TMA 02 | Taxation and provisions.

VerifiedAdded on 2022/09/09

|21

|4391

|21

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: - Taxation and provisions 0 | P a g e

TMA 02

TMA 02

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation and provisions 1 | P a g e

Contents

Part A..........................................................................................................................................................2

Answer to question no. – 1......................................................................................................................2

Answer to question no. – 2......................................................................................................................6

Answer to question no. – 3....................................................................................................................10

Part B.........................................................................................................................................................14

Introduction...........................................................................................................................................14

Unsecured Debt.....................................................................................................................................15

Different types of unsecured borrowing:...............................................................................................15

Factors which may have contributed to the level of unsecured household debt:....................................16

Part C.........................................................................................................................................................17

Team Work:...........................................................................................................................................17

References.................................................................................................................................................19

1 | P a g e

Contents

Part A..........................................................................................................................................................2

Answer to question no. – 1......................................................................................................................2

Answer to question no. – 2......................................................................................................................6

Answer to question no. – 3....................................................................................................................10

Part B.........................................................................................................................................................14

Introduction...........................................................................................................................................14

Unsecured Debt.....................................................................................................................................15

Different types of unsecured borrowing:...............................................................................................15

Factors which may have contributed to the level of unsecured household debt:....................................16

Part C.........................................................................................................................................................17

Team Work:...........................................................................................................................................17

References.................................................................................................................................................19

1 | P a g e

Taxation and provisions 2 | P a g e

Part A

Answer to question no. – 1

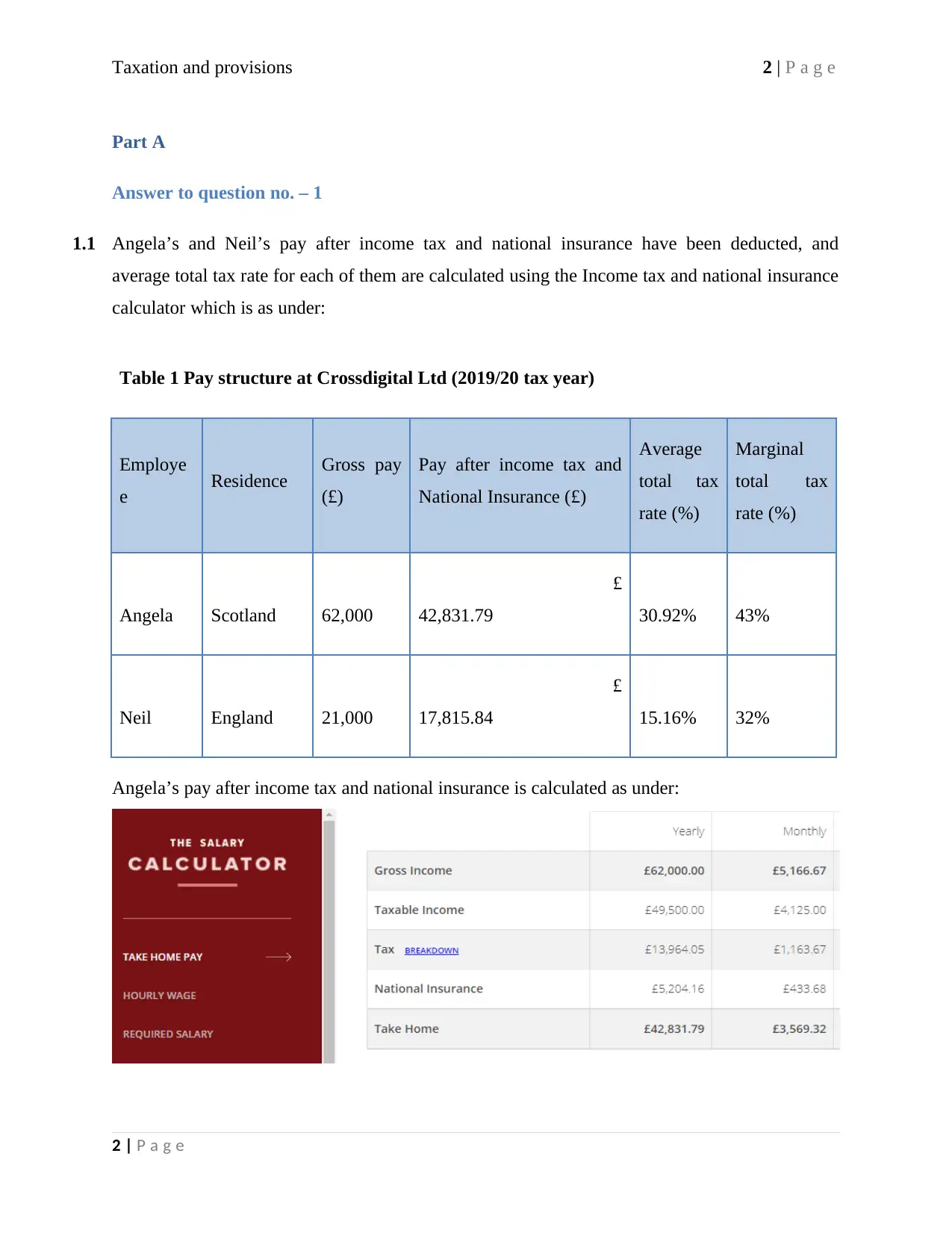

1.1 Angela’s and Neil’s pay after income tax and national insurance have been deducted, and

average total tax rate for each of them are calculated using the Income tax and national insurance

calculator which is as under:

Table 1 Pay structure at Crossdigital Ltd (2019/20 tax year)

Employe

e Residence Gross pay

(£)

Pay after income tax and

National Insurance (£)

Average

total tax

rate (%)

Marginal

total tax

rate (%)

Angela Scotland 62,000

£

42,831.79 30.92% 43%

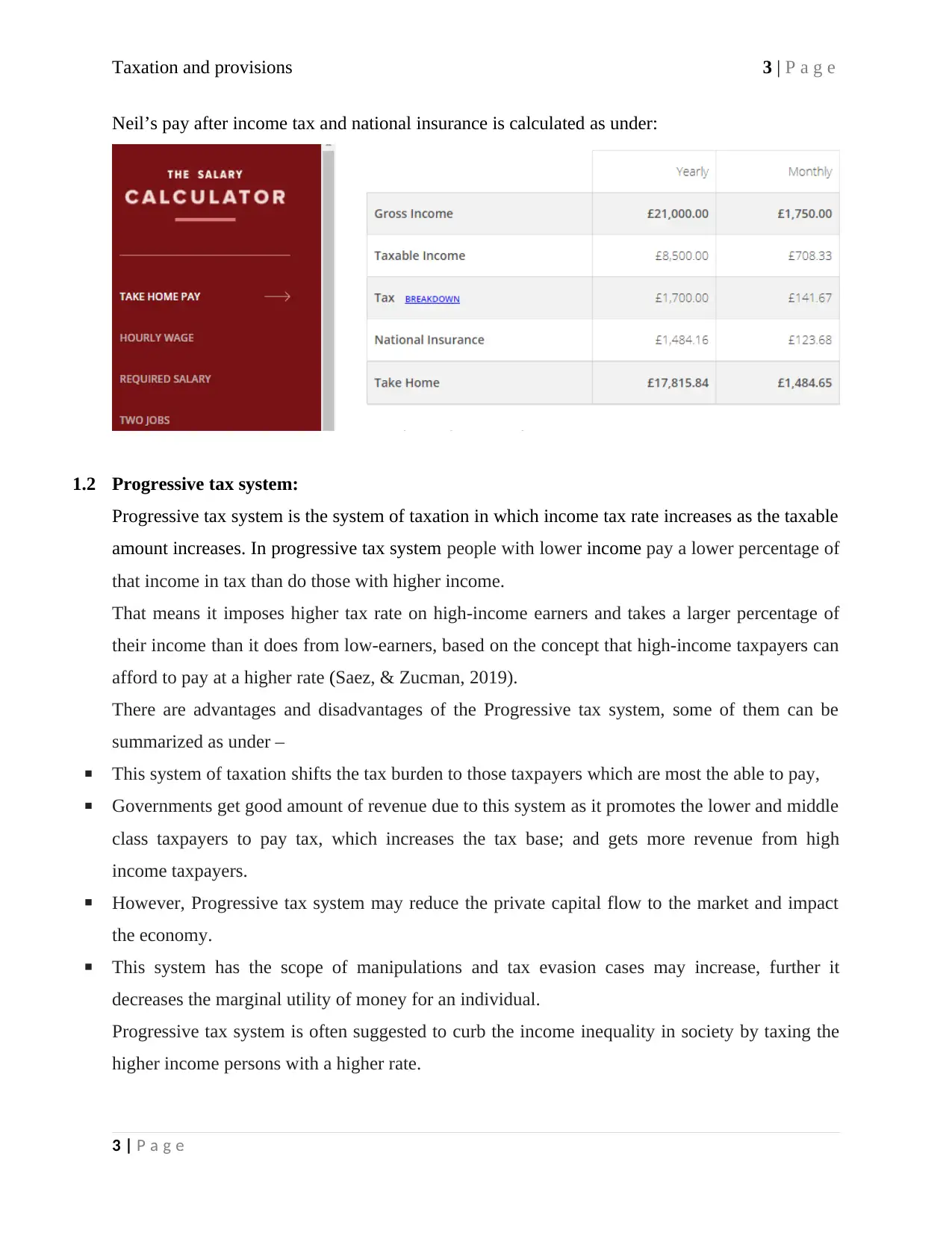

Neil England 21,000

£

17,815.84 15.16% 32%

Angela’s pay after income tax and national insurance is calculated as under:

2 | P a g e

Part A

Answer to question no. – 1

1.1 Angela’s and Neil’s pay after income tax and national insurance have been deducted, and

average total tax rate for each of them are calculated using the Income tax and national insurance

calculator which is as under:

Table 1 Pay structure at Crossdigital Ltd (2019/20 tax year)

Employe

e Residence Gross pay

(£)

Pay after income tax and

National Insurance (£)

Average

total tax

rate (%)

Marginal

total tax

rate (%)

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Neil England 21,000

£

17,815.84 15.16% 32%

Angela’s pay after income tax and national insurance is calculated as under:

2 | P a g e

Taxation and provisions 3 | P a g e

Neil’s pay after income tax and national insurance is calculated as under:

1.2 Progressive tax system:

Progressive tax system is the system of taxation in which income tax rate increases as the taxable

amount increases. In progressive tax system people with lower income pay a lower percentage of

that income in tax than do those with higher income.

That means it imposes higher tax rate on high-income earners and takes a larger percentage of

their income than it does from low-earners, based on the concept that high-income taxpayers can

afford to pay at a higher rate (Saez, & Zucman, 2019).

There are advantages and disadvantages of the Progressive tax system, some of them can be

summarized as under –

This system of taxation shifts the tax burden to those taxpayers which are most the able to pay,

Governments get good amount of revenue due to this system as it promotes the lower and middle

class taxpayers to pay tax, which increases the tax base; and gets more revenue from high

income taxpayers.

However, Progressive tax system may reduce the private capital flow to the market and impact

the economy.

This system has the scope of manipulations and tax evasion cases may increase, further it

decreases the marginal utility of money for an individual.

Progressive tax system is often suggested to curb the income inequality in society by taxing the

higher income persons with a higher rate.

3 | P a g e

Neil’s pay after income tax and national insurance is calculated as under:

1.2 Progressive tax system:

Progressive tax system is the system of taxation in which income tax rate increases as the taxable

amount increases. In progressive tax system people with lower income pay a lower percentage of

that income in tax than do those with higher income.

That means it imposes higher tax rate on high-income earners and takes a larger percentage of

their income than it does from low-earners, based on the concept that high-income taxpayers can

afford to pay at a higher rate (Saez, & Zucman, 2019).

There are advantages and disadvantages of the Progressive tax system, some of them can be

summarized as under –

This system of taxation shifts the tax burden to those taxpayers which are most the able to pay,

Governments get good amount of revenue due to this system as it promotes the lower and middle

class taxpayers to pay tax, which increases the tax base; and gets more revenue from high

income taxpayers.

However, Progressive tax system may reduce the private capital flow to the market and impact

the economy.

This system has the scope of manipulations and tax evasion cases may increase, further it

decreases the marginal utility of money for an individual.

Progressive tax system is often suggested to curb the income inequality in society by taxing the

higher income persons with a higher rate.

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation and provisions 4 | P a g e

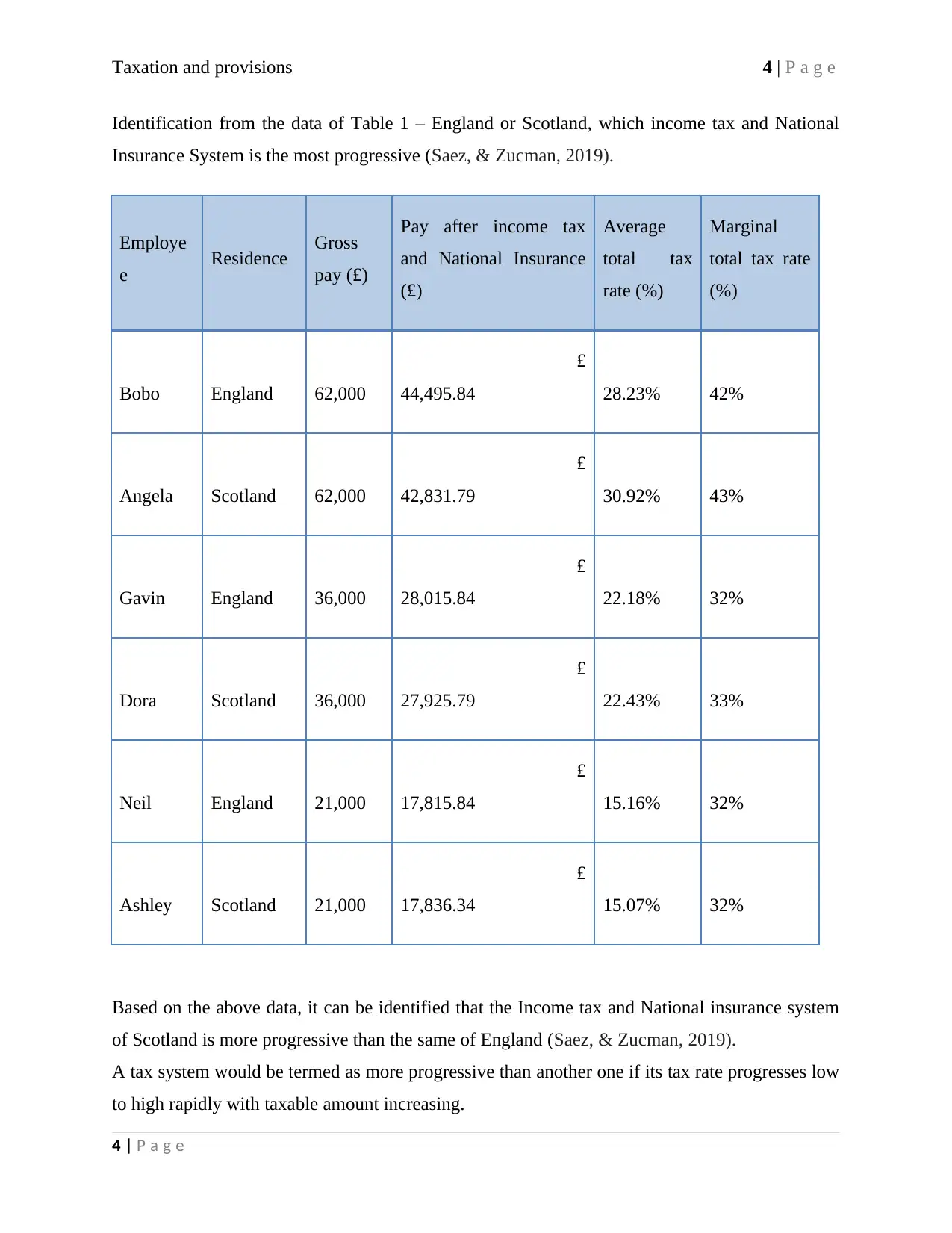

Identification from the data of Table 1 – England or Scotland, which income tax and National

Insurance System is the most progressive (Saez, & Zucman, 2019).

Employe

e Residence Gross

pay (£)

Pay after income tax

and National Insurance

(£)

Average

total tax

rate (%)

Marginal

total tax rate

(%)

Bobo England 62,000

£

44,495.84 28.23% 42%

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Gavin England 36,000

£

28,015.84 22.18% 32%

Dora Scotland 36,000

£

27,925.79 22.43% 33%

Neil England 21,000

£

17,815.84 15.16% 32%

Ashley Scotland 21,000

£

17,836.34 15.07% 32%

Based on the above data, it can be identified that the Income tax and National insurance system

of Scotland is more progressive than the same of England (Saez, & Zucman, 2019).

A tax system would be termed as more progressive than another one if its tax rate progresses low

to high rapidly with taxable amount increasing.

4 | P a g e

Identification from the data of Table 1 – England or Scotland, which income tax and National

Insurance System is the most progressive (Saez, & Zucman, 2019).

Employe

e Residence Gross

pay (£)

Pay after income tax

and National Insurance

(£)

Average

total tax

rate (%)

Marginal

total tax rate

(%)

Bobo England 62,000

£

44,495.84 28.23% 42%

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Gavin England 36,000

£

28,015.84 22.18% 32%

Dora Scotland 36,000

£

27,925.79 22.43% 33%

Neil England 21,000

£

17,815.84 15.16% 32%

Ashley Scotland 21,000

£

17,836.34 15.07% 32%

Based on the above data, it can be identified that the Income tax and National insurance system

of Scotland is more progressive than the same of England (Saez, & Zucman, 2019).

A tax system would be termed as more progressive than another one if its tax rate progresses low

to high rapidly with taxable amount increasing.

4 | P a g e

Taxation and provisions 5 | P a g e

It can be observed from the above table that with the income increasing from £21000 to £36000,

average and marginal tax rates of Scotland progresses more than that of England. Further, tax

rate progresses again for employees with the gross annual salary of £62000, and employee

residing in Scotland pays tax at a higher average rate than the employee residing in England and

gap is wider at this higher income slab.

1.3 Median value of the gross earnings of the company’s employees in today’s money:

Median salary is the center of a range of employee’s salary arranged in order from least to

greatest.

Median gross earnings of the employees of Crossdigital Ltd is as follows-

Total number of employees: 6.

Average of 3rd and 4th amount in arranged range of data: £ 36.000.

In case of even number of employees, to calculate median salary, average of earnings is required

of the two middle employees arranged in least to greatest order on the basis of pay.

In case of Crossdigital Ltd, Average of 3rd and 4th earning data arranged accordingly, would be

the median gross pay i.e. £36,000 per annum.

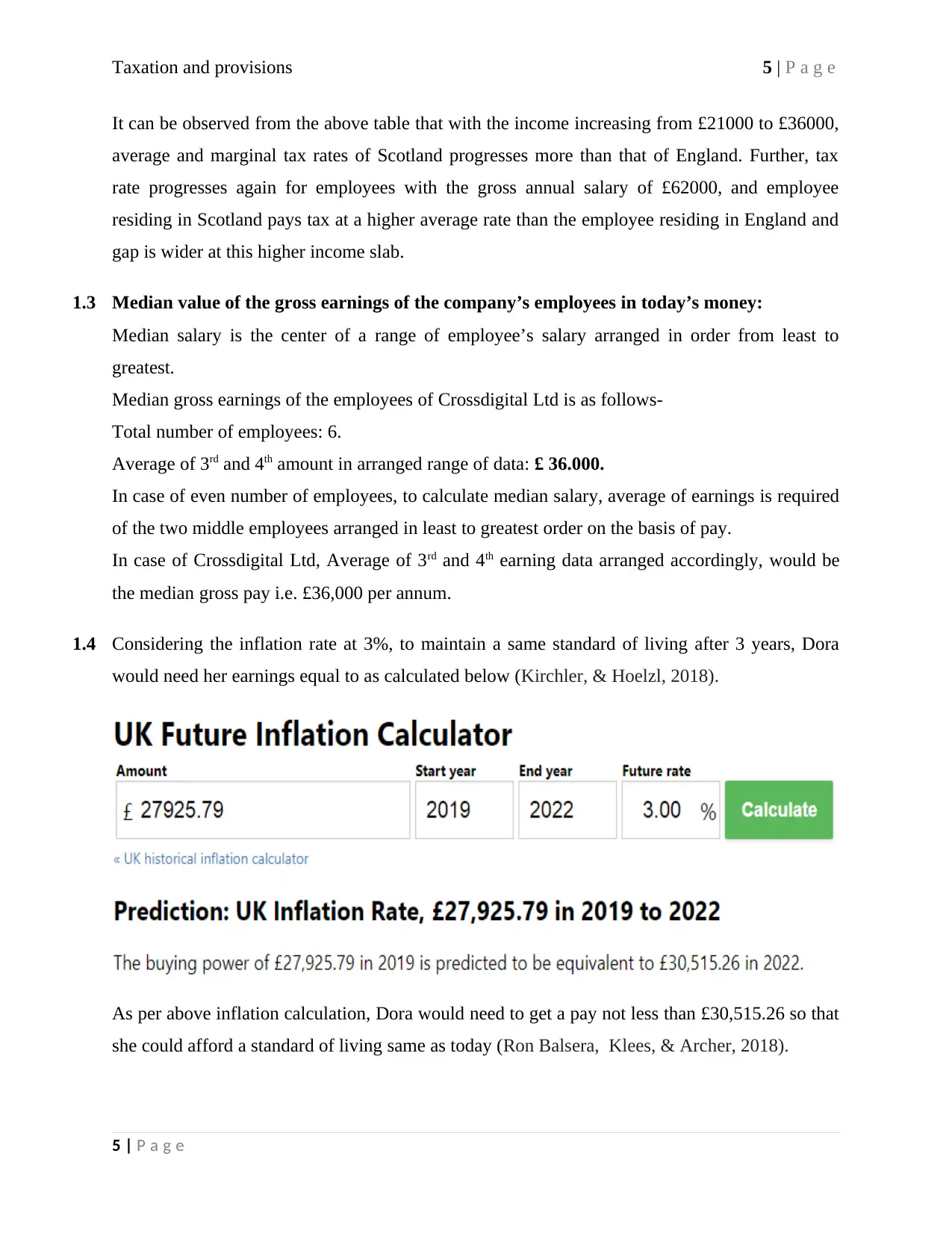

1.4 Considering the inflation rate at 3%, to maintain a same standard of living after 3 years, Dora

would need her earnings equal to as calculated below (Kirchler, & Hoelzl, 2018).

As per above inflation calculation, Dora would need to get a pay not less than £30,515.26 so that

she could afford a standard of living same as today (Ron Balsera, Klees, & Archer, 2018).

5 | P a g e

It can be observed from the above table that with the income increasing from £21000 to £36000,

average and marginal tax rates of Scotland progresses more than that of England. Further, tax

rate progresses again for employees with the gross annual salary of £62000, and employee

residing in Scotland pays tax at a higher average rate than the employee residing in England and

gap is wider at this higher income slab.

1.3 Median value of the gross earnings of the company’s employees in today’s money:

Median salary is the center of a range of employee’s salary arranged in order from least to

greatest.

Median gross earnings of the employees of Crossdigital Ltd is as follows-

Total number of employees: 6.

Average of 3rd and 4th amount in arranged range of data: £ 36.000.

In case of even number of employees, to calculate median salary, average of earnings is required

of the two middle employees arranged in least to greatest order on the basis of pay.

In case of Crossdigital Ltd, Average of 3rd and 4th earning data arranged accordingly, would be

the median gross pay i.e. £36,000 per annum.

1.4 Considering the inflation rate at 3%, to maintain a same standard of living after 3 years, Dora

would need her earnings equal to as calculated below (Kirchler, & Hoelzl, 2018).

As per above inflation calculation, Dora would need to get a pay not less than £30,515.26 so that

she could afford a standard of living same as today (Ron Balsera, Klees, & Archer, 2018).

5 | P a g e

Taxation and provisions 6 | P a g e

As per available data, Dora’s pay in 2022/23 after income tax and national insurance would rise

to £29,881, with this pay Dora could not maintain the purchasing power of £27,925.79 as that

would require a pay equivalent to £30,515.26 as calculated above; so it can be concluded that

Dora could afford a standard of living lower than as today.

Answer to question no. – 2

2.1 Calculation annual equalized net income of Lily and Rick’s new household together:

For the calculation of equalized net income of household, modified OECD scale is the standard

scale and which is being used widely.

Equalized income is a measure of household income that takes account of the differences in a

household's size and composition, and thus is equalized or made equivalent for all household

sizes and compositions. It is used for the calculation of poverty, standard of living and social

exclusion indicators (Luja, 2018).

By dividing the total household income from all the sources by its equalized size, which is

calculated by using the modified OECD scale, equalized income can be calculated.

Equalized size is the sum of weights attributed to every household member by modified OECD

scale.

Weight attributed by scale for household members are as follows:

Type of Household Member Equivalence

value

First adult 1.0

Additional adult 0.5

Child aged: 14 and over 0.5

Child aged: 0-13 0.3

6 | P a g e

As per available data, Dora’s pay in 2022/23 after income tax and national insurance would rise

to £29,881, with this pay Dora could not maintain the purchasing power of £27,925.79 as that

would require a pay equivalent to £30,515.26 as calculated above; so it can be concluded that

Dora could afford a standard of living lower than as today.

Answer to question no. – 2

2.1 Calculation annual equalized net income of Lily and Rick’s new household together:

For the calculation of equalized net income of household, modified OECD scale is the standard

scale and which is being used widely.

Equalized income is a measure of household income that takes account of the differences in a

household's size and composition, and thus is equalized or made equivalent for all household

sizes and compositions. It is used for the calculation of poverty, standard of living and social

exclusion indicators (Luja, 2018).

By dividing the total household income from all the sources by its equalized size, which is

calculated by using the modified OECD scale, equalized income can be calculated.

Equalized size is the sum of weights attributed to every household member by modified OECD

scale.

Weight attributed by scale for household members are as follows:

Type of Household Member Equivalence

value

First adult 1.0

Additional adult 0.5

Child aged: 14 and over 0.5

Child aged: 0-13 0.3

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 7 | P a g e

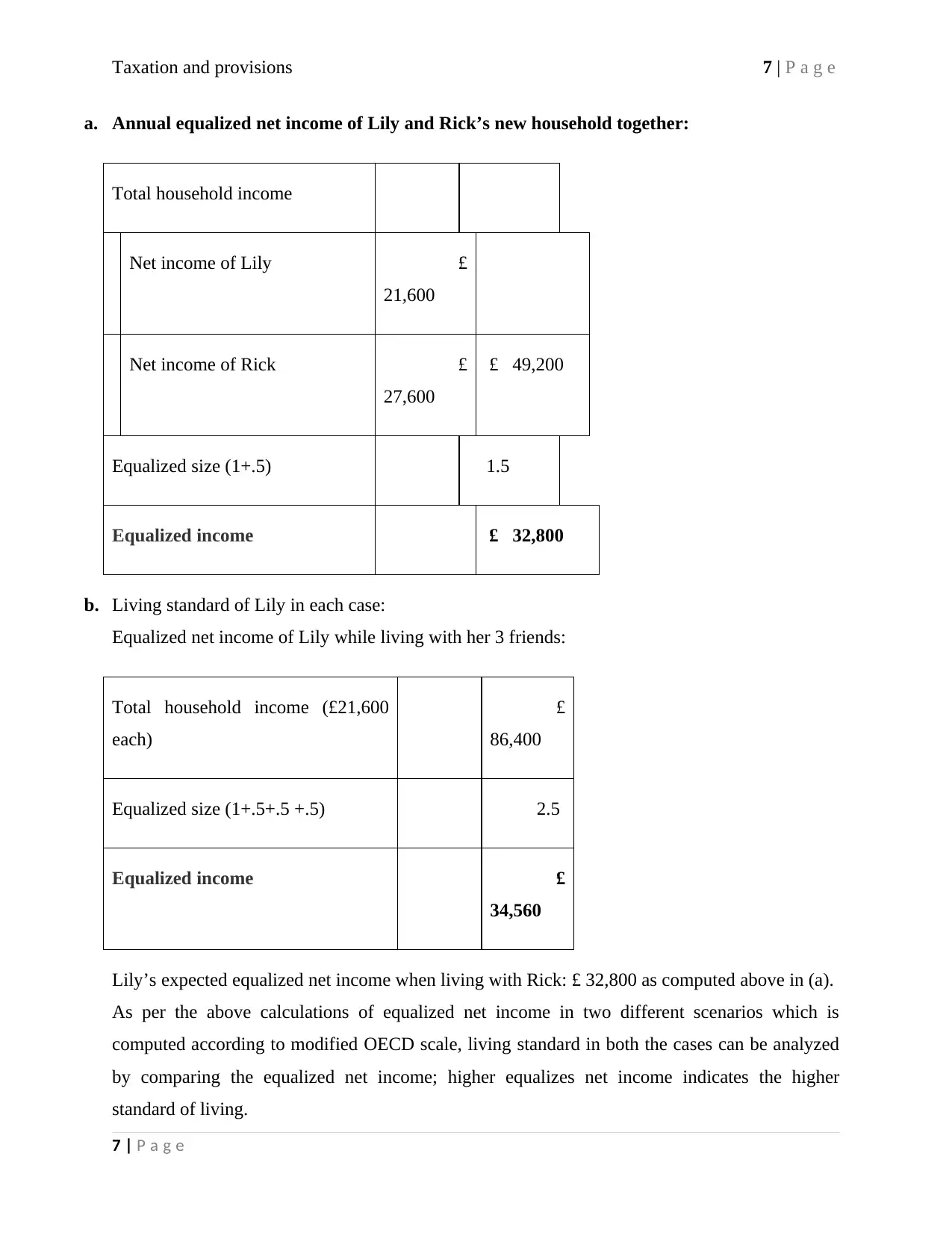

a. Annual equalized net income of Lily and Rick’s new household together:

Total household income

Net income of Lily £

21,600

Net income of Rick £

27,600

£ 49,200

Equalized size (1+.5) 1.5

Equalized income £ 32,800

b. Living standard of Lily in each case:

Equalized net income of Lily while living with her 3 friends:

Total household income (£21,600

each)

£

86,400

Equalized size (1+.5+.5 +.5) 2.5

Equalized income £

34,560

Lily’s expected equalized net income when living with Rick: £ 32,800 as computed above in (a).

As per the above calculations of equalized net income in two different scenarios which is

computed according to modified OECD scale, living standard in both the cases can be analyzed

by comparing the equalized net income; higher equalizes net income indicates the higher

standard of living.

7 | P a g e

a. Annual equalized net income of Lily and Rick’s new household together:

Total household income

Net income of Lily £

21,600

Net income of Rick £

27,600

£ 49,200

Equalized size (1+.5) 1.5

Equalized income £ 32,800

b. Living standard of Lily in each case:

Equalized net income of Lily while living with her 3 friends:

Total household income (£21,600

each)

£

86,400

Equalized size (1+.5+.5 +.5) 2.5

Equalized income £

34,560

Lily’s expected equalized net income when living with Rick: £ 32,800 as computed above in (a).

As per the above calculations of equalized net income in two different scenarios which is

computed according to modified OECD scale, living standard in both the cases can be analyzed

by comparing the equalized net income; higher equalizes net income indicates the higher

standard of living.

7 | P a g e

Taxation and provisions 8 | P a g e

As Lily’s equalized net income is higher while living with her friends (£34,560 compared to

£32,800), Lily has higher living standard than she could afford when living with Rick (Jalan, &

Vaidyanathan, 2017)

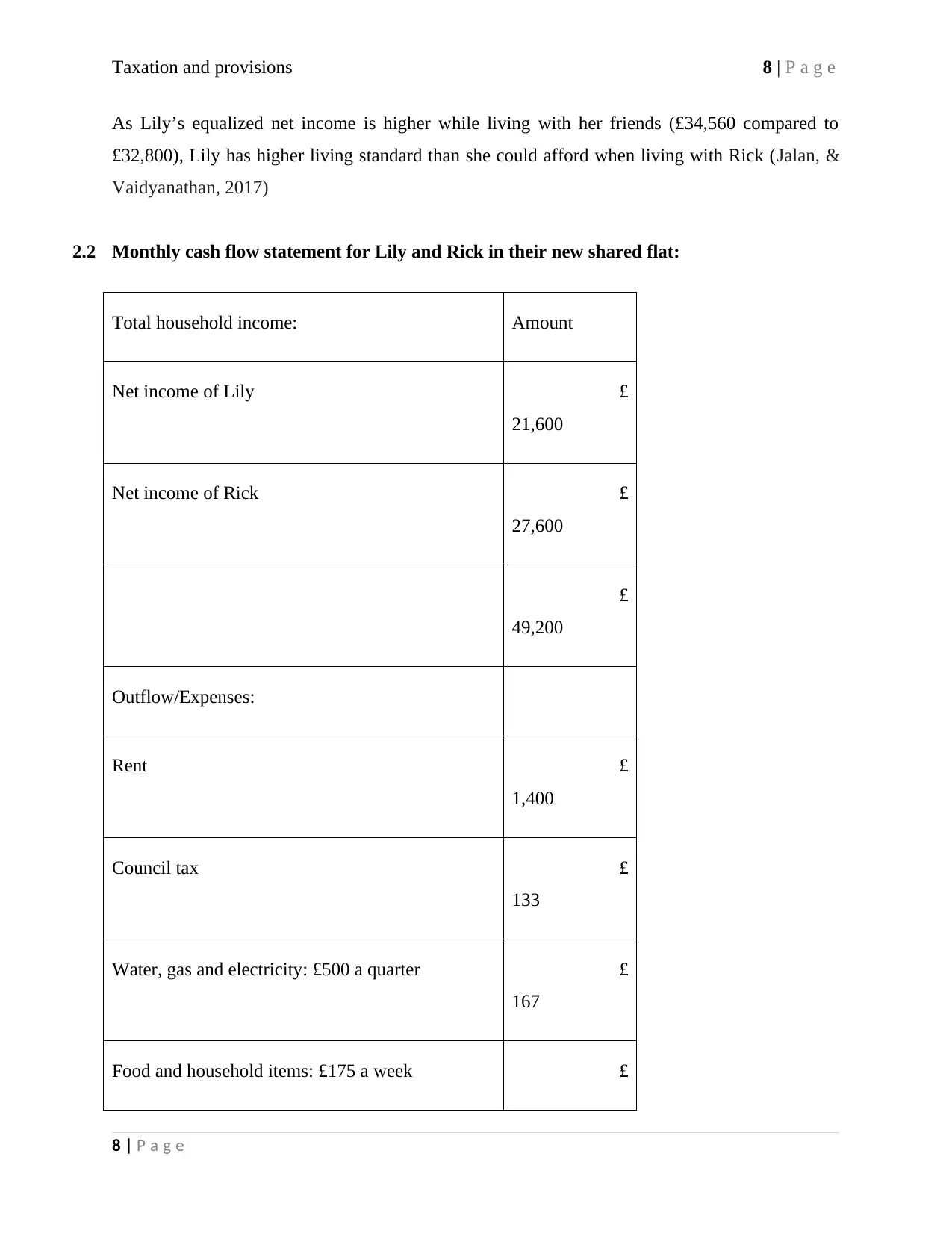

2.2 Monthly cash flow statement for Lily and Rick in their new shared flat:

Total household income: Amount

Net income of Lily £

21,600

Net income of Rick £

27,600

£

49,200

Outflow/Expenses:

Rent £

1,400

Council tax £

133

Water, gas and electricity: £500 a quarter £

167

Food and household items: £175 a week £

8 | P a g e

As Lily’s equalized net income is higher while living with her friends (£34,560 compared to

£32,800), Lily has higher living standard than she could afford when living with Rick (Jalan, &

Vaidyanathan, 2017)

2.2 Monthly cash flow statement for Lily and Rick in their new shared flat:

Total household income: Amount

Net income of Lily £

21,600

Net income of Rick £

27,600

£

49,200

Outflow/Expenses:

Rent £

1,400

Council tax £

133

Water, gas and electricity: £500 a quarter £

167

Food and household items: £175 a week £

8 | P a g e

Taxation and provisions 9 | P a g e

758

Alcohol, going out, leisure activities: £480 a

month

£

480

Phones and broadband: £108 a month £

108

Transport: £709 a month £

709

Other essentials: £262 a month £

262

£

4,017

Cash balance at the end of the month £

83

2.3 Lily and Rick’s financial position:

Lily and Rick want to save up to buying their own house which will require them to save

£10,000 over the next two years (Ron Balsera, Klees, & Archer, 2018).

As per Lily and Rick’s monthly cash flow statement, they are able to save £ 83 monthly after

considering their all the income and expenses.

Lily and Rick will need to save £ 10,000 over the next two years to buy a house, which requires

them to save at least £ 417 every month (Jalan, & Vaidyanathan, 2017).

9 | P a g e

758

Alcohol, going out, leisure activities: £480 a

month

£

480

Phones and broadband: £108 a month £

108

Transport: £709 a month £

709

Other essentials: £262 a month £

262

£

4,017

Cash balance at the end of the month £

83

2.3 Lily and Rick’s financial position:

Lily and Rick want to save up to buying their own house which will require them to save

£10,000 over the next two years (Ron Balsera, Klees, & Archer, 2018).

As per Lily and Rick’s monthly cash flow statement, they are able to save £ 83 monthly after

considering their all the income and expenses.

Lily and Rick will need to save £ 10,000 over the next two years to buy a house, which requires

them to save at least £ 417 every month (Jalan, & Vaidyanathan, 2017).

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation and provisions 10 | P a g e

By comparing their expected monthly saving with required monthly saving to buy a house, it is

clear that they need to make some adjustments in their household expenses to save further £ 334

monthly. For saving £10,000 in next two years, they can consider the adjustments in non-

essential expenditures and may also consider shifting in a less expensive residence to cut short

their expenditures (Jalan, & Vaidyanathan, 2017).

The whole calculation can be understood from following table:

Required monthly saving (£ 10,000/24 months) £

417

Monthly saving according to current budget £

83

Additional monthly saving required £

334

Answer to question no. – 3

3.1 Michelle’s borrowing options:

Monthly

payment

Repaymen

t period

Total interest

paid

Option A £ 276.47 1 Year

£

317.64

Option B £ 50.00 10 Years

£

3,870.55

10 | P a g e

By comparing their expected monthly saving with required monthly saving to buy a house, it is

clear that they need to make some adjustments in their household expenses to save further £ 334

monthly. For saving £10,000 in next two years, they can consider the adjustments in non-

essential expenditures and may also consider shifting in a less expensive residence to cut short

their expenditures (Jalan, & Vaidyanathan, 2017).

The whole calculation can be understood from following table:

Required monthly saving (£ 10,000/24 months) £

417

Monthly saving according to current budget £

83

Additional monthly saving required £

334

Answer to question no. – 3

3.1 Michelle’s borrowing options:

Monthly

payment

Repaymen

t period

Total interest

paid

Option A £ 276.47 1 Year

£

317.64

Option B £ 50.00 10 Years

£

3,870.55

10 | P a g e

Taxation and provisions 11 | P a g e

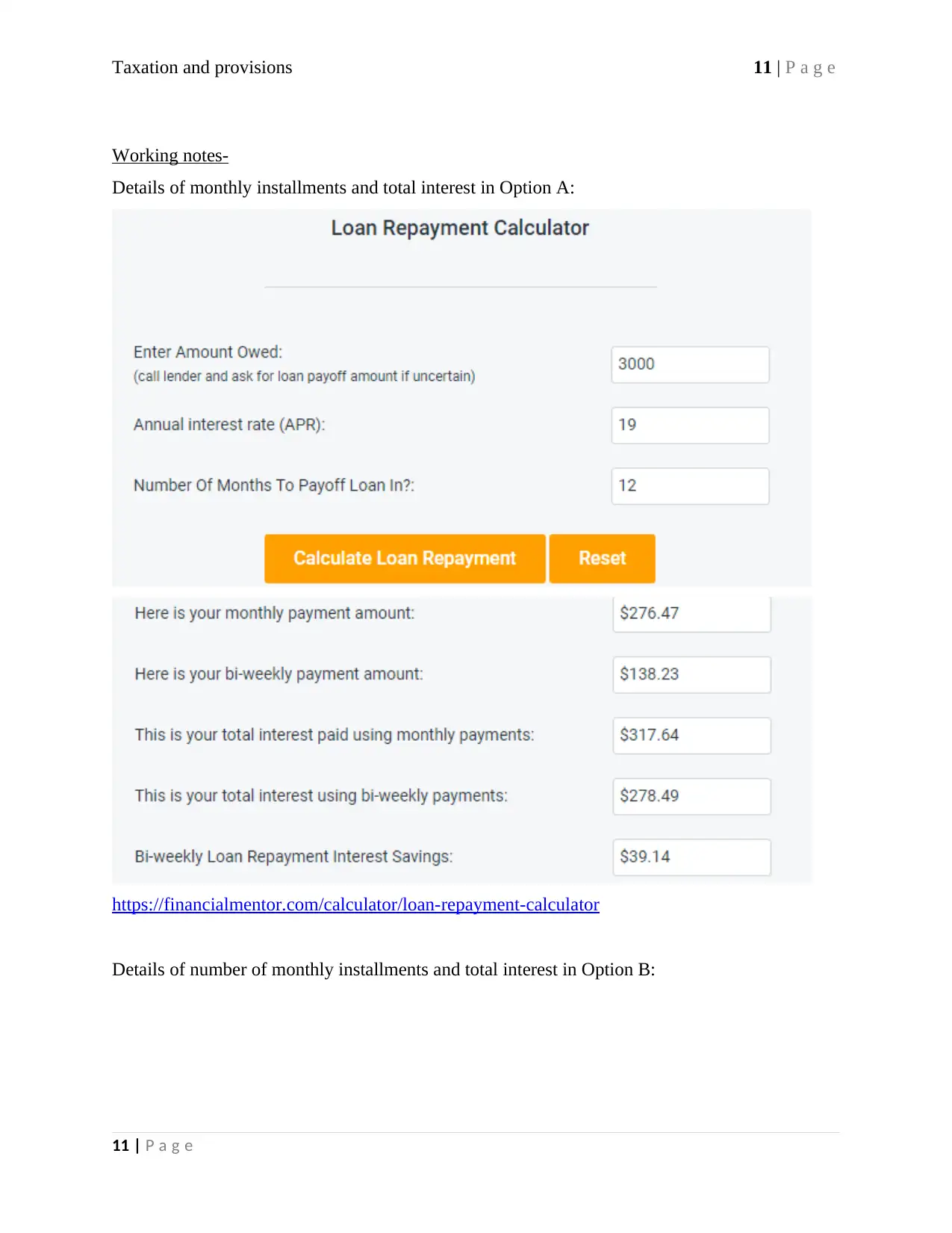

Working notes-

Details of monthly installments and total interest in Option A:

https://financialmentor.com/calculator/loan-repayment-calculator

Details of number of monthly installments and total interest in Option B:

11 | P a g e

Working notes-

Details of monthly installments and total interest in Option A:

https://financialmentor.com/calculator/loan-repayment-calculator

Details of number of monthly installments and total interest in Option B:

11 | P a g e

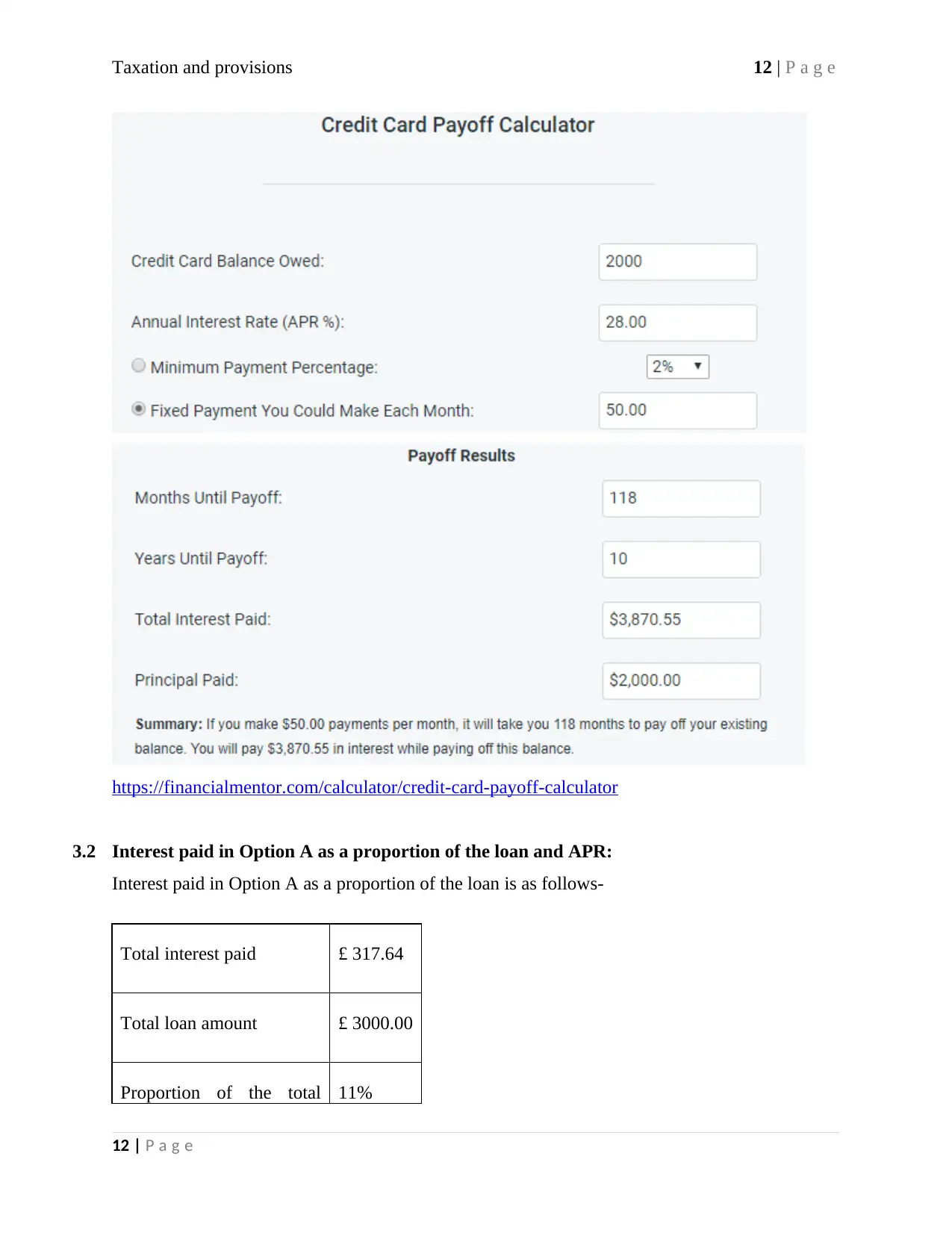

Taxation and provisions 12 | P a g e

https://financialmentor.com/calculator/credit-card-payoff-calculator

3.2 Interest paid in Option A as a proportion of the loan and APR:

Interest paid in Option A as a proportion of the loan is as follows-

Total interest paid £ 317.64

Total loan amount £ 3000.00

Proportion of the total 11%

12 | P a g e

https://financialmentor.com/calculator/credit-card-payoff-calculator

3.2 Interest paid in Option A as a proportion of the loan and APR:

Interest paid in Option A as a proportion of the loan is as follows-

Total interest paid £ 317.64

Total loan amount £ 3000.00

Proportion of the total 11%

12 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 13 | P a g e

loan

Annual percentage rate (APR): APR for loan refers to the total amount paid to lender in addition

to principal amount over the course of a year in respect to such loan, which includes both the

interest rate and any other charges or fee associated with the loan.

APR makes it clear to the borrower about the total cost of the loan which is crucial for

comparing between all the available options (Jalan, & Vaidyanathan, 2017).

In other words, APR tells how much you pay for the loan each year.

In Michelle’s borrowing Option A, total borrowing is being repaid in 12 months with monthly

installments of £ 276.47 starting from the very first month, which means that Michelle have not

used the borrowed money for the whole year, which further widens the gap between the APR

and interest as the proportion of the borrowed amount.

In Option A, if Michelle pays the whole amount at the year end, then interest cost as the

proportion to the loan and APR would be same as there are no other loan charges.

In the given situation, interest cost as a proportion of the total loan is just 11% and APR for the

loan is at 19%, and this difference is due to the repayment pattern of the loan (Saez, & Zucman,

2019).

3.3 Advantages of Option A over Option B:

Low interest cost – In the option A, Michelle can pay for the holiday in 12 monthly installments

at an APR of 19%, which is effectively at just 11% as a proportion of the total loan; wherein

Option B, Michelle is required to pay at the rate of 28% and this cost continue to incurs for the

next 10 years. In the Option B, Michelle pays 190% of the principal amount in form of interest

cost during the lifespan of the loan, which is significantly high.

Short term obligation – In the Option A, Michelle is required to repay the loan in next one year

in monthly installments, and in Option B, she needs to pay a fixed monthly installment of £ 50,

for the next 10 years. Comparing the life span of the loan in the both options, it can be observed

that repayment obligation in Option B will continue for the next 10 years where it will last for

one year only in the Option A, so obligation period to repay the loan is significantly high in

Option B (Kirchler, & Hoelzl, 2018).

13 | P a g e

loan

Annual percentage rate (APR): APR for loan refers to the total amount paid to lender in addition

to principal amount over the course of a year in respect to such loan, which includes both the

interest rate and any other charges or fee associated with the loan.

APR makes it clear to the borrower about the total cost of the loan which is crucial for

comparing between all the available options (Jalan, & Vaidyanathan, 2017).

In other words, APR tells how much you pay for the loan each year.

In Michelle’s borrowing Option A, total borrowing is being repaid in 12 months with monthly

installments of £ 276.47 starting from the very first month, which means that Michelle have not

used the borrowed money for the whole year, which further widens the gap between the APR

and interest as the proportion of the borrowed amount.

In Option A, if Michelle pays the whole amount at the year end, then interest cost as the

proportion to the loan and APR would be same as there are no other loan charges.

In the given situation, interest cost as a proportion of the total loan is just 11% and APR for the

loan is at 19%, and this difference is due to the repayment pattern of the loan (Saez, & Zucman,

2019).

3.3 Advantages of Option A over Option B:

Low interest cost – In the option A, Michelle can pay for the holiday in 12 monthly installments

at an APR of 19%, which is effectively at just 11% as a proportion of the total loan; wherein

Option B, Michelle is required to pay at the rate of 28% and this cost continue to incurs for the

next 10 years. In the Option B, Michelle pays 190% of the principal amount in form of interest

cost during the lifespan of the loan, which is significantly high.

Short term obligation – In the Option A, Michelle is required to repay the loan in next one year

in monthly installments, and in Option B, she needs to pay a fixed monthly installment of £ 50,

for the next 10 years. Comparing the life span of the loan in the both options, it can be observed

that repayment obligation in Option B will continue for the next 10 years where it will last for

one year only in the Option A, so obligation period to repay the loan is significantly high in

Option B (Kirchler, & Hoelzl, 2018).

13 | P a g e

Taxation and provisions 14 | P a g e

Disadvantage of Option A over Option B:

Higher cash outflow – In the Option A, Michelle needs to pay a sum of £3,317.64 in the first

year, where in Option B, she is required to pay £50 monthly which is annual cash outflow of just

£600. So, in Option A, cash outflow in first year is much higher than that in Option B.

Cash outflow in first year:

Option A £ 3,317.64

Option B £ 600.00

Part B

Factors that may have contributed to the level of unsecured borrowing by households in

the UK:

Introduction

UK household in year 2018 owes an average of £15,385 to credit card firms, banks and other

landers according to the TUC (Trades Union Congress) (Ron Balsera, , Klees, & Archer, 2018).

According to TUC, level of unsecured debt as a share of total household income is now 30.4%,

which is the highest level it has ever been so far and well above the peak in 2008 before the

financial crisis.

There may be various factors which have affected the unsecured debt level of UK household, for

that analysis, it should be considered that what is meant by unsecured debt, various types of

unsecured debt and the different factors which may affect the unsecured debt (Luja, 2018).

14 | P a g e

Disadvantage of Option A over Option B:

Higher cash outflow – In the Option A, Michelle needs to pay a sum of £3,317.64 in the first

year, where in Option B, she is required to pay £50 monthly which is annual cash outflow of just

£600. So, in Option A, cash outflow in first year is much higher than that in Option B.

Cash outflow in first year:

Option A £ 3,317.64

Option B £ 600.00

Part B

Factors that may have contributed to the level of unsecured borrowing by households in

the UK:

Introduction

UK household in year 2018 owes an average of £15,385 to credit card firms, banks and other

landers according to the TUC (Trades Union Congress) (Ron Balsera, , Klees, & Archer, 2018).

According to TUC, level of unsecured debt as a share of total household income is now 30.4%,

which is the highest level it has ever been so far and well above the peak in 2008 before the

financial crisis.

There may be various factors which have affected the unsecured debt level of UK household, for

that analysis, it should be considered that what is meant by unsecured debt, various types of

unsecured debt and the different factors which may affect the unsecured debt (Luja, 2018).

14 | P a g e

Taxation and provisions 15 | P a g e

Unsecured Debt

Unsecured debt refers to any type of the debt which is not secured by any collateral security of

the borrower like home or automobile, or protected by a guarantor.

In case of bankruptcy of borrower, unsecured debt can be wiped out as borrower is not required

to pledge any of his security and lender or unsecured creditors have the general claim on the

assets of the borrower after the already pledged securities assigned to secured debtors. Due to

this, unsecured creditors usually realize a smaller portion of their claims.

Unsecured debt includes credit card debt, personal loan, medical and student loan, corporate

unsecured loan, consumer durable loan (Jalan, & Vaidyanathan, 2017).

Unsecured debts generally carry a higher interest rate than the secured loans as creditors tends to

demand high interest rate as a condition to extending such debt considering the associated high

risks.

Unsecured debts are generally sought in case of requirement of additional capital although

existing assets already have been pledged to secured creditors. It also helps you clear your debt

faster and for less money by allowing exploring debt relief options like debt management, debt

consolidation and debt settlement (Bramall, 2017).

Different types of unsecured borrowing:

Credit card debts – Credit card loan is revolving line of credit, means you can keep borrowing

each month and carry over the balance. It is most pervasive type of unsecured debt, however

some credit cards are secured too angst a security deposit equal to the appending limit on the

card. Credit card interest rates can increase to 25-29% or higher in case of default.

Credit card debt was at £2688 per household at the end of November.

Personal loan – Personal loan means loan taken to meet one’s unspecified financial needs which

can be funding a start-up business or meet emergency medical expenses.

Today, personal loan segment has diverted into different specific loans. Personal loan terms are

defined on the basis of credit history, a good credit score means lower interest rates (Pántya, et

al. 2016).

15 | P a g e

Unsecured Debt

Unsecured debt refers to any type of the debt which is not secured by any collateral security of

the borrower like home or automobile, or protected by a guarantor.

In case of bankruptcy of borrower, unsecured debt can be wiped out as borrower is not required

to pledge any of his security and lender or unsecured creditors have the general claim on the

assets of the borrower after the already pledged securities assigned to secured debtors. Due to

this, unsecured creditors usually realize a smaller portion of their claims.

Unsecured debt includes credit card debt, personal loan, medical and student loan, corporate

unsecured loan, consumer durable loan (Jalan, & Vaidyanathan, 2017).

Unsecured debts generally carry a higher interest rate than the secured loans as creditors tends to

demand high interest rate as a condition to extending such debt considering the associated high

risks.

Unsecured debts are generally sought in case of requirement of additional capital although

existing assets already have been pledged to secured creditors. It also helps you clear your debt

faster and for less money by allowing exploring debt relief options like debt management, debt

consolidation and debt settlement (Bramall, 2017).

Different types of unsecured borrowing:

Credit card debts – Credit card loan is revolving line of credit, means you can keep borrowing

each month and carry over the balance. It is most pervasive type of unsecured debt, however

some credit cards are secured too angst a security deposit equal to the appending limit on the

card. Credit card interest rates can increase to 25-29% or higher in case of default.

Credit card debt was at £2688 per household at the end of November.

Personal loan – Personal loan means loan taken to meet one’s unspecified financial needs which

can be funding a start-up business or meet emergency medical expenses.

Today, personal loan segment has diverted into different specific loans. Personal loan terms are

defined on the basis of credit history, a good credit score means lower interest rates (Pántya, et

al. 2016).

15 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation and provisions 16 | P a g e

Corporate unsecured debt – Corporate debt or business loans are being used to meet the

expenses, these loans are in form of unsecured line of credit, and limits and terms are defined for

these on the basis of business’s credit rating. Credit lines are pools of cash which can

businessmen tap when money is short and needs are intense.

Consumer finance – Consumer finance is basically financing your customer to buy product,

which can be in the form of no-cost EMI, however no-cost EMI faces many rules and regulations

in different countries (Shome, 2018).

Student loans – Student loans are generally granted to students perusing graduation or post-

graduation courses, this is the major chunk of the average UK household debt. As per TUC,

graduates are now can expect to leave degree courses with debt of £50,000.

Factors which may have contributed to the level of unsecured household debt:

Interest rates and flexible repayment terms – According to FCA reports, there was an extra

borrowing of £6,00,000 in year 2018, in form of high cost loans. This is due to that high cost

lenders have moved away from stringent conditions and high interest rates and started to offer

flexible repayment terms (Aronson, Johnson, & Lambert, 2014)

More products in market have started to offer quick loans and assisting the one with bad credit

scores too, though with a higher interest rate.

Student loans – Student loans added a considerable amount to the average unsecured debt

amount and brought that to the level of 30.4% of the income across the country, which is even

higher than the period prior to the financial crisis of 2008.

However, a Bank of England figure, which excludes student loans, gave a debt data half of the

TUC figures, though that is also significantly high.

Loan reliant – Low income level due to years of wage stagnation and comparatively high living

standards and spending habits, which affects the income and borrowings data; have forced the

household to be loan reliant. Which took average unsecured debt level to worse than before the

financial crisis.

Wage stagnation and low wages – According to TUC report and as TUC general secretary

Frances O’Grady said, years of years of austerity and wage stagnation has pushed millions of

families deep into red. Further she said that economy is not working for workers and they need

stronger rights and bargaining powers. Current minimum wage of £7.83 per hour for the people

16 | P a g e

Corporate unsecured debt – Corporate debt or business loans are being used to meet the

expenses, these loans are in form of unsecured line of credit, and limits and terms are defined for

these on the basis of business’s credit rating. Credit lines are pools of cash which can

businessmen tap when money is short and needs are intense.

Consumer finance – Consumer finance is basically financing your customer to buy product,

which can be in the form of no-cost EMI, however no-cost EMI faces many rules and regulations

in different countries (Shome, 2018).

Student loans – Student loans are generally granted to students perusing graduation or post-

graduation courses, this is the major chunk of the average UK household debt. As per TUC,

graduates are now can expect to leave degree courses with debt of £50,000.

Factors which may have contributed to the level of unsecured household debt:

Interest rates and flexible repayment terms – According to FCA reports, there was an extra

borrowing of £6,00,000 in year 2018, in form of high cost loans. This is due to that high cost

lenders have moved away from stringent conditions and high interest rates and started to offer

flexible repayment terms (Aronson, Johnson, & Lambert, 2014)

More products in market have started to offer quick loans and assisting the one with bad credit

scores too, though with a higher interest rate.

Student loans – Student loans added a considerable amount to the average unsecured debt

amount and brought that to the level of 30.4% of the income across the country, which is even

higher than the period prior to the financial crisis of 2008.

However, a Bank of England figure, which excludes student loans, gave a debt data half of the

TUC figures, though that is also significantly high.

Loan reliant – Low income level due to years of wage stagnation and comparatively high living

standards and spending habits, which affects the income and borrowings data; have forced the

household to be loan reliant. Which took average unsecured debt level to worse than before the

financial crisis.

Wage stagnation and low wages – According to TUC report and as TUC general secretary

Frances O’Grady said, years of years of austerity and wage stagnation has pushed millions of

families deep into red. Further she said that economy is not working for workers and they need

stronger rights and bargaining powers. Current minimum wage of £7.83 per hour for the people

16 | P a g e

Taxation and provisions 17 | P a g e

aged more than 25, is need to be raised to at least £10 per hour as soon as possible to be out of

this crisis (Nattrass, & Seekings, 2011).)

There is a huge jump in average unsecured debts of £86 per household from just a year prior, and

in total, debt rose to a staggering £428 billion in the third quarter of year 2019.

Years of austerity and public spending cuts – As per TUC, government is skating on the thin ice

by relying on household debt to drive growth. Years of austerity and public spending cuts and

wage stagnation, all combined together are the key reasons of this unprecedented debt rise

(Lockwood, & Weinzierl, 2016).

Rise in zero-hour contract – Further, rise of the gig economy and zero-hour contracts are also the

contributors of this rise. Zero-hour contracts indicates the work insecurity which is basically due

to the gig economy, these factors resulted in wage stagnation too for a period of decade. Same

concerns were raised by Bank of England chief; which are now indicated to be key contributing

factors.

Part C

Team Work:

Team work is collective effort by a group of individuals to achieve a common goal, with the

most efficiency and effectiveness (Sadka, 2016).

In team work, interdependent individuals of a team collaborate and contribute by their skills and

providing constructive feedback to achieve predefined common goal, and teamwork is seen

within the greater framework of a team to which it proves to be backbone.

Advantage of working in a team:

Teamwork helps solve problems – Collaborating within a group helps solving complex

problems; Brainstorming is a good opportunity for the individual team members to exchange

unique ideas, which in a way foster creativity and learning of team members, and they can find

creative and best way to solve that problem (Chapman, 2013). Team work blends

complementary strengths of team members and builds trust among them, as they are required to

17 | P a g e

aged more than 25, is need to be raised to at least £10 per hour as soon as possible to be out of

this crisis (Nattrass, & Seekings, 2011).)

There is a huge jump in average unsecured debts of £86 per household from just a year prior, and

in total, debt rose to a staggering £428 billion in the third quarter of year 2019.

Years of austerity and public spending cuts – As per TUC, government is skating on the thin ice

by relying on household debt to drive growth. Years of austerity and public spending cuts and

wage stagnation, all combined together are the key reasons of this unprecedented debt rise

(Lockwood, & Weinzierl, 2016).

Rise in zero-hour contract – Further, rise of the gig economy and zero-hour contracts are also the

contributors of this rise. Zero-hour contracts indicates the work insecurity which is basically due

to the gig economy, these factors resulted in wage stagnation too for a period of decade. Same

concerns were raised by Bank of England chief; which are now indicated to be key contributing

factors.

Part C

Team Work:

Team work is collective effort by a group of individuals to achieve a common goal, with the

most efficiency and effectiveness (Sadka, 2016).

In team work, interdependent individuals of a team collaborate and contribute by their skills and

providing constructive feedback to achieve predefined common goal, and teamwork is seen

within the greater framework of a team to which it proves to be backbone.

Advantage of working in a team:

Teamwork helps solve problems – Collaborating within a group helps solving complex

problems; Brainstorming is a good opportunity for the individual team members to exchange

unique ideas, which in a way foster creativity and learning of team members, and they can find

creative and best way to solve that problem (Chapman, 2013). Team work blends

complementary strengths of team members and builds trust among them, as they are required to

17 | P a g e

Taxation and provisions 18 | P a g e

complete such work in a limited time; team work in this way finds best way to solve any

problem.

Disadvantage of working in a team:

Unequal participation – A team can only get the advantages of team work when all the team

members participate equally in particular work or task. Unequal participation is the main

disadvantage of team work; due to this a team may not get the desired outcome. Unequal

participation of team member may create many problems within the team and that negatively

affects the results. Team work might not deliver a creative and best possible solution in a timely

manner if team members are not participating equally. This may happens due to intrinsic

conflicts, avoiding work or not putting individual ideas and thinking (Schneider, 2010).

18 | P a g e

complete such work in a limited time; team work in this way finds best way to solve any

problem.

Disadvantage of working in a team:

Unequal participation – A team can only get the advantages of team work when all the team

members participate equally in particular work or task. Unequal participation is the main

disadvantage of team work; due to this a team may not get the desired outcome. Unequal

participation of team member may create many problems within the team and that negatively

affects the results. Team work might not deliver a creative and best possible solution in a timely

manner if team members are not participating equally. This may happens due to intrinsic

conflicts, avoiding work or not putting individual ideas and thinking (Schneider, 2010).

18 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 19 | P a g e

References

Aronson, J. R., Johnson, P., & Lambert, P. J. (2014). Redistributive effect and unequal income

tax treatment. The Economic Journal, 104(423), 262-270.

Bramall, R. (2017). Dreaming of what might be: tax utopias in the election. Soundings: A journal

of politics and culture, 66, 28-33.

Chapman, S. J. (2013). The utility of income and progressive taxation. The Economic

Journal, 23(89), 25-35.

Jalan, A., & Vaidyanathan, R. (2017). Tax havens: conduits for corporate tax

malfeasance. Journal of Financial Regulation and Compliance, 25(1), 86-104.

Jalan, A., & Vaidyanathan, R. (2017). Tax havens: conduits for corporate tax

malfeasance. Journal of Financial Regulation and Compliance, 25(1), 86-104.

Kirchler, E., & Hoelzl, E. (2018). 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, 255.

Lockwood, B. B., & Weinzierl, M. (2016). Positive and normative judgments implicit in US tax

policy, and the costs of unequal growth and recessions. Journal of Monetary

Economics, 77, 30-47.

Luja, R. (2018). § 6 EU State Aid Restrictions to Preferential Tax Treatment: Size-Neutral Tax

Incentives and Enforcement of General Anti Avoidance Rules. Heidelberger Beiträge

zum Finanz-und Steuerrecht, 7.

Nattrass, N., & Seekings, J. (2011). Democracy and distribution in highly unequal economies:

the case of South Africa. The journal of modern African studies, 39(3), 471-498.

Pántya, J., Kovács, J., Kogler, C., & Kirchler, E. (2016). Work performance and tax compliance

in flat and progressive tax systems. Journal of Economic Psychology, 56, 262-273.

Ron Balsera, M., Klees, S. J., & Archer, D. (2018). Financing education: why should tax justice

be part of the solution?. Compare: A Journal of Comparative and International

Education, 48(1), 147-162.

Sadka, E. (2016). On progressive income taxation. The American Economic Review, 66(5), 931-

935.

Saez, E., & Zucman, G. (2019). How Would a Progressive Wealth Tax Work? Evidence from

the Economics Literature. Unpublished paper. February, 5, 2019.

19 | P a g e

References

Aronson, J. R., Johnson, P., & Lambert, P. J. (2014). Redistributive effect and unequal income

tax treatment. The Economic Journal, 104(423), 262-270.

Bramall, R. (2017). Dreaming of what might be: tax utopias in the election. Soundings: A journal

of politics and culture, 66, 28-33.

Chapman, S. J. (2013). The utility of income and progressive taxation. The Economic

Journal, 23(89), 25-35.

Jalan, A., & Vaidyanathan, R. (2017). Tax havens: conduits for corporate tax

malfeasance. Journal of Financial Regulation and Compliance, 25(1), 86-104.

Jalan, A., & Vaidyanathan, R. (2017). Tax havens: conduits for corporate tax

malfeasance. Journal of Financial Regulation and Compliance, 25(1), 86-104.

Kirchler, E., & Hoelzl, E. (2018). 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, 255.

Lockwood, B. B., & Weinzierl, M. (2016). Positive and normative judgments implicit in US tax

policy, and the costs of unequal growth and recessions. Journal of Monetary

Economics, 77, 30-47.

Luja, R. (2018). § 6 EU State Aid Restrictions to Preferential Tax Treatment: Size-Neutral Tax

Incentives and Enforcement of General Anti Avoidance Rules. Heidelberger Beiträge

zum Finanz-und Steuerrecht, 7.

Nattrass, N., & Seekings, J. (2011). Democracy and distribution in highly unequal economies:

the case of South Africa. The journal of modern African studies, 39(3), 471-498.

Pántya, J., Kovács, J., Kogler, C., & Kirchler, E. (2016). Work performance and tax compliance

in flat and progressive tax systems. Journal of Economic Psychology, 56, 262-273.

Ron Balsera, M., Klees, S. J., & Archer, D. (2018). Financing education: why should tax justice

be part of the solution?. Compare: A Journal of Comparative and International

Education, 48(1), 147-162.

Sadka, E. (2016). On progressive income taxation. The American Economic Review, 66(5), 931-

935.

Saez, E., & Zucman, G. (2019). How Would a Progressive Wealth Tax Work? Evidence from

the Economics Literature. Unpublished paper. February, 5, 2019.

19 | P a g e

Taxation and provisions 20 | P a g e

Schneider, D. (2010). The effects of progressive and proportional income taxation on risk-

taking. National Tax Journal, 67-75.

Shome, P. (2018). Contours and conflicts in tax design: principles and international practice.

20 | P a g e

Schneider, D. (2010). The effects of progressive and proportional income taxation on risk-

taking. National Tax Journal, 67-75.

Shome, P. (2018). Contours and conflicts in tax design: principles and international practice.

20 | P a g e

1 out of 21

![[PDF] Principles of taxation](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fgv%2Fc9ce337d8a24433dbc693f94b5ce2e78.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.