Tax Law: Analysis of Deductibility, Tax Accounting & GST Implications

VerifiedAdded on 2023/03/30

|23

|3978

|124

Report

AI Summary

This assignment delves into various aspects of tax law, including the deductibility of lump sum payments, the tax treatment of different business transactions, and Goods and Services Tax (GST) implications. It analyzes scenarios involving capital and revenue expenditures, repair expenses, and depreciation methods. The report applies relevant sections of the Income Tax Assessment Act (ITAA) and examines case laws to determine tax liabilities for individuals, partnerships, and companies. Key tax accounting principles, such as cash and accrual methods, are discussed in the context of business operations. The analysis covers topics like passive ownership in partnerships, joint receipt of income, and the calculation of tax payable or refundable for shareholders.

TAX

TABLE OF CONTENT

TABLE OF CONTENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

S

QUESTION 1.............................................................................................................................1

PART A......................................................................................................................................1

Advise the deductibility of the lump sum payments..............................................................1

i)..............................................................................................................................................1

ii).............................................................................................................................................1

iii)...........................................................................................................................................1

iv)............................................................................................................................................2

PART B......................................................................................................................................2

i)..............................................................................................................................................2

ii).............................................................................................................................................2

iii)...........................................................................................................................................2

iv)............................................................................................................................................2

v).............................................................................................................................................3

vi)............................................................................................................................................3

QUESTION 2.............................................................................................................................3

PART A......................................................................................................................................3

i)..............................................................................................................................................3

ii).............................................................................................................................................3

iii)...........................................................................................................................................4

iv)............................................................................................................................................4

v).............................................................................................................................................4

vi)............................................................................................................................................4

PART B......................................................................................................................................4

Advise IPL about the tax treatment of the amounts including discussion of key tax

accounting principles, legislations ad case laws.....................................................................4

i)..............................................................................................................................................4

ii).............................................................................................................................................5

iii)...........................................................................................................................................5

iv)............................................................................................................................................6

v).............................................................................................................................................6

QUESTION 3.............................................................................................................................6

Advise BOB and Linda of the tax liabilities..........................................................................6

QUESTION 1.............................................................................................................................1

PART A......................................................................................................................................1

Advise the deductibility of the lump sum payments..............................................................1

i)..............................................................................................................................................1

ii).............................................................................................................................................1

iii)...........................................................................................................................................1

iv)............................................................................................................................................2

PART B......................................................................................................................................2

i)..............................................................................................................................................2

ii).............................................................................................................................................2

iii)...........................................................................................................................................2

iv)............................................................................................................................................2

v).............................................................................................................................................3

vi)............................................................................................................................................3

QUESTION 2.............................................................................................................................3

PART A......................................................................................................................................3

i)..............................................................................................................................................3

ii).............................................................................................................................................3

iii)...........................................................................................................................................4

iv)............................................................................................................................................4

v).............................................................................................................................................4

vi)............................................................................................................................................4

PART B......................................................................................................................................4

Advise IPL about the tax treatment of the amounts including discussion of key tax

accounting principles, legislations ad case laws.....................................................................4

i)..............................................................................................................................................4

ii).............................................................................................................................................5

iii)...........................................................................................................................................5

iv)............................................................................................................................................6

v).............................................................................................................................................6

QUESTION 3.............................................................................................................................6

Advise BOB and Linda of the tax liabilities..........................................................................6

i)..............................................................................................................................................7

ii).............................................................................................................................................7

iii)...........................................................................................................................................7

iv)............................................................................................................................................7

v).............................................................................................................................................7

vi)............................................................................................................................................8

vii)...........................................................................................................................................8

viii).........................................................................................................................................8

ix)............................................................................................................................................8

x).............................................................................................................................................8

QUESTION 4.............................................................................................................................8

PART A......................................................................................................................................8

Explain relevant parties using tax legislations and cases the tax payable under this trust

arrangement............................................................................................................................8

i)..............................................................................................................................................8

ii).............................................................................................................................................9

iii)...........................................................................................................................................9

iv)............................................................................................................................................9

v).............................................................................................................................................9

vi)..........................................................................................................................................10

PART B....................................................................................................................................10

Explain to bob the trustee of BLF family trust with reference to legislation and case law..10

i)............................................................................................................................................10

ii)...........................................................................................................................................10

iii).........................................................................................................................................10

iv)..........................................................................................................................................10

v)...........................................................................................................................................10

vi)..........................................................................................................................................10

QUESTION 5...........................................................................................................................11

PART A....................................................................................................................................11

Advise Maddox meats pty ltd about the GST implications showing calculations and

legislations............................................................................................................................11

i)............................................................................................................................................11

ii)...........................................................................................................................................11

3

ii).............................................................................................................................................7

iii)...........................................................................................................................................7

iv)............................................................................................................................................7

v).............................................................................................................................................7

vi)............................................................................................................................................8

vii)...........................................................................................................................................8

viii).........................................................................................................................................8

ix)............................................................................................................................................8

x).............................................................................................................................................8

QUESTION 4.............................................................................................................................8

PART A......................................................................................................................................8

Explain relevant parties using tax legislations and cases the tax payable under this trust

arrangement............................................................................................................................8

i)..............................................................................................................................................8

ii).............................................................................................................................................9

iii)...........................................................................................................................................9

iv)............................................................................................................................................9

v).............................................................................................................................................9

vi)..........................................................................................................................................10

PART B....................................................................................................................................10

Explain to bob the trustee of BLF family trust with reference to legislation and case law..10

i)............................................................................................................................................10

ii)...........................................................................................................................................10

iii).........................................................................................................................................10

iv)..........................................................................................................................................10

v)...........................................................................................................................................10

vi)..........................................................................................................................................10

QUESTION 5...........................................................................................................................11

PART A....................................................................................................................................11

Advise Maddox meats pty ltd about the GST implications showing calculations and

legislations............................................................................................................................11

i)............................................................................................................................................11

ii)...........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

iii).........................................................................................................................................11

iv)..........................................................................................................................................11

v)...........................................................................................................................................12

vi)..........................................................................................................................................12

vii).........................................................................................................................................12

viii).......................................................................................................................................12

ix)..........................................................................................................................................12

PART B....................................................................................................................................12

Explain using legislation ad case law...................................................................................12

ii)...........................................................................................................................................12

a)...........................................................................................................................................12

b)...........................................................................................................................................12

c)...........................................................................................................................................13

iii).........................................................................................................................................13

QUESTION 6...........................................................................................................................13

Calculate tax payable/refundable for each shareholder........................................................13

REFERENCES.........................................................................................................................14

4

iv)..........................................................................................................................................11

v)...........................................................................................................................................12

vi)..........................................................................................................................................12

vii).........................................................................................................................................12

viii).......................................................................................................................................12

ix)..........................................................................................................................................12

PART B....................................................................................................................................12

Explain using legislation ad case law...................................................................................12

ii)...........................................................................................................................................12

a)...........................................................................................................................................12

b)...........................................................................................................................................12

c)...........................................................................................................................................13

iii).........................................................................................................................................13

QUESTION 6...........................................................................................................................13

Calculate tax payable/refundable for each shareholder........................................................13

REFERENCES.........................................................................................................................14

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 1

PART A

Advise the deductibility of the lump sum payments

i)

Issue- To know that non-deductible capital expense relates to the business structure or not

Law- Section 8-1 of ITAA

Application-The person cannot deduct the loss from its income if they satisfy the given

condition that a loss arises of a nature to the capital and a specific loss arises from an activity

that is basically associated with private as well as domestic in nature.

Conclusion-A lumps sum payment of $10000 falls under the first category where this

payment made for producing income by selling the Italian brand olive oil, and this is not a

non-deducible capital expense.

ii)

Issue- The deductibility of the capital expenses and revenue expenses

Law- nature of expenses under ITAA

Application-The deductibility of the capital expenses and revenue expenses determine by

assessing the nature of two of the expenditures. The capital expense is related to the assets

held for a long-time period in an entity.

Conclusion- The revenue expense belongs to the business processes is incurred for

generating the revenues.

iii)

Issue- Deductibility of the lump payment

Law- The deductibility of the lump payment depends on some of the conditions which need

to consider in assessing the deduction of all the lump sum payments are given as below:

The benefit of one party while making the payment

Payment made for the future contract

1

PART A

Advise the deductibility of the lump sum payments

i)

Issue- To know that non-deductible capital expense relates to the business structure or not

Law- Section 8-1 of ITAA

Application-The person cannot deduct the loss from its income if they satisfy the given

condition that a loss arises of a nature to the capital and a specific loss arises from an activity

that is basically associated with private as well as domestic in nature.

Conclusion-A lumps sum payment of $10000 falls under the first category where this

payment made for producing income by selling the Italian brand olive oil, and this is not a

non-deducible capital expense.

ii)

Issue- The deductibility of the capital expenses and revenue expenses

Law- nature of expenses under ITAA

Application-The deductibility of the capital expenses and revenue expenses determine by

assessing the nature of two of the expenditures. The capital expense is related to the assets

held for a long-time period in an entity.

Conclusion- The revenue expense belongs to the business processes is incurred for

generating the revenues.

iii)

Issue- Deductibility of the lump payment

Law- The deductibility of the lump payment depends on some of the conditions which need

to consider in assessing the deduction of all the lump sum payments are given as below:

The benefit of one party while making the payment

Payment made for the future contract

1

Application- The expenses incurred by Dixon J set and published in the sun newspapers

contain one of a feature of the lump sum payment that expense incurred for getting the

benefit.

Conclusion- It is concluded that the lump sum payment belongs to the benefit received by

Dixon J

iv)

Issue- Determine the nature of the transaction by BP Australia

Law-

As per “Income tax assessment act 1997”, the basic of the capital expenditure is

associated with the expense which meets the below mention conditions.

Application-In the present scenario, the overall expenditure which is sustained by BP

Australia for selling petrol in the petrol station was earlier recognized as revenue is a capital

expenditure.

Conclusion- It is summarized that this transaction is consider as capital expenditure and not

revenue.

PART B

i)

Issue- To determine the deductibility of repair expenses

Law- Repair Expenses under section 25-10

Application- Repair expenses covered under section 25-10 should be of capital nature, which

is related to the repairing and the improvement of building by adding new material.

Conclusion- The wooden floor will satisfy the repair and its definition under the repairs of

section 25-10

ii)

Issue- Judge the nature of the assets under division 40

Law- Division 40 denotes the capital works deduction, which shows the production of

income that comprises of building

2

contain one of a feature of the lump sum payment that expense incurred for getting the

benefit.

Conclusion- It is concluded that the lump sum payment belongs to the benefit received by

Dixon J

iv)

Issue- Determine the nature of the transaction by BP Australia

Law-

As per “Income tax assessment act 1997”, the basic of the capital expenditure is

associated with the expense which meets the below mention conditions.

Application-In the present scenario, the overall expenditure which is sustained by BP

Australia for selling petrol in the petrol station was earlier recognized as revenue is a capital

expenditure.

Conclusion- It is summarized that this transaction is consider as capital expenditure and not

revenue.

PART B

i)

Issue- To determine the deductibility of repair expenses

Law- Repair Expenses under section 25-10

Application- Repair expenses covered under section 25-10 should be of capital nature, which

is related to the repairing and the improvement of building by adding new material.

Conclusion- The wooden floor will satisfy the repair and its definition under the repairs of

section 25-10

ii)

Issue- Judge the nature of the assets under division 40

Law- Division 40 denotes the capital works deduction, which shows the production of

income that comprises of building

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application- The improvements related to structure is expected over a basic period of with

the assets that are depreciating simultaneously.

Conclusion- Wooden floor constituents as a depreciable asset which meets the Division 40 of

the capital allowance for improvements in the buildings.

iii)

Issue- Test nature of $20000 expense under repair

Law- Repairs and maintenance under section 25-10.

Application- $20000 spent for the repairing and the resealing the floorboard is required for

renovating the house will fall under the category of repairs and maintenance under section

25-10.

Conclusion- This expense will meet the criteria’s of the repair expense.

iv)

Issue- Deductibility of the wooden floor

Law- Deductible repair as this meets the requirements under section 25-10.

Application- $20000 spent for replacing the floorboards in the form of wood is a deductible

repair as this meets the requirements under section 25-10.

Conclusion- This expense incurred by an individual’s meet the definition of the repair and not

the improvement under the repair expense.

v)

Issue- Test the expense as a repair or improvement

Law- Deductible repair as this meets the requirements under section 25-10.

Application-$50000 spent on the reinforcing the floor which is considered as an improvement

to the building as these expenses do not cover under section 25-10 to be called as a repair.

Conclusion-The improvement will cover under the capital works allowance where the whole

wooden floor has replaced and not repaired.

3

the assets that are depreciating simultaneously.

Conclusion- Wooden floor constituents as a depreciable asset which meets the Division 40 of

the capital allowance for improvements in the buildings.

iii)

Issue- Test nature of $20000 expense under repair

Law- Repairs and maintenance under section 25-10.

Application- $20000 spent for the repairing and the resealing the floorboard is required for

renovating the house will fall under the category of repairs and maintenance under section

25-10.

Conclusion- This expense will meet the criteria’s of the repair expense.

iv)

Issue- Deductibility of the wooden floor

Law- Deductible repair as this meets the requirements under section 25-10.

Application- $20000 spent for replacing the floorboards in the form of wood is a deductible

repair as this meets the requirements under section 25-10.

Conclusion- This expense incurred by an individual’s meet the definition of the repair and not

the improvement under the repair expense.

v)

Issue- Test the expense as a repair or improvement

Law- Deductible repair as this meets the requirements under section 25-10.

Application-$50000 spent on the reinforcing the floor which is considered as an improvement

to the building as these expenses do not cover under section 25-10 to be called as a repair.

Conclusion-The improvement will cover under the capital works allowance where the whole

wooden floor has replaced and not repaired.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

vi)

Issue- Consideration of $50000 payment under 40 division or not

Law- Division 40 of the Australian tax

Application- Division 40 of the Australian tax act states that a capital asset will be

depreciable over some time will fall under the category of a capital asset.

Conclusion- Following these criteria, a $50000 payment is considered as a capital asset as

this expense is a depreciable asset.

QUESTION 2

PART A

i)

Issue- Determining the depreciation

Law- Methods of depreciation such as prime cost and diminishing value

Application-

Method of Prime Cost

Asset cost*(Days held/365)*(100%/asset’s life)

Method of diminishing the value

This is the basic formula which is associated with the diminishing of the values:

Base value × (days held ÷ 365) × (200% ÷ asset’s effective life)

Conclusion-

Capital allowance of oil vat will determine by value method which are diminishing in nature

as the specific values of the assets are in declinationof tom nee period to another.

ii)

Issue- Amount of depreciation and cost of installation

Law- Section 40-180 and section 40-190

4

Issue- Consideration of $50000 payment under 40 division or not

Law- Division 40 of the Australian tax

Application- Division 40 of the Australian tax act states that a capital asset will be

depreciable over some time will fall under the category of a capital asset.

Conclusion- Following these criteria, a $50000 payment is considered as a capital asset as

this expense is a depreciable asset.

QUESTION 2

PART A

i)

Issue- Determining the depreciation

Law- Methods of depreciation such as prime cost and diminishing value

Application-

Method of Prime Cost

Asset cost*(Days held/365)*(100%/asset’s life)

Method of diminishing the value

This is the basic formula which is associated with the diminishing of the values:

Base value × (days held ÷ 365) × (200% ÷ asset’s effective life)

Conclusion-

Capital allowance of oil vat will determine by value method which are diminishing in nature

as the specific values of the assets are in declinationof tom nee period to another.

ii)

Issue- Amount of depreciation and cost of installation

Law- Section 40-180 and section 40-190

4

Application- Section 40-180 states the depreciating asset holds by an individual for a

stipulated tie period to know its costs in determining the capital allowance or depreciation

using different methods.

Conclusion- Above sections will help in resolving the issue in determining the depreciation

iii)

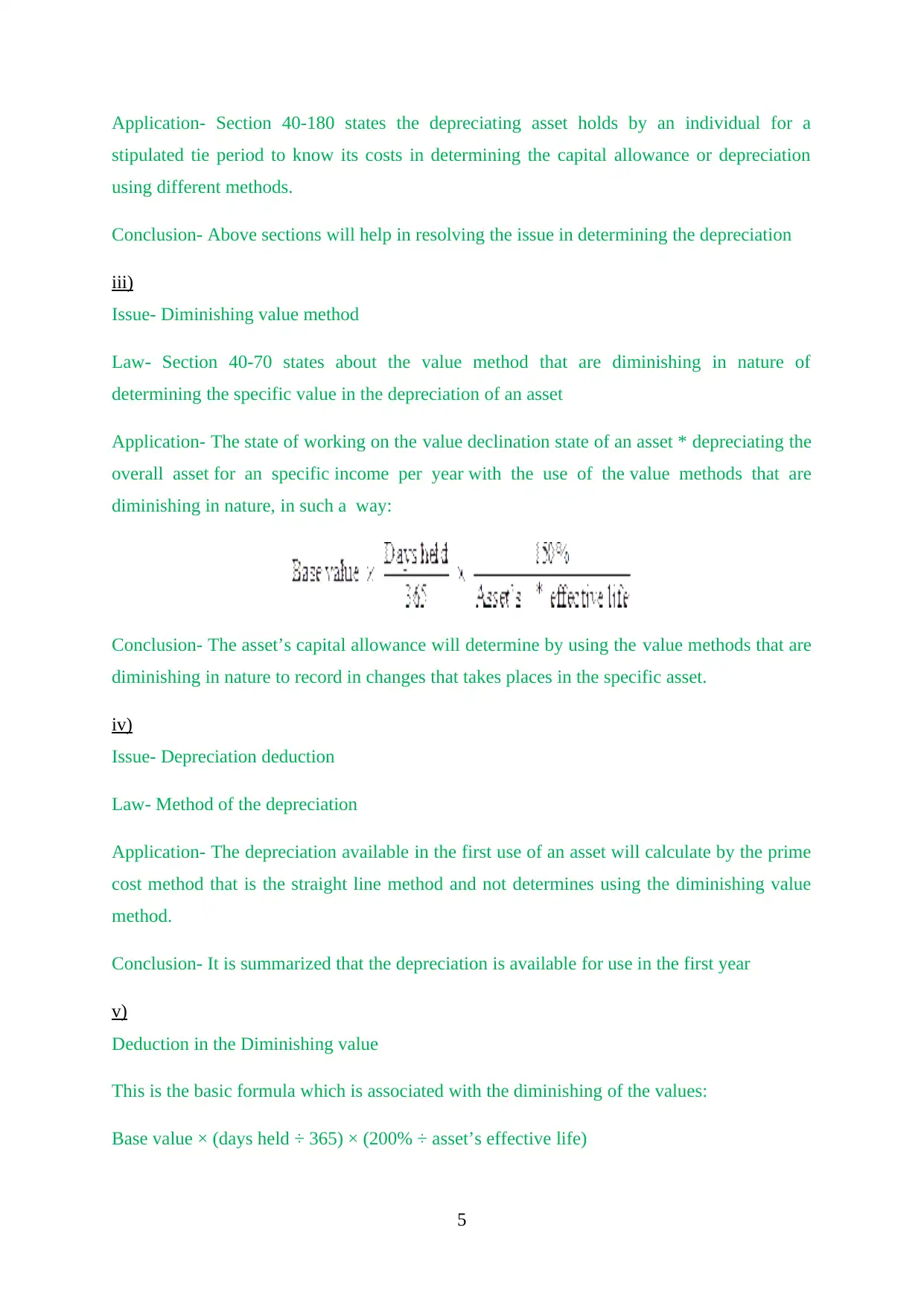

Issue- Diminishing value method

Law- Section 40-70 states about the value method that are diminishing in nature of

determining the specific value in the depreciation of an asset

Application- The state of working on the value declination state of an asset * depreciating the

overall asset for an specific income per year with the use of the value methods that are

diminishing in nature, in such a way:

Conclusion- The asset’s capital allowance will determine by using the value methods that are

diminishing in nature to record in changes that takes places in the specific asset.

iv)

Issue- Depreciation deduction

Law- Method of the depreciation

Application- The depreciation available in the first use of an asset will calculate by the prime

cost method that is the straight line method and not determines using the diminishing value

method.

Conclusion- It is summarized that the depreciation is available for use in the first year

v)

Deduction in the Diminishing value

This is the basic formula which is associated with the diminishing of the values:

Base value × (days held ÷ 365) × (200% ÷ asset’s effective life)

5

stipulated tie period to know its costs in determining the capital allowance or depreciation

using different methods.

Conclusion- Above sections will help in resolving the issue in determining the depreciation

iii)

Issue- Diminishing value method

Law- Section 40-70 states about the value method that are diminishing in nature of

determining the specific value in the depreciation of an asset

Application- The state of working on the value declination state of an asset * depreciating the

overall asset for an specific income per year with the use of the value methods that are

diminishing in nature, in such a way:

Conclusion- The asset’s capital allowance will determine by using the value methods that are

diminishing in nature to record in changes that takes places in the specific asset.

iv)

Issue- Depreciation deduction

Law- Method of the depreciation

Application- The depreciation available in the first use of an asset will calculate by the prime

cost method that is the straight line method and not determines using the diminishing value

method.

Conclusion- It is summarized that the depreciation is available for use in the first year

v)

Deduction in the Diminishing value

This is the basic formula which is associated with the diminishing of the values:

Base value × (days held ÷ 365) × (200% ÷ asset’s effective life)

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= $2396(55000*212/365)*(200%/20)

vi)

Method related to prime cost

Asset cost*(Days held/365)*(100%/asset’s life)

$1597= ($55000*212/365)*(100%/20)

PART B

Advise IPL about the tax treatment of the amounts including discussion of key tax accounting

principles, legislations and case laws

i)

Issue- Method of accounting

Law- Cash and non-cash accounting

Application- The methods of Cash accounting on the following:

Person that is not carrying a business, but holds on the enterprises ' Goods and Service Tax

turnover' is about of $2 million or less in number.

Schools owned by government

Charitable institution that are endorsed in nature or the specific trustee which are

associated with the endorsed charitable fund

Entity that are Gift-deductible in nature

Conclusion

IPL Pty Ltd Company prefers the accrual method of accounting for all its business

transactions for assessing its tax return of a particular assessment year rather than using cash

basis of accounting.

ii)

Issue- Method of accounting

Law- Accrual method of accounting

Application- As an entity uses an accrual method of accounting for determining its tax

liabilities of that year, MM medium sized's trading stock sales will be taxed for GST

6

vi)

Method related to prime cost

Asset cost*(Days held/365)*(100%/asset’s life)

$1597= ($55000*212/365)*(100%/20)

PART B

Advise IPL about the tax treatment of the amounts including discussion of key tax accounting

principles, legislations and case laws

i)

Issue- Method of accounting

Law- Cash and non-cash accounting

Application- The methods of Cash accounting on the following:

Person that is not carrying a business, but holds on the enterprises ' Goods and Service Tax

turnover' is about of $2 million or less in number.

Schools owned by government

Charitable institution that are endorsed in nature or the specific trustee which are

associated with the endorsed charitable fund

Entity that are Gift-deductible in nature

Conclusion

IPL Pty Ltd Company prefers the accrual method of accounting for all its business

transactions for assessing its tax return of a particular assessment year rather than using cash

basis of accounting.

ii)

Issue- Method of accounting

Law- Accrual method of accounting

Application- As an entity uses an accrual method of accounting for determining its tax

liabilities of that year, MM medium sized's trading stock sales will be taxed for GST

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion- The sales transactions are incurred by an entity as this expense is not a personal

expense as its s a business expense.

iii)

Issue- state the deductibility of the provision of $28000

Law- The basic amount which is paid in the income year and to the individual for whom

there is a leave relation states that:

Application-The entity is not at all necessary in the making of payments with respect of

such purposes of leave to another specific entity with the other one that has already begun in

starting to make payments in the basic respect of leave.

Conclusion

The overall provision that are subjected to $28000 and made in the accrued leave to the

paymentout of which $19000 has generally been sustained, and the others will be carried

forward to the next year for the purpose of utilization.

iv)

Issue-Nature of the expense

Law- Income tax act of Australia shows section 8-1 about the deductibility of the general

deductions to be made in the business as per the nature of the transactions such as capital or

revenue.

Application- In this case, electricity and the telephone expenses will satisfy the conditions of

section 8-1 as these expenses related to capital nature as this is fixed expenses.

Conclusion- It is summarized from the above that the electricity expense is of capital nature

v)

Issue-Inclusion of $26000 in the current period

Law- Section 8-1 of the ITAA

Application- An expense of $26000 related to the previous year but shown in the current

books of account will be written off from the current year as this expense has already paid in

the previous year's tax return.

7

expense as its s a business expense.

iii)

Issue- state the deductibility of the provision of $28000

Law- The basic amount which is paid in the income year and to the individual for whom

there is a leave relation states that:

Application-The entity is not at all necessary in the making of payments with respect of

such purposes of leave to another specific entity with the other one that has already begun in

starting to make payments in the basic respect of leave.

Conclusion

The overall provision that are subjected to $28000 and made in the accrued leave to the

paymentout of which $19000 has generally been sustained, and the others will be carried

forward to the next year for the purpose of utilization.

iv)

Issue-Nature of the expense

Law- Income tax act of Australia shows section 8-1 about the deductibility of the general

deductions to be made in the business as per the nature of the transactions such as capital or

revenue.

Application- In this case, electricity and the telephone expenses will satisfy the conditions of

section 8-1 as these expenses related to capital nature as this is fixed expenses.

Conclusion- It is summarized from the above that the electricity expense is of capital nature

v)

Issue-Inclusion of $26000 in the current period

Law- Section 8-1 of the ITAA

Application- An expense of $26000 related to the previous year but shown in the current

books of account will be written off from the current year as this expense has already paid in

the previous year's tax return.

7

Conclusion- It is concluded that $26000 is related to the prior period as this has deducted

from the business.

QUESTION 3

Advise BOB and Linda of the tax liabilities

i)

Issue- To know the passive ownership in the partnership

Law-

The partnership should be registered with the GST, in case of annual GST turnover

that is $75,000 or may be more.

Application- As per the partnership law's features mention above, the bob and Linda hold

passive ownership in a partnership business, as the property is jointly owned by these two

partners.

Conclusion- The profit received from it will get taxed in the hands of these two partners as

according to their share in the partnership.

ii)

Issue-To know the business carry on by partners

Law- The section 995-1 of income tax assessment act 1997

Application- The section 995-1 of income tax assessment act 1997 will state the definition of

the common ownership to shows the common ownership of Bob and Linda on property.

(a) They are specific members of the same category * fully-owned group; or

(b) The direct and the indirect ownership * of shares in individual companies (through the

interposition of the companies and basic trusts) that the ownership is generally held by the

individuals in a specific proportions.

Conclusion- It is concluded from the above that Bob and Linda has carried business through

direct ownership of the real estate property.

iii)

Issue- Jointly receipt of income

8

from the business.

QUESTION 3

Advise BOB and Linda of the tax liabilities

i)

Issue- To know the passive ownership in the partnership

Law-

The partnership should be registered with the GST, in case of annual GST turnover

that is $75,000 or may be more.

Application- As per the partnership law's features mention above, the bob and Linda hold

passive ownership in a partnership business, as the property is jointly owned by these two

partners.

Conclusion- The profit received from it will get taxed in the hands of these two partners as

according to their share in the partnership.

ii)

Issue-To know the business carry on by partners

Law- The section 995-1 of income tax assessment act 1997

Application- The section 995-1 of income tax assessment act 1997 will state the definition of

the common ownership to shows the common ownership of Bob and Linda on property.

(a) They are specific members of the same category * fully-owned group; or

(b) The direct and the indirect ownership * of shares in individual companies (through the

interposition of the companies and basic trusts) that the ownership is generally held by the

individuals in a specific proportions.

Conclusion- It is concluded from the above that Bob and Linda has carried business through

direct ownership of the real estate property.

iii)

Issue- Jointly receipt of income

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.