Taxation Group Assignment: Analysis of Thomas Hawks' Tax Liabilities

VerifiedAdded on 2022/10/11

|10

|3097

|41

Report

AI Summary

This report analyzes the taxation case of Thomas Hawks, a consultant providing tax and accounting services. It addresses key issues, including whether Thomas's income constitutes Personal Service Income (PSI) or Personal Service Business (PSB), the application of cash versus accrual accounting methods, and the deductibility of business expenses. The report also examines the tax treatment of compensation received from a car accident, the taxability of income derived from a photography hobby, and the related expenses. The analysis considers relevant Australian tax laws, rulings, and case law to provide advice on Thomas Hawks' tax liabilities and obligations, including a computation of his tax liability for the year ending 30 June 2020. The report concludes with a summary of the key findings and recommendations for Thomas Hawks.

Taxation

Student Name:

Student ID:

Abstract

The report is considered tax topics in relation to issue of personal business service income as well as

income in nature of personal service income. The reports also discussed several issue in relation to

compensation receiived in respect of car accident from insurance company, discussion on taxability of

income arised form hobby and related expenses. spects.

Student Name:

Student ID:

Abstract

The report is considered tax topics in relation to issue of personal business service income as well as

income in nature of personal service income. The reports also discussed several issue in relation to

compensation receiived in respect of car accident from insurance company, discussion on taxability of

income arised form hobby and related expenses. spects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.................................................................................................................................................3

a) Advice to Thomas Hawks:....................................................................................................................3

Issue 1 – PSI or PSB......................................................................................................................3

Issue 2 – Cash or accruals............................................................................................................5

Issue 3 – Business Expenses.........................................................................................................6

Issue 4 – Compensation...............................................................................................................7

Issue 5 – Business vs. Hobby........................................................................................................8

b) Computation of tax liability for the year ending 30 June 2020 of Thomas Hawks:.............................9

References.................................................................................................................................................11

Page 2 of 10

Introduction.................................................................................................................................................3

a) Advice to Thomas Hawks:....................................................................................................................3

Issue 1 – PSI or PSB......................................................................................................................3

Issue 2 – Cash or accruals............................................................................................................5

Issue 3 – Business Expenses.........................................................................................................6

Issue 4 – Compensation...............................................................................................................7

Issue 5 – Business vs. Hobby........................................................................................................8

b) Computation of tax liability for the year ending 30 June 2020 of Thomas Hawks:.............................9

References.................................................................................................................................................11

Page 2 of 10

Introduction

In this report, we had discussed the case law and tax litigation of Thomas hawks by

categorizing their income and expense under the given head of income under income

tax. Thomas Hawks is running a business that is providing services in relation to

consultancy for the tax calculation of business entities as well as individuals. The

worked in relation to office has been done by him and also by hiring the intern. There is

also mentioned his client namely, Jenny Pty Ltd who is one of the major clients. The

revenue of firms consists of a 70% amount received from Jenny Pty Ltd. Other revenue

is earned through different clients. Thomas himself working to extent of 80% of the work

of the firm and remaining is being done by his intern.

The expenditure of Thomas includes the salary and wages paid to intern or accountant,

expenses incurred to maintain office such as cleaning and heating expenses. Purchase

of office supplies, interest paid on loan mortgaged and rents in respect of premises for

office, etc. Thoman also purchased computers, a machine such as printers and furniture

and fixture. These costs are in the nature of fixed costs.

Suddenly, Thomas has fallen due to a car accident due to which the working efficiency

of Thomas has been gone down. Thomas received compensation from the insurance

company as he is already covered under private health insurance in respect of such an

accident.

The car accident is the reason due to which he decided to move to another place in

Frankston and also reduce the overload work to an extent of 50%. Thomas started to

enjoy his hobby of photography from his new place. Due to more interest and his talent,

he is able to make rich by so many followers on Instagram. He also received an offer

from the manufacturing company during the current year. He earned income of $2500

from enriching such work.

a) Advice to Thomas Hawks:

Issue 1 – PSI or PSB

o The task one involved issue in relation to determine whether the income of

Thomas is fallen under the income of business or income from personal

service. It is difficult to decide the nature of income without applying the

rules and regulations of income tax.

o In accordance with provision of Section 84.5 of ITAA (1997) which states

the provision in respect of income from personal service. As per this

section, any income which is earned by using the set of skills or effort of

his own can be deemed as income from personal service income. The

Page 3 of 10

In this report, we had discussed the case law and tax litigation of Thomas hawks by

categorizing their income and expense under the given head of income under income

tax. Thomas Hawks is running a business that is providing services in relation to

consultancy for the tax calculation of business entities as well as individuals. The

worked in relation to office has been done by him and also by hiring the intern. There is

also mentioned his client namely, Jenny Pty Ltd who is one of the major clients. The

revenue of firms consists of a 70% amount received from Jenny Pty Ltd. Other revenue

is earned through different clients. Thomas himself working to extent of 80% of the work

of the firm and remaining is being done by his intern.

The expenditure of Thomas includes the salary and wages paid to intern or accountant,

expenses incurred to maintain office such as cleaning and heating expenses. Purchase

of office supplies, interest paid on loan mortgaged and rents in respect of premises for

office, etc. Thoman also purchased computers, a machine such as printers and furniture

and fixture. These costs are in the nature of fixed costs.

Suddenly, Thomas has fallen due to a car accident due to which the working efficiency

of Thomas has been gone down. Thomas received compensation from the insurance

company as he is already covered under private health insurance in respect of such an

accident.

The car accident is the reason due to which he decided to move to another place in

Frankston and also reduce the overload work to an extent of 50%. Thomas started to

enjoy his hobby of photography from his new place. Due to more interest and his talent,

he is able to make rich by so many followers on Instagram. He also received an offer

from the manufacturing company during the current year. He earned income of $2500

from enriching such work.

a) Advice to Thomas Hawks:

Issue 1 – PSI or PSB

o The task one involved issue in relation to determine whether the income of

Thomas is fallen under the income of business or income from personal

service. It is difficult to decide the nature of income without applying the

rules and regulations of income tax.

o In accordance with provision of Section 84.5 of ITAA (1997) which states

the provision in respect of income from personal service. As per this

section, any income which is earned by using the set of skills or effort of

his own can be deemed as income from personal service income. The

Page 3 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

personal service is directly linked with individuals only. Nobody corporate

can provide personal service income. Such income can be generating by

provision of service such as completing certain tasks or performing arts,

etc. It is not necessary that the condition should be received in

accordance with the agreement. Hence, consideration can be earned

irrespective of a contract of services. (ITAA 1997, s84-5(3))

o The income from the personal service business is regulated in section

87.15 of ITAA (1997). Where any person received income from the single

client of 80% or more of total income and also satisfies one of three PSB

tests by taxpayers, then such income shall be self-treated as income from

personal business service (Para 39, p. 11, TR 2001/8).

There are three test in respect of personal service business namely:

o Test which is in relation to employment

o Test which is in relation to clients which are not related

o Test in relation to premises of business (ITAA 1997, 87-15(2)).

Section 87.18 of ITAA (1997) states that results if a test for the purpose of

determination of personal service business. In accordance with this section, there

is a minimum of 75% income of personal service income, such income is

generated from users of equipment and the responsible for correction of defaults

done, then it is said to comply with the above test (ITAA 1997, s87-18(1)).

Section 87.20 of ITAA (1997) provides the description of a test in relation to

unrelated clients. The condition in relation to an unrelated client can be satisfied

if there is no relationship with the several clients from which income is earned.

The employment test is referred through section s87-25 of ITAA (1997). It states

that condition can be said to be satisfied only if he is engaged in service of more

than one entity and such entity is engaged in performing a minimum of overall

20% of the task. (ITAA 1997, s87-25(1)).

There is no restriction on hiring apprentice, Such work can be performed by

engaging interns too. Even the Intern has completed this work, it shall be

deemed that they fulfill the condition. (ITAA, 1997, s87-25(3)).

Where the individual has used the business premised to perform the personal

service, it can be said that they complied with the test of premises. It is further

provided that such a test can be satisfied only if business premised is used for

the whole of the tax year. (ITAA 1997, s87-30(1)).

Page 4 of 10

can provide personal service income. Such income can be generating by

provision of service such as completing certain tasks or performing arts,

etc. It is not necessary that the condition should be received in

accordance with the agreement. Hence, consideration can be earned

irrespective of a contract of services. (ITAA 1997, s84-5(3))

o The income from the personal service business is regulated in section

87.15 of ITAA (1997). Where any person received income from the single

client of 80% or more of total income and also satisfies one of three PSB

tests by taxpayers, then such income shall be self-treated as income from

personal business service (Para 39, p. 11, TR 2001/8).

There are three test in respect of personal service business namely:

o Test which is in relation to employment

o Test which is in relation to clients which are not related

o Test in relation to premises of business (ITAA 1997, 87-15(2)).

Section 87.18 of ITAA (1997) states that results if a test for the purpose of

determination of personal service business. In accordance with this section, there

is a minimum of 75% income of personal service income, such income is

generated from users of equipment and the responsible for correction of defaults

done, then it is said to comply with the above test (ITAA 1997, s87-18(1)).

Section 87.20 of ITAA (1997) provides the description of a test in relation to

unrelated clients. The condition in relation to an unrelated client can be satisfied

if there is no relationship with the several clients from which income is earned.

The employment test is referred through section s87-25 of ITAA (1997). It states

that condition can be said to be satisfied only if he is engaged in service of more

than one entity and such entity is engaged in performing a minimum of overall

20% of the task. (ITAA 1997, s87-25(1)).

There is no restriction on hiring apprentice, Such work can be performed by

engaging interns too. Even the Intern has completed this work, it shall be

deemed that they fulfill the condition. (ITAA, 1997, s87-25(3)).

Where the individual has used the business premised to perform the personal

service, it can be said that they complied with the test of premises. It is further

provided that such a test can be satisfied only if business premised is used for

the whole of the tax year. (ITAA 1997, s87-30(1)).

Page 4 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The following intrepretation can be obtained through application of above lasws

and provisions:

In this instant case, thomas hawks being indivual is enagaged in business

of provision of consultancy in relation to taxation and accounting services.

It states that condition mentioned under section 84.5 of ITAA (1997) has

been satisfied. As such income is earned by him using his own set of

skills. Accordingly, it can be said that income earned is in nature of

personal business income.

There may alienation of personal business incoem if individual fulfills the

conditions given under s87.15 of ITAA (1997).

Hawks is in employment with jenny private limited from where he earned

income of more than 80% from such single client. It indicates hawks

satisfied result test.

He earned income from various clients which are unrelated to

him.However he fails to meet considition specified for unrealted clients

test.

However, he engaaged a intern to work in his consultancyfor the whole of

the year which indicates that he fulfills the condition related to employment

test.

However, He fails to meet condition in relation to use of business of

premised. He used the business premises for the whole of the year.

Accordingly, the condition referred under para 27of taxation rulling

(2001/8) provides that there is no applicationof alienation measure

doesnot apply on him and such income earned is in nature of “Personal

Services Business”. Accordingly, he will able to claim cetain deduction and

exemptions.

Issue 2 – Cash or accruals

There is a lot of confusion that will arise where income is earned and the

receipt of such income is in different tax year. Accordingly, it is difficult to

determine the tax period in respect of which such income will arise. There

are two methods which prescribes a system of accounting. Namely Cash

method and accrual method. Under the cash method, income is taxed on

the basis of receipt of such income. It means it will be taxed in the year in

which such income is received by the taxpayer. Another method is the

accrual method where income is taxed in the year in which earned

irrespective of whether cash is received or not. (Para 2, p.1, TR 98/1,

2017).

Page 5 of 10

and provisions:

In this instant case, thomas hawks being indivual is enagaged in business

of provision of consultancy in relation to taxation and accounting services.

It states that condition mentioned under section 84.5 of ITAA (1997) has

been satisfied. As such income is earned by him using his own set of

skills. Accordingly, it can be said that income earned is in nature of

personal business income.

There may alienation of personal business incoem if individual fulfills the

conditions given under s87.15 of ITAA (1997).

Hawks is in employment with jenny private limited from where he earned

income of more than 80% from such single client. It indicates hawks

satisfied result test.

He earned income from various clients which are unrelated to

him.However he fails to meet considition specified for unrealted clients

test.

However, he engaaged a intern to work in his consultancyfor the whole of

the year which indicates that he fulfills the condition related to employment

test.

However, He fails to meet condition in relation to use of business of

premised. He used the business premises for the whole of the year.

Accordingly, the condition referred under para 27of taxation rulling

(2001/8) provides that there is no applicationof alienation measure

doesnot apply on him and such income earned is in nature of “Personal

Services Business”. Accordingly, he will able to claim cetain deduction and

exemptions.

Issue 2 – Cash or accruals

There is a lot of confusion that will arise where income is earned and the

receipt of such income is in different tax year. Accordingly, it is difficult to

determine the tax period in respect of which such income will arise. There

are two methods which prescribes a system of accounting. Namely Cash

method and accrual method. Under the cash method, income is taxed on

the basis of receipt of such income. It means it will be taxed in the year in

which such income is received by the taxpayer. Another method is the

accrual method where income is taxed in the year in which earned

irrespective of whether cash is received or not. (Para 2, p.1, TR 98/1,

2017).

Page 5 of 10

Accordingly, the time of receipt is key to determine the taxability period

under the cash method accounting system. (ITAA 1997, s6-5(4))

The accrual method considers the time of income earned rather than the

time of receipt of income. (Para 9, p.2, TR 98/1, 2017).

The case laws which are related to above include Carden's case,

Henderson's case, Brent's case and Barratt's case (Para 29, p.5, TR 98/1,

2017).

There is an application of the cash method of accounting system if the

taxpayer gained income by applying a set of skills and efforts. (Para 44,

p.8, TR 98/1, 2017)

Accordingly, the provision of personal business service in the case of

Hawkins requires the application of the cash method of accounting for the

purpose of calculation of income tax.

Issue 3 – Business Expenses

Any expenses which are occured in respect of earning or generating

assessable income under business can be claimed as deduction for

calculation of taxable income (ITAA 1997, s8-1(1) (b)).

The ordinary expense as specified under section 8-1 of ITAA (1997).

There are two hands which consist one in relation to income which is

taxable and another the categories of taxpayer. Accordingly, both limbs

can be used by business taxpayers (Snowden & Willson Pty Ltd v FCT

(1958) 99 CLR 431).

Hence, Thomas Hawkins can claim deduction in respect of expenses

incurred for business purposes.

.

Issue 4 – Compensation

The receipt of the amount in the nature of compensation is prescribed in

the taxation ruling 95/35 (2006) where the tax consequences have been

explained. Any income which is earned in the nature of compensation can

be added to the total income of the assessee. Please refer to the case law

for a detailed explanation (Para 1 TR 95/35, 2006).

Page 6 of 10

under the cash method accounting system. (ITAA 1997, s6-5(4))

The accrual method considers the time of income earned rather than the

time of receipt of income. (Para 9, p.2, TR 98/1, 2017).

The case laws which are related to above include Carden's case,

Henderson's case, Brent's case and Barratt's case (Para 29, p.5, TR 98/1,

2017).

There is an application of the cash method of accounting system if the

taxpayer gained income by applying a set of skills and efforts. (Para 44,

p.8, TR 98/1, 2017)

Accordingly, the provision of personal business service in the case of

Hawkins requires the application of the cash method of accounting for the

purpose of calculation of income tax.

Issue 3 – Business Expenses

Any expenses which are occured in respect of earning or generating

assessable income under business can be claimed as deduction for

calculation of taxable income (ITAA 1997, s8-1(1) (b)).

The ordinary expense as specified under section 8-1 of ITAA (1997).

There are two hands which consist one in relation to income which is

taxable and another the categories of taxpayer. Accordingly, both limbs

can be used by business taxpayers (Snowden & Willson Pty Ltd v FCT

(1958) 99 CLR 431).

Hence, Thomas Hawkins can claim deduction in respect of expenses

incurred for business purposes.

.

Issue 4 – Compensation

The receipt of the amount in the nature of compensation is prescribed in

the taxation ruling 95/35 (2006) where the tax consequences have been

explained. Any income which is earned in the nature of compensation can

be added to the total income of the assessee. Please refer to the case law

for a detailed explanation (Para 1 TR 95/35, 2006).

Page 6 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Para 3 of TR 95/35 (2006) further stated compensation receipts which

states that any amount which is nature of compensation such as cause of

action or any pending proceeding of action are considered. (Para 3 TR

95/35, 2006):

Para 3 of TR 95/35 (2006) further stated compensation receipts which states that

any amount which is nature of compensation such as cause of actio or any

pending proceeding of action are considered. (Para 3 TR 95/35, 2006):

The types of asset underlined;

All comepensation irrespective of order of court

Any lumpsum compensation is received by the taxpayer which is not be

dissected.

Where the compensation is received from the insurance company in respect

of damage or personal injury to the individual and where such individual is

covered under health policy such as private health insurance policy is in

nature of income of capital gain. Such income is wholly taxed under section

160ZB (1). The exemption is provided irrespective of whether such personal

injury is proved by the taxpayer. There is no need to prove by the taxpayer of

such personal injury. (Example 17, Para 304, TR 95/35 2006).

In the instant case, there is personal injury to Thomas due to a car accident.

Accordingly, he had to reduce his working hours which indicates a decrease

in efficiency of Thomas. Hence Thomas can claim exemption of

compensation received from health insurance in respect of such income.

Issue 5 – Business vs. Hobby

To determine whether hobby can be treated as business, we should consider the

follwoing points:

a) Whether the individual is contuining in hobby to earn in commercial

manner?

b) Whether intention of hobby to earn profits?

c) Whether such activities are in repetitive manner?

d) Whether hobby is simmilar in nature of conducting business?

Page 7 of 10

states that any amount which is nature of compensation such as cause of

action or any pending proceeding of action are considered. (Para 3 TR

95/35, 2006):

Para 3 of TR 95/35 (2006) further stated compensation receipts which states that

any amount which is nature of compensation such as cause of actio or any

pending proceeding of action are considered. (Para 3 TR 95/35, 2006):

The types of asset underlined;

All comepensation irrespective of order of court

Any lumpsum compensation is received by the taxpayer which is not be

dissected.

Where the compensation is received from the insurance company in respect

of damage or personal injury to the individual and where such individual is

covered under health policy such as private health insurance policy is in

nature of income of capital gain. Such income is wholly taxed under section

160ZB (1). The exemption is provided irrespective of whether such personal

injury is proved by the taxpayer. There is no need to prove by the taxpayer of

such personal injury. (Example 17, Para 304, TR 95/35 2006).

In the instant case, there is personal injury to Thomas due to a car accident.

Accordingly, he had to reduce his working hours which indicates a decrease

in efficiency of Thomas. Hence Thomas can claim exemption of

compensation received from health insurance in respect of such income.

Issue 5 – Business vs. Hobby

To determine whether hobby can be treated as business, we should consider the

follwoing points:

a) Whether the individual is contuining in hobby to earn in commercial

manner?

b) Whether intention of hobby to earn profits?

c) Whether such activities are in repetitive manner?

d) Whether hobby is simmilar in nature of conducting business?

Page 7 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Generally, the provision of income tax provides an exemption in the nature of

income earned through hobby. However, income from such can be taxed if it is in

the nature of conducting business. The Australian tax law has defined the hobby

as an activity that is done in free time for the purpose of enjoyment and personal

satisfaction. It is not necessary to maintain or keep books of account in relation to

income which is earned through the hobby. No expense can be claimed as a

deduction where such expenses are incurred for the purpose of a hobby. It is not

necessary to declare income which is earned from hobby while filing income tax

return (Department of Industry, Innovation, and Science, Australia 2018).

In the instant case, Thomas has so many followers on social media. As they

started posting a photo which is taken while engaged in his passion for work. The

intention of Thomas is not to make a profit even he clicked several photographs.

Here, it is cleared that he is not involved in the business of photography.

Therefore, It can be said that he is pursuing is a hobby for personal satisfaction

and enjoyment. Such activity is not in the nature of the income of the business.

Such income earned of $2500 is not required to disclosed and also he cannot

claim exemption in respect of such income.

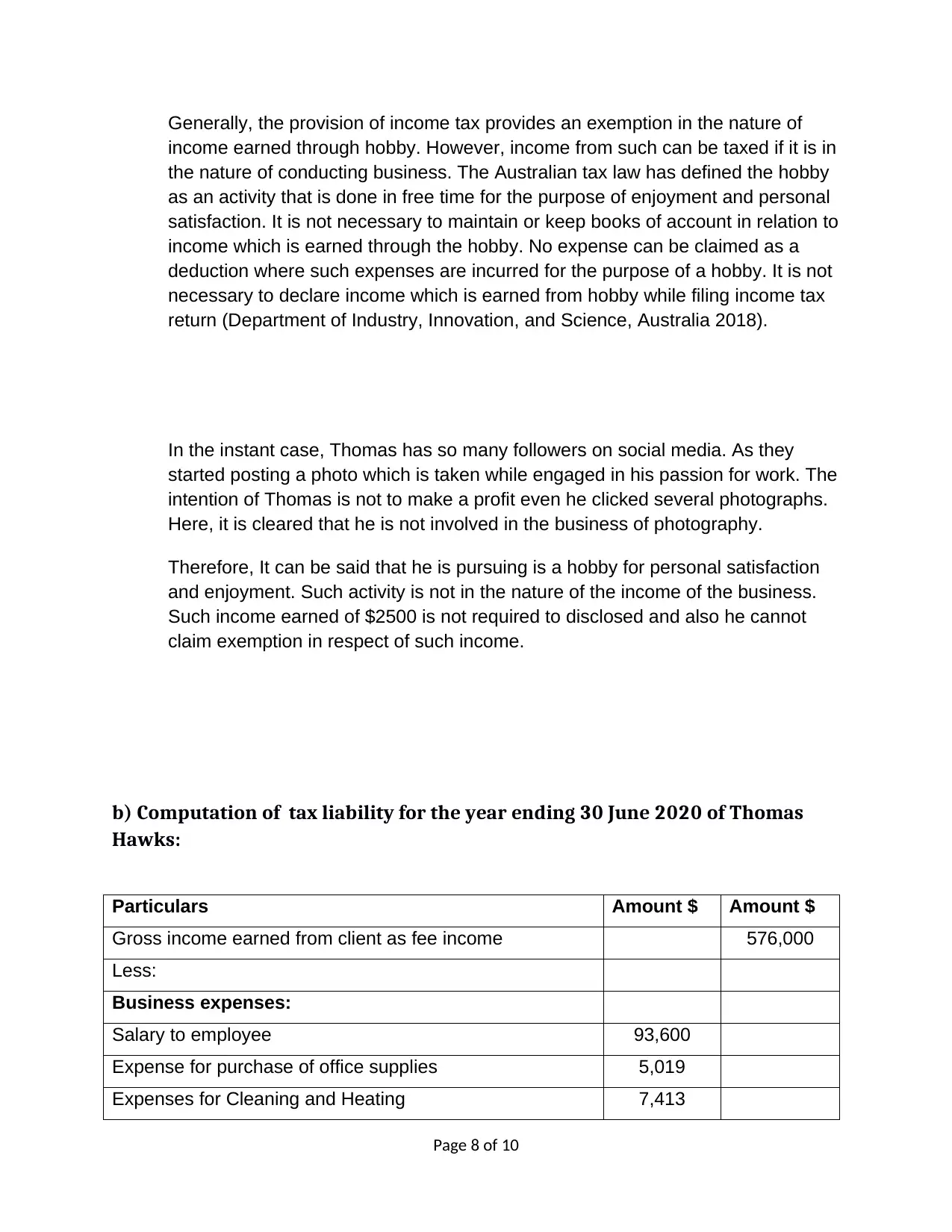

b) Computation of tax liability for the year ending 30 June 2020 of Thomas

Hawks:

Particulars Amount $ Amount $

Gross income earned from client as fee income 576,000

Less:

Business expenses:

Salary to employee 93,600

Expense for purchase of office supplies 5,019

Expenses for Cleaning and Heating 7,413

Page 8 of 10

income earned through hobby. However, income from such can be taxed if it is in

the nature of conducting business. The Australian tax law has defined the hobby

as an activity that is done in free time for the purpose of enjoyment and personal

satisfaction. It is not necessary to maintain or keep books of account in relation to

income which is earned through the hobby. No expense can be claimed as a

deduction where such expenses are incurred for the purpose of a hobby. It is not

necessary to declare income which is earned from hobby while filing income tax

return (Department of Industry, Innovation, and Science, Australia 2018).

In the instant case, Thomas has so many followers on social media. As they

started posting a photo which is taken while engaged in his passion for work. The

intention of Thomas is not to make a profit even he clicked several photographs.

Here, it is cleared that he is not involved in the business of photography.

Therefore, It can be said that he is pursuing is a hobby for personal satisfaction

and enjoyment. Such activity is not in the nature of the income of the business.

Such income earned of $2500 is not required to disclosed and also he cannot

claim exemption in respect of such income.

b) Computation of tax liability for the year ending 30 June 2020 of Thomas

Hawks:

Particulars Amount $ Amount $

Gross income earned from client as fee income 576,000

Less:

Business expenses:

Salary to employee 93,600

Expense for purchase of office supplies 5,019

Expenses for Cleaning and Heating 7,413

Page 8 of 10

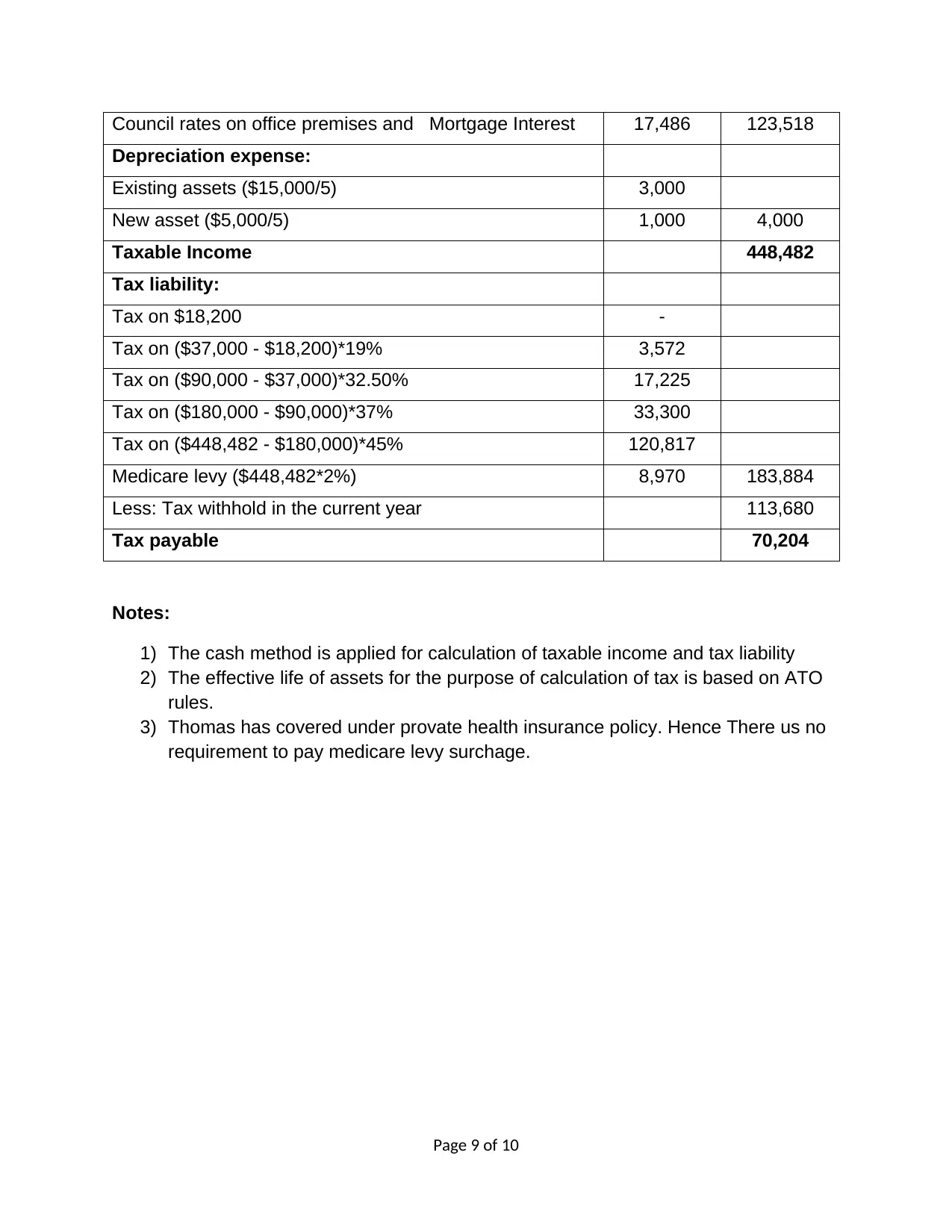

Council rates on office premises and Mortgage Interest 17,486 123,518

Depreciation expense:

Existing assets ($15,000/5) 3,000

New asset ($5,000/5) 1,000 4,000

Taxable Income 448,482

Tax liability:

Tax on $18,200 -

Tax on ($37,000 - $18,200)*19% 3,572

Tax on ($90,000 - $37,000)*32.50% 17,225

Tax on ($180,000 - $90,000)*37% 33,300

Tax on ($448,482 - $180,000)*45% 120,817

Medicare levy ($448,482*2%) 8,970 183,884

Less: Tax withhold in the current year 113,680

Tax payable 70,204

Notes:

1) The cash method is applied for calculation of taxable income and tax liability

2) The effective life of assets for the purpose of calculation of tax is based on ATO

rules.

3) Thomas has covered under provate health insurance policy. Hence There us no

requirement to pay medicare levy surchage.

Page 9 of 10

Depreciation expense:

Existing assets ($15,000/5) 3,000

New asset ($5,000/5) 1,000 4,000

Taxable Income 448,482

Tax liability:

Tax on $18,200 -

Tax on ($37,000 - $18,200)*19% 3,572

Tax on ($90,000 - $37,000)*32.50% 17,225

Tax on ($180,000 - $90,000)*37% 33,300

Tax on ($448,482 - $180,000)*45% 120,817

Medicare levy ($448,482*2%) 8,970 183,884

Less: Tax withhold in the current year 113,680

Tax payable 70,204

Notes:

1) The cash method is applied for calculation of taxable income and tax liability

2) The effective life of assets for the purpose of calculation of tax is based on ATO

rules.

3) Thomas has covered under provate health insurance policy. Hence There us no

requirement to pay medicare levy surchage.

Page 9 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Department of Industry, Innovation, and Science, Australia (2018). “A business or a

hobby?” Retrieved on 11th September from:

ICAI, Australia (2012). “Allowable Deductions – Essentials”. FCT v Snowden & Willson

Pty Ltd (1958) 99 CLR 431. Retrieved on 11th September from:

Income Tax Assessment Act (1997), s8-1(1) (b). “General deductions”. Retrieved on

11th September from:http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html#targetText=INCOME%20TAX%20ASSESSMENT%20ACT%201997%20%2D

%20SECT%208.1&targetText=(b)%20it%20is%20necessarily%20incurred,offset

%20against%20other%20assessable%20income.

Income Tax Assessment Act (1997), s84-5(3). “Meaning of personal services

income”.Retrieved on 11th September 2019 from:

Income Tax Assessment Act (1997), s87-18(1). “The results test for a personal services

business”. Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-2. “The unrelated clients test for a personal

services business”. Retrieved on 11th September from:

Income Tax Assessment Act (1997), 87-15(2). “What is a personal services business?”

Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-25. “The employment test for a personal

services business ". Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-30. “The business premises test for a personal

services business”. Retrieved on 11th September from:

Taxation Ruling 98/1, (2017). “Income tax: determination of income; receipts versus

earnings”. Australian Government Office. Retrieved on 11th September from:

Taxation Ruling 2001/8) Para 39, p.11. “The Three Personal Services Business Tests”.

Australian Government Office. Retrieved on 11th September from:

Taxation Ruling 95/35 (2016). “Income tax: capital gains: treatment of compensation

receipts”. Australian Government Office. Retrieved on 11th September from:

https://www.ato.gov.au/law/view/document?docid=TXR/TR9535/NAT/ATO/00001#P1

Page 10 of 10

Department of Industry, Innovation, and Science, Australia (2018). “A business or a

hobby?” Retrieved on 11th September from:

ICAI, Australia (2012). “Allowable Deductions – Essentials”. FCT v Snowden & Willson

Pty Ltd (1958) 99 CLR 431. Retrieved on 11th September from:

Income Tax Assessment Act (1997), s8-1(1) (b). “General deductions”. Retrieved on

11th September from:http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html#targetText=INCOME%20TAX%20ASSESSMENT%20ACT%201997%20%2D

%20SECT%208.1&targetText=(b)%20it%20is%20necessarily%20incurred,offset

%20against%20other%20assessable%20income.

Income Tax Assessment Act (1997), s84-5(3). “Meaning of personal services

income”.Retrieved on 11th September 2019 from:

Income Tax Assessment Act (1997), s87-18(1). “The results test for a personal services

business”. Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-2. “The unrelated clients test for a personal

services business”. Retrieved on 11th September from:

Income Tax Assessment Act (1997), 87-15(2). “What is a personal services business?”

Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-25. “The employment test for a personal

services business ". Retrieved on 11th September from:

Income Tax Assessment Act (1997), s87-30. “The business premises test for a personal

services business”. Retrieved on 11th September from:

Taxation Ruling 98/1, (2017). “Income tax: determination of income; receipts versus

earnings”. Australian Government Office. Retrieved on 11th September from:

Taxation Ruling 2001/8) Para 39, p.11. “The Three Personal Services Business Tests”.

Australian Government Office. Retrieved on 11th September from:

Taxation Ruling 95/35 (2016). “Income tax: capital gains: treatment of compensation

receipts”. Australian Government Office. Retrieved on 11th September from:

https://www.ato.gov.au/law/view/document?docid=TXR/TR9535/NAT/ATO/00001#P1

Page 10 of 10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.