Taxation: Income, Deductions, and Taxable Income Analysis

VerifiedAdded on 2022/10/17

|11

|1399

|287

Homework Assignment

AI Summary

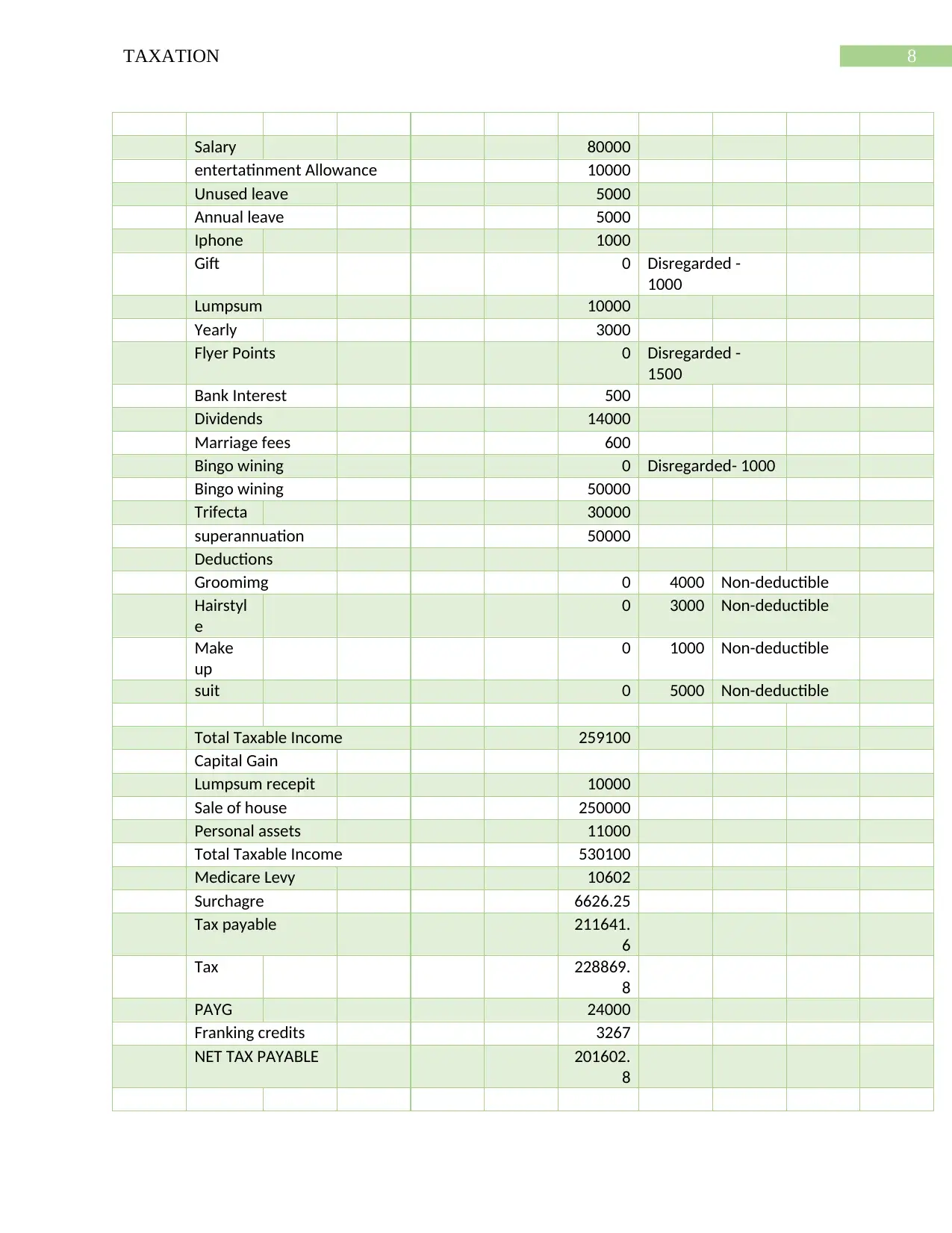

This taxation assignment analyzes various financial transactions to determine their tax implications. It covers earnings, further benefits, investment earnings, marriage celebrant fees, bingo winnings, settlement proceeds, superannuation payments, sale of residence, sale of personal items, work expenses, and car expenses. The analysis applies relevant sections of the Income Tax Assessment Act 1997 (ITAA 97) and other legal precedents to classify income as ordinary income, statutory income, or capital gains. It calculates taxable income, medicare levy, and tax payable, including PAYG and franking credits. The assignment assesses the impact of each transaction, distinguishing between assessable income, non-deductible expenses, and capital gains, providing a comprehensive overview of tax liabilities.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.