Tax Theory and Calculation - PDF

7 Pages1712 Words82 Views

Added on 2020-04-01

Tax Theory and Calculation - PDF

Added on 2020-04-01

ShareRelated Documents

TAX THEORY AND CALCULATIONS .ASSIGNMENT ON TAX LAW AND PRACTICES Students' NameCourse Title Instructor’s NameInstitutional AffiliationCity and State Date of Submission Question 1;

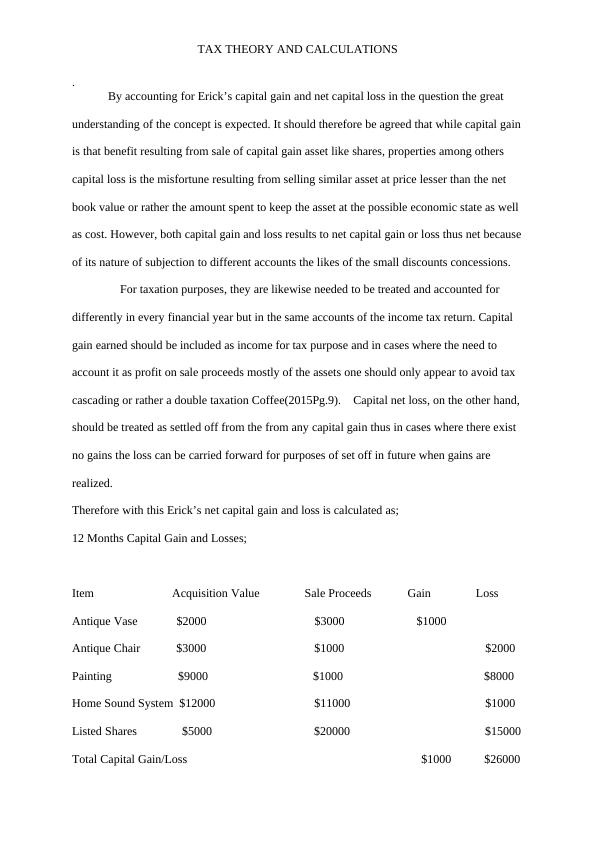

TAX THEORY AND CALCULATIONS .By accounting for Erick’s capital gain and net capital loss in the question the great understanding of the concept is expected. It should therefore be agreed that while capital gainis that benefit resulting from sale of capital gain asset like shares, properties among others capital loss is the misfortune resulting from selling similar asset at price lesser than the net book value or rather the amount spent to keep the asset at the possible economic state as well as cost. However, both capital gain and loss results to net capital gain or loss thus net becauseof its nature of subjection to different accounts the likes of the small discounts concessions. For taxation purposes, they are likewise needed to be treated and accounted for differently in every financial year but in the same accounts of the income tax return. Capital gain earned should be included as income for tax purpose and in cases where the need to account it as profit on sale proceeds mostly of the assets one should only appear to avoid tax cascading or rather a double taxation Coffee(2015Pg.9). Capital net loss, on the other hand, should be treated as settled off from the from any capital gain thus in cases where there exist no gains the loss can be carried forward for purposes of set off in future when gains are realized.Therefore with this Erick’s net capital gain and loss is calculated as;12 Months Capital Gain and Losses;Item Acquisition Value Sale Proceeds Gain LossAntique Vase $2000 $3000 $1000Antique Chair $3000 $1000 $2000 Painting $9000 $1000 $8000Home Sound System $12000 $11000 $1000Listed Shares $5000 $20000 $15000Total Capital Gain/Loss $1000 $26000

TAX THEORY AND CALCULATIONS .From the formulae;Net Capital Gain=Total Capital Gain-Total Capital Loss-Capital Gain Discounts on Small ConcessionsNet Capital Loss=Total Capital Loss-Total Capital GainNet Capital Gain=$1000-($26000)-0= $27000Net Capital Loss=$26000-$1000=$25000Therefore Erick’s Net Capital Gain and Loss respectively are $27000 and $25000Question 2;Although Brian uses 40% of the loan for income generating project and not the whole loan accorded to him we are not clearly outlined by the employer to what extent is the interestonly applicable hence assumption made on the need to work out the taxable value regardless of the usage of the loan by Brian. Since the year of the FBT is FY 2016/17, of course, the need to use benchmarked statutory interest rates of 5.65% as stipulated by the lawDelany(2012, Pg.14) therefore taxable value of FBT for Brian is approached as follows;Free from deductible rule taxable value=$1m*5.65%-1m*1% =$0.0565m-$0.01=$0.0465mInterest-Free Loan or no fringe=$1m*5.65%=$0.0565mIncase of deductible employee would have claimed=$0.0565m*40%=$0.0226mIf FBT applies its expected an allowable of 1m*1%*40%=$0.004mTherefore reduced FBT=$0.0226m-$0.004m=$0.0186MFinally the Brian FBT taxable value=$0.0465m-$0.0186M Brian Taxable Value =$0.0279mIf the interest is to be paid at the end of the loan period, of course, the answer would not be the same because of the factors like time value of money as well as because of the extension

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Practice, Theory and Law - Assignmentlg...

|10

|1898

|113

Taxation, Theory and Practice Assignmentlg...

|10

|1242

|38

Assignment Income Tax Assessment Act 1997lg...

|8

|1604

|40

HI6028 - Taxation Theory, Practice & Lawlg...

|10

|2254

|159

Application of Taxation Theory, Practice & Lawlg...

|7

|1107

|209

Assignment on Taxation Theory, Practice and Lawlg...

|8

|1602

|30