ITAA 1997 & Foreign Residents: Income Tax Treatment in Australia

VerifiedAdded on 2023/06/04

|6

|1240

|494

Report

AI Summary

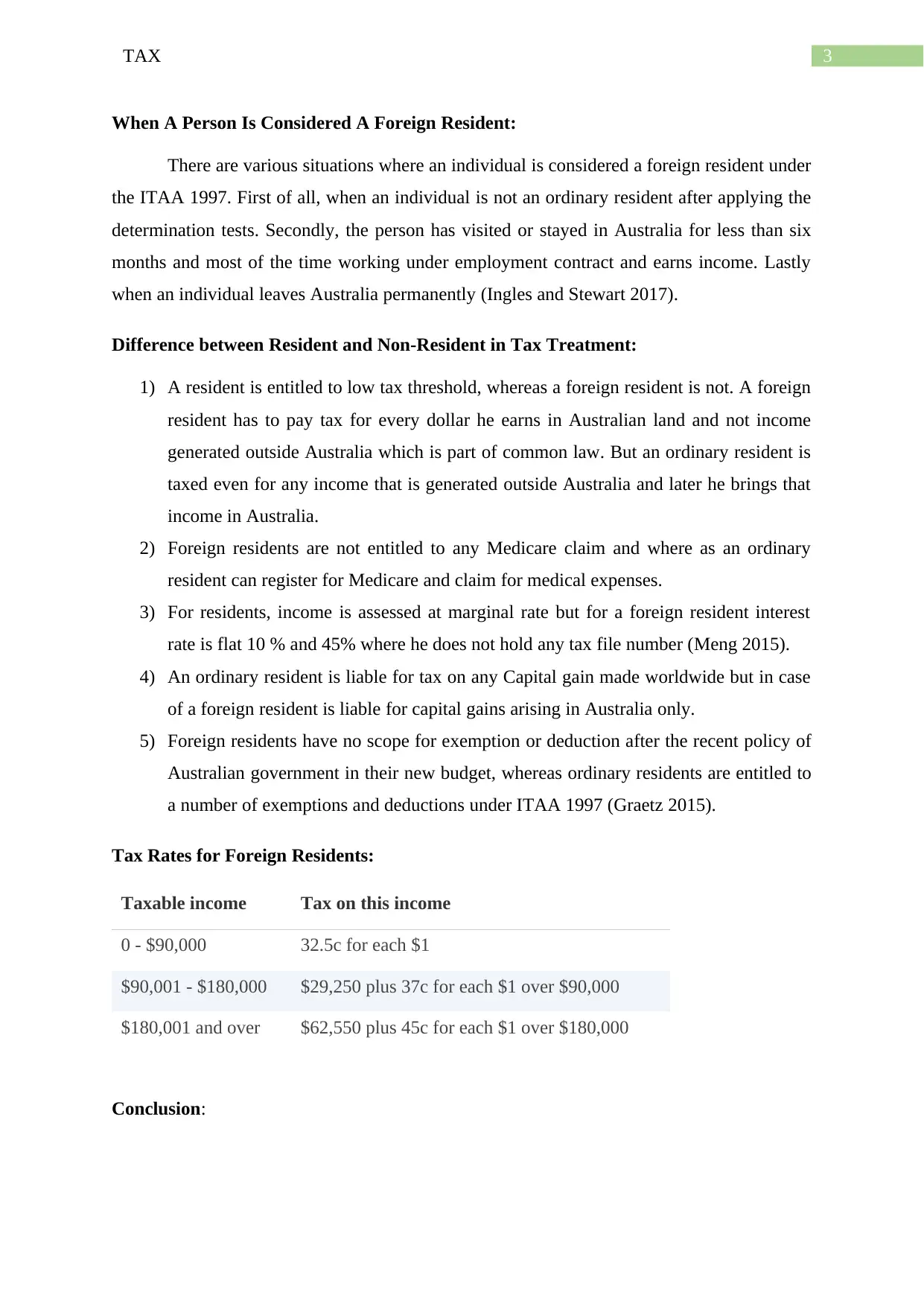

This report provides a detailed analysis of income tax treatment for foreign residents in Australia, contrasting it with that of ordinary residents under the ITAA 1997. It highlights the four rules determining taxability based on citizenship: the Ordinary Concept Rule, the 183 days rule, the Domicile Rule, and the Commonwealth Superannuation Fund rule. Unlike Australian residents who are taxed on worldwide income, foreign residents are taxed only on income generated within Australia, including employment income, rental income, pensions, annuities, and capital gains from Australian property sales. The report outlines key differences in tax treatment, such as the lack of a low tax threshold and Medicare eligibility for foreign residents, and discusses the applicable tax rates and limited scope for exemptions following recent policy changes. It concludes that Australian tax laws are generally stricter for foreign residents, emphasizing the importance of understanding residency status and the implications for tax obligations related to Australian-sourced income and investments.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.