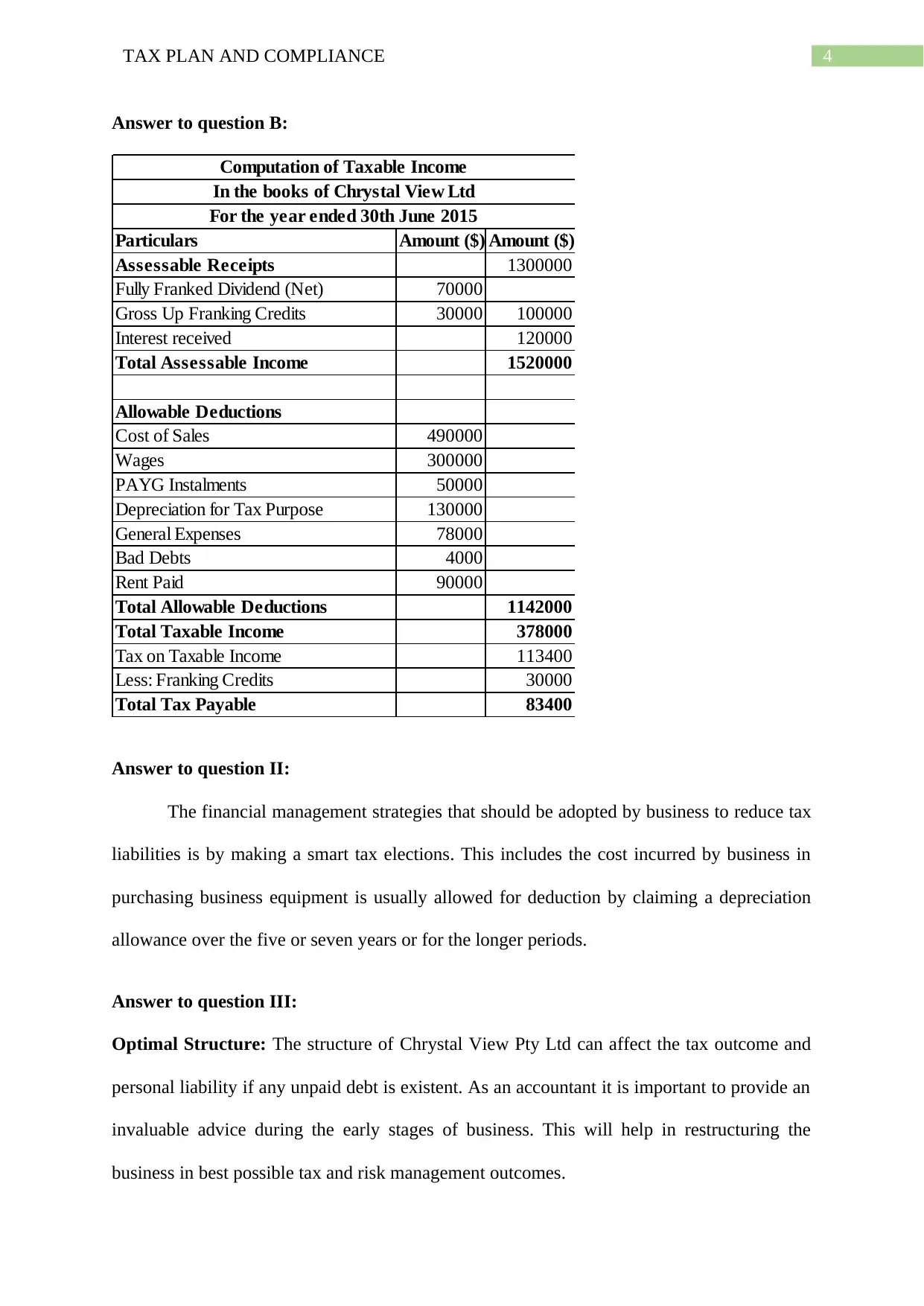

Answer to question B:

Particulars Amount ($) Amount ($)

Assessable Receipts 1300000

Fully Franked Dividend (Net) 70000

Gross Up Franking Credits 30000 100000

Interest received 120000

Total Assessable Income 1520000

Allowable Deductions

Cost of Sales 490000

Wages 300000

PAYG Instalments 50000

Depreciation for Tax Purpose 130000

General Expenses 78000

Bad Debts 4000

Rent Paid 90000

Total Allowable Deductions 1142000

Total Taxable Income 378000

Tax on Taxable Income 113400

Less: Franking Credits 30000

Total Tax Payable 83400

Computation of Taxable Income

In the books of Chrystal View Ltd

For the year ended 30th June 2015

Answer to question II:

The financial management strategies that should be adopted by business to reduce tax

liabilities is by making a smart tax elections. This includes the cost incurred by business in

purchasing business equipment is usually allowed for deduction by claiming a depreciation

allowance over the five or seven years or for the longer periods.

Answer to question III:

Optimal Structure: The structure of Chrystal View Pty Ltd can affect the tax outcome and

personal liability if any unpaid debt is existent. As an accountant it is important to provide an

invaluable advice during the early stages of business. This will help in restructuring the

business in best possible tax and risk management outcomes.

Answer to question B:

Particulars Amount ($) Amount ($)

Assessable Receipts 1300000

Fully Franked Dividend (Net) 70000

Gross Up Franking Credits 30000 100000

Interest received 120000

Total Assessable Income 1520000

Allowable Deductions

Cost of Sales 490000

Wages 300000

PAYG Instalments 50000

Depreciation for Tax Purpose 130000

General Expenses 78000

Bad Debts 4000

Rent Paid 90000

Total Allowable Deductions 1142000

Total Taxable Income 378000

Tax on Taxable Income 113400

Less: Franking Credits 30000

Total Tax Payable 83400

Computation of Taxable Income

In the books of Chrystal View Ltd

For the year ended 30th June 2015

Answer to question II:

The financial management strategies that should be adopted by business to reduce tax

liabilities is by making a smart tax elections. This includes the cost incurred by business in

purchasing business equipment is usually allowed for deduction by claiming a depreciation

allowance over the five or seven years or for the longer periods.

Answer to question III:

Optimal Structure: The structure of Chrystal View Pty Ltd can affect the tax outcome and

personal liability if any unpaid debt is existent. As an accountant it is important to provide an

invaluable advice during the early stages of business. This will help in restructuring the

business in best possible tax and risk management outcomes.

5TAX PLAN AND COMPLIANCE

Minimizing tax bill: As an accountant of Chrystal View Pty Ltd it is vital to minimize the

deductions. Since the tax laws and regulations are changing constantly it is important to go

through all the issues which can help in preparation of tax document and minimization of tax

bill as well.

Answer to question IV:

Commonly, the tax return of Chrystal View Pty Ltd is due to be lodge by 15th of the

day with the ATO for the seventh month after the end of applicable income year or dates that

may be allowed by the Commissioner of Taxation.

Answer to question V:

The document management procedure that can be adopted to make sure that the tax

return meets the compliance requirements are as follows;

Payroll reporting: Small business that has employee strength of less than 20 employees is

needed to lodge the reports with the ATO.

Monthly or quarter BAS and instalment activity statements: The ATO needs businesses

to submit a business activity statement on the monthly, quarterly or yearly basis.

Financial year reporting: This can be viewed as another way of maintaining compliance

requirements relating to tax. Business firms are under the obligation of lodging tax returns for

this period. If someone is operating their business as sole trader they can declare the business

income as their personal income tax returns.

Answer to question VI:

For Chrystal View Pty Ltd the due date to lodge BAS and pay their monthly BAS is

given below.

Minimizing tax bill: As an accountant of Chrystal View Pty Ltd it is vital to minimize the

deductions. Since the tax laws and regulations are changing constantly it is important to go

through all the issues which can help in preparation of tax document and minimization of tax

bill as well.

Answer to question IV:

Commonly, the tax return of Chrystal View Pty Ltd is due to be lodge by 15th of the

day with the ATO for the seventh month after the end of applicable income year or dates that

may be allowed by the Commissioner of Taxation.

Answer to question V:

The document management procedure that can be adopted to make sure that the tax

return meets the compliance requirements are as follows;

Payroll reporting: Small business that has employee strength of less than 20 employees is

needed to lodge the reports with the ATO.

Monthly or quarter BAS and instalment activity statements: The ATO needs businesses

to submit a business activity statement on the monthly, quarterly or yearly basis.

Financial year reporting: This can be viewed as another way of maintaining compliance

requirements relating to tax. Business firms are under the obligation of lodging tax returns for

this period. If someone is operating their business as sole trader they can declare the business

income as their personal income tax returns.

Answer to question VI:

For Chrystal View Pty Ltd the due date to lodge BAS and pay their monthly BAS is

given below.

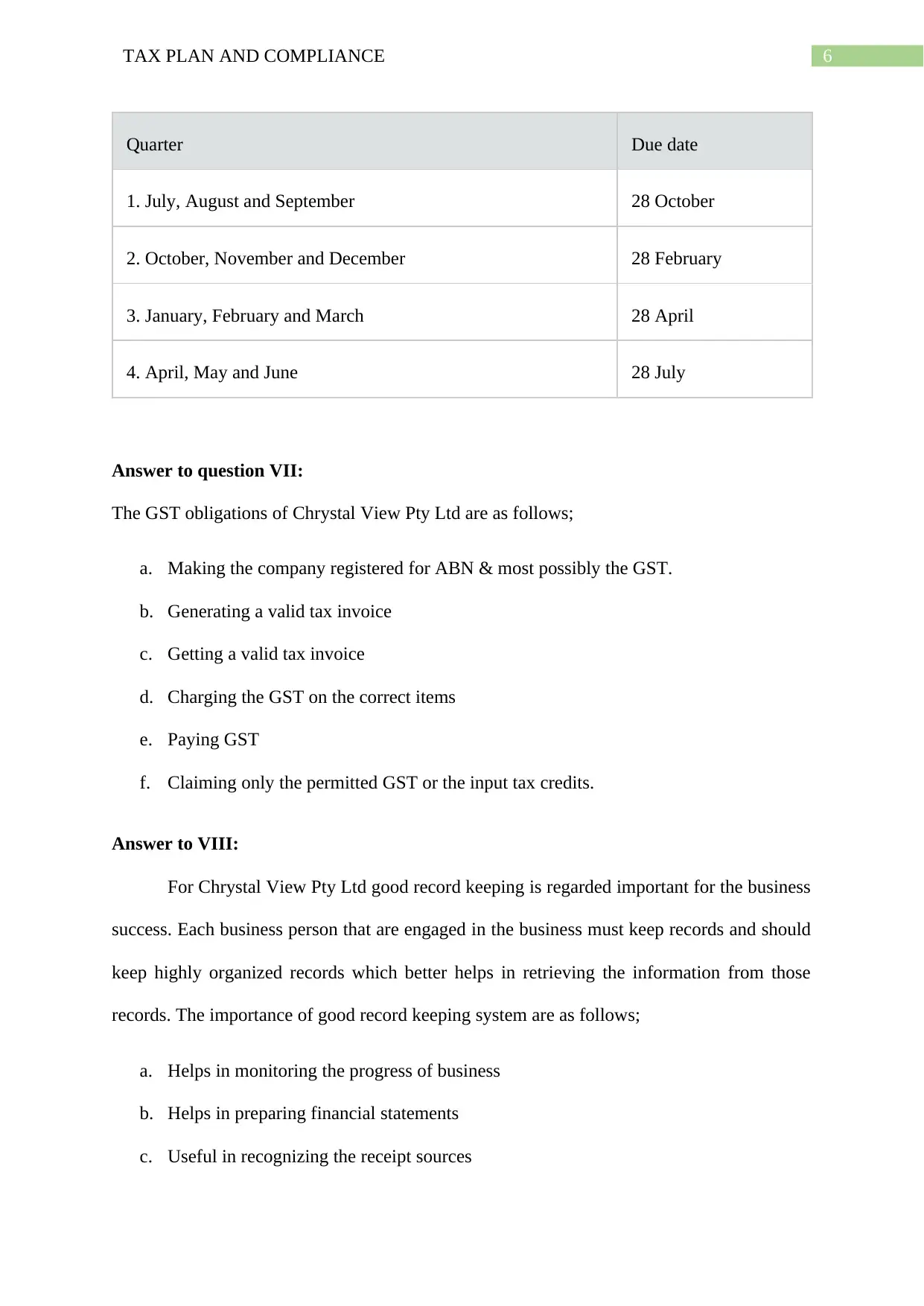

6TAX PLAN AND COMPLIANCE

Quarter Due date

1. July, August and September 28 October

2. October, November and December 28 February

3. January, February and March 28 April

4. April, May and June 28 July

Answer to question VII:

The GST obligations of Chrystal View Pty Ltd are as follows;

a. Making the company registered for ABN & most possibly the GST.

b. Generating a valid tax invoice

c. Getting a valid tax invoice

d. Charging the GST on the correct items

e. Paying GST

f. Claiming only the permitted GST or the input tax credits.

Answer to VIII:

For Chrystal View Pty Ltd good record keeping is regarded important for the business

success. Each business person that are engaged in the business must keep records and should

keep highly organized records which better helps in retrieving the information from those

records. The importance of good record keeping system are as follows;

a. Helps in monitoring the progress of business

b. Helps in preparing financial statements

c. Useful in recognizing the receipt sources

Quarter Due date

1. July, August and September 28 October

2. October, November and December 28 February

3. January, February and March 28 April

4. April, May and June 28 July

Answer to question VII:

The GST obligations of Chrystal View Pty Ltd are as follows;

a. Making the company registered for ABN & most possibly the GST.

b. Generating a valid tax invoice

c. Getting a valid tax invoice

d. Charging the GST on the correct items

e. Paying GST

f. Claiming only the permitted GST or the input tax credits.

Answer to VIII:

For Chrystal View Pty Ltd good record keeping is regarded important for the business

success. Each business person that are engaged in the business must keep records and should

keep highly organized records which better helps in retrieving the information from those

records. The importance of good record keeping system are as follows;

a. Helps in monitoring the progress of business

b. Helps in preparing financial statements

c. Useful in recognizing the receipt sources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX PLAN AND COMPLIANCE

d. Helps in keeping track of the deductible outgoings

e. Maintaining the lists of assets

f. Helps in preparation of tax returns and supports the items which is reported on the tax

returns.

Answer to question IX:

Name Elements

Receipts Payroll records, income, deduction or credit in tax return.

Cash register tapes Cash books of sales

Information of

deposits Receipts of bank deposits

Invoices Sales and purchase receipts

Bank statement Quarterly bank statement

Petty cash slips for

small cash

payments

Payment of petty cash items

Cancelled cheques Documentary evidence of cancelled cheques

Credit card receipts Receipts showing source of expense transaction.

d. Helps in keeping track of the deductible outgoings

e. Maintaining the lists of assets

f. Helps in preparation of tax returns and supports the items which is reported on the tax

returns.

Answer to question IX:

Name Elements

Receipts Payroll records, income, deduction or credit in tax return.

Cash register tapes Cash books of sales

Information of

deposits Receipts of bank deposits

Invoices Sales and purchase receipts

Bank statement Quarterly bank statement

Petty cash slips for

small cash

payments

Payment of petty cash items

Cancelled cheques Documentary evidence of cancelled cheques

Credit card receipts Receipts showing source of expense transaction.

8TAX PLAN AND COMPLIANCE

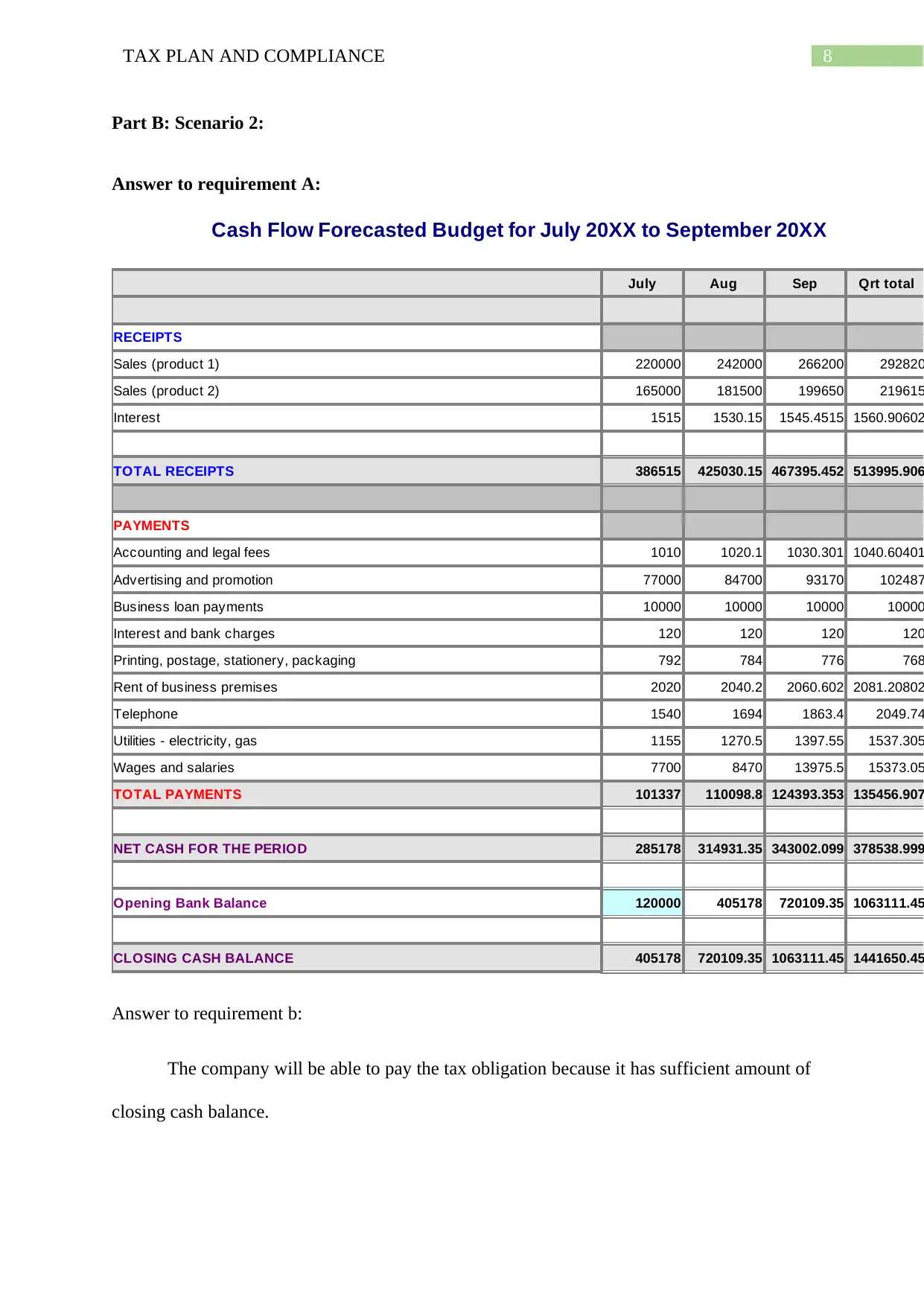

Part B: Scenario 2:

Answer to requirement A:

Cash Flow Forecasted Budget for July 20XX to September 20XX

July Aug Sep Qrt total

RECEIPTS

Sales (product 1) 220000 242000 266200 292820

Sales (product 2) 165000 181500 199650 219615

Interest 1515 1530.15 1545.4515 1560.90602

TOTAL RECEIPTS 386515 425030.15 467395.452 513995.906

PAYMENTS

Accounting and legal fees 1010 1020.1 1030.301 1040.60401

Advertising and promotion 77000 84700 93170 102487

Business loan payments 10000 10000 10000 10000

Interest and bank charges 120 120 120 120

Printing, postage, stationery, packaging 792 784 776 768

Rent of business premises 2020 2040.2 2060.602 2081.20802

Telephone 1540 1694 1863.4 2049.74

Utilities - electricity, gas 1155 1270.5 1397.55 1537.305

Wages and salaries 7700 8470 13975.5 15373.05

TOTAL PAYMENTS 101337 110098.8 124393.353 135456.907

NET CASH FOR THE PERIOD 285178 314931.35 343002.099 378538.999

Opening Bank Balance 120000 405178 720109.35 1063111.45

CLOSING CASH BALANCE 405178 720109.35 1063111.45 1441650.45

Answer to requirement b:

The company will be able to pay the tax obligation because it has sufficient amount of

closing cash balance.

Part B: Scenario 2:

Answer to requirement A:

Cash Flow Forecasted Budget for July 20XX to September 20XX

July Aug Sep Qrt total

RECEIPTS

Sales (product 1) 220000 242000 266200 292820

Sales (product 2) 165000 181500 199650 219615

Interest 1515 1530.15 1545.4515 1560.90602

TOTAL RECEIPTS 386515 425030.15 467395.452 513995.906

PAYMENTS

Accounting and legal fees 1010 1020.1 1030.301 1040.60401

Advertising and promotion 77000 84700 93170 102487

Business loan payments 10000 10000 10000 10000

Interest and bank charges 120 120 120 120

Printing, postage, stationery, packaging 792 784 776 768

Rent of business premises 2020 2040.2 2060.602 2081.20802

Telephone 1540 1694 1863.4 2049.74

Utilities - electricity, gas 1155 1270.5 1397.55 1537.305

Wages and salaries 7700 8470 13975.5 15373.05

TOTAL PAYMENTS 101337 110098.8 124393.353 135456.907

NET CASH FOR THE PERIOD 285178 314931.35 343002.099 378538.999

Opening Bank Balance 120000 405178 720109.35 1063111.45

CLOSING CASH BALANCE 405178 720109.35 1063111.45 1441650.45

Answer to requirement b:

The company will be able to pay the tax obligation because it has sufficient amount of

closing cash balance.

9TAX PLAN AND COMPLIANCE

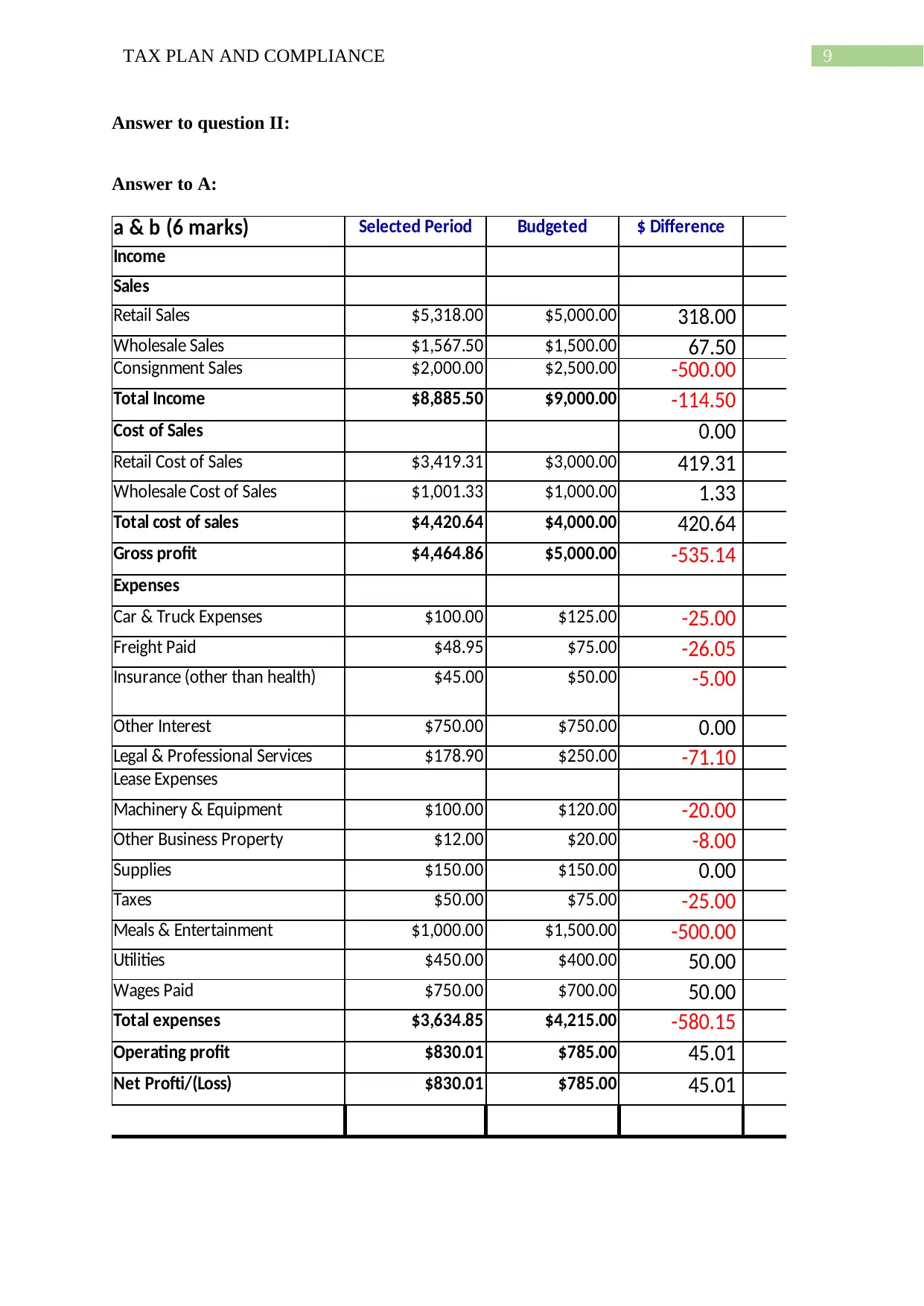

Answer to question II:

Answer to A:

a & b (6 marks) Selected Period Budgeted $ Difference

Income

Sales

Retail Sales $5,318.00 $5,000.00 318.00

Wholesale Sales $1,567.50 $1,500.00 67.50

Consignment Sales $2,000.00 $2,500.00 -500.00

Total Income $8,885.50 $9,000.00 -114.50

Cost of Sales 0.00

Retail Cost of Sales $3,419.31 $3,000.00 419.31

Wholesale Cost of Sales $1,001.33 $1,000.00 1.33

Total cost of sales $4,420.64 $4,000.00 420.64

Gross profit $4,464.86 $5,000.00 -535.14

Expenses

Car & Truck Expenses $100.00 $125.00 -25.00

Freight Paid $48.95 $75.00 -26.05

Insurance (other than health) $45.00 $50.00 -5.00

Other Interest $750.00 $750.00 0.00

Legal & Professional Services $178.90 $250.00 -71.10

Lease Expenses

Machinery & Equipment $100.00 $120.00 -20.00

Other Business Property $12.00 $20.00 -8.00

Supplies $150.00 $150.00 0.00

Taxes $50.00 $75.00 -25.00

Meals & Entertainment $1,000.00 $1,500.00 -500.00

Utilities $450.00 $400.00 50.00

Wages Paid $750.00 $700.00 50.00

Total expenses $3,634.85 $4,215.00 -580.15

Operating profit $830.01 $785.00 45.01

Net Profti/(Loss) $830.01 $785.00 45.01

Answer to question II:

Answer to A:

a & b (6 marks) Selected Period Budgeted $ Difference

Income

Sales

Retail Sales $5,318.00 $5,000.00 318.00

Wholesale Sales $1,567.50 $1,500.00 67.50

Consignment Sales $2,000.00 $2,500.00 -500.00

Total Income $8,885.50 $9,000.00 -114.50

Cost of Sales 0.00

Retail Cost of Sales $3,419.31 $3,000.00 419.31

Wholesale Cost of Sales $1,001.33 $1,000.00 1.33

Total cost of sales $4,420.64 $4,000.00 420.64

Gross profit $4,464.86 $5,000.00 -535.14

Expenses

Car & Truck Expenses $100.00 $125.00 -25.00

Freight Paid $48.95 $75.00 -26.05

Insurance (other than health) $45.00 $50.00 -5.00

Other Interest $750.00 $750.00 0.00

Legal & Professional Services $178.90 $250.00 -71.10

Lease Expenses

Machinery & Equipment $100.00 $120.00 -20.00

Other Business Property $12.00 $20.00 -8.00

Supplies $150.00 $150.00 0.00

Taxes $50.00 $75.00 -25.00

Meals & Entertainment $1,000.00 $1,500.00 -500.00

Utilities $450.00 $400.00 50.00

Wages Paid $750.00 $700.00 50.00

Total expenses $3,634.85 $4,215.00 -580.15

Operating profit $830.01 $785.00 45.01

Net Profti/(Loss) $830.01 $785.00 45.01

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAX PLAN AND COMPLIANCE

Answer to B:

As evident from the above given table it is noticed that the retail sales have

represented a rise in sales by 106 while the wholesale have portrayed an increase in sales by

105%. The consignment sales actually stood 80% while the total income declined by 1% to

stand at 99%. The business has also occurred an increase in the retail cost of sales of 114%

while cost of wholesale trade has remained at 100%. Overall gross profit has represented a

decline by 89% and the variance amount standing for the same was 535. The business

reported a decline in car and truck expenses as the expenditure represented 80% of the total

budgeted amount. The overall expenses stood 86% while the business has reported a net

profit of 106%.

Answer to C:

In order to improve the tax obligations Super Cool Pty Ltd is required to improve its

gross profit. This can be improved by increasing the sales price and taking more of a cash

discount from the suppliers.

Answer to D:

For Super Cool Pty Ltd there are numerous areas of tax planning is applicable. The

area of tax planning for budget variance is the choice of accounting and the method of

inventory valuations. This also includes the timing of purchasing equipment, spreading the

business income and involves the selection of tax favoured benefit as well as investment

plans.

Answer to requirement III:

Yes, it can be stated that there is a legislative and professional requirement of

monitoring as well as reviewing the tax document. Regularly reviewing the legislation and

regulation which affects the working environment. The monitoring and reviewing of tax

Answer to B:

As evident from the above given table it is noticed that the retail sales have

represented a rise in sales by 106 while the wholesale have portrayed an increase in sales by

105%. The consignment sales actually stood 80% while the total income declined by 1% to

stand at 99%. The business has also occurred an increase in the retail cost of sales of 114%

while cost of wholesale trade has remained at 100%. Overall gross profit has represented a

decline by 89% and the variance amount standing for the same was 535. The business

reported a decline in car and truck expenses as the expenditure represented 80% of the total

budgeted amount. The overall expenses stood 86% while the business has reported a net

profit of 106%.

Answer to C:

In order to improve the tax obligations Super Cool Pty Ltd is required to improve its

gross profit. This can be improved by increasing the sales price and taking more of a cash

discount from the suppliers.

Answer to D:

For Super Cool Pty Ltd there are numerous areas of tax planning is applicable. The

area of tax planning for budget variance is the choice of accounting and the method of

inventory valuations. This also includes the timing of purchasing equipment, spreading the

business income and involves the selection of tax favoured benefit as well as investment

plans.

Answer to requirement III:

Yes, it can be stated that there is a legislative and professional requirement of

monitoring as well as reviewing the tax document. Regularly reviewing the legislation and

regulation which affects the working environment. The monitoring and reviewing of tax

11TAX PLAN AND COMPLIANCE

document is considered important because it helps in preserving the sensitive information that

are confidential and disclosing these information only to those that need it and when

disclosing the same in a legal manner. It is recommended to avoid those situations that simply

threatens the professional independence.

Part C: Scenario 3:

Answer to question I:

The ATO normally aims to lower the risk of tax crime by making the tax and super

system secure. In context of Benjamin, this implies that a systematic solutions must be

develop which remove the opportunity for people to commit the crime and avoid the

detection. The entire crime treatment procedure should be adopted as this will allow

Benjamin in providing a long-term change in participation by removing the opportunity of

repeating the offence. The review techniques which can be applied to diagnose the fraudulent

and dishonest business operations of Benjamin is given below;

a. Securing systems and procedure: Tax crime can be prevented by designing a

corporate and trusted third party systems to rely on.

b. Sustainable compliance: Compliance strategies must emphasize on attaining the

sustainable improvement in business compliance.

c. Robust law and administration: Benjamin should adopt the legal and administrative

framework in focussing on eliminating the opportunities for tax crime.

Answer to question II:

Normally, the ATO identifies the risk of compliance when it reviews their tax affairs.

The ATO might take the decision of conducting an audit if it is able to recognize the areas of

concerns which requires closer examination. The ATO is normally guided by the facts and

will not necessary adhere with the each step of the typical tax assurance procedure. The ATO

document is considered important because it helps in preserving the sensitive information that

are confidential and disclosing these information only to those that need it and when

disclosing the same in a legal manner. It is recommended to avoid those situations that simply

threatens the professional independence.

Part C: Scenario 3:

Answer to question I:

The ATO normally aims to lower the risk of tax crime by making the tax and super

system secure. In context of Benjamin, this implies that a systematic solutions must be

develop which remove the opportunity for people to commit the crime and avoid the

detection. The entire crime treatment procedure should be adopted as this will allow

Benjamin in providing a long-term change in participation by removing the opportunity of

repeating the offence. The review techniques which can be applied to diagnose the fraudulent

and dishonest business operations of Benjamin is given below;

a. Securing systems and procedure: Tax crime can be prevented by designing a

corporate and trusted third party systems to rely on.

b. Sustainable compliance: Compliance strategies must emphasize on attaining the

sustainable improvement in business compliance.

c. Robust law and administration: Benjamin should adopt the legal and administrative

framework in focussing on eliminating the opportunities for tax crime.

Answer to question II:

Normally, the ATO identifies the risk of compliance when it reviews their tax affairs.

The ATO might take the decision of conducting an audit if it is able to recognize the areas of

concerns which requires closer examination. The ATO is normally guided by the facts and

will not necessary adhere with the each step of the typical tax assurance procedure. The ATO

12TAX PLAN AND COMPLIANCE

usually reviews the business based on the level of higher level by using the risk filtering

procedure. The ATO makes the use of cooperative compliance approach to recognize non-

compliance and evaluate the risk as and when they originate. The nature of transaction and

the knowledge of compliance risk signifies that it would proceed directly for audit following

the analysis of risks.

usually reviews the business based on the level of higher level by using the risk filtering

procedure. The ATO makes the use of cooperative compliance approach to recognize non-

compliance and evaluate the risk as and when they originate. The nature of transaction and

the knowledge of compliance risk signifies that it would proceed directly for audit following

the analysis of risks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAX PLAN AND COMPLIANCE

Bibliographies:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Bibliographies:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.