University Taxation 1A Final Assessment Exam Solution

VerifiedAdded on 2022/09/25

|17

|1962

|20

Homework Assignment

AI Summary

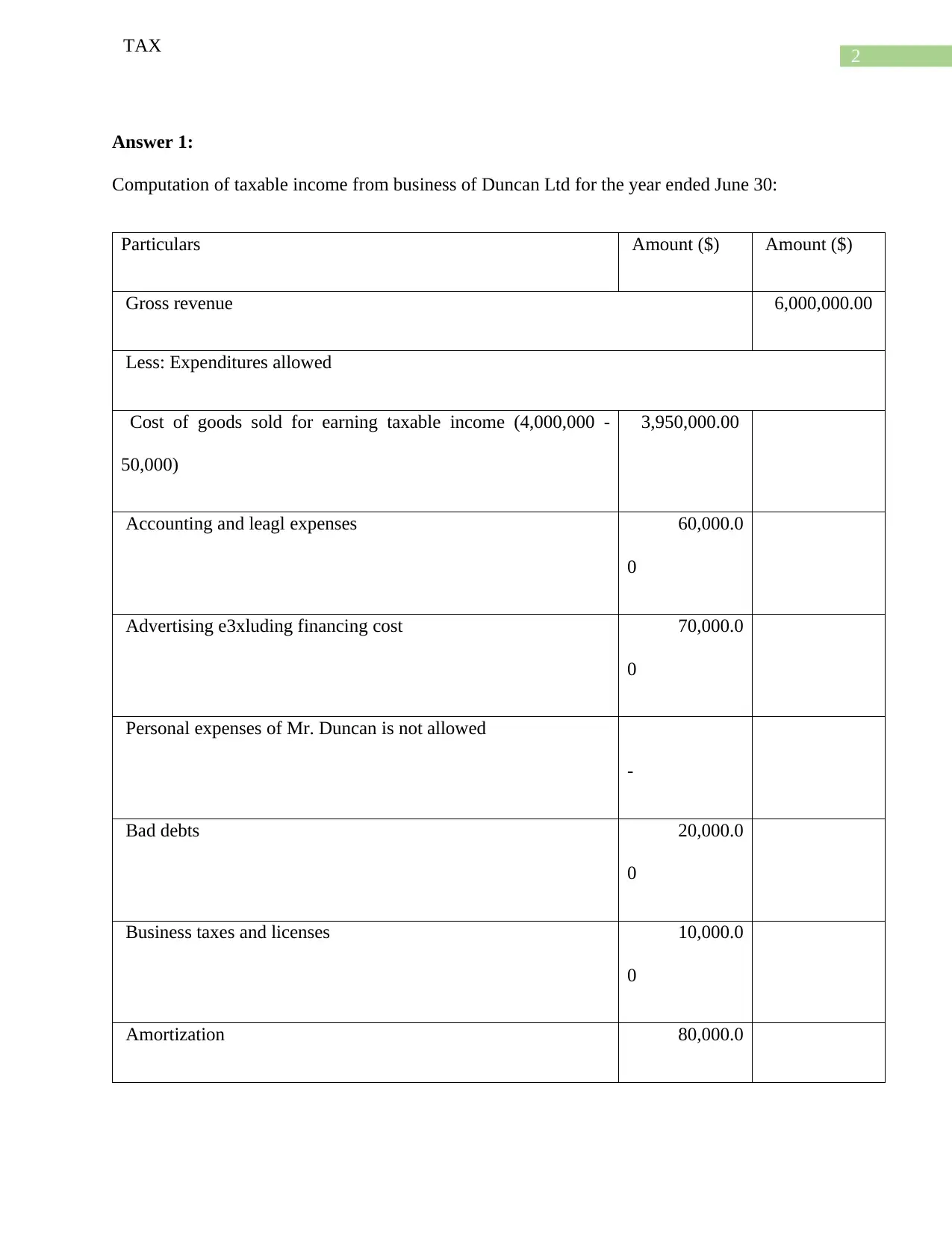

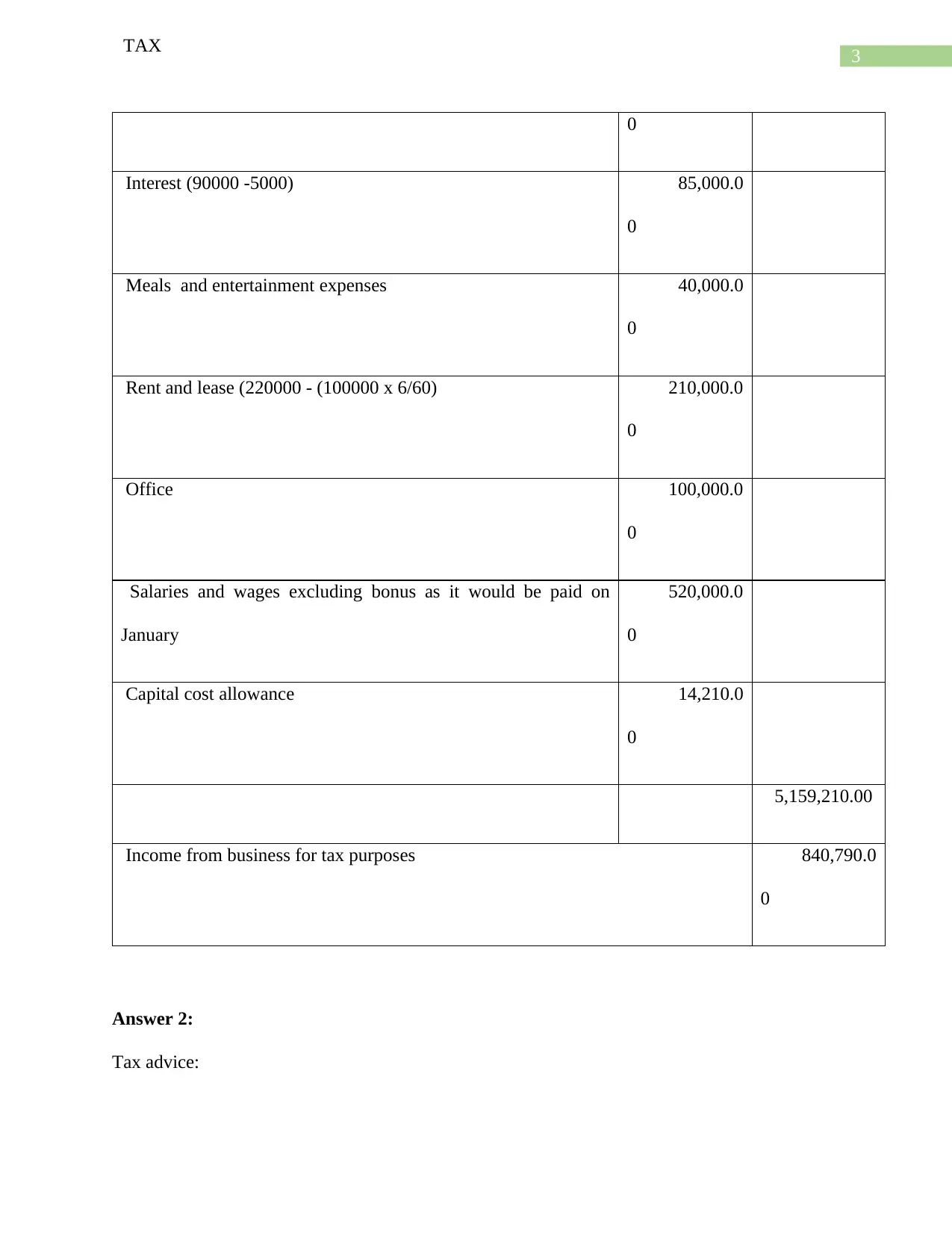

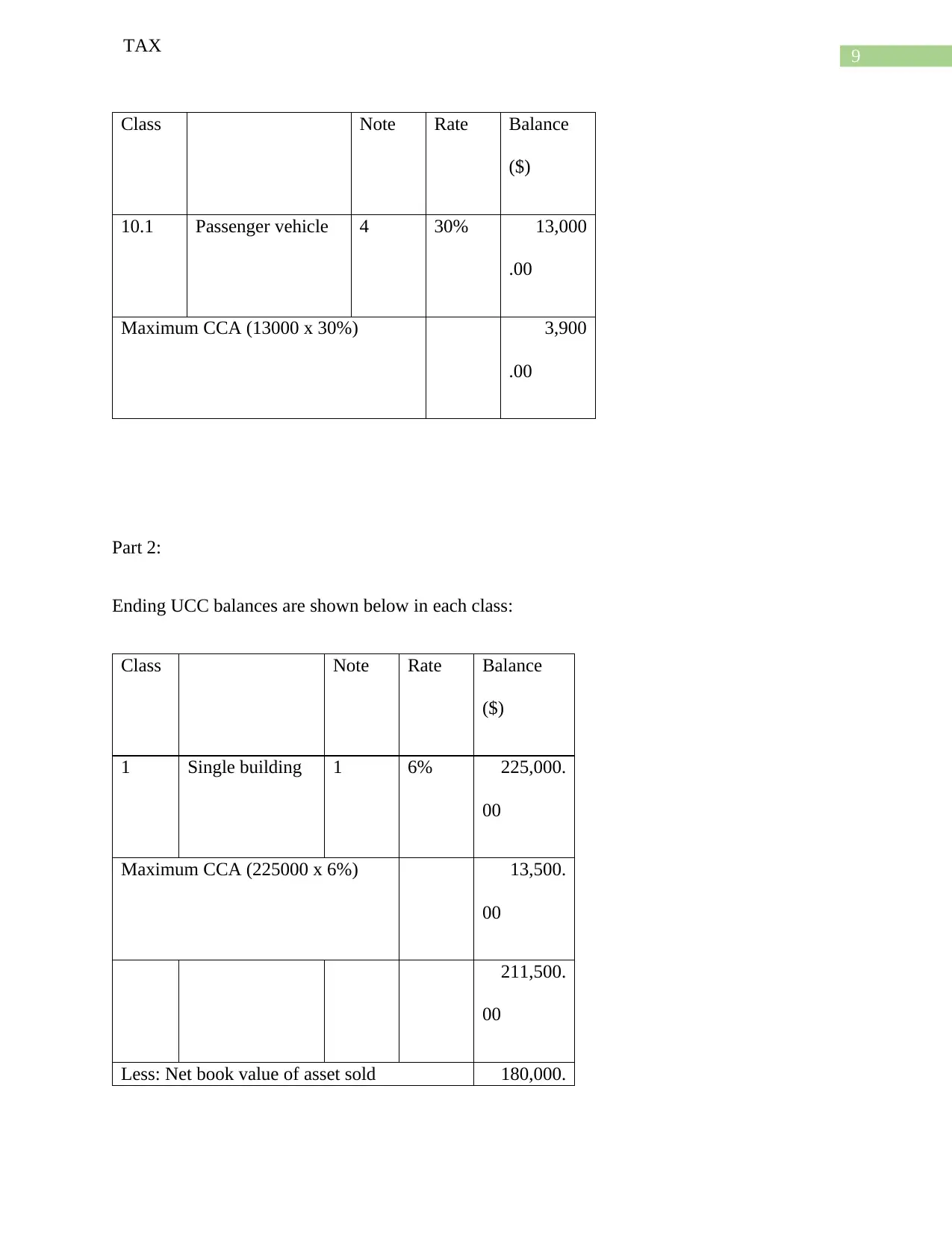

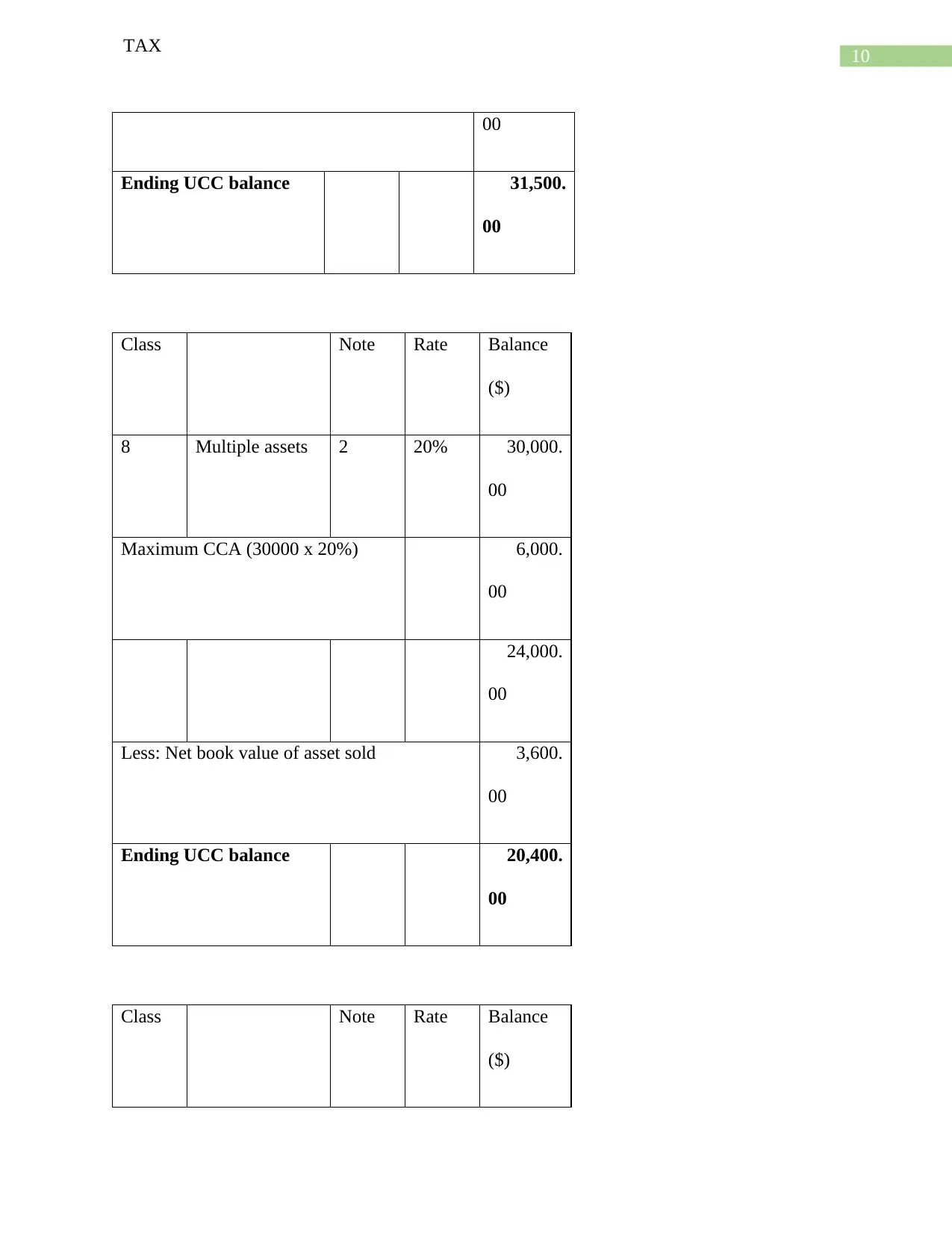

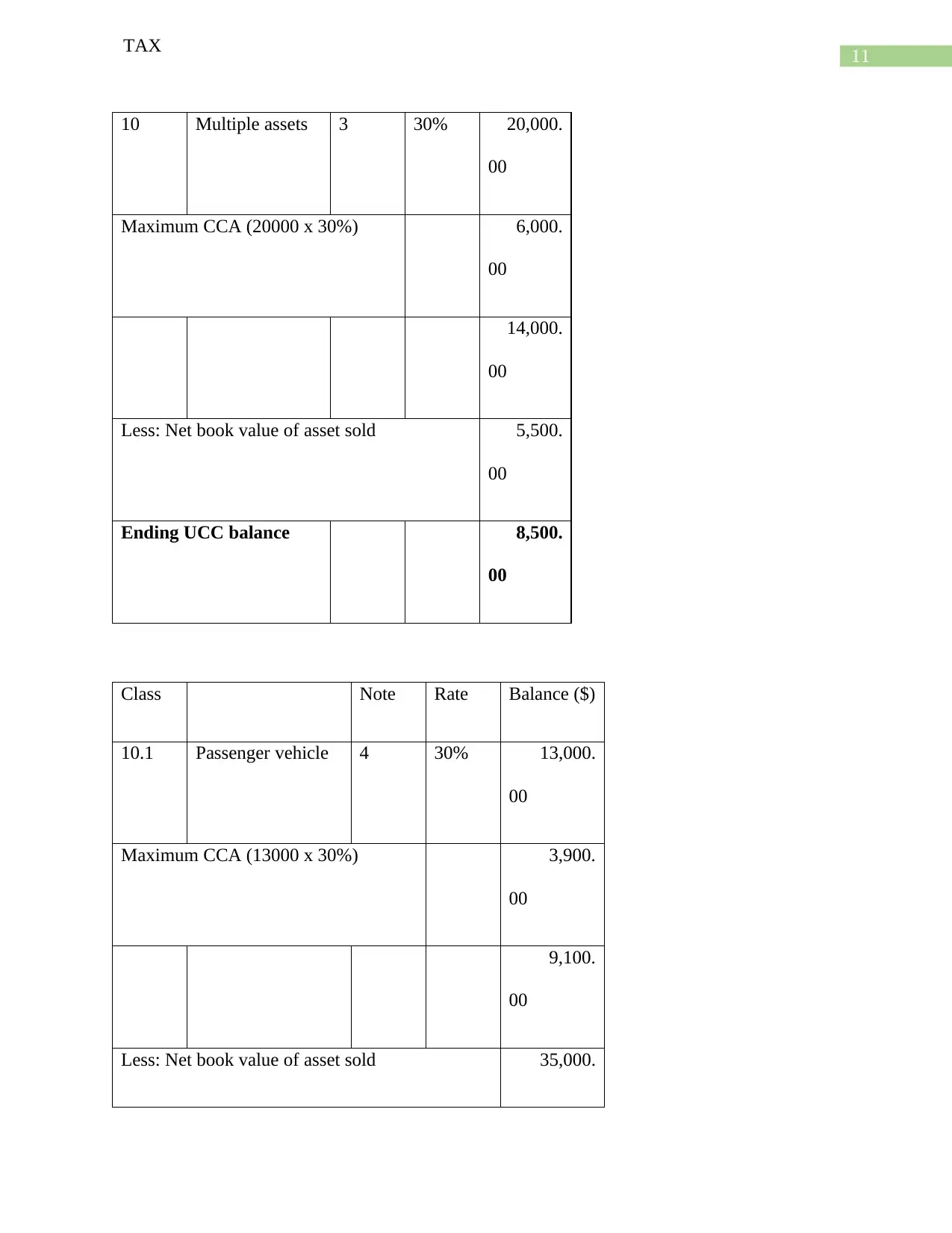

This document presents a comprehensive solution to a Taxation 1A final assessment exam. It includes detailed calculations of taxable income for a business (Duncan Ltd), tax advice on interest-free loans and gifts, and an analysis of tax implications for business owners. The solution further addresses the tax implications of the disposition of assets (van), including capital cost allowance (CCA) calculations. The document also covers maximum CCA claims, ending UCC balances, gain/loss on asset sales, and the taxability of various employee benefits such as parking, gifts, and company-paid dues. Finally, it addresses GST registration requirements and the calculation of income from property, including the sale of property and rental income.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.