Taxation Assignment: CGT and GST Analysis for HI6028, T2 2019, Holmes

VerifiedAdded on 2022/10/16

|12

|2724

|135

Homework Assignment

AI Summary

This taxation assignment analyzes two key issues: the eligibility of a property development company, City Sky Co., to claim input tax credit (ITC) for legal services under GST, and the calculation of Capital Tax Gain (CGT) for an individual, Emma, based on her property transactions. The assignment applies relevant sections of the Goods and Services Tax Act 1999 (GSTA) to determine the ITC amount and utilizes the Income Tax Assessment Act 1997 to compute Emma's CGT liability, considering factors like cost base, capital proceeds, and the holding period of assets. The solution provides detailed calculations and interpretations of the relevant tax laws to arrive at the final conclusions for both scenarios.

Running head: TAX

TAX

Name of the Student:

Name of the University:

Author Note:

TAX

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Answer to 1:

Issue

The issue that is required to be thrown light upon is whether City Sky Co. is liable of

claiming input tax credit.

Rules:

Input tax credit can be claimed on particular category of goods and services on which

GST can be made to impose (Carling 2015). Section 7.1 of the Goods and Services Tax 1999,

enumerates the provisions regarding GST as well as input tax credits. GST can be paid on

taxable importations and taxable supplies. The entitlements pertaining to input tax credit come

into existence on acquisitions and importations that are creditable (Barkoczy 2016).

For the purpose of claiming Input tax credit hereinafter referred to as ITC the services

and the goods must be subjected to GST. For imposing GST, two main elements are to be

fulfilled which are taxable importations together with taxable supplies. In usual course, taxable

importation or taxable supply is taken into consideration when the organization is subjected to

registration such that GST can be imposed on it.

Section 9.5, GSTA enumerates the taxable supplies. It provides a taxable supply is done

when a supply is made for consideration. Such kind of supply is required to be made during the

carrying on of any enterprise or business or to further the business carried on already

(Freudenberg 2017). Moreover such supply must be in connection with the zone of indirect

taxation. Moreover such supplier must have undergone registration or in the process of

Answer to 1:

Issue

The issue that is required to be thrown light upon is whether City Sky Co. is liable of

claiming input tax credit.

Rules:

Input tax credit can be claimed on particular category of goods and services on which

GST can be made to impose (Carling 2015). Section 7.1 of the Goods and Services Tax 1999,

enumerates the provisions regarding GST as well as input tax credits. GST can be paid on

taxable importations and taxable supplies. The entitlements pertaining to input tax credit come

into existence on acquisitions and importations that are creditable (Barkoczy 2016).

For the purpose of claiming Input tax credit hereinafter referred to as ITC the services

and the goods must be subjected to GST. For imposing GST, two main elements are to be

fulfilled which are taxable importations together with taxable supplies. In usual course, taxable

importation or taxable supply is taken into consideration when the organization is subjected to

registration such that GST can be imposed on it.

Section 9.5, GSTA enumerates the taxable supplies. It provides a taxable supply is done

when a supply is made for consideration. Such kind of supply is required to be made during the

carrying on of any enterprise or business or to further the business carried on already

(Freudenberg 2017). Moreover such supply must be in connection with the zone of indirect

taxation. Moreover such supplier must have undergone registration or in the process of

2TAX

registration. But it is to be taken into consideration that no supply is taxable supply when it is

free from GST or input taxed.

GST on taxable supplies is given under section 9.70 of the Act which is equal to 10% of

the valuation of the taxable supply.

Therefore, GST on taxable supply= 10percent on valuation of supply that is taxable.

Taxable supply value is provided under s 9.75 of the Act which states that value of any

taxable supply is price multiplied by 10/11. Here price refers to the consideration. When the

consideration is monetary then it must be devoid of GST discount and where the consideration is

not money then it includes GST. Hence the price equals to consideration without GST amount.

The creditable acquisitions have been provided under S. 11.5. It states that a creditable

acquisition occurs when anything has been acquired for any creditable reason absolutely or

partially. The creditable acquisition is also made in case a thing is supplied which is a taxable

supply. For these consideration is being paid against such supply. Moreover the tax payer must

be registered.

Meaning of acquisition is given under section 11.10 of the Act where acquisition can

include acquisition of goods, services, rights, supply and others.

The tax payer is entitled to input tax credit in respect of any taxable acquisition is made

by him. This is given under section 11.20. Moreover the amount of ITC for creditable type of

acquisitions is given under section 11.25. It enumerates that the ITC amount for any type of

creditable acquisition refers to an amount which is equal to the GST which can be paid on a

registration. But it is to be taken into consideration that no supply is taxable supply when it is

free from GST or input taxed.

GST on taxable supplies is given under section 9.70 of the Act which is equal to 10% of

the valuation of the taxable supply.

Therefore, GST on taxable supply= 10percent on valuation of supply that is taxable.

Taxable supply value is provided under s 9.75 of the Act which states that value of any

taxable supply is price multiplied by 10/11. Here price refers to the consideration. When the

consideration is monetary then it must be devoid of GST discount and where the consideration is

not money then it includes GST. Hence the price equals to consideration without GST amount.

The creditable acquisitions have been provided under S. 11.5. It states that a creditable

acquisition occurs when anything has been acquired for any creditable reason absolutely or

partially. The creditable acquisition is also made in case a thing is supplied which is a taxable

supply. For these consideration is being paid against such supply. Moreover the tax payer must

be registered.

Meaning of acquisition is given under section 11.10 of the Act where acquisition can

include acquisition of goods, services, rights, supply and others.

The tax payer is entitled to input tax credit in respect of any taxable acquisition is made

by him. This is given under section 11.20. Moreover the amount of ITC for creditable type of

acquisitions is given under section 11.25. It enumerates that the ITC amount for any type of

creditable acquisition refers to an amount which is equal to the GST which can be paid on a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

supplying of a thing that has been acquired. But it has to borne in mind that the ITC amount will

be subjected to reduction where such acquisition can be said to be creditable partially.

An organization that has undergone registration under scheme of GST can avail Input

Tax Credit in case of its creditable importation and acquisitions (Tran-Nam 2016). Such

organization or company has to be registered under GST scheme and for that such organization

or company as the case may be must carry on dealings related to its business activities. GST

imposition cannot be restricted on such company or organization. Moreover, such organization

or company must avail any supply or goods as end customer.

Application:

Here a company called City Sky Co is formed and it is a property developing and

investing company. The company in recent days bought a land block which is vacant and located

in Brisbane for the purpose of building 15 flats and selling them.

The company has contacted a lawyer named Maurice Blackburn for providing legal

service in this regard and he charged 33000 dollars for it. He had a trading business whose yearly

turnover is 300,000 $.

Section 9.5, GSTA enumerates the taxable supplies. It provides a taxable supply is done

when a supply is made for consideration. Such kind of supply is required to be made during the

carrying on of any enterprise or business or to further the business carried on already. Moreover

such supply must be in connection with the zone of indirect taxation. Moreover such supplier

must have undergone registration or in the process of registration. But it is to be taken into

consideration that no supply is taxable supply when it is free from GST or input taxed.

supplying of a thing that has been acquired. But it has to borne in mind that the ITC amount will

be subjected to reduction where such acquisition can be said to be creditable partially.

An organization that has undergone registration under scheme of GST can avail Input

Tax Credit in case of its creditable importation and acquisitions (Tran-Nam 2016). Such

organization or company has to be registered under GST scheme and for that such organization

or company as the case may be must carry on dealings related to its business activities. GST

imposition cannot be restricted on such company or organization. Moreover, such organization

or company must avail any supply or goods as end customer.

Application:

Here a company called City Sky Co is formed and it is a property developing and

investing company. The company in recent days bought a land block which is vacant and located

in Brisbane for the purpose of building 15 flats and selling them.

The company has contacted a lawyer named Maurice Blackburn for providing legal

service in this regard and he charged 33000 dollars for it. He had a trading business whose yearly

turnover is 300,000 $.

Section 9.5, GSTA enumerates the taxable supplies. It provides a taxable supply is done

when a supply is made for consideration. Such kind of supply is required to be made during the

carrying on of any enterprise or business or to further the business carried on already. Moreover

such supply must be in connection with the zone of indirect taxation. Moreover such supplier

must have undergone registration or in the process of registration. But it is to be taken into

consideration that no supply is taxable supply when it is free from GST or input taxed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

GST on taxable supplies is given under section 9.70 of the Act which is equal to 10% of

the valuation of the taxable supply.

Therefore, GST on taxable supply= 10percent on valuation of supply that is taxable.

Taxable supply value is provided under s 9.75 of the Act which states that value of any

taxable supply is price multiplied by 10/11. Here price refers to the consideration. When the

consideration is monetary then it must be devoid of GST discount and where the consideration is

not money then it includes GST. Hence the price equals to consideration without GST amount.

The creditable acquisitions have been provided under S. 11.5. It states that a creditable

acquisition occurs when anything has been acquired for any creditable reason absolutely or

partially. The creditable acquisition is also made in case a thing is supplied which is a taxable

supply. For these consideration is being paid against such supply. Moreover the tax payer must

be registered.

Meaning of acquisition is given under section 11.10 of the Act where acquisition can

include acquisition of goods, services, rights, supply and others.

The tax payer is entitled to input tax credit in respect of any taxable acquisition is made

by him. This is given under section 11.20. Moreover the amount of ITC for creditable type of

acquisitions is given under section 11.25. It enumerates that the ITC amount for any type of

creditable acquisition refers to an amount which is equal to the GST which can be paid on a

supplying of a thing that has been acquired. But it has to borne in mind that the ITC amount will

be subjected to reduction where such acquisition can be said to be creditable partially.

GST on taxable supplies is given under section 9.70 of the Act which is equal to 10% of

the valuation of the taxable supply.

Therefore, GST on taxable supply= 10percent on valuation of supply that is taxable.

Taxable supply value is provided under s 9.75 of the Act which states that value of any

taxable supply is price multiplied by 10/11. Here price refers to the consideration. When the

consideration is monetary then it must be devoid of GST discount and where the consideration is

not money then it includes GST. Hence the price equals to consideration without GST amount.

The creditable acquisitions have been provided under S. 11.5. It states that a creditable

acquisition occurs when anything has been acquired for any creditable reason absolutely or

partially. The creditable acquisition is also made in case a thing is supplied which is a taxable

supply. For these consideration is being paid against such supply. Moreover the tax payer must

be registered.

Meaning of acquisition is given under section 11.10 of the Act where acquisition can

include acquisition of goods, services, rights, supply and others.

The tax payer is entitled to input tax credit in respect of any taxable acquisition is made

by him. This is given under section 11.20. Moreover the amount of ITC for creditable type of

acquisitions is given under section 11.25. It enumerates that the ITC amount for any type of

creditable acquisition refers to an amount which is equal to the GST which can be paid on a

supplying of a thing that has been acquired. But it has to borne in mind that the ITC amount will

be subjected to reduction where such acquisition can be said to be creditable partially.

5TAX

An organization that has undergone registration under scheme of GST can avail Input

Tax Credit in case of its creditable importation and acquisitions. Such organization or company

has to be registered under GST scheme and for that such organization or company as the case

may be must carry on dealings related to its business activities. GST imposition cannot be

restricted on such company or organization. Moreover, such organization or company must avail

any supply or goods as end customer. This is also applicable to City Sky co.

Thus it has an eligibility of claiming ITC for making transaction with Maurice Blackburn.

Such transaction can be used to calculate the ITC.

The GST amount on the taxable supplies is given under s 9.70 of the Act which is equal

to 10% of the valuation of the taxable supply.

Therefore, GST on taxable supply = 10% on valuation of supply that is taxable.

Value of the taxable supply provided u/s 9.75 which states that value of any taxable

supply is price multiplied by 10/11 where price refers to the consideration.

Therefore, taxable value= (33000*10) divided by 11= 30000 dollars.

ITC= 10% * taxable value= (10* 30000)/100= 3000 $.

Conclusion:

Hence, City Sky Co. has the eligibility of claiming input tax credit of 3000 dollars.

Answer to question 2:

Issue:

An organization that has undergone registration under scheme of GST can avail Input

Tax Credit in case of its creditable importation and acquisitions. Such organization or company

has to be registered under GST scheme and for that such organization or company as the case

may be must carry on dealings related to its business activities. GST imposition cannot be

restricted on such company or organization. Moreover, such organization or company must avail

any supply or goods as end customer. This is also applicable to City Sky co.

Thus it has an eligibility of claiming ITC for making transaction with Maurice Blackburn.

Such transaction can be used to calculate the ITC.

The GST amount on the taxable supplies is given under s 9.70 of the Act which is equal

to 10% of the valuation of the taxable supply.

Therefore, GST on taxable supply = 10% on valuation of supply that is taxable.

Value of the taxable supply provided u/s 9.75 which states that value of any taxable

supply is price multiplied by 10/11 where price refers to the consideration.

Therefore, taxable value= (33000*10) divided by 11= 30000 dollars.

ITC= 10% * taxable value= (10* 30000)/100= 3000 $.

Conclusion:

Hence, City Sky Co. has the eligibility of claiming input tax credit of 3000 dollars.

Answer to question 2:

Issue:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

Issue to be analyzed here is regarding Emma’s transactions for which Capital Tax Gain is

to be computed.

Rules:

To analyze this case study, the Income Tax Assessment Act 1997 is to be considered

((Barkoczy 2016)). Here disposal of a CGT asset resulting into A1 CGT event has to be thrown

light given u/s 104.10. It states that an A1 CGT event occurs in case any CGT asset is disposed

of. The disposal of CGT asset takes place when the said transaction of disposing of the asset

involves transfer of ownership from one individual to another. Such change of ownership occurs

by either act of the parties involved or by law. But this change in ownership will not happen in

case there is only change in the nature of ownership but not in the actual ownership. Another

condition required to be satisfied here in case of happening of a CGT event is that the asset

whose transfer is involved must be acquired in respect of the tax payer after 20th September in

the year of 1985. If its acquisition occurs after this date then only it will be regarded as an asset

subjected to CGT else not. Those assets acquired after this date are known as post CGT assets

(Tran-Nam 2016).

Moreover in this regard s110.25 must be taken into consideration. This section

enumerates the rules in respect of CB. Here it is provided that CB of an asset has got 5 elements.

Those 5 elements are discussed below.

The first element as given under subsection 2 of the said section includes any money that

has been paid or has to be paid for the purpose of acquiring it. Where there is no monetary

consideration and a property is exchanged for another then the present market must be taken into

account.

Issue to be analyzed here is regarding Emma’s transactions for which Capital Tax Gain is

to be computed.

Rules:

To analyze this case study, the Income Tax Assessment Act 1997 is to be considered

((Barkoczy 2016)). Here disposal of a CGT asset resulting into A1 CGT event has to be thrown

light given u/s 104.10. It states that an A1 CGT event occurs in case any CGT asset is disposed

of. The disposal of CGT asset takes place when the said transaction of disposing of the asset

involves transfer of ownership from one individual to another. Such change of ownership occurs

by either act of the parties involved or by law. But this change in ownership will not happen in

case there is only change in the nature of ownership but not in the actual ownership. Another

condition required to be satisfied here in case of happening of a CGT event is that the asset

whose transfer is involved must be acquired in respect of the tax payer after 20th September in

the year of 1985. If its acquisition occurs after this date then only it will be regarded as an asset

subjected to CGT else not. Those assets acquired after this date are known as post CGT assets

(Tran-Nam 2016).

Moreover in this regard s110.25 must be taken into consideration. This section

enumerates the rules in respect of CB. Here it is provided that CB of an asset has got 5 elements.

Those 5 elements are discussed below.

The first element as given under subsection 2 of the said section includes any money that

has been paid or has to be paid for the purpose of acquiring it. Where there is no monetary

consideration and a property is exchanged for another then the present market must be taken into

account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

As per subsection 3, second element of CB denotes the incidental costs incurred by the

tax payer. Such costs will include the cost of giving away the concerned property.

The third element as given under subsection 4 includes the cost incurred for owning the

CGT asset. Those costs involve interest to be paid on the money that the taxpayer has borrowed

for asset acquisition, the cost of insurance, maintenance and repairing and other incidental costs.

Such asset is required to be acquired after 20.08.1991. Moreover according to provisions

contained under s 118.17 and s 108.30, E 3 is not applied on assets for personal use or on

collectables.

Section 110.25(5) enumerates that fourth element of CB is the expenses made by the tax

payer with the objective of preserving it or increasing its value. It also includes cost of installing

and moving the said asset too. However expenditure related to goodwill is not included here.

Section 110.25(6) includes the 5th element and it involves the cost incurred in relation to

legal title or right pertaining to the asset like establishing one’s title or defending such title or

right or even preserving the same.

Sec. 116.20 enumerates rules about capital proceeds. It enumerates that capital proceeds

or CP in respect of the CGT event is the total of money that is received or may be received in

relation to the happening an event. Where there is no monetary consideration and a property is

exchanged for another then the present market value of the concerned property must be taken

into account. Again when the said property held by the tax payer for more than 1 year, then 50%

is imposed on Capital gain that arises from disposing of the same.

Application:

As per subsection 3, second element of CB denotes the incidental costs incurred by the

tax payer. Such costs will include the cost of giving away the concerned property.

The third element as given under subsection 4 includes the cost incurred for owning the

CGT asset. Those costs involve interest to be paid on the money that the taxpayer has borrowed

for asset acquisition, the cost of insurance, maintenance and repairing and other incidental costs.

Such asset is required to be acquired after 20.08.1991. Moreover according to provisions

contained under s 118.17 and s 108.30, E 3 is not applied on assets for personal use or on

collectables.

Section 110.25(5) enumerates that fourth element of CB is the expenses made by the tax

payer with the objective of preserving it or increasing its value. It also includes cost of installing

and moving the said asset too. However expenditure related to goodwill is not included here.

Section 110.25(6) includes the 5th element and it involves the cost incurred in relation to

legal title or right pertaining to the asset like establishing one’s title or defending such title or

right or even preserving the same.

Sec. 116.20 enumerates rules about capital proceeds. It enumerates that capital proceeds

or CP in respect of the CGT event is the total of money that is received or may be received in

relation to the happening an event. Where there is no monetary consideration and a property is

exchanged for another then the present market value of the concerned property must be taken

into account. Again when the said property held by the tax payer for more than 1 year, then 50%

is imposed on Capital gain that arises from disposing of the same.

Application:

8TAX

Here Emma’s transactions are to be analyzed by means of which Capital Tax Gain is to

be computed.

Selling the land:

She bought the land for 250,000 dollars in 1991. It is known that the first element as

given u/s 110.25 (2) of the said section includes money that has been paid or has to be paid for

the purpose of acquiring it. Where there is no monetary consideration and a property is

exchanged for another then the concerned property’s present market value must be taken into

account. So, 250000$ forms element 1.

She also spent 5,000 as stamp duty, $10,000 in legal fees. This is element 2 as per

110.25(3).

While she was holding the property, she spent about 22000 $ for water rates, council

rates as well as insurance cost. This amounts to element 3 as per s110.25(4).

Moreover, she spent 5000 $ as an expense for resolving a legal dispute with her neighbor.

This amounts to E 5 as per section 110.25(6).

Further she had spent 27500$ for removal of the pine tree. This amounts to element 4 as

per section 110.25(5).

Other expenditure made by her includes 25000$ for advertisements, agent fee and legal

fee are not considered.

Hence, sale proceeds equals to = 1,000,000$- 25000$= 975000$.

Shares selling:

Here Emma’s transactions are to be analyzed by means of which Capital Tax Gain is to

be computed.

Selling the land:

She bought the land for 250,000 dollars in 1991. It is known that the first element as

given u/s 110.25 (2) of the said section includes money that has been paid or has to be paid for

the purpose of acquiring it. Where there is no monetary consideration and a property is

exchanged for another then the concerned property’s present market value must be taken into

account. So, 250000$ forms element 1.

She also spent 5,000 as stamp duty, $10,000 in legal fees. This is element 2 as per

110.25(3).

While she was holding the property, she spent about 22000 $ for water rates, council

rates as well as insurance cost. This amounts to element 3 as per s110.25(4).

Moreover, she spent 5000 $ as an expense for resolving a legal dispute with her neighbor.

This amounts to E 5 as per section 110.25(6).

Further she had spent 27500$ for removal of the pine tree. This amounts to element 4 as

per section 110.25(5).

Other expenditure made by her includes 25000$ for advertisements, agent fee and legal

fee are not considered.

Hence, sale proceeds equals to = 1,000,000$- 25000$= 975000$.

Shares selling:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

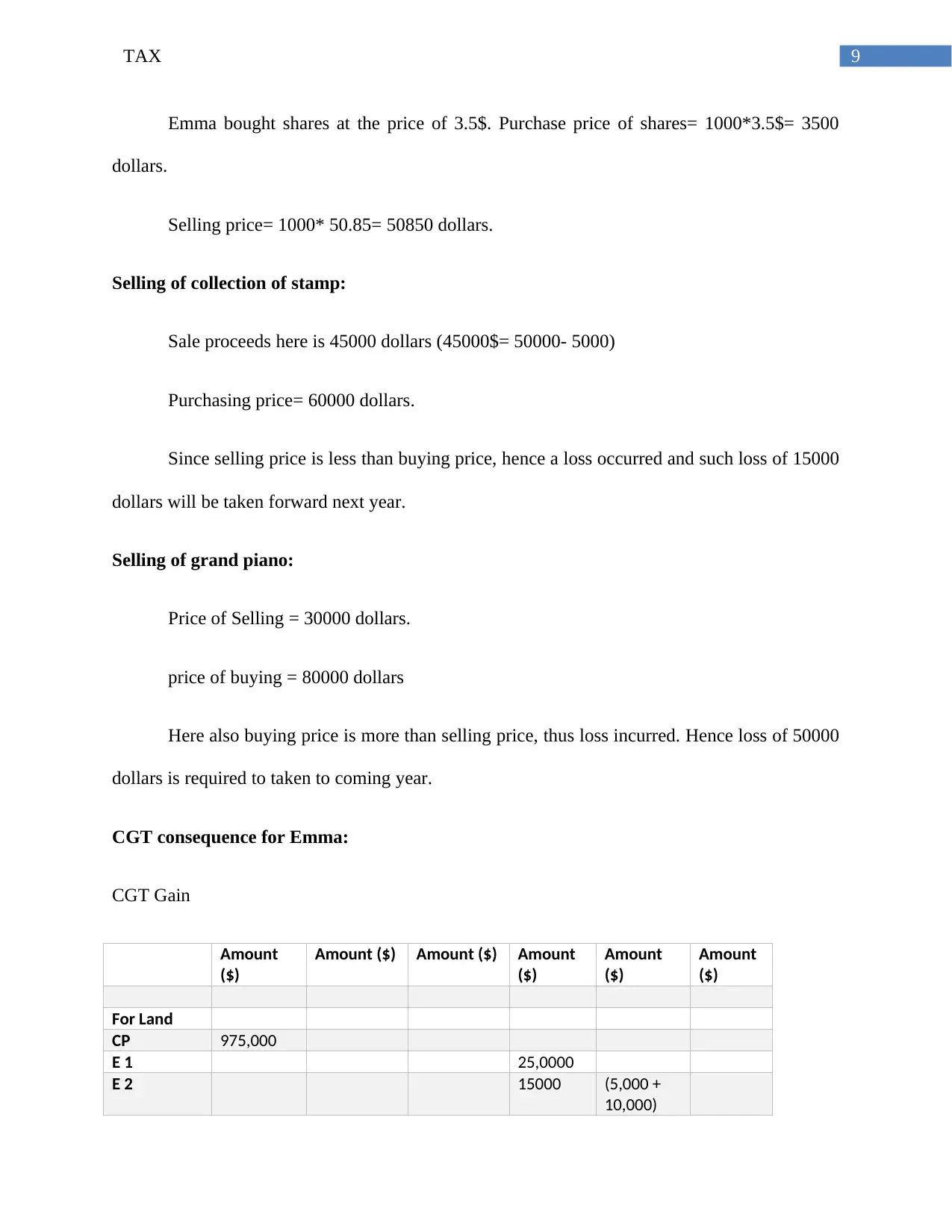

Emma bought shares at the price of 3.5$. Purchase price of shares= 1000*3.5$= 3500

dollars.

Selling price= 1000* 50.85= 50850 dollars.

Selling of collection of stamp:

Sale proceeds here is 45000 dollars (45000$= 50000- 5000)

Purchasing price= 60000 dollars.

Since selling price is less than buying price, hence a loss occurred and such loss of 15000

dollars will be taken forward next year.

Selling of grand piano:

Price of Selling = 30000 dollars.

price of buying = 80000 dollars

Here also buying price is more than selling price, thus loss incurred. Hence loss of 50000

dollars is required to taken to coming year.

CGT consequence for Emma:

CGT Gain

Amount

($)

Amount ($) Amount ($) Amount

($)

Amount

($)

Amount

($)

For Land

CP 975,000

E 1 25,0000

E 2 15000 (5,000 +

10,000)

Emma bought shares at the price of 3.5$. Purchase price of shares= 1000*3.5$= 3500

dollars.

Selling price= 1000* 50.85= 50850 dollars.

Selling of collection of stamp:

Sale proceeds here is 45000 dollars (45000$= 50000- 5000)

Purchasing price= 60000 dollars.

Since selling price is less than buying price, hence a loss occurred and such loss of 15000

dollars will be taken forward next year.

Selling of grand piano:

Price of Selling = 30000 dollars.

price of buying = 80000 dollars

Here also buying price is more than selling price, thus loss incurred. Hence loss of 50000

dollars is required to taken to coming year.

CGT consequence for Emma:

CGT Gain

Amount

($)

Amount ($) Amount ($) Amount

($)

Amount

($)

Amount

($)

For Land

CP 975,000

E 1 25,0000

E 2 15000 (5,000 +

10,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

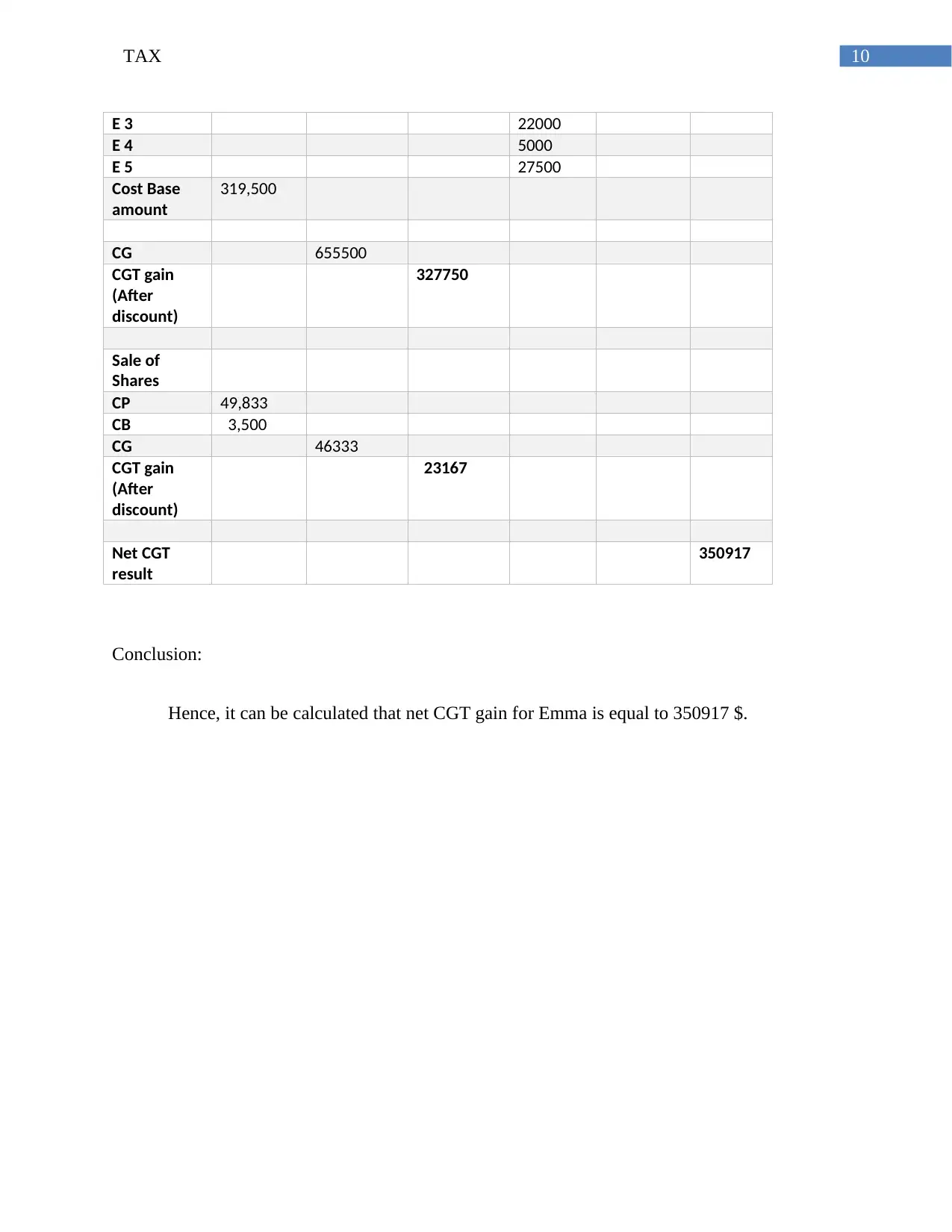

E 3 22000

E 4 5000

E 5 27500

Cost Base

amount

319,500

CG 655500

CGT gain

(After

discount)

327750

Sale of

Shares

CP 49,833

CB 3,500

CG 46333

CGT gain

(After

discount)

23167

Net CGT

result

350917

Conclusion:

Hence, it can be calculated that net CGT gain for Emma is equal to 350917 $.

E 3 22000

E 4 5000

E 5 27500

Cost Base

amount

319,500

CG 655500

CGT gain

(After

discount)

327750

Sale of

Shares

CP 49,833

CB 3,500

CG 46333

CGT gain

(After

discount)

23167

Net CGT

result

350917

Conclusion:

Hence, it can be calculated that net CGT gain for Emma is equal to 350917 $.

11TAX

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Carling, R.G., 2015. Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian small

businesses. J. Austl. Tax'n, 19, p.21.

The Goods and Services Tax 1999 (Cth)

The Income Tax Assessment Act 1997 (Cth)

Tran-Nam, B., 2016. Tax reform and tax simplification: Conceptual and measurement issues and

Australian experiences. In The Complexity of Tax Simplification (pp. 11-44). Palgrave

Macmillan, London.

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Carling, R.G., 2015. Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian small

businesses. J. Austl. Tax'n, 19, p.21.

The Goods and Services Tax 1999 (Cth)

The Income Tax Assessment Act 1997 (Cth)

Tran-Nam, B., 2016. Tax reform and tax simplification: Conceptual and measurement issues and

Australian experiences. In The Complexity of Tax Simplification (pp. 11-44). Palgrave

Macmillan, London.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.