Income Tax Assignment - Analysis of Tax Residency and Deductions

VerifiedAdded on 2023/05/30

|7

|1996

|267

Homework Assignment

AI Summary

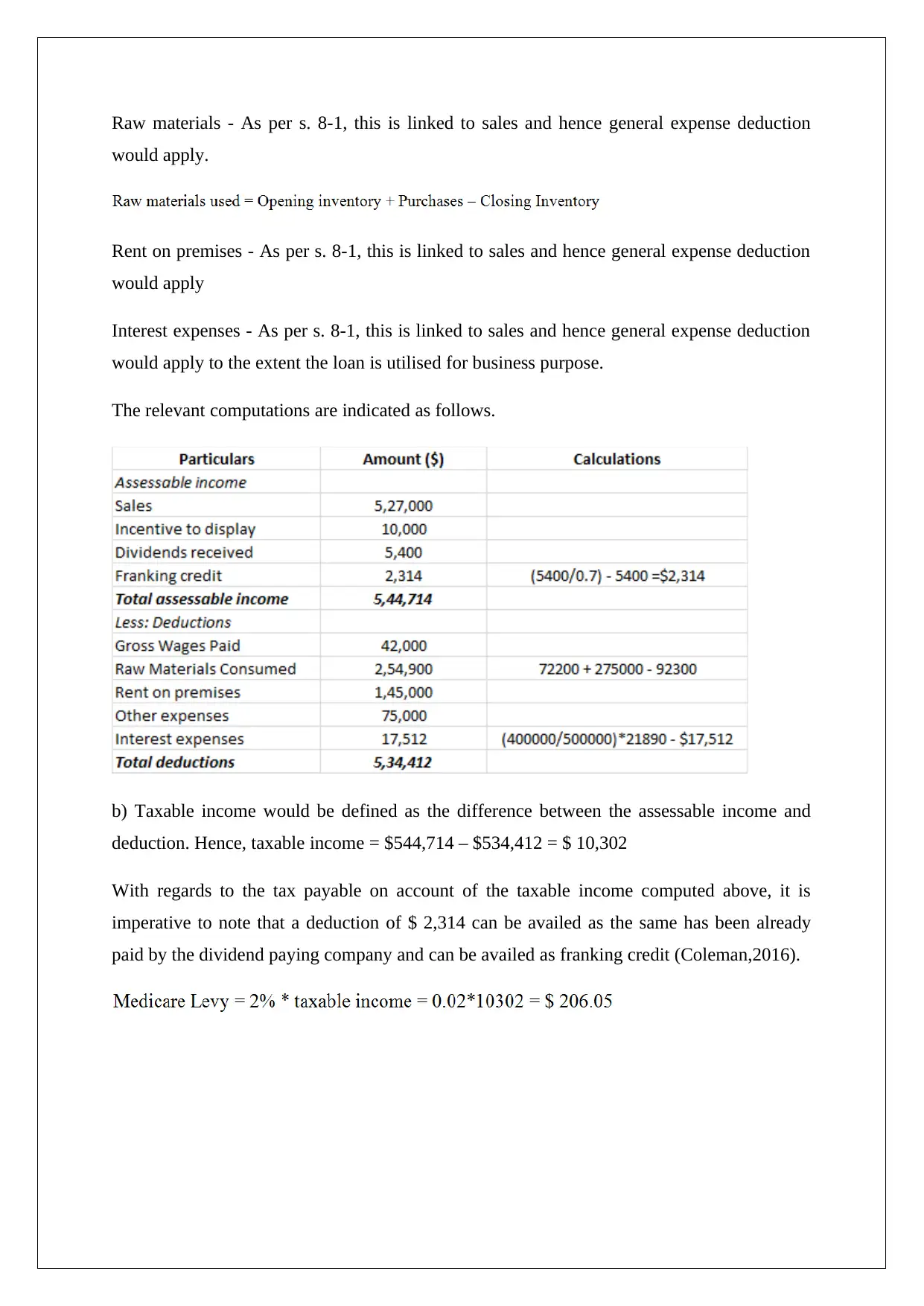

This assignment solution addresses several income tax scenarios. Question 1 focuses on determining Amity's tax residency for the year ending June 30, 2016, considering her employment in Australia, relocation to Kiribati, and relevant case law like F.C. of T. v. Applegate. Question 2 examines a barter transaction and the tax implications of a prize, referencing cases like F.C. of T. v. Cooke & Sherden and Scott v. Federal Commissioner of Taxation. Question 3 explores tax deductions related to loan interest for a property used for both residential and commercial purposes, and also for a business that has wound up, referencing Ronpibon Tin v FC of T. Finally, Question 4 analyses assessable income and deductible expenses for a business, calculating taxable income and tax payable, including franking credits. The solution utilizes relevant sections of ITAA 1936 and ITAA 1997, as well as various case laws to support its conclusions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.